April 27, 2018

Fiat Lux

Featured Trade:

(THURSDAY, JUNE 14, 2018, NEW YORK, NY, GLOBAL STRATEGY LUNCHEON)

(APRIL 25 BIWEEKLY STRATEGY WEBINAR Q&A),

(TLT), (TBT), (GOOGL), (NVDA), (PIN),

(SPY), (C), (AMD), (EEM), (HEDJ)

Featured Trade:

Below please find subscribers Q&A for the Mad Hedge Fund Trader April Global Strategy Webinar with my guest co-host Mike Pisani of Smart Option Trading.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Are you out of Alphabet (GOOGL) and Microsoft (MSFT)?

A. I'm out of Alphabet and I'm in Microsoft, but only for the very short term. I'm waiting for another big meltdown day to go back and buy everything back because I think the FANGs and technology in general are still in a secular bull market.

Q. Are Advanced Micro Devices (AMD) and NVIDIA (NVDA) affected by the underperformance of Bitcoin?

A. They are. Bitcoin has been an important part of the chip story for the last two years because mining, or the creation of bitcoins, creates enormous demand for chips to do the processing. I think selling in bitcoin is over for the time being. You had a $25 billion in capital gains taxes that had to be paid by April 15.

People were paying those bills by selling their bitcoins. That's over now, and bitcoin is rallied about 30% since Tax Day because of that. So, yes, bitcoin is getting so big that it is starting to affect the chip sector meaningfully. That is another reason why we see secular long-term growth in the entire chip sector.

Mike Pisani: Interesting take on bitcoin today, and I've been with you on it. I think the worst of it is over; it's going to go. Today is the largest volume day we've seen on it so far. We're up over 15,500 contracts traded.

Q: If you're 100% cash, is now a good time to commit funds to the equity market?

A. Franz, I would say nein. Absolutely not. 2009 was the time to commit funds to the equity market. If you're 100% cash now I would stay out for the next six months. We may get a good entry point over the summer or the fall. I'll let you know when that happens because I will be jumping back in myself.

But right now, a week ahead of the worst six months of equity investment of the year, I would stay away and do research instead. Read your Mad Hedge Fund Trader letters. Build a list of names that you're going to buy on the next meltdown and practice buying meltdowns with your practice account, which doesn't use real money.

There's a lot of things you can get ready to do for the next leg up in the bull market, but buying right now, NO! I would put that in the category of, "Is it time to start shorting bonds question?" that we got a few minutes ago.

Q: Why did tech stocks sell off when they have great earnings results?

A: It's called, "Buy the rumor, sell the news." So many people already own the stocks and were expecting good earnings that there was no surprise when they were announced. These are some of the most over-owned stocks in history.

Everybody in the world owns them. Many people have multiple weightings in them, so when we enter a high-risk macro environment, which we have now, you want to get rid of the most over-owned stocks. That is exactly why all of these stocks that have had great runs are selling off, even though they have great earnings report.

Q: Are financials a good play here with interest rates rising though 3%?

A. Normally I would say yes. However, the macro background for the general market are so negative they are overwhelming any positive fundamentals specific to individual sectors like banks and stocks like Citigroup (C). By the way, financials all reported great results and got killed, so that is why I bailed out of my (C) position this morning at around cost. If you throw the best news in the world on a stock and it won't go up, it's time to get out of there.

Q: Would an unleveraged inverse ETF like the ProShares Short S&P 500 ETF (SH) be good at a spike even now?

A. Yes, but when I say spike up better expect at least 20 (SPY) points or 1,000 Dow points. All these downside ETFs are great but you've got to get in at the right price. You know as they say in trading school, the profit is always made on the "BUY" and not on the "SELL."

So, if you can get on one of these super spikes up on the short side that is a great trade. So is the ProShares Ultra Short ETF (SDS) if you want to do the 2X leverage short fund. We've recently started doing this every month. We've been shorting (SPY)s and buying (VIX) on every one of these spikes up, and it's been working like a charm.

Q: Here's the best question of the day. Your timing has been perfect says Mary in Chicago, Ill.

A: Well, I'll take that kind of question all day long. Thank you very much. You're too nice to do that.

Q: Richard is asking would you buy an NVIDIA (NVDA) LEAP?

A: I would wait for meltdown days. Remember this is a market that gives you lots of meltdown days. Just wait for the next presidential tweet and you might get another 600-700-point dip in the markets. Those are the days you buy LEAPS. You don't have to get buy writing Trade Alerts like I do. You can just enter a limit order in your account. Put it as a stupidly low level to "BUY" and you may get hit. And that's where you really make the big money in this kind of market.

Q: Is there a good one- or two-month trade in Amazon?

A: Yeah, Paul, with this volatility you can pick a big winner like Amazon and you know to buy the 250-point dips and sell the rallies. These ranges are so wide now that even a beginner can make money. So, I would say you have to wait until after tomorrow on Amazon and let them get their earnings out. We know they're going to be great. They're doing home deliveries now to your car.

Q: Can long bond interest rates go up to 4%, and if that happens what would the market do?

A: Yes, they can go up to 4%, and I expect them to probably do that next year. What will it do to the market? Answer: Cause a bear market and a recession. Is that answer clear enough? My bet is that interest rates cap in this cycle much lower than they did in past cycles, maybe 4%-5%. We have been used to zero cost of money for so long that a move to 4% would be like stabbing somebody in the chest. People are much less able to deal with rising rates than they ever have been in the past, so watch this space.

Q: Should I buy the ProShares Ultra Short Treasury ETF (TBT) or the iShares 20+ Year Treasury Bond Fund (TLT)?

A: Brad, it's really is a leverage question for you. The (TLT) is 1X; the TBT is 2X, so I would be taking profits on the (TBT) here and then buying a couple of points lower. Or if you want to keep it for the long term you can but remember the cost of carry on the TBT is around 7% a year.

Q: Yves in Paris, France is asking: What possible scenario will you see material wage growth that could lead to higher inflation?

A: We're starting to see that now with the ultra-low unemployment rates. People are having great difficulty hiring anyone in technology. But at the minimum wage level there seems to be plenty of supply. The other possibility is that the cost of everything else goes up but wages, because technology is replacing jobs so fast there may never be any increase in wages.

So, we will get inflation, but nothing like the inflation we saw in the past driven by rising wages, commodity prices, oil prices, and interest rates. Yes, money is a commodity, which can add quite a lot to the cost of leveraged companies like airlines, REITs, and so on.

Q: Will rising interest rates force the US dollar up?

A. The answer is yes! It has been a long time coming, but if rates continue to rise from here, you can expect that to lead to a continuously rising dollar and falling foreign currencies, and that will become a major drag on the economy and corporate earnings going forward.

Q: When is a good time to buy TIPS?

A: Just like your Treasury bond short, I would buy Treasury Inflation Protected Securities (TIPS) on the next rally in bond prices (TLT) and dip in yields. That will give you a decent entry point. That said, TIPS have been a horrible performer for the last 10 years because there has just been no inflation. A lot of people just keep TIPS as a hedge in their portfolio and it just costs them money every year.

Q: Which could blow up, Brad wants to know, TBT or TLT?

A: The easy answer there is probably neither. But if I had to pick between the two, the (TBT) would be the one to blow up because it's a 2X and has a lot less liquidity. So, I can't image in what world has (TBT) blowing up, but then I don't watch zombie TV shows either.

Q: I think US equities are expensive. Are emerging markets (EEM) or Europe (HEDJ) a better bet for the rest of the year?

A: I would say yes. Because if interest rates here in the US go higher that means a stronger dollar. That means a weaker US stock market. Because US companies are punished by a rising dollar. And European and Asian companies benefit from a rising dollar and falling home currencies, so that makes Europe the first choice of any of the global markets.

Q: Does oil going to $100 have a chance of bringing down the US economy?

A: Absolutely yes. If oil prices don't start to slow down, they will start having a big impact on the economy because that means rising prices for any energy consumer, which is you and me.

With no ability to offset that by rising prices of your products that would put a squeeze on any oil consuming industry, which is why things like the transports and consumer staples have been performing so poorly. If we get to $100, then you're really looking at a full-on recession and bear market for stocks. By bear market I mean down 25% or more in stocks.

Q: How do you see the India ETF?

A: We like it. India is the No. 1 pick of any hedge fund investor in emerging markets, and the ETF you can buy there is the PowerShares India Portfolio ETF (PIN).

I have been to Greece many times over the past 45 years, and I?ll tell you that I just love the place. The beaches are perfect, the Ouzo wine enticing, and I?ll never say ?No? to a good moussaka.

However, I don?t let Greece dictate my investment strategy.

Greece, in fact, accounts for less than 2% of Europe?s GDP. It is not a storm in a teacup that is going on there, but a storm in a thimble. Greece is really just a full employment contract for financial journalists, who like to throw around big words like bankruptcy, default and contagion.

I have other things to worry about.

In fact, I am starting to come around to the belief that Europe is looking pretty good right here. Cisco (CSCO) CEO, John Chambers, announced that he was seeing the early signs of a turnaround.

Fiat CEO, Sergio Marchionne, the brilliant personal savior of Chrysler during the crash, thinks the beleaguered continent is about to recover from ?hell? to only ?purgatory.?

Only a devout Catholic could come up with such a characterization. But I love Sergio nevertheless because he generously helps me with my Italian pronunciation when we speak (aspirapolvere for vacuum cleaner, really?).

What are the two best performing stock markets since the big ?RISK ON? move started last Thursday? Greece (GREK) (+5%) and Russia (RSX) (+7.5%)!

