Mad Hedge Technology Letter

February 19, 2019

Fiat Lux

Featured Trade:

(THE SAFE PLACE TO HIDE IN TECH),

(CSCO), (ORCL), (WDAY), (ZEN), (HUBS), (NOW), (PYPL), (VEEV), (TWLO)

Mad Hedge Technology Letter

February 19, 2019

Fiat Lux

Featured Trade:

(THE SAFE PLACE TO HIDE IN TECH),

(CSCO), (ORCL), (WDAY), (ZEN), (HUBS), (NOW), (PYPL), (VEEV), (TWLO)

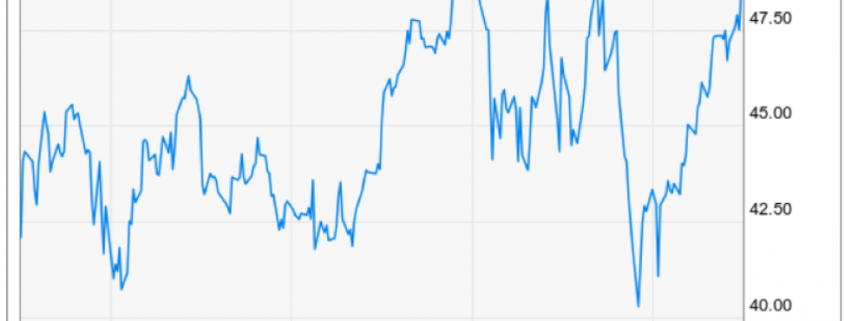

Great quarter by Cisco (CSCO).

That was the first thought in my head when perusing their quarterly earnings.

It’s been hit or miss for tech companies lately and at the end of 2018, I stood up and told readers to double down on software companies and specifically enterprise software companies.

Well, Cisco has skin in this software game because corporations cultivating software need the best type of network infrastructure money can buy.

Cisco is the foundational hardware on what current high-end software is built on.

It is all rosy to have a spectacular roof design, but without a solid foundation, we have nothing more than a house of cards.

The great part about Cisco is that they are immune to the software battle taking place inside of industries because they do not build the enterprise software that is built on top of the Cisco infrastructure.

We have seen our fair share of software companies go sideways such as Oracle (ORCL) who have presided over a stale patchwork of database system software created last gen.

However, on the other side of the coin, my prediction of enterprise software companies leading tech has been spot on.

Zendesk (ZEN), HubSpot (HUBS), ServiceNow (NOW), Workday (WDAY), PayPal (PYPL), Salesforce (CRM), Veeva Systems (VEEV), and Twilio (TWLO) are software companies that I was incredibly bullish on as we turned the calendar year and they have not disappointed with nearly all of these names flirting with all-time highs.

All these software companies need Cisco.

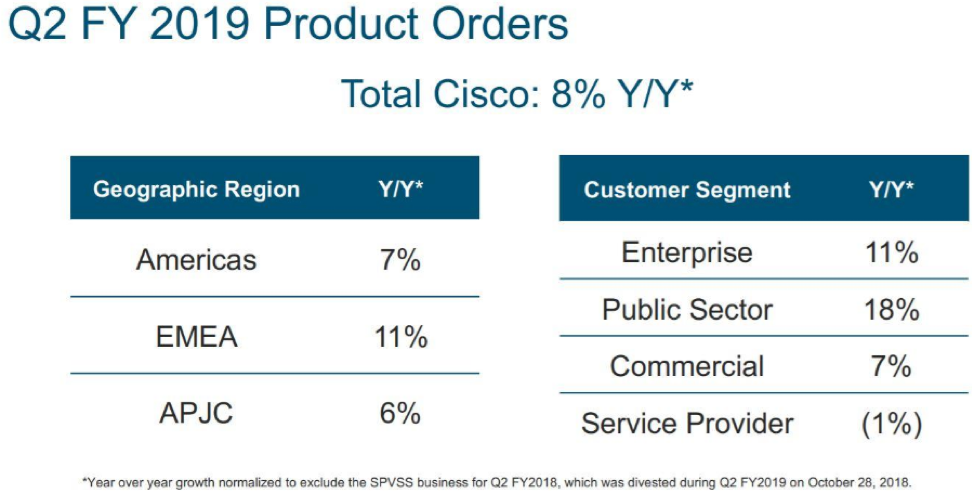

What stood out for me was that public sector orders grew 18% last quarter signaling that not only are the private corporations snapping up Cisco products, but governments are embedding their offices with Cisco’s Internet Protocol-based networking and other products related to the communications and information technology industry.

And if you wanted a general tech stock to capture the migration from analog commerce to digital and stay out of the high stakes online media segment, this would be the stable name that would check all the boxes.

And if you thought this was just a domestic story, once again, the scope is wider with Europe, the Middle East and Africa (EMEA) sales expanding by 11% which eclipsed America sales by 4%.

The only blip on the radar was service revenue slipping by 1% to $3.17 billion, but I do not view that as a pattern of sequential deceleration and pricing mechanisms can be altered to relaunch growth.

If you thought that Cisco doesn’t sell any software – you are wrong.

The software they do sell applies to operating the proprietary hardware that they produce.

Cisco’s wide competitive advantage stems from the industries toweringly high barriers of entry and that they make great products relative to other players.

The infrastructure software that liaises brilliantly with its hardware is succinctly named Cisco ONE Software.

This software suite is molded to face the most relevant use cases in the data center, WAN, and access edge.

CEO of Cisco Chuck Robbins characterized the current geopolitical and overall economic landscape as “complex” but experienced “zero difference” in Chinese revenue giving the company a quarterly victory in the Middle Kingdom.

China’s economy is decelerating faster than we can understand. The latest details of ride-hailing leader Didi sacking 2,000 employees is a warning flare to the rest that open wounds are appearing in the economy and are becoming harder to conceal.

And for Cisco to do a quarter with no significant Chinese downdraft is a good sign that the company can handle the upcoming recession in 2020.

As a sign of further strength, Cisco raised its dividend and boosted stock buybacks which are all the trappings of what great companies do.

Cisco already made $5 billion of repurchases last quarter which was on top of the $6 billion they bought in October 2018.

This method of financial engineering helps put a solid floor under the stock delighting investors and ignites the share price.

And the capital allocation encore means that Cisco will pile $15 billion into its buyback program with this fresh authorization, and the company is forecasted to produce at least $15 billion in free cash flow over the next year.

Cisco’s balance sheet is glistening and even has options to adventure into meaningful M&A if they see something that catches their eye without any real hit to the balance sheet.

These multiple tailwinds in a precarious economic point in the cycle have investors aware that there are worse options out there to invest capital than tech thoroughbred Cisco.

And if you thought the one variable that could turn this earnings report from good to bad was expenses and margins, well, Cisco covered their bases on that one too.

Margins came within the forecasted guidance with gross margins slightly trending down by 1% to 64.1%.

Expenses were reigned in and management saw a small nudge up of 3% causing investors to take a deep sigh of relief.

Cisco is in a superior strategic spot to most tech companies and is a staunch participant of the migration to digital.

Buy shares on the dip.

If you are on the prowl for a cloud-based software company with super-charged growth that is still in the early stages, then I have the one for you.

HubSpot (HUBS) sells online marketing software.

They are the one-stop for CRM (client relationship management), email and sales automation, pretty landing pages, social media marketing, keyword research, website analytics, and lead generation tools all on one platform.

In general, HubSpot targets the SMEs (small and medium enterprises) and offers an intuitively designed product adding value to over 50,000 firms.

They even have a freemium package allowing newbies to sample the power the software tools possess.

This service starts its pricing at $50 per month for the basic package and it may not seem like much.

But then there are the add-ons that guarantee lead to a wave of additional upselling - a boon to quarterly revenue.

The initial price base is usually followed with price increases into the thousands because business needs more contacts to slot into its data silos and features to harness elaborate marketing campaigns.

This is all the cost of doing business and signals that HubSpot has the ability to carve out even more revenue than the starter packages they offer.

If companies are moaning about the boost in costs, I would lash back and say the added costs are warranted because of the enticing surge in productivity that scaling and better tools offer marketers leading to higher performance.

Plus, HubSpot isn’t the only cloud-based software company offering add-on tools to massage the customer’s demands.

These demands are multiplying by the day as marketing software becomes more complicated and sellers require hybrid-solutions to seal the deal with the end-buyer.

Sequentially, HubSpot’s revenue is expanding ferociously up 35% from last quarter.

On a 3-year basis, HubSpot has demonstrated it can uphold a furious pace of growth averaging a 42% growth rate during this time.

The company is still smallish with a market capitalization of $5 billion, but that won’t last for long as revenue expansion will reward shareholders with a higher share price.

Some of the positives from this marketing software is that its quality is highly competitive with other industry players such as Infusionsoft.

There will be certain companies that fit different software as marketing software is incredibly diverse.

The way that developers approach certain tools will naturally result in a different product altogether.

Specifically, I favor the centralization of HubSpot’s tools.

The holistic nature of HubSpot’s software makes the sum of the parts more valuable.

Online marketing is not just a one-day fly-by-night operation. Industry professionals would admit it’s an arduous grind. They must commit to one platform because HubSpot has made it hard to hop around.

Specifically, I like that HubSpot locks up companies with 1-year contracts instead of a rolling month-to-month contract that encourages companies to jump ship whenever there is an incremental upgrade elsewhere.

This has the effect of smoothing over revenue with the recurring billing helping the CFO plan the future allocation of the company and, most importantly, retaining its core customer base.

HubSpot also charges for technical support topping up its revenue by deciding to avoid giving this service for free. Professional guidance shouldn’t be free and, in digital marketing, you pay for what you get, period.

Catering towards its lower-end customers, HubSpot offers a comprehensive training and extensive support material making the platform easy to maneuver around from the get-go.

HubSpot is also integrated into Salesforce showing that it doesn’t have to be the star of the show all the time but can play the role of supporting actor just as well.

Revenue is revenue.

But I would personally go even further and claim that HubSpot’s functionality not only blows Infusionsoft’s, an online marketing competitor, out of the water, but it pushes omnipotent Salesforce (CRM) to its limits.

All of this means that HubSpot is predicted to surpass revenue of $500 million in 2018 after posting revenue of $375 million last year.

HubSpot doubled sales revenue in just two years.

Even though they are expanding from a small base and is blown out of the water by Salesforce on this metric, they are doing exactly what companies this size should be doing in the tech industry.

Stalling growth like over at Venice Beach at Snapchat’s (SNAP) headquarter is a bona fide red flag.

Accelerating revenue is the most pivotal deal-clincher for investors and separates the men between the boys.

Technology is one of the few industries in the economy that have a panoply of companies able to accomplish this feat.

Like it or not, online marketing is one section of tech that is not going away.

Have you realized the heavy stream of emails alerting you to different services and products?

There is a high chance those emails originated from HubSpot and this trend is not going away.

Marketing email volume will only climb until the cost of emails rises substantially which I highly doubt.

Technology is getting cheaper and so is the cost of running a business because of this technology.

Being able to offer poignant tools to its customer base has led to a heavy dose of R&D spending increasing 63% YOY. Even with these higher expenses, HubSpot was able to deliver a stellar EPS beat last quarter posting 17 cents when the consensus was a minuscule 5 cents, beating the forecast by more than three times.

The future looks rosy for this company because we are just in the early innings of the digital revolution for smaller companies.

They will have to migrate or die out.

Even the IT staff at the Mad Hedge Fund Trader has integrated HubSpot into our bevy of software tools and there are no complaints.

The bottom line is that HubSpot grew its customer base 40% YOY to over 52,500.

That is hard to beat.

On the downside, lower average revenue per customer is a concern. The 4% drop is not in tune to what growth companies should demonstrate but I believe the reacceleration of investment into its marketing tools will bear fruit and elevate this dragging number.

That being said, the $9,959 per customer is not a shabby figure at all, and a certain reversion to the mean was due to take place at some point. I would be worried if this drop happened at a much lower average number.

When you delve deeper into the numbers, it appears as if the culprit was HubSpot offering too many teaser starter packages to lure in new business.

Therefore, a slight pricing hiccup for this online marketing company is a one-off and can easily be rectified by upselling its pricing packages from a more advantageous starting point.

HubSpot doesn’t need to dig deeper into the lower end of the bush league and pull out all the nasties.

Moving forward, the roadmap looks fruitful as HubSpot plans to migrate from the smaller companies to higher end and more lucrative business boding well for margin expansion and future average revenue per customer.

This will feedback growing capital into its R&D to develop even more shiny tools for these more advanced marketers.

Shares of HubSpot are a little frothy at this point, and if shares pull back to $120, it would serve as a premium entry point.

Online marketing works well and new business will be up for grabs as a whole slew of companies pivot towards online marketing giving HubSpot a chance to slice off another massive chunk of business powering up annual revenue.

If you have a small business and are considering traversing into the world of online marketing, then visit HubSpot’s website at https://www.hubspot.com