Mad Hedge Biotech & Healthcare Letter

April 20, 2021

Fiat Lux

FEATURED TRADE:

(A DEPENDABLE BUT UNDERVALUED HEALTHCARE STOCK)

(UNH), (ANTM), (CI), (HUM), (CNC), (CHNG)

Mad Hedge Biotech & Healthcare Letter

April 20, 2021

Fiat Lux

FEATURED TRADE:

(A DEPENDABLE BUT UNDERVALUED HEALTHCARE STOCK)

(UNH), (ANTM), (CI), (HUM), (CNC), (CHNG)

The ongoing seesaw fights in the stock market are causing too much drama that cunning investors can—and definitely should—steer clear from.

Instead of fretting over speculative and risky investments, it’s better off staying with tested and proven big-name companies that will remain solid buys for the years to come and continue to deliver positive results despite periods of uncertainty.

Among the huge names in the healthcare industry, United Health (UNH) is a strong contender that meets the criteria.

After almost a decade of delivering high returns, which shows off fast-rising earnings expectations, it’s interesting to see that the market has recently backed away from this blue-chip stock.

Nonetheless, the market’s skittishness offers an opening for investors looking to buy in the dip a company that pays dividends and promises to steadily boost your savings in the years to come.

Founded way back in 1974, UNH has become a top name in the healthcare industry, landing in seventh place on the Fortune 500 list.

To date, UNH has four main divisions handling its over 50 million members both in the US and across the globe: its private health insurance business UnitedHealthcare, its pharmacy benefits segment OptumRx, its healthcare services provider branch OptumHealth, and its analytics platform OptumInsight.

UNH has a market capitalization of $354 billion.

In comparison, the closest competitor is Anthem (ANTM), with $87.93 billion. In terms of market cap, the two are followed by Cigna (CI) with $85 billion, Humana (HUM) with $53.81 billion, and Centene (CNC) with $36.19 billion.

Amid the financial crisis brought about by the pandemic, UNH still reported a 6.2% jump in its revenue in 2020 to reach $257.1 billion.

The company’s most prominent growth driver is its Optum line, and UNH is making sure that this division continues to grow.

One of the most indicative moves towards that direction is UNH’s $7.8 billion acquisition announcement of technology and data analytics company Change Healthcare (CHNG), which should be completed by the second quarter of 2021.

In the agreement, UNH is offering Change Healthcare $25.75 for its shares, representing a premium of roughly 41% above the latter’s stock price.

UNH plans to merge Change Healthcare’s operation into OptumInsight, which currently handles hospital systems health plans, life sciences companies, and even governments.

In the first nine months of 2020 alone, OptumInsight generated over $1.9 billion, contributing to roughly 11% of UNH’s total bottom line.

The combination of these two will all but guarantee that UNH’s possession of the biggest and most powerful platform in the entire healthcare industry, with the acquisition projected to add approximately $470 million to the company’s adjusted earnings in 2022.

The decision to acquire Change Healthcare is part of the string of M&A deals executed by UNH to stay ahead of the game.

In 2019, it bought two companies to expand its operations: the DaVita Medical Group for $4.3 billion and Equian for $3.2 billion. Prior to these, UNH splurged on a $12.8 billion acquisition of Catamaran in 2015.

For 2021, UNH projects its earnings to increase, estimating its per-share profits to be somewhere between $16.90 and $17.40—and that estimate already took into consideration the headwinds involving COVID-19 that could still weigh on the company’s bottom line.

While this may appear optimistic, the truth is, generating strong results isn’t a novel accomplishment for UNH.

In the past three years, the company reported a net income of $10 billion or higher, with net margins recorded at 5% above its revenue.

Over the course of the last 12 months, UNH stock has climbed 24%, beating the S&P 500, which rose 18% during the same period. It also offers a decent dividend of 1.5%, which is admittedly slightly lower than the S&P 500 average at 1.6%.

Overall, UNH is a safe stock that you will not have to anxiously watch over and can hold in your portfolio for years.

More importantly, this company remains undervalued and still shows a lot of room for growth.

So if you’re a value investor looking with an interest in the insurance and healthcare services industry, then this market leader is a sustainable addition to your portfolio.

Although late to the party, giant biopharmaceutical company AbbVie (ABBV) is now going all-out on its coronavirus disease (COVID-19) treatment program.

The Illinois-based company, which has a market capitalization of $162.95 billion, aims to come up with a treatment that can block the SARS-CoV-2 coronavirus that causes COVID-19. The drug is currently dubbed 47D11.

AbbVie is working on this cure alongside Netherlands’ Erasmus Medical Center and Utrecht University as well as China’s bio-therapeutics developer Harbour BioMed.

It’s worth noting that AbbVie isn’t the first company to use this approach.

Earlier this year, Regeneron (REGN) announced a similar strategy to beat COVID-19. Its experimental cure, called REGN-COV2, is an antibody cocktail composed of two to three proteins working together to fight off the virus. The company plans to start clinical trials sometime this month.

Aside from AbbVie and Regeneron, Eli Lilly (LLY) is also utilizing the same technology.

In fact, the Indiana-based biotechnology leader already started dosing actual patients with COVID-19 with its experimental treatment, LY-CoV555.

Eli Lilly’s drug was actually developed using the antibodies collected from one of the first patients in the US to recover from the disease.

Using the same approach to find a COVID-19 cure isn’t the only thing Regeneron and AbbVie have in common, though.

To bulk up its oncology pipeline, AbbVie forged a partnership with Danish biotechnology company Genmab (GMAB) earlier this month.

Interestingly, Genmab is the same company behind the clinical progress of the bispecific antibody treatments of both Regeneron and Roche Holding (RHHBY).

AbbVie and Genmab agreed to collaborate on bispecific antibody development to come up with treatments that can target cancer cells and strengthen immune cells. The three drugs included in the deal are epcoritamab (DuoBody-CD3xCD20), DuoHexaBody-CD37, and DuoBody-CD3x5T4.

Aside from the three candidates already lined up, the two companies are also ironing out details on four additional cancer treatments.

The deal is estimated to be worth almost $4 billion, with AbbVie paying $750 million upfront.

On top of that, Genmab will also be entitled to get potential payments of up to $3.15 billion in milestone payments. The four potential cancer treatments could also entitle Genmab with an additional $2 billion.

Since bispecific antibodies are hailed as the “next-generation cancer therapy,” this market continues to attract big names in the industry.

So far, the list of companies working on bispecific antibodies includes Amgen (AMGN), Johnson & Johnson (JNJ), Novartis (NVS), GlaxoSmithKline (GSK), Merck (MRK), AstraZeneca (AZN), and Sanofi (SNY).

Aside from improving its oncology lineup, Abbvie has shown more creativity in diversifying its products.

Throughout the years, AbbVie had been considered as a strictly pharmaceutical company in the past. However, its recent purchase of Allergan set off a series of decisions that showcased the company’s plan to expand its portfolio.

With AbbVie’s revenue reaching $33.3 billion in 2019, several experts disagreed with the company’s decision to buy Allergan (AGN).

However, the move is estimated to add roughly $50 billion to the company’s annual revenue and help AbbVie’s bottom line.

One of the biggest products added to AbbVie’s portfolio is Botox, which has been long-regarded as Allergan’s prized cash cow.

In fact, this widely popular injectible raked in $1.02 billion in sales for Allergan in the fourth quarter of 2019 alone. Another promising product is the dermal filler Juvederm, which brought in $347.3 million in the same period.

Despite the excitement from the newly formed partnerships, a lot of investors remain apprehensive over AbbVie’s future.

These fears are rooted in the doomsday countdown for the company’s blockbuster rheumatoid arthritis drug Humira — and for good reason.

In its 2020 first quarter report, AbbVie recorded $8.6 billion in revenue, indicating a 10.1% jump year over year.

From this, Humira contributed nearly 58% despite the growing number of biosimilar rivals in Europe. In fact, Humira sales reached $4.7 billion, showing a 14.5% climb from the same period last year.

In 2019, experts predicted that Humira is poised to overtake Pfizer’s (PFE) Lipitor as the top-selling drug of all time by 2024.

AbbVie’s rheumatoid arthritis drug is estimated to reach a whopping $240 billion in sales in the next four years.

As expected, biosimilar competition, led by Amgen, has been licking their chops to get a piece of the action for years now, and they would do everything to dethrone AbbVie from its top spot in the autoimmune diseases sector.

Hence, AbbVie implemented two strategies to address this issue.

The first is forestalling the inevitable. In a recent court victory, AbbVie secured patent exclusivity for Humira until 2023.

Although this only leaves AbbVie with three short years to deal with the problem, it’s sufficient period for the company to execute its second plan: “Humira on steroids.”

Since Humira’s patent exclusivity has been a sore issue for AbbVie for years, the company decided to solve it by creating a stronger version of the drug.

The new antibody treatment, called ABBV-3373, is said to be more effective than Humira.

If all goes well in its clinical trials, then this “new Humira” can very well be AbbVie’s next megablockbuster and main moneymaker after 2023.

Humira isn’t the only big seller in AbbVie’s lineup.

Other blockbusters include cancer drug Imbruvica, which recorded $1.2 billion in revenue in the first quarter, up by 20.6% compared to the same period last year. Another cancer drug, Venclexta, is also performing well, bringing in $317 million in net revenue.

AbbVie has been boosting its next-generation treatments as well.

So far, two more Humira-like drugs stand out --severe plaque psoriasis medication Skyrizi and rheumatoid arthritis treatment Rinvoq.

Skyrizi’s annual sales are projected to grow from $1 billion to hit $4.4 billion by 2025, with the numbers going higher than $7.4 billion in the following years.

Rinvoq is expected to bring in $3.7 billion in sales by 2025 and increasing to reach $5.9 billion after that.

Right now, AbbVie appears to be oddly cheap as its shares are trading at only 9 times its expected earnings this year. This is possibly due to the anxiety over the loss of Humira’s patent exclusivity by 2023.

As AbbVie has shown in the past months, it has solid plans on how to deal with the impending loss. Its acquisition of Allergan, partnership with Genmab, and development of the “next Humira” all prove that claim.

Mad Hedge Biotech & Healthcare Letter

June 16, 2020

Fiat Lux

Featured Trade:

(THE ONE BRIGHT STAR IN THE HEALTHCARE INDUSTRY),

(ANTM), (TDOC), (CVS), (HUM), (CNC), (UNH)

The COVID-19 crisis has yanked the rug from under companies across all industries, and among the businesses that experienced a completely altered landscape these days is the health insurance industry. Imagine a business where sales increase fourfold overnight, but the customers can’t pay.

With the unemployment rate rising to historic levels since the pandemic hit, more people are dropping off commercial coverage rolls. Visits to the doctors and other elective procedures have been postponed indefinitely. Even political talks on healthcare reforms appear to be tabled until 2021.

Overnight, some doctors at country hospitals have seen workloads double and the suicide rate soar, while those in private practice are essentially unemployed.

While healthcare stocks are understandably struggling to survive, there are standouts that managed to take the blow without crumbling to ruins.

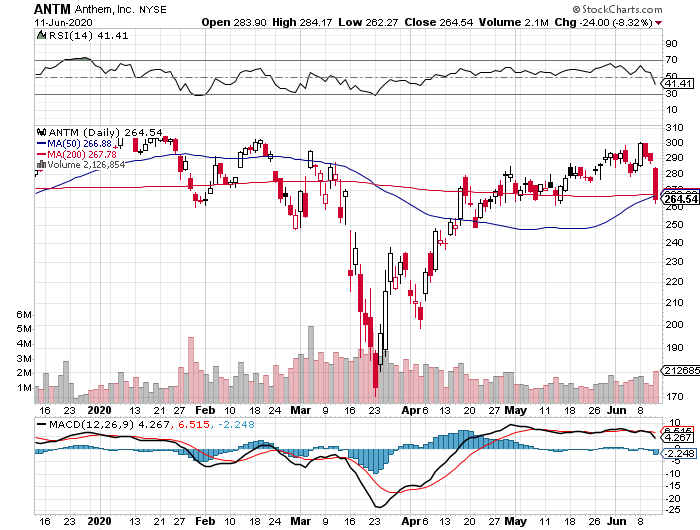

One of them is Anthem (ANTM).

With a market capitalization of $75.78 billion, Anthem is one of the biggest health insurers in the United States today.

Recently, the company wielded its power to offer $2.5 billion worth of premium credits as a form of financial assistance to its members during the pandemic.

This comes in the form of cost-share waivers, extensions for their virtual care coverage, and even assistance for struggling employers to help in maintaining the healthcare of their own employees.

While a lot of companies have been rapidly downgrading 2020 guidance due to the pandemic, Anthem updated its 2020 forecasts to reflect an increase in its adjusted net income from $19.44 per share to an eye-popping $22.30.

This indicates that Anthem has extra bandwidth for growth primarily thanks to its stable revenue stream, increasing membership, and solid earnings.

In its first quarter report for 2020, Anthem’s operating revenues jumped by 20.7% year over year to reach $29.4 billion, with profits from its IngenioRx launch.

As for its net income in the said period, Anthem raked in $1.52 billion or roughly $5.94 per share compared to $5.91 per share in 2019.

Anthem even increased its dividend by 19% in January.

However, it’s Anthem’s cash flow that continues to impress. From 2019 up until the first quarter of this year, Anthem’s cash flow surged by 58% year over year.

One of the main factors that boost the growth of a health insurance company is membership, and Anthem managed to tick off that box as well in the first quarter.

Anthem’s medical enrollment climbed to 42.1 million members, showing off a 3.2% increase year over year. With backing from government business enrollment as well as commercial and specialty businesses, this number is expected to climb higher this year.

Even Anthem’s inorganic growth ventures promise great results, with acquisitions and collaborations continuously boosting the Medicare Advantage growth of the company.

A good example is its acquisition of the Medicaid members in Missouri and Nebraska via WellCare Health at the beginning of 2020. This led to 849,000 lives added to its government business enrollment since 2019.

Meanwhile, its acquisition of AmeriBen added 452,000 members to its commercial and specialty business sector.

Anthem’s takeover of Beacon Health, which is the biggest independent behavioral health firm in the US, serves to further strengthen its position in this sector. This move added roughly 300,000 Medicaid members under Anthem’s coverage.

In terms of adapting to the needs of its members during the pandemic, Anthem is making more aggressive moves to promote its telehealth services.

Although this sector is currently widely associated with Teladoc Health (TDOC), which has a market capitalization of $12.93 billion, the rest of the league is catching up quick.

Since the average cost per telehealth session is roughly $100 less compared to fees paid in visits to the doctor’s office, this is definitely a platform-managed care providers are looking into.

According to Anthem, its telehealth app recorded over 170,000 new downloads since the COVID-19 crisis started.

It also reported a 250% surge in the demand for its virtual care services.

Anthem isn’t the only health insurer joining the telehealth fray. CVS Health (CVS), Humana (HUM), Centene (CNC), and even industry leader UnitedHealth Group (UNH) has been looking into the service.

In this period of uncertainty, choosing a stable company with a robust outlook and sold at a reasonable price is always a wise investment.

With Anthem’s profits projected to grow by roughly 47% over the next years, this company’s future offers security to its investors. Its impressive cash flow also plays a significant role in its higher share valuation.

Global Market Comments

March 5, 2020

Fiat Lux

SPECIAL MARKET BOTTOM ISSUE

Featured Trade:

(FRIDAY, APRIL 17 SAN FRANCISCO STRATEGY LUNCHEON),

(A LEAP PORTFOLIO TO BUY AT THE BOTTOM),

(TEN LONG-TERM BIOTECH & HEALTHCARE LEAPS TO BUY AT THE BOTTOM)

(UNH), (HUM), (AMGN), (BIIB), (JNJ), (PFE), (BMY)

Mad Hedge Biotech & Healthcare Letter

March 5, 2020

Fiat Lux

SPECIAL MARKET BOTTOM ISSUE

Featured Trade:

(TEN LONG TERM BIOTECH & HEALTH CARE LEAPS TO BUY AT THE BOTTOM)

(UNH), (HUM), (AMGN), (BIIB), (JNJ), (PFE), (BMY)

Joe Biden’s romp over Bernie Sanders in the Tuesday Democratic primary takes the lid off on the entire biotech and healthcare sector. Sanders has promised to dismantle the entire sector by promising Medicare for all and banning private coverage.

Sanders was also about to take a cudgel to drug pricing. While Sanders was leading in the primary, the threats hung over the industry like an 800-pound gorilla.

Yesterday, Sanders went down in flames. You can see this clearly in the price action of Humana (HUM), which rose a ballistic 14.44% yesterday. Similarly, United Health Group (UNH) was up a monster 10.72%.

It is safe to say that the bottom is in for biotech and healthcare stocks.

I am often asked how professional hedge fund traders invest their personal money. They all do the exact same thing. They wait for a market crash like we are seeing now and buy the longest-term LEAPs possible for their favorite names.

The reasons are very simple. The risk of a LEAP is limited. You can’t lose any more than you put in. At the same time, they permit enormous amounts of leverage.

Two years out, the longest maturity available for most LEAPs, allow plenty of time for the world and the markets to get back on an even keel. Recessions, pandemics, hurricanes, oil shocks, interest rate spikes, and political instability all go away within two years and pave the way for dramatic stock market recoveries.

You just put them away and forget about them. Wake me up when it is 2022.

I put together this portfolio using the following parameters. I set the strike prices just short of the all-time highs set two weeks ago. I went for the maximum maturity. I used today’s prices. And of course, I picked the names that have the best long-term outlooks.

If you buy LEAPs at these prices and the stocks all go to new highs, then you should earn an average 229% profit from an average stock price increase of only 11.4%. That is a return 20 times greater than the underlying stock gain. And let’s face it. None of the companies below are going to zero, ever. Now you know why hedge fund traders only employ this strategy.

There is a smarter way to execute this portfolio. Put in throw-away crash bids at levels so low they will only get executed on the next 1,000 point down day in the Dow Average.

You can play around with the strike prices all you want. Going farther out of the money increase your returns, but raises your risk as well. Going closer to the money reduces risk and returns, but the gains are still a multiple of the underlying stock.

Buying when everyone else is throwing up on their shoes is always the best policy. That way your return will rise to ten times the move in the underlying stock.

Amgen (AMGN) - January 21 2022 $235-$240 bull call spread at $3.68 delivers a 172% gain with the stock at $245, up 14% from the current level

Biogen (BIIB) - January 21 2022 $365-$375 bull call spread at $3.89 delivers a 157% gain with the stock at $375, up 14% from the current level

Johnson & Johnson (JNJ) - January 21 2022 $150-$155 bull call spread at $1.63 delivers a 206% gain with the stock at $155, up 8.3% from the current level

Pfizer (PFE) - January 21 2022 $40-$45 bull call spread at $1.05 delivers a 376% gain with the stock at $40.60, up 11.5% from the current level

Bristol Meyers Squibb (BMY) - January 21 2022 $65-$70 bull call spread at $1.50 delivers a 233% gain with the stock at $68, up 11.40% from the current level

Mad Hedge Biotech & Health Care Letter

October 29, 2019

Fiat Lux

Featured Trade:

(THE BIG MEDICARE PLAN WITH HUMANA),

(ANTM), (CI), (HUM), (UNH)

Sometimes, markets are right, and sometimes, they are wrong. With regard to the healthcare industry these days, they have definitely got it wrong. For they are overweighting the political risk to this group presented by the 2020 presidential election.

Even if the most extreme leftist candidate, Elizabeth Warren, wins, she will still have to get the plans through congress. And after the experience of the last three years, you can bet the next congress will be a pretty moderate bunch.

Just as President Trump found it impassable to kill Obamacare, even with an all-Republican Congress, Warren will find it equally difficult to get the most expensive form of Medicare for all passed into law.

Take this view, and all of a sudden, the healthcare industry becomes wildly cheap. In fact, it is one of the lowest valued, highest earning sectors in the entire stock market.

Shares of managed care companies have certainly struggled this year. For instance, Anthem (ANTM) went down 5.1%, Cigna (CI) sunk 13.2%, UnitedHealth Group (UNH) declined by 2.2%, and Humana (HUM) fell 0.3%.

Due to the country’s turbulent political climate courtesy of the impending 2020 elections, investors are anxious over Medicare for All, which has the capacity to shut down the entire industry altogether.

As expected, these fears have weighed heavily on health insurance stocks and these companies are anticipated to experience a rollercoaster of emotions in the next year and a half. However, there could be convincing reasons for Humana to stand out from the rest.

Zeroing in on “population health management” along with “social determinant of health,” the company has been working on boosting its dominance on nonclinical services to deliver better health results. This is because approximately 80% of health outcomes are linked to nonclinical issues. Hence, this initiative could lead to improved products for customers and cost savings.

This is why Medicare Advantage, which allows private insurers to collaborate with Medicare for care coverage, turned into the “crown jewel” of Humana’s growth strategies. Basically, this plan appears and functions like a private health plan but is actually a government-sponsored program.

To date, Humana is the second biggest Medicare Advantage provider growing its membership by 15% during the second quarter of both 2018 and 2019.

As of 2018, the company holds a 17% share of the 20.4 million people enrolled in the Medicare Advantage program, with plans comprising roughly a quarter of the managed care’s medical membership. This accounts for almost three times the industry average, which indicates a positive growth for Humana as Medicare is projected as the fastest-growing sector of the insurance industry in terms of spending.

Actually, basic math could easily illustrate Humana’s upward trajectory as well. The number of Americans eligible for a Medicare plan is increasing by roughly 3% annually. Based on data from the Congressional Budget Office, the number of Medicare recipients opting for Medicare Advantage is estimated to climb from 34% of those eligible for Medicare in 2018 to 42% by 2028. Clearly, this increase offers a lot of room for growth, and Humana is smack dab in the center of it.

Although UnitedHealth actually has more members in the said program at the moment, no other managed care company is as intensive and focused as Humana. In fact, 73% of Humana’s consolidated revenue comes from its Medicare Advantage membership earnings alone. This makes the company a Medicare Advantage pure play.

Holding its position as one of the leaders in this private option available within the Medicare community, Humana has established a stronghold in this ever-evolving and constantly turbulent industry. So far, the stock’s price target is projected to hit $315. Long-term investors could also finally expect to shake off healthcare fear jitters and big rewards from 2021 onwards if the elections result in Democratic leadership.

Looking at Humana’s earnings history, it can be seen that it has grown from $7.75 per share in 2015 to $14.55 by 2018. For this year, the company’s projected earnings is expected to reach $17.50 a share. However, the possibility of a federal tax on health insurers could pose a threat to the company’s growth.

Humana is well-poised for advancement on the back of its strategic plans involving its Medicare business and promising initiatives. In the past years, Humana has been deploying excess capital and hiking its dividend. Just in February 2019, the company increased its dividend by 10% to reach 55 cents a share.

As part of its repurchase strategy, Humana allocated $3 billion for its buyback plans. These moves further indicate the financial capacity of the company and could hopefully reinvigorate investor confidence.