Global Market Comments

March 19, 2021

Fiat Lux

Featured Trade:

(MARCH 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(JPM), (TLT), (TBT), (SQ), (MMM), (SIL), (QQQ), (WMP), (CCIV), (TSLA), (USO), (CRSP), (PLTR), (HYG), (FCX), (XME)

Global Market Comments

March 19, 2021

Fiat Lux

Featured Trade:

(MARCH 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(JPM), (TLT), (TBT), (SQ), (MMM), (SIL), (QQQ), (WMP), (CCIV), (TSLA), (USO), (CRSP), (PLTR), (HYG), (FCX), (XME)

Below please find subscribers’ Q&A for the March 17 Mad Hedge Fund Trader Global Strategy Webinar broadcast from frozen Incline Village, NV.

Q: I’ve heard that the COVID-19 cases are being understated by 16 million. Do you think this is true?

A: Yeah, I've always argued that the previous government's numbers were vastly underestimating the true number of cases out there for political purposes, but we are on the downslide regardless, so that’s good.

Q: When are tech stocks going to bottom out and when can I buy them?

A: I knew I would get this question. This is the question of the day. Picking bottoms is always tough because these are momentum plays and not valuation plays. I’ll give you a couple of levels though. The tech (QQQ) multiple is now at 25X earnings and the S&P 500 (SPY) is at 22X, so your first bottom will be down about 10% from here, or a 22X multiple. And I don’t think we will get much lower than that because tech stocks are growing at 20-25% a year, versus the (SPY) growing at maybe 10%, and I don’t think tech goes to much of a discount in that situation. So, you’re just waiting for interest rates to top out and start to go down, which will be the other indicator of a tech bottom. We had a slowdown in the rise of rates for just a couple of days this week, and tech stocks took off like a rocket. Those are your two big signals.

Q: With the Fed announcement, are you still in the Invesco QQQ Trust NASDAQ ETF (QQQ) bear put spread?

A: Yes, one of them expires in two days so that’s a piece of cake. The other one expires in a month, but it is way out-of-the-money—the April $240-$245 bear put spread, so I’ll keep that for a real meltdown day. But if it looks like we’re getting a breakout, I will come out of that short position so fast it will make your head spin.

Q: Do you like Palantir (PLTR)?

A: Absolutely yes—screaming LEAP candidate. It traded all the way down to $20 two weeks ago and is trading around $25 now. It’s a huge data firm, lots of CIA and defense work, huge government contracts extending out for years, cutting edge technology, and run by a nut job, so yes screaming buy at this level.

Q: Freeport McMoRan (FCX) is taking some pain here, is this still a buy and hold?

A: Yes, it’s taking the pain along with all the other domestic stocks, which is natural. In their case though, it’s up almost 10x from its bottom a year ago where we recommended it, so yeah I'd say time for a rest. So I’m still a buyer of the metals and (FCX) on dips, but like all other metals, it did get overextended. EV manufacturing is doubling this year, which uses a ton of copper. The same is true with solar panels and Chinese industrial recovery. When all your major markets are doubling in size, it’s usually good for the stock. I peaked at $50 in the last cycle and could touch $100 in this one.

Q: What are your thoughts about the Lucid EV SPAC, Churchill Capital IV (CCIV)?

A: Don’t touch it with a ten-foot pole. They only have 1 or 2 concept vehicles for high-end investors to test drive. The rumor is that their main factory will be in Saudi Arabia where the bulk of the seed capital came from. They’ll never catch up with Tesla (TSLA) on the technology. There's always going to be a few niche $250,000 cars out there, and they have no proof they can actually make these things. When they get to a million vehicles a year, then I might be interested. But they haven't done the hard part yet, which is mass-producing battery packs for a million cars. They've only done the easy part which is designing one sexy prototype to raise money. So, stay away from Lucid, I don’t think they’re going to make it.

Q: What about oil?

A: I am avoiding oil plays like the plague.

Q: When do you anticipate your luncheons to be back?

A: Maybe in 2023. I don’t want to scare off my customers by inviting them to a lunch where they all get COVID-19. If I did have a lunch, I’d have a vaccine requirement and a temperature gun to hit them at the door like everywhere else. I really miss meeting subscribers in person.

Q: Should I buy banks like JP Morgan (JPM) at this level?

A: I would say no. That ship has sailed. Wait for a steeper selloff or just let it run. We’ve already had an enormous move and you don’t want to chase it with a low discipline trade, which is what that would be.

Q: What do you think of silver (SLV)?

A: It’s a buy long term, short term it’s in the grim spiral of death along with the other precious metals, which absolutely hate rising interest rates. A silver long here is the equivalent of a bond (TLT) long. When you do go into silver, buy Wheaton Precious Metals (WPM) for the leveraged long play.

Q: Is 3M (MMM) going to extend the upside?

A: Probably yes, that's a classic American industrial play and a great company. I have friends who work there. How could we live without Post-it notes, Scotch Tape, and Covid-19 N-95 masks?

Q: What about Square (SQ)?

A: I love it in the long term, buy on the dips and buy it through LEAPS (long term equity anticipation securities).

Q: Should I unwind my leveraged financial ETF?

A: I’d say take a piece off, yeah; you never get fired for taking a profit. And they have had a tremendous move. Plus of course, the flip side of taking profits on domestic recovery stocks is to buy tech with that money. And eventually, that's what the entire market will do, it just may still be a little bit early.

Q: What’s a good target for LEAPS for CRISPR (CRSP) and Palantir (PLTR)?

A: Put your first strike 30% higher than today’s stock price and go 2 years out in maturity. I noticed on some names, the June 2023’s are starting to trade, but they’re highly illiquid. But if you put a bid in there and you get a market meltdown, you will get hit.

Q: If the long-term future for oil (USO) is so bad, why is it $65?

A: A few reasons. #1, huge short covering action. #2, economy recovery faster than people expected because of the stimulus. #3, a lot of people, mostly in Texas, Oklahoma, and Louisiana, don’t believe that there will be an all-electric grid in 20 years and think that oil will be in demand forever, including the entire oil industry, so they’re in there buying. And #4, the Saudis have held back with production increases to push the price up, so they’re letting it run so they can sell at a higher price. When they do sell, oil crashes again.

Q: Can we re-watch this presentation?

A: Yes, we post it about 2 hours later on the website so all our people in about 135 countries can access it whenever they like. Just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Q: How often do you have these webinars?

A: Every two weeks, and if you need help accessing it on your account page, email customer support at support@madhedgefundtrader.com.

Q: Is it time to initiate short positions on oil companies?

A: Not yet but keep it in the back of your mind. When some of the super-hot economic data come out after Q2, that may be your short in oil—then we may get into the $70’s a barrel. But not yet, there’s still too much upward momentum.

Q: Do you think we will see the 30-year fix below a 3.00% yield again?

A: Yes, in the next recession, which may be 5 or 10 years off because we’re starting at such a low base.

Q: Regarding copper, EV motors require a ton of copper. Doesn’t that make the metals a BUY?

A: That is true, and why we recommended Freeport McMoRan at $4 a year ago and recommended buying every dip. Each one of these rotor motors on each wheel of a Tesla weighs about 100 lbs—I’ve lifted them. Remember I tore apart a Tesla once just to see what made it tick, and they’re really heavy, and they use a lot of copper, and silver as well. So that has always been the bull market case for copper, as well as the fact that China re-emerged as a major buyer for their industrial buildout. That’s why we had a long in the SPDR S&P Metals and Mining ETF (XME).

Q: Do you foresee a good opportunity to go heavy into margin again?

A: Maybe if we get a decent selloff this summer, but you’ll never get the opportunity we had a year ago when you really wanted to put 100% of your portfolio into 2-year LEAPS. The people who did that made many tens of millions of dollars, which is why I get a free bottle of Bourbon every month. That was a once in 20 years event.

Q: What is your 2021 target for the S&P 500 (SPX)?

A: $4,860. It’s in my strategy letter which I sent out on January 6th, and that is all still posted on the website, click here for it.

Q: How do I renew my subscription with your company, and how do I figure out what I bought?

A: Email customer support at support@madhedgefundtrader.com and they will answer you immediately.

Q: Do you follow the iShares IBoxx High Yield Corporate Bond ETF (HYG)?

A: Yes, that is the high yield junk bond fund, but I have been avoiding long bond plays, as you may have noticed with my screaming short of the past year. We list (HYG) in these slides in the Bonds section.

To watch a replay of this webinar, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER (as the case may be), then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 24, 2020

Fiat Lux

FEATURED TRADE:

(WHY TECHNICAL ANALYSIS IS A DISASTER)

(THE COOLEST TOMBSTONE CONTEST)

(SJB), (JNK), (HYG)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader April 8 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Is it premature to be buying long-term LEAPS?

A: Absolutely not—a long-term leap is a bet that your stock will recover beyond your strike prices in two years, which I certainly believe is the case with all of the quality tech and biotech names. These are pretty illiquid so the only way to get a good price is to have a bid in place on one of those absolute puke out days. You will never buy these at the bottom.

Q: Do you see a rally in the stock market in the fourth quarter of this year after the election?

A: For sure—we should be well clear of the pandemic by then, and all of the $6 trillion stimulus will be hitting at the same time.

Q: With the rally in the S&P 500, would you double up on the (SPY) put spread—the May $300-$310?

A: No, keeping your leveraged positions small is crucial in this kind of environment, and the big short play is basically behind us. Better to add the 2X ProShares Ultra Short S&P 500 (SDS) to catch a smaller move down.

Q: Will gold work if the market sells off as a safety trade?

A: Yes, it will. Gold (GLD) had that big 15% selloff a couple of weeks ago when it looked like all financial markets worldwide were going to completely freeze up, and everyone got margin calls all at the same time. We are clear of that now and I expect gold and other traditional hedges like shorting volatility, for example, to also work as a hedge. Gold is going to a new all-time high soon. Buy (GLD), (GDX), (GOLD), and (NEM).

Q: When do you think international borders will open up again, and will that have a positive effect on the economy?

A: Absolutely. You can expect the market to rally 10% into the opening of borders, and then another 10% afterwards depending on where the starting point for the market is in that. As for timing, they may open up in June, and then close up in again in the fall when a second Corona wave hits.

Q: Will you teach us how to buy LEAPS?

A: Just go to my website, type in LEAPS in all caps, and everything you need to know about leaps is there. I will also be following up soon with more individual stock LEAPS ideas, but I don’t want to put them out now because we have just had a $5,000-point rally on the Dow.

Q: Please talk about 5G.

A: The best play is Qualcomm (QCOM). They have a near-monopoly on a 5G chip which virtually the entire world has to buy. The stock has also held up incredibly well. Buy two-year LEAPS on Qualcomm with probably a $90 or $100 strike price.

Q: What level in the S&P do you think this will fail?

A: I think it will fail right around here, so that's why I have been adding on the short positions on every rally. We are exactly at halfway point between the February high and the March low, which is a perfect bear market rally.

Q: What’s the definition of the next big dip?

A: You give up the 5000-point rally we just had, and whether we give up 4000 or 6000 of it, at these kinds of conditions, 1000 points in the Dow (INDU) is a round lot, like the daily move. So, looking at the charts and these lows, it could be a $19,000, $18,000, or $17,000.

Q: Fundamentals may tell you the virus may be peaking, but the worst of the economy is yet to come.

A: True. Do all the markets follow fundamentals now? No, they will look at the virus numbers. Economic numbers are utterly meaningless and out of date here. I wouldn’t depend on them at all, just look at the new cases every day from the Johns Hopkins website, and that gives you a better buy signal than any economic indicator can.

Q: Are all the good shorts are over?

A: When I say shorts are over, from here you’re not going to get the 80% and 90% down moves that we have seen so far; those are gone. The reason I bought the 2X ProShares Ultra Short S&P 500 (SDS) is to play for the bottom end of the range, which could be down 2000 to 4000 points from here, and also to hedge the short volatility (VXX) puts that I already have. A rising market should make the (VXX) go down, and a falling market will make the (VXX) and the (SDS) go up. So, it's both a hedge and a view on a range of a market.

Q: Could the Federal Reserve buy shares?

A: Yes, they have done that already in Japan, with no success whatsoever in helping the economy, but I doubt the Fed will buy shares here. The government will take minority share ownerships in the troubled industries like the airlines, much like they did with (GM) and the top 20 banks during the 2008-09 crash and sell them later at huge profits. I don't expect them to go beyond that. The Fed here has too many other things to buy, like all of our different bond and money markets; those don't exist in other countries like Japan or Europe. Stocks are often the only thing they can buy, and in Japan’s case, they already own the entire government bond market, so they had nothing else left to buy besides stocks.

Q: How about buying Boeing (BA)?

A: I would buy Boeing LEAPS here, something like a $170-$180. If you’re going to make a 1,000% return on LEAPS on any one stock, it's going to be Boeing. That company will be around somehow, and you could get literally a 10-fold return just by going 50% out of the money on two-year LEAPS.

Q: How is liquidity on 2-year 30% out of the money LEAPS?

A: It is practically nonexistent. You have to put in a limit order and then wait for a dump in the market to get filled. That’s how all the people who have been doing LEAPS have been getting them. Put in a bid and when you get these cataclysmic, down-1,000-point days, they hit any bid. The algos go in there and they just say hit any bid, and you can get done at incredible prices in those situations.

Q: Are the fees on (SDS) a problem?

A: No, your standard equity commission is all you should be paying. They trade like water.

Q: Would you short junk bonds short-term?

A: No, because you short the (HYG) or the (JNK), you are shorting a 7.5% yield which you have to pay if you’re short, so the great short in junk bond play was in February when it was yielding 4.5%. It’s too late now.

Q: Will treasuries go to zero?

A: They could, but we’re close enough to zero where you might as well think of them at zero.

Stay healthy all.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 6, 2019

Fiat Lux

2020 Annual Asset Class Review

A Global Vision

FOR PAID SUBSCRIBERS ONLY

Featured Trades:

(SPX), (QQQQ), (XLF), (XLE), (XLY),

(TLT), (TBT), (JNK), (PHB), (HYG), (PCY), (MUB), (HCP)

(FXE), (EUO), (FXC), (FXA), (YCS), (FXY), (CYB)

(FCX), (VALE), (AMLP), (USO), (UNG),

(GLD), (GDX), (SLV), (ITB), (LEN), (KBH), (PHM)

Global Market Comments

November 13, 2019

Fiat Lux

Featured Trade:

(HOW TO HANDLE THE FRIDAY, NOVEMBER 15 OPTIONS EXPIRATION),

(TAKE A RIDE IN THE NEW SHORT JUNK ETF),

(SJB), (JNK), (HYG),

(THE COOLEST TOMBSTONE CONTEST)

Stocks will drop sharply in the coming year. It will most likely happen when the Democratic candidate takes a substantial lead over the president, which recent by-elections have shown is likely.

What could be better than an ETF that benefits from both falling bonds AND stocks?

It just so happens that there is such an animal.

When you look at the profusion of new ETFs being launched today, you find that they almost always correspond with market tops.

The higher the market, the greater the demand for the underlying, and the more leverage traders bay for it. The resulting returns for investors are usually disastrous.

But occasionally, a blind squirrel finds an acorn, and if you fire buckshot long enough, you hit a barn.

That’s why I am getting interested in the new ProShares Short High Yield ETF (SJB). After riding the bull move in junk all the way up with (JNK), (HYG), I have recently turned negative on the sector.

Junk bonds have moved too far too fast. Current spreads for junk paper are now only 200 basis points over equivalent term Treasury bonds, and investors at these levels are in no way being compensated for their risk.

If the stock market starts to roll over in 2018, then the junk bond market will follow it in the elevator going down to the ladies' underwear department in the basement.

Keep in mind that when shorting the junk market, you run into the same problem you have with the (TBT), a leveraged short ETF for the Treasury bond market.

Buy the (JNK) and you are short a 5.75% coupon which, with the management fees, works out to a monthly cost of more than 50 basis points. That is a big nut to cover.

So timing for entry into this fund will be crucial

Global Market Comments

September 20, 2019

Fiat Lux

Featured Trade:

(SEPTEMBER 18 BIWEEKLY STRATEGY WEBINAR Q&A),

(TLT), (FDX), (FB), (HYG), (JNK), (EEM), (BABA), (JD), (TBT), (FXE), (UUP), (AMZN), (FB), (DIS), (MSFT), (USO), (INDU),

(THE GREAT TRADING GURU SPEAKS)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader September 18 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What would happen to the United States Treasury Bond Fund (TLT) if the Fed does not lower rates?

A: My bet is that it would immediately have a selloff—probably several points—but after that, recession worries will take bond prices up again and yields down. I don’t think we have seen the final lows in interest rates by a long shot. That’s why I bought the (TLT) last week.

Q: Is it good to buy FedEx (FDX) considering the 13% fall today?

A: I use the 3-day rule on these situations. That's how long it takes for the dust to settle from an earnings shock like this and find the real price. The problem with FedEx is that it’s a great early recession predictor. When the number of delivered packages decreases, it’s always an indicator that the economy as a whole is slowing down, which we know has been happening. It’s one of the most cyclical stocks out there, therefore one of the most dangerous. I wouldn’t bother with FedEx right now. Go take a long nap instead.

Q: Would you be a buyer of Facebook (FB) here, given they seem to have weathered all the recent attacks from Washington?

A: Not here in particular, but I would buy it 20% down when it gets to the bottom edge of its upward channel—it still looks like it’s going crazy. They’re literally renting or buying buildings to hire an additional 50,000 people in San Francisco anticipating huge growth of their business, so that’s a better indicator of the future of Facebook than anything.

Q: Will junk bonds be more in demand now that rates are cratering?

A: Junk bonds (HYG), (JNK) are driven more by the stock market than the bond market, as you can see in the huge rally we just had. Junk bonds are great because their default ratios are usually far below that which the interest rate implies, but you really have to trade them like stocks. Think of them as preferred stocks with really high dividends. When the stock market tops, so will junk bonds. Remember in 2008, junk yields got all the way up to 15% compared to today’s 5.6%.

Q: What will happen to emerging markets (EEM) as rates lower?

A: If lower interest rates bring a weaker US dollar, that would be very positive for emerging markets over the long term and they would be a great buy. However, emerging markets will take the hardest hit if we actually do go into a recession. So, I would pass for now.

Q: What are your thoughts on Alibaba (BABA) and JD.com (JD)?

A: They are great for the long term. However, expect a lot of volatility in the short term. As long as the trade war is going on, these are going to be hard to trade until we get a settlement. (JD) is already up 50% this year but is still down 40% from pre trade war levels. These things will all be up 20-30% when that happens. If you can take the heat until then, they would probably be okay for a long-term portfolio globally diversified.

Q: What do you have to say about the ProShares Ultra Short 20+ Year Treasury ETF (TBT)—the short bond ETF?

A: If you have a position, I’d be selling now. We just had a massive 20%, 4-point rally from $22 to $27 and now would be a good time to take a profit, or at least get out closer to your cost. The zero interest rates story is not over yet.

Q: Would you short the US dollar?

A: I would most likely short it against the euro (FXE), which now has a massive economic stimulus and quantitative easing program coming into play which should be positive for it and negative for the US dollar (UUP). That’s most likely why the euro has stabilized over the last couple of weeks. That said, the dollar has been unexpected high all year despite falling interest rates so I have been avoiding the entire foreign exchange space. I try to stay away from things I don’t understand.

Q: If all our big tech September vertical bull call spreads are in the money, what should we do?

A: You do nothing. They all expire at the Friday close in two trading days. Your broker should automatically use your long call position to cover your short call position and credit your account with the total profit on the following Monday, as well as release the margin for holding that position. After that, we’ll probably wait for another good entry point on all the same names, (AMZN), (FB), (DIS), (MSFT).

Q: If the US fires a cruise missile at Iran, how would the market react?

A: It would selloff pretty big—markets hate wars. And the US wouldn’t send one missile at Iran; it would be more like 100, probably aimed at what little nuclear facilities they have. I doubt that is going to happen. The world has figured out that Trump is a wimp. He talks big but there is never any action or follow through. Inviting the Taliban to Camp David while they were still blowing up our people? Really?

Q: Will the housing market turn on the turbochargers after this dip in rates?

A: It wouldn't turn on the turbochargers, but it might stabilize the market because money is available now at unprecedentedly low interest rates. However, we still have the loss of the SALT deductions—the state and local taxes and real estate taxes that came in with the Trump tax bill. Since then, real estate has been either unchanged or has fallen on both the East and West coast where the highest priced houses are. It’s the most expensive houses that take the loss of the SALT deduction the hardest. Don’t expect any movement in these markets until the SALT deduction comes back, probably in 16 months.

Q: What catalyst do you think would cause a 10% correction in the next 2-3 months?

A: Trump basically saying “screw you” to the Chinese—a tweet saying he’s going to bring another round of tariff increases. That’s worth a minimum of 2,000 points in the Dow Average (INDU), or about 7% percent. Either that or no move in Fed interest rates—that would also create a big selloff. My guess is that and adverse development in the trade war will be what does it. That’s why my positions are so small now.

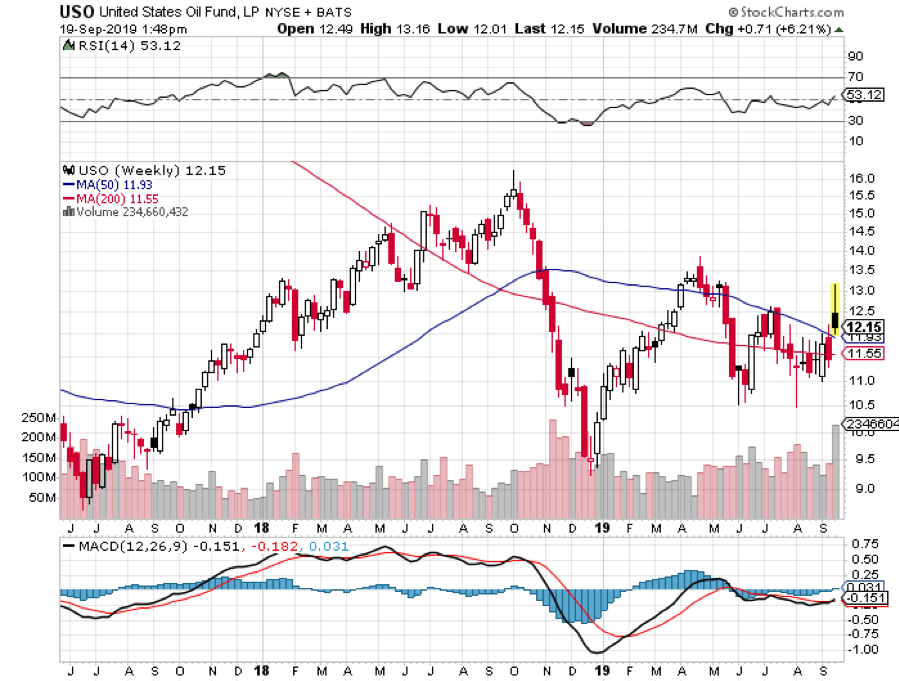

Q: We have a big short position in the United States Oil Fund (USO) now. Are you going to run this into expiration until October $18?

A: Even though oil has already collapsed by 10% since we put this position on last Friday, premiums in oil options are still close to record levels. So, it pays us to hang on for the time decay. The world is still massively oversupplied in oil and the Saudis were able to bring half of the lost production back on in a day. Oil will keep falling unless there is another attack and it is unlikely we will see one again on this scale. And, we only have 20 more days to go to capture the full 14.8% profit.

Good luck and good trading.

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

Global Market Comments

January 9, 2019

Fiat Lux

2019 Annual Asset Class Review

A Global Vision

FOR PAID SUBSCRIBERS ONLY

Featured Trades:

(SPX), (QQQQ), (XLF), (XLE), (XLI), (XLY),

(TLT), (TBT), (JNK), (PHB), (HYG), (PCY), (MUB), (HCP)

(FXE), (EUO), (FXC), (FXA), (YCS), (FXY), (CYB)

(FCX), (VALE),

(DIG), (RIG), (USO), (UNG), (USO), (OXY),

(GLD), (GDX), (SLV),

(ITB), (LEN), (KBH), (PHM)