And here is where I come in with my own 30,000 foot view.

The undisputed lesson of the past five years is that you always want to own stock markets that are about to receive an overdose of quantitative easing.

Since the US Federal Reserve launched their aggressive monetary policy, the S&P 500 (SPY) nearly tripled off the bottom.? Look how well US markets have performed since American QE ended 18 months ago.

Europe has only just barely started QE, and it could run for five more years. Corporations across the pond are about to be force-fed mountains of cash at negative interest rates, much like a goose being fattened for a fine dish of foie gras (only decriminalized in California last year).

Mind you, it could be another year before we get another dose of Euro QE, which is why I just bought the Euro (FXE) for a short-term trade.

A cheaper currency automatically reduces the prices of continental exports, making them more competitive in the international markets, and boosting their economies. Needless to say, this is all great new for stock markets.

Get Europe off the mat, and you can also add 10% to US share prices as well, as the global economy revives. The Euro drag dies and goes to heaven.

Buy the Wisdom Tree International Hedged Equity Fund ETF (HEDJ) down here on dips, which is long a basket of European stocks and short the Euro (FXE). This could be the big performer this year.

Praise the Lord and pass the foie gras!

I noticed last week that Angela Merkel, the Chancellor of Germany, was picked by the editors of Time Magazine as their ?Person of the Year.?

This is creating an outstanding investment opportunity, a real game changer. As a result, Germany?s economy could grow by an extra 1% a year. But more on that later.

She received the accolade for convincing her country to accept 1 million refugees from the Middle East. They will be plopped down in the middle of a population of 80.6 million, so it is a very big deal.

That is like the US taking in 4 million refugees with no notice. The most we took in after the collapse of Vietnam was 125,000.

In addition, she talked her electorate into bailing out Greece, not once, but twice.

I SAY ?THREE CHEERS? FOR GERMANY.

History has really come full circle. After bearing the cross for the holocaust for seven decades, the country carries out one of the greatest humanitarian acts of all time.

I know the Germans well.

I lived in West Berlin during the 1960?s with a former Nazi family. Needless to say, the dinner conversations were interesting. But they loved Americans, for it was we who rescued them from the Russians and Bolshevism in 1945.

I spent my weekends smuggling western newspapers and US dollars into East Berlin to the underground across Checkpoint Charlie. I was too young and dumb to know any better.

When I got caught, I spent a night in a communist jail cell. To this day, the words ?Das ist Verboten? still send a chill down my back. The East German Volkspolizei were not very nice guys.

If you want to see a close approximation of that prison, go watch the just released Stephen Spielberg movie ?Bridge of Spies,? about the Gary Powers exchange. They really nailed the Cold War atmosphere of Berlin during the sixties.

Yes, when I was 16, I used to listen to machine guns mow down fleeing refugees at night. Every time a guard hit someone, they were awarded a gold watch. I lived in Tiergarten, within easy earshot of the Berlin Wall at Brandenburg Gate. And you wonder why I?m such a tough guy.

Angela Merkel has always been an enigma to me. Those of us who know the old East Germany well, find it difficult to imagine anyone intelligent or useful coming from there. To see her leading an essentially conservative country is positively mind blowing.

She is clearly brilliant, with a PhD in physics. She is fluent in Russian, and is in close communication with Vladimir Putin on a regular basis in his own language. She entered politics as soon as the wall came down in 1989, signing up with the conservative Christian Democratic Union.

Today, she is widely considered the de facto leader of Europe. She is also regarded as the most powerful woman in history (at least for another year).

Full Disclosure: During my annual European sojourns, I always spend a day briefing Merkel?s staff in Berlin about the current state of the world. I also attempt to decode the American political scene, which Europeans find an indecipherable mystery, but which has enormous implications for them.

?The Person of the Year? can be a dubious honor, and is defined as the person who most influenced history that year. Aviation pioneer Charles Lindbergh, who first soloed the Atlantic Ocean, was originally picked by Time in 1927.

Adolph Hitler was named in 1938 for peacefully redrawing the map of Europe. The only other Germans so named were Konrad Adenauer in 1953, the country?s postwar leader, and Willy Brandt in 1970, noted for normalizing relations with the Soviet Union and Eastern Europe.

To say that Germany is overwhelmed by the immigrant crisis would be a severe understatement.

Almost every high school gym in the country has been converted to emergency housing. There are shortages of everything, from blankets to clothing and translators.

Medieval Afghan men are showing up with 13-year old brides. The backlash is that the Nazi party is experiencing a resurgence of popularity, not only in Germany, also in the Netherlands, France, and Sweden.

If it weren?t for the commitments of this newsletter, I would be back in Berlin in a heartbeat volunteering my services.

Needless to say, the bill for all of this will be enormous. Germany is really the only country that could afford dispensing so much aid.

One of the reasons it can do so is that it happens to have a spare country at hand. Much of the old East Germany is still empty, its cities depopulated. This is where the new immigrants will eventually be settled.

It is perhaps because Angela is a mathematician that she understands there is an enormous long-term dividend that the country will reap.

Look at the economic growth rates of the US and Europe for the past 50 years, and the continent has always lagged the US by 1% per annum. By opening up the gates to a flood of immigration, Germany can make up this difference. So can the rest of Europe.

The great thing for Germany is that these are not your ordinary political or economic refugees. Much of the Syrian middle class has decamped, bringing their educational and professional skills with them. For the Germans, it is a win-win.

This is not a long-term thing. German GDP growth recently and unexpectedly surged, from a 0.3% to a +1.5% annual rate. Some of this is no doubt due to the European Central Bank?s newly aggressive policy of monetary easing. Massive spending on social services has to also be a factor.

European stocks are already poised to outperform American ones by two to one in 2016, thanks to quantitative easing, the postponement of the Greek crisis, and a generation low in asset prices there. Immigrants could pour the economic gasoline to the fire.

Clearly German stocks are a prime target here, which you can buy through the iShares Germany Fund (EWG), as is Europe in general, with the Wisdom Tree European Hedged Equity Fund (HEDJ). But make sure you hedge out your European currency risk for the short term, as the (HEDJ) does.

A revival of the continental economy will also eventually engineer a recovery in the Euro (FXE), (EUO) against the dollar. Don?t press those shorts too aggressively down here.

The great irony here is that this is all unfolding in Germany while mosque burning and bombing are taking place across the US, and there is talk of closing its border on religious grounds.

It is the sort of thing that happened in Germany in 1938, as my former Berlin hosts would have reminded me.

History is coming full circle a second time.

Good for You Angela

Good for You Angela

ECB president Mario Draghi certainly let go of a lead balloon today.

Instead of announcing a 20 basis point cut in Euro interest rates, we only got 10.

The world blew apart.

The Euro rocketed against the dollar some 3.5% in minutes, the best gain since 2009, and one of the top ten moves of all time for the beleaguered continental currency.

US Treasury bonds crashed, giving up $3, and popping yields from 2.18% to 2.32%. Stocks fell to pieces globally. The Volatility Index (VIX) went through he roof.

Never mind that Draghi announced an extension of European quantitative easing by six more months to March 2017, or that the number of qualified securities for the central bank could buy was expanded.

All traders wanted was one more rally before yearend into which they could unload their sizable Euro shorts. When they didn?t get it, they panicked and stampeded for the exits.

It was your classic flash fire in the movie theater.

This is what happens when positioning in financial markets gets too one-sided. Risk managers talk about too many passengers in one side of the canoe. Everyone gets to go swimming.

That is why I quit rolling down the strikes on my Euro shorts three weeks ago, loathe to sell to much at the bottom. My one remaining short Euro position successfully weathered today?s spike, is still in the money, and only has ten trading until expiration.

The important takeaway here is that today?s moves were entirely technical, and had nothing to do with fundamentals, which always win out over time.

The meteoric move in the Euro did not occur because of a sudden burst of strength in the European economy. It didn?t take place because the ECB is raising rates.

So, I think this entire move is bogus. It is a typical December event, where all of the hot money wants to get out of the market within the next four weeks so they can close their books and start over again next year.

It is also a great lesson on what happens when you have too many hedge fund chasing the same few trades. It always ends in tears.

Which leads me to believe that the dramatic moves we saw today will reverse themselves shortly. Stocks (SPY) will soar, bonds (TLT) will rise modestly, and the Euro (FXE), (EUO) will take the express train downtown. The (VIX) will fade, again.

These gyrations could possibly take place as soon as Friday?s November nonfarm payroll report. All we need is a number north of 200,000, and it will be off to the raises once again.

I am so convinced of my convictions that I bought the Velocity Shares Daily Inverse VIX ETF (XIV) 30 minutes before the close (that?s the latest I can send out a Trade Alert and expect readers to have time to open and execute).

USE THE HEDGE FUNDS? PAIN FOR YOUR GAIN!

If you still hold a Euro short, keep it.

If you are underweight stocks, here is another fine entry point.

This is especially true for hedged European stocks (HEDJ), which have just opened an excellent entry point.

The (SPY) is only down 2.1% from its recent high, and off 3.7% from its all time high, hardly the stuff of bear markets, or even corrections.

Surprise!

Surprise!

You wanted clarity in understanding the current state of play in the global financial markets? Here?s your #$%&*#!! clarity.

You should expect nothing less for this ridiculously expensive service of mine.

But maybe that is the cabin fever talking, now that I have been cooped up in my Tahoe lakefront estate for a week, engaging in deep research and grinding out the Trade Alerts, devoid of any human contact whatsoever.

Or, maybe it?s the high altitude.

I did have one visitor.

A black bear broke into my trash cans last light and spread garbage all over the back yard. He then left his calling card, a giant poop, in my parking space.

Judging by the size of the turds, I would say he was at least 600 pounds. This is why you never take out the trash at night in the High Sierras.

Ah, the delights of Mother Nature!

We certainly live in a confusing, topsy-turvy, tear your hair out world this year. Good news is bad news, bad news worse, and no news the worst of all.

The biggest under performing week of the year for stocks is then followed by the best. Net net, we are absolutely at a zero movement, and lots of clients complaining about poor returns on their investment.

I tallied the year-on-year performance of every major assets class and this is what I found.

+16% - Hedged Japanese Stocks (DXJ)

+15% - Hedged European stocks (HEDJ)

+13% - US dollar basket (UUP)

+10% - My house

0% - Stocks (SPY)

0% -? bonds (TLT)

-5% - Japanese Yen (FXY)

-11% - Euro (FXE)

-12% - Gold (GLD)

-18% -? Oil (USO)

-27% -? Commodities (CU)

-27% - Natural Gas (UNG)

There are some sobering conclusions to be drawn from these numbers.

There were very few opportunities to make money this year. If you were short energy, commodities, and foreign currencies, you did very well.

Followers of the Mad hedge Fund Trader can?t help but know and love these ticker symbols. They?ll notice that our long plays were found among the asset classes with the best performance, while our short bets populated the losers.

The problem with that is most financial advisors are not permitted to place client funds in the sort of inverse or leveraged ETF?s that most benefit from these kinds of moves (like the (YCS), (EUO), and (DUG)).

That left them reading about the success of others in the newspapers, even when they knew these trends were unfolding (through reading this letter).

How frustrating is that?

What was one of my best investments of 2015?

My San Francisco home, which has the additional benefit in that I get to live in it, have a place to stash all my junk, and claim big tax deductions (depreciated home office space, business use of phone, blah, blah, blah).

Of course, I do have the advantage of living in the middle of one of the greatest technology and IPO booms of all time. Every time one of these ?sharing? companies goes public, the value of my home rises by a few hundred grand.

The real problem here is that investing since the end of the Federal Reserve?s quantitative easing program ended a year ago has become a real uphill battle.

While the government was adding $3.9 trillion in funds to the economy we traders enjoyed one of the greatest free lunches of all time. It made us all look like freakin? geniuses!

Just maintaining their present $3.9 trillion balance sheet, not adding to it, has left almost every asset class dead in the water.

Heaven help us if they ever try to unwind some of that debt!

Janet has promised me that she isn?t going to engage in such monetary suicide.

The Fed is continuing with Ben Bernanke?s plan to run all of their Treasury bond holdings into expiration, even if it takes a decade to achieve this. And with deflation accelerating (see charts below), the need for such a desperate action is remote.

Still, one has to ponder the potential implications.

It all kind of makes my own 43% Trade Alert gain in 2015 look pretty good. But I don?t want to boast too much. That tends to invite bad luck and losses, which I would much rather avoid.

What! No QE?

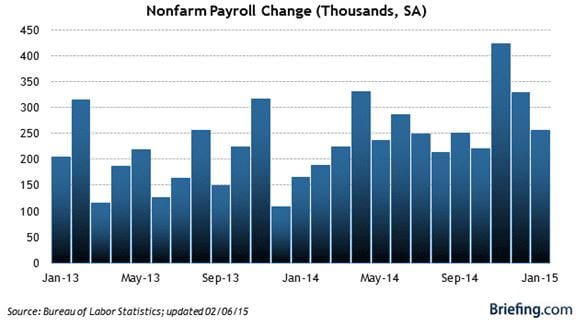

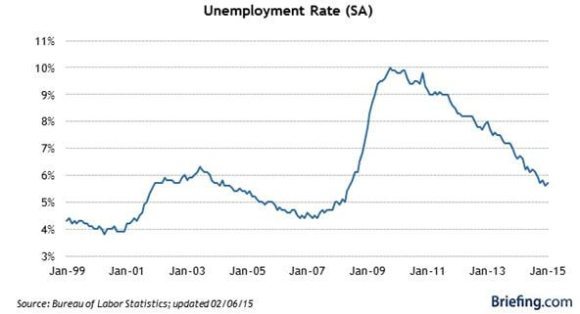

Economists were blown away by the January nonfarm payroll numbers, announced on Friday.

Some 257,000 jobs were added the previous month, holding the headline unemployment figure at 5.7%. Far more important were the revisions for earlier months, which saw December increased to a robust 329,000 and November bumped up to a breathtaking 423,000.

These numbers are almost back to ?normal.? Are ?normal? interest rates to follow?

All told, the January report, the revisions and the additions to the work force means that 703,000 jobs were added to the economy, taking the year on year increase to a positively boom time 3 million. The last quarter has seen the fastest jobs growth rate since 1997. Yikes!

A major part of the new jobs were in retail, proof that our windfall tax cut in the form of falling gasoline prices is finally kicking in.

Needless to say, this is all a bit of a game changer.

It totally vindicates the high-end forecasts for the US economy of 3% plus I made in my New Year forecasts (click here for my ?2015 Annual Asset Class Review?).

The data confirms my thesis that investors are substantially underestimating the strength of the US economy. Furthermore, they have yet to understand the enormously positive impact of cheap energy prices.

It also means that the bull market in stocks is alive and well. It is only resting.

To understand why, let me highlight the major points brought to the fore by the Bureau of Labor Statistics report.

1) The US Economy Has Entered a Self Sustaining Recovery

The trend line for many economic data points are now moving so convincingly upward that they can no longer be treated as statistical anomalies. Nor can they be ascribed to temporary artificial overstimulation by the Federal Reserve in the form of quantitative easing.

Count on Treasury Secretary, Jack Lew, to announce ?mission accomplished? when he address congress later on this week (click here for my one-on-one with Jack, ?Riding With the Treasury Secretary?).

My bet is that this is not our last blockbuster revision. Next to come will be the Q4 GDP, from the just reported flaccid 2.6% annual rate back towards the red hot 5% seen in Q3.

2) The Date for the Next Fed Rate Hike has Been Moved Up

The bond market certainly believed this last week, giving up 9 full points in a couple of days, taking yields from 2.62% to 2.92% in a heartbeat.

I still think this is a 2016 story. The pernicious effects of deflation are still advancing, not retreating, and are not exactly an argument for raising interest rates. But there is no doubt that the desire among the Fed governors to return rates to normal levels is growing, especially if the impact on the economy will be minimal. So call the next rate rise an early, rather than a later, 2016 eventuality.

3) The Strong Dollar is Becoming a Factor With Earnings

The Euro (FXE) has depreciated 31% against the dollar from its 2008 peak, and the yen (FXY) 38% from its 2011 apex. Yet the impact on corporate earnings so far has been marginal at best.

Where will it really start to hurt?

When these currencies approach my final targets of 87 cents and 150, or down another 22% and 18%. It is safe to say that a strong dollar will command an increasing amount of our attention going forward.

This is the argument for investing in small cap US stocks (IWM), where the currency exposure is minimal. Hedge European (HEDJ) and Japanese (DXJ) stocks start to look pretty good too.

4) Wages May Finally Be Rising

The biggest structural impediment facing the US economy has been wage inequality, where virtually all of the benefits of growth accrue to the risk investors of the 1% at the expense of the working class. Hyper accelerating technology and dreadfully imbalanced tax policies are to blame.

January brought us an increase in wages that was miniscule, incremental and modest at best, but it was an increase nonetheless. Average hourly earnings fell by 5 cents in December and then rose by 12 cents the following month.

If this continues, consumer spending will see a big revival, giving us yet another leg to a rising stock market, and creating a win-win situation for all.

One can only hope.

5) More Americans Are Looking for Work

The really amazing thing about the January numbers that they occurred in the face of a large increase in the work force. The participation rate, which has been plummeting for a decade, rose smartly. Long-term U-6 unemployment stayed high, but is down a quarter from peak levels.

To me, this is all a warm up for my ?Golden Age? in the 2020?s. The best is yet to come.

Suddenly, the Line is Getting Shorter

When a rogue element of Ukrainian separatists used a heavy antiaircraft battery supplied by the Russians to shoot down Malaysian Airlines flight 17, who knew that it would send the European bond market into turmoil?

Yet, that is exactly what happened.

German and French ten-year bond yields have hit 300 year lows at around 1.12% and 1.50%. They achieved 500-year lows in the Netherlands, only because it has the longest record for publicly trading debt (the Dutch East India Company was a big borrower to colonize Asia).

Spanish government debt is now trading at higher prices than equivalent US debt. Perish the thought! Weren?t they supposed to be bankrupt?

Yet, the ultra low Japanese levels of interest rates now found on the continent are justified by the new pall cast upon the European economy.

The first round of sanctions imposed by the European Community on Russia a few months ago were little more than symbolic gestures. Close friends of Putin saw bank accounts frozen, and invitations to international gatherings rescinded. Putin could easily afford to laugh them off.

Not so with the second round, which officials have dubbed ?Sanctions 2.5?. The Europeans are taking the Malaysian Air incident personally, as the great majority of the 295 victims were theirs, primarily from Holland. Restricting access to the crash site has only made the pain greater and Russian obtuseness more offensive.

Russian banks have been barred from the European capital markets, greatly increasing their cost of funds. There is a new ban on military contracts, although existing deals are grandfathered, such as France?s sale of two ultra modern helicopter carriers for $4 billion.

Sitting in Europe as I write this, I am inundated by news of the adverse effects of the New Cold War on the European economy. Germany, alone, has 300,000 jobs dependent on trade with Russia, which is a major buyer of industrial machinery and automobiles.

Unfortunately, the timing for all of this couldn?t be worse. It is happening just as the economic data was showing glimmers of a nascent, but sustainable recovery. Look no further than the Euro (FXE), (EUO) which has greatly accelerated its collapse against the US dollar.

Europe has also become hugely dependent on Russia for energy, particularly natural gas. Putin has already used his energy weapon on the Europeans over a contract dispute, arbitrarily cutting off supplies during one of the coldest winters on record.

The problem is that this is not a challenge that can be dealt with easily. On paper, the US could supply a substantial portion of Europe?s energy needs with its newfound windfall from fracked natural gas (UNG).

However, anyone in the energy industry will tell you that installing the needed infrastructure is at least a 20-year job, and maybe ten years if you put it on a military footing.

The new sanctions were instrumental in the announcement of a major expansion of fracking in Europe, which until now has been held back by environmental concerns. The coal bearing areas of Germany, Poland, and France have the perfect geology for fracking, which will enable the continent to become energy independent.

But again, we are talking about very long timelines. This is another reason why US fracking stocks, like USA Compression Partners (USAS), Nuverra Environmental Solutions (NES), and US Silica Holdings (SLCA), have been on a tear.

The late President Ronald Reagan must be laughing in his grave. When I was a young White House correspondent, his administration fought the energy deals Europe was negotiating with Russia tooth and nail.

In the end, the Europeans ignored the ?Gipper,? wary of his conservative, saber rattling, Cold War rhetoric. The headache is that the EC is now in so deep with Russia, recently describing it as a ?strategic partner,? that it can only extricate itself at great cost.

The US cannot just sit back and laugh this off with a giant ?I told you so.? The collapse in bond yields has been a global affair, dragging our interest rates down to one year lows at 2.45% for ten year Treasury bonds, and 3.24% for the 30 year.

At the very least, it postpones a major switch by American investors out of bonds and into stocks that was imminent. It also hits American companies, that until recently have been cashing in on new trade with Russia. Who is the biggest casualty? Exxon (XOM), which has several ongoing projects to modernize Russian oil production.

Sanctions 3.0 could be worse, if Putin doesn?t get the message. The US Treasury is prepared to ban Russia from global US dollar clearing if it doesn?t back off from the Ukraine. Trying selling 10.5 million barrels a day of oil without using the greenback.

What could they accept in return other than the buck? Gold? North Korean Won? Chinese Renminbi? The collapse of the Russian economy would be total and absolute, not that anyone cares. Its GDP is only $2 trillion, 3% of the world total, and they have an even smaller share of international trade.

Fortunately, I have been able to dance between the raindrops with my Trade Alert service. I have been marginally caught out by premature short positions in the Treasury bond market (TLT), (TBT).

But so far, these losses have been offset by my aggressive shorts in the Euro, which has been cratering, thanks to ECB president Mario Draghi?s new found belief in quantitative easing. Breaking even when a flock of ?black swans? descends upon you is a ?win? in my book.

It?s a classic example of, ?The harder I work, the luckier I get.?

Grandfathered

Grandfathered

The stock markets are on the verge of a small correction, perhaps less than 5%, which should unfold over the next six weeks.

There is just not enough juice in a mini crisis triggered by one lousy Portuguese bank, the Banco Espiritu Santo, to take us any further. Bonds globally should put in their highs for the year during this period.

After that, it will be off to the races with a major year-end rally that could take us up another 10%. Both old tech and new tech, plus biotech and social media will be the front runners in this next leg of the bull market. Fixed income products will suffer across the board.

These were the results of the exhaustive research Jim undertakes every quarter using his proprietary analytical system. His goal is to define the best long and short opportunities across all asset classes.

Ignore him at your peril. Last year Jim?s system delivered a gob smacking trading return of over 300%.

Jim, a 40-year veteran of the trading pits in Chicago, would tell you all this himself. But as he is a product of the Windy City?s lamentable school district, the task of translating his pivot points, swing counts, and support and resistance levels into simple ?BUYS? and ?SELLS? falls to me.

What else can I say?

By the way, a pivot point is a number Jim?s system serves up once a quarter dictating the tone of the market for individual securities. Trade above the pivot, and we are in ?RISK ON? mode. Trade below it, and we need to take a decidedly ?RISK OFF? posture.

Swing counts then project the distance a security should travel once the directional call has been determined. Think of it as your own private inertial navigation system for your trading approach.

Equities

With that said, Jim?s pivot for the S&P 500 for Q3 is 1,970. As we are well below that now, you can expect some further work to be done on the downside, possibly as low at the 1,875-1,895 range over the next six weeks.?That would then be a sweet spot to initiate new longs.

The NASDAQ 100 has a pivot of 3,811 for Q3, a few percent above here. Jump back into the technology arena with a tight stop in the 3,700-3,725 neighborhood, or down some 5%, which works out to around $90 for ETF (QQQ) players.

Among foreign markets, Jim likes Japan?s Nikkei (DXJ), is wary of the German DAX, and is neutral on Australia (EWA).

Point a gun to his head, and Jim will opt for the Wisdom Tree Europe Hedged Equity Fund (HEDJ), a customized long European equity/short Euro ETF that effectively prices these stocks in US dollars. Think of it as a (DXJ) with a French accent.

?Bonds

Jim sees a rare, generational opportunity, to sell bonds setting up for August. They could grind up until then off the back of today?s news from Europe, but not by much. Use $137.00 as the pivot point for the 30-year bonds futures.

The market?s Focus will remain on the SPX/Bond spread, as it has all year. When the Equity Indices go into profit taking mode, bonds are the only place to park money, taking prices northward.

Long term, he favors the short side of the bond market, when conditions allow.?His game plan remains to sell bonds at these levels, with tight stops, until proven wrong.

My own strategy of buying out of the money (TLT) put spreads on a monthly basis also works perfectly in this scenario. Use every three-point rally as an opportunity to get in.

We are on the threshold of a more normalized interest rate environment, with a long awaited reversion to the mean in rates imminent. Jim says that the entire bond world is about to roll over.

Foreign Currencies

Jim isn?t getting too excited about foreign currencies these days, which appear to have fallen into a bottomless volatility trap. He doesn?t see any big moves unless a serious risk off trend develops in the equity markets, which is unlikely.

Use the Australian dollar (FXA) as your lead currency with which to make directional calls for the entire asset class. The pivot there is $94.60 in the cash market. As we are now at $93.68, stand aside.

The Japanese yen (FXY) has done its best impression of a Kansas horizon this year of any financial asset. It will continue to flat line as long as the jury is out on Prime Minister Shinzo Abe?s ?third arrow? economic and reform strategy. The yen will eventually weaken against the greenback, but it could be a long wait. Until then, use 101.33 as a pivot.

If you have to hate a currency in 2014, make it the Euro (FXE), with a pivot of $139.50. Sell every rally against this figure until the cows come home. The fundamentals for a weaker continental currency are building by the day. But we won?t see real fireworks until we close below $135.50. Then we?ll be targeting $127.50.

Commodities

Jim likes the precious metals (GLD), (SLV) and thinks the recent bottom will last for some time. This is further confirmed by the miners (GDX), which appear to have staged a major turnaround.

Bond market rallies have been highly correlated to metals rallies this year, at least for over the short term. So follow the sparkly stuff along with a bond rally into August. Lower rates will be price positive the metals. Use $1,265-$1,275 as your pivot for gold going forward. For silver use $19.70.

Copper (CU) is a bit of a conundrum, as it is stuck, in the middle of one-year range, so don?t chase recent rally. Use $2.95 as the pivot there. It?s not going anywhere until China decides what to do with its economy.

Don?t buy into the upside breakout school of thought for oil (USO) until we close over 104.70-105.30 (last qtr's high). That?s where you can count on the buy stops to kick in. At the current $102, we are firmly in bear territory. Talk to Jim when oil breaks this quarter?s resistance and upside momentum level at 107.50.

Infrastructures plays are still the best way to participate in any move in the natural gas (UNG) market. At the top of the list is Mad Hedge Fund Trader long time favorite, Cheniere Energy (LNG), up from $6 to $74.??(LNG) should be on your shopping list on any big equity index sell-off.?This week may see a low, and then a substantial rally when July futures expire.

The Ags

Agricultural commodities (CORN), (SOYB), (WEAT), (DBA) have been the major disaster area of 2014, thanks to the best growing conditions in history. Not only has the weather been perfect, the US Department of Agriculture keeps ?finding? new stockpiles. Conditions have been improving in major export markets abroad, as well.

Farmers may get a break this week when multiple futures contracts expire. At the very least, we should get a dead cat bounce. After that, it?s up to Mother Nature.

By the way, Jim Parker?s Mad Day Trader service has attracted a substantial following over the past year. If you are not already getting Jim?s dynamite short term ?BUY? and ?SELL? calls, please get yourself the unfair advantage you deserve.

Just email Nancy in customer support at support@madhedgefundtrader.com and ask for the $1,500 a year upgrade from your existing Global Trading Dispatch service to Mad Hedge Fund Trader PRO. The service includes Jim?s timely Trade Alerts, a running daily market commentary, and the daily morning webinar, The Opening Bell with Jim Parker.

The Quarterly Calls Are In

The Quarterly Calls Are In