Mad Hedge Technology Letter

September 23, 2022

Fiat Lux

Featured Trade:

(CORPORATE TECH NOTCHES ANOTHER WIN)

(HOOD), (SEC), (VIRT), (SEC), (HFT)

Mad Hedge Technology Letter

September 23, 2022

Fiat Lux

Featured Trade:

(CORPORATE TECH NOTCHES ANOTHER WIN)

(HOOD), (SEC), (VIRT), (SEC), (HFT)

The US Securities and Exchange Commission (SEC) will stop short of banning payment for order flow, which is essentially high-frequency trading (HFT) firms buying the trading history of retail traders.

I believe this was a huge mistake because it inserts an unneeded middleman between the trader and his profits while raising the costs to the trader.

Why do HFT want the trading history in the first place?

They have algorithms built in place that reveals trends in the data allowing them to profit off it.

I guess one might be able to argue that this could also lead to big losses if algorithms are built wrong.

However, much of the time, the profits are risk free by front running the retail traders’ orders by buying and selling in the microsecond after the retail trader clicks buy and receiving the shares.

The outcome is earning a few pennies.

However, multiply that over million and billions of trades each year and that is why CEO of Citadel Ken Griffin has a net worth of over $30 billion and the Founder and Chairman of Virtu Financial (VIRT) Vincent Viola owns the NHL’s Florida Panthers.

Risk free trades work 100% of the time so their trades are never exposed to losses.

Granted, they had to build out the tech expertise and technological infrastructure to pull it off.

In the end, US regulators have been quite tight lipped on what might actually happen, and any move could make Griffin’s and Viola’s HTF companies less profitable.

It’s still a massive victory for the HFT industry as CEO of the SEC Gary Gensler walked back threats of banning payment of order flow.

That is now off the table.

Funnily enough, HFT firms argue they are delivering “greater liquidity” to the end buyer, but that liquidity is almost always in the form of a higher price.

Cynical and straight forward people would call this a rip off.

The flip side is that platforms can offer commission-free trading in the US.

Since 2019, most major online brokerages haven’t charged retail clients fees for their transactions, following a model made popular by Robinhood.

As for the here and now, Virtu’s stock isn’t a buy because the downdraft in the broader tech market has punished Virtu’s stock.

Remember, HFT firms can only front run orders for market orders and not limit orders that specify a certain price.

As for trading platform Robinhood (HOOD), this means that their stock isn’t a zero either, but they bet big on crypto and that investor base in now impoverished.

Citadel and Griffin announced $4.2 billion in net trading revenue in the first 8 months of the year which is a 23% year-over-year bump.

The outperformance occurred because they have gained market share from bigger investment banks and remember that they earn revenue on sell orders as well as buy orders.

Sadly, for investors, Citadel is a private company.

Ultimately, it’s not a good time to buy Robinhood or Virtu Financial, but strategically, selling any large tech rally makes sense as the macro risks of interest rates still rock the market on a consistent basis as high inflation roars along.

Mad Hedge Technology Letter

June 10, 2022

Fiat Lux

Featured Trade:

(STOCKBROKERS SIGNALING BIG CHANGES AHEAD)

(VIRT), (HOOD), (CITADEL)

Virtu Financial, Inc. (VIRT), Robinhood Markets, Inc. (HOOD), and Citadel Securities will need to change business models after the SEC plans unprecedented market changes so that high-frequency trading companies cannot front-run retail orders anymore.

Citadel is the only one of these 3 that is not public and for the other 2, heavy short interest will attract these stock names.

It’s about time.

The regulation revolves around retail investors finally getting a fair order for their market stock orders.

Market orders aren’t specified at a certain price and because of that, companies front-run these orders and skim a few pennies off their orders, before finally selling them to the end retail investor.

Crazily enough, this has been legal for many years, which is why the CEO of Citadel Ken Griffin can buy a new $100 million property every year.

Under current rules, brokers must perform “reasonable diligence” to determine the likely best market for executing a trade.

Robinhood Markets essentially sell historical retail trade data to Citadel and Virtu, better known as Payment for order flow (PFOF).

This is the juice that these HFT firms use to front-run the retail traders by deploying their professional algorithms.

Nobody in the trading community thought the SEC would get their heads around and do something about this egregious loophole in trading.

I need to give credit where credit is due, and diverting market trades into an auction where the actual best price is procured for the retail trader finally gives power back to the little man after getting fleeced for so many years.

