No other industry has ever been watched as closely in 2020 as the healthcare and biotechnology sector, with drug developers placed under pressure to deliver COVID-19 treatments and vaccines within an unprecedented timeframe.

Despite all the attention and fanfare, the overall performance of the sector’s stocks remained underwhelming. However, 2021 promises to bring in better returns and bring back the industry to pre-pandemic performance.

For perspective, the S&P 500 Health Care Sector Index rose by 8% through mid-December compared to the 13% increase of the S&P 500.

The financial and health crises affected the performance of the subgroups in different ways. For example, the diagnostics subgroup jumped by 31% while the demand for clinical labs was up 18%.

Meanwhile, biotechnology stocks rose by 13%. In comparison, traditional pharmaceutical stocks and even hospitals only managed to record a measly 3% increase.

As for retail pharmacies, this subgroup sank by 18%.

Despite the underperformance of the industry, there are still companies that stood out this year and are poised to soar come 2021.

One of them is Vertex Pharmaceuticals (VRTX).

Vertex is possibly one of the most undervalued large-cap biotechnology stocks in the market today.

This company, which has $61.7 billion in market capitalization, has been continuously growing and transforming into the most dominant player in the cystic fibrosis (CF) space.

Truth be told, Vertex holds the monopoly on the approved drugs used to treat CF, namely, Trikafta, Kalydeco, Orkambi, and Symdeko.

With the recent approvals the company received, this momentum is expected to grow.

Vertex just won additional EU approval for its CF drug Kaftrio. This indicates another cash cow for the company as the drug, also known as Trikafta, already transformed itself into a megablockbuster in the US market.

Apart from its efforts to continuously dominate the CF sector, Vertex also has several moonshots that can eventually turn into major catalysts.

Among those is its partnership with CRISPR Therapeutics (CRSP).

The two biotechnology companies are developing a gene therapy, called CTX001, which can cure rare genetic blood diseases. Specifically, CTX001 is designed to cure beta-thalassemia and sickle cell disease.

Apart from its partnership with CRISPR Therapeutics, Vertex also acquired Semma Therapeutics in 2019 with the goal of coming up with a cure for Type 1 diabetes.

If things go as planned, a gene therapy for this genetic disease will advance to clinical testing by early 2021.

Another under the radar biotechnology stock set to soar in 2020 is Illumina (ILMN).

Illumina, with a market capitalization of $54.10 billion, is the leader in the genomics market.

Since the pandemic broke, the biotechnology sector’s leading manufacturer of hardware for genetic sequencing has been supplying testing kits for hospitals across the US.

Apart from Illumina, other companies in the genomics sectors include Vertex’s partner, CRISPR Therapeutics, which has a market capitalization of $4.48 billion, and bluebird bio (BLUE) with $4.03 billion.

In a nutshell, genomics refers to the analysis of the genetic information found in human cells. Companies working on this field aim to not only develop more accurate and efficient disease testing processes but also come up with more personalized treatments for a range of diseases including cancer.

Looking at Illumina’s profile and even taking into consideration the effects of the recession along with the competitive pressure to be expected soon enough, this biotechnology company is still set to deliver solid returns over the next 3 to 5 years.

Ever since its establishment, Illumina has been hailed as the leader in the gene-sequencing segment.

To date, the company holds almost 90% of the market.

Apart from that, the company has been an active participant in the move to lower the costs of gene-sequencing processes. In effect, Illumina managed to expand its customer reach.

Illumina’s participation in the 13-year Human Genome Project, which started at $3 billion per genome submitted for sequencing in 2003.

Nowadays, the cost has dropped to $800 for each genome, with Illumina eyeing to drop the price to $100 via its NovaSeq platform.

Based on the company’s performance in the past years, Illumina’s revenue is expected to climb higher annually in the next 5 years.

By 2021, the company is projected to report a 21.16% year over year growth in annual revenue to reach 4.23 billion.

Meanwhile, its 2022 annual revenue is estimated to hit $4.79 billion, showing off a 13.37% increase.

Despite the attention it has been receiving, Illumina remains a bargain buy.

This is because the company’s gene-sequencing projects have been moving along at a decent pace even before the COVID-19 crisis hit.

Given the company’s growth and future plans, Illumina is a no-brainer long-term investment. However, investors looking for quick returns might find the company’s pace a bit sluggish for their liking.

Among the biotechnology companies out there today, I think Vertex and Illumina stand out the most because both hold a monopoly in their respective fields.

Sure, there would be competition eventually but the combination of all their strengths and the strong potential of their pipeline put them in a league of their own.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-12-31 12:00:542021-01-05 00:39:50Monopoly is the Name of the Game

Followers of the Mad Hedge Fund Trader alert service have the good fortune to own FOUR deep in-the-money options positions that expire on Friday, July 17, and I just want to explain to the newbies how to best maximize their profits.

These involve the:

Seattle Genetics (SGEN) 7/140-$145 call spread

Illumina (ILMN) 7/$320-$330 call spread

Regeneron (REGN) 7/$570-$580 call spread

JP Morgan Chase (JPM) 7/$80-$85 call spread

Provided that we don’t have another 3,000-point move down in the market by next week, these positions should expire at their maximum profit points.

So far, so good.

I’ll do the math for you on our oldest and least liquid position which I almost certainly will run into expiration. Your profit can be calculated as follows:

Profit: $5.00 expiration value - $4.30 cost = $0.70 net profit

(23 contracts X 100 contracts per option X $0.70 profit per option)

= $1,610 or 16.27% in 18 trading days.

Many of you have already emailed me asking what to do with these winning positions.

The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck, and pat yourself on the back for a job well done.

You don’t have to do anything.

Your broker (are they still called that?) will automatically use your long position to cover your short position, canceling out the total holdings.

The entire profit will be credited to your account on Monday morning July20 and the margin freed up.

Some firms charge you a modest $10 or $15 fee for performing this service.

If you don’t see the cash show up in your account on Monday, get on the blower immediately and find it.

Although the expiration process is now supposed to be fully automated, occasionally machines do make mistakes. Better to sort out any confusion before losses ensue.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. You can probably unload them pennies below their maximum expiration value.

Keep in mind that the liquidity in the options market understandably disappears, and the spreads substantially widen, when a security has only hours, or minutes until expiration on Friday, July 17. So, if you plan to exit, do so well before the final expiration at the Friday market close.

This is known in the trade as the “expiration risk.”

One way or the other, I’m sure you’ll do OK, as long as I am looking over your shoulder, as I will be, always. Think of me as your trading guardian angel.

I am going to hang back and wait for good entry points before jumping back in. It’s all about keeping that “Buy low, sell high” thing going.

I’m looking to cherry-pick my new positions going into the next month-end.

Take your winnings and go out and buy yourself a well-earned dinner. Just make sure it’s take-out. I want you to stick around.

Well done, and on to the next trade.

You Can’t Do Enough Research

https://www.madhedgefundtrader.com/wp-content/uploads/2019/09/john-and-girls.png322345Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-07-10 09:02:552020-07-10 09:17:12How to Handle the Friday, July 17 Options Expiration

The free Fed put was tested once again last week, and once again it held. It seems that the line in the sand is $300 for the (SPY), and if that doesn’t hold, $270 will do. At least, for a month.

How long this game will last is anyone’s guess. $14 trillion is a lot of money to throw at the problem. But then so are US Covid-19 deaths approaching 1,000 a day. Who knows what Jay Powell has up his sleeve? Probably quite a lot.

A large chunk of the US economy has gone missing and is never coming back, especially the portion represented by small companies. Whether stock investors will notice this will be the big bet for the remainder of 2020. My bet is they will if the spread of the epidemic can’t be stopped. I give it a 50/50 chance.

If the worst-case scenario happens, get ready to load the boat of LEAPS once again, for we have a Roaring Twenties and second American Golden Age ahead of us, if you can live to see it. We are one wonder drug discovery away from that starting tomorrow morning at 9:00 AM.

We got encouraging news last week with the commonplace steroid dexamethasone, which reduces deaths by 30%. Publishing the Mad Hedge Biotechnology & Health Care Letter, I can tell you there are hundreds more drugs like this under rapid development. Click here. There is no doubt that biotech stocks (IBB) are breaking out to the upside. Take a look at the ten largest components of the iShares NASDAQ Biotechnology ETF and you’ll see they all have virtually the same chart (click here), stocks like Amgen (AMGN), Gilead Sciences (GILD), and Illumina (ILMN) The trillions of dollars pouring into Covid-19 research is a big driver. In the meantime, past headaches have magically gone away, like the threat of a nationalization and drug price controls. No one feels like regulating drug companies in this environment. Almost all impediments to research have been tossed away. Relative to the rest of the superheated stock market, biotech shares are still cheap.

The Fed is to starting to buy individual bonds, in another unprecedented expansion of quantitative easing. They are clearly worried about exploding Corona cases, as I am. US Treasury bonds (TLT) dove two points on the news as this may represent a diversion of Fed buying from that market. Stocks soared 1,000 points.

The big message is more QE to come. Another election play? It is called “QE Infinity” for a reason. It’s a great level to trade against. I hope you loaded up on tech LEAPS at the bottom, as I begged you to do.

The Fed balance sheet soars, from $4 trillion to $7 trillion this year, says Fed governor Jay Powell. It is the fastest debt blow up in history. That’s $18,750 per taxpayer in four months. It could be $10 trillion by yearend. If you received less than this stimulus money, you got screwed. This always ends in stagflation….high inflation and slow growth, like we saw after the Vietnam War. Your grandkids are going to have to take side jobs driving for Uber to pay off this bill.

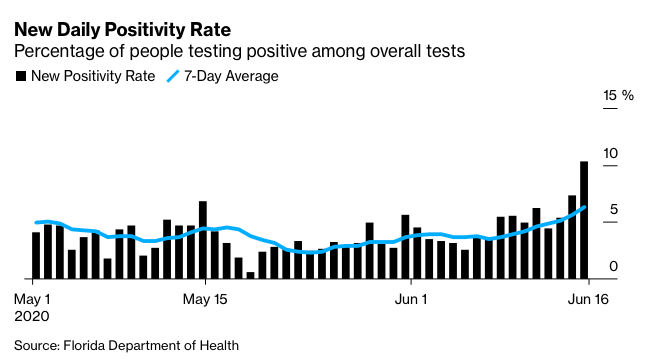

Reopening states see corona cases explode, tossing the “V” shaped economic recovery out the window. Some 25 states are seeing a rapid rise in new cases. Is this the second wave or an extension of the first? The green shoots have been squashed. Stocks won’t like it. The free pass is over.

Stocks pop on miracle steroid drug that reduces Covid-19 death rates. Dexamethasone is the drug in question, normally used for arthritis treatments. It’s just in time as Beijing is closing down schools again in the wake of a second wave.

A US dollar crash is a sure thing, says my old Morgan Stanley colleague, Steven Roach. I couldn’t agree more. Steve is expecting a 35% swan dive for Uncle Buck. A negative savings rate combined with a retreat from Globalization is a toxic combo. A 1970s type stagflation could ensue.

Weekly Jobless Claims are still sky-high, at 1.51 million, far above estimates. The Dow gave up 300 points at the opening, then quickly clawed it back. Walk down Main Street these days and they are still filled with empty storefronts. Many companies are simply running out of money, unable to wait for a recovery. In the meantime, Corona cases are hitting new records every day. Florida cases are off the charts. Things will get worse before they get better.

Retail Sales posted record pop, up 17.7% in May. You are going to see a lot of these record data points because we are coming off a near-zero base. It will actually take years to get to January business levels. I’m sorry, but the higher the free Fed put drives the stock market, the worse the long-term outlook for the economy is going to be.

Homebuilder Confidence is off the charts, with Sales Expectations jumping 22 points to 68. It’s a positive perfect storm, with record-low 2.90% 30-year fixed rate mortgage, Fed buying of mortgage securities and a massive Millennial tailwind that I have been calling for years. A sudden Corona-driven urban flight is sending customers into the arms of suburban builders. Get into Lennar Homes (LEN), KB Homes (KBH), and Pulte Homes (PHM) on dips if you can.

Tesla (TSLA) to open the second US factory this year, somewhere in the southwest as demand overwhelms supply for electric vehicles, exacerbated by the two-month Corona shutdown. The tax break bidding war has already begun, with Texas and Oklahoma slugging it out. The factory comes with 5,000 jobs. Tesla got its first factory for free, giving stock to Toyota for $10 a share. It was the best investment Toyota ever made.

The Mad Hedge June 4 Traders & Investors Summit recording is up. For those who missed it, I have posted all 9:15 hours of recordings of every speaker. This is a collection of some of the best traders and investors I have stumbled across over the past five decades. To find it, please click here.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

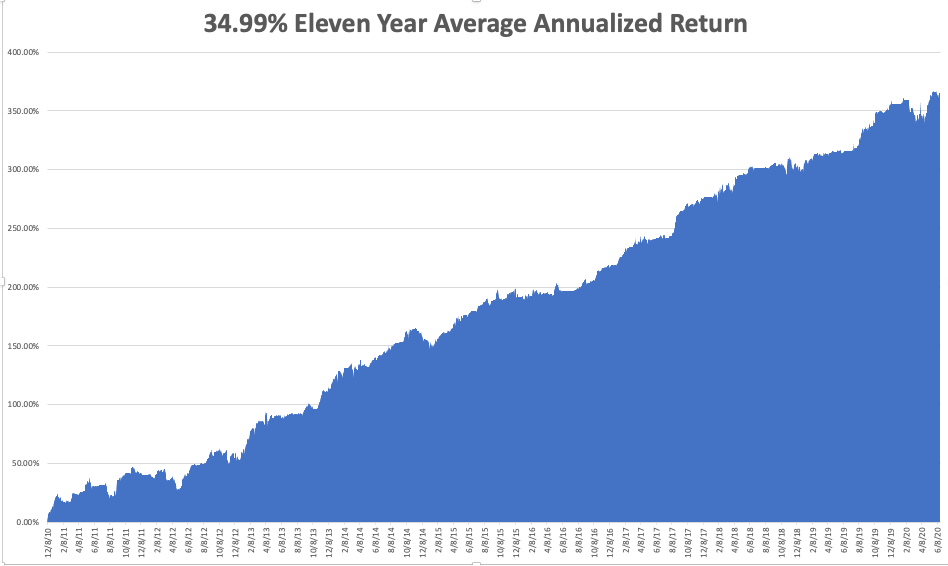

My Global Trading Dispatch performance nicely recouped the pasting we took last week, taking in a nice 7%, bringing June in at +1.21%. With the June options expiration, we managed to cash in on the accelerated time decay in seven positions for Global Trading Dispatch and another three for the Mad Hedge Technology Letter. My eleven-year performance stands at a new all-time high of 367.44%.

That takes my 2020 YTD return up to a more robust +11.53%. This compares to a loss for the Dow Average of -9.2%, up from -37% on March 23. My trailing one-year return popped back up to 51.92%. My eleven-year average annualized profit recovered to +34.99%.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here. On the economic front, some low-grade inflation numbers are published.

On Monday, June 22 at 11:00 AM EST, the May Existing Home Sales are out.

On Tuesday, June 23 at 11:00 AM EST, May New Home Sales are published.

On Wednesday, June 24, at 8:15 AM EST, the National Home Price Index is printed. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are published.

On Thursday, June 25 at 8:30 AM EST, Weekly Jobless Claims are announced. Also out it the final figure for Q1 GDP.

On Friday, June 26, at 10:00 AM EST, the Baker Hughes Rig Count is out. At 11:00, we get the University of Michigan Inflation Expectations.

As for me, I’ll spend the weekend modernizing my camping equipment, some pieces of which are WWII surplus, or are at least 50 years old. Since all of the Boy Scout summer camps for the year have been cancelled, such a Philmont and Catalina Island, I’m creating my own.

We’re going on a 50-mile hike around California’s High Sierra Desolation Wilderness, a part of Northern California my family has been fishing at for a hundred years.

We’ll be trekking on the Pacific Crest Trail featured in the film Wild. I’ll try to regale you with pictures on my return and wild fish stories.

It’s easier said than done, for there is a national camping boom going on. It can be difficult to get simple things, like maps, without an August delivery date. Some of my WWII stuff may have to suffice after all.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Wine Tasting is Just Not the Same

https://www.madhedgefundtrader.com/wp-content/uploads/2020/06/john-wine-tasting-mask.png432324Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-06-22 09:02:352020-06-22 09:35:52The Market Outlook for the Week Ahead, or The Fed Rides Again

Hyper-personalized treatments, otherwise known as precision medicine, have been hailed as one the hallmarks of the healthcare revolution in the past decade.

Although a lot of people don’t see the need for such personalized treatments, a 2017 study by Boston medicine professor Jason Vassy indicated otherwise.

In his paper, titled “Annals of Internal Medicine,” Vassy discussed how his team performed whole-genome sequencing to 100 perfectly healthy adults.

To give you a better picture of how big this project was, whole-genome sequencing involves the analysis of the entire body’s DNA -- yes, all 3 billion pairs of letters found in every individual’s body.

So, you can imagine how tedious and complicated Vassy’s process was and why a lot of people found that to be incredibly pointless, especially since the adults in the study are all “healthy.” More importantly, the naysayers believed that this process would only bring unnecessary panic and anxiety to the subjects.

However, the results shocked them as 20% of the people tested positive for rare, life-threatening conditions that required immediate medical attention.

This prompted more experts to delve deeper into gathering genetic data sets in an effort to bolster the preventive power of genomics. This movement was supported by the National Institutes of Health in 2018 via their “All of Us” project, investing $27 million.

Meanwhile, a Harvard geneticist named George Church founded a similar organization called Nebula Genomics.

Basically, the idea behind precision medicine is very simple: Understanding how your genome works means knowing exactly how to “optimize” your body.

That means health professionals will be able to determine the perfect diet, perfect exercise routine, and of course, the perfect drugs for every patient. You’ll even learn the diseases your body is most susceptible to and how to prevent those.

At the moment, the biotechnology world only has a handful of companies focusing on precision medicine.

One of the leading biotechnology companies in this field is Illumina (ILMN), which focuses on DNA sequencing.

Utilizing its advanced machines, Illumina has been designing treatments to target specific cells in the human body -- and its efforts have been rewarded in recent years.

So far, Illumina stock has been up by 5,791% since its initial public offering back in 2000.

At the moment, Illumina practically controls approximately 80% of the next-generation sequencing space geared towards human genome analysis.

The key to its success is the company’s move to zero in on short-read data sequencing, which has been known as the cheapest, quickest, and most accurate service available in the market.

Since Illumina is one of the top movers in this field, it has easily become the top dog with a long waiting list of clients willing to pay tons of cash for the biotechnology firm’s machines.

While the machines definitely cost a lot upon purchase, Illumina actually earns more from the follow-up revenues generated from all the instances that a biotechnology or research laboratory uses the company’s technology to sequence a genome.

In 2019, Illumina earned $390 million in instrument revenue and $1.73 billion in consumables profit in the first three quarters alone.

Unfortunately, one of Illumina’s efforts to broaden its hold of the market failed.

The company opened 2020 to bad news as regulatory pressures pushed Illumina to shut down its plan to acquire its rival, Pacific Biosciences (PACB), for $1.2 billion.

While no particular reason was officially given by the reviewing bodies, reports indicate that the merger had been delayed due to fears of creating a monopoly.

Nonetheless, many consider this an odd excuse considering that Illumina’s supposed “monopoly” would actually compete directly with Roche (RHHBY).

For comparison, Roche’s market capitalization is $275 billion while Illumina is at $49 billion. In terms of revenue, Illumina earns $3.5 billion annually while Roche rakes in $56.8 billion.

Nevertheless, Illumina has decided to shrug off the rejection and move on to another potentially lucrative deal -- a 15-year partnership with another up and coming next-generation sequencing company: Qiagen (QGEN).

Initially thought to be a surefire acquisition candidate by Thermo Fisher Scientific (TMO) to the tune of $8 billion, Qiagen opted to reject the offer.

Instead, the smaller biotechnology firm has decided to focus on expanding its product portfolio. In the next five years, Qiagen estimates an earnings growth rate of roughly 9.1%.

Between Qiagen and Illumina, the former focuses more on individually customized treatments or “N-of-1 medicine.”

This has become even more pronounced following Qiagen’s acquisition of N-of-One, which raised $12.4 million in funding at the time, in January 2019.

N-of-One provides precision cancer care services. It offers clinical solutions like molecular interpretation to doctors and other healthcare professionals.

Apart from its partnership with Illumina, Qiagen also collaborates closely with NeoGenomics for cancer genetic testing services and DiaSorin for automated TB testing.

We’re in an era of remarkably personalized medical care.

With more and more genetic data made available for analysis, the rare diseases that boggled the minds of the healthcare industry are gradually becoming a thing of the past.

Now, we have access to tools that help with preventive measures to save us from the rare conditions that plagued our predecessors. If you really stop to think about it, targeted medicine just might be the key to immortality -- or at least to a significantly less disease-laden life.

If you’re looking to invest in Illumina or Qiagen stock (or both), the best thing to do is to take advantage of the next price drop.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/01/illumina.png393393Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-01-16 13:00:252020-01-16 13:55:10The Future of Precision Medicine

No sector has been beaten, maligned, and abused more than the biotech sector in recent years. However, some of them are so bad they’ve become good, which piques my interest.

Investing in biotech stocks is not for the faint of heart. The road to developing and commercializing new drugs is long and riddled with hard battles, and an anxious investor won’t be able to sleep at night.

However, the returns offer incredible gains when everything falls into place. In this sector you’re almost buying lottery tickets rather than investing in shares.

In 1919, the term "biotechnology" was coined by a Hungarian agricultural engineer named Karl Ereky to define the merging of two industries: biology and technology. Almost a century later, Ereky's vision has been realized with thousands of products and services available in the biotech market today.

Despite the advancements of this industry though, the majority of the buy-and-hold investors choose to steer clear of biotech stocks -- and for sensible reasons.

It's no secret that investing in biotechnology firms can be unnervingly risky. Since its advent, investors have been regaled with horror stories of costly stage three drug trials going bust or plummeting stock prices due to the expiration of critical patents. Needless to say, these stories have soured would-be investors on the whole biotech world.

However, inadequate information and a lack of understanding of how the biotech industry really operates along with reliance on the performance of only a handful of biotech stocks may have caused investors to miss out on attractive risk-reward relationships. Not all biotech investments lead to disastrous results.

You may be surprised to learn that shares of the biotech industry has collectively gone up by approximately 70% in the past five years. This proves just how much these biotech companies rewarded their enduring. Success in biotech investing is simply a matter of buckling down to do your homework and applying a tad of common sense.

Throughout this decade, one sector has managed to outperform the S&P 500 index (SPY) in terms of total return annually: the healthcare sector. While there's no guarantee that healthcare stocks will go on to beat the S&P 500 in the years to come, the fact remains that people will continue to need medicines as well as healthcare services regardless of the country's economic status. The increasing reliance of the healthcare industry on technology has put the biotech industry smack dab in the center of all these demands.

I’ll give you some of my favorite plays in the sector.

Vertex Pharmaceuticals (VRTX)

Big-cap pharmaceutical company Vertex Pharmaceuticals Inc currently has the monopoly on the treatment of cystic fibrosis (CF) with three approved drugs out in the market, Kalydeco, Orkambi, and Symdeko, along with several promising products in the pipeline to target other auto-immune diseases.

In June, Vertex turned its sights on the genetic therapy part of the business via an expansion of its ongoing collaboration with CRISPR Therapeutics (CSPR). Vertex also purchased gene therapy firm ExonicsTherapeutics to strengthen its foothold in this revolutionary technology.

Given the spectacular success of Vertex with CF treatments, its work with gene therapy is projected to bring in another blockbuster deal to the company. To ensure its monopoly in the CF market, Vertex has been aggressively seeking additional regulatory approvals to cater to younger CF patients. If the company succeeds, its target market of 75,000 CF patients would gain an additional 44,000.

Vertex is not limiting its efforts in this field though. To seal its position as the leader in CF treatments, the company is looking at developing triple-drug therapies as the next big development in their treatment plans. It has been performing clinical trials on three varying triple-drug combinations. If approved, these therapies would be able to address approximately 90% of the total number of CF patients.

As for the remaining 10% with no operational CF treatment, Vertex aims to address this via its work on gene editing alongside CRISPR Therapeutics. Aside from CF, the two companies have commenced clinical studies on applying gene-editing therapies to treat rare blood diseases and sickle cell disease.

Overall, Vertex is a certified outperformer in the world of big-cap biotech and provides good value to its shareholders.

Johnson & Johnson(JNJ)

Johnson & Johnson (JNJ) is one of the most attractive names in the biotech space. While the lawsuits against it involving alleged toxic baby powder endanger (JNJ)’s equity, the company is still hailed as one of the most notable innovators in the healthcare ecosystem.

The company recently disclosed its progress in developing an AIDS vaccine. Although the negative headlines about the company can be a cause of concern to some, it could turn out to be a win-win situation for long-term investors who can then take advantage of the bargain basement stock price.

(JNJ) has reinforced its stronghold in the fields of neuroscience, oncology, and immunology with these three areas generating over 72% of the company’s drug sales in the first quarter. In fact, (JNJ) recently received an FDA approval on its myeloma drug Dexamethasone. Its collaborative work on cancer treatment with Celgene’s (CELG) Revlimid and its own Darzalex received the FDA’s green light as well.

Apart from developing new treatments and medications, (JNJ) is also moving forward in the development of its robotic sector. Earlier this year, the company purchased robotic surgery firm Auris Health for $3.4 billion in an effort to dethrone the current sector leader Intuitive Surgical (ISRG).

With all that is in its drug and services pipeline along with its earlier successes, (JNJ) raised its 2019 outlook despite its legal woes. The biopharma giant now anticipates a sales growth of 2.5% to 3.5%. Meanwhile, its adjusted earnings per share now stands somewhere in the range of $8.53 and $8.63 per share.

Celgene (CELG)

Celgene (CELG) is one biotech stock that you can get on the cheap. It offers shares trading at only 7.4 times expected earnings.

With its shares trading well below the total book value courtesy of the pending acquisition by Bristol-Myers Squibb (BMY), investors would be hard-pressed not to take advantage of the opportunity to add a company leading in the development of treatments for cancer, blood disorders, and immunological conditions.

Aside from the looming acquisition, another reason for Celgene’s dirt-cheap stock involves the decision to sell blockbuster immunology drug Otezla to allow Bristol-Myers Squibb to appease the Federal Trade Commission’s concerns over the deal. Nonetheless, Celgene’s remaining drugs still perform well in the market.

Its blood cancer drugs, Revlimid and Pomalyst, are the leading go-to drug for multiple myeloma. Revlimid has been approved to treat two additional rare blood diseases, myelodysplastic syndromes and mantle cell lymphoma. Another winner in Celgene’s lineup is its solid tumor drug Abraxane, which has been approved for advanced breast cancer treatment along with non-small-cell lung cancer and advanced pancreatic cancer.

Celgene’s pipeline is loaded with promising winners as well, with myelofibrosis drug Fedratinib and multiple sclerosis treatment Ozanimod up for FDA approval this year. Three additional blood disease drugs including Luspatercept are also in the works along with a cell therapy called Liso-cel, which engineers the body’s immune cells to target particular types of cancer. Celgene’s work with Bluebird Bio is expected to bring another cell therapy procedure called bb2121, which is anticipated to bolster the biopharma firm’s dominance on the multiple myeloma market.

Amgen (AMGN)

With its ability to flex its financial muscles at will, Amgen (AMGN) has accumulated nearly $30 billion in cash and investments. In the past four years, it has recorded an average annual net profit of roughly $6 billion.

The company has achieved tremendous success in developing groundbreaking technology and edging out its competition courtesy of its innovative treatments like the post-chemo therapy called Neulasta. Its cholesterol drug Repatha and arthritis medication Enbrel are both impressive performers in the market as well.

Despite its aggressive drive to acquire small biopharma firms, Amgen is actually a pretty safe investment. Throughout the years, the company has made a conscious effort to diversify its portfolio to steer clear of dependence on a single product.

In fact, no single drug provides more than one-fourth of Amgen’s total income. Among its products, only two drugs generate over a tenth of its revenue. This pattern of revenue diversity doesn’t stop here either as Amgen’s pipeline has nine Phase 3 trials and an additional five Phase 2 trials.

Illumina (ILMN)

One of the incredible developments in healthcare involves the unlocking of the secrets of the human genome – and Illumina (ILMN) has been widely recognized as the leader in this field. In fact, this company has performed more than 90% of all gene sequencing procedures ever recorded.

Branded as the “gold standard” for gene sequencing, Illumina’s highly accurate technology has turned the company into one of the leaders in the biotech space. Illumina is projected to dominate the industry for a very long time.

More importantly, Illumina has managed to make these treatments affordable. Using Illumina’s technology, the cost of human genome therapy has been remarkably cut from a staggering $100 million back in 2002 to an affordable $1,000 today.

Despite its potential, Illumina released lower-than-expected revenue guidance for this year. However, its track record indicates that the company has the tendency to underpromise but overdeliver.

Its revolutionary gene sequencing equipment NovaSeq has made remarkable progress since its availability in 2017 and has yet to reach its peak. Illumina has been on the lookout for high-growth markets currently in their infancy in an effort to become a pioneering force in other fields.

A good example of this is Illumina’s move on noninvasive prenatal testing (NIPT), which has recently gained popularity among patients. The company released an updated and more powerful version of its fetal genome detector system VeriSeq this year. This technology offers the quickest processing time compared to its rivals.

Illumina is also looking to utilize gene sequencing to bolster cancer research efforts and screening through its TruSight Oncology 500, which is a molecular test used to detect lung cancer. Since its release in 2018, the company has been seeking ways to expand TruSight’s application to include blood tests capable of detecting the very early stages of several types of cancer.

Another significant growth driver for Illumina is population genomics, with the United States, France, Singapore, England, and other countries already utilizing the company’s technology. Consumer genomics also shows a promising fiscal advancement for Illumina. To date, the company has been catering to major providers including Ancestry and 23andMe. Illumina even created its own genealogical spinoff called Helix.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-17 08:02:542019-08-19 16:05:13Five Biotech Stocks to Buy at the Bottom

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.