Global Market Comments

February 5, 2020

Fiat Lux

Featured Trade:

(A NOTE ON OPTIONS CALLED AWAY),

(MSFT), (TLT), (BA), (GOOGL), (SPY)

Global Market Comments

February 5, 2020

Fiat Lux

Featured Trade:

(A NOTE ON OPTIONS CALLED AWAY),

(MSFT), (TLT), (BA), (GOOGL), (SPY)

Mad Hedge Technology Letter

January 27, 2020

Fiat Lux

Featured Trade:

(HOW TO PLAY THE CHINESE PANDEMIC)

(TRIP), (TCOM), (GOOGL), (EXPE)

Am I going to rant about Peloton today?

No, I’ll save that for another day.

Let’s get straight to the chase – the epidemic from Wuhan is crushing tech stocks.

If you want a way to play the Chinese coronavirus outbreak, then look no further than Trip.com Group Limited (TCOM).

This company owns a series of reputable Chinese travel apps from Trip.com, Skyscanner, and Ctrip.com.

The Mad Hedge Technology Letter doesn’t tend to do tech alerts on Chinese companies listed in America as American depository receipts.

We rather not expose readers to the high risk of one of them suddenly being kicked off of one of the exchanges.

American investors have zero rights of recouping any losses if Alibaba or Baidu delists or even announces to switch its listing on the Shenzhen tech exchange.

Remember that founder of Alibaba Jack Ma signed over the PayPal of China Alipay to himself without even telling Yahoo about it.

Yahoo was also locked out of any profits from the decision as well even though they were seed investors in Alibaba.

That is China in a nutshell for you!

So what’s happening now? Tourists are staying home in droves and the ones that support the economy which are the Chinese ones during the peak travel season of Chinese New Year.

Cities are getting quarantined left and right in China and the mainland has ordered all travel agencies to suspend sales of domestic and international tours.

Chinese shares have felt the pain with shares of China Southern Airlines Co. – the carrier most exposed to the site of the outbreak – cratering 20% since the second death from the virus was confirmed.

If the situation unfolds like the SARS outbreak of 2003, things could turn bleak quickly.

Remember that in just one month of the SARS outbreak, Chinese air passenger traffic fell 71%, and Trip.com was rerated and has fell off the face of the earth.

I am predicting the same type of devastating numbers to the online travel world.

Trip.com has struggled to keep up with competition from digital rivals like Meituan Dianping and Alibaba, and even if the virus is conquered, business might never come back.

Despite the trade war and Hong Kong’s protests, the world has been held up by the Chinese tourist.

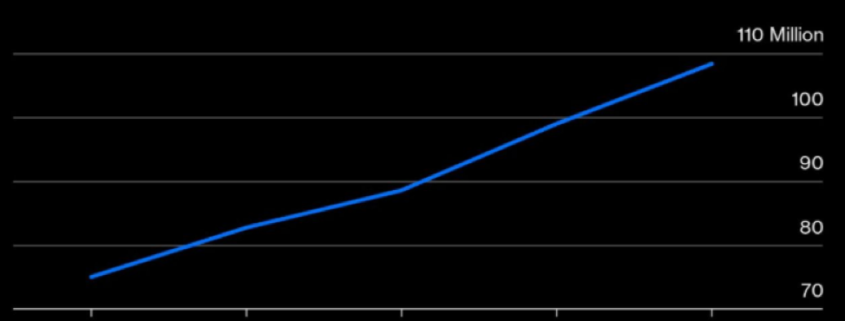

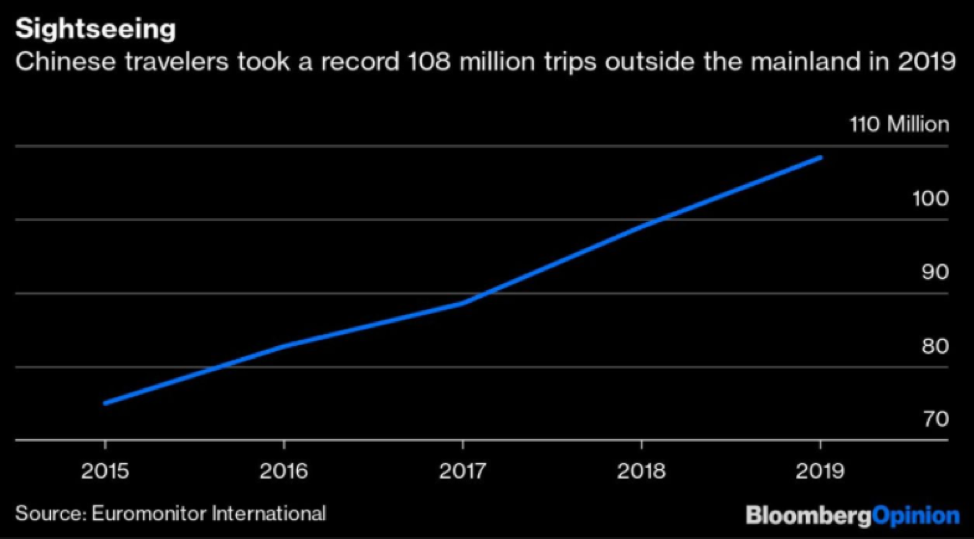

108.39 million Chinese overseas trips were taken last year, a 9.5% gain, after surging 11.7% in 2018.

Flight volume was brimming along nicely until the virus, but the hotel-booking sector is getting crowded.

Meituan Dianping has recently overtaken Trip.com as China’s top site, and now has 47% of China's market, 13% higher than Trip.com.

Now, Meituan is moving further onto Trip.com’s turf with luxury hotels, while chains like Marriott International Inc. are pushing for direct booking on their China websites.

Alibaba said part of the $13 billion it raised from its Hong Kong listing in November would go toward fliggy.com, its online travel group site.

The way the Mad Hedge Technology Letter is playing the sudden drop in overseas travel confidence is through the travel app I dislike the most – TripAdvisor (TRIP).

I actually don’t have a personal problem with the functionality, but the business behind it is terrible.

That was the main reason I strapped on a put spread and I can’t see TripAdvisor outperforming dramatically in the next few weeks in the face of a global pandemic.

This was a short-term trade that TripAdvisor won’t rise 11% in 30 day

I didn’t like this company before the coronavirus and now that Chinese tourists are home sitters for the Chinese New Year, this could put a dent into TripAdvisor’s new China initiative.

Trip.com Group had taken the lead in the day-to-day running of TripAdvisor China. It owns the majority share, with TripAdvisor claiming a 40 percent stake.

Chinese were supposed to increasingly travel the world while its customer base is also becoming more global, in particularly with Trip.com and Skyscanner.

But that is all on hold now.

Yes, it is possible that there could be a dead cat bounce in shares if the virus is tamed, but the 2-week travel season is something you can’t get back once it’s over for TripAdvisor.

I believe this will come out in the numbers along with details about Google’s algorithms further destroying TripAdvisor’s relevancy in the online travel industry.

Then take into account that the company just announced a 200-employee purge for the explicit reason of increased competition from Google and things seem to be going from bad to worse.

The company has done a proverbial deal with the devil by positioning itself to be utterly tied to Google’s search algorithm while Google is going head-to-head with them.

Google has upgraded its travel search tools recently to turn the screws on several trip booking websites like TripAdvisor, Booking.com and Priceline.

In its last earnings release, TripAdvisor noted that Google has placed ads at the top of its search results, forcing companies like it to buy more ads.

The company had a rough last quarter, reporting adjusted earnings of 58 cents a share, down from 72 cents a year earlier and short of analysts’ estimates of 69 cents.

Rhetoric from management was equally as disappointing with them saying, “Google (is) pushing its own hotel products in search results and siphoning off quality traffic that would otherwise find TripAdvisor via free links and generate high margin revenue in our hotel click-based auction.”

“Google has got more aggressive. We’re not predicting that it’s going to turn around.” TripAdvisor CEO Stephen Kaufer said at the time and I don’t see how our put spread will lose money in the short-term.

I will advise readers to take profits when the time comes. Be aware that TripAdvisor also has an earnings report coming up in 2 weeks that could gyrate the stock.

I expect broad-based weakness in guidance and poor performance last quarter in the report.

Mad Hedge Technology Letter

January 15, 2020

Fiat Lux

Featured Trade:

(THE TRADE ALERT DROUGHT EXPLAINED)

(GOOGL), (AMZN), (MSFT), (FB), (JPM)

Why has there been a dearth of Mad Hedge Tech trade alerts to start the year?

Let me explain.

Love it or hate it – earnings' season is about to kick off.

And now, this is the part where it starts to get ugly with consensus of a 2% year-over-year decline in fourth-quarter S&P 500 earnings.

Banks are expected to be a rare bright spot and JPMorgan (JPM) delivered us stable results as one of the first to report.

The unfortunate part of the equation is that a lot has to go right for tech shares to go unimpeded for the rest of the year.

What we have seen in the first 2 weeks of the year is a FOMO (fear-of-missing-out) environment in which valuations have lurched forward to 20 times forward earnings.

Tech is overwhelmingly carrying the load and I have banged on the drums about this thread advising readers to be acutely aware of a heavy positive bias towards the FANGs in 2020.

Well, that is already panning out in the first two weeks.

Examples are widespread with Facebook (FB) up over 8% and Apple (AAPL) already topping 6% to start the year.

It would be farfetched to believe that the tech sector can keep pilfering itself higher in the face of negative earnings growth.

However, behind the scenes, relations between China and America are improving, the threat of war with Iran is subsiding, and the Fed continues strong support tempering down risk to tech shares.

The situation we find ourselves in is that of an expensive tech sector that will again guide down on upcoming earnings’ reports telegraphing softness moving into the middle part of the year.

The ensuing post-earnings sell-off in specific software stocks will offer optimal short-term entry points.

The current risk-reward of chasing FANGs at these levels is unfavorable.

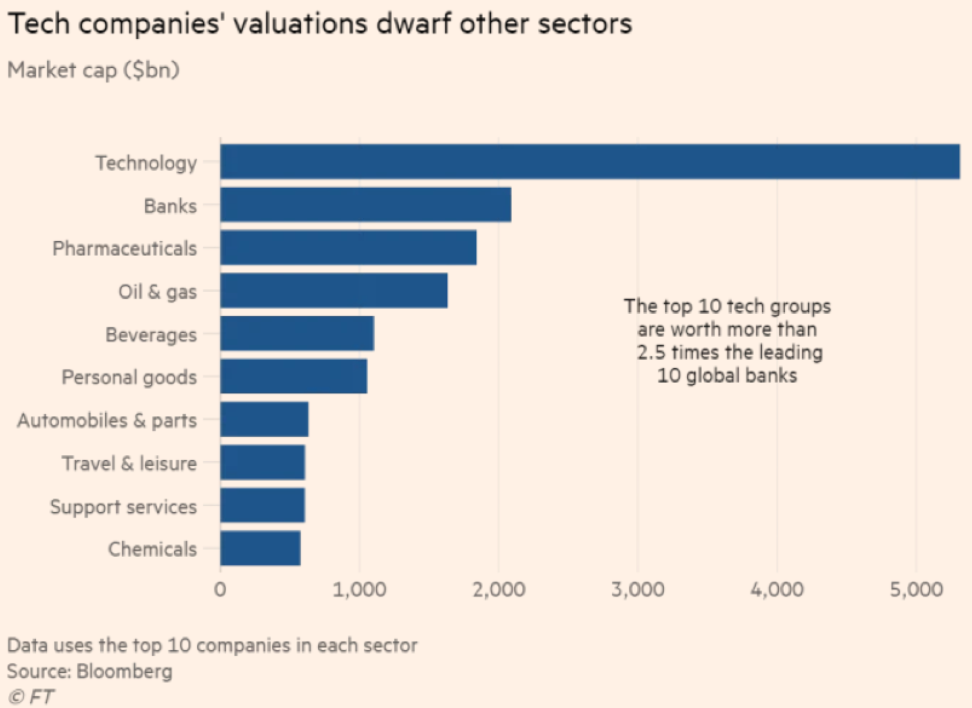

Another glaring example of the FANG outperformance is Alphabet who rose 26% last year.

