Featured Trade:

(MY UPDATED PERSONAL ECONOMIC INDICATOR),

(HMC), (NSANY), (GM), (F), (TSLA) (HERE IS YOUR TOP PERFORMING INVESTMENT FOR THE NEXT FIVE YEARS),

(ITB), (PHM), (KBH), (DHI)

(TESTIMONIAL)

There is no limit to my desire to get an early and accurate read on the US economy, which at the end of the day is what dictates the future of all of our trades and investments.

I flew over one of my favorite leading economic indicators only last weekend at the controls of a vintage Cessna 172.

Honda (HMC) and Nissan (NSANY) import millions of cars each year through their Benicia, California facilities, where they are loaded onto thousands of rail cars for shipment to points inland as far as Chicago.

In 2009, when the US car market shrank to an annualized 8.5 million units, I flew over the site and it was choked with thousands of cars parked bumper to bumper, rusting in the blazing sun, bereft of buyers.

Then, “cash for clunkers” hit (remember that?).

The lots were emptied in a matter of weeks, with mile-long trains lumbering inland, only stopping to add extra engines to get over the High Sierras at Donner Pass.

The stock market took off like a rocket, with the auto companies leading.

I flew over the site last weekend, and guess what?

The lots are empty.

U.S. new vehicle sales, including retail and non-retail transactions, are estimated to reach 1,354,600 units in August, a 15.4% jump from a year earlier, according to the joint report by J.D. Power and GlobalData. Consumers are estimated to spend $47.8 billion on new vehicles, the highest on record for the month of August, and 10.5% higher than last year, the report said.

Japanese cars are suddenly selling so fast that vehicles are being sold even before they land on the dock.

It is all further evidence that my increasingly optimistic view on the US economy is correct, that multiple crises this year are fully discounted, and that the stock market is poised for new highs.

The conventional auto industry should lead to the upside, as it has already done, led by General Motors (GM) and Ford (F). But the move may not happen until the second half of 2024 when the market’s love affair with big tech stocks reaches the point of temporary exhaustion.

As for Tesla (TSLA), better to buy the car than the stock at these depressed prices. Once the EV price wars end, the stock should double again to new all-time highs.

This is a big deal because the auto industry directly and indirectly accounts for about 10% of the total US economy.

It is also the largest manufacturing employer, with the legacy Big Three accounting for 6 million jobs, 4.87% of the 124 million US total.

Not only do you have to include the big four automakers, but you also must include the vast number of parts suppliers, advertisers, and the national dealer networks.

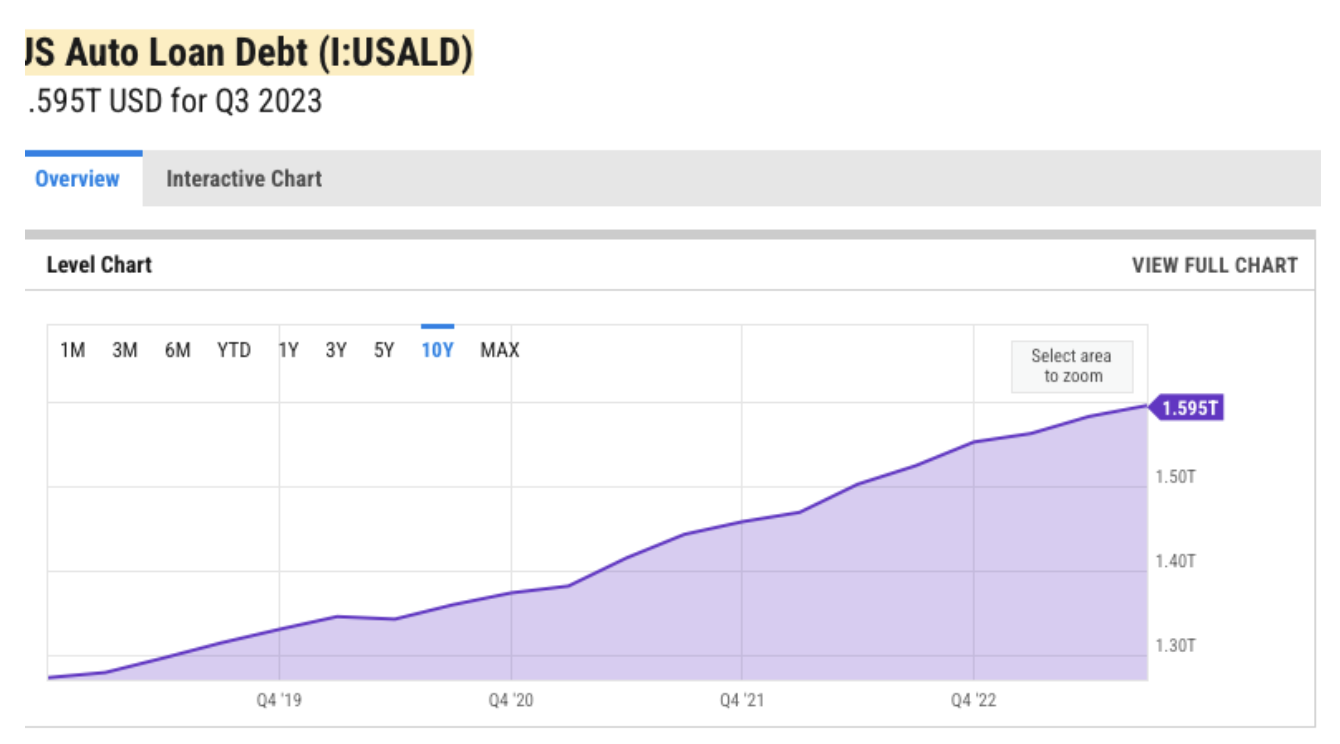

Since so many car purchases are financed with loans, it turns out that the industry is a great play on falling interest rates.

There are $1.6 trillion in subprime auto loans on lenders’ books now.

If you don’t believe me, check out the resale market price of your wheels at Kelly Blue Book (click here for the site)

You will see they have recently risen steadily in value.

It is all further evidence of the hard data/soft data conundrum, which I have written about extensively in the past.

Look no further than Consumer Sentiment, which has held up remarkably well for the past three consecutive months.

Sorry the photo below is a little crooked, but it's tough holding a camera in one hand and a plane's stick with the other, while flying through the never-ending turbulence of the San Francisco Bay’s Carquinez Straight.

Air traffic control at nearby Travis Air Force Base usually has a heart attack when I conduct my research in this way, with a few joyriding C-130s having more than one near miss in recent years.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/10/Honda-Car-Lot.jpg181603Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-11-24 09:06:002023-11-24 12:08:16My Updated Personal Leading Economic Indicator

I have been in the much-talked-about and often despised 1% for most of my adult life.

I started my relentless march towards wealth and financial independence when I was 11 years old and landed a job delivering newspapers for the Los Angeles Herald Examiner, an old Hearst rag, earning $30 a month.

I’ll never forget the weight of 30 pounds of newsprint on my shoulders as I delivered them around my neighborhood in the dark on my Schwinn bicycle.

I eventually got fired because I found the stock pages so enthralling that I was always late delivering the papers. The Herald was run out of business by the Los Angeles Times in 1989.

My next step towards success came with a job in the snack bar at the May Company, a Los Angeles department store that also no longer exists, earning the untold sum of $1 an hour, then the minimum wage.

The really smart thing I did there was that whenever a customer paid for a hot dog with a 40% pure Kennedy silver half dollar, which in 1967 was still in widespread circulation, I would switch it for paper money.

Eventually, I accumulated 100 of these half dollars.

At age 15, I was willing to bet that someday the US would go off the gold standard and all precious metals would rise in value.

President Nixon did exactly that in 1971, and the value of my stash rose 100-fold to $5,000.

I still have those silver half dollars. I understand that Texas hedge fund manager Kyle Bass owns the rest.

I finally made it into the 1% when I was 33, after spending two years at Morgan Stanley. By then, my pay there had rocketed from an entry level $45,000 to $300,000 a year.

It helped that I won the betting pool for picking the best performing stock in the world two years running.

Back then, nobody had ever heard of an obscure electronics company in Japan called Sony (SNE) which rose in value 85-fold in dollar terms over the following seven years.

Nor had they heard of Honda Motors (HMC). When the other traders saw their little eggshell shaped cars for the first time, they laughed.

The pitiful vehicles had to make a high-speed run to make it to the top of an American freeway onramp. Its shares rose 45 times in dollar terms.

This was back when $300,000 could buy you a luxury two-bedroom condo on the 34th floor on the upper east side of Manhattan. That is exactly what I did, right next door to corporate raider Carl Icahn, and across the street from Henry Kissinger and Ginger Rogers.

A London mansion followed, located between other homes owned by Jacob Rothschild and Sir Richard Branson.

After a few more years at Morgan Stanley, and then founding the first-ever dedicated international hedge fund, I soon found myself in the much-vaunted 1/10th of the top 1% of American earners.

I stayed there for quite a while.

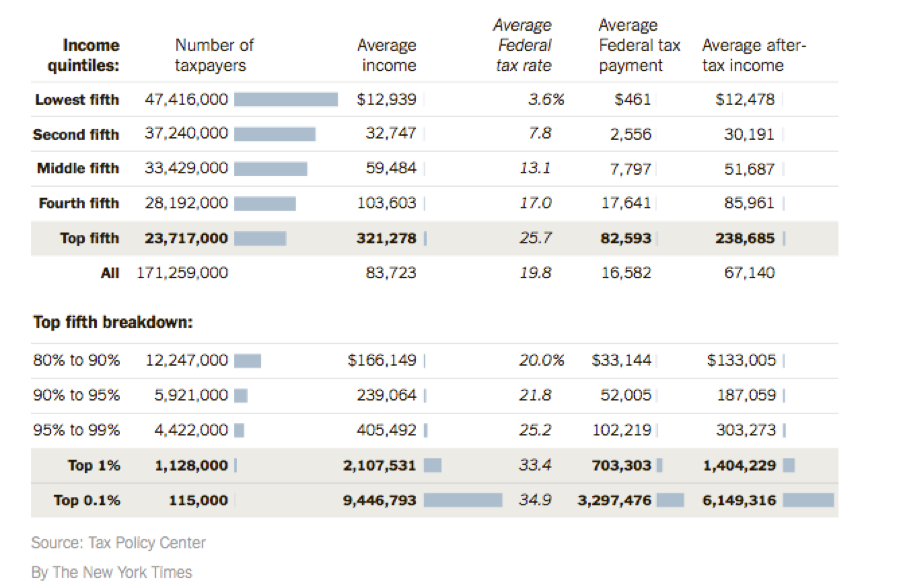

However, I recently got the bad news from the New York Times that I have been kicked out of the top tier.

According to their research, to prove I have grabbed the brass ring, I have to have an average annual income of $9,446,793. Only 115,000 taxpayers can meet this elevated standard.

I am still in the top 1%, where I only need to earn $2,107,531 to qualify and can remain with my 1,128,000 friends.

My Brioni suits, Turnbull & Asser Sea Island Silk shirts, and Bruno Magli shoes will not be found for sale on eBay anytime soon.

Which left me to ponder why I had lost my position at the apex of US earning power.

It turns out that the concentration of wealth at the top has vastly accelerated since the stock market bottomed in March 2009.

Risk takers, like those who owned stocks, bonds, and real estate, were tremendously rewarded by the recovery of asset prices.

Those who don’t own any assets, about 40% of the country, were left behind in the dust.

So, the low tax leveraged longs, like those running big hedge and private equity funds, started to greatly outpace my own earning power.

Concentrating so much wealth at the top is a problem for the United States. As any financial advisor can tell you, the richer people become, the more conservative they get with their investments.

Eventually, it all ends up in the bond market, where positions are never sold to avoid paying taxes. In other words, it stagnates and is one of the causes of our present low 2.5% GDP growth rate.

It is also where the 1.46% ten-year Treasury bond (TLT) comes from.

It is usually NOT placed with higher risk, job-creating, equity type investments. For more on this, click here for “The Bond Market and the 1%”.

This always happens when you have a big bulge generation retire all at once, like the 85 million baby boomers.

Another reason I lost my guarantee of the best table in every restaurant I walk into is that I am paying a lot more in taxes than I used to.

This is because I shifted careers from the hedge fund business, where I paid a bargain 15% tax rate on my realized carried interest, to the newsletter game where I am tagged for a heart-rending 43.4%, including the Obamacare add on.

As a result, I pay more in taxes in a single year than most people earn in a lifetime. In other words, for the first time in my life, I am paying taxes like everyone else.

Ouch, and double ouch!

Want to know why I am so interested in what happens in Washington? BECAUSE IT’S MY MONEY THEY’RE SPENDING!

It is also why I have come to learn so much about our arcane and abstruse tax system, and how I am able to periodically pass on insights to you.

I have to pay my accountants tens of thousands of dollars to ferret this stuff out, for your benefit.

When I had dinner with former Federal Reserve Chairman Ben Bernanke, he told me that “rising income inequality is the biggest structural problem we face.”

To find out where you stand in the country’s multi-tiered income structure, I have reproduced the New York Times data below.

Who has seen the greatest accumulation of wealth since the 2009 low? The Koch Brothers, whose combined net worth has soared from $26 billion to $90 billion since then.

Go Figure.

For one more piece on the 1%, please click here for “Mixing With the 1% at Pebble Beach”.

These days, I get to download my papers on my iPad every morning no matter where I am in the world, which then update themselves throughout the day.

I now get up even earlier than when I delivered the papers by bike.

Come to think of it, that “Horatio Alger Effect” that Ben Bernanke mentioned to me over dinner the other day applies to me as well.

I bet it has worked for a lot of you too.

Being a Hedge Fund Manager Did Have Its Advantages

https://www.madhedgefundtrader.com/wp-content/uploads/2015/10/Man-Money.jpg393330MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-09-04 04:04:202019-10-14 09:46:01Are You in the 1%?

Featured Trade:

(I HAVE AN OPENING FOR THE MAD HEDGE FUND TRADER CONCIERGE SERVICE), (DON’T MISS THE AUGUST 7 GLOBAL STRATEGY WEBINAR), (HAVE WE SEEN “PEAK AUTO SALES”),

(GM), (TM), (F), (HMC), (TSLA), (NSANY),

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-08-06 01:08:412019-08-05 17:35:33August 6, 2019

There is no limit to my desire to get an early and accurate read on the US economy, which at the end of the day is what dictates the future returns on our investments.

I flew over one of my favorite leading economic indicators only last week.

Honda (HMC) and Nissan (NSANY) import millions of cars each year through their Benicia, California facilities where they are loaded on to hundreds of rail cars for shipment to points inland as far as Chicago.

In 2009, when the US car market shrank to an annualized 8.5 million units, I flew over the site and it was choked with thousands of cars parked bumper to bumper in their white plastic wrappings, rusting in the blazing sun and bereft of buyers.

Then, “cash for clunkers” hit (remember that?). The lots were emptied in a matter of weeks, with mile-long trains lumbering inland, only stopping to add extra engines to get over the High Sierras at Donner Pass. The stock market took off like a rocket, with the auto companies leading.

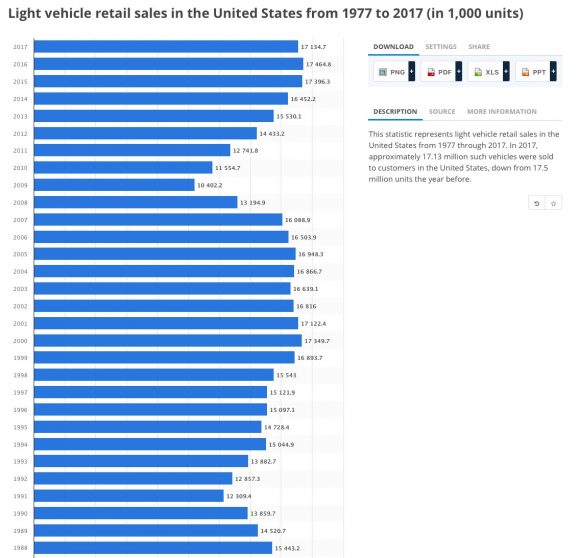

I flew over the site last weekend, and guess what? The lots are full again. Not only that, the trains lined up to take them away are gone. US Auto Sales peaked in October 2017 when they fell just short of a 19 million annualized rate. As of the end of June this year, they had fallen to a 15.1 million annualized rate. July is looking worse still.

And this is what I’m worried about. Auto Sales may not only be peaking for this economic cycle. They may be peaking for all time.

This is my logic.

As they slowly age, Millennials are about to become the principal buyers of automobiles. The problem is that Millennials are purchasing cars at a far slower rate than previous generations.

This is because they have a much higher concentration in urban areas where the cost of car ownership is the most expensive in history. $40 for parking for an evening? Give me a break. But good luck finding free on-street parking, and if you do, your windows will probably get smashed.

In cities like San Francisco, public transportation, bicycles, and electric scooters are the preferred mode of transportation.

It doesn’t help that this generation is shouldering the burden of the bulk of $1.5 trillion in student loan debt. When you owe $2,000 a month in interest, there is little room for a car payment, and you probably don’t have the credit rating to buy a car anyway.

When they do buy cars, all-electric is their first choice, if they can get access to overnight charging. A lot of companies are making this easy by offering free charging for electric commuters in corporate parking lots. This explains why Tesla (TSLA) has taken deposits from 400,000 for their low-end Tesla 3, which has a two-year waiting list for new buyers.

When Millennials do drive, such as on business, for weekend trips or summer vacations, they either rent or “share.” Driving around the city, you see cars parked everywhere with bizarre names like Upshift, Getaround, Zipcar, Turo, and Casual Carpool.

Indeed, Detroit takes the car-sharing threat so seriously that the Big Three have all bought into the technology, with General Motors taking a stake in Maven. (GM) plans to start its own peer-to-peer car-sharing service this summer.

This is all a mystery for my generation, which grew up tearing apart old cars and putting them back together. I spent a year trying to put the engine on my 1955 Volkswagen back together. When I gave up, I towed the car and a big box full of greasy parts to a local mechanic, a German Army veteran. When he finished, even he had four parts left over.

Do you know who believes my rash, possible MAD theory? Investors in auto stocks, one of the worst-performing sectors of the stock market this year. Shares like those of General Motors (GM) keep breaking new valuation lows.

What was (GM)’s price earnings multiple today? Try a miserable zero since the company loses money, one of the lowest of all S&P 500 stocks. Hapless portfolio managers keep getting sucked into the shares, which have become one of the ultimate value traps.

It is all further evidence that my cautious view on the US economy is correct, that multiple crises overseas are ahead of us, and that the stock market could drop 5%-10% at any time. The auto industry should lead the charge to the downside, especially General Motors (GM) and Ford (F).

As for Tesla (TSLA), better to buy the car than the stock.

Sorry, the photo is a little crooked, but it's tough holding a camera in one hand and a plane's stick with the other while flying through the turbulence of the San Francisco Bay’s Carquinez Straight.

Air traffic control at nearby Travis Air Force base usually has a heart attack when I conduct my research in this way, with a few joyriding C-130s having more than one near miss.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/tesla.png222745MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-08-06 01:02:192019-09-04 13:22:00Have We Seen “Peak Auto Sales”?

Featured Trade: (MONDAY, JUNE 11, 2018, FORT WORTH, TEXAS, GLOBAL STRATEGY LUNCHEON), (ARE WE SEEING "PEAK AUTO SALES"?), (GM), (TM), (F), (HMC), (TSLA) (NSANY), (TESTIMONIAL)

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.