Mad Hedge Technology Letter

January 13, 2020

Fiat Lux

Featured Trade:

(THE DEATH OF THE GIG ECONOMY)

(GRUB), (OYO), (LYFT), (UBER), (RAPPI)

Mad Hedge Technology Letter

January 13, 2020

Fiat Lux

Featured Trade:

(THE DEATH OF THE GIG ECONOMY)

(GRUB), (OYO), (LYFT), (UBER), (RAPPI)

The demise of the gig economy is upon us.

That is the latest takeaway from a slew of negative news overflowing the news wires lately.

As many of you know, I hate this niche of tech with a passion, and it has been discovered as nothing more than a marginal fly-by-night sub-sector passing off the cost of employees and their wages to the investor.

They also contribute no meaningful technology that moves the needle.

When the hammer fell on Adam Neumann’s WeWork, the hammer fell equally as hard on the gig economy business model that brought public markets the likes of Uber and Lyft.

The path to venture capitalist’s cashing in abruptly closed off was the end development to all this mayhem.

So I was not surprised when online food deliverer Grubhub (GRUB) had a dead cat bounce after rumors of them looking for a sale to their badly run company.

Then last Friday was the day the chickens came home to roost with Grubhub shares cratering over 8%.

If there is a sale, at what heavily discounted price will it go for?

We could see a marked down shell of its former self.

Grubhub naturally came out and rejected the notion that they are about to be sold off.

Where there is smoke – there is fire.

They did, however, admit they are in the process of “consulting” about certain acquisitions which could mean purchasing inorganic growth to juice up their numbers ahead of a sale.

There are four market leaders who control roughly 80% of the food delivery service business.

But the food war is far from over as competitors undercut each other time after time.

Competition in the food delivery market is driving down the unit economics of online food delivery to a nadir at a time when they can least afford it.

The other three involved are Uber Eats division of Uber (UBER) as well as Postmates and DoorDash.

Grubhub mentioned that there will likely be opportunities to acquire market share, but at what cost?

Acquiring inorganic revenue is at peak cost in 2020.

Cost per unit matters more now than any other time in the past 10 years boding ill for Grubhub and its competition.

And until they adequately address the unit economics in detail, readers must assume that Grubhub is on a suicide mission and you won’t know how close they are to the end until there is a dramatic announcement describing it.

The big takeaway here is that conditions are ripe for consolidation in the online delivery business.

As we go further out on the risk curve, private unicorns are in dire straits too.

Taking a barometer of this subsector allows investors to digest the level of risk premium in the overall markets that can be applied to safer parts of the tech ecosphere through extrapolation techniques.

Venture capitalist Masayoshi Son is infamous for overpaying a slew of tech growth firms and in 2020, so far, it has not been kind to him.

Oyo allows customers to book hotel rooms in more than 80 countries through its app.

It even converts struggling local hotels into Oyo franchises, puts up some money to remodel the interior, and takes commission on every booking.

The startup is dumping 5% of its staff in China and another 12% of employees in India, as part of a reorganization.

Oyo is the third company in SoftBank's portfolio to shed jobs in a week, following the layoffs at robotic pizza startup Zume and car rental company Getaround.

Oyo has sucked in more than $3 billion in capital and the last insane tranche of investment values the company at more than $10 billion.

SoftBank has been throwing money at the company since 2015.

The firm is otherwise known as the "SoftBank's jewel in India" for being one of the country's most valuable private companies.

However, there has been a recent barrage of sub-optimal reports suggesting they have accelerated sales by underhanded business practices.

A peek into the firm showed explicit evidence that Oyo rented thousands of rooms at unlicensed hotels and guesthouses then allowing police and other officials use the service for free to avoid trouble with the authorities.

The pain for Softbank doesn’t just stop at Oyo, Rappi has been dragged down as well.

The Latin American delivery startup is laying off 6% of its workforce, less than a year after Japan’s SoftBank Group pumped in nearly $1 billion in the company.

Softbank is putting pressure on local management to trim the fat off their models and forcing them to become profitable now.

Rappi has expanded to nine countries since its founding in 2015.

It plans to be the swiss army knife of online deliveries by getting into groceries, restaurant meals, medication, furniture, and has even foolishly branched out into scooter rental, travel, and basic banking services.

Softbank plans to pour another $4 billion into South American startups but one must beg to ask, are they throwing good money on top of bad money?

Certainly seems so.

When asked how soon Rappi would turn in a profit, co-founder Sebastian Mejia was adamant that his sole priority was to grow fast, and that investors were on board with the plan.

This is code name for NEVER!

Softbank and its vision fund are set for more death by a thousand cuts in 2020, and being in the wrong place at the wrong time aggravates the mess they find themselves in.

Short all companies reliant on gig economy workers in the public markets and prepare for a gloomy IPO pipeline that will last through the end of 2020.

Mad Hedge Technology Letter

October 30, 2019

Fiat Lux

Featured Trade:

(GRUBHUB'S TOXIC MEAL),

(GRUB), (UBER), (LYFT)

It took me precisely 28 days and not a day more.

That’s how long it took for my bearish call on desperate online food delivery company, GrubHub (GRUB) to come to fruition.

I wrote an overly negative report on the company which was published on October 2nd explaining why this company and its terrible unit economics were set for a rude awakening.

I usually don’t revisit the same company within the same month in this newsletter, but when I looked at the price this morning, it took me a few minutes to wrap my head around the 44% daily decline.

I will go one more step now and profusely recommend that nobody in their right mind should currently take any bullish positions on any company reliant on employing the gig economy.

The gig economy has been found out for what it is – an elaborate scheme enriching tech stakeholders while shorting American blue-collar labor.

Instead of proper wages flowing to the Uber driver or in this case the GrubHub driver, management has maneuvered its way through some nifty alternative classifications enabling companies to divert a chunk of capital back into the business model.

If these companies can’t make money with skimping on driver pay, how will they make money when American law mandates them to cover sick leave, paid vacations, health insurance, and overtime pay which could soon be coming?

And on top of the subsidies which add to the overall unit cost, how on earth will they piece together a solution that would satisfy shareholders?

Then mix the unworkable unit economics and fuse it with a boatload of competition and my conclusion is clear - profitability is a pipedream.

Buttressing my claims of unprofitability and market stagnation in a note to shareholders, the company admitted, “supply innovations in online takeout have been played out.”

The pitiful food delivery company slashed fourth-quarter revenue projections to between $315 million and $335 million making a mockery of the $387.3 million consensus.

The house of cards is finally collapsing.

Who is the competition?

There are three fierce contestants in UberEats, DoorDash and PostMates.

And to add even more spice inside the fajita, PostMates has recently shelved a planned 2019 IPO because of “market conditions,” a testament to the poor growth prospects for online food deliveries.

I believe no food delivery stock will ever go public again unless they revalue themselves 65% lower from today’s prices.

Much of the value in these companies is a mirage.

To give GrubHub credit, they didn’t put up Chinese walls in their guidance and mentioned that competition is wreaking havoc detailing that their customers are not “extremely loyal.”

They should expect investors to not be extremely loyal either.

Existing customers are now price-shopping by surfing around different apps to take advantage of price promotions proving my point that these gig economy companies contribute minimal incremental value to the end user.

Their secret sauces are hardly secret.

These apps are commodities and yes, there is value in their proprietary algorithms, but by no means are the barriers of entry so colossal that it would take North Korean engineers 10 years to reverse-engineer these same algos.

And with wielding low-grade tech and resigned to “low double-digit” growth, the bullish case behind this stock and the industry as a whole becomes almost laughable.

Don’t bring a knife to a gunfight!

If Uber can perform miracles and reach $40 or if Lyft can snake its way up to $55, these would be the perfect entry points to scale into these cash burn disasters from the short side.

As for GrubHub, don’t buy the dead cat bounce.

Mad Hedge Technology Letter

October 2, 2019

Fiat Lux

Featured Trade:

(IT’S TIMES UP FOR GRUBHUB)

(GRUB), (UBER)

The jury is out, and heads could roll.

That is what the tech market has been telling us and that is why I am slapping a conviction sell rating on the struggling online food delivery company GrubHub (GRUB).

The gig economy has been found out and the industry is about to have their free lunch taken away.

Many tech companies handling cheap labor by employing key workers as independent contractors are about to lose their shirt.

Considering that GrubHub cannot make the unit economics work in their favor when times are good, what do you think will happen if they have to start paying overtime, healthcare, and bonuses to full-time drivers?

Unfortunately for GrubHub, you cannot just strip out the driver in the business model, someone needs to get the hot tacos from point A to point B and back.

Along with higher labor costs, delivery fees are on the verge of cratering because of elevated competition.

GrubHub doesn’t have a monopoly in this industry and restaurants continue to complain that the likes of Postmates, DoorDash, GrubHub and Uber (UBER) Eats rip them off leaving the restaurants with their necks just above water.

GrubHub is so pitiful that they have had to resort to nefarious tactics condemning a failing business model.

Investors should aggressively short the stock or avoid it at all costs.

What type of tricks has GrubHub been up to?

If you hadn’t heard already, Senator Chuck Schumer was in contact with the CEO of GrubHub Matt Maloney over fraudulent fees the food-delivery giant has been charging restaurants nationwide and demands full refunds for cheated customers.

GrubHub was charging restaurants fees for phone calls that didn’t result in food orders and the company admitted wrongdoing.

The company responded by offering only 60 days’ worth of refunds even though this dark practice had taken place for years.

The exploitation took place because of in-house algorithms that calculate fees, which restaurants say can range between $5 and $9 for a single phone call.

GrubHub recently refunded one New York City restaurant vendor over $10,000 for the fraud, covering fees going back to 2014.

GrubHub agreed to extend the refund to 120 days of ill-gotten fees, but many regulators have said this is still not enough.

Then if you didn’t think that was bad, GrubHub had its hand in anti-competitive tactics that sum up the plight of the company.

GrubHub has been creating fake websites, impersonating third party restaurants by undercutting them to take control over their own web sites then taking a larger cut of commissions.

The company says that the fake websites are “a service” for clients, but when the cybersquatting has been to the detriment to the restaurant, using this point of leverage to swindle restaurants out of more fees and sometimes charging them more than 400% of the actual cost.

This insane move has strained relations and murdered trust between GrubHub and outside vendors while making it extraordinarily difficult to take back control over their website.

As you would expect, GrubHub is monetarily incentivized to control the thoroughfare.

A GrubHub spokesman commented saying there would be “no changing of our algorithm” but from how I see it, the writing is on the wall, the equity in the company is in a vicious spiral downward.

It’s hard to make money in restaurants but GrubHub is overreaching big time.

Invest in this company at your peril and avoid all online food delivery platforms, they are simply ghastly investments.

Mad Hedge Technology Letter

July 15, 2019

Fiat Lux

Featured Trade:

(HOW SOFTBANK IS TAKING OVER THE US VENTURE CAPITAL BUSINESS),

(SFTBY), (BABA), (GRUB), (WMT), (GM), (GS)

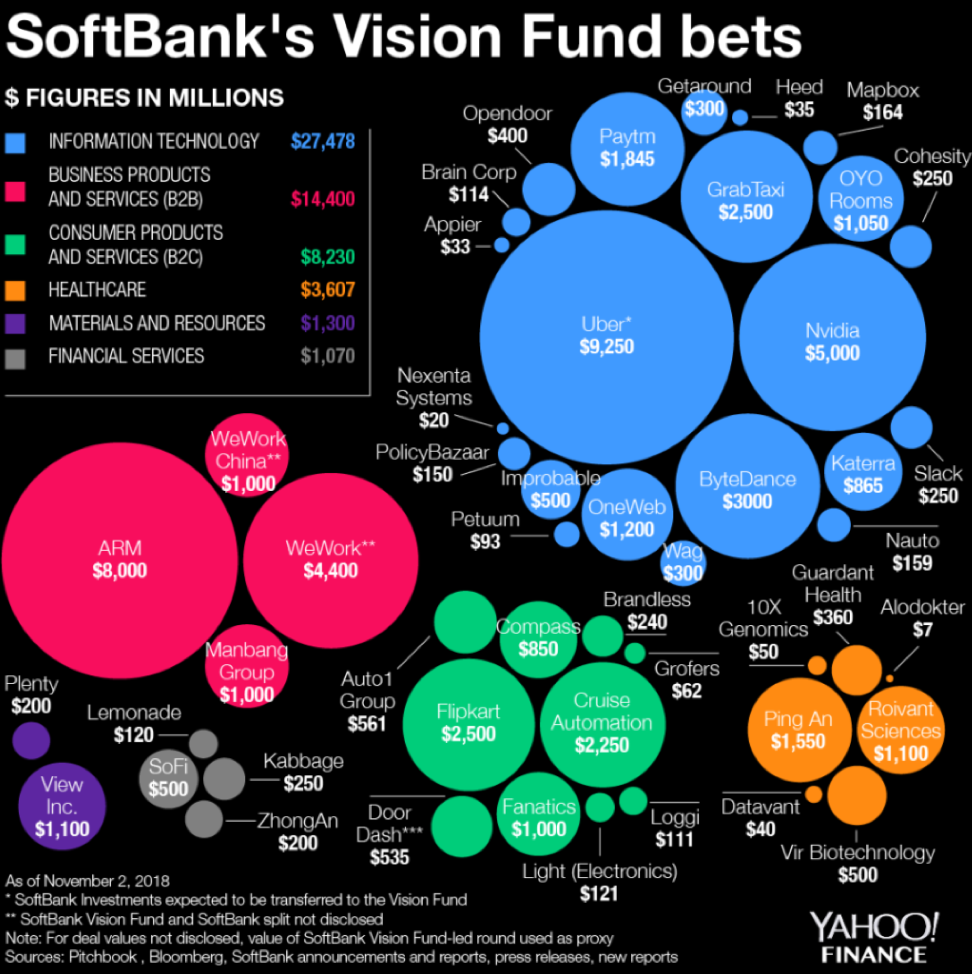

The man with the 300-year vision - Softbank’s Masayoshi Son.

He is the sole force exerting stultifying pressure on the venture capitalists of Silicon Valley.

What a ride it has been so far.

His $100 billion SoftBank Vision Fund has put the Sand Hill Road faithful in a tizzy – utterly revolutionizing an industry and showing who the true power resides with.

He has even gone so far as to double down on his exploits by claiming that he will raise additional $100 billion fund every few years and spend $50 billion per year.

This capital logically would flow into what he knows best – technology and the best technology money can buy.

Lately, Son said it best of the performance of the Vision Fund saying, “Results have actually been too good.”

So good that after this June, Son changed his schedule to spend 3% of his time on his telecom business down from 97% before June.

His telecommunications business in Japan has turned into a footnote.

It was just recently that Son’s tech investments eclipsed his legacy communications company.

Son vies to rinse and repeat this strategy to the horror of other venture capitalists.

The bottomless pit of capital he brings to the table predictably raises the prices for everyone in the tech investment world.

Son’s capital warfare strategy revolves around one main trope – Artificial Intelligence.

He also strictly selects industry leaders which have a high chance of dominating their field of expertise.

Geographically speaking, the fund has pinpointed America and China as the best sources of companies. India takes in the bronze medal.

His eyes have been squarely set on Silicon Valley for quite some time and his record speaks for himself scooping up stakes in power players such as Uber, WeWork, Slack, and GM (GM) Cruise.

Other stakes in Chinese firms he’s picked up are China’s Uber Didi Chuxing, China’s GrubHub (GRUB) Ele.me and the first digital insurer in China named Zhongan International costing him $500 million.

Other notable deals done are its sale of Flipkart to Walmart (WMT) for $4 billion giving SoftBank a $1.5 billion or 60% profit on the $2.5 billion position.

In 2016, the entire venture capitalist industry registered $75.3 billion in capital allocation according to the National Venture Capital Association.

This one company is rivalling that same spending power by itself.

Its smallest deal isn’t even small at $100 million, baffling the local players forcing them to scurry back to the drawing board.

The reverberation has been intense and far-reaching in Silicon Valley with former stalwarts such as Kleiner Perkins Caufield & Byers breaking up, outmaneuvered by this fresh newcomer with unlimited capital.

Let me remind you that it was once considered standard to cautiously wade into investment with several millions.

Venture capitalists would take stock of the progress and reassess if they wanted to delve in some more.

There was no bazooka strategy then.

SoftBank has promised boatloads of capital up front even overpaying in some cases in order to set the new market price.

Conveniently, Son stations himself nearby at a nine-acre estate in Woodside, California complete with an Italianate mansion he bought for $117.5 million in 2012.

It was one of the most expensive properties ever purchased in the state of California, even topping Hostess Brands owner Daren Metropoulos, who bought the Playboy Mansion from Hugh Hefner in 2016 for $100 million.

If you think Son is posh – he is not. He only fits himself out in the Japanese budget clothing brand Uniqlo. He just needed a comfortable place to stay and he hates hotels.

SoftBank hopes to cash in on its $4.4 billion investment in WeWork, an American office space-share company, proclaiming that WeWork would be his “next Alibaba.”

The company plans to shortly go public.

Son continued to say that WeWork is “something completely new that uses technology to build and network communities.”

Other additions to SoftBank’s dazzling array of unicorns is Bytedance, a start-up whose algorithms have fueled shot form video content app TikTok.

The deal values the company at $75 billion.

They have been able to insulate themselves from local industry giants Tencent and Alibaba.

Son has revealed that the Vision Fund’s annual rate of return has been 44%.

Cherry-picking off the top of the heap from the best artificial intelligence companies in the world is the secret recipe to outperforming your competitors.

At the same time, aggressively throwing money at these companies has effectively frozen out any resemblance of competition. Once the competition is frozen out, the value of these investments explodes, swiftly super-charged by rapidly expanding growth drivers.

How can you compete with a man who is willing to pay $300 million for a dog walking app?

This genius strategy has made the founder of SoftBank the most powerful businessman in the world.

Son owns the future and will have the largest say on how the world and economies evolve going forward.

Mad Hedge Technology Letter

March 20, 2019

Fiat Lux

Featured Trade:

(LYFT), (UBER), (GRUB), (POSTMATES), (DOORDASH), (GOOGL)

The imminent launch of the Lyft IPO is telling investors that the next era of technology is upon us.

Does that mean that you should go out and buy Lyft shares as soon as they hit the market?

Yes and no.

30 million shares are up for grabs and the price of the IPO appears to be pinpointed between $62 and $68.

Even though this company is a huge cash burning enterprise, the fact is that they have been catching up to industry leader Uber and snatching away market share from the incumbent.

It was only in January 2017 that Lyft had accumulated 27% of the domestic market share, and in the recent filing for the IPO, that number had exploded to 39%.

If Lyft can start to gnaw into Uber's lead even more, shares will be prime to rise beyond the likely $62 to $68 level.

Let's remember that one of the main reasons for Uber giving up ground in this 2-way race is because of the toxic work environment embroiling many of the upper management and the subsequent damage to its broad-based public image.

If you wanted the definition of a public relations disaster, Uber was the poster boy.

Story after story leaked detailing payment problems to Uber drivers, a huge data leak revealing millions of lost personal information, and even a crude video of the founder berating a driver went viral.

There might be no Cinderella ending for this ride-hailing operation as litigious time bombs stemming from an aggressive high-risk, high-reward strategy skirting local taxi laws have flaunted the feeling of corporate invincibility in the face of government.

Being the first of its kind to hit the market, I do believe the demand will outstrip the supply.

There is a scarcity value at play here that cannot be quantified.

And an initial pop from the low-to-mid $60 range to about $80 is a real possibility in the short-term.

However, expect any robust price action to be met with rip-roaring volatility, meaning there is a legitimate chance that shares will consolidate back to $50 before they head up to $100.

Some of my favorite picks have echoed this same price action with fintech juggernaut Square (SQ) and streaming platform Roku (ROKU) mimicking heart-stopping price action with 10% moves up or down on any given day.

This doesn't mean that these are bad companies, but they do become harder to trade when entry points and exit points become harder to navigate around because of the extreme beta attached to the package.

The big winner of this IPO is ultimately self-driving technology.

Let's not skirt around the issue - Lyft loses a lot of money and so does Uber and that needs to stop.

It has been customary for tech companies to go public in order for the initial venture capitalists to cash out so they can rotate capital into different appreciating assets.

When companies are on the verge of ex-growth, maintaining the same growth trajectory becomes almost impossible without even more incremental cash burn relative to sales.

This leads to an even more arduous pursuit of revenue acceleration with stopgap solutions calling for riskier strategies.

What this means for Lyft is that they will need to double down on their self-driving technology because they are incentivized to do so, otherwise face an existential crisis down the road.

The most exorbitant cost for Uber and Lyft is by far employing, servicing, and paying out the drivers that shuttle around passengers.

I cannot envision these companies becoming profitable unless they find a way to eliminate the human driver and automate the driving function.

I will say that Uber benefitting from the Uber Eats business has been a high margin bump to the top line.

Yet, food delivery is not the main engine that will spur on these IPO darlings.

This part of the business is getting more saturated with margins getting chopped down every day.

What food delivery mainstays like Doordash and GrubHub don't have, is the proprietary self-driving technology that at some point will be present in every vehicle in the United States and the world.

What we are seeing now is a race to perfect, optimize, and implement this technology in order to further license it out to food delivery operations and other logistic heavy business that focus on the last mile.

The licensing portion out of self-driving technology will become a massive revenue driver eclipsing anything that the actual ride-hailing revenue from passengers can inject.

Well, that is at least the hope.

And because Lyft going public might force the company to remove the subsidies provided to the lift operators, this could translate into higher costs per unit.

The pathway is a no-brainer – Lyft needs self-driving technology more than the technology needs them.

And even though Google is head and shoulders the industry leader with Waymo, Lyft and Uber don't have a world-famous search engine that they can fall back on if the sushi hits the fan.

I believe Lyft passengers will have to pay more for rides in the future because of the demand for meeting short-term targets incentivizing management to raise fares.

Going public first will allow them to set the industry standards before Uber can participate in the discussion gifting a tactical advantage to Lyft.

That is why Uber is attempting to go public as fast as possible because every day that Lyft is a public company is every day that they can push their unique narrative and standardize what is a nascent industry that never existed 20 years ago with their new capital.

If high risk is your cup of tea, then buy shares when you get the first crack at it, otherwise, take a backseat with a bag of popcorn and watch history unfold.

This trade is not for the faint of heart and until we can get some more color on the business model and the ability or not of management to meet quarterly or annual expectations, there will be many moving parts with cumbersome guesswork involved.

To read up on Lyft’s IPO filing on the SEC website, please click here.