CEO of Virtu Douglas Cifu and Ken Griffin must now expose their capital to risk if they wish to make money in markets.

What a thought!

The zero-risk era of front-running trading is coming to a close meaning companies like Robinhood are worth zero since their profits come from PFOF.

HOOD is worth zero because they don’t charge traders for trading fees because they package all revenue in the form of PFOF.

If that is now worth zero, then do the math: the company is also worth nothing.

This would also take down one of the biggest crypto-based companies whose claim to fame was being the rock-solid broker for the crypto traders.

Well, it’s hard to make money when your customer goes bankrupt, which is exactly what happened to crypto traders since November 2021.

Now, imagine charging for trades and competing with real brokers in the vanilla game of stock broking and the future looks quite daunting.

On the plus side, VIRT and Citadel can roll their mass profits into risk-based trading strategies. However, that could lose money, which they aren’t used to.

This is still only a proposal and not legislation yet, so the dust has yet to settle.

However, if this does come to pass, expect trading commissions to come back in full and no more free trading, because stockbrokers need some way to make money if they can’t sell your trading data.

The gamification of trading by HOOD has alerted the SEC to tighten down the hatches; and this has been coming for quite a time.

The SEC has proven in the past that when there is a red target on one’s back, they usually don’t just give a pass.

As a response to the SEC proposal, HFT brokers are pedal to the metal with lobbyists and government pressure to block this proposal.

If this proposal goes through in some potent form, expect HOOD and VIRT to be down big and for Ken Griffin to purchase less $100 million mansions.

Global Market Comments

January 7, 2022

Fiat Lux

Featured Trades:

(JANUARY 5 BIWEEKLY STRATEGY WEBINAR Q&A),

(IWM), (RUA), (TSLA), (NVDA), (USO), (TBT), (ROM), (SDS), (ZM), (AAPL), (FCX), (HOOD), (BRKB)

Below please find subscribers’ Q&A for the January 5 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, Nevada.

Q: What’s a good ETF to track the Russell 3,000 (RUA)?

A: I use the Russell 2,000 (IWM) which is really only about the Russell 1500 because 500 companies have been merged or gone bankrupt and they haven't adjusted the index yet. This is the year where value plays and small caps should do better, maybe even outperforming the S&P500. These are companies that do best in a strong economy.

Q: Should I focus on value dividends growth, or stick with the barbell?

A: I think you have to stick with the barbell if you’re a long-term investor. If you’re a short-term trader, try and catch the swings. Sell tech now, buy it back 10% lower. Keep financials; when they peak out you, dump them and go back into tech. It’ll be a trading year, but if a lot of you are just indexing the S&P500 or doubling up through a 2x ETF like the ProShares ultra S&P 500 (SSO), it may be the easiest way to go for this year.

Q: Will higher rates sabotage tech, particularly smaller companies?

A: They’ve already done so with PayPal (PYPL) down 44% in six months—I’d say that’s sabotaged. Same with Square (SQ) and a lot of the other smaller tech companies. So that has happened and will continue to happen a bit more, but we’re really getting into the extreme oversold levels on a lot of these companies.

Q: Should we cash out on the iShares 20 Plus Year Treasury Bond ETF (TLT) summer 150/155 put spread LEAPS?

A: No, because you haven't even realized half of the profit in that yet since there is so much time value left in those options. As long as you stay below $150 in the (TLT), which I'm pretty sure we will, you will get your full 100% profit on that position. On the six month and one year positions, they don’t really move very much because they have so much time value in them. Once you get into the accelerated time decay, which is during the last 3 months before expiration, they catch like a house on fire. So, if you're willing to keep a safe long-term position, this thing will write you a check every day for the next six months or a year to expiration. I know we have absolutely everybody in these deep in the money TLT puts; some people even did $165-$170’s—you know, my widows and orphans crowd—and they are doing well, but not as much as if you’d had a front month.

Q: What scares you most for the next 12 months?

A: Another variant that is more fatal than either Delta or Omicron. Unlikely, but not impossible.

Q: Do you expect Freeport McMoRan (FCX) to break out to the upside?

A: I do, I did the numbers over the vacation for copper production to meet current forecast demands for electric vehicle production. Global copper has to increase 11 times, and that can’t be done, so prices are going to have to go up a lot. One of my concerns with these lofty EV projections (that even I make) is that there aren’t enough commodities in the world to make all these cars with the current infrastructure. And you’re not going to find a replacement for copper—it's just too perfect of an electrical conductor. So, that means higher prices to me—you increase demand 11 times on a stable supply, and it takes 10 years to bring a new copper mine online.

Q: Do you have any open trades?

A: No, and one reason is that I figured they would probably crash the market on the last trading day of the year, which they did. If I had positions, they would have crushed them on the last year and my performance. And all hedge fund traders do this; they try to go 100% cash at the end of the year to avoid these things. And whatever you lost on Friday you made back on Monday morning at the expense of last year's performance. But you have to wait 15 months to get paid on today's performance, and, that is the reason I do that. So, looking for higher highs to sell, lower lows to buy.

Q: Should I be buying NVIDIA (NVDA) and Tesla (TSLA) on the dip?

A: Absolutely yes, but Tesla's prone to 45% corrections—we had one last year and the year before—and Nvidia tends to have 25% corrections. So yes, NVIDIA could well be the stock of the decade, but you don’t want to buy it right now. It’s starting to lose steam already.

Q: Will ProShares Ultra Technology (ROM) be under pressure?

A: Keep your position small now, take some profits, look to buy on a bigger dip. If the big techs drop 10%, (ROM) will drop 20% and get you below $100.

Q: Do you offer trade alerts on small caps for short term traders?

A: No, because you can’t execute those trades. A lot of them are just so illiquid, you can’t even trade one share unless you want to pay a huge spread. Keep in mind, when I worked at Morgan Stanley (MS), I covered the Rockefeller Foundation, the Ford Foundation, George Soros, Paul Tudor Jones, the government of Abu Dhabi, California State Pension Fund, and a lot of other huge funds; and the last thing they’re interested in is short term trades for the small-cap stocks. So, I don't really know much about those, but they tend to change the names every year anyway. And it really is a beginner trader type area because the volatility is so enormous. You can get 10x moves one day going to zero the next. It is also an area full of scams, cons, and pump and dump schemes.

Q: What is your advice when it comes to the ProShares UltraShort 20+ Year Treasury (TBT)?

A: Short term, take the profits—you just got a $14 point rally in your favor. Short term traders, take profits on bonds here, cover your shorts. Long term investors keep it, the cost of carry is only about 4% right now, not that high, so I would keep it for a great year-end move for 2.5% yields on the ten-year.

Q: I hate oil (USO) because it’s going to zero. Should I keep trading in it?

A: Very few are nimble enough to trade oil, it’s really an insider’s game. No new capital is moving into the oil industry and oil companies themselves won’t invest in their own businesses anymore.

Q: Would you put on a new position on the iShares 20 Plus Year Treasury Bond ETF (TLT) today?

A: No, you don’t sell short things after they move down $14 points. You put them on before that. If I were to do a short-term trade in (TLT) I would be a buyer, I’d maybe buy it for a countertrend rally of maybe $4 or $5 points.

Q: What should I do with my FCX 2023 LEAP?

A: There is enough time on it, so I would keep running it along as is—don’t get greedy. Keep the LEAPS you have and you should do well by it.

Q: Could the iShares 20 Plus Year Treasury Bond ETF (TLT) bottom out in the near term?

A: Yes, it could, on a short-term basis. $141 is the nine-month low for the (TLT), so a great place to take short term profits. (TLT) is right now at $142.56, so we’re approaching that $141 handle closely. Every technical trader on the market’s going to cover their shorts on the $141 or $142 handle, so just congratulate yourself going into this move short, and take the money and run. You take every $14 point move in your favor in the (TLT); and let it rally 5 points and then reestablish, that’s how you trade.

Q: Do you think there will be a delay in the first interest rate hike due to COVID?

A: Yes, Jay Powell is the ultra-dove—any excuse to delay rate hikes, he’ll do it. And the way you’ll know is he’ll delay the end of other things which you don’t see, like daily mortgage bond purchases, daily US Treasury purchases, and other backdoor forms of QE. We’ll know well in advance if he’s going to raise or not by March or even June. We watch this stuff every day, we talk to people at the Fed every week. And remember, the Treasury Secretary Janet Yellen is a good friend of mine, I get a good handle on these things; this is why 99% of my bond trades make money.

Q: What if I have the $135-$140 put spread in January?

A: Sell it now, take what you can, take the hit; because that’ll expire at zero unless we break down to new lows on the (TLT) in the next ten days or so. That's not a good bet, especially on top of a $14 point drop. Capture what you can on that one and keep the cash for a better entry point. That’s exactly what I did—I sold all my January positions yesterday no matter what they were, because when you get to two weeks to expiration the moves become random.

Q: Do you think inflation will last longer than expected?

A: No, I think it will last shorter than expected because I think at least half of the inflation rate, if not more, are caused by supply chain problems which will end within the next six months, and therefore lead to the over-order problem that I was talking about earlier.

Q: What’s your outlook on energy this year?

A: It could go higher. On the way to zero, you’re going to have several double, tripling’s, even 10x increases in the price of oil, like we saw in the last 18 months. We went from negative numbers to 80, and what happens is oil becomes more volatile as the supply becomes more variable, that's a natural function. But trading this is not for non-professionals.

Q: Since sector rotation is happening, do you think we should sell all tech positions?

A: Short term yes, long term no. Tech will still lead with earnings, and even if they have a bad five months coming, they have a terrific long-term view. For the last 30 years, every sale of tech has been a mistake, especially in Apple (AAPL). So if you’re a trader, yes, you should have been selling since November. If you’re a long-term investor, keep them all.

Q: Is the ProShares UltraShort S&P 500 (SDS) a good position to buy up when the market timing index goes into sell territory?

A: Yes it is, and that will probably work better this year than it did last year because narrow range volatile markets are much more technically oriented than straight-up markets or long term bull markets. Pay close attention to those markets, you could make a lot of money trading them.

Q: Do Teslas have good car heaters for climates up North in -25 or -30?

A: You plug them in. When it gets below zero you actually get a warning message on your Tesla app telling you to plug it in, and then the car heats itself off of the power input. Otherwise, if you get to below zero, the range on the car drops by half. If you have a 300-mile range car like I do and then you freeze it, it drops to like 150 miles. In Tahoe, I keep my car plugged in all the time when I'm not using it, just to keep it warm and friendly.

Q: Is Zoom (ZM) a good buy here?

A: No, I think they’re going to keep punishing these overpriced small cap techs like they have been. We’re a long way from value on small tech. That was a 2020 story.

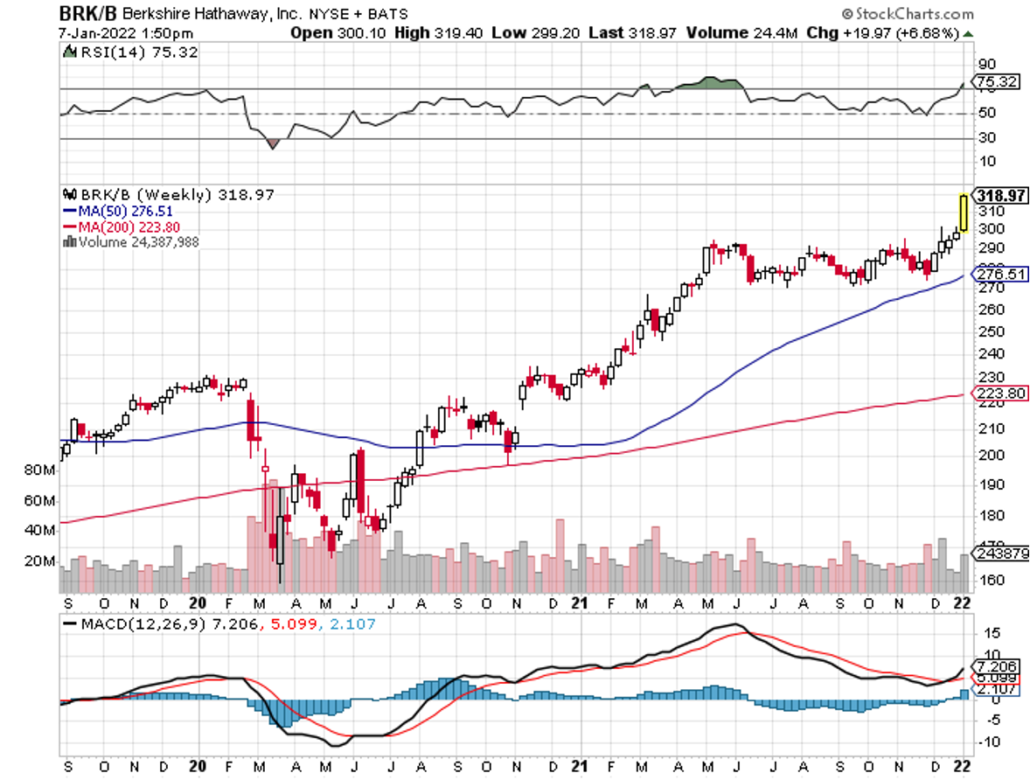

Q: What about Berkshire Hathaway (BRKB)?

