Global Market Comments

March 3, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ARMAGEDDON)

(JPM), (IBKR), (TSLA), (NVDA), (TLT), (GS), (BRK/B), (PRIV), (GLD), (FXI)

Global Market Comments

March 3, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ARMAGEDDON)

(JPM), (IBKR), (TSLA), (NVDA), (TLT), (GS), (BRK/B), (PRIV), (GLD), (FXI)

Armageddon is not a word I use lightly. But this weekend, every technical service I subscribed to warned that the recent damage to the market was immense. It’s time to raise cash, hedge your positions, or otherwise position for a bear market.

I have noticed over the past half-century that the best technicians spend a lot of time reading up on fundamentals, and the best fundamentalists spend a lot of time looking at charts. When both go to hell in a handbasket, as they are now, it’s time to head for the hills.

The only way Armageddon can be avoided, or at least postponed, is if the trade war, which is about to cut S&P 500 (SPY) earnings by half, suddenly ends. Only one person knows if that is going to happen, and he isn’t sharing any of his cards with me.

If the trade war continues or expands, the math here becomes very simple. The shares of companies that earn less money are worth less.

You learn in flight school that accidents aren’t usually the result of a single problem but several compounding ones. I know this too well because I have crashed three planes, in the Austrian Alps, in Sicily, and in Paris. First, the gyroscope blows up, then the radio goes out, and then you lose an engine when the weather turns bad. It doesn’t help when someone is shooting at you, either.

The problem for stock owners now is that there isn’t just one thing going wrong with the investment landscape right now; there are several compounding ones, like inflation, immigration, taxes, the deficit, the Ukraine War, and the end of American leadership of the West.

Loss of confidence in the top, which took a quantum leap downward in the wake of the dumpster fire at a White House Zelinski meeting, has consequences. At this point, every businessman in America is asking himself if he can survive the current regime.

With a scant one-seat majority in Congress, a budget can’t pass by March 14, when a government shutdown begins. It means that there will be no new tax cuts by year-end. Chaos ratchets up. Businessmen hate chaos.

It also means that the 2017 tax cuts extension isn’t going to happen, which adds $5 trillion in new taxes on the country just when the economy is slowing dramatically. Uncertainty runs rampant.

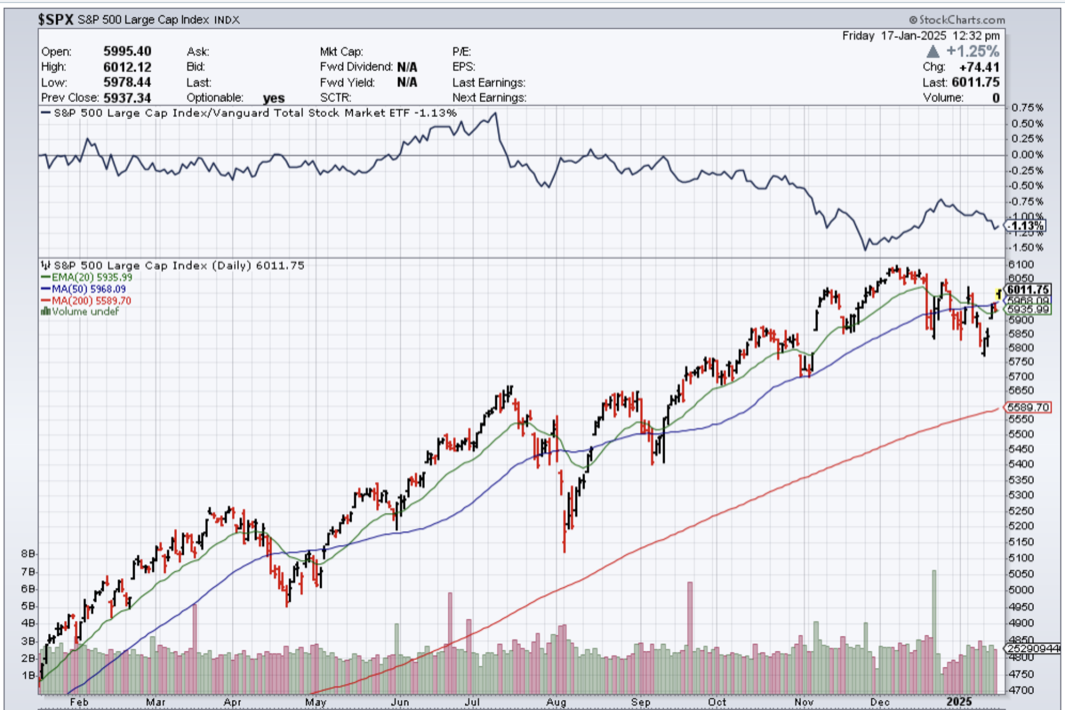

Here's the problem for investors with that. Confident markets trade at big premiums, as we saw for the last three years. Uncertain markets trade at big discounts. If I’m right, that discount will be 20%. If I’m wrong, it's 50%.

Ceding America’s leadership of the West comes at a heavy price. It started 80 years ago with the end of WWII. American stock markets have done pretty well during this time, rising by 435 times. Why anyone would want to give up such a system is beyond me.

For example, the US dollar would lose its reserve currency status. There is no way the national debt could have risen to $36 trillion, half of which was bought by foreigners, and all of which was used to stimulate the economy, without reserve currency status. Take that away, and economic growth goes elsewhere. So do higher stock prices, which we have already seen this year in China and Europe.

There is a fundamental repricing of the market taking place, and we are only just at the beginning.

About that economy thing. On Friday, the Atlanta Fed predicted that the US economy SHRANK by -1.5% in Q1. It would be easy to say, “There goes the Atlanta Fed again,” whose model is always prone to extreme predictions. But it is safe to say that the economy is either not growing or growing at a dramatically slowing rate.

The problem for investors? Reliable growing economies, which we have had since the Pandemic five years ago, support high stock multiples. Non-growing or shrinking economies can only support low earnings multiple. Remember back in 2009, the S&P 500 traded at a lowly multiple of only 9X, against today’s 25X.

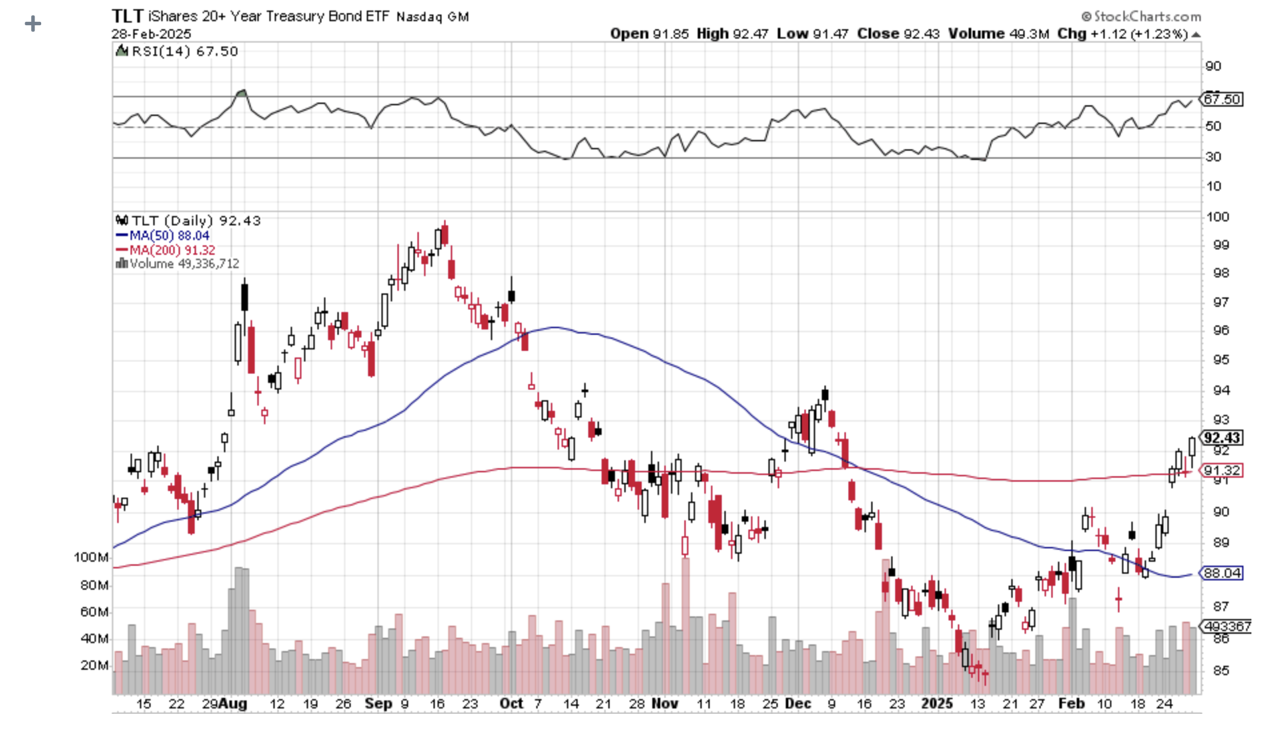

This isn’t just me howling at the moon. With a meteoric $10 rally this year, the bond market is starting to warn of a coming recession. Ten-year US Treasury bond yields have cratered from 4.80% to 4.20%. This is in the face of massive bond issuance in 2025, some $1.7 trillion worth, the product of the 2017 Trump tax cuts. Almost all new government policies are anti-economy and anti-growth.

The DOGE campaign is sucking massive amounts of money out of the economy. The yield curve has inverted, meaning that short-term interest rates are higher than long-term ones, indicating that the recession risk is real.

The dividend yield on the S&P 500 is at 1.2%. It was 2% only a couple of years ago. That is not much yield competition.

As I have been warning my Concierge members for weeks, get rid of all the stocks and asset classes you have been dating and only keep the ones you are married to. And what you keep should be hedged, such as through selling short call options against your longs, buying the (SDS), the 2X short S&P 500 ETF. And then there are 90-day US Treasury bills yield 4.2%, where nobody has ever lost money.

I learned something interesting the other day about your largest holding.

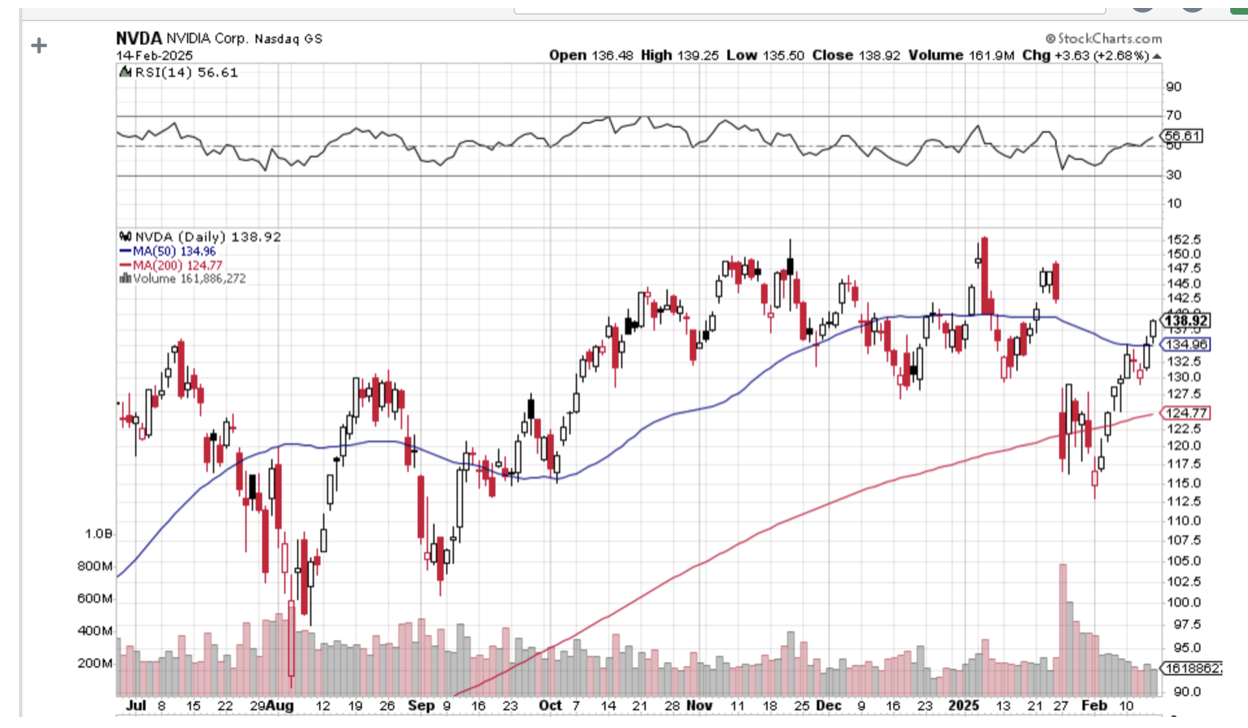

Some 70% of Nvidia is now held by indexes like the S&P 500. That’s because it has become an index proxy. It means that the shares have become an index hedge for hedge funds against which they can trade a myriad of options. This is why the (NVDA) options have implied volatilities four times those of the (SPY). It is a great arbitrage.

I watch closely the launch of new ETFs and write about the most interesting ones. I have been inundated by requests for private credit investments, which, by definition, are not available to the public.

Now, we will soon have the SPR SSGA Apollo IG Public & Privat Credit ETF (PRIV) out soon (https://www.ssga.com/us/en/intermediary/etfs/spdr-ssga-apollo-ig-public-private-credit-etf-priv ).

The fund will launch with an initial $50 million, and the minimum investment is $100,000. The fund essentially offers daily liquidity for illiquid long-duration loans. The yield should be in line with private illiquid debt, or about 10%-12%.

How they pull this off is anybody’s guess. Past funds that tried to do this closed their doors during times of economic distress, known as “gating, “so beware of gating when market conditions turn less than ideal. The fund promises to hold up to 35% of its funds in private credit and the rest in a mix of junk bonds. No word yet on the yield, but it will be much higher than the leading junk bond fund (JNK), which is offering 6.48%.

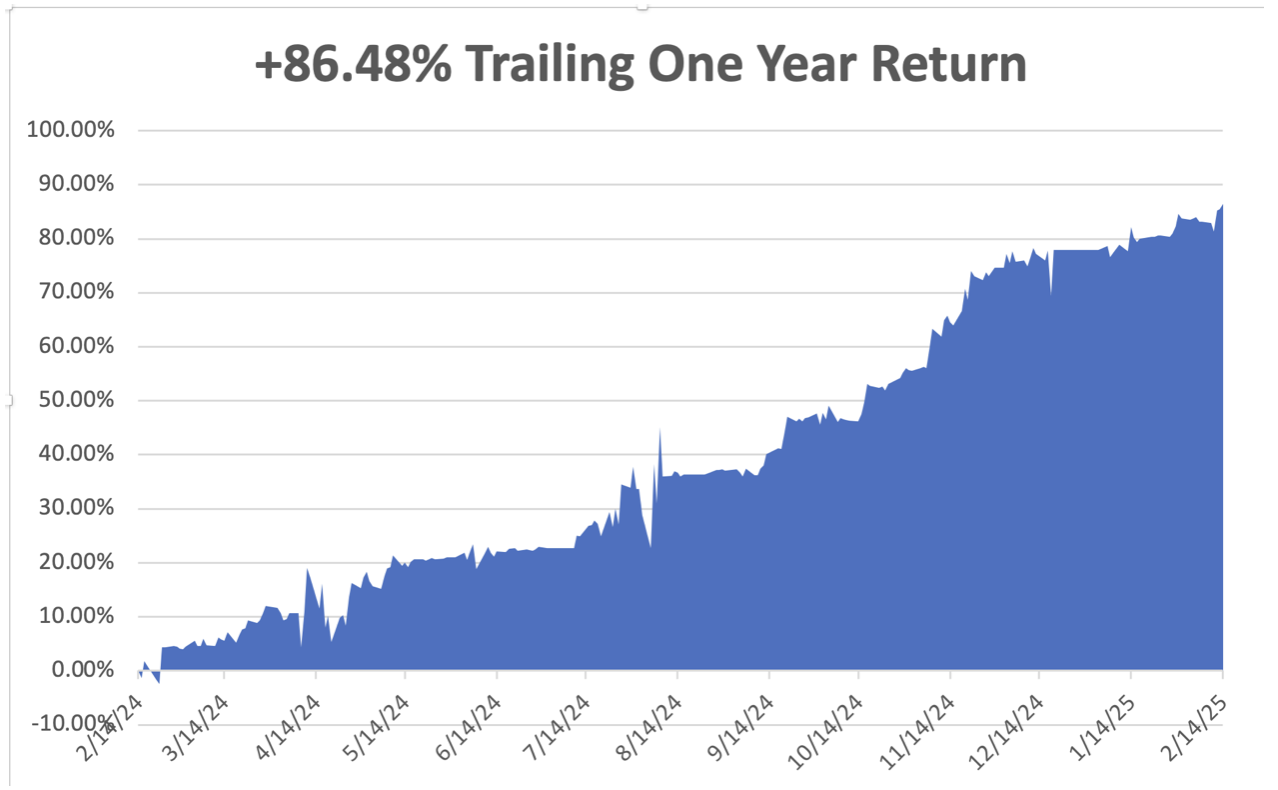

February has started with a respectable +2.25% return so far. That takes us to a year-to-date profit of +9.46% so far in 2025. My trailing one-year return stands at a spectacular +81.87% as a bad trade a year ago fell off the one-year record. That takes my average annualized return to +49.83% and my performance since inception to +761.36%.

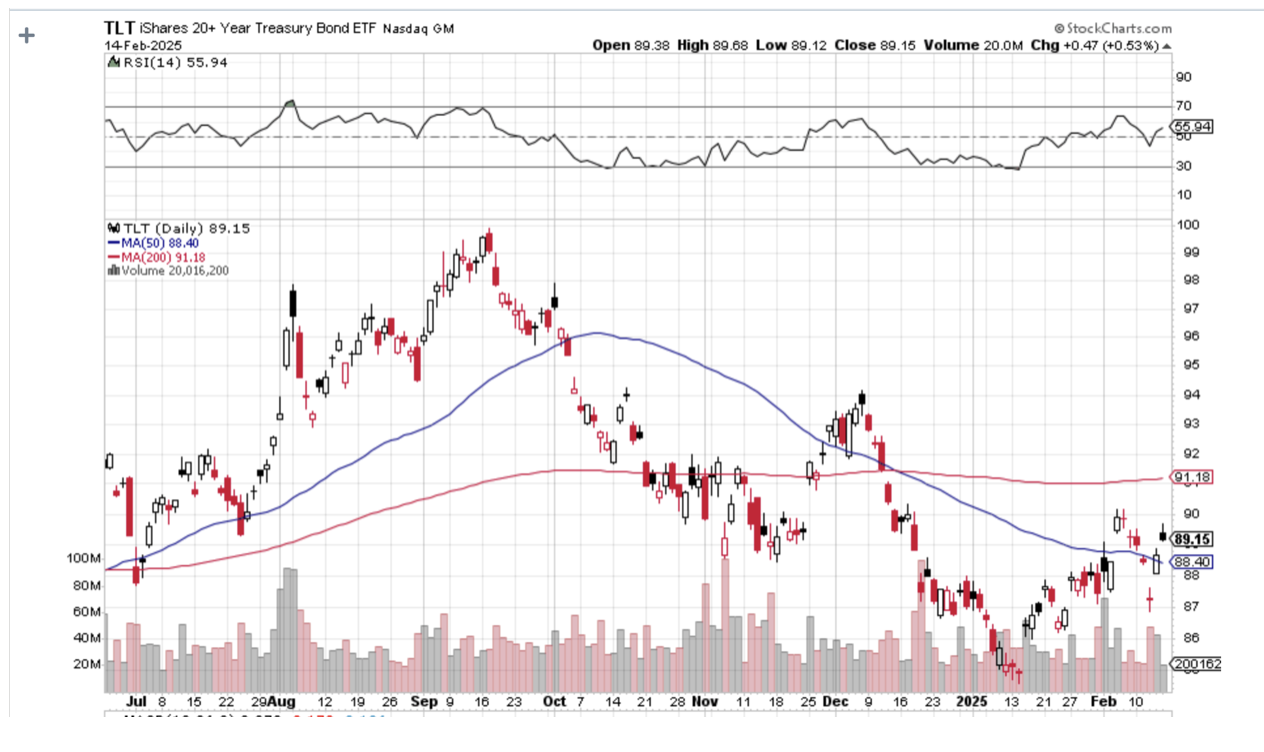

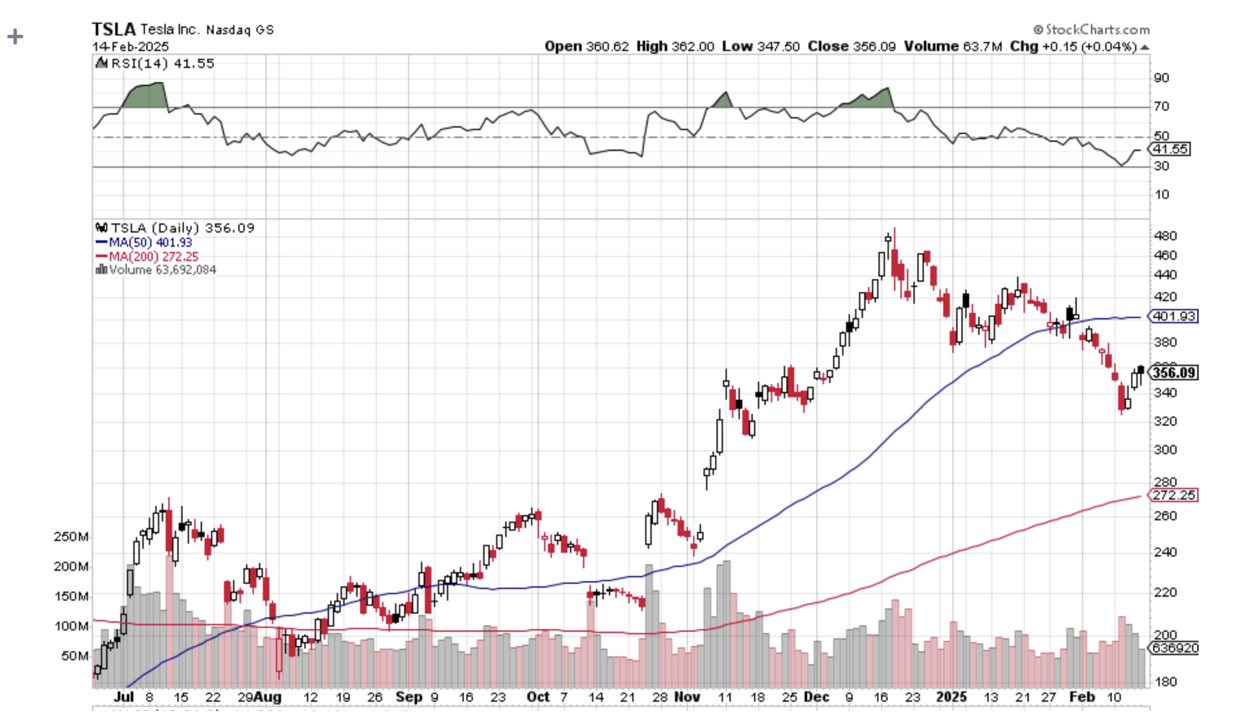

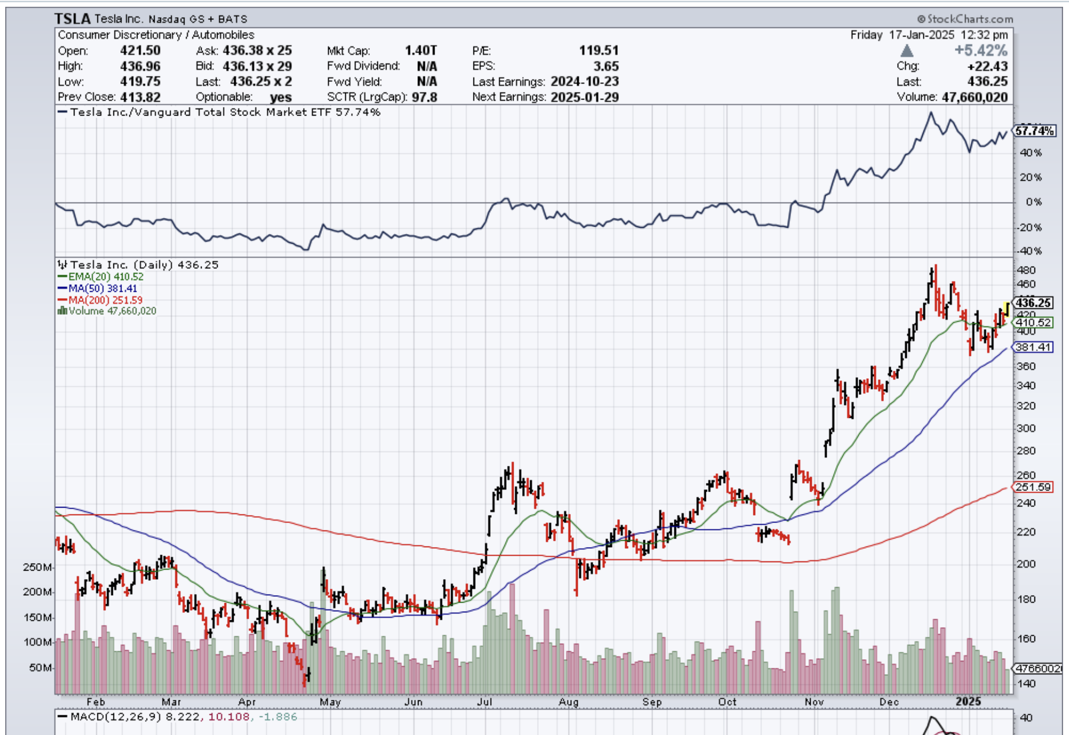

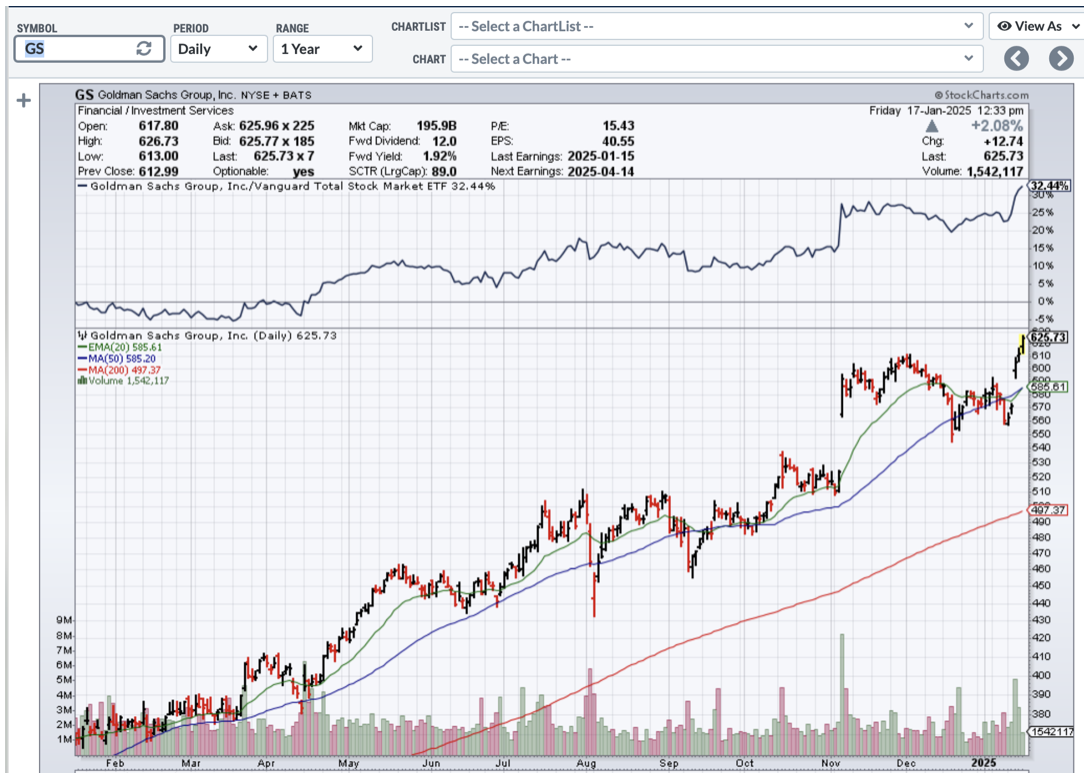

I saw the market breakdown coming a mile off and used my 90% cash to pile into new very short-term longs in JP Morgan (JPM), Interactive Brokers (IBKR), Tesla (TSLA), and Gold (GLD). I poured into new short positions with Tesla (TSLA), Nvidia (NVDA), and the United States US Treasury Bond Fund (TLT). This is in addition to an existing long in Goldman Sachs (GS). Last week, I leapt from 90% cash to 40% long, 40% short, and 20% cash.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 74 of 94 trades have been profitable in 2024, and several of those losses were really break-even. That is a success rate of +78.72%.

Try beating that anywhere.

Core PCE Price Index Comes in Line. The personal consumption expenditures price index, the Federal Reserve’s preferred inflation measure, increased 0.3% for the month and showed a 2.5% annual rate. Excluding food and energy, core PCE also rose 0.3% for the month and was at 2.6% annually. Fed officials more closely follow the core measure as a better indicator of longer-term trends. Personal income posted rose 0.9% against expectations for a 0.4% increase. However, the higher incomes did not translate into spending, which decreased by 0.2%, versus the forecast for a 0.1% gain.

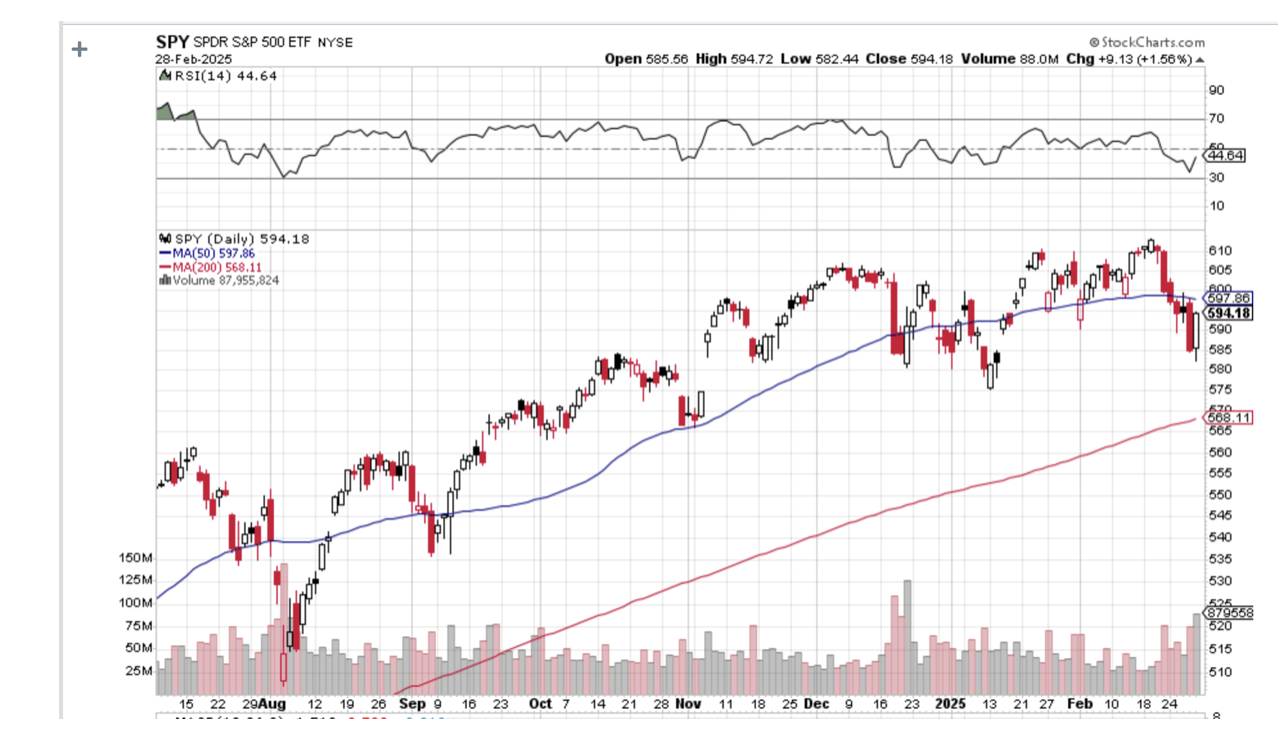

Retail Investors Market Sentiment Hit All-Time Bearish Highs. Options activity has also taken a big swing towards put buying. Dump all the stocks you were dating. Both Nvidia (NVDA) and Tesla (TSLA), the two most widely traded stocks in the market, broke their 200-day moving averages today. This is a very negative medium-term indicator. Only keep the ones you’re married to, not the ones you’re dating. This is not the rose garden we were promised.

US Margin Debt Hits All-Time High, at $937 billion as of January. That’s up 33% from $701 billion in January 2024. Over the same period, the S&P 500 gained 24.7%. Speculation on credit is running rampant. Margin trading, in which investors borrow funds from their brokerage firms in order to buy stocks, can amplify returns.

Weekly Jobless Claims Jump to 242,000, up 22,000, as the government firings kick in. In Washington, D.C., new claims totaled 2,047, an increase of 421, or 26%, the largest number for the city since March 25, 2023.

Nvidia Beats (NVDA) even the most optimistic expectations. The company forecasted higher first-quarter revenue, signaling continued strong demand for artificial intelligence chips, and said orders for its new Blackwell semiconductors were "amazing." The forecast helps allay doubts around a slowdown in spending on its hardware that emerged last month, following DeepSeek's claims that it had developed AI models rivaling Western counterparts at a fraction of their cost. Nvidia's outlook for gross margin in the current quarter was slightly lower than expected, though, as the company's Blackwell chip ramp-up weighs on Nvidia's profit. Nvidia forecast first-quarter gross margins will sink to 71%, below the 72.2% forecast by Wall Street, according to data compiled by LSEG.

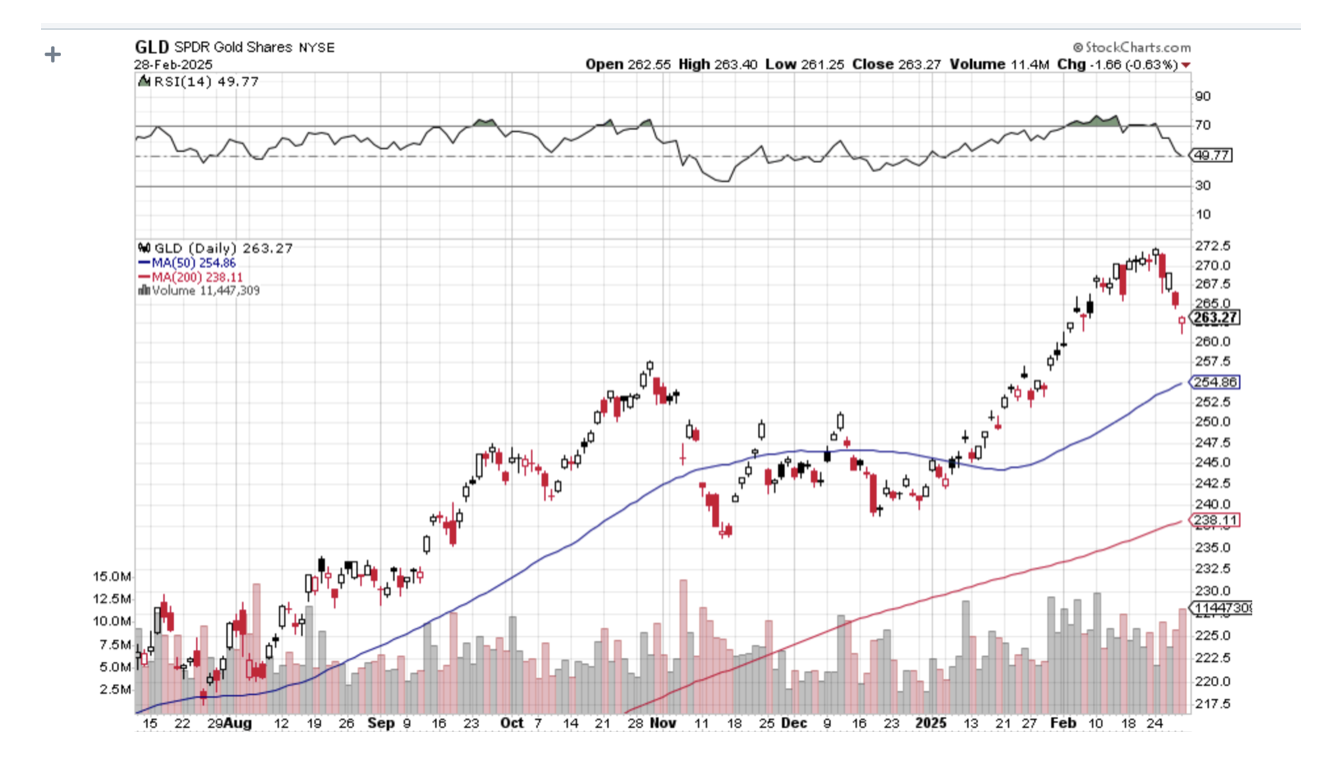

Gold ETFs (GLD) Have Become a Hot Commodity, with $4.5 billion pouring into (GLD) — with around half of that inflow occurring during Friday’s stock market selloff. The flight to safety bid is on. Those moves come as gold prices are at all-time highs in early 2025, boosted by trade uncertainty and inflation concerns. Buy (GLD) on dips.

Chinese Inflation (FXI) Hits 20-Year Lows, as the economy continues in free fall. Beijing is also expected to release its plans for spending on defense and technological development in the year ahead, along with details on private sector support. Last year, the inflation rate came in at only 0.2%.

Pending Homes Sales Hit All-Time Low, in January down 4.6% MOM and 5.2% YOY. Inventories are rising, but affordability is at record lows. Exceptionally cold weather was a factor. Homebuilder Sentiment plummeted to 42, a two-year low, and tariff concerns. Our drywall comes from Mexico, and our lumber comes from Canada. Avoid all real estate plays like the plague.

Home Prices are Still Rising, according to the S&P Case Shiller National Home Price Index. House prices rose 0.4%. They increased 4.7% in the 12 months through December. The strong increase in prices was despite rising housing supply, which is being driven by ebbing demand amid higher mortgage rates. New York showed the biggest gain at 7.2% YOY, followed by Chicago at 6.6% and Boston at 6.35%. Washington, DC, was the only city showing a loss at -1.1%.

Consumer Confidence Collapses to a Four-Year Low, down 7 points from 105 to 98, as tariff-driven inflation fears ramp up. The Conference Board’s Consumer Confidence Index for February, released Tuesday morning, fell to 98.3, falling for the third-straight month and marking the largest monthly decline since August 2021. Technology stocks sold off hard. Bonds are starting to discount a recession.

Berkshire Hathaway (BRK/B) Builds Record Cash, at $334 billion, up $9 billion in December alone. The Oracle of Omaha has been selling huge chunks of Apple (AAPL) and Bank of America (BAC) and putting the money into US Treasury Bills. Warren earned an eye-popping $47 billion in 2024, up 27% YOY. A price earnings multiple at a record 25X for the S&P 500. If Warren Buffet is selling, should you be buying?

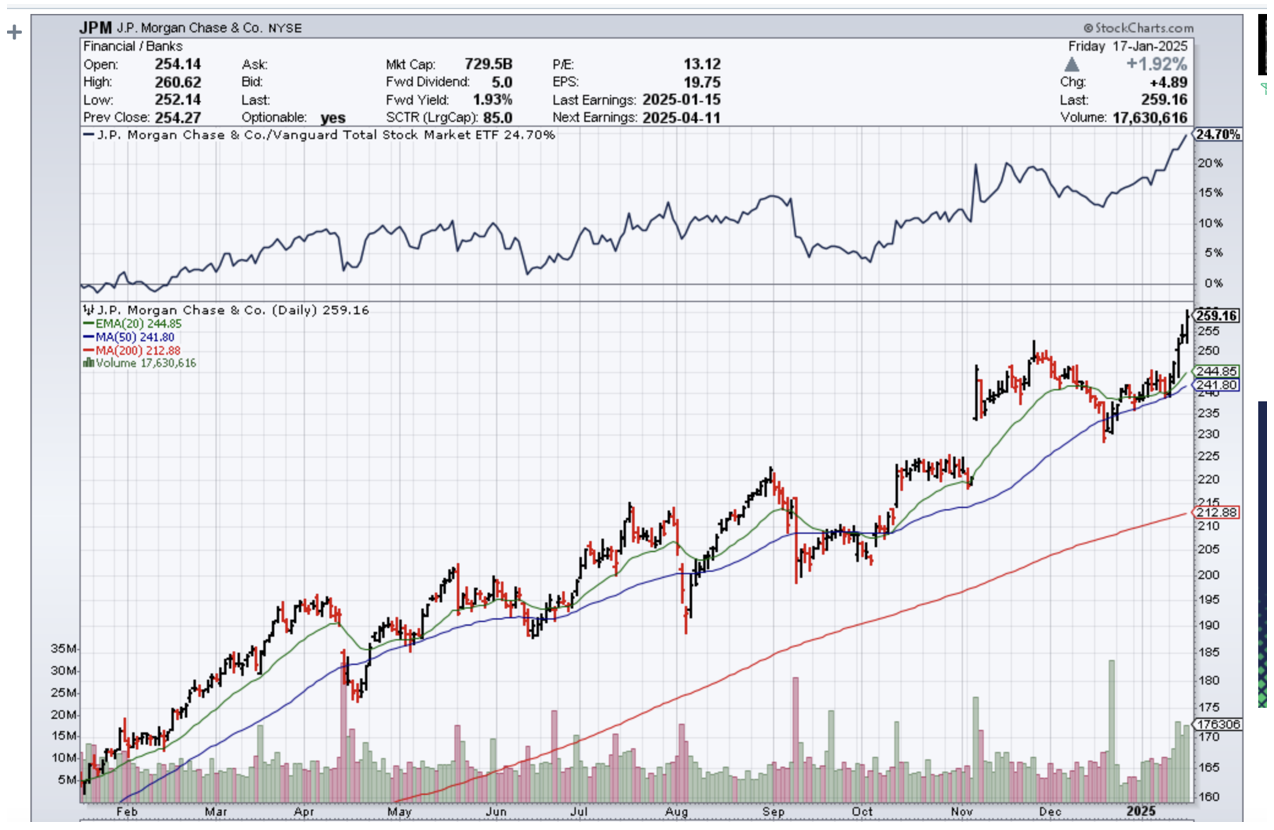

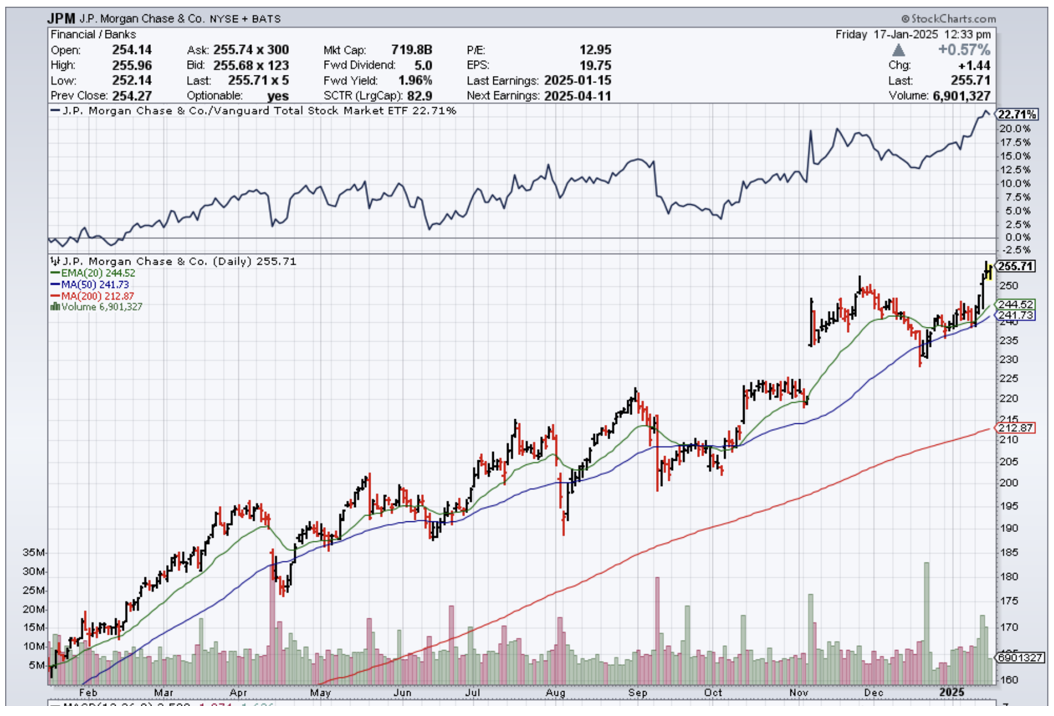

Jamie Dimon Sells 30% of JP Morgan Stock, yet another indicator of a market top. Jamie is famous for loading up on (JPM) at the absolute market bottom in 2009. Does he know something we don’t? Banks have been the lead sector in the market since the summer.

Existing Homes Sales Crater, on a closing contract basis, down 4.9% in January to 4.09 million units. Terrible weather was a factor. Inventories are up 17% YOY and 3.5% for the month. Al cash sales hit 29%. The average price of a home is at an all-time high at $396,800, up 4.5% YOY.

My Ten-Year View – A Reassessment

We have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties, is now looking at multiple gale force headwinds. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

My Dow 240,000 target has been pushed back to 2035.

On Monday, March 3 at 8:30 AM EST, the ISM Manufacturing PMI is announced.

On Tuesday, March 4 at 8:30 AM, the API Crude Oil Stocks is released.

On Wednesday, March 5 at 8:30 AM, the ADP Employment Index is printed.

On Thursday, March 6 at 8:30 AM, the Weekly Jobless Claims are disclosed.

On Friday, March 7 at 8:30 AM, the Nonfarm Payroll Report for February is announced, as well as the headline Unemployment Rate. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I’ll never forget when my friend Don Kagin, one of the world’s top dealers in rare coins, walked into my gym one day and announced that he had made $1 million that morning. I enquired. “How is that, pray tell?”

He told me that he was an investor and technical consultant to a venture hoping to discover the long-lost USS Central America, which sunk in a storm off the Atlantic Coast in 1857, heavily laden with gold from the California gold fields. He just received an excited call that the wreck had been found in deep water off the US east coast.

I learned the other day that Don had scored another bonanza in the rare coins business. He had sold his 1787 Brasher Doubloon for $7.4 million. The price was slightly short of the $7.6 million that a 1933 American $20 gold eagle sold for in 2002.

The Brasher $15 doubloon has long been considered the rarest coin in the United States. Ephraim Brasher, a New York City neighbor of George Washington, was hired to mint the first dollar-denominated coins issued by the new republic.

Treasury Secretary Alexander Hamilton was so impressed with his work that he appointed Brasher as the official American assayer. The coin is now so famous that it is featured in a Raymond Chandler novel where the tough private detective, Phillip Marlowe, attempts to recover the stolen coin. The book was made into a 1947 movie, “The Brasher Doubloon,” starring George Montgomery.

This is not the first time that Don has had a profitable experience with this numismatic treasure. He originally bought it in 1989 for under $1 million and has made several round trips since then. The real mystery is who bought it last. Don wouldn’t say, only hinting that it was a big New York hedge fund manager who adores the barbarous relic. He hopes the coin will eventually be placed in a public museum.

Mad Hedge followers should start paying more attention to gold, which I believe just entered another decade-long bull market, thanks to falling US interest rates. You can’t go wrong buying LEAPS in the top two miners, Barrack Gold (GOLD) and Newmont Mining (NEM).

Who says the rich aren’t getting richer?

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 24, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE DOWNSIDE OF DOGE, plus THE LAST GLASS OF KOOL-AID)

(SPY), (TLT), (GS), (VST), (TSLA), (WMT), (UNH)

Global Market Comments

February 18, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD or THE TALE OF TWO MARKETS)

(GS), (TSLA), (NVDA), (VST)

While trading one market is hard enough, two is almost more than one can bear. In fact, we have all been trading two markets since 2025 began.

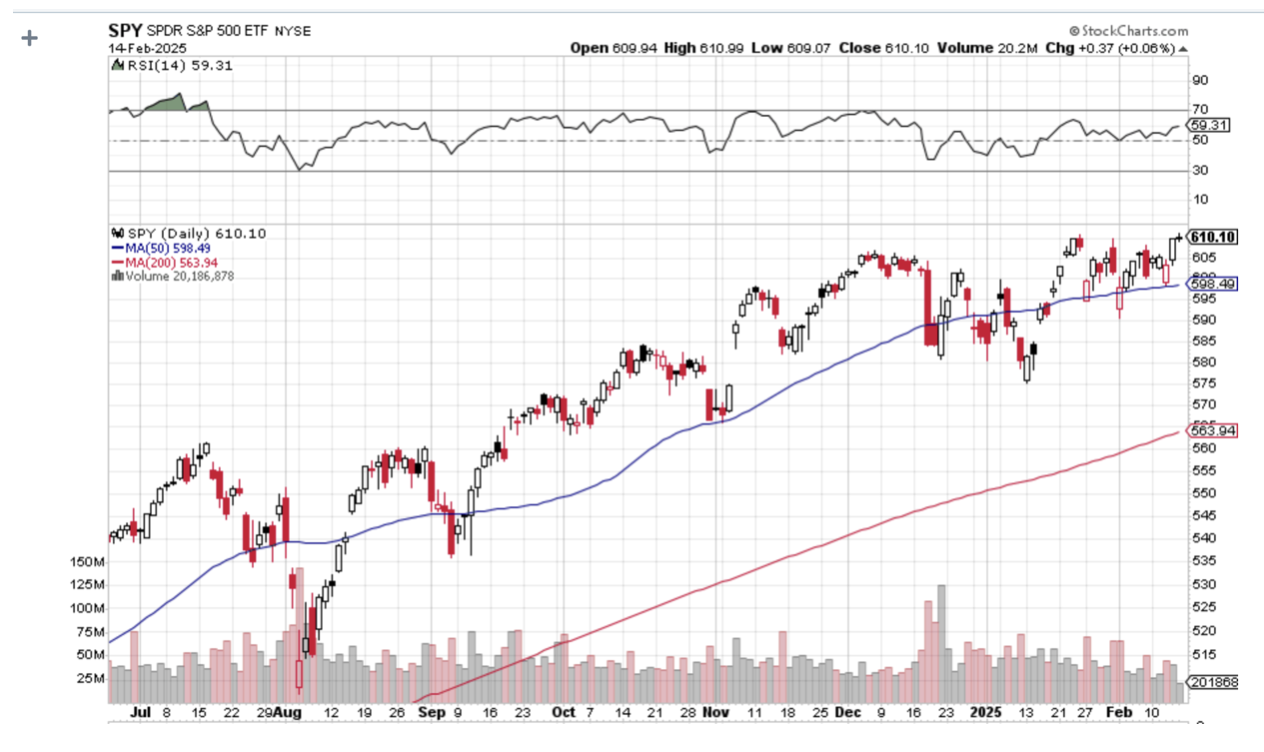

On the up days, it appears that the indexes are about to break out of a tediously narrow trading range. The market’s inability to go down is proof that it has to go up. Thursday was one of those days.

These are followed by down days, it appears that the indexes are about to break down. The market’s inability to stay up is proof that it has to go down. Wednesday was one of those days.

Up….down….up….down. Please excuse me if I get dizzy, which I shouldn’t, as I am a former combat pilot.

The market is calling Trump's bluff, rising in the face of threatened whopping great tariff increases against most of the world. So far, lots of noise, no action. The bark is worse than the bite. As I have been saying all year, ignore the noise and don’t fight the tape.

Which brings me to the price of copper.

Look at the ten-year chart of the red metal below, and you see a pretty positive formation is taking place. You have a similar set up in the chart of Freeport McMoRan, the world’s largest producer of copper.

This is in the face of huge negatives, like the failure of the Chinese economy to recover, the end of all alternative energy subsidies, the government announcing that it will no longer mint pennies, and the ongoing recession in residential real estate.

The seasoned trader in me knows that when you throw bad news on a commodity and it fails to go down, you buy the heck out of it. Is copper discounting the expansion of the grid independent of government assistance? There is more than meets the eye here.

What if the end of the Ukraine War is the big black swan of 2025? The best estimate for the cost of the reconstruction of Ukraine is $1 trillion. That would require a lot of copper, maybe a China’s worth.

It would also present major positives for the global economy. It would give us a peace dividend on the scale of the last one that started in 1991. For a start, energy prices would collapse as restrictions on the export of 10 million barrels a day of Russian oil come off. Ukraine would reclaim its position as one of the world’s largest food exporters, especially wheat and sunflower oil.

I know that Russia is close to running out of weapons. Some two-thirds of Russia’s tanks and planes have been destroyed, and they don’t have the parts to build new ones. That is forcing them to draw on military stockpiles from the 1950s.

I have first-hand knowledge of this. I learned from the Pentagon that the Russian missile fired at me on the eastern front lines failed to explode because it was 55 years old. The best estimate is that Russia will completely run out of some kinds of weapons by this summer.

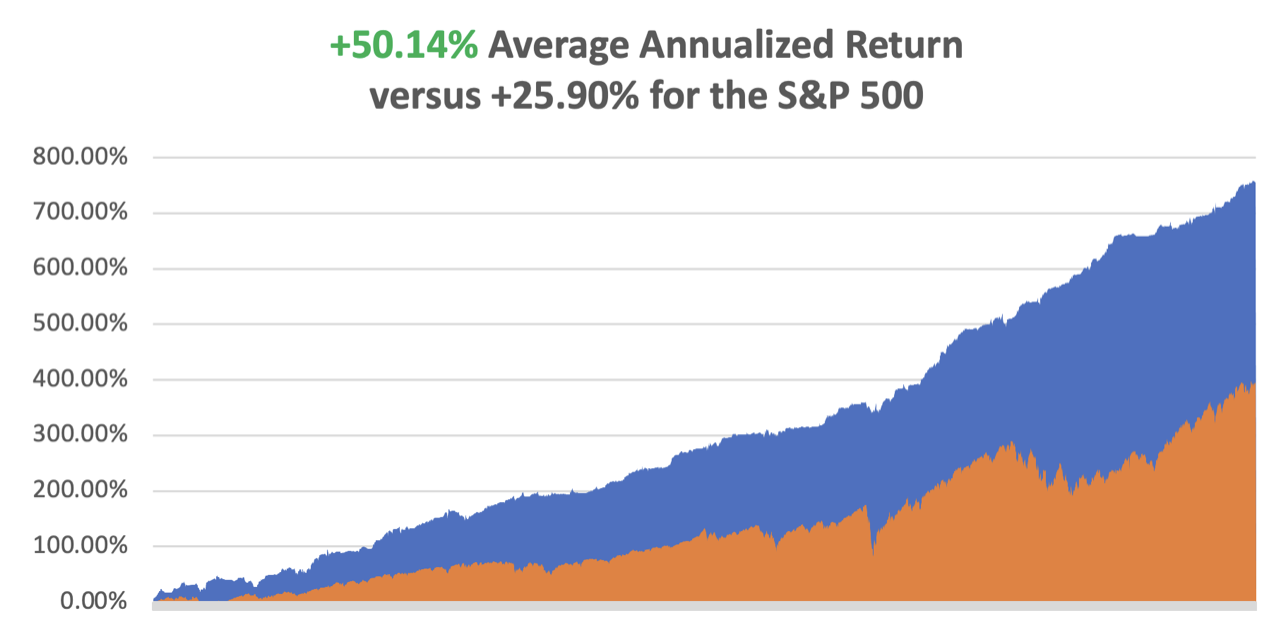

February has started with a respectable +2.73% return so far. That takes us to a year-to-date profit of +8.53% so far in 2025. My trailing one-year return stands at a spectacular +86.48% as a bad trade a year ago fell off the one-year record. That takes my average annualized return to +50.14% and my performance since inception to +759.42%.

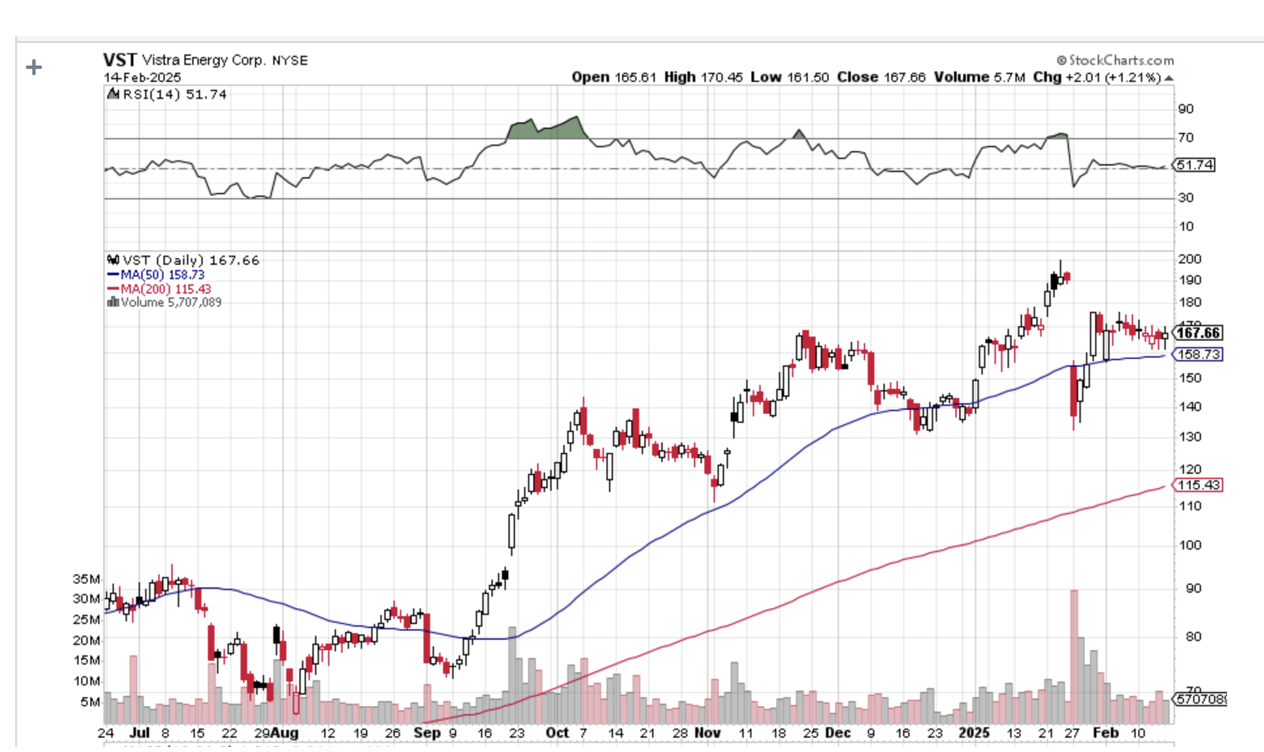

I used the brief weakness in Goldman Sachs (GS) to add a new long. I took profits on my two longs in Tesla on a bounce. That tops up our portfolio with a remaining short in (TSLA) and longs in (NVDA) and (VST). These latter positions expire in three trading days at max profit.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 74 of 94 trades have been profitable in 2024, and several of those losses were really break-even. That is a success rate of +78.72%.

Try beating that anywhere.

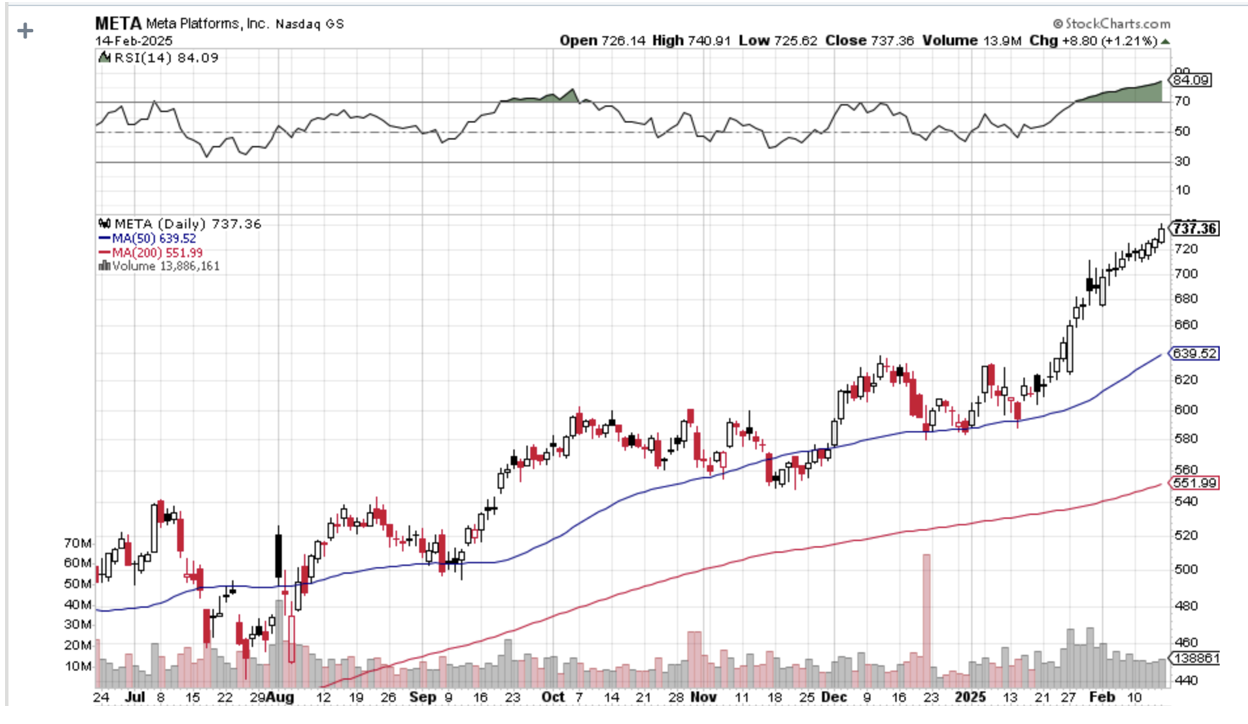

US Q4 Profits Hit Three-Year High. With reports in from nearly 70% of the S&P 500 companies as of Wednesday, fourth-quarter earnings are estimated to have risen 15.1% from a year earlier, up from an estimate of 9.6% growth at the start of January. The S&P 500 communication services sector, which includes companies such as Meta Platforms (META), is leading estimated fourth-quarter earnings gains among sectors, with year-over-year growth of 32.2%.

Core Inflation Rate Comes in Red Hot at 0.50%. Overall, advance was broad, led by shelter, food, and medicine. Shelter accounted for nearly 30% of the advance, according to the report from the Bureau of Labor Statistics out Wednesday. The so-called core CPI also climbed by more than forecast. That reflected higher prices for car insurance, airfares, and a record monthly increase in the cost of prescription drugs. It looks like no interest rate cuts for 2025.

PPI comes in Hot, reversing the gains on inflation of the past two years. The Producer Price Index, a measurement of average price changes seen by producers and manufacturers, rose 0.4% on a monthly basis and 3.5% for the 12 months ended in January. That held steady with December, which was upwardly revised to 3.5% according to Bureau of Labor Statistics data released Thursday.

US announced European Tariffs this Week, tanking stocks on Friday. Steel and metals shares are surging this morning. It’s pretty clear that markets hate all things tariff-related. Can we talk more about deregulation, which markets love? The reality is that markets don’t know how to price in Trump, swinging back and forth between euphoria one moment to Armageddon another. Best case, markets flatline. Worst case, they crash.

Gold (GLD) is headed for $3,000, my long-term target, on central bank and flight to safety buying. What’s the next target? $5,000 is the current turmoil in Washington continues. Notice that it’s the physical metal that’s moving, not the miners.

Foreign Investors Continue to Soak Up US Debt, seeking higher interest rates in an appreciating currency. Americans own 55% of the outstanding $36 trillion in US debt, while foreign investors own 24%, and the Federal Reserve 13%.

Wall Street Souring on Magnificent Seven. The market stronghold has diminished slightly, as the cohort struggles to meet ever-loftier expectations, and investors rotate into other parts of the market such as small caps. Tech titans also took a hit in late January after the emergence of Chinese startup DeepSeek raised concerns over how much spending will be needed to implement AI capabilities.

Market is Giving Up on any Interest Rate Cuts this Year, as the prospects of rising inflation from trade wars weigh on the market. Economists have warned that a wide-scale trade war could significantly raise prices, and consumers appear to be worried as well. Respondents to the University of Michigan’s consumer sentiment poll released Friday indicated they expect inflation to run at a 4.3% rate a year from now, up a full percentage point from the January reading.

Tesla Tanks 7%, and down 34% since December after Chinese competitor BYD announces a partnership with DeepSeek. The move is expected to accelerate BYD’s move into full self-driving. Tesla sales are falling in all major markets. Call it DeepSeek hit part 2.

Weekly Jobless Claims Fall. Initial claims for state unemployment benefits fell 7,000 to a seasonally adjusted 213,000 for the week ended February 8, the Labor Department said on Thursday. Economists polled by Reuters had forecast 215,000 claims for the latest week.

My Ten-Year View – A Reassessment

We have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties, is now looking at multiple gale force headwinds. The economy will completely stop decarbonizing. Technological innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

My Dow 240,000 target has been pushed back to 2035.

On Monday, February 17, markets are closed for President's Day.

On Tuesday, February 18 at 8:30 AM EST, the New York Empire State Manufacturing Index is released.

On Wednesday, February 19 at 8:30 AM EST, the New Housing Starts are printed.

On Thursday, February 20 at 8:30 AM, the Weekly Jobless Claims are disclosed.

On Friday, February 21 at 8:30 AM, the Existing Home Sales are announced. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, I was having lunch at the Paris France casino in Las Vegas at Mon Ami Gabi, one of the top ten grossing restaurants in the United States. My usual waiter, Pierre from Bordeaux, took care of me in his typical ebullient way, graciously letting me practice my rusty French.

As I finished an excellent but calorie-packed breakfast (eggs Benedict, caramelized bacon, hash browns, and a café au lait), I noticed an elderly couple sitting at the table next to me. Easily in their 80s, they were dressed to the nines and out on the town.

I told them I wanted to be like them when I grew up.

Then I asked when they first went to Paris, expecting a date sometime after WWII. The gentleman responded, “Seven years ago”.

And what brought them to France?

“My father is buried there. He’s at the American Military Cemetery at Colleville-sur-Mer along with 9,386 other Americans. He died on Omaha Beach on D-Day. I went for the D-Day 70th anniversary.” He also mentioned that he never met his dad, as he was killed in action weeks after he was born.

I reeled with the possibilities. First, I mentioned that I participated in the 40-year D-Day anniversary with my uncle, Medal of Honor winner Mitchell Paige, and met with President Ronald Reagan.

We joined the RAF fly-past in my own private plane and flew low over the invasion beaches at 200 feet, spotting the remaining bunkers and the rusted-out remains of the once floating pier. Pont du Hoc is a sight to behold from above, pockmarked with shell craters like the moon. When we landed at a nearby airport, I taxied over railroad tracks that were the launch site for the German V1 “buzz bomb” rockets.

D-Day was a close-run thing and was nearly lost. Only the determination of individual American soldiers saved the day. The US Navy helped too, bringing destroyers right to the shoreline to pummel the German defenses with their five-inch guns. Eventually, battleships working in concert with very lightweight Stinson L5 spotter planes made sure that anything the Germans brought to within 20 miles of the coast was destroyed.

Then the gentleman noticed the gold Marine Corps pin on my lapel and volunteered that he had been with the Third Marine Division in Vietnam. I replied that my father had been with the Third Marine Division during WWII at Bougainville and Guadalcanal and that I had been with the Third Marine Air Wing during Desert Storm.

I also informed him that I had led an expedition to Guadalcanal two years ago looking for some of the 400 Marines still missing in action. We found 30 dog tags and sent them to the Marine Historical Division at Quantico, Virginia, for tracing. I proudly showed them my pictures.

When the stories came back, it turned out that many survivors were children now in their 80s who had never met their fathers because they were killed in action on Guadalcanal.

Small world.

I didn’t want to infringe any further on their fine morning out, so I excused myself. He said Semper Fi, the Marine Corps motto, thanked me for my service, and gave me a fist pump and a smile. I responded in kind and made my way home.

Oh, and say “Hi” when you visit Mon Ami Gabi. Tell Pierre that John Thomas sent you and give him a big tip. It’s not easy for a Frenchman to cater to all these loud Americans.

Third Marine Air Wing

The D-Day Couple

The American Military Cemetery at Colleville-sur-Mer

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 21, 2025

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD or NOW WE ENTER THE GREAT UNKNOWN),

(GS), (MS), (JPM), (C), (BAC) (TLT), (TSLA)

I am writing this to you from Indian Rock Beach, Florida, an extended sand bar outside of Tampa on the west coast. Cabin cruisers pass by every five minutes. There is not much fishing though with rain and temperatures in the low 40s, the coldest of the year. leaving a lot of free time for indoor work. Every building is missing a chunk of wall or roof if not totally destroyed from the October hurricane Helena, including my own Airbnb. The last hurricane here took place in 1921.

Everywhere I look, hedge fund managers are derisking, cutting exposure, and laying on hedges. The reason is that no one has a handle on what is going to happen in financial markets in the short term. Do we go up, down, or nowhere? The rapid unwind of the post-election rally has put the fear of markets back in them once again.

There is also a rare shortage of news in the financial media. It’s as if someone is sucking all the oxygen out of the room.

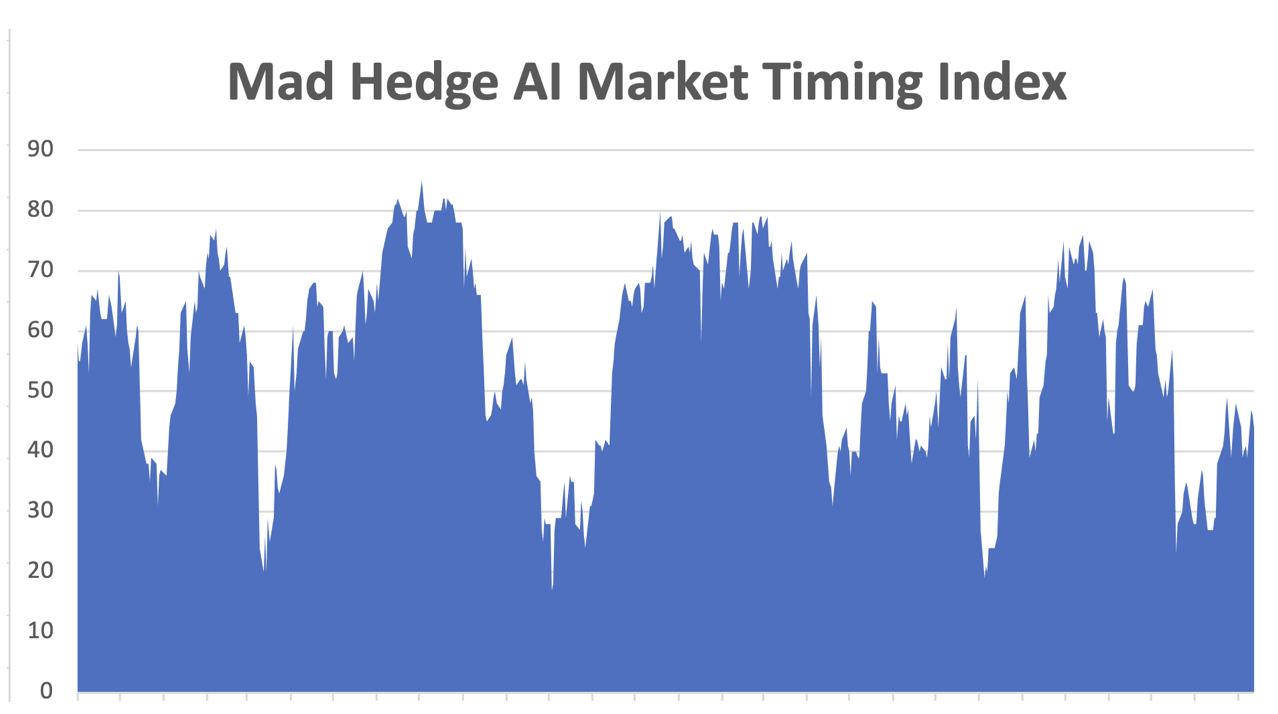

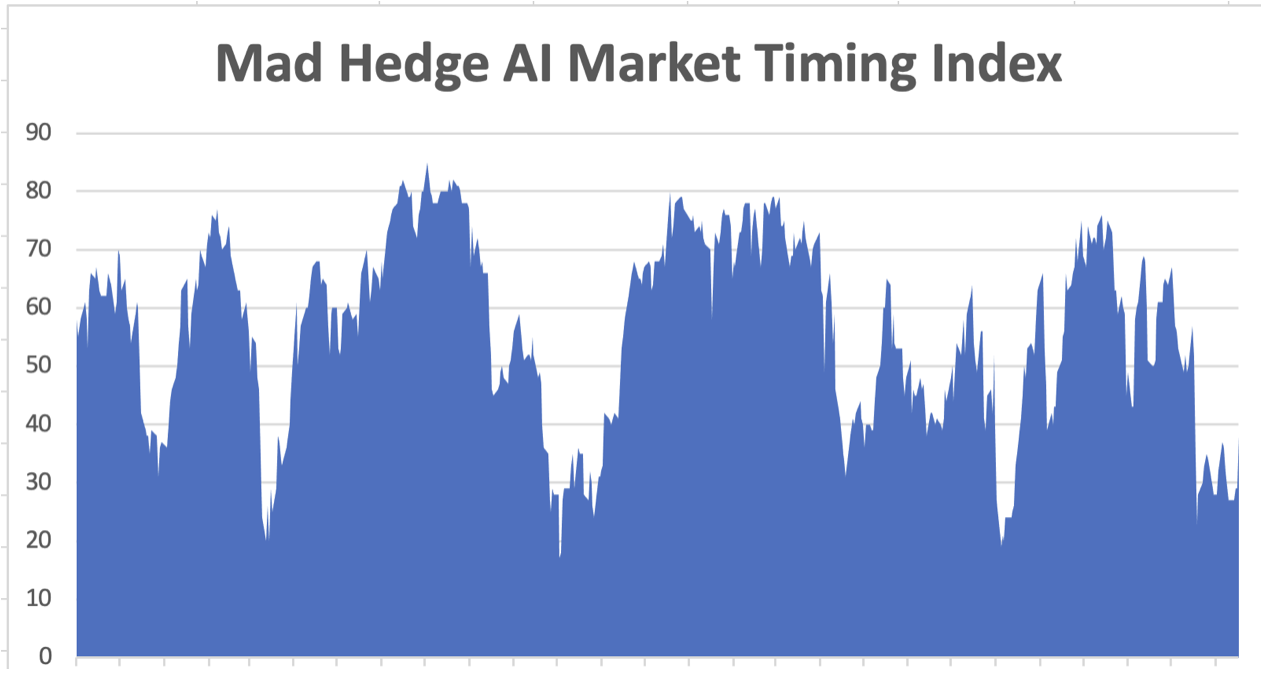

We had about a week where the Mad Hedge Market Timing Index in the mid-twenties was enticing us back into the market. I was expecting a hot December Consumer Price Index to give us a nice selloff and the perfect entry point I had been waiting a month for, in line with all the economic warm data of the last three months.

But it was not to be. The CPI printed at a cool 2.9% YOY and the Dow Average opened up 700 points the next morning, the first step in a 1,700-point three-day rally. Half the December losses came back in a heartbeat.

So much for the great entry point.

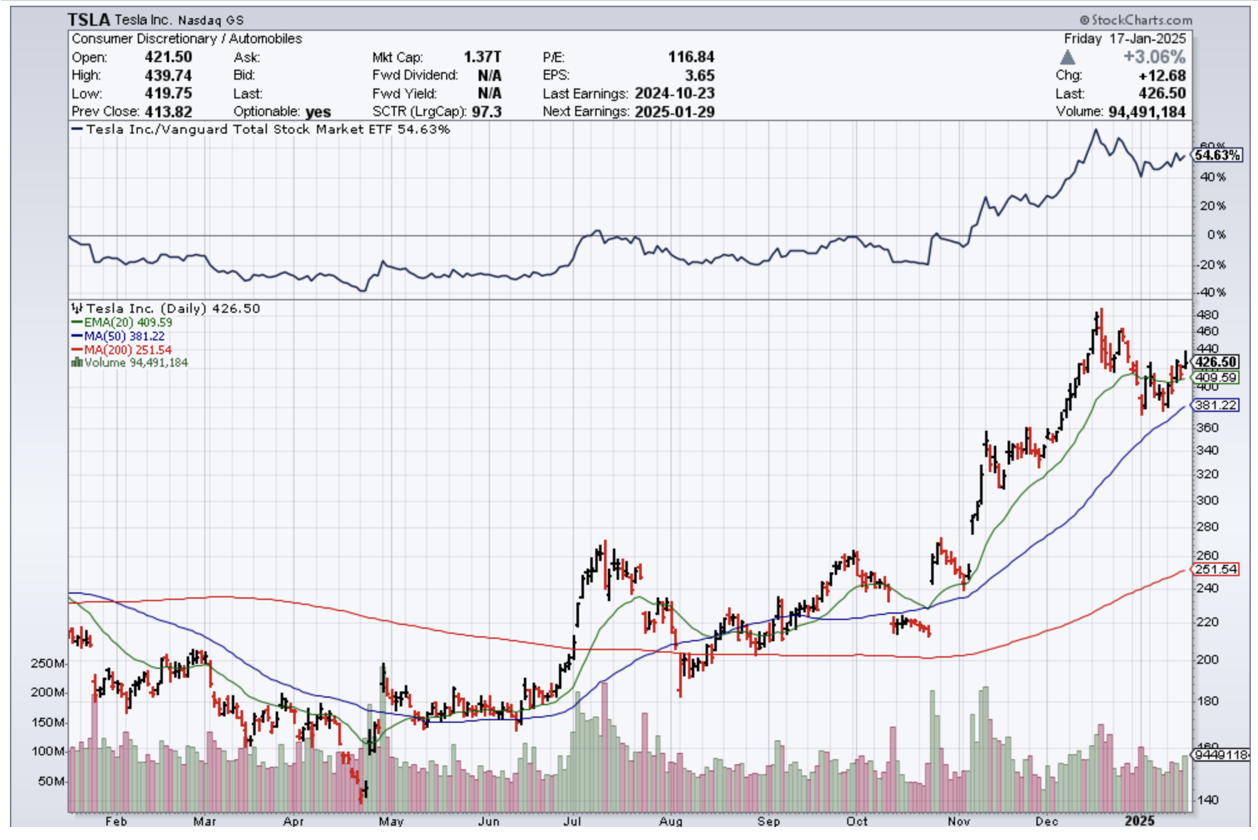

All of my target stocks like (GS), (MS), (JPM), (C), and (BAC) went ballistic. I only managed to get into a long in Tesla (TSLA) because the implied volatility was a sky-high 70%. That way, the stock could take a surprise hit and I still would have a safety cushion large enough to eke out the maximum profit by the February 20 option expiration. What’s next? How about a $100 in-the-money bearish Tesla put spread, once the rally burns out?

I can’t remember a time when there was such a narrow field of attractive trading targets. Rising interest rates have killed off bonds, foreign currencies, precious metals, and real estate. A weak China has destroyed commodities and energy, with US overproduction contributing to the latter. Only financials look interesting for the short term and big tech for the long term.

At that point, financials are not exactly undiscovered investments, but they should have another three months of life in them. That’s when big tech should reclaim the leadership, when we get another surprise AI-driven earnings burst.

What does this get us in the major indexes? With so much of the stock market on life support, not much, maybe 10% at best. After that, who knows?

There is no point in looking for any more financial news today (Sunday), as there isn’t any with a holiday tomorrow. So I am headed out for a one-hour walk of the beach.

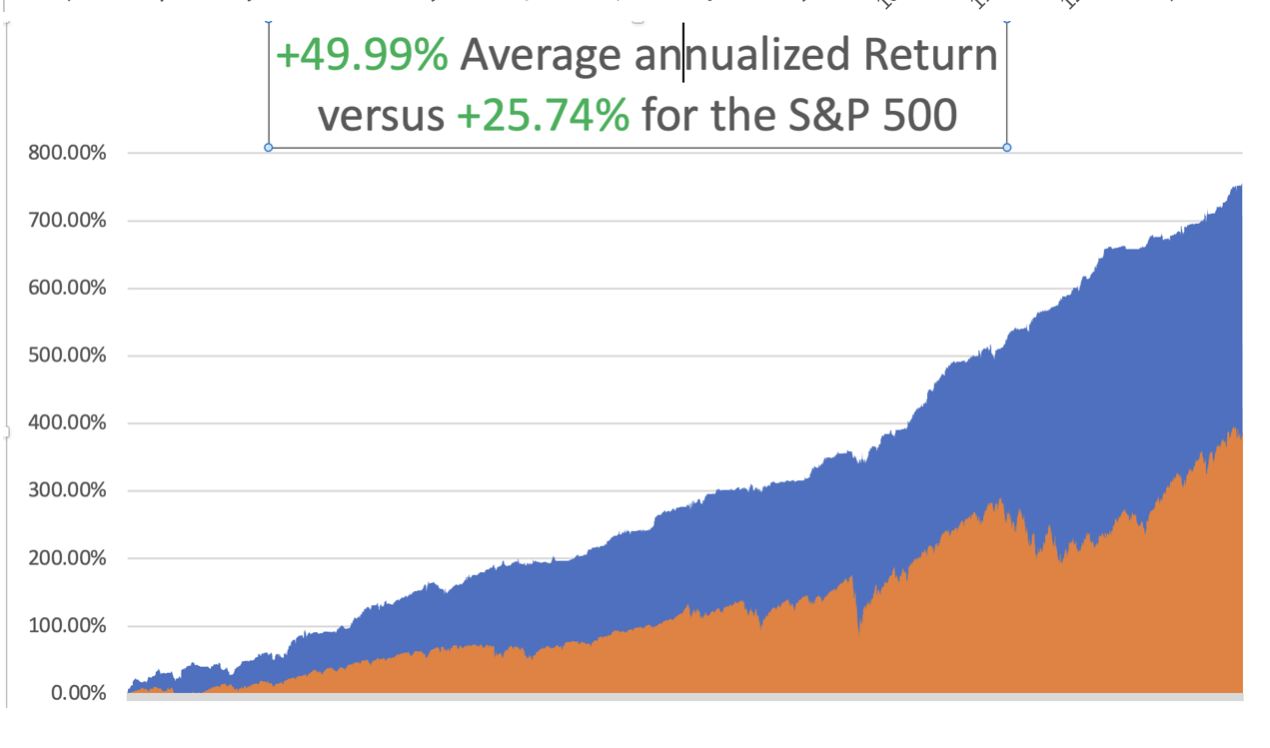

We managed to grind out a +2.07% return so far in January. That takes us to a year-to-date profit of +2.07% so far in 2025. My trailing one-year return stands at +75.92%. That takes my average annualized return to +49.99% and my performance since inception to +753.93%.

I stopped out of my long position in (TLT) near cost. My January 2025 (TSLA) expired on Friday at its maximum profit point, soaring a torrid $50 in the two days going into expiration.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 74 of 94 trades were profitable in 2024, and several of those losses were really break-evens. That is a success rate of +78.72%.

Try beating that anywhere.

My Ten-Year View – A Reassessment

When have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties is now looking at a headwind. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

My Dow 240,000 target has been pushed back to 2035.

Consumer Price Index Cools at 0.2%, or 3.2% YOY, the first drop in six months. Economists see the core gauge as a better indicator of the underlying inflation trend than the overall CPI which includes often-volatile food and energy costs. The headline measure rose 0.4% from the prior month, with over 40% of the advance due to energy.

Los Angeles Fires to Cost $270 Billion, with only $30 billion covered by insurance. Inflation will rise as the cost of construction labor and materials soar. Tradesmen around the country are packing their trucks and heading west to snare work at double the normal rate. There is no trade here as the new home builders are not involved, who are set up to only build mass-produced tract homes. Yet another black swan for 2025.

$4 Trillion in Asset Management Disrupted by the Los Angeles Fires, with some relocating office space and supporting staff members who have lost their homes. The LA area is home to large industry players like Capital Group, TCW Group, hedge funds Oaktree Capital and Ares Management.

Bonds Hit 14-Month Lows at a 4.80% Yield, as fixed income dumping continues across the board. “Higher Rates for longer” don’t fit in here anywhere. But there may be a BUY setting up for (TLT) at 5.0%.

The Trump Bump is Gone, stock markets giving up all their post-election gains. Technology was especially hard hit, with lead stock NVIDIA down 15%. It seems that people finally examined the implications of what Trump was proposing for the stock market. Tax-deferred selling of the enormous profits run up under the Biden administration is a big factor.

Amazon is Getting Ready for Another Run. Strong earnings and continuing excitement about artificial intelligence will help Amazon stock move back into the green. The e-commerce and cloud company to beat estimates when it reports its fourth-quarter results—analysts are expecting a profit of $1.48 a share on sales of $187.3 billion, according to data from FactSet. Buy (AMZN) on dips.

JP Morgan Announces Record Profits, boosted by volatility tied to the US elections in November. Trading revenue at the firm rose 21% from a year earlier, jumping to $7.05 billion. Fixed income was the star, with revenue beating analysts’ estimates, while equities-trading revenue fell short. Buy (JPM) on dips.

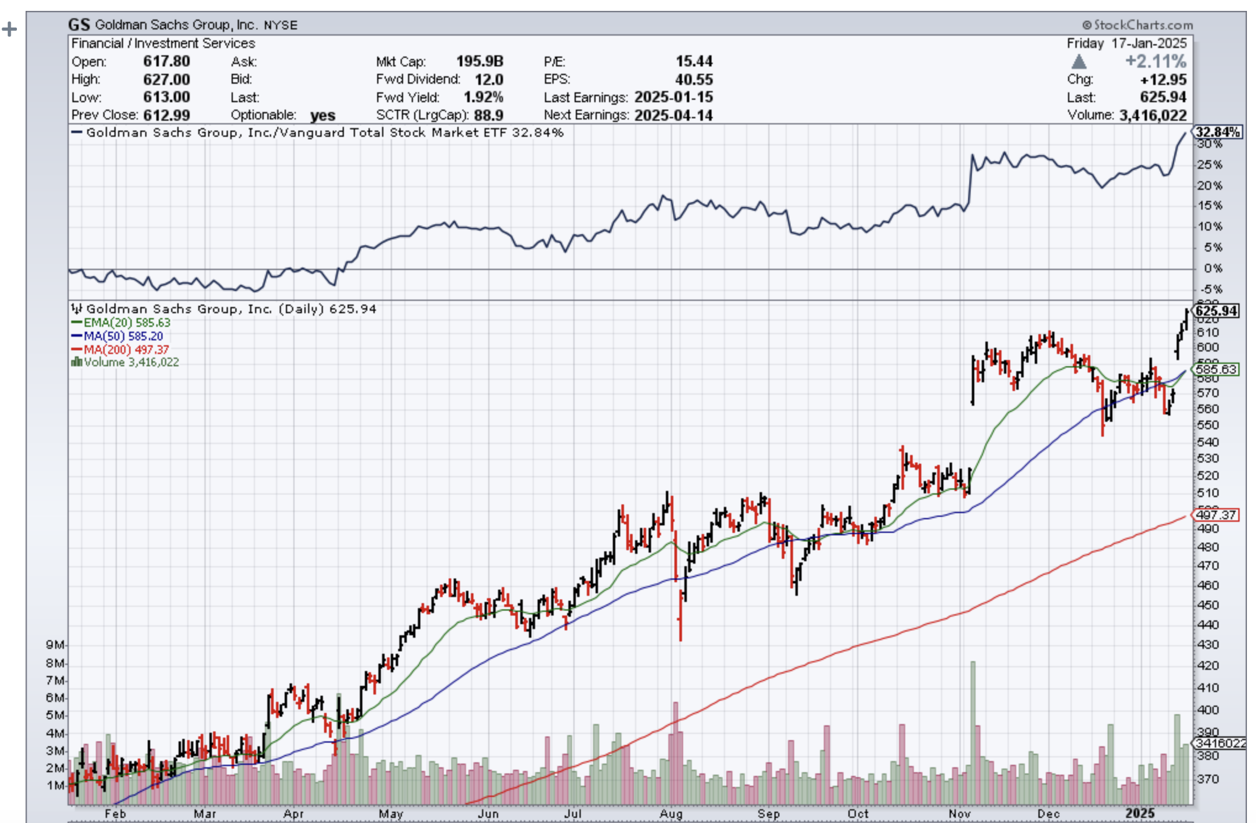

Goldman Sachs Beats. The firm’s fourth-quarter profits more than doubled to $4.1 billion, buoyed by strength in its investment bank, expansion of its asset management business, and a surprise $472 million gain from a balance sheet bet. Goldman ended 2024 as the best-performing stock among major US banks with a 48% advance. The bank is positioning itself for a long-awaited resurgence in deals after ditching major parts of a consumer foray.

Morgan Stanley Doubles Profits. Equities were the big winner, with revenue jumping 51% in the quarter and reaching an all-time high for the full year. In the wealth business, net new assets fell just shy of estimates even as revenue topped expectations.

SEC Sues Elon Musk, alleging the billionaire violated securities law by acquiring Twitter shares at “artificially low prices.” In his purchases, Musk underpaid for Twitter shares by at least $150 million, the SEC says. Musk bought Twitter in 2022 for about $44 billion, later changing the name to X. Expect this case to get lost behind the radiator next week.

Fed Minutes are Turning Hawkish, making an interest rate cut at the March 19 meeting unlikely. Inflation is stubbornly above target, the economy is growing at about 3% pace and the labor market is holding strong. Put it all together and it sounds like a perfect recipe for the Federal Reserve to raise interest rates or at least to stay put.

