Mad Hedge Technology Letter

April 8, 2024

Fiat Lux

Featured Trade:

(BRANCHING OUT)

(INTC), (MSFT)

Mad Hedge Technology Letter

April 8, 2024

Fiat Lux

Featured Trade:

(BRANCHING OUT)

(INTC), (MSFT)

Intel (INTC) is an intriguing chip company that has been around for a long time but has seldom been at the vanguard of the tech movement.

Until now…

Remember the US government is pouring dollars at the tune of billions upon billions into the domestic semiconductor industry to maintain a competitive advantage that is quickly being challenged by China.

Intel could solidify itself as a real tech player if it can figure out the foundry business which has been largely ineffective as of late.

Even if the foundry business is a big-time loss maker right now, Intel is laying the groundwork to become a strategically important company to the US government and US tech industry in 5 years.

Government dollars are usually viewed as a more stable stream of revenue.

It’s true that Intel is better known for designing its own chips, but that type of barrier to entry isn’t as high as foundry production.

Many chip companies aren’t interested in the production of what they design, because of the capital-intensive nature of the process.

It’s easier to outsource designs and just collect the product after.

Intel shares fell 4% last Tuesday after the company revealed long-awaited financials for its semiconductor manufacturing business or foundry business.

Intel said its foundry business recorded an operating loss of $7 billion in 2023 on sales of $18.9 billion. That’s a wider loss than the $5.2 billion Intel reported in its foundry business in 2022 on $27.5 billion in sales.

It has been pitching investors to double down on an external foundry business to make chips for other companies.

In theory, it sounds promising.

Intel’s role as one of the only U.S. companies doing cutting-edge semiconductor manufacturing on American soil was a big reason it secured nearly $20 billion in CHIPS and Science Act funding last month.

Its management said that it expected its foundry’s losses to peak in 2024 and eventually break even “midway” between this quarter and the end of 2030.

The company previously said that Microsoft (MSFT) would use its foundry services and that it has $15 billion of revenue for the foundry already booked.

The foundry business at Intel will ostensibly drive larger revenue momentum each approaching year to 2030.

Granted, it doesn’t take one day for chip production to come online, but the contract signed with Microsoft is a positive signal that will likely lead to other behemoths inking deals.

Intel even admitted that the lack of profitability in the foundry business from the past was correctable through better focus and execution.

I do believe Intel morphing into a multi-dimensional chip company is highly supportive of a higher share price only if they can get a handle on expense control.

Many times companies go too big with the government subsidies and need even more subsidies to dig themselves out of a hole.

I don’t believe that will be the case with Intel’s foundry business and installing a concrete plan has gone a long way to soothe investor fear.

The stock was crushed in 2020 and hit a nadir of $25 per share in 2023.

Intel shares then reversed and doubled to around $50 per share.

They have now settled in the high $30 range and I do believe any dips should be bought and held long-term.

Global Market Comments

March 6, 2024

Fiat Lux

Featured Trade:

(WHY THE DOW IS GOING TO 240,000)

(X), IBM (IBM), (GM), (MSFT), (INTC), (DELL), (NVDA), (NFLX), (AMZN), (META), (GOOGL), (BITO)

For years, I have been predicting that a new Golden Age was setting up for America, a repeat of the Roaring Twenties. The response I received was that I was a permabull, a nut job, or a conman simply trying to sell more newsletters.

Now some strategists are finally starting to agree with me. They too are recognizing that a ganging up of three generations of investment preferences will combine to drive markets higher during the 2020s, much higher.

How high are we talking? How about a Dow Average of 240,000 by 2035, up another 515% from here? That is a 40-fold gain from the March 2009 bottom.

It’s all about demographics, which are creating an epic structural shortage of stocks. I’m talking about the 80 million Baby Boomers, 65 million from Generation X, and now 85 million Millennials. Add the three generations together and you end up with a staggering 230 million investors chasing stocks, the most in history, perhaps by a factor of two.

Oh, and by the way, the number of shares out there to buy is actually shrinking, thanks to a record $1 trillion or more in corporate stock buybacks for the past decade.

I’m not talking pie-in-the-sky stuff here. Such ballistic moves have happened many times in history. And I am not talking about the 17th-century tulip bubble. They have happened in my lifetime. From August 1982 until April 2000, the Dow Average rose, you guessed it, exactly 20 times, from 600 to 12,000, when the Dotcom bubble popped.

What have the Millennials been buying? I know many, like my kids, their friends, and the many new Millennials who have recently been subscribing to the Diary of a Mad Hedge Fund Trader. Yes, it seems you can learn new tricks from an old dog. But they are a different kind of investor.

Like all of us, they buy companies they know, work for, and are comfortable with. During my dad’s generation that meant loading your portfolio with US Steel (X), IBM (IBM), and General Motors (GM).

For my generation, that meant buying Microsoft (MSFT), Intel (INTC), and Dell Computer (DELL).

For Millennials that means focusing on NVIDIA (NVDA), Netflix (NFLX), Amazon (AMZN), Meta (META), and Alphabet (GOOGL). Oh, and they like Bitcoin too (BITO).

That’s why the Magnificent Seven account for all of the past year’s monster gains.

There is another gale force tailwind pushing stocks up. The enormous profits created by artificial intelligence are essentially replacing the Federal Reserve as an unlimited source of liquidity. If you missed the quantitative easing and the free money of the 2010s, you get another pass at the brass ring. But you have heard me talk about this before so I won’t bore you.

There is one catch to this hyper-bullish scenario. Somewhere on the way to the next market apex at Dow 240,000, we need to squeeze in a recession. Bear markets in stocks historically precede recessions by an average of seven months. But for the time being, it looks like smooth sailing.

When I get a better read on precise dates and market levels, you’ll be the first to know.

Global Market Comments

December 27, 2023

Fiat Lux

SPECIAL ISSUE ABOUT THE FAR FUTURE

Featured Trade:

(PEAKING INTO THE FUTURE WITH RAY KURZWEIL),

(GOOG), (INTC), (AAPL), (TXN)

Global Market Comments

August 24, 2023

Fiat Lux

Featured Trades:

(AN INSIDER’S GUIDE TO THE NEXT DECADE OF TECH INVESTMENT),

(AMZN), (AAPL), (NFLX), (AMD), (INTC), (TSLA), (GOOG), (META)

CLICK HERE to download today's position sheet.

Global Market Comments

March 24, 2023

Fiat Lux

Featured Trade:

(MARCH 22 BIWEEKLY STRATEGY WEBINAR Q&A),

(IBB), (INTC), (AMD), (XLU), (NVDA), (TSLA), (FRC), (QQQ), (SPY), (TLT), (UNG), (USO), (VLO), (DINO), (SUN), (FCX), (JPM), (RIVN), (DVN), (LNG), (KMI), (DAL)

CLICK HERE to download today's position sheet.

Below please find subscribers’ Q&A for the March 22 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: I have big losses in biotech (IBB) but am a long-term believer—do you think it will recover?

A: Yes, I do. But we are still looking at the post-COVID hangover, where Biotechs rocketed for about a year. We’re simply coming off that overbought situation. In the meantime, the industry continues to generate groundbreaking discoveries at the fastest rate in history. When those translate into profit-making products, the stocks will perform, and many of them already have.

Q: Advanced Micro Devices (AMD) appears to be overbought, what are your thoughts?

A: Yes absolutely, the whole chip sector is overbought, because guess what, they benefit from falling interest rates and an economic recovery. That group will absolutely lead going into the future, and it’s hard to get into—these things just go up in a straight line. Look at Nvidia (NVDA), it has more than doubled since the October low and you barely get pullbacks. It’s looking like Nvidia is going to take over the world; we’d love to get into it but it seems like it will only be a high-risk/high-reward stock. They are now having the tailwind with Chat GPT—which everyone has to own now or go out of business—and buy Nvidia chips to make it work.

Q: Would you recommend banks and brokerages here?

A; Yes, because of the banking crisis, they’ll be the best performers as we come out of it. The end of the interest rate rising cycle is now in sight, and we are about to enter the golden age of banking. Institutions are buying stocks for that now. And your next entry point will be Friday because the pattern has been to sell off everything on Fridays in expectation of a new bank going under on the weekend. If nothing happens, then you have a big rally on Monday morning. So that you can probably play.

Q: Are there recordings of this webinar?

A: Yes, to find all past recordings, just go to www.madhedgefundtrader.com and log in.

Q: When does Intel (INTC) become a buy, if ever?

A: It’s probably a “BUY” right here. You never want to buy a tech company run by a salesman, and that’s what happened with Intel. As soon as you had a salesman guaranteeing he’d turn the company around, the stock dropped by half. So down here, it’s looking more likely that they’ll fire the head of Intel, get an engineer back in charge, and the stock should double. But clearly, it’s the only value left in the semiconductor area.

Q: Would you double up on the United States Natural Gas Fund (UNG)?

A: Yes, and I'd be doing 2-year (UNG) LEAPS. There’s no way you have an economic recovery over the next two years that will get us a double, triple, or quadruple in the price of natural gas, and (UNG) will catch that move less 35% for the contango (the 1-year differential between front month and one-year futures contracts).

Q: What’s your favorite tech stock to buy on the dip?

A: It has to be Tesla (TSLA). And I’m in the middle of writing a massive opus on the Tesla Investors Day, which included far more news and content than people realize. That's because you have journalists covering investors' day, not engineers. So I’ll get to the engineers’ and scientists view, which is much more interesting.

Q: Buy bitcoin after the financial contagion?

A: No, bitcoin is what you bought at the market top because there was nothing else to buy because everything else was so expensive. Now everything else is cheap when you can buy Apple (AAPL) at $160, Nvidia at $272 (NVDA), or Tesla (TSLA) at $200. Those are far better choices than a purely speculative asset class which you may never see again once you send in your money. That has been the experience of a lot of people.

Q: Should I sell short the Utility ETF (XLU) if investors head into growth stocks?

A: No, utilities are very heavy borrowers with big capital requirements, and also will benefit heavily from falling interest rates. Basically, everything goes up on an economic recovery. So, your short ideas were great a year ago, not so much now. Now we’re looking for long plays, and just a few hedges, like in bonds, to control risk.

Q: What's the net entry point for Freeport McMoRan (FCX)?

A: I would say here, and my target for this year for Freeport is at the very least hitting $50 again; someday we hit $100, once we get another ramp-up for EV production and the demand for copper sores accordingly.

Q: I hear China has a battery that will go 600 miles and is coming soon.

A: Tesla has a battery that will go 1,000 miles now, but it can only be recharged once. It turns out that the military is very interested in using these, converting Humvees to EVs; then you could parachute them charged batteries which you just pop in. That eliminates having to move these giant bladders of gasoline which easily explode. So yes, the 1,000-mile battery has actually been around for 10 years but can’t be mass-produced. That is the issue.

Q: How will Tesla deal with hydrogen?

A: It will ignore it. Hydrogen will never go mainstream—it can’t compete with an existing electric power grid. But there are fleet or utility applications that make sense; so other than a small, limited fleet confined to a local area, I don't see hydrogen ever catching up. And Saudi Arabia can easily convert their entire oil supply into hydrogen to create a “green” carbon-free fuel. Remember, the cost of electric power cars is dropping dramatically—at about 20% a year—so hydrogen has to keep up with that too which they’re not.

Q: Please explain a bank LEAPS.

A: You buy a call option, you sell short a call option higher up, and you do it with a maturity of one year longer, or more. That’s what makes it a LEAPS. If you want more details, just go to www.madhedgefundtrader.com, and search LEAPS and a full explanation of how to execute these will come up.

Q: What do you think of Rivian (RIVN)?

A: It’s a long-term play—they got knocked down by half on their latest $1.2 billion capital raise, which everybody knew was coming, but still seemed to surprise some traders. It’s a long-term hold, not a short term trade. That said, it’s tempting to do LEAPS on Rivian right here going out two years. The stock is down 95% from the highs.

Q: What level LEAPS do you do on JP Morgan (JPM)?

A: I sent that out to everybody last week—that would be to buy the $130 call option and sell short the $135 call option for January of 2024. That way the stock only has to go up 4% for you to make a 100% return on that investment. That’s why we love LEAPS.

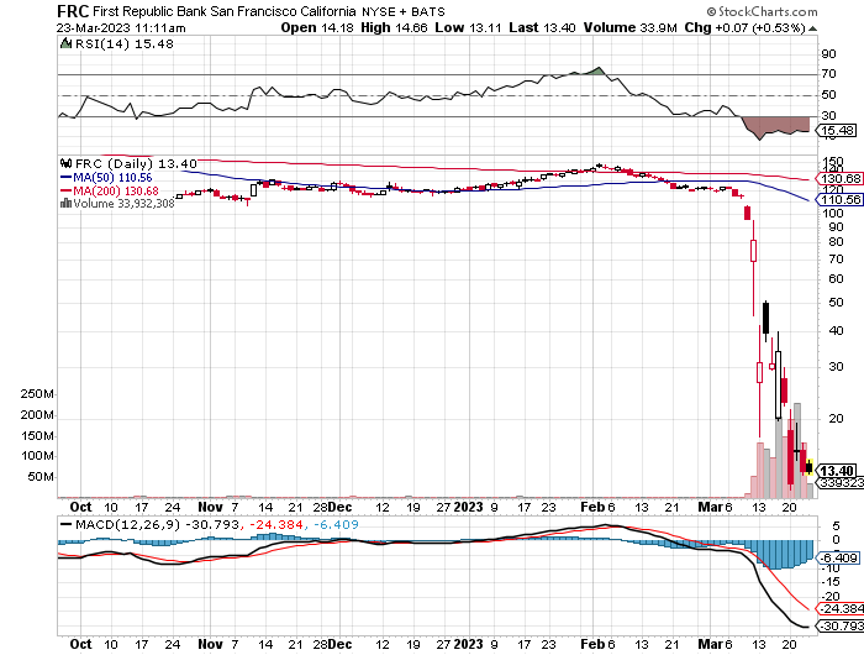

Q: I had First Republic Bank (FRC) at $30, took a bath, and got rid of it. Should I have held on?

A: Yes. There's nothing wrong with First Republic's business, and that’s what's new in all of this current round of bank failures—the assets are fine. Usually when a bank goes under it’s because they extended too many dubious loans that defaulted. First Republic not only has a great loan book, but a great asset base in high-net-worth individuals. This is not a bank you would normally expect to go under. Which is why private banks are pouring money into it to save it. I’d be a buyer at the $10 level if we get down that far again. And I actually bought a little bit of First Republic myself on Monday, the meltdown day at $15, with the theory that it will get bailed out and the stock goes up ten times.

Q: Would you do vertical credit spreads on the SPDR S&P 500 ETF Fund (SPY) or Invesco QQQ ETF (QQQ) with the $2 spread?

A: No, the big money is made on single stocks, which have double or triple the volatility of indexes, and you know which single stocks to buy right now—the ones that just had a big selloff. You want more volatility at market bottoms, not less; and I would recommend doing all the financial and call spreads and LEAPS right here. They will have higher volatility and deliver much better risk/reward ratios. That is basic trading 101: you short indexes on the way down, you buy single stocks on the way up. That's what every hedge fund worth its salt does.

Q: Do you have an opinion on Zero Days to Expiration causing greater volatility?

A: Absolutely, it is—especially on Fridays. And I'm not doing these because they are basically lottery tickets. But, if it's a coin toss on whether you make money or not, and you write off the bad ones and make a nice profit on the good ones, that could be a profitable trade. I actually have several followers experimenting with that type of strategy, so I'll let you know if they make any money on it.

Q: What do you think about oil in this environment?

A: It’s discounting a recession which is never going to happen; so oil and oil plays are probably a good trade here, especially with front-month calls. I would be going for Valero Energy (VLO) and the refiners like Sinclair (DINO) and Sunoco (SUN), rather than the big producers because they have already had big moves which they have held onto mostly. Expect oil to go up—I’d be buying the commodity here (USO) and I’d be buying the United States Natural Gas Fund (UNG).

Q: What's the maximum downside in the next 30 days?

A: Well I showed you on that S&P 500 (SPY) chart at the beginning—$350 is the worst-case scenario with a deep recession, and that assumes the banking crisis doesn’t go away and gets worse. I think the banking crisis is done and getting better so we won’t test the downside, but the unanticipated can happen, so you have to be ready for anything. The non-recessionary low looks to be $375.

Q: What if you can’t do spreads in an IRA, like for iShares 20 Plus Year Treasury Bond ETF (TLT)?

A: Just buy the (TLT) outright, or buy it on 2:1 margin. (TLT) is probably a great buy around 100 or 101. ProShares has the 2X long Ultra Treasury ETF (UBT), but the fees are high, the spreads are wide, and the tracking error is large, as is standard for these kinds of instruments.

Q: When taking a position in LEAPS, how do you decide the position size per holding?

A: I send out all the LEAPS assuming one contract, then you can adjust your size according to your own experience level and risk tolerance. Keep in mind that if I’m wrong on everything, the value of all LEAPS goes to zero, so it may not be for you. On the other hand, if I am right on my one-year and two-year views, all these LEAPS will deliver a 100-120% return. You decide.

Q: Are you expecting a seasonal rally in oil?

A: Yes I am, and we’re coming off very low levels. Buy the United States Oil ETF (USO) and buy the United States Natural Gas Fund (UNG).

Q: Is a recession still on the table with all the banking crises?

A: No, if anything, it brings the end of any possibility of a recession because it’s bringing interest rate cuts sooner than expected, which brings a recovery that’s sooner than expected. And that’s why you’re getting interest-rate-sensitive stocks holding here and starting to rally.

Q: My retirement account won’t let me buy (UNG)—Are there any other good companies I can buy?

A: Yes, Devon Energy (DVN) is big in the gas area. So are Cheniere Energy (LNG) and Kinder Morgan (KMI).

Q: If the market is oversupplied with oil, why is gasoline so expensive?

A: Endless middlemen add-ons. This is one of the greatest continuing rip-offs in human history—gasoline prices always take the elevator up and the escalator down, it’s always that way. And that's how oil companies make money—by squeezing consumers. I’ve been tracking it for 50 years and that’s my conclusion. The State of California has done a lot of research on this and learned that only half of their higher prices are from taxes to pay for roads and the other half comes from a myriad of markups. Also, a lot of businessmen just don’t want to be in the gasoline retailing business and will only enter when the returns are very high. Plus, oil companies are trying to milk companies for all their worth right now because the industry may disappear in 10 years. Go electric, that’s my solution. I haven’t bought gasoline for 13 years, except for my kids. I only buy cars for my kids at junkyards and fix them up. If they want to do better they can go out and earn it.

Q: Do we need to worry about China supporting Russia in the war against Ukraine?

A: Not really, because all we have to do to cut off Chinese supplies for Russia is to cut off trade with China, and their economy will completely collapse. China knows this, so they may do some token support for Russia like send them sweatshirts or something like that. If they start a large arms supply, which they could, then the political costs and the trade costs would be more than it’s worth. And at the end of the day, China has no principles, it really is only interested in itself and its own people and will do business with anybody.

Q: What do you think about the recovery in solar?

A: What’s been going on in solar is very interesting because for the last 20 years, solar has moved one to one with oil. So, you would expect that from collapsing oil prices and more price competition from oil, solar would collapse too. Instead, solar has had tremendous moves up and is close to highs for the year. The difference has to be the Biden alternative energy subsidies, which are floating the entire industry and accelerating the entire conversion of the United States to an all-electric economy. So they've had great runs. I wouldn’t get involved here, but it’s nice to contemplate what this means for the long-term future of the country.

Q: Should I buy the airline stocks here?

A: Yes, I’d go for Delta (DAL). Again, it’s one of the sectors that’s discounting a recession that’s not going to happen. They’re going to have the biggest airline boom ever this summer as the reopening trade continues on for another year, and a lot of pent-up travel demand hits the market.

Q: Do you like platinum?

A: I do—not because of EVs but because of hydrogen. You need platinum for hydrogen fuel cells to work. That’s a brand new demand, and there’s supposed to be a shortage of half a million ounces of platinum this year.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

February 27, 2023

Fiat Lux

Featured Trade:

(THE UNBEATABLE PARTNERSHIP)

(EMR), (GRMN), (AMBA), (NVDA), (DXCM), (CSCO), (INTC), (QCOM)

Let me introduce to you one of the hottest trends in tech.

They have been on the tip of everyone's lips for years, and that might be an understatement, but the interaction of the internet of things (IoT) and artificial intelligence (AI) offers companies a wide range of advantages.

In order to get the most out of IoT systems and to be able to interpret data, the symbiosis with AI is almost a must.

If the Internet of Things is merged with data analysis based on artificial intelligence, this is referred to as AIoT.

Moving forward, expect this to be the hot new phrase in an industry backdrop where investors love these hot catchphrases and monikers.

What is this used for?

Lower operating costs, shorter response times through automated processes, and helpful insights for business development are just a few of the notable advantages of the Internet of Things.

AI also offers a variety of business benefits: it reduces errors, automates tasks, and supports relevant business decisions. Machine learning as a sub-area of AI also ensures that models – such as neural networks – are adapted to data. Based on the models, predictions and decisions can be made. For example, if sensors deliver new data, they can be integrated into the existing modules.

The Statista research institute assumes that there will be 75 billion networked devices by 2025.

This is exactly where AI comes into play, which generates predictions based on the sensor values received.

However, many companies are still unable to properly benefit from the potential of connecting IoT and AI, or AIoT for short.

They are often skeptical about outsourcing their data - especially in terms of security and communication.

In part because the increased number of networked devices, which requires the connection of IoT and AI, increases the security requirements for infrastructure and communication structure enormously.

It is not surprising that companies are unsettled: Industrial infrastructures have grown historically due to constantly increasing requirements and present companies with completely new challenges, which manifest themselves, for example, in an increasing number of networked devices. With the combination of IoT and AI, many companies are venturing into relatively new territory.

By connecting IoT and AI, a continuous cycle of data collection and analysis is developing.

But companies can no longer deny the advantages of AIoT because this technical combination makes networked devices and objects even more useful.

Based on the insights generated by the models, those responsible can make decisions more easily and reliably predict future events. In this way, a continuous cycle of data collection and analysis develops. With predictive maintenance, for example, production companies can forecast device failures and thus prevent them.

The combination of the two technologies also makes sense from the safety point of view: continuous monitoring and pattern recognition help to identify failure probabilities and possible malfunctions at an early stage – potential gateways can thus be better identified and closed in good time.

The result: companies optimize their processes, avoid costly machine failures, and at the same time reduce maintenance costs and thus increase their operational efficiency.

In this way, IoT and AI represent a profitable fusion: While AI increases the benefit of existing IoT solutions, AI needs IoT data in order to be able to draw any conclusions at all.

AIoT is therefore a real gain for companies of all sizes. They thus optimize processes, are less prone to errors, improve their products and thus ensure their competitiveness in the long term.

Some hardware, software, and semiconductor stocks that will offer exposure into AIoT are Emerson Electric Co. (EMR), Garmin (GRMN), Ambarella (AMBA), Nvidia (NVDA), DexCom (DXCM), Cisco (CSCO), Intel (INTC), and Qualcomm (QCOM).