A: Berkshire Hathaway is doing a major breakout because they own financials up the wazoo and they’re all breaking out. And YOU should be long up the wazoo on these things because I’ve been recommending them for the last 4 months.

Q: What do you think of Robinhood (HOOD)?

A: Robinhood I like long term, but it is high risk, high volatility. It is down 78% from the IPO so it is busted. Kind of tempting down here, but again, all the non-earning overvalued stocks are getting their clocks cleaned right here; I'm not in a rush to get involved.

Q: When you enter a LEAP, is the straight call or call spread?

A: It’s a call spread. You finance the high cost of one-year options by selling short a call option against it further out of the money. And that way you can get enormous leverage for practically nothing, 10 or 20 times in some cases, depending on how you structure the strikes.

Q: Best stock to play Copper?

A: Freeport McMoRan (FCX). I’ve been recommending it since it was $4.00.

Q: Oil is the pain train until EVs actually take over.

A: That’s true, and they haven’t. EVs have about a 6% market share now of new car sales worldwide, but that could rapidly accelerate given all the subsidies that EVs are getting. Also, we have many future recessions to worry about, during which oil could easily drop 290% like it did last year. If you can hack that kind of volatility, go for it, but I find better things to do quite honestly. And I think my next oil trade will be a short, especially if we go over $100.

Q: What about Bitcoin?

A: It could go sideways in a range for a while. If we can’t hold the 200-day, we’re going back down to the high 30,000s, where we were at the start of the year—we could give up the entire year of 2021. Bitcoin also suffers from rising interest rates since they don’t yield anything.

Q: Is this recorded?

A: Yes, the webinar recording goes out in about 2 hours. Log into the madhedgefundtrader.com website and go to my account, where you’ll find it with all the different products you’ve purchased.

Q: I just closed out my (TLT) 150 put option for the biggest single trade profit in my life; I just made 20% of my annual salary alone today. Thank you, John!

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Bitcoin Letter

September 14, 2021

Fiat Lux

Featured Trade:

(CRYPTO IS LEGIT)

(HOOD), (BTC), (FINRA), (SEC), (CFTC)

There was a fresh wave of optimism that swept across Washington when SEC Chair Paul Atkins spoke to Congress about making the United States a global hub for digital-asset innovation. Headlines painted him as the opposite of Gary Gensler - friendlier, more flexible, and eager to strike a “balanced” approach.

But anyone who has lived through a regulatory cycle knows better. The pendulum swings, but the incentives at the center never change.

Atkins now gestures to the Senate committee that overly harsh enforcement may have stifled innovation - and that perhaps it is time to bring crypto into a more cooperative regulatory framework. These developments suggest the industry has grown too large and systemically relevant to operate outside the official perimeter of federal oversight.

Don’t blame me for being cynical, but whether the rhetoric is friendly or hostile, boiling this down to money and power still cuts through many adjacent industries.

It’s just the way of life.

Crypto has become lucrative, and every administration - no matter how innovation-forward their branding - still wants a slice of this golden goose.

Why do I say that?

The SEC’s core revenue mechanics have not changed. Every movement on regulated exchanges, from buying to selling, generates the fees that fuel its operations. The language used to justify them may evolve, but the incentive remains untouched.

Investing with retail brokerages is marketed as commission-free, now and forever. They do not charge fees to open or maintain accounts. Yet the fee structure underneath always finds its way back to the same place.

Self-regulatory organizations (SROs) such as the Financial Industry Regulatory Authority (FINRA) impose small fees for sell orders. These fees apply across brokerages. Firms pass them to customers, who indirectly fund regulatory bodies. FINRA is required by law to forward certain fees to the Securities and Exchange Commission.

The numbers shift with time, but the mechanism stays the same: fees ultimately cover the government’s cost of supervising markets and securities professionals.

There are numerous layers of cost embedded into participating on exchanges regulated by the SEC. The result is a well-oiled system of fee collection and institutional reinforcement.

So when Atkins offers his stamp of legitimacy to the crypto sector, the underlying exchange is simple: innovation-friendly messaging in return for bringing digital assets into the fee-generating ecosystem.

For lack of a better word, these fees allow regulators like FINRA and the SEC to rake in the cash, and as we know in this business, money is power.