They are on the brink of joining the $1 trillion club that Apple and Microsoft (MSFT) have joined.

Its market value currently sits idling at $985 billion and its surge towards the vaunted trillion-dollar mark is more of a case of when than if.

Alphabet (GOOGL), more or less, still expands at the same rate of low-20% annually that it did 10 years ago.

Sales have ballooned to $160 billion annually and they sit at the forefront of every cutting-edge sub-sector in technology from artificial intelligence, autonomous driving, and augmented reality.

The engine that drives Google is still its core advertising business and strategic premium acquisitions like YouTube and penetration into other fast-growing areas such as cloud computing.

It has rounded out into a broad-based revenue accumulator.

Apple was the first public company to surpass a $1 trillion market cap and ended the year up 86% in 2019, and it has only gone up since then currently checking in at a $1.36 trillion market cap.

Microsoft followed Apple, hitting the $1 trillion mark during the first half of 2019, and it is now worth $1.23 trillion.

Amazon fell back after surging past the $1 trillion mark but inevitably will achieve it on the next heave up.

Amazon shares have been quickly heating up since its capitulation from $2,000 in July 2019 and round out the group of overperforming tech behemoths.

Although the rush into big-cap tech stocks in the first two weeks has been a bullish signal, it still doesn’t marry up with the lack of earnings growth in the overall tech sector.

Companies beating meager expectations will experience strong share appreciation although not at the pace of last year and will still serve investors pockets of overperformance.

We will find our spots to trade shortly, but better to keep our gunpowder dry at the moment.

Mad Hedge Technology Letter

January 8, 2020

Fiat Lux

Featured Trade:

(THE TOP IS NOT IN FOR TECH STOCKS))

(AAPL), (FB), (GOOGL)

Tech shares are pricey, but that doesn’t mean they can’t get more expensive.

Strength often begets strength.

Let’s take for instance Apple (AAPL) – it delivered investors 86% in 2019 and that was their best performance in the past 10 years.

This was on the heels of a tumultuous 2018 where Apple sank 6%.

Many of the best of brightest of the tech industry beat the S&P last year, which itself gained 29%.

And as Apple leapfrogged into the software as a service business, they find themselves shunning China hardware revenue that got themselves into the 2018 mess.

Apple is betting that the confines of stateside consumer culture will offer greener pastures.

Overall, the market is pricing in a lukewarm 2020 for tech earnings boding well for the elite tech stocks that celebrated touchdown after touchdown in 2019.

Surpassing low expectations could be another rewind back to Q4 2019 which was a time that offered tech shares a platform to surge to all-time highs.

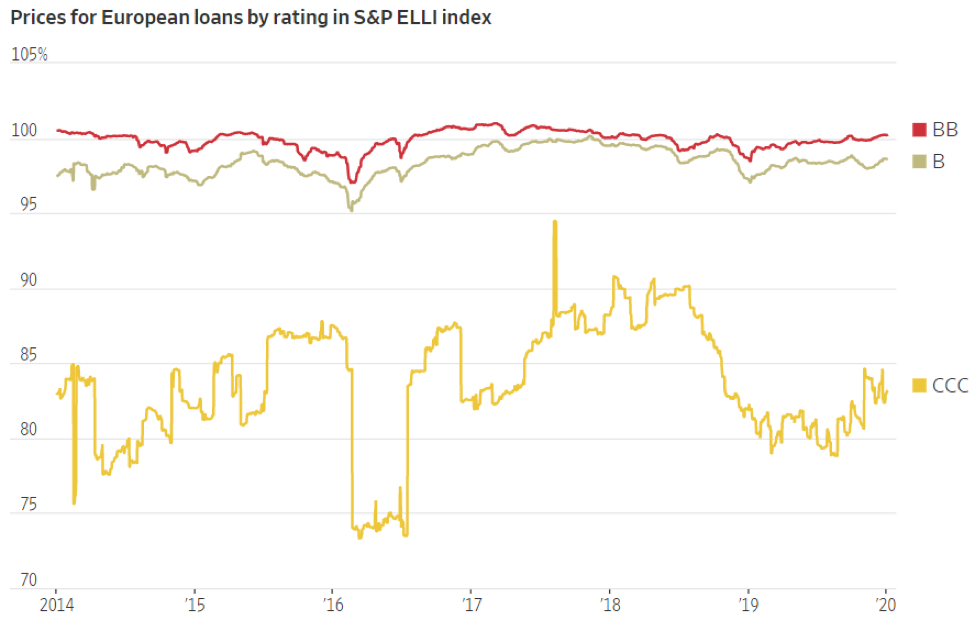

The worrying development for 2020 is that poorer-rated tech corporations won’t have the same access to cheap debt as they did in 2018 or even 2019.

The chapter of loose credit is about to close stymying loss-making tech companies who thought they could use subsidies to achieve success.

The prices of CCC-rated European bonds have declined immensely in the past year showing investors' lack of appetite for the riskier part of the corporate debt market.

Venture capitalists aren’t going to foot the bill for the next big thing in Silicon Valley at this point in the economic cycle unless the unit economics are too good to be true.

The story of 2020 will be the intensification between the haves and have nots in tech.

This is the case of the market putting a premium on time-honored tech brands and bulletproof balance sheets that they have cultivated.

On a broader level, the Fed who has presided over a $600 billion expansion in their balance sheet in the last four months offers yet another tailwind to tech shares in the short-term.

The Fed’s decision in the last few months to re-start large-scale asset purchases will help keep a foot under tech shares in early 2020 and responds like a de facto QE.

If you thought 2019 was a bad year for Uber and Lyft, then wait until this year plays itself out.

The gig economy stocks are in the direct firing line with nowhere to run and other non-sensical profit models will find it costly to search for debt alternatives in which to service their visions.

If the tech sector does become a war of attrition between the FANGs staving off one another by acquiring inorganic growth, then marginal tech players will get squeezed because they don’t have the capital bazookas to compete with the likes of Facebook (FB) and Google (GOOGL).

This is the year that we could see a slew of fringe tech companies go bust as debt markets sour on false narratives of future profits and equity markets turn against them.

The feast versus famine theme is also aligned with 5G, with many of the same cast of characters such as Apple, Alphabet posed to usurp revenue when this new technology finally becomes pervasive in consumer culture.

The Apple refresh cycle will dust off its playbook for another blockbuster rollout later this year when Apple debuts its much-awaited 5G phone.

Much of the share appreciate in Apple of late can be attributed to the anticipation of the new iPhone and the fresh infusion of revenue that branches off from it.

The applications that result from the new 5G Apple phone is seen as a luscious force multiplier to many 3rd party companies as well.

Chip stocks will be counted on as the ones lifting the tech foundations and just looking at shares in China, demonstrations of frothiness are running wild throughout their markets.

The Chinese government, to counteract the trade war, has been on a mission to flood its tech sector with unlimited capital as a catchup mechanism to overcome its inferior domestic chip industry.

Will Semiconductor, a supplier of integrated circuit products for telecommunications and electronics for cars, delivered a 390% performance in 2019 ranking it as the best performer in the Chinese stock market.

Luxshare Precision Industry and GoerTek, suppliers of consumer electronics products supplying Apple, and GigaDevice Semiconductor, producing flash chips, weren’t too shabby either each eclipsing at least 193% last year.

Even though 5G construction isn’t fully operational, I can attest that revenue creation for the companies involved are in full swing.

Investors must narrow their pickings to the biggest and financially resilient; this is not the time to expose oneself to the ugly trepidations of the mood-sensitive tech market.

For investors who can balance the delicate relationship of risk and surgical maneuvering, this year will end positive.

Mad Hedge Technology Letter

December 30, 2019

Fiat Lux

Featured Trade:

(TECH TALENT PUTS THEIR FOOT DOWN ),

(EA), (ADBE), (TSLA), (GOOGL), (TWTR)

Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(WHY YOU CANNOT NEGLECT THE CLOUD)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

Mad Hedge Technology Letter

December 20, 2019

Fiat Lux

Featured Trade:

(THE BIG TECH TRENDS OF 2020)

(AAPL), (GOOGL), (FB), (AMZN), (NFLX)