Mad Hedge Technology Letter

April 26, 2021

Fiat Lux

Featured Trade:

(BUY OR SELL DOORDASH?)

(DASH), (GRUB), (UBER)

Mad Hedge Technology Letter

April 26, 2021

Fiat Lux

Featured Trade:

(BUY OR SELL DOORDASH?)

(DASH), (GRUB), (UBER)

As the work from home economy de-levers, the biggest loser of this trend will be the food delivery company DoorDash (DASH).

As the stock rallied last Friday by 6% into the close, I couldn’t help but think to myself that it is a great time to short the stock.

Considering that total sales grew close to 400% last year but the stock is lower, this basically means that DASH couldn’t deliver what shareholders wanted in a historic year for most tech companies.

What makes anyone think that 2021 will be different?

Imagine what the next phase of development looks like, quite bleak.

The health crisis unlocked a tsunami of growth for many emerging and unprofitable technologies.

Software and hardware companies were clear beneficiaries of economic lockdowns that triggered a boom in the food delivery industry.

With nowhere to eat out at, the business of eating a prepared meal was effectively handed to DoorDash on a silver spoon.

Despite this powerful tailwind, the company still failed to deliver positive earnings amid additional expenditure such as marketing.

As the pandemic navigates towards a solid solution and consumers return to restaurants, DoorDash will be left holding the bag.

First, let me say, DoorDash’s operating narrative is weak.

They earn revenue by taking a percentage of restaurant sales on its platform.

A glorified pizza delivery boy at scale is what they really are.

They describe sales as marketplace gross order value or GOV which totaled $24.66 billion in 2020 — a 326% increase over 2019.

In short, it's the total amount of money that DoorDash users paid for food.

For context, this metric grew 187% in 2019 compared to 2018, but off a much lower base from $2.8 billion and now project marketplace GOV in 2021 in the range of $30 billion to $33 billion, which is a substantial deceleration in growth rate from 2020.

The bottom line is they are still losing around the same amount of money with no solution in sight.

The next steps of the global economies are to open further, with fewer people staying home and using food delivery, so the question is whether the DoorDash marketplace will grow at all this year.

Despite a record 2020 that more than quadrupled the company's revenues, it is becoming clear that DoorDash will not even be close to profitable.

It appears DoorDash's growth in costs tracked closely with growth in revenue, in dollar terms, leading to net losses that only marginally improved.

The main thesis of these gig economies is that they become incrementally profitable at scale, but DoorDash’s financials suggest it isn’t.

I would like to hear what the next way forward is, but the firm is essentially a one-trick pony in a hopeless industry.

If interests tick higher and regulation toughens, this stock will get hit hard.

There are too many tech firms in the food delivery space and consolidation will force management’s hand.

Uber Eats is the reason that DASH won’t be able to raise prices.

DoorDash holds an advantage with 55% of the US market, but both Uber Eats (at 21%) and GrubHub (GRUB) (at 16%) have made aggressive acquisitions to help them grab market share.

All of these companies often mirror age products with no differentiation.

It is a very homogenized product.

Uber Eats has the largest global footprint in the industry, with a higher overall gross order value that hit record levels in 2020, yet that company loses money like DASH.

GrubHub also delivers the same terrible unit economics that DASH does, giving investors higher revenue but marginal margin improvements and profitability.

Companies that cannot become profitable when 4X their revenue need to be overlooked and this statement could cut across all industries from energy to retail.

Imagine that Dash also couldn’t improve unit economics when gas prices cratered as well.

It appears that Dash will have most external forces working against them for the rest of the year and this is a great stock to sell rallies on.

The initial peak of $230 could well become the peak for this stock and the current share price is 1/3 lower, but I believe a fair market cap would be half the peak of $230 in 2021.

Mad Hedge Technology Letter

March 26, 2021

Fiat Lux

Featured Trade:

(AVOID THIS KOREAN ECOMMERCE COMPANY)

(CPNG), (AMZN), (GRUB), (UBER), (JD), (SHOP), (MELI)

I might characterize Coupang (CPNG) as something akin to China’s JD.com.

It's an e-commerce company that has fulfillment solutions, not dissimilar to Amazon (AMZN) Fulfillment. They also have storefronts that they provide for businesses, which isn't dissimilar to say, a Shopify (SHOP).

Even combining aspects of Amazon and Shopify are there but they don’t have the powerful AWS cloud business.

Similar to JD.com (JD), which is a Chinese e-commerce platform, Coupang has differentiated itself by owning its entire logistics and delivery system.

What is different about Coupang versus the other players in Korean e-commerce is that they own their own inventory for the most part.

That means that they have inventory sitting on their balance sheets.

They have responsibility for pushing that through. But it also means, since they directly negotiate with the manufacturers of these items, they're able, for the most part, to get lower prices.

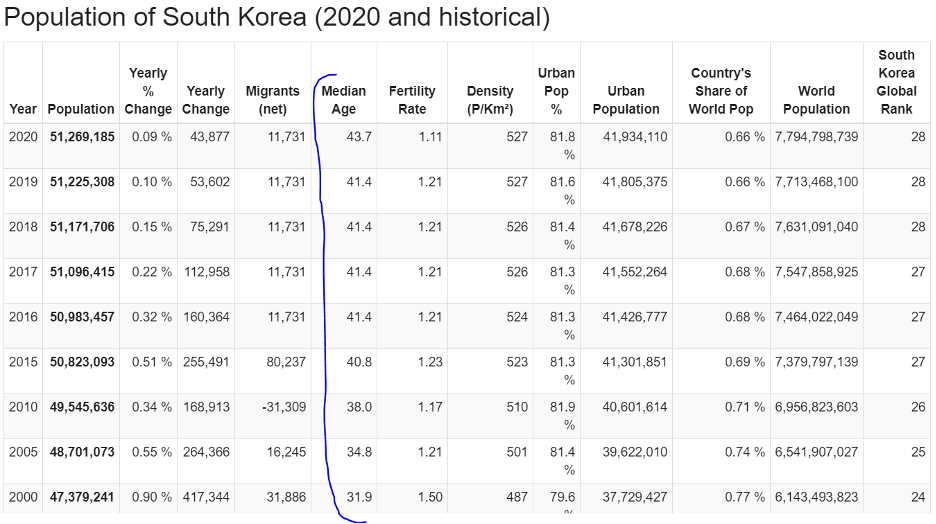

Total Korean e-commerce spend was $128 billion in 2019, which is expected to grow to $206 billion by 2024, implying a CAGR of approximately 10%.

This is where Coupang has a chance but in a rising interest rate environment and with competition on the New York exchanges from Amazon (AMZN), Shopify (SHOP), even MercadoLibre (MELI), I don’t believe Coupang is more attractive than these 3 in its current form as it relates to American investors pouring money into their stock.

Is it an advantage if 70% of Koreans live within seven miles of the Coupang logistic centers?

Certainly, there is that train of thought.

The massive investments into fulfillment centers mean they can surpass the delivery speed of many of its competitors because South Korea is essentially one capital city with millions upon millions hovering on top of each other like many other parts of Asia.

The problem I can have with this scenario is that margins could suffer because a busy Korean lifestyle doesn't lend itself to things like in-store shopping as readily as it does in the United States, and it could manifest itself with Koreans tapping into higher frequency in which they buy online which will push up total spend, but margins will decrease because you are buying stuff that won’t move the needle higher because you've paid for the service.

I can easily see someone just buying one item for delivery in the morning and doing that seven days per week.

Now I need a set of tweezers, I'm going to order that. Tomorrow, I need cotton pads, I’m going to order that.

Over time, operating margin will get butchered with a business like this.

And what do you know? I’m right, they have been losing billions upon billions the past few years with no end in sight.

How long will the external investors subsidize their losses?

At a broader level, mobile phone penetration is already at 96% of Koreans and 40% of Koreans order groceries online, so it’s hard for me to digest where the addressable market can expand from here because they have already collected so much of the available harvest.

This IPO does feel a little bit like an ex-growth dump on the retail investor and that’s not saying shares can’t appreciate at all, but investors believing this is the next Amazon are sorely mistaken.

They are not Amazon, not even close, and they are also confined to one small market where the population has peaked and will start decreasing in numbers.

The population is only 15% of the U.S. and incomes in the U.S. are vastly higher, so how does Coupang become an Amazon without the AWS business?

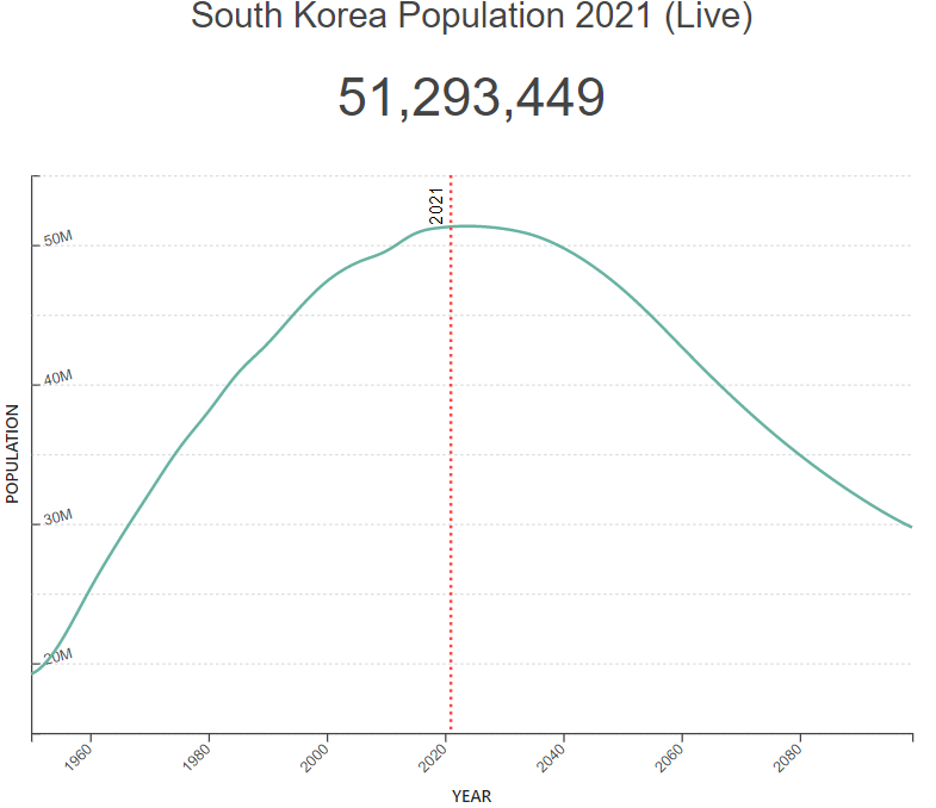

Just as disturbing, the median age in Korea has ballooned from 31.9 in 2000 to 43.7 in 2020 and this cohort doesn’t strike me as the group in the glory years of family formation, peak spend, or technological know-how.

As the Korean population starts to decline in 2025 and the median age creeps up from 43.7 to 50, then aside from adult diapers, where does the incremental growth come from in Korea?

I just don’t see it.

Personal incomes are going to rise at an annualized rate of about 3% every year and I believe much of the total spend will be fought out attempting to woo the big buyers which offer a point of attack for competition that should come around in the next 2 to 3 years.

They also have Coupang Eats, not dissimilar to Grubhub (GRUB) or Uber (UBER) Eats. They have grocery delivery, and even an integrated payment processor. All of these things that took Amazon much longer to build out, admittedly, were a little before their time there, Coupang has already integrated that into the platform.

For this, I give them credit, but they are still nothing like Amazon in terms of potency and scale.

In 2019, active customers rose 34% and that’s what a prototypical growth company should do.

It’s not shocking.

Then an analyst would think that with covid and all that public chaos pinning consumers at home, surely, Coupang would grow active customers by 50% of even 60% in 2020, right?

But active customers only grew 18% in 2020, and they provided zero insight about why active customer growth slowed nearly in half year-over-year, and that for me shows, Coupang is severely limited by what Korea can offer in terms of growth and total spend.

If readers want to get into the Korean economy then I would advise to wait on other Korean homegrown entrepreneur-led startups with IPOs in the pipeline by Krafton Inc., the creator of hit game PUBG, and the country’s biggest mobile-only bank Kakao Bank. Unlike Coupang, those firms are profitable.

Ultimately, total e-commerce spend for all Internet buyers in Korea is expected to grow from approximately $2,600 in 2019 to approximately $4,300 in 2024 on a per buyer basis and Coupang will take advantage of that but I don’t foresee the 30% annual rise in underlying shares that others do.

I can definitely visualize a grind up with periodical substantial selloffs because of missed targets and disappointing forecasts.

That’s not the type of price action I want to see.

The signs point to Coupang maturing immediately and the executive management creating a special clause to allow them to dump shares right after the IPO illustrates that this tech company will stall out moving forward.

Normally, management must wait 6 months after going public before the lock-up period ends.

Highly unusual and can you believe it? They even gave stock shares to their courier drivers at the IPO, making me pause, then come to the conclusion that I rather invest in a tech company returning incremental value to the shareholders and not the manual labor that is paid by an hourly wage. How bizarre!

Avoid Coupang like the plague.

Mad Hedge Technology Letter

November 9, 2020

Fiat Lux

Featured Trade:

(UBER BACK FROM PURGATORY)

(UBER), (LYFT), (GRUB)

The most impacted tech company in 2020 is most likely ridesharing company Uber and is highly likely to become the new “buy the dip” tech stock.

I’ll tell you why and how they managed to turn it around.

Foundationally, two important data points from their earnings report have to be total revenue declining 18% year-over-year and delivery revenue growing 125% year-over-year.

The good news is that delivering food is turning out to be a monumental growth engine and the bad news is that the core business is hamstrung by the current conditions stemming from the global health crisis.

Even with their core business declining, Uber benefits from a silver lining of the macroeconomy recovering from summer lows and this will follow through into its ride-sharing operations.

The initial recovery from terrible to bad is usually the greatest in terms of percentages similar to recent quarterly GDP numbers.

I am definitely observing positive movement in Uber’s direction, especially as consumers feel less comfortable taking mass transit during the pandemic.

This development is clearly much better than a mass lockdown where Uber is unable to deliver on any rideshare volume whatsoever.

Management has also indicated that the overall environment is starting to considerably improve over the coming quarters with Q2 marking a clear trough in volumes and fundamentals.

Another potential tailwind is that the consumer element is becoming commonplace across cities both in the US and internationally and their preference will steer them away from mass transportation given health concerns.

This could result in an incremental demand driver for ridesharing vendors over the next few quarters and beyond.

Structurally, Uber will get to the other end of the health crisis intact and as a healthy corporation.

That speaks volumes compared to corporates floundering in damaged industries like energy and retail.

But the elephant in the room was finally addressed with the passage of California’s Proposition 22, a measure that exempts it, along with rival Lyft (LYFT) and businesses like Instacart and GrubHub (GRUB), from having to pay drivers like in-house employees.

This is the feather in their cap they needed to become the newest buy the dip tech stock because it essentially means they won’t have to pay drivers much to drive for Uber instead of doling out proper employment contracts.

The passage of the proposition legitimizes Uber’s business model at a time where the global economic environment is precarious, and we could be walking straight into legislative gridlock and an inadequate fiscal stimulus package.

This obviously means putting less dollars in consumers’ pockets to pay for Uber Eats and Uber rideshares.

This was essentially an existential issue for Uber in the state of California and without a win, Uber and Lyft threatened to pull out of California entirely.

This has happened before like in Austin, Texas, which Uber deserted in 2016 after the city passed a measure calling for stricter background checks and fingerprinting for drivers.

Fortunately for Uber, Texas State Legislature overruled Austin, and Uber and Lyft returned to the city.

The current ballot count is 58.4% in favor of Prop 22 and 41.6% in opposition meaning Californian citizens overwhelmingly voted to pass this measure.

Californians, no doubt, were scared to lose their cheap way of getting around the suburban sprawl that is California.

Even if Uber’s company creates a traffic snarl of drivers meaninglessly idling around for more rides – that is a moot point right now.

Gig workers will continue to be classified as independent contractors in the state.

It also essentially makes these gig companies exempt from AB-5, the gig worker bill that went into law at the beginning of the year that forces gig companies to pay sub-contractors like regular workers.

That is off the table and a massive win for Uber.

On the back of this legislative success, Uber will now take this win and go after other states to pass similar types of legislation.

This political template for future anti-labor, corporate law-making is pro-capital to the extreme extent of the law for better or mostly worse in my eyes if you aren’t a corporate shareholder.

This perhaps could open up all corporations in California to never pay health or social security benefits in the future to employees.

If Uber doesn’t have to, then why does Google, Facebook, or Apple need to share the burden of paying for medical and social security benefits?

Labor groups are considering potentially lobbying the newly elected Biden administration’s Department of Labor for improved federal laws for worker classification.

Biden has pledged to narrow economic inequalities and Uber’s win could be in his crosshairs because the result is a massive setback for labor laws in California and potentially around the United States.

Intervention would take some balls by the Biden administration and the most likely scenario is him giving Uber a pass.

Gig Workers Rising, a campaign supporting and educating app and platform workers, had this to say, “Billionaire corporations just hijacked the ballot measure system in California by spending millions to mislead voters. The victory of Prop 22, the most expensive ballot measure in U.S. history, is a loss for our democracy that could open the door to other attempts by corporations to write their own laws.”

Yes, this is terrible for Uber drivers but highly positive for shareholders of Uber’s stock.

The cost of doing business is effectively passed on to the guy at the bottom – sub-contracted drivers.

Like it or not, it will be enshrined into Californian law and this makes serious inroads to Uber’s business model actually becoming profitable which has been the big knock on this company.

At the very minimum, this will give a stop-gap measure for the 10 or so years Uber needs to get to autonomous driving technology where they can just never pay the driver again.

Not only does the path to autonomous driving technology look optimistic, but the excess liquidity circulating in the market effectively means that zombie companies will be funded infinitely.

Although not a zombie company, Uber has really had a hard time making up the numbers to prove a viable path to sustainability and that basically doesn’t matter anymore.

The existential threat is now out of the window and with several structural tailwinds powering Uber, the stock and the company have never had a brighter future and any medium-sized pullback should be bought.

This one is going higher.

Mad Hedge Technology Letter

May 15, 2020

Fiat Lux

Featured Trade:

(WHY UBER IS BUYING GRUBHUB),

(GRUB), (UBER)

To understand the unintended consequences of the Fed’s helicopter money to U.S. capitalism, we can put a magnifying glass over Uber’s (UBER) recent takeover attempt of Grubhub (GRUB) as what’s in store for not only the tech sector but the wider public markets.

Zombie companies parade around Europe and Japan because of an era of low interest rates and cozy bank relationships that keep these companies from dying out.

To read more about Allianz Economic Advisor Mohamed El-Erian’s take on zombie companies – click here.

It’s not a surprise that Japan and Europe are highly unproductive, and innovation ceases to exist when capital is being tied up in marginal companies with management happy to let capital slosh about without adding extra added value.

I get it that the Fed is trying to “save” the wider U.S. economy by bringing out the bazookas and even by buying junk-graded debt which was once seen as heresy.

But what we have now are inferior companies that will never turn a profit masquerading as real companies that would be on life support if not for cheap capital.

In almost every instance, the only winners are the executive management who pillage the system and cash out when they are allowed to sell their stock.

U.S. Representative for Rhode Island David Cicilline hit the nail on the head when he described the fluid situation by focusing on two of the bad apples, saying “Uber is a notoriously predatory company that has long denied its drivers a living wage. Its attempt to acquire Grubhub — which has a history of exploiting local restaurants through deceptive tactics and extortionate fees — marks a new low in pandemic profiteering.”

Uber is a taxi service that undercompensates its highest expense - the driver, and Grubhub delivers restaurant food but rips off the restaurants in doing it.

I defined exorbitant delivery fees as up to 40% which Grubhub is infamous for charging.

Yes, even with predatory practices, they cannot turn a profit.

Now, in this new normal of coronavirus, it would be a miracle to make any operational headway.

Uber’s attempted market grab is a giant red flag.

My guess is that they are doing this in order to jazz up the balance sheet and concoct some ridiculous new metric showing a pathway to growth.

By adding growth to revenue, Uber would be able to preach “growth” even if it’s of bad quality.

I thought the tech market was done looking through to grow by essentially killing off the “WeWork model.”

However, Uber is going for a model that is one notch above that model and repurposing it as something actually meaningful, which of course, it’s not.

They are already in litigious hell regarding driver’s remuneration, and that will not die down and could even destroy Uber.

Uber has in fact ignored California state orders to reclassify its drivers as employees and have appealed the court’s decision.

The New York state government has validated my theory of these fly-by-night delivery outfits being a net negative for business and society.

The New York City Council compared food ordering apps Grubhub and UberEats to blood-sucking parasites this week before passing emergency legislation aimed at helping struggling restaurants lower delivery costs during a precarious time.

During the state of emergency, a new vote passed capping food ordering and delivery app fees at 15% in delivery fees and 5% “other” takeout order fees.

To read more about this decision by the New York City Council – click here.

This was done to give some power back to the restaurants that have been getting fleeced.

The balance sheet shows the whole story with Uber's net loss totaling more than $8.5 billion in 2019 and in February, they reported a net loss of $1.1 billion in the fourth quarter.

Let me remind readers that Grubhub posted a net income loss of $27.7 million for the last reported quarter as well.

As it turned out, Grubhub rejected Uber’s offer believing it didn’t meet their valuation of the company.

It would appear natural that a predatory company with no competitive advantage would set a market premium that would align with their borderline extortionate ways.

Do not own either one of these companies – there are far better ones out there in tech and no need to scrounge at the bottom of the barrel.

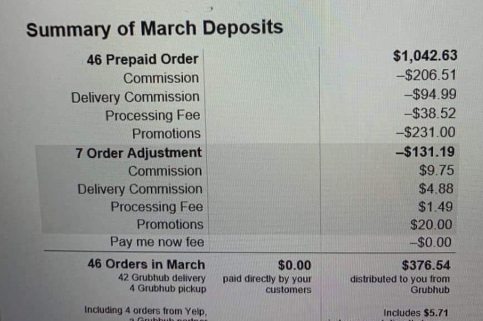

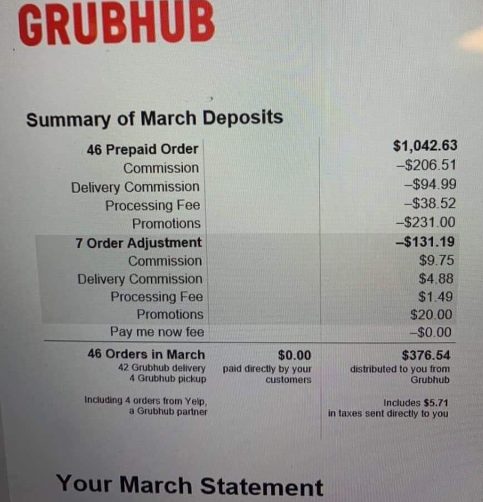

Monthly Grubhub bill for Chicago Pizza Boss During the Epidemic

Mad Hedge Technology Letter

April 8, 2020

Fiat Lux

Featured Trade:

(AVOID YELP ON PAIN OF DEATH)

(YELP), (GRUB)

Tech investors should be migrating towards stocks that have high visibility of an earnings turnaround once a health solution is discovered for the current health scare. One that definitely does not fit the bill is Yelp (YELP) who has experienced negative earnings growth for the past three years.

What’s the deal with Yelp?

The company recently withdrew its first quarter and 2020 financial guidance because the coronavirus has destroyed large parts of its business probably to never return.

If you didn’t know, Yelp provides information through online communities on restaurants, shopping, nightlife, financial, health, and other services, so it’s easy to do the calculus as to why lockdowns and restrictions on public life are affecting these revenue streams.

A recent survey reported a higher average likelihood of households missing a debt payment over the next three months, meaning the consumer is in dire straits unless there is a swift 180 in circumstances.

In the longer-term, the New York Fed affirms a “persistent deterioration” in consumers’ expectations to access credit throughout the rest of 2020.

The New York Fed said the sharp decline in consumer expectations cuts across all age, education, and income groups.

Less money for consumer spending means less consumer demand on Yelp translating into lower ad revenue – it’s that simple.

On a conference call on February 13, Yelp mentioned that it expects 2020 revenues to grow between 10% and 12% year over year and adjusted EBITDA by 1 to 2 percentage points. It had also expected margins to expand again in 2020.

What a difference 4 weeks makes!

Now almost every company is in survival mode and Yelp is the weakest link.

Consumer interest in restaurants and nightlife has taken a nosedive in the new coronavirus economy.

Yelp data shows that consumer interest had declined 54% for restaurants and 69% for nightlife venues.

Cafes, French restaurants, and wineries decreased their share of daily consumer actions (down 66%, 47% and 44%, respectively) week over week.

In contrast, the weekly growth numbers favor just a select few - grocery stores interest is up 102%, fruit and vegetable shops are up 102%, fast-food joints are up 64%, and pizzerias round out the bunch up 44%.

Some hard-hit companies come in the form of bowling, yoga and martial arts services which tend to involve groups of people, declined by a respective 43%, 38%, and 33%, and these are all companies that would be spending ad money.

Even worse news on the financial side - mom and pop stores have a short leash with median cash buffer for a small business at just 27 days.

As you would assume, searches on home fitness equipment surged 344%, and interest in parks rose 53%.

Interest was also up 360% for buying guns and 166% up for buying water - breweries were down 61%.

Lawmakers and states, including New York, New Jersey, California, and Pennsylvania, have ordered a temporary closure of restaurants and bars and I can safely say that consumers probably won’t return the next day to barge down the entrance door.

The last earnings report wasn’t all that hot for Yelp who missed on revenue while spending 10% more on advertising to get to that miss.

Earnings per share also missed estimates by sliding 35% year over year validating my thesis that this is a sinking ship headed towards an iceberg.

These propped up numbers were before the coronavirus hit the company and the business model is poorly prepared for this type of phenomenon and the lasting effects.

I expect a material decrease in the growth of the number of paying advertising locations and lower advertising budgets from multi-location customers.

Paying advertising locations should drop by half just this quarter.

Materially lower traffic dropping over 50% is a trend that will perpetuate and even if there is a dead cat bounce because shares are so beaten down, this is an unequivocal “sell on the rally” type of stock.