I only see it as a matter of time before the SEC, FINRA, and Commodity Futures Trading Commission (CFTC) expand their reach further into crypto infrastructure - not just through enforcement, but through officially sanctioned pathways that look friendly on paper yet consolidate control.

And I’m not blaming them. Everyone is in the business of adding to their nest eggs, and the SEC, FINRA, and CFTC are no different.

However, ultimately this is what it’s about: a cash grab dressed up in innovation-forward language. The legitimization of crypto is merely the collateral benefit - one any asset class would be ecstatic to receive.

Take sports as an example. Football leagues scramble for the NFL’s approval, but the NFL rarely offers its blessing. They don’t care if college football and startup leagues battle it out away from the confines of professional football. The cost of lacking an NFL stamp of approval has been devastating for newcomers.

If the SEC once again vouches for large elements of the crypto ecosystem - this time through cooperative rulemaking under Atkins - this will start a chain reaction. It offers an olive branch to wealthy investors who have waited for a friendlier regulator.

Consequently, they would come pouring in, guns blazing, with the heft of their capital and the strength of their financial connections.

Atkins announcing that cryptocurrency exchanges may receive a clearer path to registration, as opposed to the adversarial gridlock of the Gensler era, makes this one step closer to reality.

During his early remarks, Atkins stated that recent regulatory battles left both investors and innovators without adequate clarity. His angle appears the inverse of Gensler’s warnings, but the subtext is the same: the SEC cannot effectively shape a market from which it remains partially excluded.

I want to remind readers that any SEC chair has the choice to allow crypto to operate in a vacuum, but doing so risks letting it grow too big to regulate - and too large to fold into traditional fee structures. They all know that.

Atkins highlights crypto as an asset class with enormous potential, yet one that requires consistent regulatory engagement.

The moral high ground is still shaky.

The SEC continues to permit the listing of foreign firms under structures that allow significant opacity, yet remains eager to frame crypto as the primary risk vector in modern markets.

Atkins acknowledges that Congress must ultimately define jurisdiction, just as Gensler once did. He may sound more cooperative, but the underlying tension is the same.

Regulation would be a huge win for the crypto universe, but it invariably infringes on the decentralized ideals that first drew people to digital assets.

Regulators love to preach about safety, but they preside over a system that endlessly erodes the purchasing power of fiat currency through policy choices far outside the crypto world.

Thus, does anyone sitting in the SEC chair truly believe that preserving the dollar’s value - or crypto’s future - is something they can call safe?

Global Market Comments

August 27, 2021

Fiat Lux

Featured Trade:

(AUGUST 25 BIWEEKLY STRATEGY WEBINAR Q&A),

(ROM), (EEM), (FXI), (DIS), (AMZN), (NFLX), (CHPT), (TLT), (TBT), (AAPL),

(GOOG), (WPM), (GOLD), (NEM), (GDX), (X), (SLV), (FCX), (BA), (HOOD), (USO)

Below please find subscribers’ Q&A for the August 25 Mad Hedge Fund Trader Global Strategy Webinar broadcast from The Atlantis Casino Hotel in Reno, NV.

Q: How does a 2X ProShares Ultra Technology ETF (ROM) February 2022 vertical bull call spread on the ROM look? Would you do $110-$115 or $115-$120?

A: I would do nothing here at $112.50 because we’ve just gone up 10 points in a week. I’d wait for some kind of pullback, even just $5 or $10 points, and then I would do the $110-$115. I’m leaning towards more conservative LEAPS these days—bets that the market goes sideways to up small rather than going ballistic, which it has done for the last 18 months. Think at-the-money strikes, not deep out-of-the-money on your LEAPS from here on for the rest of this economic cycle. The potential profits are still enormous. The only problem with (ROM) is that the longest maturities on the options are only six months.

Q: How do you recommend entering your long-term portfolio?

A: I would use the one-third rule: you put on ⅓ now, ⅓ higher or lower later on, and ⅓ higher or lower again. That way you get a good average price. Long term, everything goes up until we hit the next recession, which is probably several years off.

Q: I keep reading that the Delta variant is a market risk, but I don’t think that investors will look through this. Is Delta already priced into the shares?

A: Yes, what is not priced into the shares is the end of Delta, the end of the pandemic—and that will lead to my “everything” rally that I’ve been talking about for a month now. And we have already seen the beginning of that, especially with the price action this week. So yes, Delta in: dead market; Delta out: roaring market.

