Global Market Comments

May 6, 2025

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

Global Market Comments

May 6, 2025

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

If demographics are destiny, then America’s future looks bleak. You see, they’re just not making Americans anymore.

At least that is the sobering conclusion of the latest Economist magazine survey of the global demographic picture.

I have long been a fan of demographic investing, which creates opportunities for traders to execute on what I call “intergenerational arbitrage”. When the number of middle-aged big spenders is falling, risk markets plunge.

Front run this data by two decades, and you have a great predictor of stock market tops and bottoms that outperforms most investment industry strategists.

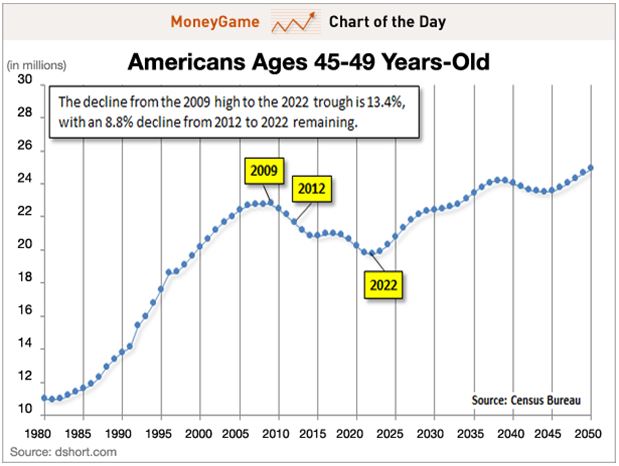

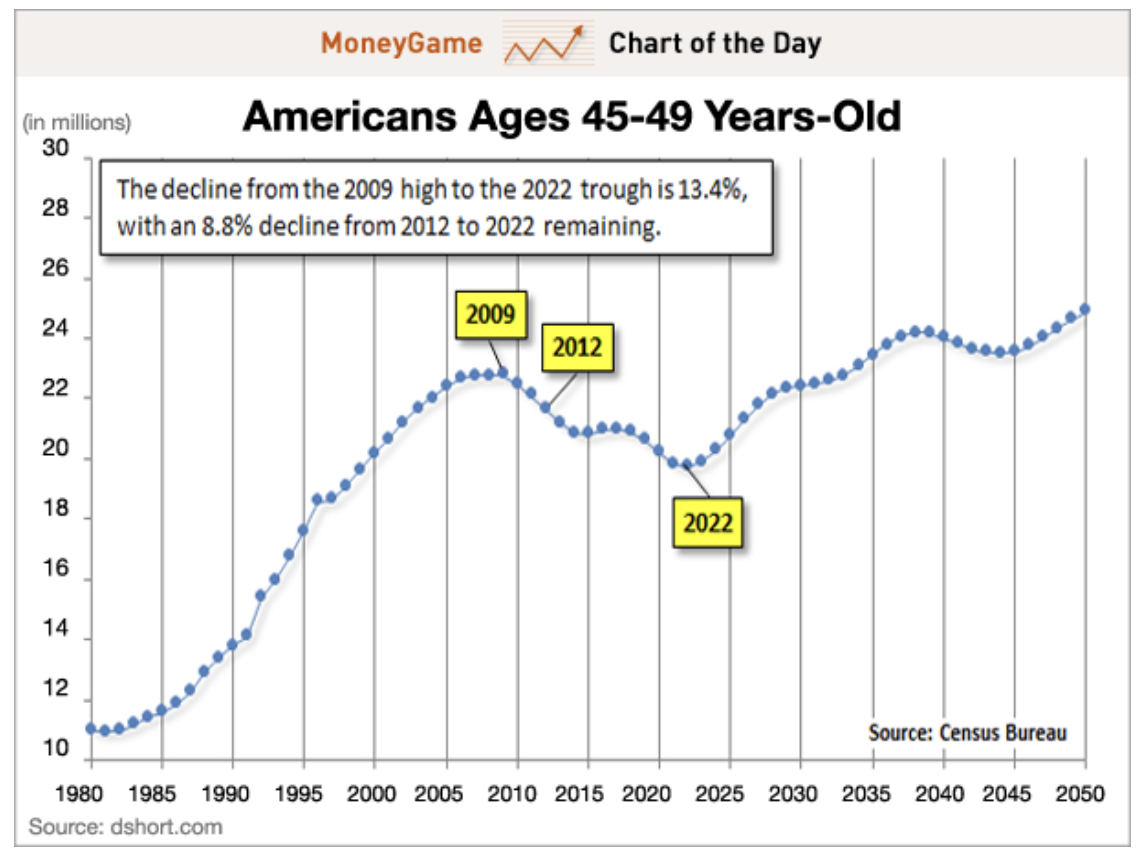

You can distill this even further by calculating the percentage of the population that is in the 45-49 age bracket.

The reasons for this are quite simple. The last five years of child rearing are the most expensive. Think of all that pricey sports equipment, tutoring, braces, SAT coaching, first cars, first car wrecks, and the higher insurance rates that go with it.

Older kids need more running room, which demands larger houses with more amenities. No wonder it seems that dad is writing a check or whipping out a credit card every five seconds. I know, because I have five kids of my own. As long as dad is in spending mode, stock and real estate prices rise handsomely, as do most other asset classes. Dad, you’re basically one generous ATM.

As soon as kids flee the nest, this spending grinds to a juddering halt. Adults entering their fifties cut back spending dramatically and become prolific savers. Empty nesters also start downsizing their housing requirements, unwilling to pay for those empty bedrooms, which in effect, become expensive storage facilities.

This is highly deflationary and causes a substantial slowdown in GDP growth. That is why the stock and real estate markets began their slide in 2007, while it was off to the races for the Treasury bond market.

The data for the US is not looking so hot right now. Americans aged 45-49 peaked in 2009 at 23% of the population. According to US census data, this group then began a 13-year decline to only 19% by 2022.

You can take this strategy and apply it globally with terrific results. Not only do these spending patterns apply globally, but they also backtest with a high degree of accuracy. Simply determine when the 45-49 age bracket is peaking for every country, and you can develop a highly reliable timetable for when and where to invest.

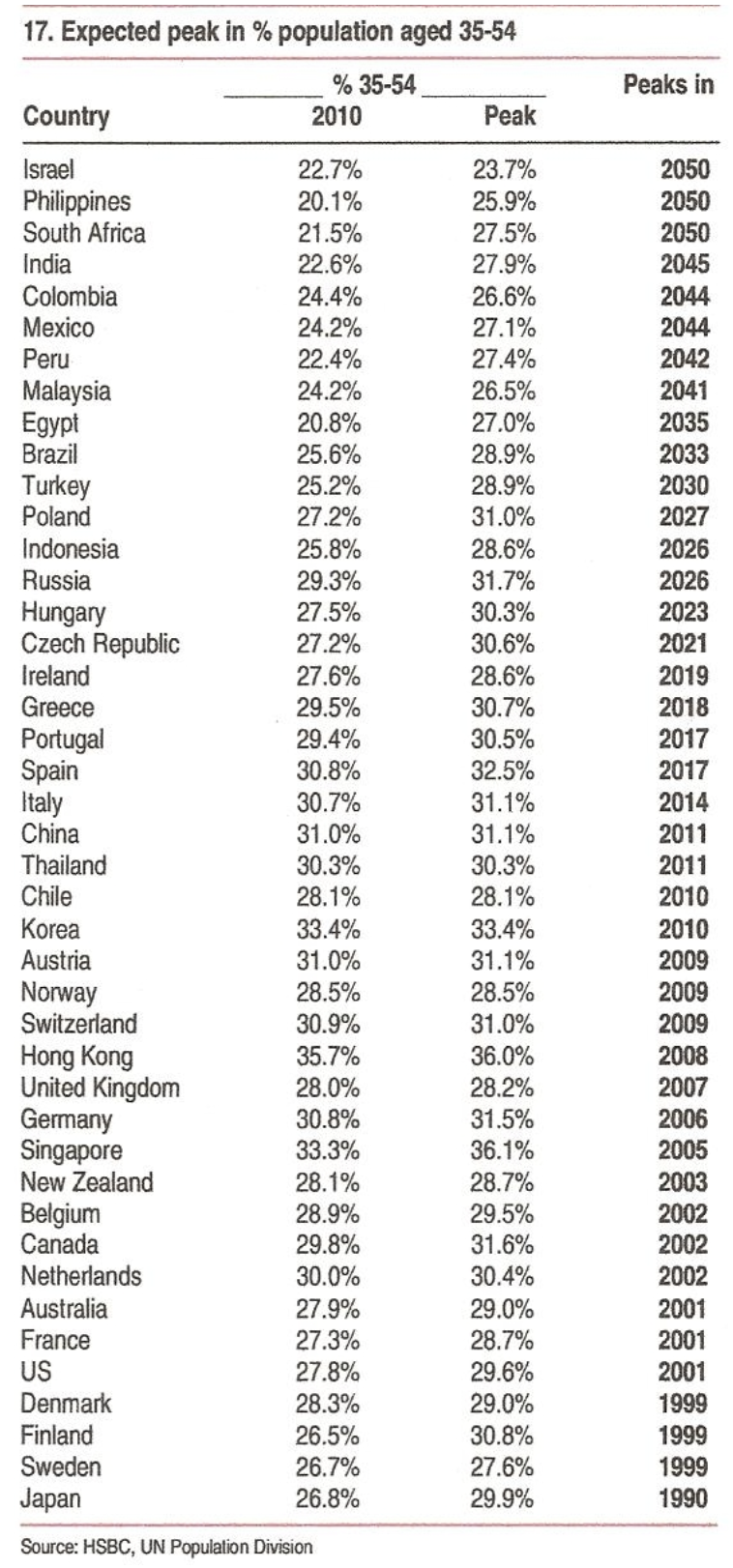

Instead of poring through gigabytes of government census data to cherry-pick investment opportunities, my friends at HSBC Global Research, strategists Daniel Grosvenor and Gary Evans, have already done the work for you. They have developed a table ranking investable countries based on when the 34-54 age group peaks—a far larger set of parameters that captures generational changes.

The numbers explain a lot of what is going on in the world today. I have reproduced it below. From it, I have drawn the following conclusions:

* The US (SPY) peaked in 2001 when our first “lost decade” began.

*Japan (EWJ) peaked in 1990, heralding 32 years of falling asset prices, giving you a nice back test.

*Much of developed Europe, including Switzerland (EWL), the UK (EWU), and Germany (EWG), followed in the late 2,000’s, and the current sovereign debt debacle started shortly thereafter.

*South Korea (EWY), an important G-20 “emerged” market with the world’s lowest birth rate, peaked in 2010.

*China (FXI) topped in 2011, explaining why we have seen three years of dreadful stock market performance despite torrid economic growth. It has been our consumers driving their GDP, not theirs.

*The “PIIGS” countries of Portugal, Ireland (EIRL), Greece (GREK), and Spain (EWP) don’t peak until the end of this decade. That means you could see some ballistic stock market performances if the debt debacle is dealt with in the near future.

*The outlook for other emerging markets, like Indonesia (IDX), Poland (EPOL), Turkey (TUR), Brazil (EWZ), and India (PIN) is quite good, with spending by the middle-aged not peaking for 15-33 years.

*Which country will have the biggest demographic push for the next 38 years? Israel (EIS), which will not see consumer spending max out until 2050. Better start stocking up on things Israelis buy.

Like all models, this one is not perfect, as its predictions can get derailed by a number of extraneous factors. Rapidly lengthening life spans could redefine “middle age”. Personally, I’m hoping 72 is the new 42.

Emigration could starve some countries of young workers (like Japan), while adding them to others (like Australia). Foreign capital flows in a globalized world can accelerate or slow down demographic trends. The new “RISK ON/RISK OFF” cycle can also have a clouding effect.

So why am I so bullish now? Because demographics is just one tool in the cabinet. Dozens of other economic, social, and political factors drive the financial markets.

What is the most important demographic conclusion right now? That the US demographic headwind veered to a tailwind in 2022, setting the stage for the return of the “Roaring Twenties.” With the (SPY) up 27% since October, it appears the markets heartily agree.

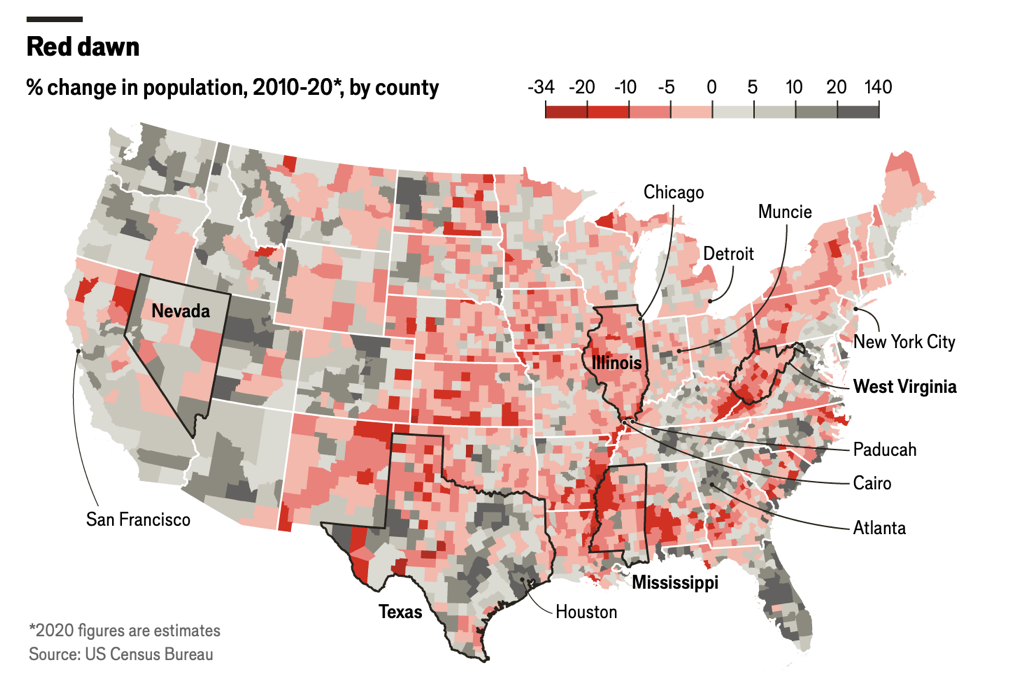

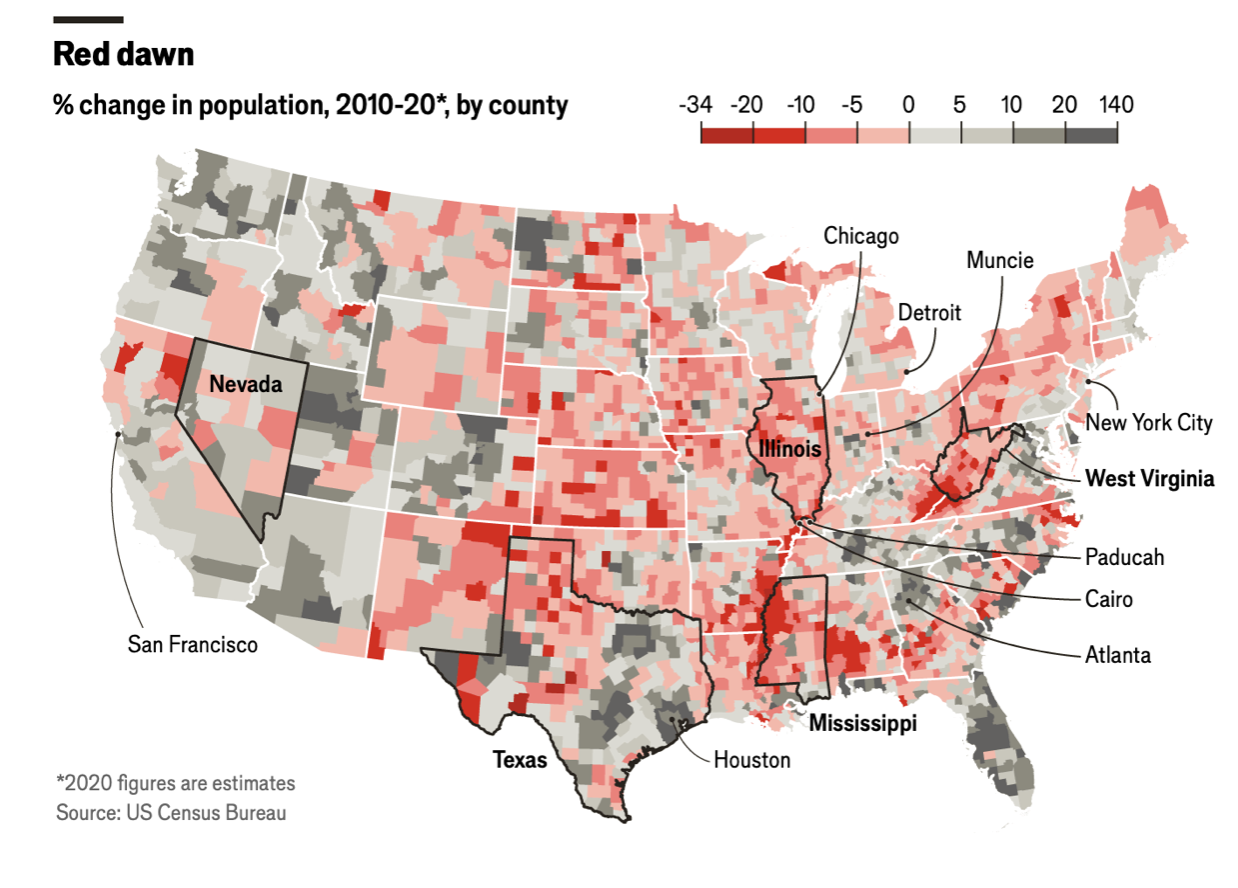

While the growth rate of the American population is dramatically shrinking, the rate of migration is accelerating, with huge economic consequences. The 80-year-old trend of population moving from North to South to save on energy bills is picking up speed, and the Midwest is getting hollowed out at an astounding rate as its people flee to the coasts, all three of them.

As a result, California, Texas, Florida, Washington, and Oregon are gaining population, while Missouri, Iowa, Nebraska, Kansas, and Wyoming are losing it (see map below). During my lifetime, the population of California has rocketed from 10 million to 40 million. People come in poor and leave as billionaires, as Elon Musk did.

In the meantime, I’m going to be checking out the shares of the matzo manufacturer down the street.

Global Market Comments

April 24, 2024

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

If demographics is destiny, then America’s future looks bleak. You see, they’re not making Americans anymore.

At least that is the sobering conclusion of the latest Economist magazine survey of the global demographic picture.

I have long been a fan of demographic investing, which creates opportunities for traders to execute on what I call “intergenerational arbitrage”. When the numbers of the middle-aged big spenders are falling, risk markets plunge. Front run this data by two decades, and you have a great predictor of stock market tops and bottoms that outperforms most investment industry strategists.

You can distill this even further by calculating the percentage of the population that is in the 45-49 age bracket.

The reasons for this are quite simple. The last five years of child rearing are the most expensive. Think of all that pricey sports equipment, tutoring, braces, SAT coaching, first cars, first car wrecks, and the higher insurance rates that go with it.

Older kids need more running room, which demands larger houses with more amenities. No wonder it seems that dad is writing a check or whipping out a credit card every five seconds. I know, because I have five kids of my own. As long as dad is in spending mode, stock and real estate prices rise handsomely, as do most other asset classes. Dad, you’re basically one generous ATM.

As soon as kids flee the nest, this spending grinds to a juddering halt. Adults entering their fifties cut back spending dramatically and become prolific savers. Empty nesters also start downsizing their housing requirements, unwilling to pay for those empty bedrooms, which in effect, become expensive storage facilities.

This is highly deflationary and causes a substantial slowdown in GDP growth. That is why the stock and real estate markets began their slide in 2007, while it was off to the races for the Treasury bond market.

The data for the US is not looking so hot right now. Americans aged 45-49 peaked in 2009 at 23% of the population. According to US census data, this group then began a 13-year decline to only 19% by 2022.

You can take this strategy and apply it globally with terrific results. Not only do these spending patterns apply globally, they also back-test with a high degree of accuracy. Simply determine when the 45-49 age bracket is peaking for every country and you can develop a highly reliable timetable for when and where to invest.

Instead of pouring through gigabytes of government census data to cherry-pick investment opportunities, my friends at HSBC Global Research, strategists Daniel Grosvenor and Gary Evans, have already done the work for you. They have developed a table ranking investable countries based on when the 34-54 age group peaks—a far larger set of parameters that captures generational changes.

The numbers explain a lot of what is going on in the world today. I have reproduced it below. From it, I have drawn the following conclusions:

* The US (SPY) peaked in 2001 when our first “lost decade” began.

*Japan (EWJ) peaked in 1990, heralding 32 years of falling asset prices, giving you a nice backtest.

*Much of developed Europe, including Switzerland (EWL), the UK (EWU), and Germany (EWG), followed in the late 2000s and the current sovereign debt debacle started shortly thereafter.

*South Korea (EWY), an important G-20 “emerged” market with the world’s lowest birth rate peaked in 2010.

*China (FXI) topped in 2011, explaining why we have seen three years of dreadful stock market performance despite torrid economic growth. It has been our consumers driving their GDP, not theirs.

*The “PIIGS” countries of Portugal, Ireland (EIRL), Greece (GREK), and Spain (EWP) don’t peak until the end of this decade. That means you could see some ballistic stock market performances if the debt debacle is dealt with in the near future.

*The outlook for other emerging markets, like Indonesia (IDX), Poland (EPOL), Turkey (TUR), Brazil (EWZ), and India (PIN) is quite good, with spending by the middle age not peaking for 15-33 years.

*Which country will have the biggest demographic push for the next 38 years? Israel (EIS), which will not see consumer spending max out until 2050. Better start stocking up on things Israelis buy.

Like all models, this one is not perfect, as its predictions can get derailed by a number of extraneous factors. Rapidly lengthening life spans could redefine “middle age”. Personally, I’m hoping 72 is the new 42.

Emigration could starve some countries of young workers (like Japan) while adding them to others (like Australia). Foreign capital flows in a globalized world can accelerate or slow down demographic trends. The new “RISK ON/RISK OFF” cycle can also have a clouding effect.

So why am I so bullish now? Because demographics is just one tool in the cabinet. Dozens of other economic, social, and political factors drive the financial markets.

What is the most important demographic conclusion right now? That the US demographic headwind veered to a tailwind in 2022, setting the stage for the return of the “Roaring Twenties.” With the (SPY) up 27% since October, it appears the markets heartily agree.

While the growth rate of the American population is dramatically shrinking, the rate of migration is accelerating, with huge economic consequences. The 80-year-old trend of population moving from North to South to save on energy bills picking up speed, the Midwest is getting hollowed out at an astounding rate as its people flee to the coasts, all three of them.

As a result, California, Texas, Florida, Washington, and Oregon are gaining population, while Missouri, Iowa, Nebraska, Kansas, and Wyoming are losing it (see map below). During my lifetime, the population of California has rocketed from 10 million to 40 million. People come in poor and leave as billionaires, as Elon Musk did.

In the meantime, I’m going to be checking out the shares of the matzo manufacturer down the street.

I have been to Greece many times over the past 45 years, and I?ll tell you that I just love the place. The beaches are perfect, the Ouzo wine enticing, and I?ll never say ?No? to a good moussaka.

However, I don?t let Greece dictate my investment strategy.

Greece, in fact, accounts for less than 2% of Europe?s GDP. It is not a storm in a teacup that is going on there, but a storm in a thimble. Greece is really just a full employment contract for financial journalists, who like to throw around big words like bankruptcy, default and contagion.

I have other things to worry about.

In fact, I am starting to come around to the belief that Europe is looking pretty good right here. Cisco (CSCO) CEO, John Chambers, announced that he was seeing the early signs of a turnaround.

Fiat CEO, Sergio Marchionne, the brilliant personal savior of Chrysler during the crash, thinks the beleaguered continent is about to recover from ?hell? to only ?purgatory.?

Only a devout Catholic could come up with such a characterization. But I love Sergio nevertheless because he generously helps me with my Italian pronunciation when we speak (aspirapolvere for vacuum cleaner, really?).

What are the two best performing stock markets since the big ?RISK ON? move started last Thursday? Greece (GREK) (+5%) and Russia (RSX) (+7.5%)!

And here is where I come in with my own 30,000 foot view.

The undisputed lesson of the past five years is that you always want to own stock markets that are about to receive an overdose of quantitative easing.

Since the US Federal Reserve launched their aggressive monetary policy, the S&P 500 (SPY) nearly tripled off the bottom.? Look how well US markets have performed since American QE ended 18 months ago.

Europe has only just barely started QE, and it could run for five more years. Corporations across the pond are about to be force-fed mountains of cash at negative interest rates, much like a goose being fattened for a fine dish of foie gras (only decriminalized in California last year).

Mind you, it could be another year before we get another dose of Euro QE, which is why I just bought the Euro (FXE) for a short-term trade.

A cheaper currency automatically reduces the prices of continental exports, making them more competitive in the international markets, and boosting their economies. Needless to say, this is all great new for stock markets.

Get Europe off the mat, and you can also add 10% to US share prices as well, as the global economy revives. The Euro drag dies and goes to heaven.

Buy the Wisdom Tree International Hedged Equity Fund ETF (HEDJ) down here on dips, which is long a basket of European stocks and short the Euro (FXE). This could be the big performer this year.

Praise the Lord and pass the foie gras!

I have been relying on David Hale as my de facto global macro economist for decades and I never miss an opportunity to get his updated views. The challenge is in writing down David?s eye popping, out of consensus ideas fast enough, because he spits them out in such a rapid-fire succession.

Since David is an independent economic advisor to many of the world?s governments, largest banks and investment firms, I thought his views would be of riveting interest to you.

I met him this time at the posh Ozumo restaurant on San Francisco?s waterfront, near the Ferry Building. A favorite of Silicon Valley?s tech titans, I bumped into Marc Andreessen on the way in, nearly impaling myself on his pointed head.

I settled for a delicate vegetable tempura and eel sushi, while David, being from the Midwest, dug into an excellent Wagyu beefsteak. We washed it all down with liberal doses of Kirin beer and Takagi Shuzo designer sake.

David is an unmitigated bull on the economy, predicting that growth will leap from 2.0% in 2013 to 3% in 2014. Fading away of the fiscal drag created by a gridlocked congress will be the main reason.

Last year, we were hobbled by the maximum Federal income tax rising from 35% to 39.5% for income over $400,000. Capital gains rose from 15% to 20% as well. These combined to subtract 1% off US GDP growth in 2013. There are no such tax hikes planned for 2014.

The economy continues to power along, supported by three legs: housing, the energy boom and a reviving auto industry. Detroit is expected to pump out over 17 million vehicles this year, a figure only dreamed about six years ago, when it hit a rock bottom 9 million unit annual rate.

Management has a death grip on controlling costs, which is why they aren?t hiring, and explains the feeble employment statistics. This has enabled profit margins to surge to all time highs. Expect more of the same.

Europe should grow by 1% in 2014 after delivering a near zero rate this year. It will take years for them to return to any kind of normalized growth rate. That said, continental stock markets could well outperform those in the US in the near term.

David spends much of his time traveling, doing a major intercontinental trip almost every month. The coming calendar includes Japan, Australia, and Europe by yearend. To have his frequent flier points!

Two years ago, David was banging his drum about an imminent recovery in Japan (EWJ) and a collapse in the yen (FXY), (YCS). He was ignored by virtually all, except by me. As you may recall, I started laying on major short positions in the yen about then at David?s behest, which proved wildly successful.

The proof is in the constant testimonials that I regularly publish in my letter. I don?t make these up and they come in almost every day.

David believes that Prime Minister Shinzo Abe is doing all the right things, so the recovery is real, sustainable and will play out over several more years. However, he would have been wise to spread out the VAT tax rise that took place in April, from 5% to 8%, over five years instead of bunching it all up in one.

He also should spend less time focusing on domestic nationalistic issues, which have the undesirable effect in that it focuses China on Japan?s regrettable past, not its bright future.

He is also quite an authority on emerging markets (EEM), which account for 40% of global GDP, and sees the recent collapse as presenting a once in a generation buying opportunity.

His favorite is Mexico (EWW), which will benefit hugely from the first new round of political and economic reforms in 20 years. The new oil and gas fracking technology has also arrived just in the nick of time, as its existing conventional fields are approaching exhaustion.

David thinks Greece (GREK) has more to run, although not at the heady pace of the past year. Nigeria (NGE) is another outstanding opportunity, where he recently visited. A privatization wave there could boost GDP growth from 7% to 10%.

To show you how wide David casts his net, he had lunch with none other than Syria?s Bashar al-Assad a decade ago. The country was then enacting a series of ground-breaking liberalizations by privatizing banks, and was viewed as the hot frontier market of the day. How things change!

This is why investors expect outsized returns from these countries. Less, and the risk is not worth it. They?re called ?frontier? for a reason.

David has in the past made some far out predictions that were real zingers. Population growth is grinding to a halt throughout Asia. It is already well below the replacement rate in Japan and South Korea, which will soon be joined by China.

This will eventually lead to labor shortages in Asia, and bring to an end the cheap labor regime, which has driven their economies for the past 100 years. The Chinese work force will shrink from five times ours to only three times.

Their cost advantage then goes out the window. The upshot for us is that perhaps half of the 6 million jobs that America lost to China over the last 20 years will come back. Many items can now be bought cheaper in Chicago than they can in Shanghai.

This explains why ?onshoring? is accelerating with a turbocharger (click here for ?The American Onshoring Trend is Accelerating?).

China will still become far and away the world?s largest economy in our lifetimes. In 1700, Asia accounted for 58% of world GDP. Some 250 years of wars pulled that figure down to 15% by 1950. It is on track to recover to 50% by 2050.

To learn more about David Hale and the extensive list of services he offers; please visit the website of David Hale Global Economics at http://www.davidhaleweb.com.

I have been relying on David Hale as my de facto global macro economist for decades, and I never miss an opportunity to get his updated views. The challenge is in writing down David?s eye popping, out of consensus ideas fast enough, because he spits them out in such rapid-fire succession.

Since David is an independent economic advisor to many of the world?s governments, largest banks, and investment firms, I thought his views would be of riveting interest to you.

I met him this time at the posh Ozumo restaurant on San Francisco?s waterfront, near the Ferry Building. A favorite of Silicon Valley?s tech titans, I bumped into Marc Andreessen on the way in, nearly impaling myself on his pointed head. I settled for a delicate vegetable tempura and eel sushi, while David, being from the Midwest, dug into an excellent Wagyu beefsteak. We washed it all down with liberal doses of Kirin beer and Takagi Shuzo designer sake.

David is an unmitigated bull on the economy, predicting that growth will leap from this year?s 2.5% to 3% next year. Fading away of the fiscal drag created by a gridlocked congress will be the main reason. This year, we were hobbled by the maximum Federal income tax rising from 35% to 39.5% for income over $400,000. Capital gains rose from 15% to 20% as well. These combined to subtract 1% off US GDP growth in 2013. There are no such tax hikes planned for 2014.

The economy continues to power along, supported by three legs: housing, the energy boom, and a reviving auto industry. Detroit is expected to pump out over 16 million vehicles this year, a figure only dreamed about five years ago when it hit a rock bottom 9 million unit annual rate.

The real surprise this year was how hot the second quarter came in, with corporate profits soaring by 17% YOY. Q3 should fall back to a more sustainable 5% rate. Managements have a death grip on controlling costs, which is why they aren?t hiring, and explains the feeble employment statistics. This has enabled profit margins to surge to all time highs. Expect more of the same.

Europe should grow by 1% in 2014 after delivering a near zero rate this year. It will take years for them to return to any kind of normalized growth rate. That said, continental stock markets could well outperform those in the US in the near term.

David spends much of his time traveling, doing a major intercontinental trip almost every month. The coming calendar includes Japan, Australia, and Europe by yearend. To have his frequent flier points!

A year ago, David was banging his drum about an imminent recovery in Japan (EWJ) and a collapse in the yen (FXY), (YCS). He was ignored by virtually all, except by me. As you may recall, I started laying on major short positions in the yen last November at David?s behest, which proved wildly successful. The proof is in the constant testimonials that I regularly publish in my letter. I don?t make these up.

David believes that Prime Minister Shinzo Abe is doing all the right things, so the recovery is real, sustainable, and will play out over several more years. However, he would be wise to spread out the coming VAT tax rise planned for April, from 5% to 8%, over five years instead of bunching it all up in one. He also should spend less time focusing on domestic nationalistic issues, which have the undesirable effect in that it focuses China on Japan?s regrettable past, not its bright future.

He is also quite an authority on emerging markets (EEM), which account for 40% of global GDP, and sees the recent collapse as presenting a once in a generation buying opportunity. His favorite is Mexico (EWW), which will benefit hugely from the first new round of political and economic reforms in 20 years. The new oil and gas fracking technology has also arrived just in the nick of time, as its existing conventional fields are approaching exhaustion.

David thinks Greece (GREK) has more to run, although not at the heady pace of the past year. Nigeria (NGE) is another outstanding opportunity, where he recently visited. A privatization wave there could boost GDP growth from 7% to 10%.

To show you how wide David casts his net, he had lunch with none other than Syria?s Bashar al-Assad a decade ago. The country was then enacting a series of ground-breaking liberalizations by privatizing banks, and was viewed as the hot frontier market of the day. How things change! This is why investors expect outsized returns from these countries. Less, and the risk is not worth it. They?re called ?frontier? for a reason.

What could bring the cheering bull parade to a grinding halt? The debt ceiling crisis, which could start generating headlines in a few weeks. If the government really does shut down in mid October, as Treasury Secretary, Jack Lew, told me a few weeks ago (click here for ?Riding With the Treasury Secretary Jack Lew?) no one will care if it reopens the next day, or the next week. Longer than that and it could be a real problem not just for the US, but for the global economy as well. A similar shut down during the 1990?s lasted only a day, but cost the Republicans dearly in the next election.

David has in the past made some far out predictions that were real zingers. Population growth is grinding to a halt throughout Asia. It is already well below the replacement rate in Japan and South Korea, which will soon be joined by China. This will eventually lead to labor shortages in Asia, and bring to an end the cheap labor regime, which has driven their economies for the past 100 years. The Chinese work force will shrink from five times ours to only three times.

Their cost advantage then goes out the window. The upshot for us is that perhaps half of the 6 million jobs that America lost to China over the last 20 years will come back. Many items can now be bought cheaper in Chicago than they can in Shanghai. This explains why ?onshoring? is accelerating with a turbocharger (click here for ?The American Onshoring Trend is Accelerating?).

China will still become far and away the world?s largest economy in our lifetimes. In 1700, Asia accounted for 58% of world GDP. Some 250 years of wars pulled that figure down to 15% by 1950. It is on track to recover to 50% by 2050.

To learn more about David Hale and the extensive list of services he offers, please visit the website of David Hale Global Economics at http://www.davidhaleweb.com.

It looks like the (FXE) gave us the double top at $133 which I predicted in my August 28 webinar, which very conveniently, was the lower strike of my Currency Shares Euro Trust (FXE) September, 2013 $133-$135 bear put spread. We have since backed off $3, and lower levels beckon.

I originally wrote this Trade Alert on July 18 while on the express train from Berlin to Frankfurt. I had to wait until we stopped at a station before I could send it on my iPhone. My friends in the German government had just painted a picture of the European economy which approximated Hieronymus Bosch?s vision of hell. My later discussions with European central bankers and CEO?s confirmed the worse.

Since then the Euro has appreciated against the dollar almost everyday, slowly draining profits from my model-trading portfolio. Lugging this position in the baggage of my summer vacation was no fun. That abruptly ended last week when traders returning from vacation, well rested and feeling their oats, decided collectively to take another run at the beleaguered European currency.

As of this morning, the market priced our spread at $1.92, just eight cents short of its maximum potential profit. That leaves 77% of the profit for us. So I am going to take the money and run. This reduces our risk for the month of September, when we are threatened by Syria and the regional contagion that will follow, the debt ceiling crisis, the taper, the identity of Ben Bernanke?s replacement, and a giant asteroid destroying the earth.

Since I sold short the Euro, almost every continental economic data point has been positive. Just this morning, we learned that the August Eurozone PMI Index rose from 50.5 to 51.5, a two year high. The UK August Business Activities Index leapt from 60.2 to 60.5, a six and a half year peak, no doubt in part due to the wad of money I dropped there a few weeks ago. The trend is your friend here, and like a giant supertanker slowly turning, the information flow is gradually turning from red to green.

If anything, I am now inclined to start examining European equity markets, which may bounce back stronger than those in the US. On the short list will be Germany (EWG), which is already in a solid uptrend, and Italy (EWI) for a turnaround play. Greece (GREK) has already made its move, nearly tripling off the bottom.

On to the next trade.

The victory of the centrist pro bailout New Democracy Party in the Sunday Greek elections sparked a furious rally in the overnight Asian markets, much of it driven by hedge fund short covering. The socialist, anti-bailout parties went down in flames. As I write this on Sunday night, the Dow futures are trading up 78 points from the Friday close and the Japanese yen is in free-fall. Too bad that I?m 110% long ?RISK ON? positions in my model portfolio.

That was no surprise as 70% of Greeks want to stay in the EC. The way is now paved for a more civilized workout of the country?s financial problems which spreads austerity out over many more years, making it more tolerable and digestible for its citizens.

The latest Commitment of Traders report showed the Euro (FXE) (EUO) shorts in the futures hit yet another all-time high, and that the underlying was now worth $20 billion in the foreign exchange market. Shorts in the interbank cash market and ETF?s are thought to be much larger. On top of that, central banks have been seen unloading reserves denominated in Euros.

This witches brew of one-sided positions made up the perfect ingredients for the type of rip-your-face-off, snap back short covering rally that we have seen in past days. This is why I covered my own shorts three weeks ago when it pierced the $126 handle.

Keep in mind that the media has a lot of blood on its hands with its wild over exaggeration in its predictions of the imminent collapse of Greece and its withdrawal from the European Community that was never going to happen. It is focusing 99% of its attention on the Land of Socrates and Plato that accounts for 1% of European GDP. In the meantime, it is ignoring Germany which has 30% of GDP and is still growing, albeit at a slower 1% rate.

CNBC, in particularly, seems to be mercilessly beating this dead horse, holding it out as an example of what will happen to the US if it pursues similar high spending polices. This is why they send a Tea Party activist out to Athens at great expense every week to provide your coverage and to bait the Socialist candidates. They haven?t been this wrong since they reported that the Facebook issue was 30 times oversubscribed in Asia the night before it became the worst IPO in history.

But Greece has about as much in common with America as the US Treasury has with the bankrupt city of Vallejo, California. If anything, Greece is a perfect example of what happens when the wealthy get away with paying no taxes. Anyone with substantial means there stashes their dosh in Swiss bank accounts, leaving only the poor to cough up government revenues. Rich Greeks are just better at it than Americans. After all, they have been practicing for 5,000 years.

Greece is so small that it would be economic for Germany to just pay off half of its national debt just to maintain stability for its largest export markets. Should they spend $270 billion to protect $1.27 trillion in annual exports? It makes sense to me.

And let me give you a little back story here which you probably haven?t heard. Where did all this debt come from? Greedy unions? Careless bureaucrats? Spendthrift socialists? Expensive national health care?? A very big chunk was the result of the 2004 Athens Olympics where the government spent billions on huge sporting facilities and infrastructure that would only be used once and that it could never afford. Who constructed these massive edifices? German engineering firms. I know because I was there. There is always more to the story than the headline.

I hope my guests at my upcoming July 18 Frankfurt strategy luncheon don?t tar and feather me, or whatever they inflict on miscreants there, for expressing this opinion.

All of this is leading up to a great shorting opportunity for the beleaguered European currency. Given the current positive background, it could make it all the way back up to $127.80. That is a neat 50% retracement of the recent move down from $132.80 to $123.00. But be careful not to fall in love with it. The major trend in the Euro is still down, aiming for $1.17. And with a 0.50% interest rate cut by the European Central Bank imminent, that target could be hit sooner than later.

Don?t Fall in Love With the Euro