EIA Expects Weak Oil Prices for All of 2025. Many analysts expect an oversupplied oil market this year after demand growth slowed sharply in 2024 in the top consuming nations: the U.S. and China. The EIA said it expects Brent crude oil prices to fall 8% to average $74 a barrel in 2025, then fall further to $66 a barrel in 2026.

Housing Starts were up 3.0% in December, with single-family homes up only 3%, while multifamily saw a 59% rise. It should shift away from home sales crushed by 7.2% mortgage rates. You can write off real estate in 2025.

EV and Hybrid Sales Reach a Record 20% of US Vehicle Sales in 2024 and now account for 10% of the total US fleet. And you wonder why oil prices are so low. That includes 1.9 million hybrid vehicles, including plug-in models, and 1.3 million all-electric models. Tesla continued to dominate sales of pure EVs but Cox Automotive estimated its annual sales fell and its market share dropped to about 49%.

SpaceX Starship Blows Up on test launch number seven. The Federal Aviation Administration issued a warning to pilots of a “dangerous area for falling debris of rocket Starship,” according to a pilots’ notice. Looks like that Mars trip will be delayed.

On Monday, January 20, the markets are closed for Martin Luther King Day.

On Tuesday, January 21 at 8:30 AM EST, nothing of note takes place.

On Wednesday, January 22 at 8:30 AM, the API Crude Oil Stocks are printed.

On Thursday, January 23 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, January 24 at 8:30 AM, Existing Home Sales are published. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, back in the early 1980s, when I was starting up Morgan Stanley’s international equity trading desk, my wife Kyoko was still a driven Japanese career woman.

Taking advantage of her near-perfect English, she landed a prestige job as the head of sales at New York’s Waldorf Astoria Hotel.

Every morning, we set off on our different ways, me to Morgan Stanley’s HQ in the old General Motors Building on Avenue of the Americas and 47th street and she to the Waldorf at Park and 34th.

One day, she came home and told me there was this little old lady living in the Waldorf Towers who needed an escort to walk her dog in the evenings once a week. Back in those days, the crime rate in New York was sky-high and only the brave or the reckless ventured outside after dark.

I said, “Sure, what was her name?”

Jean MacArthur.

I said, "THE Jean MacArthur?"

She answered, “Yes.”

Jean MacArthur was the widow of General Douglas MacArthur, the WWII legend. He fought off the Japanese in the Philippines in 1941 and retreated to Australia in a dramatic night PT Boat escape.

He then led a brilliant island-hopping campaign, turning the Japanese at Guadalcanal and New Guinea. My dad was part of that operation, as were the fathers of many of my Australian clients. That led all the way to Tokyo Bay where MacArthur accepted the Japanese in 1945 on the deck of the battleship USS Missouri.

The MacArthurs then moved into the Tokyo embassy where the general ran Japan as a personal fiefdom for seven years, a residence I know well. That’s when Jean, who was 18 years the general’s junior, developed a fondness for the Japanese people.

When the Korean War began in 1950, MacArthur took charge. His landing at Inchon Harbor broke the back of the invasion and was one of the most brilliant tactical moves in military history. When MacArthur was recalled by President Truman in 1952, he had not been home for 13 years.

So it was with some trepidation that I was introduced by my wife to Mrs. MacArthur in the lobby of the Waldorf Astoria. On the way out, we passed a large portrait of the general who seemed to disapprovingly stare down at me taking out his wife, so I was on my best behavior.

To some extent, I had spent my entire life preparing for this job.

I had stayed at the MacArthur Suite at the Manila Hotel where they had lived before the war. I knew Australia well. And I had just spent a decade living in Japan. By chance, I had also read the brilliant biography of MacArthur by William Manchester, American Caesar, which had only just come out.

I also competed in karate at the national level in Japan for ten years, which qualified me as a bodyguard. In other words, I was the perfect after-dark escort for Midtown Manhattan in the early eighties.

She insisted I call her “Jean”; she was one of the most gregarious women I have ever run into. She was grey-haired, petite, and made you feel like you were the most important person she had ever run into.

She talked a lot about “Doug” and I learned several personal anecdotes that never made it to the history books.

“Doug” was a staunch conservative who was nominated for president by the Republican party in 1944. But he pushed policies in Japan that would have qualified him as a raging liberal.

It was the Japanese who begged MacArthur to ban the army and the navy in the new constitution for they feared a return of the military after MacArthur left. Women gained the right to vote on the insistence of the English tutor for Emperor Hirohito’s children, an American Quaker woman. He was very pro-union in Japan. He also pushed through land reform that broke up the big estates and handed out land to the small farmers.

It was a vast understatement to say that I got more out of these walks than she did. While making our rounds, we ran into other celebrities who lived in the neighborhood who all knew Jean, such as Henry Kissinger, Ginger Rogers, and the UN Secretary-General.

Morgan Stanley eventually promoted me and transferred me to London to run the trading operations there, so my prolonged free history lesson came to an end.

Jean MacArthur stayed in the public eye and was a frequent commencement speaker at West Point where “Doug” had been a student and later the superintendent. Jean died in 2000 at the age of 101.

I sent a bouquet of lilies to the funeral.

Kyoko passed away in 2002.

In 2014, China’s Anbang Insurance Group bought the Waldorf Astoria for $1.95 billion, making it the most expensive hotel ever sold. Most of the rooms were converted to condominiums and sold to Chinese looking to hide assets abroad.

The portrait of Douglas MacArthur is gone too. During the Korean War, he threatened to drop atomic bombs on China’s major coastal cities.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

![]()

Global Market Comments

January 17, 2025

Fiat Lux

Featured Trades:

(JANUARY 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(GS), (MS), (JPM), (C), (BAC), (TSLA), (HOOD), (COIN), (NVDA), (MUB), (TLT), (JPM), (HD), (LOW), FXI)

Below please find subscribers’ Q&A for the January 15 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Sarasota, Florida.

Q: What would I recommend right now for my top five stocks?

A: That’s easy. Goldman Sachs (GS), Morgan Stanley (MS), JP Morgan (JPM), Citibank (C), and Bank of America (BAC). There's five right there—the top five financials that are coming out of a decade-long undervaluation. A lot of the regional banks, which are also viable, are still trading to discount the book value, which all the financials used to trade out only a couple of years ago. Of course, JP Morgan's reaching a two-year return of around double, but the news just keeps getting better and better, so buy the dips. Buy every sell-off in financials and you will be a happy camper for the year.

Q: What do you think about Robin Hood (HOOD)?

A: Well, the trouble with Robinhood is it’s very highly dependent on crypto volumes. If you think crypto is going to go higher and volumes will increase, this is a great play. However, you get another 95%, out-of-the-blue selloff in crypto like we had three years ago and Coinbase (COIN) will follow it right back down again. On the last downturn, there were concerns that Coinbase would go under, so if you can hack the volatility, take a shot, but not with my money. I have the largest banks in the country that are about to double again; I would much rather be buying LEAPS in that area and getting anywhere from 100% to 1000% percent returns on a 2-year view—much more attractive risk-reward for me. And they pay a dividend.

Q: How do you define a 5% correction?

A: Well, if you have a $100 stock and it drops $5, that is a 5% correction.

Q: Can you please explain what Tesla 2X leverage actually means and is it a way to trade Tesla as an alternative?

A: I steer people away from the 2Xs because the tracking error is really quite poor. You only get 1.5% of the upside, but 2.5 times the downside over time. These are more day trading vehicles. They take out huge fees, and huge dealing spreads—it's a very expensive way to trade. Far cheaper is just to buy Tesla (TSLA) stock on margin at 2 to 1, and there your tracking error is perfect, your fees are much lower, and you just have the margin interest rate to pay on the position, which is 6% a year or 50 basis points a month. No reason to make the ETF people richer than they already are. They keep coining these products—1x, 2x, 3x long shorts on every one of the high volume stocks, and it sucks a lot of people in, but it's higher risk, lower returns for the amount of money you're risking as far as I'm concerned. So that's the way to do it.

Q: What are your projections for Nvidia (NVDA)?

A: I think not just Nvidia, but all of the big tech is going to be kind of trading in a sideways range for a while, maybe 6 months, and then we get an upside breakout if you get the earnings breakout, which we are all expecting. AI is still in business, and still growing gangbusters. There are always a lot of Cassandra's out there saying that we're going to crash anytime, and I just don't see it. I know a lot of these people, I'm in touch with a lot of the companies, I see Beta releases of all products, the consumer products, and…the slowdown just ain't happening, I'm sorry. And I've been through a lot of these tech booms over the last 40 years, and this is only showing signs of just getting started.

Q: How come Tesla (TSLA) is up and down $30 every couple of days?

A: Number one, it is the most actively traded stock in the market right now. It has implied volatility on the options of 70%, which is really the highest in the market of any individual stock. That just creates immense amounts of trading by options traders, volatility traders, by call writing, and 2x and 3x ETF long and short players. All of the financial engineering and new products that we see all gravitate toward the high volume stocks like Nvidia, Tesla, and Apple because that's where the money is being made. Some days Tesla accounts for 25% of all the market trading. Financial engineers go where the action is, where the volume is, where the customer demand is.

Q: Why do you expect only 5% to 10% corrections if the Fed rate cuts get completely priced out?

A: I don't expect the Fed to keep cutting interest rates. We should get another rate cut this year, and that may be it for the year. If inflation comes back (and of course, all of the new administration’s policies are highly inflationary) it’s just a question of how long it takes for it to hit the system.

Q: Do you believe I should hold all of my municipal bonds (MUB) with 10-year call protection at 4.75%?

A: On a tax-adjusted basis, I would say yes. You know, stock markets may peak and deliver a zero return, and in that situation, muni bonds are very attractive. The nice thing about bonds is that you hold on to maturity—you get 100% of your money back. With stocks, that is not always the case. Stocks you have to trade because the volatility can be tremendous. And in fact, what I do is I keep all of my money in one year Treasury bills. Last time I did this, which was in September, I locked in a one-year return for 5%.

Q: Would you prefer to buy deep in the money and put spreads on top of any rally?

A: Absolutely yes. If this is a real trading year, you not only buy the dips, you sell the rallies. We did almost no real selling last year. We really only did it in June and July because the market essentially went straight up, except for two hickeys. This could be the year of not only call sprints but put spreads as well. You just have to remember to sit down when the music stops playing.

Q: You say buy the dips; what would your dip be in JP Morgan (JPM)?

A: Well lower volatility stocks by definition have smaller drawdowns. JP Morgan (JPM) is one of those, so I'd be very happy to buy a 5% dip in JP Morgan. If it drops more, you double the position on a 10% pullback. Higher volatility stocks like Tesla—I'm really waiting for 10% or 20% corrections. You saw I just bought a 22% correction twice in Tesla with it down 110 points. One of those trades is at max profit right now and the other one has probably made half its money since yesterday. That is the game. The amount of dip you buy is directly related to the volatility of the stock.

Q: Should you let your cash go uninvested?

A: Yes, never let your cash go uninvested just sitting as cash. Your broker will take that money and put it in 90-day T-bills and keep the money for himself. So buy 90-day T-bills as a cash management tool—they're paying about 4.21% right now— and you can always use those as collateral under my positions on margin.

Q: Is Home Depot (HD) a buy on the LA reconstruction story?

A: I would say no, Los Angeles is probably no more than 5% of Home Depot's business—the same with Lowe's (LOW). A single city disaster is not enough to move the stock for more than a few days, and the fact is: Home Depot is mostly dependent on home renovation, which tends not to happen during dead real estate markets because, you know, it takes the flippers out of the market. It really needs lower interest rates to get Home Depot back up to new highs.

Q: Do you expect a big market move at the end of the day when the Fed makes its announcement?

A: The market has basically fully discounted the move on January 28, and if anything happens, there'll probably be a “sell on the news.” So, I expect we could give up a piece of the recent performance on the announcement of the Fed news.

Q: Should we expect trade alerts for LEAPS coming from you?

A: Absolutely, yes. However, LEAPS are something you really only want to do on down moves. If we don't get any, we'll just do the front-month call spreads. You can still make 10%, 20% a month just concentrating on financial call spreads.

Q: What would have happened to our accounts if we kept the (TLT) $82-$85 iShares 20+ Year Treasury Bond ETF (TLT) call spread and it went all the way down to $82?

A: The value of your investment goes to zero. Of course, it was declining at a very slow rate, and the $80: you might have gotten a bounce off the $85 level. But if the inflation number had come in hot, as had all other economic data of the last month, then you could have easily gotten a gap down to $82 and lost your entire investment, because two days is not enough time to expiration to recover that 3-point loss. And that's why I stopped out yesterday.

Q: Didn't David Tepper buy China (FXI)?

A: With both hands last September, yes he did. And my bet is he got out before he got killed. I mean, that's what hedge funds do. He probably got out close to cost, and you likely won't see him promoting China again anytime in the near future.

Q: I have June 530 puts on the S&P 500, should I get rid of them?

A: Yes, I don't see a big crash coming. You probably paid a lot going all the way out to June, and it's probably not worth hanging on to. Put spreads are the better way to go—that cuts your cost by two-thirds and those you only want to put on at market tops.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or JACQUIE'S POST, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 13, 2025

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD or WHAT’S NEXT),

(SPY), (TSLA), (TLT), (GS)