Q: Do you think there will eventually be a rotation into emerging markets (EEM), or has the virus battered these markets too much to even consider it?

A: Sometime in our future—not yet—the emerging markets will be our core holding. And the trigger for that will be the collapse of the dollar, which is hitting an interim high right now. When the greenback rolls over and dies, you can expect emerging markets, especially China, to take off like a rocket. That’s going to be our next big trade. I don't know if it will be this year or next year but it’s coming, so start doing your emerging market research now, and keep reading my newsletter.

Q: Is the coming tax hike a problem for the stock market?

A: No, I don’t think so. First off, I don’t think they’re going to do a tax bill this year; they don’t want anything to interfere with the 2022 election, so it may be next year’s business. Also, any new taxes are going to be overwhelmingly focused on billionaires, carried interest, offshoring, and large corporations. The middle class, people who make less than $400,000 a year, will not see any tax hike at all, possibly even getting some tax cuts via restored SALT deductions. So, I don't really see it affecting the stock market at all.

Q: What do you think about Chinese stocks (FXI)?

A: Long-term they’re okay, short term possibly more downside. Interestingly, the bigger risk may not be China itself and how the government is beating up its own tech companies, but the SEC. It has indicated they don’t really like these offshore vehicles that have been listed on the New York Stock Exchange, and they may move to ban them. I’m not rushing into China right now, only because there are just so many better opportunities in the US stock market for the time being. I may go back in the future—it’s a case where I’d rather buy them on the way up than trying to catch a falling knife on China right now.

Q: Do you expect any market impact from the Jackson Hole meeting?

A: Yes, whatever J Powell says, even if he says nothing, will have a market impact. And it will have a bigger impact on the bond market than it will on the stock market, which is down a full point this morning. So yes, but not yet. I imagine we’ll hear something very soon.

Q: September and October tend to be volatile; do you see us having a 5% or 10% pullback in those months?

A: I don’t see any more than 5%, with the hyper liquidity that we have in the system now. There just aren’t any events out there that could trigger a pullback of 10%—no geopolitical events, and the economy will be getting stronger, not worse. So yes, an “everything rally” doesn’t give you many long side entry points, so I just don’t see 10% happening.

Q: What about a Walt Disney (DIS) January 2022 $180-$220 LEAPS?

A: I would do the $180-$200. I think you can afford to be tighter on your spread there, take some more risk because I think it’s just going to go nuts to the upside once we get a drop in COVID cases. By the way, Disney parks are only operating at 70% capacity, so if you go back up to 100% that's a near 50% increase in profits for the company. And it’s not just Disney, but Netflix (NFLX), Amazon (AMZN), and everybody else that’s about to have the greatest number of blockbuster movies released of all time. They’re holding back their big-ticket movies for the end of the pandemic when people can go back into theaters. We’ll start seeing those movies come out in the last quarter of this year, and I’m particularly looking forward to the next James Bond movie, a man after my own heart.

Q: Are EV car charging companies like ChargePoint Holdings (CHPT) going to do as well as the car companies?

A: No. They’re low margin business, so it’s not a business model for me. I like high-profit margins, huge barriers to entry, and very wide moats, which pretty much characterizes everything I own. The big profits in EVs are going to be in the cars themselves. Charging the cars is a very capital-intensive, highly regulated, and low-margin business.

Q: Would a Fed taper cause a 10% pullback?

A: Absolutely not; in fact, I think a taper would make the market go up because Jay Powell has been talking it into the market all year. And that’s his goal, is to minimize the impact of a taper so when they finally do it, they say ho-hum and “okay you can take that risk out of the market.” That’s the way these things work.

Q: What is your yearend target for United States Treasury Bond Fund (TLT)?

A: $132. Call it bold, but I'm all about bold. I think the first stop will be at $144, then $138, then bombs away!

Q: What will it take for (TLT) to dip below $130?

A: Another year of hot economic growth, which Congress seems hell-bent on delivering us.

Q: What are your ProShares Ultra Short 20+ Year Treasury ETF (TBT) targets?

A: When we were at 1.76% on the 10-year bond, the (TBT) made it all the way back to 22 ½. Next year we go higher, probably to $25, maybe even $30.

Q: What’s your 10-year view on the (TBT)?

A: $200. That’s when you get interest rates back to 10% in 10 years on the 10-year bond. So yes, that’s a great long-term play.

Q: How long can we hold (TBT)?

A: As long as you want. Ten years would be a good time frame if you want to catch that $17 to $200 move. The (TBT) is an ETF, not an option, therefore it doesn’t expire.

Q: Are you working on an electrification stock list?

A: I am not, because it’s such a fragmented sector. It’s tough to really nail down specific stocks. I think it’s safe to say that the electric power grid is going to change beyond all recognition, but they won’t necessarily be in high margin companies, and I tend to prefer high-profit-margin, large-moat companies which nobody else can get into, like Apple (AAPL) or Google (GOOG).

Q: What about gas pipelines with high yields?

A: They have a high yield for a reason; because they’re very high risk. If you're going to a carbon-free economy, you don’t necessarily want to own pipelines whose main job is moving carbon; it’s another buggy whip-type industry I would avoid. I’ve seen people get wiped out by these things more times than I could count. If you remember Master Limited Partnerships, quite a few of them went bankrupt last year with the oil crash, so I would avoid that area. These tend to be very highly leveraged and poorly managed instruments.

Q: Best play on silver (SLV)?

A: Wheaton Precious Metals (WPM) is the highest leveraged silver play out there, and a great LEAPS candidate. Go out 2 years and triple your money.

Q: Geopolitical oil (USO) risks?

A: No, nobody cares about oil anymore—that’s why we’re giving up on Afghanistan. China is buying 80% of the Persian Gulf oil right now. We don’t really need it at all, so why have our military over there to protect China’s oil supply?

Q: What about Freeport McMoRan (FCX)?

A: I absolutely love it. Any big economic recovery can’t happen without copper, and you have a huge tailwind there from electric cars which need 200 pounds of copper each, as opposed to 20 pounds in conventional cars.

Q: I see AMC Entertainment Holdings (AMC) is up 20% today; should everyone be chasing this stock?

A: No, absolutely not. (AMC) and all the meme stocks aren’t investments, they’re gambling, and there are better ways to gamble.

Q: Should I buy the lumber dip?

A: Yes. I think the slowdown on housing is temporary because it will take 10 years for supply and demand in the housing market to come back into balance because of all the millennials entering the housing market for the first time. So, that would be a yes on lumber and all the other commodities out there that go into housing like copper, steel, and aluminum.

Q: Should I put money into Canadian Junior Gold Miners (GDX)?

A: No, I would rather go out and take a long nap first. These are just so high risk, and they often go bankrupt. The liquidity is terrible, and the dealing spreads are wide. I would stick with the bigger precious metal plays like Newmont Mining (NEM), Barrick Gold (GOLD), and Wheaton Precious Metals (WPM).

Q: Is Boeing (BA) a buy here?

A: Yes, we’re back at the bottom end of the trading range for the stock. It’s just a matter of time before they get things right, and the 737 Max orders are rolling in like crazy now that there’s an airplane shortage.

Q: What do you think about Robinhood (HOOD)?

A: I like it quite a lot; I got flushed out of my long position on Friday with a 10% down move. Of course, 90% of my stop losses end up expiring at their maximum profit points, but I have to do it to keep the volatility of the portfolio down. So yes, I’ll try to buy it again on the next dip. The trouble is it’s kind of a quasi-meme stock in its own right, hence the volatility; so I would say on the next 10% down day, you go into Robinhood, and I probably will too.

Q: How are the wildfires around Tahoe?

A: They’re terrible and there are three of them. I did a hike two days ago there, and out of a parking lot with 100 spaces, I was the only one there. It’s the only time I’d ever seen Tahoe deserted in August. With visibility of 500 yards, it's just terrible. Fortunately, I was able to hike without coughing my guts out—it’s not so thick that you can’t breathe.

Q: What do you think of US Steel (X)?

A: I like it, I think the whole industrial commodity complex rallies like crazy going into the end of the year.

Q: As a new member, where is the best place to start? It’s just kind of like drinking from a fire hose.

A: Wait for the trade alerts; they only happen at sweet spots and you may have to wait a few days or weeks to get one since we only like to enter them at good points. That’s the best place to enter new positions for the first time. In the meantime, keep reading all the research, because when these trade alerts do come out, they’re not surprises because I’m pumping out research on them every day, across multiple fronts. Be patient— we are running a 93% success rate, but only because we take our time on entering good trades. The services that guarantee a trade alert every day lose money hand over fist.

Q: If they do delist Chinese stocks, will US investors be left holding the bag?

A: Yes, and that will be the only reason they don’t delist them, that they don’t want to wipe out all current US investors.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER (whichever applies to you), then select WEBINARS and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader