Global Market Comments

January 15, 2019

Fiat Lux

SPECIAL ARMAGEDDON ISSUE

Featured Trade:

(HERE’S THE WORST-CASE SCENARIO),

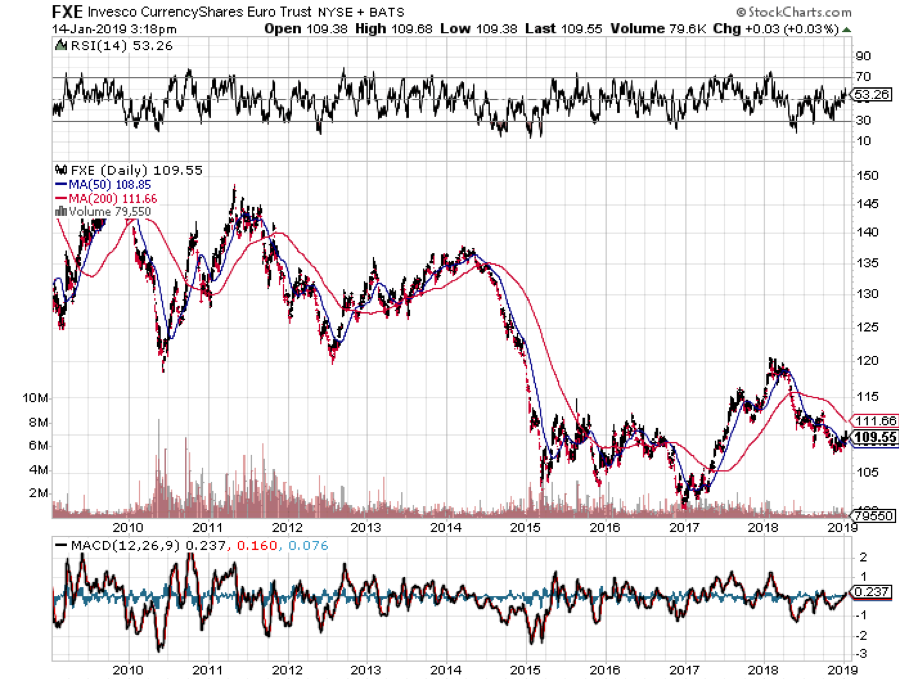

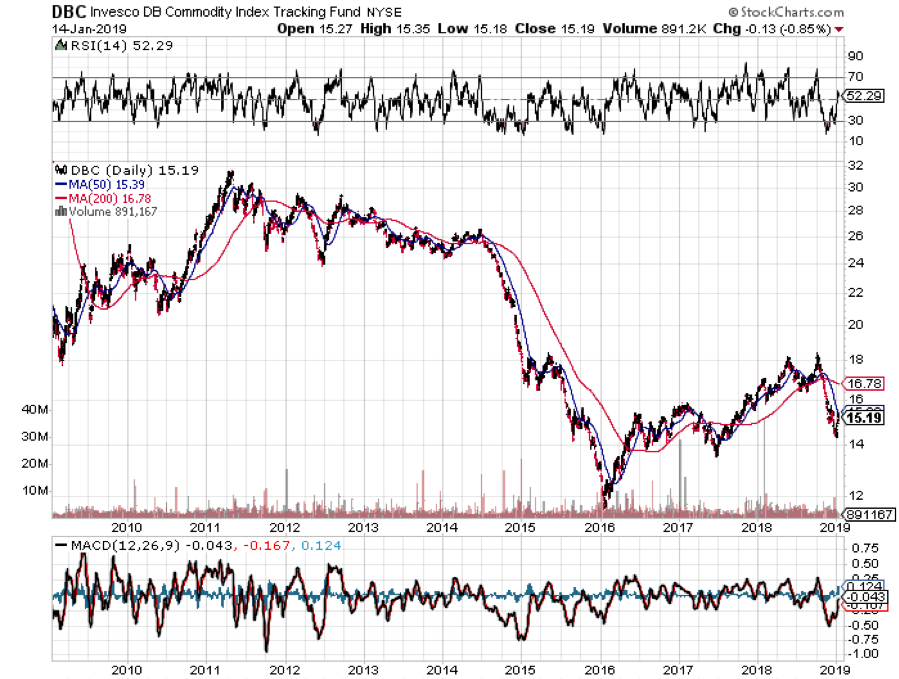

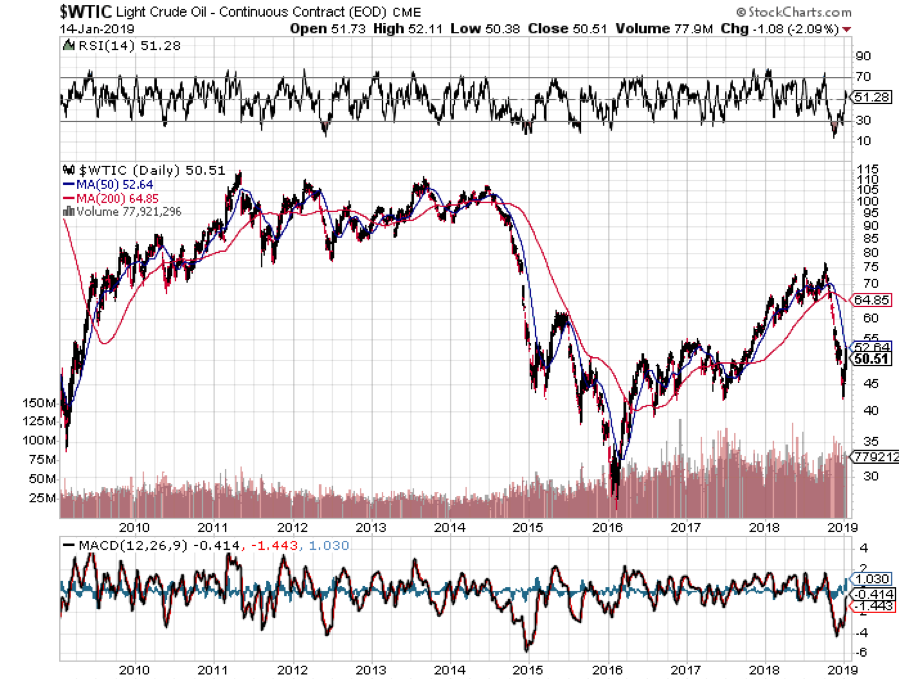

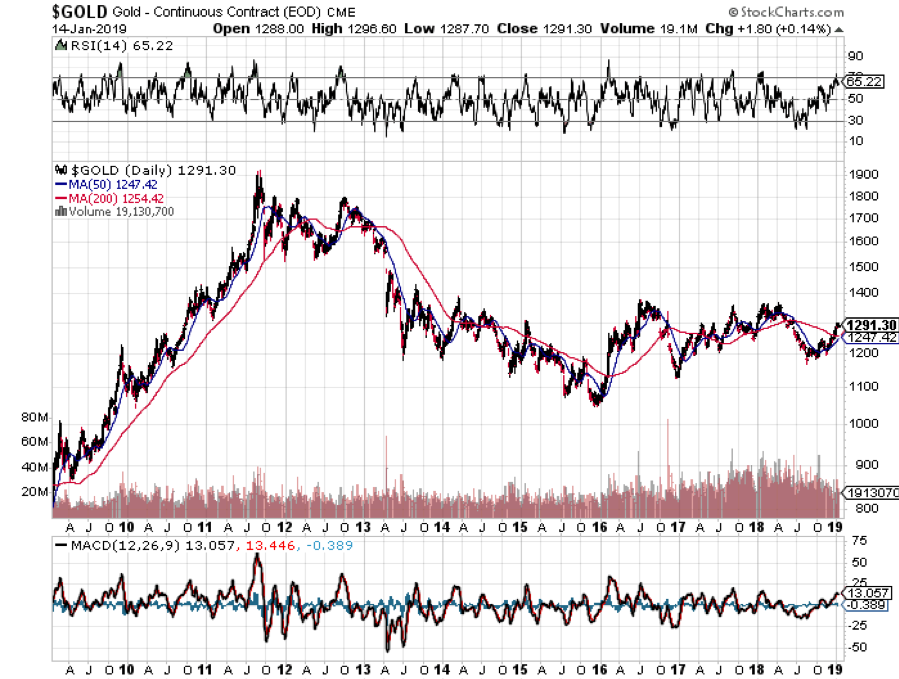

($INDU), (SPY), (SDS), (TLT), (TBT), (FXE), (FXY),

(UUP), (DDP), (USO), (SCO), (GLD), (DGZ), (ITB)

Global Market Comments

January 15, 2019

Fiat Lux

SPECIAL ARMAGEDDON ISSUE

Featured Trade:

(HERE’S THE WORST-CASE SCENARIO),

($INDU), (SPY), (SDS), (TLT), (TBT), (FXE), (FXY),

(UUP), (DDP), (USO), (SCO), (GLD), (DGZ), (ITB)

Yesterday, I listed my Five Surprises of 2019 which will play out during the first half of the year prompting stocks to take another run at the highs, and then fail.

What if I’m wrong? I’ve always been a glass half full kind of guy. What if instead, we get the opposite of my five surprises? This is what they would look like. And better yet, this is how financial markets would perform.

*The government shutdown goes on indefinitely throwing the US economy into recession.

*The Chinese trade war escalates, deepening the recession both here and in the Middle Kingdom.

*The House moves to impeach the president, ignoring domestic issues, driven by the younger winners of the last election.

*A hard Brexit goes through completely cutting Britain off from Europe.

*The Mueller investigation concludes that Trump is a Russian agent and is guilty of 20 felonies including capital treason.

*All of the above are HUGELY risk negative and will trigger a MONSTER STOCK SELLOFF.

It’s really difficult to quantify how badly markets will behave given that this scenario amounts to five black swans landing simultaneously. However, we do have a recent benchmark with which to make comparisons, the 2008-2009 stock market crash and great recession. I’ll list off the damage report by asset class. I also include the exchange-traded fund you need to hedge yourself against Armageddon in each asset class.

*Stocks – Depending on how fast the above rolls out, you will see a stock market (SPY) collapse of Biblical proportions. You’ll easily unwind the Trump rally that started at a Dow Average of 18,000, down 25% from the current level, and off a gut-churning 9,000 points or 33% from the September top. The next support below is the 2015 low at 15,500, down 11,500 points, or 43% from the top. By comparison, during the 2008-2009 crash, we fell 52%. Everything falls and there is no safe place to hide. Buy the ProShares UltraShort S&P 500 bear ETF (SDS).

*Bonds – With the ten-year US Treasury yield peaking at 3.25% last summer, a buying panic would spill into the bond market. Inflation is nonexistent, we are running at only a 2.2% YOY rate now, so widespread deflation would rapidly swallow up the entire economy. In that case, all interest rates go to zero very quickly. The Fed cuts rates as fast as it can. Eventually, the ten-year yield drops to -0.40%, the bottom seen in Japanese and German debt three years ago. Buy the 2X short bond ETF (TBT) which will rocket to from $35 to $200.

*Foreign Exchange – With US interest rates going to zero, the US Dollar (UUP) gets the stuffing knocked out of it. The Euro soars from $1.10 to $1.60 last seen in 2010, and the Japanese yen (FXY) revisits Y80. Strong currencies then crush the economies of our largest trading partners. Their governments take their interest rates back to negative numbers to cool their own currencies. Cash becomes trash….globally.

*Commodities

Here’s the really ugly part about commodities. They are only just starting to crawl OUT of a seven-year bear market. To hit them with another price collapse now would devastate the industry. Producer bankruptcies would be widespread. The ags would get especially hard hit as they have already been pummeled by the trade war with China. Midwestern regional banks would get wiped out. Buy the DB Commodity Short ETN (DDP).

*Energy

The price of oil (USO) is also just crawling back from a correction for the ages, down from $77 to $42 a barrel in only three months. Hit the sector with a recession now in the face of global overproduction and the 2009 low of $25 becomes a chip shot, and possibly much lower. Those who chased for yield with energy master limited partnerships will get flushed. Several smaller exploration and production companies will get destroyed. And gasoline drops to $1 a gallon. The Middle East collapses into a geopolitical nightmare and much of Texas files chapter 11. Buy the ProShares UltraShort Bloomberg Crude Oil ETF (SCO).

*Precious metals

Gold (GLD) initially rallies on the flight to safety bid that we have seen since September. However, if things get really bad, EVERYTHING gets sold, even the barbarous relic, as margin clerks are in the driver’s seat. You sell what you can, not what you want to, as liquidity becomes paramount. This is what took the yellow metal down to $900 an ounce in 2009. Buy the DB Gold Short ETN (DGZ).

*Real Estate

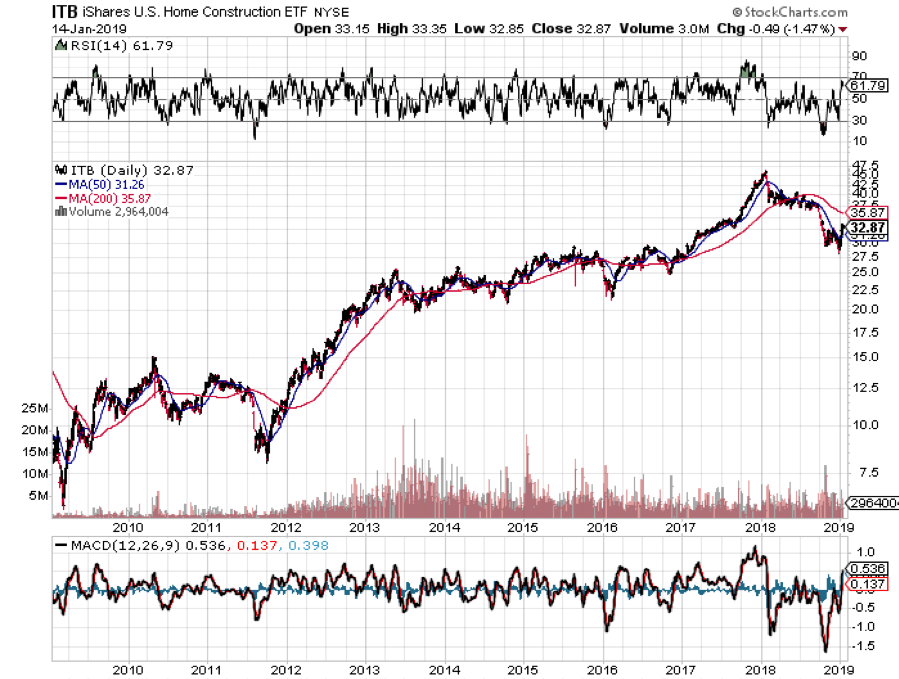

Believe it or not, real estate doesn’t do all that bad in a worst-case scenario. It is perhaps the safest asset class around if a new crisis financial unfolds. For a start, interest rates at zero would provide a huge cushion. The Dodd-Frank financial regulation bill successfully prevented lenders returning to even a fraction of the leverage they used in the run-up to the last recession. We are about to enter a major demographic tailwind in housing as the Millennial generation become the predominant home buyers. I’ve never seen a housing slump in the face of a structural shortage. And homebuilder stocks (ITB) have already been discounting the next recession for the past year. A lot is already baked in the price.

Conclusion

Of course, it is highly unlikely that any of the above happens. Think of it all as what Albert Einstein called a “thought experiment.” But it is better to do the thinking now so you can do the trading later. There may not be time to do otherwise.

Be Careful, They Bite!

Be Careful, They Bite!Global Market Comments

January 11, 2019

Fiat Lux

Featured Trade:

(WHY THE MARKET CRASHED IN DECEMBER),

(SPY), ($INDU), (VIX)

(THE GOVERNMENT’S WAR ON MONEY),

(TESTIMONIAL)

Were you horrified by the market action in December? The next one could get much worse.

We are all used to market corrections. Live long enough and you will endure hundreds of them.

But December? That was a real first class crash, a four times a century event. And to see this occur in the face of solid economic data made it totally unexpected by all. The only analysts predicting a collapse like this one are the ones who have been expecting it daily for the past decade.

To see a 20% decline in NASDAQ and a 50% plunge in market leaders in the face of a 3.2% GDP growth rate and a 3.9% unemployment rate is a first. It makes no sense.

This wasn’t a correction. This was an instance where the market ceased to function and was effectively closed. In fact, it took a conspiracy of several independent forces to get the meltdown we got.

The bottom line here is that this is not your father’s stock market.

The low hanging fruit here is to blame in the high-frequency algorithms. But that is the cheap shot. Algos don’t care which way markets go. They take volatility up sharply, but they take it down as well, as any long-suffering vol player will tell you.

Over time, their market impact is neutral. And algo traders go home 100% in cash every night. That doesn’t explain opening meltdowns of 500 points a day or more. No, there was something much more structural at work.

Human emotions are easy to predict. Take the humans out of the equation and markets can only be read by mainframe computers, at least on a short-term basis. That’s why so many of these market traditions, like “Sell in May and go away,” and the “Santa Claus rally” have quit working.

Only about 10% of today’s daily traders are the breathing kind. The rest are all made of silicon. Even I have come to rely heavily on my own personal algorithms in the Mad Hedge Market Timing Index. It has been worth its weight in gold and saved my bacon many times.

There is no doubt that pure quant strategies have blood on their hands. These funds strictly adhere to rules that have identified the long-term relationships between different asset classes and act accordingly.

For example, when bonds go up, you sell them and buy more stock, but sell more foreign currencies as well, and perhaps pick up some copper as well. All of this is adjusted for risk and volatility. There is thought to be about $1.5 trillion committed to this kind of strategy.

Among these, you can include “risk parity traders” of the kind pioneered by my friend Ray Dalio in the 1990s. (Ray will tell you how he did it in his fascinating book, Principals, out last year). Ray, by the way, is one of the top performing money managers over the last 30 years.

Trend followers pour more gasoline on the fire. If you sell, they will sell more, creating these massive 100 handle days in the S&P 500 (SPY).

Heightening fears was a never-ending torrent of bad news out of Washington. Two out of three key cabinet positions were emptied by presidential firings and remain unoccupied. Trade talks with China came to an impasse. It was not what investors wanted to hear.

All of this set up the perfect storm for December.

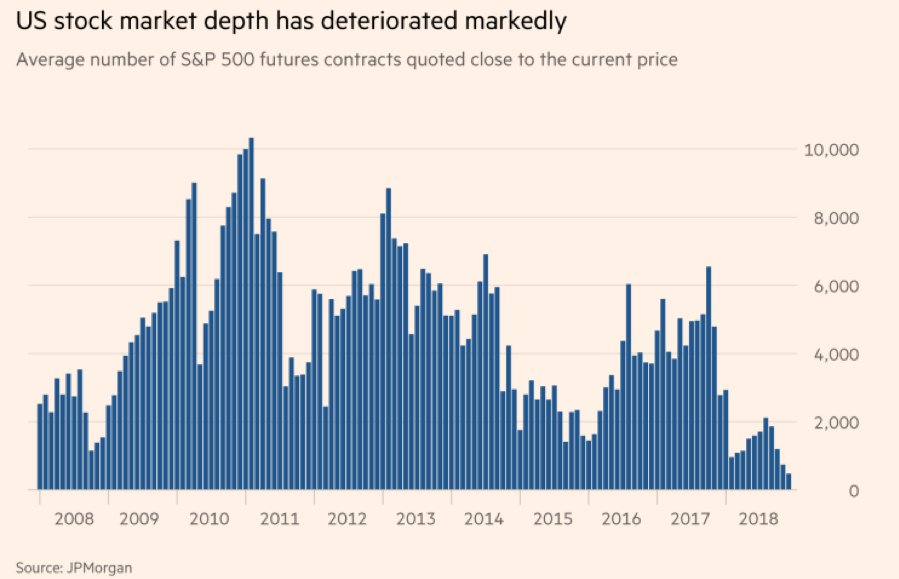

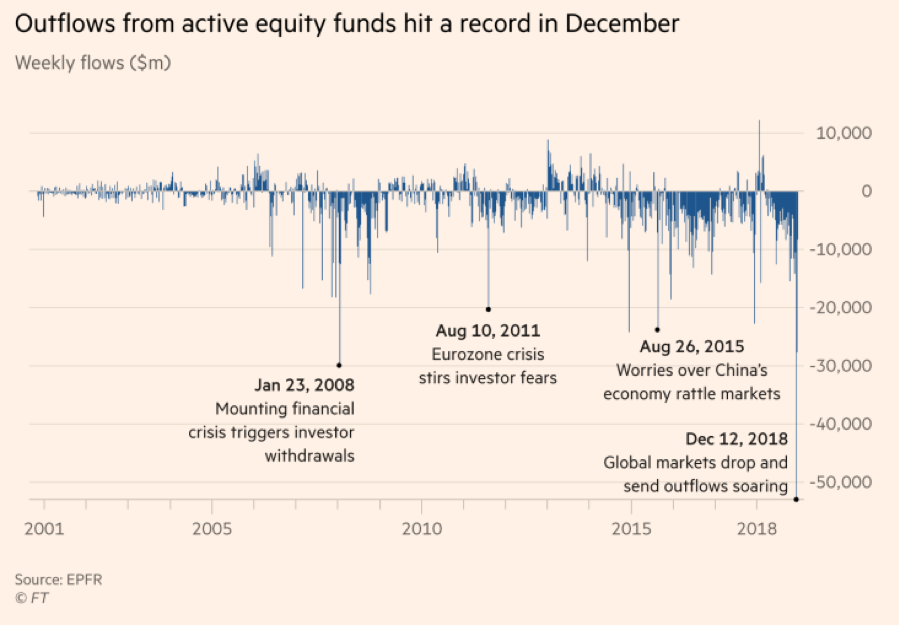

Equity mutual fund redemptions hit a record $53 billion in early December. Market liquidity dramatically shrank as players took off for the holidays, as seen on the chart below. Liquidity during the second half of December was thinner than the worst days of the 2008 financial crisis.

A two-decade-long flight of capital from the floor of the New York Stock Exchange was also a factor. The inevitable result was for the Volatility Index (VIX) to take a run at its highs for the year.

If you wanted to sell anything in size, it could only take place at throwaway prices. It all culminated in the notorious Christmas Eve Massacre which saw a 1,000-point range day in the Dow Average in a holiday-shortened trading day. If it had been a full day it might have been down 2,000 points.

Don’t expect any respite from these strategies any time soon. In fact, we could see worse moves ahead. The current administration believes in a free market, non-interventionist approach to securities markets. That means no new regulation.

The same thing happened in the run-up to the 2008 crash when Christopher Cox (brother of my old boss at Morgan Stanley, Archie Cox) was basically told to go play golf instead of regulate.

Welcome to the new age of investing. The bottom line for all of us traders and investors is that we are going to have to pedal a lot harder to earn our crust of bread….or become a computer.

Global Market Comments

December 21, 2018

Fiat Lux

Featured Trade:

(WHY CASH IS THE BEST HEDGE)

(INDU)

(PRINT YOUR OWN CAR),

(TESTIMONIAL)

Over the decades, I have been besieged by suggestions by various market players over how to hedge their downside risk in the stock market.

I have analyzed most of these, experimented with them, and even tried out a few. These range from buying equity put options to selling call options, investing in bear ETFs, and trading the volatility index (VIX).

My conclusion is always the same: Cash is always the best hedge.

Hedge fund managers like me are always under pressure to deliver positive returns whether the stock market goes up, down, or sideways. A lot make this promise but few are actually able to deliver. You can almost count them on one hand and I know all of them personally.

And here is a hedge fund manager’s worst nightmare: both your longs go down and your shorts go down, eroding capital at a double rate. This is often the result when you come to rely on these esoteric “hedges.”

This happens when you have done all the research in the world, have countless mathematical formulas to back you up, and you backtest your data for 30 years.

First of all, assets classes don’t always perform according to financial models because there is always one big variable that managers can’t quantify: human emotion.

While algorithms and computers are completely rational, people aren’t, even the most experienced ones. After watching markets for over 50 years I can tell you that there is only one certainty. That the natural tendency of most people is to buy at market tops and sell at market bottoms.

In order words, making money in the stock market is an unnatural act and fights against the long-term tide of evolution. We, humans, are predators and hunters evolved to track game on the horizon of an African savanna. Modern humans are maybe 5 million years old but civilization has been around for only 10,000 years. Our brains have not had time to make the adjustment.

In the market, this means that if a stock has gone up, you believe it will continue to do so. This is why market tops and bottoms see volume spikes. To make money, you have to go against these innate instincts. Some people are born with this ability while others can only learn it through decades of training. I am in the latter group.

The 4,400-point decline we have all suffered over the last 2 ½ months is a classic example. Prices earnings multiples have given up half of their gains since the 2009 bear market bottom. It is one of the best buying opportunities in four years. So, what are investors doing? Selling.

Share prices are now discounting a severe recession in 2019 that probably isn’t going to happen. I don’t believe that we’ll get one until the end of 2019 and even then it will be a modest one. Essentially, we already have a recession in the price at these levels. If the recession doesn’t show, stocks will rocket.

What hedges worked during this time? Absolutely none. If you shifted from growth stocks to value ones, or from high beta ones to low beta shares, you still lost money, probably a lot. Those who hedged with volatility probably has some one-hit wonders, but add up their profit and loss for the entire year and it probably comes to negative numbers.

You know what didn’t lose money? Cash which in fact is now earning 2%-4% depending on where you have it parked.

This is why I have been running cash positions of 70%-90% for the past four months. Oh, how I love the smell of cash in the morning. Logging into my online trading account every morning and seeing a wad of cash is like getting a short rush of adrenaline.

Absolutely, cash is the best hedge.

Global Market Comments

December 20, 2018

Fiat Lux

Featured Trade:

(THE GLASS HALF EMPTY MARKET)

($INDU), (SPY)

(HOW TO EXECUTE A VERTICAL BULL CALL SPREAD),

(AAPL)

Dovish, but not dovish enough.

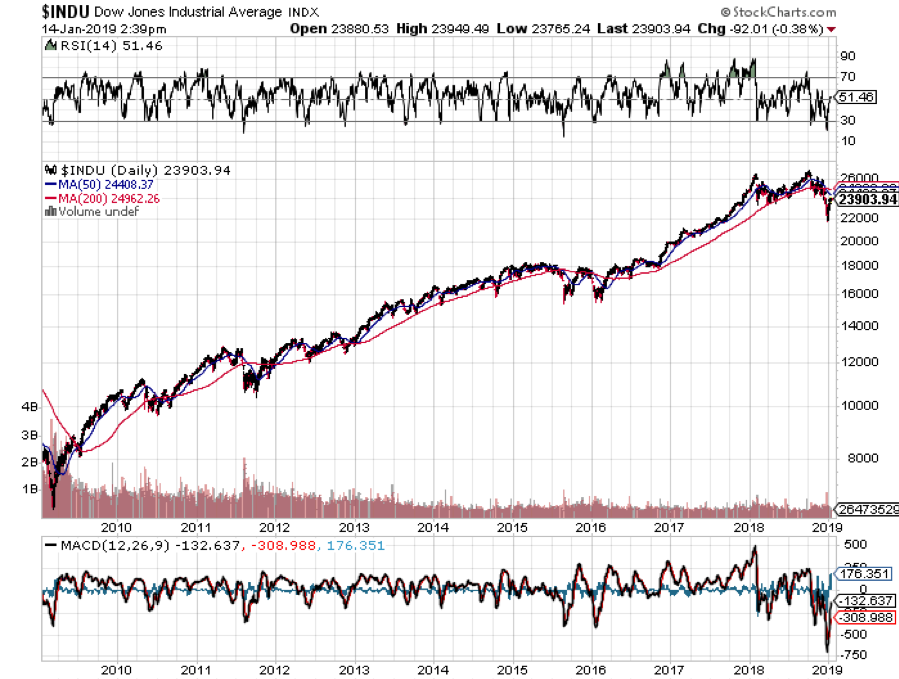

That seems to be the judgment of the markets today in the wake of the Fed’s decision to raise interest rates by 25 basis points. The overnight range for Fed funds is now 2.25%-2.50%.

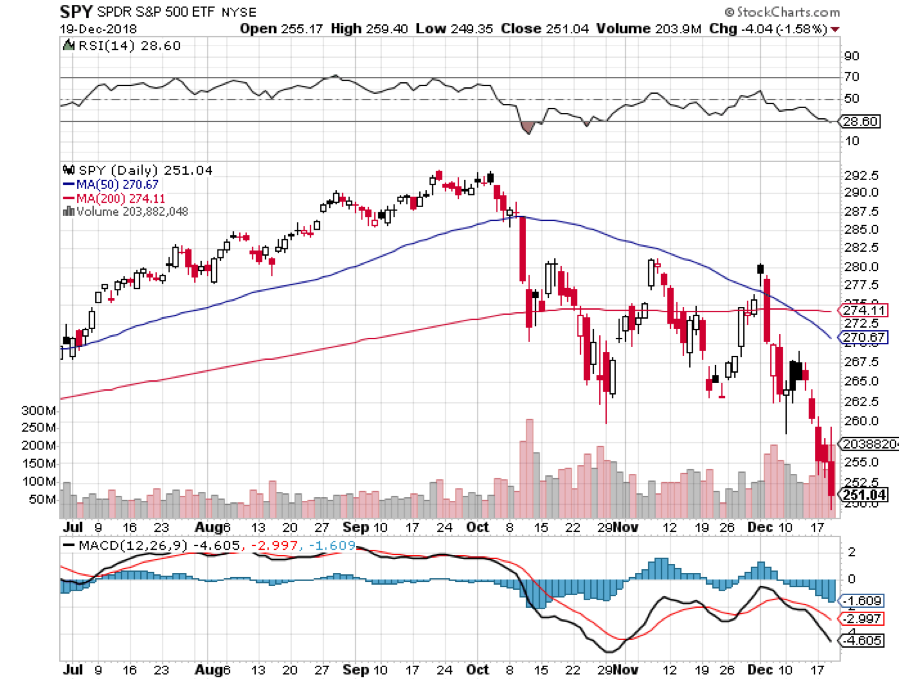

The Dow Average soared by 350 points going into the decision. Then it plunged by 900 points to 23,200, a new low for 2018. It was one of the largest range days in market history.

Traders chose to focus only on the bad news and completely ignore the good. That makes this a totally “glass half empty” market.

Never mind Chairman Jerome Powell’s statement that the Fed was cutting back its 2019 forecast from three interest rate hikes to only two. Stocks should have rallied 1,000 points on just that! And they still might!

Powell also redefined the meaning of the word “neutral”, taking it down from 3.0% to 2.8%. That means only one more quarter-point hike would take us to the low end of neutral, and that might be it. That should have been worth another 1,000 points, and we still might get that as well.

The Fed affirmed that the economy is still generally strong and that unemployment is at historic lows. Nothing to worry about here.

You can see where I’m going with this.

Down 3,800 points from the October high, stocks are now approaching stupidly cheap prices and valuations. Call it insanely cheap. What we are seeing here is the coiling up of a spring that will lead to an explosive upside move.

That may happen with the quadruple witching options expiration on Friday, the last real trading day of the year. It may wait until January 2, the first trading day of 2019. But coming it is.

And let me throw a theory at you which a hedge fund friend bounced off of me yesterday while I was on one of my legendary night hikes.

What if we really have been in a bear market since January 31 and we are now approaching the end of it? That would give us a typical one-year long bear market from which we are about to blast out to the upside.

When does this new bull market begin? When the last week hands intent on avoiding another 2008 repeat bails on their holdings. In other words, it could happen any day now.

Interesting food for thought.

Global Market Comments

December 17, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or THERE’S NO SANTA CLAUS IN CHINA)

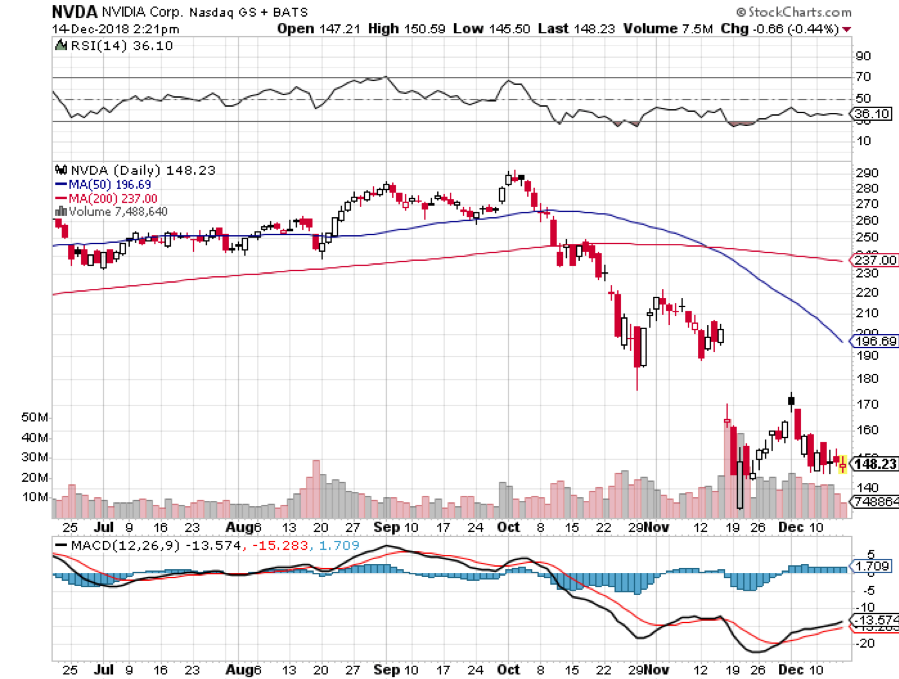

($INDU), (SPY), (TLT), (AAPL), (AMZN), (NVDA), (PYPL), (NFLX)

On Friday, five serious hedge fund managers separately called me out of the blue and all had the same thing to say. They had never seen the market so negative before in the wake of the worst quarter in seven years. Therefore, it had to be a “BUY”.

I, on the other hand, am a little more cautious. I have four 10% positions left that expire on Friday, in four trading days, and on that day I am going 100% into cash. At that point, I will be up 3.5% for the month of December, up 31.34% on the year, and will have generated positive return for one of the worst quarters in market history.

I’m therefore going to call it a win and head for the High Sierras for a well-earned Christmas vacation. After that, I am going to wait for the market to tell me what to do. If it collapses, I’ll buy it. If it rockets, I’ll sell short. And I’ll tell you why.

These are not the trading conditions you would expect when the economy is humming along at a 2.8% annual rate, unemployment is running at a half-century low, and earnings are growing a 26% year on year. You can’t find a parking spot in a shopping mall anywhere.

However, the lead stocks like Apple (AAPL), Amazon (AMZN), and Netflix (NFLX) have plunged by 30%-60%. Price earnings multiples dropped by a stunning 27.5% from 20X to 14.5X in a mere ten weeks. Half of the S&P 500 (SPY) is in a bear market, although the index itself isn’t there yet. I would rather be buying markets on their way up than to try and catch a falling knife.

There is only one catalyst for that apparent yawning contradiction: The President of the United States.

Trump has created a global trade war solely on his own authority. Only he can end it. As a result, asset classes of every description are beset with uncertainty, confusion, and doubt about the future. Analysts are shaving 2019 growth forecasts as fast as they can, businesses are postponing capital spending plans, and investors are running for the sidelines in droves. Business confidence is falling like a rock

To paraphrase a saying they used to teach you in Marine Corps flight school, “It’s better to be in cash wishing you were fully invested than to be fully invested wishing you were in cash.”

The Chinese have absolutely no interest in caving into Trump’s wishes. They read the New York Times, see the midterm election result and the opinion polls, and are willing to bet that they can get a much better deal from a future president in two years.

I have been dealing personally with both Trump and the Chinese government for four decades. The Middle Kingdom measures history in Millenia. The president lives from tweet to tweet. The Chinese government can take pain by simply ordering its people to take it. We have elections every two years with immediate consequences.

The best we can hope for is that the president folds, declares victory, and then retreats from his personal war. This can happen at any time, or it may not happen at all. No one has an advantage in predicting what will happen with any certainty. Not even the president knows what he is going to do from minute to minute.

It is the possibility of trade peace at any time that has kept me out of the short side of the stock market in this severe downturn. That robs a real hedge fund manager of half his potential income. Trade peace could be worth an instant rally of 10% in the stock market. Even a lesser move, like the firing of trade advisor Peter Navarro, would accomplish the same.

The market was long overdue for a correction like the one we have just had. Investors were getting overconfident, cocky, and excessively leveraged. In October, we really needed the tide to go out to see who was swimming without a swimsuit. But if the tide goes out too far, we will all appear naked.

Thanks to some very artful trading, my year to date return recovered to +27.54% boosting my trailing one-year return back up to 27.54%. I covered an aggressive short position in the bond market (TLT) for a welcome 14.4% profit. I also took profits with an instant winner in PayPal (PYPL). On the debit side, I stopped out of an Apple call spread for a minimal loss.

December is showing a very modest loss at -0.26%. The market has become virtually untradeable now, with tweets and China rumors roiling markets for 500 points at a pop. And this is against a Dow Average that is down a miserable -2.8% so far in 2018. I should have listened to my mother when she wanted me to become a doctor.

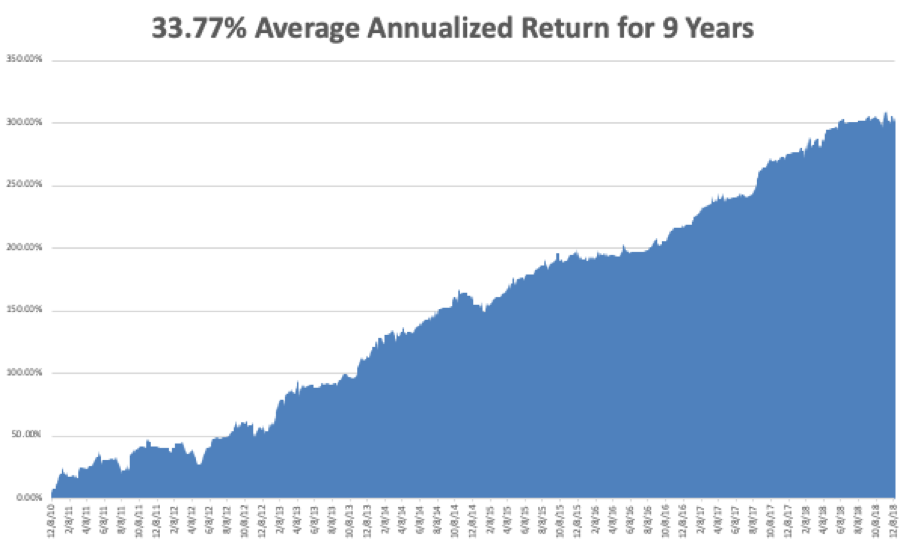

My nine-year return nudged up to +304.01. The average annualized return revived to +33.77.

The upcoming week is all about housing data, with the big focus on the Fed’s interest rate hike on Wednesday.

Monday, December 17 at 10:00 AM EST, the November Homebuilders Index is out.

On Tuesday, December 18 at 8:30 AM, November Housing Starts are published.

On Wednesday, December 19 at 10:00 AM EST, November Existing Home Sales are released.

At 10:30 AM EST the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

At 2:00 PM the Federal Reserve Open Market Committee announces a 25 basis point rise in interest rates, taking the overnight rate to 2.25% to 2.50%. An important press conference with governor Jay Powell follows.

Thursday, December 20 at 8:30 AM EST, we get Weekly Jobless Claims.

On Friday, December 21, at 8:30 AM EST, we learn the latest revision to Q3 GDP which now stands at 2.8%.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’ll be battling snow storms driving up to Lake Tahoe where I’ll be camping out for the next two weeks. Mistletoe, eggnog, and endless games of Monopoly and Scrabble await me.

Good luck and good trading!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader