Global Market Comments

August 2, 2022

Fiat Lux

Featured Trade:

(AN INSIDER’S GUIDE TO THE NEXT DECADE OF TECH INVESTMENT),

(AMZN), (AAPL), (NFLX), (AMD), (INTC), (TSLA), (GOOG), (META)

Global Market Comments

August 2, 2022

Fiat Lux

Featured Trade:

(AN INSIDER’S GUIDE TO THE NEXT DECADE OF TECH INVESTMENT),

(AMZN), (AAPL), (NFLX), (AMD), (INTC), (TSLA), (GOOG), (META)

Last weekend, I had dinner with one of the oldest and best-performing technology managers in Silicon Valley. We met at a small out-of-the-way restaurant in Oakland near Jack London Square so no one would recognize us. It was blessed with a very wide sidewalk out front and plenty of patio tables.

The service was poor and the food indifferent, as are most dining experiences these days. I ordered via a QR code menu and paid with a touchless Square swipe.

I wanted to glean from my friend the names of the best tech stocks to own for the long term right now, the kind you can pick up and forget about for a decade or more, a “lose behind the radiator” portfolio.

To get this information, I had to promise the utmost confidentiality. If I mentioned his name, you would say “oh my gosh!”

Amazon (AMZN) is now his largest holding, the current leader in cloud computing. Only 5% of the world’s workload is on the cloud presently so we are still in the early innings of a hyper-growth phase there.

By the time you price in all the transportation, labor, and warehousing costs, Amazon breaks even with its online retail business at best. The mistake people make is only focusing on this lowest of margin businesses.

It’s everything else that’s so interesting. While its profitability is quite low compared to the other FANG stocks, Amazon has the best growth outlook. For a start, third-party products hosted on the Amazon site, most of what Amazon sells, offer hefty 30% margins.

Amazon Web Services (AWS) has grown from a money loser to a huge earner in just four years. It’s a productivity improvement machine for the world’s cloud infrastructure where they pass all cost increases on to the customer who, once in, buy more services.

Apple (AAPL) is his second holding. The company is in transition now justifying a massive increase in earnings multiples, from 9X to 25X. The iPhone has become an indispensable device for people around the world, and it is the services sold through the phone that are key.

The iPhone is really not a communications device but a selling device, be it for apps, storage, music, or third-party services. The cream on top is that Apple is at the very beginning of an enormous replacement cycle for its installed base of over one billion phones. Moving from upfront sales to a lifetime subscription model will also give it a boost.

Half of these are more than four years old, and positively geriatric in the tech world. More than half of these are outside the US. 5G has added a turbocharger.

Netflix (NFLX) is another favorite. The world is moving to “over the top” content delivery and Netflix is already spending twice as much on content as any other company in this area. This is why the company won an amazing 44 Emmys last year. This will become a much more profitable company as it grows its subscriber base and amortizes its content costs. Their cash flow is growing by leaps and bounds, which they can use to buy back stock or pay a dividend.

Generally speaking, there is no doubt that the pandemic has pulled forward some future technology demand with the stay-at-home trend. But these companies have delivered normal growth in a hard world.

5G has enabled better Internet coverage for everyone and increased the competitiveness of the telecom companies. Factory automation has been another big area for 5G, as it is reliable and secure, and can be integrated with artificial intelligence.

Transportation will benefit greatly. Connected self-driving cars will be a big deal, improving safety and the quality of life.

My friend is not as worried about government-threatened break-ups as regulation. There will be more restraints on what these companies can do going forward. Europe, which has no big tech companies of its own, views big American tech companies simply as a source of revenue through fines. Driving companies out of business through cutthroat competition is simply not something Europeans believe in.

Google (GOOG) is probably more subject to antitrust proceedings both in Europe and the US. The founders have both retired to pursue philanthropic activities, so you no longer have the old passion (“don’t be evil”).

Both Google and Meta (META) control 70% of the advertising market between them, which is inherently a slow-growing market, expanding at 5% a year at best. (META)’s growth has slowed dramatically, while it has reversed at (GOOG).

He is a big fan of (AMD), one of his biggest positions, which is undervalued relative to the other chip companies. They out-executed Intel (INTC) over the last five years and should pass it over the next five years.

He has raised value tech stocks from 15% to 30% of his portfolio. Apple used to be one of these. Semiconductor companies today also fall into this category. Samsung with 40% margins in its memory business is a good example. Selling for 10X earnings is ridiculously cheap. It is just a matter of time before semiconductors get rerated too.

He was an early owner of Tesla (TSLA) back in the nail-biting days when it was constantly running out of cash. Now they have the opposite problem, using their easy access to cash through new share issues as a weapon to fight off the other EV startups. Tesla is doing to Detroit what Apple did to the cell phone companies, redefining the car.

Its stock is overvalued now but will become much more profitable than people realize. They also are starting to extract services revenues from their cars, like Apple has. Tesla will grow revenues by 30%-50% a year for the next two or three years. They should sell several millions of the new small SUV Model Y. Most other companies bringing EVs will fall on their faces.

EVs are a big factor in climate change, even in China, the world’s biggest polluter. In Europe, they are legislating gasoline cars out of existence. If you can make money building cars in Fremont, CA, you can make a fortune building them in China.

Tech valuations are high, there is no doubt about it. But interest rates are much lower by comparison. The Fed is forcing people to buy stocks, enabling these companies to evolve even faster.

Tech stocks have a lot more things going for them than against them. The customers keep coming back for more.

Needless to say, the above stocks should make up your short list for LEAPS to buy at the coming market bottom.

Global Market Comments

July 30, 2021

Fiat Lux

Featured Trade:

(JULY 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (CRSP), (TLT), (TBT), (BABA), (BIDU), (FXI), (RAD), (TSLA), (NASD), (NKLA), (NIO), (INTC), (MU), (NVDA), (AMD), (TSM), (VXX), (XVZ), (SVXY), (FCX), (ROM), (SPG)

July 28 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the July 28 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Lake Tahoe, NV.

Q: What is your plan with the (SPY) $443-$448 and the $445/450 vertical bear put spreads?

A: I’m going to keep those until we hit the lower strike price on either one and then I’ll just stop out. If the market doesn’t go down in August, then we are going straight up for the rest of the year as the earnings power of big tech is now so overwhelming. Sorry, that’s my discipline and I’m sticking to it. Usually, what happens 90% of the time when we go through the strike, and then go back down again by expiration for a max profit. But the only way to guarantee that you'll keep your losses small is by stopping out of these things quickly. That’s easy to do when you know that 95% of the time the next trade alert you’ll get is a winner.

Q: Are you still expecting a 5% correction?

A: I am. I think once we get all these great earnings reports out of the way this week, we’re going to be in for a beating. I just don't see stocks going straight up all the way through August, so that’s another reason why I'm hanging on to my short positions in the S&P 500 (SPY).

Q: What’s the best way to play CRISPR Therapeutics (CRSP) right now?

A: That is with the $125-$130 vertical bull call spread LEAPS with any maturity in 2022. We had a run in (CRSP) from $100 up to $170 and I didn’t take the damn profit! And now we’ve gone all the way back down to $118 again. Welcome to the biotech space. You always take the ballistic moves. Someday I should read my own research and find out why I should be doing this. For those who missed (CRSP) the last time, we are one proprietary drug announcement, one joint venture announcement, or one more miracle cure away from another run to $170. So that will probably happen in the next year, you get the $125-$130 call spread, and you will double your money easily on that.

Q: I’m down 40% on the United States Treasury Bond Fund (TLT) January $130-$135 vertical bear put spread LEAPS. What would you do?

A: Number one, if you have any more cash I would double up. Number two, I would wait, because I would think that starting from the Fall, the Fed will start to taper; even if they do it just a little bit, that means we have a new trend, the end of the free lunch is upon us, and the (TLT) will drop from $150 down to $132 where it was in March so fast it will make your head spin. I'm hanging onto my own short position in (TLT). If you are new to the (TLT) space and you want some free money, put on the January 2020 $150-$155 vertical bear put spread now will generate about a 75% return by the January 21, 2022 options expiration. I just didn't figure on a 6.5% GDP growth rate generating a 1.1% bond yield, but that’s what we have. I'm sorry, it’s just not in the playbook. Historically, bonds yield exactly what the nominal GDP growth rate is; that means bonds should be yielding 6.50% now, instead of 1.1%. They will yield 6.5% in the future, but not right now. And that's the great thing about LEAPS—you have a whole year or 6 months for your thesis to play out and become right, so hang on to those bond shorts.

Q: Do you have any ideas about the target for Facebook (FB) by the end of the year?

A: I would say up about 20% from current levels. Not only from Facebook but all the other big tech FANGS too. Analysts are wildly underestimating the growth of these companies in the new post-pandemic world.

Q: Do you think the worst of the pandemic will be over by September?

A: Yes, we will be back on a downtrend by September at the latest and that will trigger the next leg up in the bull market. Delta with its great infectious and fatality rates is panicking people into getting shots. The US government is about to require vaccinations for all federal employees and that will get another 5 million vaccinated. Americans have the freedom to do whatever they want but they don’t have the freedom to kill their neighbors with fatal infections.

Q: What should I do with my China (BABA), (BIDU), (FXI) position? Should I be doubling down?

A: Not yet, and there’s no point in selling your positions now because you’ve already taken a big hit, and all the big names are down 50% from the February high. I wouldn't double down yet because you don’t know what's happening in China, nobody does, not even the Chinese. This is their way of addressing the concentration of the wealth in the top 1% as has happened here in the US as well. They’re targeting all the billionaire stocks and crushing them by restricting overseas flotations and so on, so it ends when it ends, and when that happens all the China stocks will double; but I have absolutely no idea when that's going to happen. That being said, I have been getting phone calls from hedge funds who aren’t in China asking if it's time to get in, so that's always an interesting precursor.

Q: What happened to the flu?

A: It got wiped out by all the Covid measures we took; all the mask-wearing, social distancing, all that stuff also eliminates transmission of flu viruses. Viruses are viruses, they’re all transmitted the same way, and we saw this in the Rite Aid (RAD) earnings and the 55% drop in its stock, which were down enormously because their sales of flu medicines went to zero, and that was a big part of their business. I didn’t get the flu last year either because I didn’t get Covid; I was extremely vigilant on defensive measures in the pandemic, all of which worked.

Q: Why would the Fed taper or do much of anything when Powell wants to be reappointed in February 2022?

A: I don’t think he is going to get reappointed when his four-year term is up in early 2022. His policies have been excellent, but never underestimate the desire of a president to have his own man in the office. I think Powell will go his way after doing an outstanding job, and they will appoint another hyper dove to the position when his job is up.

Q: What are your thoughts on the Chinese electric auto company Nio competing here in the U.S.?

A: They will never compete here in the U.S. China has actually been making electric cars longer than Tesla (TSLA) has but has never been able to get the quality up to U.S. standards. Look what happened to Nikola (NKLA) who’s founder was just indicted. Avoid (NIO) and all the other alternative startup electric car companies—they will never catch up with Tesla, and you will lose all your money. Can I be any clearer than that?

Q: You recently raised the ten-year price target up for the Dow Average from 120,000 to 240,000. What is Nasdaq's target 10 years out?

A: I would say they’re even higher. I think Nasdaq (NASD) could go up 10X in 10 years, from 14,000 to 140,000 because they are accounting for 50% of all earnings in the U.S. now, and that will increase going forward, so the stocks have to go ballistic.

Q: What do you think of Intel (INTC)?

A: I don’t like it. They had a huge rally when they fired their old CEO and brought in a new one. There was a lot of talk on reforming and restructuring the company and the stock rallied. Since then, the market has started insisting on performance which hasn’t happened yet so the stock gave up its gains. When it does happen, you’ll get a rally in the stock, not until then, and that could be years off. So I'd much rather own the companies that have wiped out Intel: (MU), (NVDA), (AMD), and (TSM).

Q: When you do recommend buying the Volatility Index (VIX), do you recommend buying the (VIX) or the (VXX)?

A: You can only buy the VIX in the futures market or through ETFs and ETNs, like the (VXX), the (XVZ), and the (SVXY), or options on these. I would be very careful in buying that because time decay is an absolute killer in that security, and that's why all the professionals only play it from the short side. That's also why these spikes in prices literally last only hours because you have professionals hammering (VIX). Somebody told me once that 50% of all the professional traders in the CME make their living shorting the (VIX) and the (VXX). So, if you think you’re better than the professionals, go for it. My guess is that you’re not and there are much better ways to make money like buying 6-to-12-month LEAPS on big tech stocks.

Q: Can the Delta variant get a bigger pullback?

A: Yes. I expect one in August, about 5%. But if Delta gets worse, the selloff gets worse. You saw what it did last year, down 40% in the (SPY) in only two months, so yes, it all depends on the Delta virus. I'm not really worrying about Delta, it's the next one, Epsilon or Lambda, which could be the real killer. That's when the fatality rate goes from 2% to 50%, and if you think I'm crazy, that's exactly what happened in 1919. Go read The Great Influenza book by John Barry that came out 20 years ago, which instantly became a best seller last year for some reason.

Q: Does the Matterhorn have enough flat space on the top to stand on it?

A: Actually, there is a 6’x6’ sort of level rock to stand on top of the Matterhorn. If you slip, it’s a 5000’ fall straight down on any side, and on a good weather day in the summer, there are 200 people climbing the Matterhorn. There's sometimes a one-hour line just to take your turn to get to the top to take your pictures, and then get down again to make space for the next person. So that's what it's like climbing the Matterhorn, it's kind of like climbing Mount Everest, but I still like to do it every year just to make sure I can do it, and one year I hope to win the prize for the oldest climber of the year to climb the Matterhorn. Every year this German guy beats me; he’s two years older than me.

Q: When will Freeport McMoRan (FCX) start going up? I have the 2023 LEAPS

A: Good thing you have the two-year LEAPS because that gives you two years for inflation to show its ugly face once again. You just have to be patient with these. I think we’ll get a rally in the Fall along with all the other interest rate plays like banks, industrials, money management companies, and so on. (FCX) will certainly participate in that. In the meantime, if we get all the way down to $30 in Freeport McMoRan, I would double up your position.

Q: Why is oil (USO) not a buy? Oil is the ultimate inflation hedge.

A: Yes, unless all of the cars in the United States become electric in the next 15 years, which they will, wiping out half of all demand from the largest oil consumer. The United States consumes about 20 million barrels of oil a day, half of that is for cars, and if you take that out of the demand picture you dump 10 million barrels a day on the market and oil goes back to negative numbers like we saw last year. Never do counter-trend trades unless you’re a professional in from of a screen 24 hours a day.

Q: Should I take profits on my ProShares Ultra Technology ETF (ROM) November $90-$95 vertical bull spread and then enter a new spread when tech sells off?

A: Absolutely! When you have that much leverage and you get these price spikes, you sell! The leverage on this position is 2X on the ETF and 10X on the options for a total of 20X! Well done, nice trade and nice profit, go out and buy yourself a new Tesla and wait for the next dip in tech, which may have already started, and which could power on for the rest of August.

Q: What’s the next move for REITs?

A: REITs came off of historic lows last year; a lot of people thought they were going to go bankrupt, and for companies like (SPG) it was a close-run thing. I would be inclined to take profits on REITs here. The next thing to happen is for interest rates to go up and REITs don’t do that great in a rising rate environment.

Q: When is the off-season in Incline Village?

A: It’s the Spring and the Fall, in between ski season and the summer season. That means there are four months a year here, May/June and September/October, where I’m the only one here and the parking lots are empty. There is no one on the trails, the weather is perfect, the leaves are changing colors, and the roads aren’t crowded, so that is the time to be here. It’s a mob scene in the winter and a worse mob scene in the summer!

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

July 21, 2021

Fiat Lux

Featured Trade:

(AN INSIDER’S GUIDE TO THE NEXT DECADE OF TECH INVESTMENT),

(AMZN), (AAPL), (NFLX), (AMD), (INTC), (TSLA), (GOOG), (FB)

Mad Hedge Technology Letter

May 21, 2021

Fiat Lux

Featured Trade:

(THE STRENGTH OF AMD)

(AMD), (INTC), (TSM), (XLNX), (SMH)

Advanced Micro Devices Inc. (AMD) is a chip stock that needs some serious attention, even more so because of their new share repurchase program that has no end date.

They are led by one of the best tech CEOs in Silicon Valley Lisa Su, who has been in charge since 2014.

She transformed the company into a profitable one, secured incremental market share from Intel Corp. (INTC) and diminished concerns that AMD has a weak balance sheet.

Strength begets strength as AMD introduced a $4 billion stock buyback plan, its first repurchase authorization since 2001, signaling the chipmaker’s robust momentum in their own business.

The buyback will be distributed through cash from operations and will total about 4% of AMD’s market value.

AMD's stock in the high $70s right here looks like a screaming buy.

Share buyback is not only something Apple and Microsoft do, but other smaller players are getting in on the action displaying the great breadth and depth of the tech market.

We don’t see this anywhere else in any other industry because profitable companies simply return money back to shareholders and tech has the luxury of accelerated future earnings and revenue growth to buttress this.

Cut it up however you want, the tech sector is responsible for the bulk of earnings as it relates to the total market and that won’t change.

AMD delivered $832 million in free cash flow in Q1 2021.

The company has now pivoted from a net debt position to a balance sheet that will harness over $3 billion in net cash by the end of the current quarter.

This strength of the balance sheets is even pertinent if you strip out the Xilinx deal which will bring in their own array of financial pluses to add on to the might of AMD's current cash flow situation.

An accumulating share count is something to be wary of in any stock and given that AMD had the opportunity to reduce share count, it was a no-brainer.

Years ago, AMD had 766 million shares outstanding, and it would have climbed to over 1.6 billion considering the Xilinix shares by the end of this year.

This obviously makes EPS metrics appear rosier in future earnings reports and inching them up is a nod to AMD CFO Devinder Kumar who usually has a big say in these decisions.

Under Su’s helmsmanship, the company’s market value has toppled the $90 billion mark from only $2 billion just seven years ago.

That was the year she was named CEO and she hasn’t looked back.

Su’s key to returning AMD to profitability was to rely on the quality of product delivered — these new products snatched market share from Intel.

As what a savvy CEO usually does, she has played down success in order to tamper down high expectations in the stock price and business by saying, “without a doubt it does not get easier.”

I don’t think it was ever easy to begin with but that’s beside the point.

Su’s AMD has gone from an inferior chipmaker building cheaper knockoffs to Intel products to a premium provider of computer processors that win orders solely based on superior performance.

AMD has already repurchased $77 million of stock in its prior buyback plan two decades ago.

Su has rejuvenated AMD’s reputation and performance at a critical juncture and as chip shortages become the norm in this boom-and-bust industry.

The public health problem triggered a crazy demand for remote work and the devices that facilitate a work from home economy.

During this sensitive period, the world’s largest chipmaker, Intel, had struggled to develop its manufacturing technology, one of the foundations of its decades-long dominance of the computer industry.

The chip shortage is an example of the periodic mismatch between supply and demand in the semiconductor market whose companies avoid dipping into capital expenditure until capacity is stretched to the extreme limit.

This is an expensive business to get into, constructing high-performance chips is time-consuming and an engineering headache, thus barriers of entry are incredibly insurmountable.

Most new chip foundries and designers don’t happen unless sovereign nations make it a national security issue which is the case lately.

Ancillary industries started to hoard chips 6-8 months ago and I believe that these pressures will begin to subside soon as supply chains start to normalize.

These longer-term contracts to secure inputs we are seeing now will eventually be reduced easing the supply crunch as demand begins to slow and capacity begins to rise.

Even Su predicts supply of AMD chips, which are built by Taiwan Semiconductor Manufacturing (TSM), will catch up throughout 2021.

As the tech consolidation rips through chip stocks, I see this as an unequivocal buying opportunity for the strongest of names.

If AMD continues to build on their strong financial position — continue to offer more share repurchases and even a sweet dividend — it clearly means they are building premium products buyers want and that satisfaction not only filters down to the end-user of their chips but the owners of the stock.

I first recommended this stock at $18 at the advent of the Mad Hedge tech letter in 2018, and I am still bullish AMD long term period.

It was a great company in 2018 — it’s gotten even better in 2021 — don’t miss out.

Global Market Comments

March 29, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WEEK THAT NEVER WAS),

(SPY), (TLT), (TBT), (TSLA), (CSCO), (ORCL), (INTC)

Of course, WWII historians know well the man who never was, the popular name for Operation Mincemeat.

In 1943, British intelligence found a homeless man who died on the streets of London, dressed him up as a Royal Marine Major William Martin, and released his body from a submarine off the coast of Spain, a German ally.

Handcuffed to his wrist was a briefcase with highly detailed plans for the allied invasion of Greece and the Balkans. The Germans shifted ten divisions to defend the region.

When the allies invaded Sicily instead, it came completely out of the blue. The invading American and British forces found the island almost undefended and inadequately manned and supplied by Italian troops. The allies planned for three months to capture Sicily. Instead, they did it in a mere 38 days. Allied losses came in at a tenth of those expected, thanks to Royal Marine Major William Martin.

The analogy here is that last week, we witnessed the market that never was. Stocks went down, then up. Bonds went up, then down. Even Tesla was virtually unchanged. It all ended up as a big fat zero for traders.

What all of this means for us investors is a subject of heated discussion among strategists. Of course, the Cassandras are always out there arguing that this is all proof that markets are peaking and that the mother of all stock market crashes is just ahead of us.

I take a different tack.

I think we are well into a long-overdue “time” correction whereby stocks go sideways for weeks or months before resuming their heroic assault on new highs. The timing will be dictated by the frantic reversal of the bond market at a ten-year Treasury yield of 2.00%.

Investors will rotate from the newly expensive recovery plays like banks into the newly cheap, such as technology stocks. Notice the sudden recent interest in legacy companies like Oracle (ORCL), Intel (INTC), and Cisco Systems (CSCO), which completely missed the great 2020 tech rally.

All of this sets up perfectly for the barbell portfolio which I have been advocating all year.

If there is a selloff, it will be by things that normal people don’t own. Those include SPACS, anything the Reddit crowd chases, stay-at-home stocks, and very high-priced tech stocks with no earnings.

Much focus has been placed on the Taiwanese-owned Ever Given stuck in the Suez Canal. As a Middle Eastern war correspondent for many years, I spent endless hours debating with my compatriots over what closure of the canal would mean.

What hasn’t been mentioned was that the accident was not caused by a Chinese captain, but Egyptian pilot ships are required to take on to raise revenues, and bribes, for the impoverished country. This all happened in the middle of a sandstorm where visibility is near zero.

I can tell you right now that they won’t get the Ever Given off there until they start to unload containers and lift off some weight so the 200,000-ton ship can rise of its own accord. Good luck with that in the middle of the Sinai Desert. Why not just sell all the contents on Amazon and have them deliver it for free as part of their prime membership?

This is a debacle that will last weeks, if not months, and will cost $9 billion a day in international trade until it’s over. In the meantime, commercial shippers have asked for protection from pirates from the US Navy as they navigate the unfamiliar water around the tip of Africa.

The Mad Hedge Summit Videos are Up, from the March 9,10, and 11 confab. Listen to 27 speakers opine on the best strategies, tactics, and instruments to use in these volatile markets. The product discounts offered last week are still valid. Start, stop, and pause the videos at your leisure. Best of all, access to the videos is FREE. Access them all by clicking here, click on CURRENT SUMMIT REPLAYS in the upper right-hand corner, and then choose the speaker of your choice.

Weekly Jobless Claims dive by 100,000, to 684,000, a one-year low. The decline was led by Illinois and Ohio. Labor shortages are popping up around the country in skilled areas, but bars and restaurants are still lagging severely.

Huge Office Cuts are coming, with execs planning a permanent 20% cut. Better to give the money to shareholders. Downtowns across the country will change beyond all recognition. How do you turn an office into an apartment?

CP Rail buys Kansas City Southern, for $25 billion, further concentrating the north American rail industry. It’s a steal because an economy entering a decade-long boom moves lots of stuff. It’s also a great North/South international trade play, which is recovering strongly with the exit of our last president. I used to ride box cars on the old Canadian Pacific back in the sixties (you can’t hitch hike where there are no cars), and occasionally the engineers would let me drive. It suddenly makes Norfolk South (NSC) and Union Pacific (UNP) look very tempting.

Another Tesla $3,000 Target was issued by Ark’s Cathie Wood, an early investor. Cathie’s Ark Innovation Fund ETF was up 180% last year largely on the strength of a massive Tesla (TSLA) holding. Her bear case is a low of $1,500 by 2025, nearly triple the current price. She has only one more triple to go to get to my own $10,000 forecast.

Biden has $3 Trillion More to Spend on top of the just passed $1.9 trillion rescue package. It's all rocket fuel for the stock market, not so much for bonds. The money will be spent on a mix of old-line freeway and bridge repair along with new spending on decarbonizing the power grid and social measures. It will be financed by tax hikes on those earning over $400,000. Remember, Roosevelt hiked the maximum tax rate to 90% on the wealthy, where it stayed for 30 years, and Biden is old enough to remember.

Daily Air Travelers top 1.5 Million, for the first time in a year. The pandemic low was 200,000 a day. It’s an indication of how anxious Americans have become to travel, and how strong the imminent economic boom will be.

Intel to build two chip fabs for $20 billion in Arizona to address the current severe shortage. US construction is a positive as it helps reduce reliance on foreign supplies. Too bad it will still leave them five years behind (AMD), but it’s a major move in the right direction. It deals with everything investors wanted to hear and moves them solidly into the 10nm architecture market. Buy (INTC) on dips.

New Home Sales Dive, off 18.2% in February, now that the free money train has left the station. Weather was blamed as a factor, with giant snowstorms slamming much of the country. Shortage of supply is another big issue. Some big builders are basically out of inventory and are reduced to selling floor plans with extended completion dates.

US Dollar (UUP) hits a four-month high, with a major assist from rising US bond interest rates. Expect the rally to continue until ten-year yields hit 2.00%, then sell the daylights out of it. With the US money supply growing at a near exponential 30% annual rate, there’s no way the dollar strength can continue. When you increase the supply, you decrease the value, simple supply and demand. My first pick is to buy the Aussie (FXA) a call option on a global synchronized economic recovery.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000, here we come!

It’s amazing how well patience can help your performance. My Mad Hedge Global Trading Dispatch profit reached a super-hot 18.61% so far in March on the heels of a spectacular 13.28% profit in February.

It was a go-nowhere week in the market, so I limited myself to a single trade all week, a double short in the bond market (TLT) on top of a welcome $5 rally. The position turned immediately profitable.

I still have a deep in-the-money call spread Tesla (TSLA) that is profitable and expires in 14 trading days. That leaves me with 70% cash and a barrel full of dry powder.

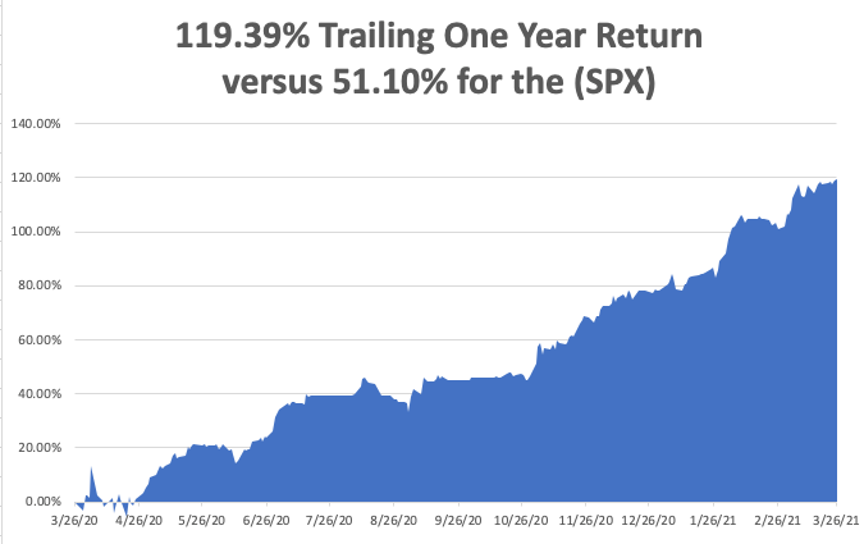

This is my fifth double-digit month in a row. My 2021 year-to-date performance soared to 42.10%. The Dow Average is up 9.9% so far in 2021.

That brings my 11-year total return to 464.65%, some 2.08 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 41.30%.

My trailing one-year return exploded to positively eye-popping 119.39%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Corona virus cases at 30.2 million and deaths topping 550,000, which you can find here.

Thankfully, death rates have slowed dramatically, but Obituaries are still the largest sector in the newspaper. At this point, some 47% of the US population has achieved immunity through vaccination or catching the disease. Herd immunity is near.

The coming week is a big one for jobs data.

On Monday, March 29, at 9:00 AM, the Dallas Fed Manufacturing Index for March is released.

On Tuesday, March 30, at 9:00 AM, the S&P Case Shiller National Home Price Index for January is published.

On Wednesday, March 31 at 8:15 AM, the ADP Challenger Private Employment Report for March is out. Pending Home Sales for February are indicated at 9:00 AM.

On Thursday, April 1 at 8:30 AM, the Weekly Jobless Claims are published.

On Friday, April 2 at 8:30 AM we get the Nonfarm Payroll Report for March. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, tax time is coming up and let me tell you, I have absolutely the best IRS story of all time.

It comes from my late, dear friend, Al Pinder, who I sat next to for ten years at the Foreign Correspondents of Japan in Tokyo, pounding away on antiquated Royal typewriters until our shoulders were as stiff as boards. Al then was the shipping correspondent for the New York Journal of Commerce newspaper.

Al was a colorful character, to say the least.

In the run up to WWII, Al took an extended vacation in Japan where he toured and photographed the country’s beaches, looking for the best landing sites for the US military in case war broke out.

To sneak the top-secret pictures out of the country, he bought a large steamer trunk and placed them a false bottom. Then he went to Tokyo’s red-light district in Yoshiwara, bought a dubious sex toy, an inflatable life-sized Japanese doll, and placed it on top.

When the trunk was searched, the customs officials found the doll, had a good laugh and passed him on. Al’s photos were the basis of Operation Olympic, the 1945 US invasion of Japan, made unnecessary by the dropping of the atomic bomb.

When the war broke out, Pinder parachuted into western China, where he acted as the liaison with Mao Zedong’s guerilla forces in Hunan province. In 1944, Al received a coded message from headquarters ordering him to intercept a top-secret airdrop from a DC3 in the middle of the night.

Knowing he would be mercilessly tortured by the Japanese if caught, he set up three signal fires in a triangle in a remote part of the desert and managed to find the parachute. Dodging enemy patrols all the way, he returned to his hideout in a mountain cave and opened the package.

In it was a letter from the IRS asking why he had not filed a tax return for the past three years.

I told this story at Al’s wake a few years ago and everyone had a good laugh. Al went on to run CIA operations in Japan during the fifties and sixties. When he passed away, there was a frantic search for a safe deposit box by American intelligence officials containing records of all CIA payoffs to Japan’s leading conservative party.

When the box was finally found, there was an enormous sigh of relief at the embassy. I still miss Al.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

December 28, 2020

Fiat Lux

SPECIAL ISSUE ABOUT THE FAR FUTURE

Featured Trade:

(PEEKING INTO THE FUTURE WITH RAY KURZWEIL),

(GOOG), (INTC), (AAPL), (TXN)