Global Market Comments

July 7, 2021

Fiat Lux

Featured Trade:

(JUNE 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (BRKB), (GOOG), (NVDA), (FB), (TSLA), (JPM), (BAC), (C), (GS), (MS), (NASD), ((X), (FCX), (AMZN), (MSFT), (AAPL), (FCX)

Global Market Comments

July 7, 2021

Fiat Lux

Featured Trade:

(JUNE 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (BRKB), (GOOG), (NVDA), (FB), (TSLA), (JPM), (BAC), (C), (GS), (MS), (NASD), ((X), (FCX), (AMZN), (MSFT), (AAPL), (FCX)

Global Market Comments

May 10, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE SUSHI HITS THE FAN),

(SPY), (TLT), (TBT), (V), (UNP), (DAL), (MSFT), (GS), (JPM), (FCX)

During my senior year in High School, I had the good fortune to date the daughter of Richard Knerr, the founder of Wham-O, the inventor of Hula Hoops, Silly Putty, Super Balls, Frisbee’s, and Slip & Slides (click here).

At six feet, she was the tallest girl in the school, and at 6’4” I was an obvious choice.

After the senior prom and wearing my tux, I took her to the Los Angeles opening night of the new musical Hair. In the second act, the entire cast dropped their clothes onto the stage and stood there stark naked. The audience was stunned, shocked, embarrassed, and even gob-smacked.

Those were the reactions I saw on Friday, when the April Nonfarm Payroll Report was released showing a gain of only 266,000 jobs. A million had been expected.

So, how does that work? Red hot ADP private jobs and a year low in Weekly Jobless Claims, but a horrific monthly Payroll report?

They say economic data can be “noisy”. This time it was positively cacophonous. The fact is that these data points were never created to handle times like this, the most disruptive in history.

When the data are useless, all you have to do is take a walk down Main Street. There are “Help Wanted” signs at virtually every business.

The data dissonance created a wild day in the markets on Friday. Bonds soared, causing ten-year yields to dive to 1.48%. Then they rallied all the way back up to 1.58%.

That was seen as the end of the two-month long rally in bonds, so stock took off like a rocket. Essentially everything went up, both cyclicals, banks, AND tech.

All those bond shorts you have been nursing since March? They are about to explode to the upside. The next leg down in the year-old bear market in bonds is about to begin.

And what about that 266,000-payroll report? If you didn’t get a million jobs print in April, then you’ll almost certainly get it in May. Stocks could well keep rally until then. That’s how traders are seeing it.

Just another reason to buy.

By the way, I learned one of the great untold business stories from Richard Knerr. When the Hula Hoop was first launched in 1957, sales went ballistic. Some 25 million were sold in the first four months.

The Hula Hoop was made of a plastic tube stapled together with an oak cork made in England. Since demand seemed infinite, Wham-O ordered 50 million corks. Then the republican party claimed the toy was a communist conspiracy to destroy the youth of America as the swiveling of hips was deemed obscene. This was at the tail end of the McCarthy period.

Sales of Hula Hoops collapsed.

They cancelled the order for 50 million oak corks, which were thrown overboard mid-Atlantic. They are still floating out there somewhere today. Wham-O almost went bankrupt from the experience but was eventually saved by the Frisbee.

Richard Knerr died in 2008 at the age of 82. Wham-O was taken over by Mattel in 1995. For his obituary, please click here.

April Nonfarm Payroll Report is a huge disappointment, at 266,000 when up to one million was expected. April’s hiring boom goes bust. March was revised down massively, from 916,000 to 770,000. The headline Unemployment Rate rose to 6.1%. It was one of the most confusing reports in recent memory. Bonds rocketed, interest rates crashed, and tech stocks took off like a scalded chimp. Inflation expectations have been shattered. Leisure & Hospitality kicked in at 331,000. But Professional & Business Services collapsed by 111,000. The two million businesses that went under last year aren’t hiring. Much of the return to work has been by people who already have jobs.

Weekly Jobless Claims plunged to 488,000, one of the sharpest drops on record at 100,000. Go down any Main Street today and instead of a sea of plywood, it is plastered with “Help Wanted” signs. Productivity is soaring, while average labor costs are actually falling.

ADP Private Employment Report soars, up by 742,000 in April, the biggest gain since September. It makes the coming Friday Nonfarm Payroll Report look outstanding. The jobs market is booming, but competition for the top jobs is also fierce.

Europe’s Q1 GDP falls by 0.6%. That’s better than expected, but disastrous when compared to America’s spectacular 6.4% print. Blame the bumbled slow-motion vaccine rollout. European governments wasted time negotiating on price like it was just another government program, while the US poured billions into vaccine makers, no questions asked. European vaccines, like Astra Zeneca’s, were flawed. It’s amazing that a big government continent can’t perform a big government task, even when millions of lives depend on it.

US Factory Orders gain, up 1.1% in March, providing more evidence that stimulus is working. Most economists are expecting double-digit growth in Q2. Driving up to Lake Tahoe, the number of trucks on the road has doubled in the last month.

Personal Income Explodes, up 21.1% in March, the most since 1945 according to the Bureau of Economic Analysis. What the heck happened in 1945? $1,400 stimulus checks are clearly burning holes in the pockets of consumers. Expect all numbers to hit lifetime highs in the coming months. The sun, moon, and stars are all lining up and standard of living is soaring.

Chicago PMI rockets to a 40-year high, up to 72.1 versus an expected 65. It seems everyone is already trying to buy what I am trying to buy. My bet is that the stock market is wildly underestimating the coming onslaught of economic numbers and will go to new highs once it figures out the game.

Lumber Prices are becoming a big deal, soaring 70% in two months and a staggering 340% in a year, igniting inflation fears. It’s only a tiny fraction of our tiny spending but is adding $36,000 to the cost of a new home. Someone in four homes sold today are newly built, the highest ratio ever. Punitive Trump lumber tariffs against Canada years ago shut down a lot of production and now that we need it, it isn’t there.

IBM brings out the 2-Nanometer Chip, taking semiconductor technology to the next evolutionary level. Any smaller and electrons will be too big to squeeze through the gates. The current battle is over 7 nm technology. It promises to bring much faster computing at a lower price and will act as a temporary bridge to lightening quantum computing.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 2.38% gain during the first week of May on the heels of a spectacular 15.67% profit in April.

I took profits in my long in Goldman Sachs (GS) and my short in the United States Treasury Bond Fund (TLT). I then plowed the cash into a new June short position in the (TLT) and a new short in the S&P 500 (SPY). That gave me a heart attack on my bond shorts when bond prices soared and then an immediate rebirth when they collapsed two points in the afternoon.

That leaves me 100% invested, as I have been for the last six months.

My 2021 year-to-date performance soared to 62.14%. The Dow Average is up 14.45% so far in 2021.

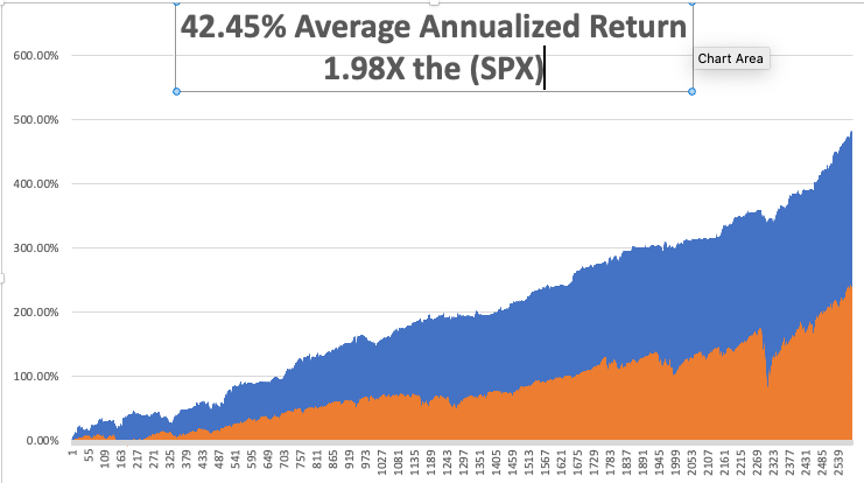

That brings my 11-year total return to 484.89%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.45%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 127.09%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 32.7 million and deaths topping 581,000, which you can find here. New cases are in free fall, with only 12 here in Washoe County Nevada out of a population of 500,000. We could approach zero by the summer.

The coming week will be weak on the data front.

On Monday, May 10, at 9:45 AM, the April ISM New York Index is out. Roblox (RBLX) and BioNTech (BNTX) report earnings.

On Tuesday, May 11, at 10:00 AM, the NFIB Small Business Optimism Index for April is released. Palantir reports results (PLTR).

On Wednesday, May 12 at 2:00 PM, the US Core Inflation Rate for April is published. Softbank (SFTBY) reports results.

On Thursday, May 13 at 8:30 AM, the Weekly Jobless Claims are published. Walt Disney (DIS), Airbnb (ABNB), and Alibaba (BABA) report results.

On Friday, May 14 at 8:30 AM, Retail Sales for April are indicated. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I’ve found a new series on Amazon Prime called Yellowstone. It is definitely NOT PG-rated, nor is it for the faint of heart. But it does remind me of my own cowboy days.

When General Custer was slaugherted during his last stand in Montana at the Little Big Horn in 1876, my ancestors spotted a great buying opportunity. They used the ensuing panic to pick up 50,000 acres near the Wyoming border for ten cents an acre.

Growing up as the oldest of seven kids, my parents never missed an opportunity to farm me out with relatives. That’s how I ended up with my cousins near Broadus, Montana for the summer of 1967.

When I got off the Greyhound bus in nearby Sheridan, I went into a bar to call my uncle. The bartender asked his name and when I told him “Carlat” he gave me a strange look.

It turned out that My uncle killed someone in a gunfight in the street out front a few months earlier, which was later ruled self-defense. It was the last public gunfight seen in the state, and my uncle hadn’t been seen in town since.

I was later picked up in a beat-up Ford truck and driven for two hours down a dirt road to a log cabin. There was no electricity, just kerosene lanterns and a propane-powered refrigerator.

Welcome to the 19th century!

I was hired on as a cowboy, lived in a bunkhouse with the rest of the ranch hands, and was paid the princely sum of a dollar an hour. I became popular by reading the other cowboys' newspapers and their mail since they were all illiterate. Every three days, we slaughtered a cow to feed everyone on the ranch. I ate steak for breakfast, lunch, and dinner.

On weekends, my cousins and I searched for Indian arrowheads on horseback, which we found by the shoebox full. Occasionally, we got lucky finding an old rusted Winchester or Colt revolver just lying out on the range, a remnant of the famous battle 90 years before. I carried my own six-shooter to help reduce the local rattlesnake population.

I really learned the meaning of work and had callouses on my hands in no time. I had to rescue cows trapped in the mud (stick a burr under their tail), round up lost ones, and saw miles of fence posts. When it came time to artificially inseminate the cows with superior semen from Scotland, it was my job to hold them still. It was all heady stuff for a 16-year-old.

The highlight of the summer was participating in the Sheridan Rodeo. With my uncle, one of the largest cattle owners in the area, I had my pick of events. So, I ended up racing a chariot made from an old oil drum, team roping (I had to pull the cow down to the ground), and riding a Brahma bull. I still have a scar on my left elbow from where a bull slashed me, the horn pigment clearly visible.

I hated to leave when I had to go home and back to school. But I did hear that the winter in Montana is pretty tough.

It was later discovered that the entire 50,000 acres was sitting on a giant coal seam 50 feet thick. You just knocked off the topsoil and backed up the truck. My cousins became millionaires. They built a modern four-bedroom house closer to town with every amenity, even a big screen TV. My cousin built a massive vintage car collection.

During the 2000s, their well water was poisoned by a neighbor’s fracking for natural gas, and water had to be hauled in by truck at great expense. In the end, my cousin was killed when the engine of the classic car he was restoring fell on top of him when the rafter above him snapped.

It all did give me a window into a lifestyle that was then fading fast. It’s an experience I’ll never forget.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 26, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE CORRECTION IS OVER)

(PAVE), (NFLX), (AAPL), (AMD), (NVDA), (ROKU), (AAPL), (AMZN), (MSFT), (FB), (GOOGL), (TSLA), (KSU), (CP), (GS), (UNP) (LEN), (KBH), (PHM)

This is a classic example of if it looks like a duck and quacks like a duck, it’s definitely not a duck….it’s a giraffe.

In stock market parlance, that means we have just suffered an eight-month correction which is now over. Look at the charts and a correction is nowhere to be found. The largest pullback we have seen in the past year has been a scant 12% dip right before the presidential election.

If that’s all the pain we have to suffer to be rewarded with an 80% gain, I’ll take that all day long.

Instead, what we have seen has been a series of sector-specific rolling corrections that were masked by the indexes that were steadily grinding up.

During this time, the best quality stocks endured pretty dramatic hits, like Netflix (NFLX) (-21%), Apple (AAPL) (-26%), Advanced Micro Devices (AMD) (-25%), NVIDIA (NVDA) (-28%), and Roku (ROKU) (-40%).

Stocks sold off hard after Q1 earnings. They are doing the same now with Q2 earnings. That ends on Tuesday after the close when the 800-pound gorilla of them all announces on Wednesday, April 28.

After that, we could be in for another leg in the bull market that could take us up by 10% by the summer.

Some 85% of all companies are now beating forecasts handily. But half are seeing shares fall after the announcement. That shows how professional the market is getting. So, if you eliminate the earnings announcement, you eliminate the share falls?

This is all in the face of economic growth predictions of lifetime proportions. Analysts are now looking for 43% earnings growth in Q2, 55% in Q3, and 75% in Q4. These are WWII-type numbers.

And the Fed put is still good at the bank. Jerome Powell is promising no rate rises until 2023 on an almost daily basis.

It all sets up a continuing pattern of sideways “time” corrections like we’ve just seen followed by frenetic legs up to new highs. This could go on for years.

It worked last time.

The coming week should be quite a blockbuster. It is only the fifth time in history that the five largest stocks in the S&P 500 accounting for 25% of the market cap all report in the same week. These are Apple (AAPL), Amazon (AMZN), Microsoft (MSFT), Facebook (FB), and Alphabet (GOOGL).

That’s going to leave a mark! Biden’s rumored proposal that high-end earners will see doubled capital gains taxes knocked 500 points of the Dow in seconds. The new tax would apply to Americans earning a net income of $1 million or more. Never mind that congress would have to approve the move first, as Trump found out to his chagrin. It’s a trial balloon that was shot down immediately. Trump had planned to cut capital gains to a 15% rate and run a bigger deficit.

It would only apply to Americans who own stocks and never sell. Guess why? To avoid taxes, dummy!

US Stock Funds take in a record $157 billion in March. That beats the record $144 billion that came in during February. Warning: these massive cash flows are consistent with short-term market tops. Vanguard and iShares index funds took in far and away the most money. The Global X US Infrastructure Fund (PAVE) was one of the most popular directed funds.

The labor shortage is on, with companies engaging in mass hiring and paying signing bonuses for low-end jobs. I was awoken by workers putting up a fence next door on a Saturday morning. They’re working weekends to pay back the debts they ran up last year to keep eating. If you are planning any jobs this year, buy the materials now. The country will be out of everything in three months, with current quarter GDP topping a historic 10%.

SPACS have crashed, with the average SPAC down 23% since the February top, and some like Virgin Galactic Holdings off by 50%. Don’t touch these things with a ten-foot pole, as 80% will go under or shut down with no investments. It reminds me of five online pet food companies at the Dotcom Bubble top. It's all a symptom of too much cash flooding the financial system.

Takeover battle for Kansas City Southern (KSU) ensues, with Canadian Nation making a sweeter $33.7 billion offer than Canadian Pacific’s (CP) $30 billion bid. It just shows how valuable railroads really are in a booming economy that urgently needs to move a lot of stuff. Good thing I’m long (UNP). Is the Reading Railroad still available? How about the B&O or the Short Line?

Yellen sets Zero Emissions Target for 2035. That sets up one of the biggest investment opportunities of the century. The trick is to find companies that have viable technologies that can make a stand-alone profit that haven’t already gone up ten times, like Tesla (TSLA). Most of the new EV IPOs aren’t going to make it. This will be a major focus of Mad Hedge research going forward. I hope I live that long!

Existing Home Sales down 12.3% YOY, down 3.7% in March, to 6.03 million units. Prices are up 17.02% YOY, the highest on record. Sales of homes over $1 million are up 108%. Inventory is still the issue, down to only 1.07 million units, off 28% in a year. Truly stunning numbers.

New Home Sales up a ballistic 20.7% YOY in March on a signed contracts basis. This is in the face of rising home mortgage interest rates. The flight to the suburbs continues. Homebuilder stocks took off like a scalded chimp. Buy (LEN), (KBH), and (PHM) on dips.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 9.48% gain during the first half of April on the heels of a spectacular 20.60% profit in March.

I used the dip early in the week to add two more positions in Goldman Sachs (GS) and Union Pacific (UNP). I suffered a day of buyer’s remorse on Thursday when Biden floated his capital gains plan and tanked the Dow by 500 points. Then everything took off like a rocket to new highs on Friday.

That leaves me 80% invested and 20% in cash. The markets went up too fast to get the last match of money in the market.

My 2021 year-to-date performance soared to 53.57%. The Dow Average is up 12.3% so far in 2021.

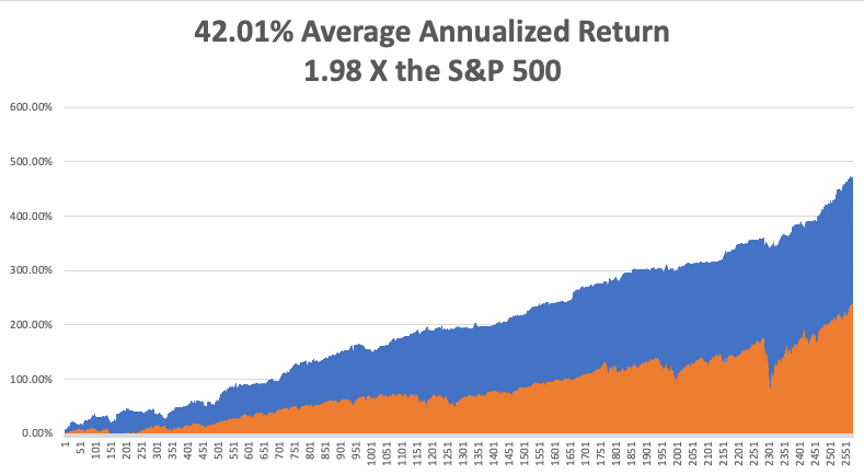

That brings my 11-year total return to 476.12%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.01%, the highest in the industry.

My trailing one-year return exploded to positively eye-popping 132.09%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 31.9 million and deaths topping 570,000, which you can find here.

The coming week will be big on the data front, with a couple of historic numbers expected.

On Monday, April 26, at 8:30 AM, US Durable Goods for March are out. Earnings for Tesla (TSLA) and NXP Semiconductors (NXP) are out.

On Tuesday, April 27, at 9:00 AM, we learn the S&P Case Shiller National Home Price Index for February. We also get earnings for Alphabet (GOOGL), Microsoft (MSFT), and Visa (V).

On Wednesday, April 28 at 2:00 PM, The Fed Open Market Committee releases its Interest Rates Decision. The following press conference is more important. Apple (AAPL), Boeing (BA), and QUALCOMM (QCOM) earnings are out.

On Thursday, April 29 at 8:30 AM, the Weekly Jobless Claims are printed. We also obtain the blockbuster US GDP for Q1. Amazon (AMZN), Caterpillar (CAT, and Merck (MRK) release earnings.

On Friday, April 30 at 8:30 AM, we get US Personal Income and Spending for March. Exxon Mobile (XOM) and Chevron (CVX) release earnings. Berkshire Hathaway (BRK/B) announces the next day. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, after telling you last week why I walked so funny, let me tell you the other reason.

In 1987, to celebrate obtaining my British commercial pilot’s license, I decided to fly a tiny single-engine Grumman Tiger from London to Malta and back.

It turned out to be a one-way trip.

Flying over the many French medieval castles was divine. Flying the length of the Italian coast at 500 feet was fabulous, except for the engine failure over the American airbase at Naples.

But I was a US citizen, wore a New York Yankees baseball cap, and seemed an alright guy, so the Air Force fixed me up for free and sent me on my way. Fortunately, I spotted the heavy cable connecting Sicily with the mainland well in advance.

I had trouble finding Malta and was running low on fuel. So I tuned into a local radio station and homed in on that.

It was on the way home that the trouble started.

I stopped by Palermo in Sicily to see where my grandfather came from and to search for the caves where my great-grandmother lived during the waning days of WWII. Little did I know that Palermo was the worst wind shear airport in Europe.

My next leg home took me over 200 miles of the Mediterranean to Sardinia.

I got about 50 feet into the air when a 70-knot gust of wind flipped me on my side perpendicular to the runway and aimed me right at an Alitalia passenger jet with 100 passengers awaiting takeoff. I managed to level the plane right before I hit the ground.

I heard the British pilot say on the air “Well, that was interesting.”

Giant fire engines descended upon me, but I was fine, sitting on my cockpit, admiring the tree that had suddenly sprouted through my port wing.

Then the Carabinieri arrested me for endangering the lives of 100 Italian tourists. Two days later, the Ente Nazionale per l’Avizione Civile held a hearing and found me innocent, as the wind shear could not be foreseen. I think they really liked my hat, as most probably had distant relatives in New York.

As for the plane, the wreckage was sent back to England by insurance syndicate Lloyds of London, where it was disassembled. Inside the starboard wing tank, they found a rag which the American mechanics in Naples had left by accident.

If I had continued my flight, the rag would have settled over my fuel intake vavle, cut off my gas supply, and I would have crashed into the sea and disappeared forever. Ironically, it would have been close to where French author Antoine de St.-Exupery (The Little Prince) crashed in 1945.

In the end, the crash only cost me a disk in my back, which I had removed in London and led to my funny walk.

Sometimes, it is better to be lucky than smart.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Antoine de St.-Exupery on the Old 50 Franc Note

Global Market Comments

April 1, 2021

Fiat Lux

Featured Trade:

(MARCH 31 BIWEEKLY STRATEGY WEBINAR Q&A),

(FB), (ZM), ($INDU), (X), (NUE), (WPM), (GLD), (SLV), (KMI), (TLT), (TBT), (BA), (SQ), (PYPL), (JNP), (CP), (UNP), (TSLA), (GS), (GM), (F)

Below please find subscribers’ Q&A for the March 31 Mad Hedge Fund Trader Global Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Would you buy Facebook (FB) or Zoom (ZM) right here?

A: Well, Zoom was kind of a one-hit wonder; it went up 12 times on the pandemic as we moved to a Zoom economy, and while Zoom will permanently remain a part of our life, you’re not going to get that kind of growth in stock prices in the future. Facebook on the other hand is going to new highs, they just announced they’re laying a new fiber optic cable to Asia to handle a 70% increase in traffic there. So, for the longer term and buying here, I think you get a new high on Facebook soon; there's maybe another 20-30% move in Facebook this year.

Q: I can’t really chase these trades here, right?

A: Correct; if you wait any more than a day or 2 on executing a trade alert, you’re missing out on all of the market timing value we bring to the game. So that's why I include an entry price and the “don’t pay more than” price. And we never like to chase, except last year, when we did it almost all the time. But last year was a chase market, this year not so much.

Q: How are LEAP purchase notifications transmitted?

A: Those go out in the daily newsletter Global Trading Dispatch when I see a rare entry point for a LEAP, then we’ll send out a piece and notify everybody. But it’s very unusual to get those. Of course, a year ago we were sending out lists of LEAPS ten at a time when the Dow Average ($INDU) is at 18,000. But that is not now, you only wait for those once or twice a year. On huge selloffs to get into two-year-long options trades, and that is definitely not now. The only other place I've been looking out for LEAPS right now are really bombed out technology stocks begging for a rotation. Concierge members get more input on LEAPS and that is a $10,000 a year upgrade.

Q: What are your thoughts on silver (SLV) and long-term gold (GLD)?

A: I see silver going to $50 and eventually $100 in this economic cycle, but it's out of favor right now because of rising interest rates. So, once we hit 2.00% in the ten years, it’s not only off to the races for tech but also gold and silver. Watch that carefully because your entry point may be on the horizon. That makes Wheaton Precious Metals (WPM) a very attractive “BUY” right now.

Q: Are you going to trade the (TLT)?

A: Absolutely yes, but I’m kind of getting picky now that I’m up 42% on the year; and I only like to sell 5-point rallies, which we got for about 15 minutes last week. And I also only like to buy 5- or 10-point dips. Keep your trading discipline and you’ll make a ton of money in this market. Last year we made about 30% trading bonds on about 30 round trips.

Q: How much further upside is there for US Steel (X) and Nucor Corp. (NUE)?

A: More. There's no way you do infrastructure without using millions of tons of steel. And I kind of missed the bottom on US Steel because it had been a short for so long that it kind of dropped off the radar for me. I think we have gone from $4 to 27 since last year, but I think it goes higher. It turns out the US has been shutting down steel production for decades because it couldn't compete with China or Japan, and now all of a sudden, we need steel, and we don’t even make the right kind of steel to build bridges or subways anymore—that has to be imported. So, most of the steel industry here now is working for the car industry, which produces cold-rolled steel for the car body panels. Even that disappears fairly soon as that gets taken over by carbon fiber. So enough about steel, buy the dips on (X) and (NUE).

Q: What stocks should I consider for the infrastructure project?

A: Well, US Steel (X) and Nucor Corp (NUE) would be good choices; but really you can buy anything because the infrastructure package, the way it’s been designed, is to benefit the entire economy, not just the bridge and freeway part of it. Some of it is for charging stations and electric car subsidies. Other parts are for rural broadband, which is great for chip stocks. There is even money to cap abandoned oil wells to rope in Texas supporters. All of this is going to require a massive upgrade of the power grid, which will generate lots of blue-collar jobs. Really everybody benefits, which is how they get it through Congress. No Congressperson will want to vote against a new bridge or freeway for their district. That’s always the case in Washington, which is why it will take several months to get this through congress because so many thousands of deals need to be cut. I’ve been in Washington when they’ve done these things, and the amount of horse-trading that goes on is incredible.

Q: Is it a good thing that I’ve had the United States Treasury Bond Fund (TLT) LEAPS $125 puts for a long time.

A: Yes. Good for you, you read my research. Remember, the (TLT) low in this economic cycle is probably around $80, so you probably want to keep rolling forward your position….and double up on any ten-point rally.

Q: Do you think we get a pop back up?

A: We do but from a lower level. I think any rallies in the bond market are going to be extremely limited until we hit the 2.00%, and then you’re going to get an absolute rip-your-face-off rally to clean out all the short term shorts. If you're running put LEAPS on the (TLT) I would hang on, it’s going to pay off big time eventually.

Q: If we see 3.00% on the 10-year this year, do you see the stock market crashing?

A: I don’t think we’ll hit 3.00% until well into next year, but when we do, that will be time for a good 10% stock market correction. Then everyone will look around again and say, “wow nothing happened,” and that will take the market to new highs again; that's usually the way it plays out. Remember, then year yields topped all the way up at 5.00% when the Dotcom Bubble topped in April 2020.

Q: Has the airline hospitality industry already priced in the reopening of travel?

A: No, I think they priced in the hope of a reopening, but that hasn’t actually happened yet, and on these giant recovery plays there are two legs: the “hope for it” leg, which has already happened, and then the actual “happening” leg which is still ahead of us. There you can get another double in these stocks. When they actually reopen international travel to Europe and Asia, which may not happen this year, the only reopening we’re going to see in the airline business is in North America. That means there is more to go in the stock price. Also coming back from the brink of death on their financial reports will be an additional positive.

Q: Do you think a corporate tax increase will drive companies out of the US again and raise the unemployment rate?

A: Absolutely not. First of all, more than half of the S&P 500 don’t even pay taxes, so they’re not going anywhere. Second, I think they will make these offshoring moves to tax-free domiciles like Ireland illegal and bring a lot of tax revenues back to the US. And third, all Biden is doing is returning the tax rate to where it was in 2017; and while the corporate tax rate was 35%, the stock market went up 400% during the Obama administration, if you recall. So stocks aren't really that sensitive to their tax rates, at least not in the last 50 years that I’ve been watching. I'm not worried at all. And Biden was up on the polls a year ago talking about a 28% tax rate; and since then, the stock market has nearly doubled. The word has been out for a year and priced in for a year, and I don't think anybody cares.

Q: What about quantum computers?

A: I’m following this very closely, it’s the next major generation for technology. Quantum computers will allow a trillion-fold improvement in computing power at zero cost. And when there's a stock play, I will do it; but unfortunately, it’s not (IBM), because we’re not at the money-making stage on these yet. We are still at the deep research stage. The big beneficiaries now are Alphabet (GOOGL), Microsoft (MSFT), and Amazon (AMZN).

Q: Is it time to buy Chinese stocks?

A: I would say yes. I would start dipping in here, especially on the quality names like Tencent (TME), Baidu (BIDU), and Alibaba (BABA), because they’ve just been trashed. A lot of the selloff was hedge fund-driven which has now gone bust, and I think relations with China improve under Biden.

Q: Your timing on Tesla (TSLA) has been impeccable; what do you look for in times of pivots?

A: Tesla trades like no other stock, I have actually lost money on a couple of Tesla trades. You have to wait for things to go to extremes, and then wait two more days. That seems to be the magic formula. On the first big selloff go take a long nap and when you wake up, the temptation to buy it will have gone away. It always goes up higher than you expect, and down lower than you expect. But because the implied volatilities go anywhere from 70% to 100%, you can go like 200 points out of the money on a 3-week view and still make good money every month. And that’s exactly what we’re going to do for the rest of the year, as long as the trading’s down here in the $500-$600 range.

Q: Is Editas Medicine (EDIT), a DNA editing stock, still good?

A: Buy both (EDIT) and Crisper (CRSP); they both look great down here with an easy double ahead. This is a great long-term investment play with gene editing about to dominate the medical field. If you want to learn more about (EDIT) and (CRSP) and many others like them, subscribe to the Mad Hedge Fund Biotech & Healthcare Letter because we cover this stuff multiple times a week (click here).

Q: Is the XME Metals ETF a buy?

A: I would say yes, but I'd wait for a bigger dip. It’s already gone up like 10X in a year, but the outlook for the economy looks fantastic. (XME) has to double from here just to get to the old 2008 high and we have A LOT more stimulus this time around.

Q: What about hydrogen?

A: Sorry, I am just not a believer in hydrogen. You have to find someone else to be bullish on hydrogen because it’s not me. I've been following the technology for 50 years and all I can say is: go do an image Google for the name “Hindenburg” and tell me if you want to buy hydrogen. Electricity is exponentially scalable, but Hydrogen is analog and has to be moved around in trucks that can tip over and blow up at any time. Hydrogen batteries are nowhere near economic. We are now on the eve of solid-state lithium-ion batteries which improve battery densities 20X, dropping Tesla battery weights from 1,200 points to 60 pounds. So “NO” on hydrogen. Am I clear?

Q: Why do you do deep-in-the-money call and put spreads?

A: We do these because they make money whether the stock goes up down or sideways, we can do them on a monthly basis, we can do them on volatility spikes, and make double the money you normally do. The day-to-day volatility on these positions is very low, so people following a newsletter don’t get these huge selloffs and sell at bottoms, which is the number one source of retail investor losses. After 13 years of trade alerts, I have delivered a 40.30% average annualized return with a quarter of the market volatility. Most people will take that.

Q: Is ProShares Ultra Short 20 Year Plus Treasury ETF(TBT) still a play for the intermediate term?

A: I would say yes. If ten-year US Treasury bonds Yields soar from 1.75% to 5.00% the (TBT) should rise from $21 to $100 because it is a 2X short on bonds. That sounds like a win for me, as long as you can take short term pain.

Q: What is the timing to buy TLT LEAPS?

A: The answer was in January when we were in the $155-162 range for the (TLT). Down here I would be reluctant to do LEAPS on the TLT because we’ve already had a $25 point drop this year, and a drop of $48 from $180 high in a year. So LEAP territory was a year ago but now I wouldn’t be going for giant leveraged trades. That train has left the station. That ship has sailed. And I can’t think of a third Metaphone for being too late.

Q: Would you buy Kinder Morgan (KMI) here?

A: That’s an oil exploration infrastructure company. No, all the oil plays were a year ago, and even six months ago you could have bought them. But remember, in oil you’re assuming you can get in and out before it crashes again, it’s just a matter of time before it does. I can do that but most of you probably can’t, unless you sit in front of your screens all day. You’re betting against the long-term trend. It works if you’re a hedge fund trader, not so much if you are a long-term investor. Never bet against the long-term trend and you always have a tailwind behind you. All surprises work to your benefit.

Q: If you get a head and shoulders top on bitcoin, how far does it fall?

A: How about zero? 80% is the traditional selloff amount for Bitcoin. So, the thing is: if bitcoin falls you have to worry about all other investments that have attracted speculative interest, which is essentially everything these days. You also have to worry about Square (SQ), PayPal (PYPL), and Tesla (TSLA), which have started processing Bitcoin transactions. Bitcoin risk is spread all over the economy right now. Those who rode the bandwagon up will ride it back down.

Q: Is Boeing (BA) a long-term buy?

A: Yes, especially because the 737 Max is back up in the air and China is back in the market as a huge buyer of U.S. products after a four-year vacation. Airlines are on the verge of seeing a huge plane shortage.

Q: What about Ags?

A: We quit covering years ago because they’re in permanent long-term downtrends and very hard to play. US farmers are just too good at their jobs. Efficiencies have double or tripled in 60 years. Ag prices are in a secular 150-year bear market thanks to technology.

Q: Is this recorded to watch later?

A: Yes, it goes on our website in about two hours. For directions on where to find it, log in to your www.madhedgefundrader.com account, go to “My Account,” and it will be listed under there, as are all the recorded webinars of the last 12 years.

Q: Would you buy Canadian Pacific (CP) here, the railroad?

A: No, that news is in the price. Go buy the other ones—Union Pacific (UNP) especially.

Q: What are your thoughts on Bitcoin?

A: We don’t cover Bitcoin because I think the whole thing is a Ponzi scheme, but who am I to say. There is almost ten times more research and newsletters out there on Bitcoin as there is on stock trading right now. They seem to be growing like mushrooms after a spring storm. There are always a lot of exports out there at market tops, as we saw with gold in 2010 and tech stock in 2000.

Q: What do you think about Juniper Networks (JNP)?

A: It’s a Screaming “BUY” right here with a double ahead of it in two years. I’m just waiting for the tech rotation to get going. This is a long-term accumulate on dips and selloffs.

Q: Did the Archagos Investments hedge fund blow threaten systemic risk?

A: No, it seems to be limited just to this one hedge fund and just to the people who lent to it. You can bet banks are paring back lending to the hedge fund industry like crazy right now to protect their earnings. I don’t think it gets to the systemic point, but this is the Long Term Capital Management for our generation. I was involved in the unwind of the last LTCM capital, which was 23 years ago. I was one of the handful of people who understood what these people were even doing. So, they had to bring me in on the unwind and huge fortunes were made on that blowup by a lot of different parties, one of which was Goldman Sachs (GS). I can tell you now that the statute of limitations has run out and now that it's unlikely I'll ever get a job there, but Goldman made a killing on long-term capital, for sure.

Q: Will Tesla benefit from the Biden infrastructure plan?

A: I would say Tesla is at the top of the list of companies the Biden administration wants to encourage. That means more charging stations and more roads, which you need to drive cars on, and bridges, and more tax subsidies for purchases of new electric cars. It’s good not just Tesla but everybody’s, now that GM (GM) and Ford (F) are finally starting to gear up big numbers of EVs of their own. By the way, I don't see any of the new startups ever posing a threat to Tesla. The only possible threats would be General Motors, Ford, and Volkswagen, which are all ten years behind.

Q: Would you put 10% of your retirement fund into cryptocurrencies?

A: Better to flush it down the toilet because there’s no commission on doing that.

Q: Is growing debt a threat to the economy? How much more can the government borrow?

A: It appears a lot more, because Biden has already indicated he’s going to spend ten trillion dollars this year, and the bond market is at a 1.70%—it’s incredibly low. I think as long as the Fed keeps overnight rates at near-zero and inflation doesn't go over 3%, that the amount the government can borrow is essentially unlimited, so why stop at $10 or $20 trillion? They will keep borrowing and keep stimulating until they see actual inflation, and I don’t think we will see that for years because inflation is being wiped out by technology improvements, as it has done for the last 40 years. The market is certainly saying we can borrow a lot more with no serious impact on the economy. But how much more nobody knows because we are in uncharted territory, or terra incognita.

To watch a replay of this webinar just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 1, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WAKE UP CALL),

(TLT), (JPM), (BAC), (C), (MS), (GS),

(JNJ), (AAPL), (FB), (AMZN), (GOOGL)

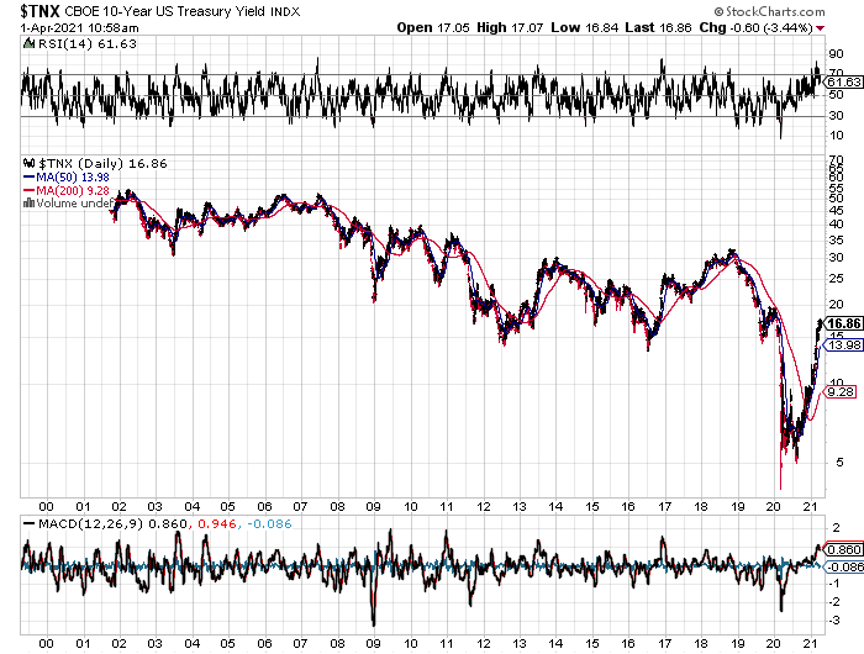

This was the week the stock traders learned there was such a thing as a bond market. They know this because it was bonds that completely demolished their stock trading books.

Suddenly, markets went from zero offered to zero bid. Many strategists labored under the erroneous assumption that ten-year US Treasury yields would never surpass 1.50% in 2021. Yet, here we are only in March and it’s already topped 1.61%. It’s become the one-way trade of the year.

The bond market seems to be discounting an imminent runaway inflation rate. But at a 1.4% annual figure, it's nowhere to be seen, not with 20 million unemployed and Main Streets everywhere looking like ghost towns.

I still believe that technology is evolving so fast, hyper-accelerated by the pandemic, that it will wipe out any return of inflation. I will not believe in inflation until I see the whites of its eyes, to paraphrase Colonel William Prescott at the Battle of Bunker Hill.

Of course, it is I who has been screaming from the rooftops about the coming crash of the bond markets, since March 20. Being short the bond market has been one of my most profitable trades of 2020 AND 2021. If I am annoyed by anything, it happened too fast, depriving me several more round trips a slower crash would have permitted.

When you have to own stocks, make them financials (JPM), (BAC), (C), which benefit from rising rates. Their loan rates are rocketing while their cost of money is fixed at the Fed overnight cost of funds at 0.25%. Trading volumes at the brokers (MS), (GS) are through the roof, especially for options traders.

It is all a perfect money-making machine. At least, the stock market thinks so.

I’ll tell you something that markets are not paying attention to at all, and it is the tremendous improvement in the pandemic. Since January 20, news cases have cratered from 250,000 a day to only 70,000, down 72%. The best-case scenario which markets discounted by near doubling in 11 months is happening.

With the addition of the Johnson & Johnson (JNJ) vaccine, some 700 million doses will be available by June. We could be back to normal by summer, at least in the parts of the country that don’t believe it is still a hoax.

This breathes life into the blockbuster 7.5% GDP growth scenarios now making the rounds. I think people have no idea how hot the economy is really going to get. Labor and materials shortages may be only three months off, but with no inflation.

So, what does all this mean for the markets? It all sets up the normal 5%-10% correction that I have been predicting. If you have two-year LEAPS on your favorite names, hang on to them. We are going much higher.

I went into the Monday selloff with a rare 100% cash position. The 20% I have now in commodities I picked up on puke out, throw up on your shoe capitulation days.

The barbell is still the winning strategy.

Domestic recovery stocks have been on fire for six months, with small banks up a ballistic 80%. Big tech has gone nowhere. But their earnings are still exploding, in effect, making them 20% cheaper over the same time period.

It’s just a matter of time before markets rotate back into tech and give domestic recovery a break. Think (AAPL), (FB), (AMZN), and (GOOGL). That is where the smart money is going right now.

The bond auction was a total disaster. The US Treasury offered $62 billion worth of seven-year US Treasury bonds, double the amount a year earlier. At a 1.95% yield and no one showed. Foreign participation was the worst in seven years. The bid-to-cover ratio was pitiful. Over issuance by the government crushing the market? Who knew? Imagine how high interest rates would be if the Fed wasn’t buying $120 billion a month of bonds?

The insanity is back, with GameStop (GME) doubling in the last 15 minutes of the month. Nobody knows why. It was why stocks tanked at the close on Thursday, scaring away real investors in real stocks. (GME) has become an indicator of all that’s wrong with the market.

Copper demand is rocketing, says Freeport McMoRan (FCX) CEO Richard Adkerson. That’s why he is opening three new US mines this year, adding 250 million pounds in annual output. Biden’s ambitious EV plans are the trigger. You can’t build an EV without a lot of the red metal. The world’s largest copper producer has become a major climate change and ESG play.

NVIDIA blows it away, with sales up a blockbuster 66%. Demand from gamers locked up at home was overwhelming. Purchases by bitcoin miners were through the roof. Even demand from the auto industry was up 16%, even though card sales aren’t. Too bad they picked the wrong day to announce, with the stock off 8.2%. (NVDA) is the one tech stock I would buy on dips.

Fed says business failures will continue at record pace, mostly occurring among small, unlisted local businesses. Biden’s $1.9 trillion rescue budget will come too late for many. Unemployment could stay chronically high for years, as the Weekly Jobless Claims are suggesting.

Housing starts fell in January, down 6.0% to 1.58 million units. A much smaller drop was expected. Rising land and lumber costs are cutting into the economics of new construction. Home prices are going to have to accelerate to suck in more supply. Housing Permits for new construction soared by 10.4% last month, so the future looks bright for builders.

Tesla (TSLA) crashed, down $180 in two days. We have just suffered a perfect storm of bad news about Tesla. Interest rates have been soaring, bad for all tech in the mind of the market. Competitor Lucid Motors announced a SPAC valued at $11 billion. And Elon Musk said Bitcoin looked “high” after investing $1.5 billion. Get ready to buy the dip, but not yet.

Quantitative easing to continue, says Fed governor Jay Powell, even if the economy improves. The $120 billion in bond-buying remains, even if the economy improves. He’s doing everything possible to create inflation.

Panic hits the crypto markets, dragging down technology equities with them. The two have been trading 1:1 for four months. Bitcoin suffered an eye-popping 25% plunge from $58,000 to 43,600. The tail is now wagging the dog. All risk-taking may have spiked with the Friday options expiration. Watch Bitcoin for a tech stock revival and vice versa. Stocks have earnings multiple support. Crypto doesn’t. I’ll buy Bitcoin when they post a customer support number.

Australian dollars soars as predicted, from $58 to $79 in 11 months. We could hit parity in 2022. The Aussie is basically a call option on a synchronized global economic recovery. End of the pandemic will also bring a resumption of massive Chinese investment in the Land Down Under. Keep buying the dips in (FXA).

Case-Shiller explodes to the upside, up 10.4% in December. It’s the hottest read in seven years for the National Home Price Index. Phoenix (14.4%), San Diego (13.0%), and Seattle (13.6%) were the strongest cities. The flight from the cities continues.

(TLT) breaks $138, surpassing my end 2021 target of a 1.50% ten-year US Treasury yield. So, I lied. My new yearend target is now $120, which would take ten-year yields to 2.00%. With a $1.9 trillion rescue budget about to kick in after the $900 billion that passed in December, the economy and demand for funds are about to rocket. Better hurry up and buy that house before mortgage rates rise out of reach.

Weekly Jobless Claims sink to 730,000. I can’t believe that 730,000 is now considered a good number, compared to 50,000 a year ago.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch closed out with a 13.28% profit in February after a blockbuster 10.21% in January. The Dow Average is up a miniscule 1.1% so far in 2021.

This is my fourth double-digit month in a row. My 2021 year-to-date performance soared to 23.49%. After the February 19 option expiration, I am now 80% in cash, with longs in (XME) and (FCX).

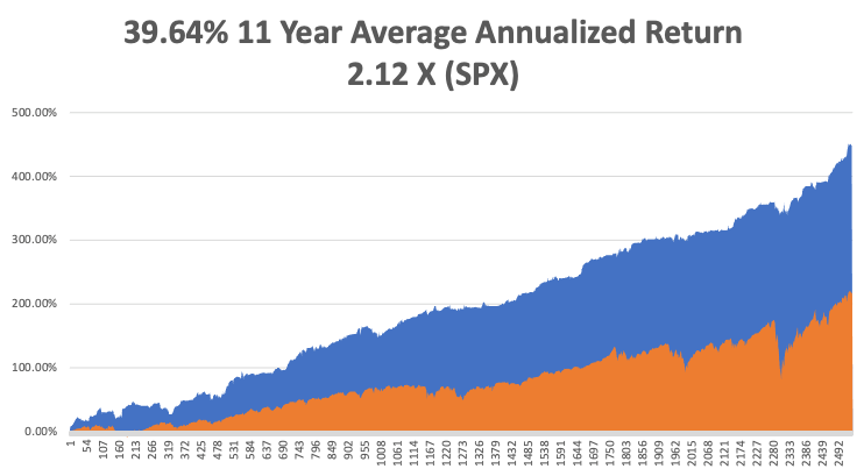

That brings my 11-year total return to 446.04%, some 2.12 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 39.64%.

My trailing one-year return exploded to 93.48%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 103.31% since the March 20, 2020 low.

We need to keep an eye on the number of US Coronavirus cases at 28 million and deaths topping 510,000, which you can find here.

The coming week will be a boring one on the data front.

On Monday, March 1, at 10:00 AM EST, the ISM Manufacturing Index is out. Zoom (ZM) reports.

On Tuesday, March 2, at 9:00 AM, Total US Vehicle Sales for February are announced. Target (TGT) and Hewlett Packard (HPQ) report.

On Wednesday, March 3 at 8:15 AM, the ADP Private Employment Report is released. Snowflake (SNOW) reports.

On Thursday, March 4 at 9:30 AM, Weekly Jobless Claims are printed. Broadcom (AVG) and Costco (CSCO) report.

On Friday, March 5 at 8:30 AM, The February Nonfarm Payroll Report is announced. Big Lots (BIG) reports. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, the deed is done, I got my first Covid-19 shot, pure Pfizer.

The Marine Corps failed to deliver, as only active duty are getting shots. Washoe County ran out. Incline Village said I couldn’t get a shot until July. My own doctor had no clue.

Then I got an automated call from the doctor who did my stem cell treatment on my knees five years ago. They belonged to a large group that had my birthday in their system and my number came up on the first day the under ’70s opened up.

Going there was a celebration. Everyone was thrilled to death to get their shot. It was like winning the lottery. Our little local hospital operated with machine-like efficiency, inoculating 1,300 a day. It was a straight drive in, dive out. It was an “all hands-on deck” effort, with everyone from the board directors to the billing clerks manning the needles. It took longer to buy a Big Mac than to get my shot.

To make sure I didn’t pass out, I was sent to a holding area, where a person was assigned to each car. I got the CEO and grilled him relentlessly on his business model for 30 minutes.

I haven’t felt this good since I got my polio vaccine sugar cube in 1955.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

January 20 Infection Rate

March 3 Infection Rate

Global Market Comments

February 22, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or TIME FOR A BREAK)

(GME), (TLT), (FB), (AMZN), (AAPL), (XME), (FCX), (MS), (GS), (BLX), (KO), (AMD)