Nvidia (NVDA) was right to pull the trigger – that was my first reaction when I first learned that they had aggressively acquired Israeli chip company Mellanox for $6.9 billion.

The fight to seize these assets were fierce triggering a bidding war -American heavyweights Intel and Microsoft were also in the mix but lost out.

CEO of Nvidia Jensen Huang touted the importance of the deal by explaining that “the emergence of AI and data science as well as billions of simultaneous computer users, is fueling skyrocketing demand on the world's data centers."

Therefore, satisfying this demand will require holistic architectures that connect massive numbers of fast computing nodes over intelligent networking fabrics to form a giant datacenter-scale compute engine.

Mellanox and its capabilities cover all the bases for Nvidia and will nicely slot into its portfolio offering, an added bonus of cross-selling and upselling opportunities to existing clients.

The strategic motives behind the deal are plentiful with increased importance of connectivity and bandwidth enhancing Nvidia's ability to provide datacenter-scale computing across the full stack for next-generation high-performance computing and AI workloads.

The agreement is the result of the company's shift toward next-gen technology as adoption of cloud, AI, and robotics ramps up and Nvidia will be at the forefront of this massive migration.

As the fourth industrial revolution advances, Nvidia is best of breed of semiconductor companies and the imminent adoption of 5G will aid the likes of Microchip Technology (MCHP) and Xilinx (XLNX).

Technology is rapidly changing, and the data center is the segment that is accelerating at a faster clip than in previous years translating into de-emphasizing current revenues of gaming and autonomous on a relative growth basis.

These segments will be secondary to the addressable opportunity in data center and signing up Mellanox is a key strategic initiative to exploit this growth opportunity.

Missing the boat on this compelling opportunity could have dragged Nvidia into an existential crisis down the road as the missed opportunity costs of lucrative data center revenues would begin to bite, and with no quick fix on the horizon, Nvidia’s growth drivers would be potentially disarmed.

Investors need to remember that Nvidia derives half of its revenue from China and up until this point, gaming had been a huge tailwind to its total revenue, however, the Chinese communist party has identified gaming addiction in young adults as a national crisis and have been refusing to deliver new gaming licenses to gaming creators.

As the data center via the cloud begins its next ramp-up of insatiable demand, Nvidia was acutely aware they could not miss the boat and to grab a foot hole against larger player Intel.

Almost overpaying to have more skin in the game does not do justice to what the ramifications would have been if Intel or even Microsoft were able to hijack this deal.

The two-fold victory will in turn boost sales of Nvidia's data center products long term while depriving Intel of extending the lead in data center.

And after the lack of recent underperformance in the prior quarter, Nvidia needed a gamechanger to cauterize the blood flow.

Nvidia's total revenue plunged more than 24% YOY in Q4 of 2018, and shareholders have been looking for remedies, especially after the once mythical cryptocurrency business blew up and the company was stuck with a glut of inventory.

The purchase of Mellanox will help Nvidia start competing with other dominant players like Cisco Systems (CSCO) and Arista Networks (ANET).

Mellanox is one of a handful of firms selling hardware that connects devices in the data center through network cards, switches, and cables.

The deal still needs regulatory approval and could be a stumbling block if Chinese authorities drag this into the orbit of the trade war and make it a bullet point in negotiations.

The net result is positive to the overall business model, and this move will breathe oxygen into Nvidia’s long-term narrative with a flow of revenue set to come online once the 5,000 Mellanox employees are integrated into Nvidia’s levers of operation.

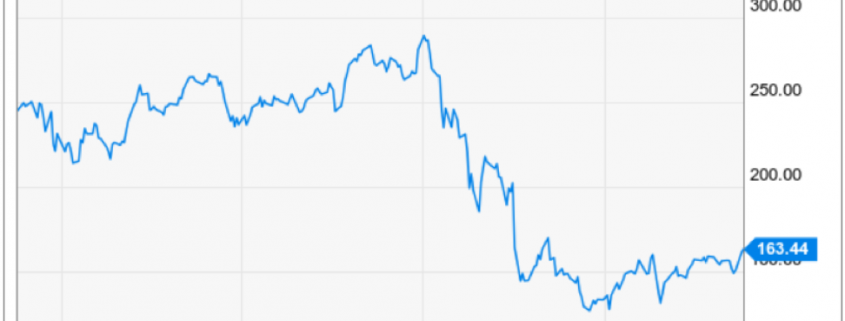

Shares should be the recipient of short-term strength and after getting smushed by a poor last quarter, there is substantial room to the upside.

A dip back to $150 would serve as a good entry point to strap on a short-term bullish trade in Nvidia shares.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/NVDA-mar13.png564972Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-13 01:06:052019-07-10 21:43:29Nvidia Steps Up its Game

Anyone would be forgiven for thinking that the stock market has become bipolar.

According to the Commerce Department’s Bureau of Economic Analysis, the answer is that corporate profits account for only a small part of the economy.

Using the income method of calculating GDP, corporate profits account for only 15% of the reported GDP figure. The remaining components are doing poorly or are too small to have much of an impact.

Wages and salaries are in a three-decade-long decline. Interest and investment income are falling because of the ultra-low level of interest rates. Farm incomes are at a decade low, thanks to the China trade war, but are a tiny proportion of the total, and agricultural prices have been in a seven-year bear market.

Income from non-farm unincorporated business, mostly small business, is unimpressive.

It gets more complicated than that.

A disproportionate share of corporate profits is being earned overseas.

So, multinationals with a big foreign presence, like Apple (AAPL), Intel (INTC), Oracle (ORCL), Caterpillar (CAT), and IBM (IBM), have the most rapidly growing profits and pay the least amount in taxes.

They really get to have their cake and eat it too. Many of their business activities are contributing to foreign GDPs, like China’s, far more than they are here.

Those with large domestic businesses, like retailers, earn less but pay more in tax as they lack the offshore entities in which to park them.

The message here is to not put all your faith in the headlines but to look at the numbers behind the numbers.

Caveat emptor. Buyer beware.

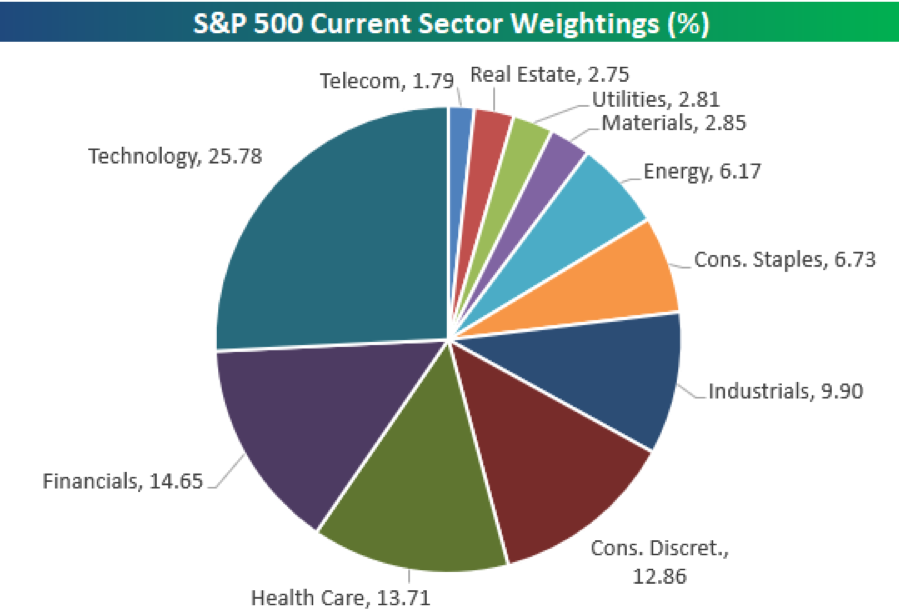

What’s In the S&P 500?

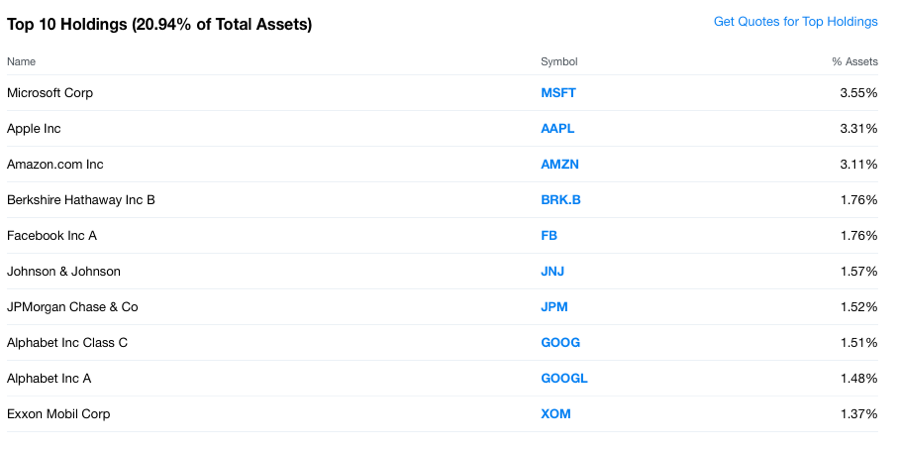

S&P Top 10 Holdings 3-4-2019

Has the Market Become Bipolar?

https://www.madhedgefundtrader.com/wp-content/uploads/2017/01/Bipolar-Masks-e1485650935616.jpg316400The Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngThe Mad Hedge Fund Trader2019-03-05 02:07:572019-03-05 01:52:18The Bipolar Economy

The company is doing backflips and edging around other fertile pastures to the dismay of competitors.

They jumped all over Intel’s (INTC) CPU lead promising more cores and adding on more features to lure in a new audience.

In terms of computer graphics, Nvidia (NVDA) still wields more clout in the higher-grade GPU space and AMD has been playing second fiddle with cheaper, value-oriented GPU cards that can be best described as mid-range.

That is about to change.

AMD is at it again acing its attempt to pull down Goliath with its new Radeon VII.

This $700 GPU card is the first 7 nanometer (nm) GPU on the market and is a warning shot to Nvidia who they plan to surgically invade in order to snatch market share.

This new AMD GPU is a direct threat to Nvidia’s set of RTX 2080 graphics cards and is set at the same price point with comparable performance.

The Radeon VII is the next iteration to AMD’s Vega 64 and possesses similar architecture with specific enhancements in clock speeds and VRAM.

Gamers are still on the fence to whether this new product can eclipse the heavily entrenched Nvidia graphics cards that are time-honored, tested and stamped with the industries seal of approval.

It is still uncertain whether AMD can introduce the necessary supply and if you still remember when the prior iteration Vega 64 debuted in 2017, it was a threat to Nvidia’s top-tier GTX 1080, but ran out of inventory quickly.

The new Radeon VII card is one of the best on the market for professional work and still does well in the gaming realm, albeit with a lack of ray tracing.

Few video games support ray tracing currently but new game studios plan to adopt this cutting edge technology later this year.

I commend AMD’s first foray into this part of the niche market and when AMD upgrades its architecture and improves on the next iteration, Nvidia will be squarely in their crosshairs.

The number of new products that drive top-line growth is another reason to be positive on this stock.

Looking at the CPU market – momentum would be the key word to describe AMD’s current trajectory.

For generations, Intel has had a secure stranglehold on this rapidly expanding market, but the fringes of the industry have been hijacked by AMD and they seek to spread its tentacles deeper into foreign CPU waters.

By the end of the year, I believe that AMD will carve out a nice high single digit market share of global CPU sales.

Intel has been bogged down by production setbacks in the deployment of the 10-nm server chip giving AMD a chance to take advantage of this gaping pothole to jack up sales with its EPYC chip.

Not only that, AMD is motoring ahead with a superior 7-nm chip which is a faster processor and is more energy-friendly than Intel’s 10-nm version.

I can conclude that AMD is blowing past Intel in chip technology, and has its third generation of CPUs earmarked for the market in the summer ready to stretch the lead.

CEO of AMD Dr. Lisa Su is compounding the misery for Intel, offering a physical glimpse of plans to roll out its third generation Ryzen CPUs for PCs by the middle of the year at the Consumer Electronics Show in January.

Another catalyst that could drive the stock higher is a favorable earnings outlook in 2019.

After meeting expectations last quarter, expansion is expected in the high single digits in a tough chip environment that has wrought its fair share of carnage.

I wouldn’t pigeonhole the new product line as mere hype, it’s clear they are meaningfully enhanced and improved with each successive iteration.

I estimate that these new products will give AMD solid traction to close in on the competition in the CPU and GPU markets.

Clearly, this isn’t a 1-quarter venture, but visibly aware that AMD is making inroads into other markets are a demonstrably net negative to weight on Intel and Nvidia shares.

This part of tech is not without its headaches and is fraught with China risk.

Chinese gaming regulators have put the kibosh on new gaming licenses and AMD’s scaling back of forecasts should reflect this development.

Intel cited falling spend on server chips and Nvidia came out with a dreadful earnings report to forget lately.

However, when there is blood in the streets, the status quo is ripe for some change and I am confident that AMD can execute this aggressive ramp up after digesting some of the excessive inventory in the first quarter.

As AMD trades at $24, I can’t help but believe this name will end the year higher.

Investors must remember that in the near term, the Fed has hit the pause button aiding the equity market, and China has reportedly been keen on some massive chip purchases to help soothe the nerves of the administration.

If the market can marry this up with favorable reviews of AMD’s latest products, I don’t see why AMD can’t be trading at $30 by the end of the year.

At the Mad Hedge Lake Tahoe Conference, I proclaimed that AMD was one of my favorites going into 2019 and exploded upwards from $17 in October 2018.

AMD truly has not disappointed.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/02/AMD.png499972Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-02-21 08:06:162019-07-09 12:11:47Buy AMD on the Dip

Great company – lousy time to be this great company.

That is the least I can say for GPU chip company Nvidia (NVDA) who issued a cataclysmic earnings alert figuring it was better to spill the negative news now to start the healing process earlier.

This stock is a great long-term hold because they are the best of breed in an industry fueled by a secular tailwind in GPUs.

But this doesn’t mean they will be gifted any freebies in the short term and, sad to say, they have been dragged, kicking and screaming, into the heart of the trade skirmish along with Apple (AAPL) and buddy Intel (INTC) amongst others.

The best thing a tech company can have going for them right now is to have no China exposure, that is why I am bullish on software companies such as PayPal, Twilio, and Microsoft.

I called the chip disaster back in summer of 2018 recommending to stay away like the plague.

The climate has worsened since then and like I recently said – don’t buy the dead cat bounce in chips because the bad news isn’t baked into the story yet or at least not fully baked.

It’s actually a blessing in disguise if banned in China if you are firms such as Facebook (FB), Google (GOOGL), and Amazon (AMZN).

I recently noted that a material end to this trade war could be decades away and the tech world is already being reconfigured around the monopoly board as we speak with this in mind.

Where do things stand?

The US administration took a scalp when Chinese communist backed DRAM chip maker Fujian Jinhua effectively shuttered its doors.

Victory in a minor battle will likely embolden the US administration into continuing its aggressive stance if it is working.

If you forgot who Fujian Jinhua was… they are the Chinese chip company who were indicted by the U.S. Justice Department for stealing intellectual property (IP) from Boise-based chip behemoth Micron (MU).

The way they allegedly stole the information was by poaching Taiwanese chip engineers who would divulge the secrets to the Chinese company buttressing China in pursuing their hellbent goal of being able to domestically supply enough quality chips in order to stop buying American chips in the future.

Officially, China hopes to ramp up its self-sufficiency ratio in the semiconductor industry to at least 70% by 2025 which dovetails nicely with the broader goal of Chinese tech hegemony.

Fujian Jinhua was classified as a strategically important firm to the Chinese state and knocking the wind out of their sails will have a reverberating effect around the Chinese tech sector and will deter Taiwanese chip engineers to act as a go-between.

According to a research note by Zhongtai Securities, Jinhua’s new plant was expected to have flooded the market with 60,000 chips per month and generate annual revenue of $1.2 billion directly competing with Micron with their own technology borrowed from Micron themselves.

Jinhua’s overall goal was to support a monthly manufacturing target of 240,000 chips spoiling Chinese tech companies with a healthy new stream of state-subsidized allotment of chips needed to keep costs down and build the gadgets and gizmos of the future.

For the most part, it was unforeseen that the US administration had the gall and calculative nous to combat the nurtured Chinese state tech sector.

However, I will say, it makes sense to pick off the Chinese tech space now before they stop needing American chips at all in 5-7 years and when all remnants of leverage disappear.

The short-term pain will be felt in the American chip tech sector which is evident with the horrid news Nvidia reported and the aftermath seen in the price action of the stock.

Nvidia expects top line revenue to shrink by $500 million or half a billion – it’s been a while since I saw such a massive cut in forecasts.

Half of revenue comes from the Middle Kingdom and expect huge downgrades from Apple on its earnings report too.

If this didn’t scare you, what will?

These short-term headwinds are worth it to the American tech sector as a whole.

To eventually ward off a future existential crisis when Chinese GPU companies start offering outside business actionable high quality chips curated with borrowed technology, funded by artificially low debt, and for half the price is worth its weight in gold.

The same story is playing out with Huawei around the globe but at the largest scale possible.

This is what happens when the foreign tech sector is up against companies who have access to unlimited state loans and is part of wider communist state policy to take over foundational technology globally.

I will also emphasize that the Chinese communist party has a seat on every board at any notable Chinese tech company influencing decisions at the top even more than the upper management.

If upper management stopped paying heed to the communist voice at the table, they would be out of business in a jiffy.

Therefore, Huawei founder Ren Zhengfei standing at a podium promulgating a scenario where Huawei is operating freely from the government is what dreams are made of.

It’s not a prognosis rooted in reality.

The communist party are overlords breathing down the neck of Huawei after any material decisions that can affect the company and subsequently the government’s position in the interconnected world.

The China blue print essentially entails a pan-Amazon strategy emphasizing large volume – low cost strategy.

Amazon was successful because investors would throw money at the company until it scaled up and wiped the competition away in one fell swoop.

Amazon is on a destructive path bludgeoning every American second-tier mall reshaping the economic world.

The unintended consequences have been profound with the ultimate spoils falling at the feet of CEO and Founder of Amazon Jeff Bezos, his phalanx of employees as well as Amazon stockholders which are mostly comprised of wealthy investors.

Well, Chairman Xi Jinping and the Chinese communist party are attempting to Amazon the American tech sector and the broader American economy.

The American economy could potentially become the second-tier mall in this analogy and the game playing out is an existential crisis for the likes of Advanced Micro Devices (AMD), Nvidia, Micron, Intel and the who’s who of semiconductor chips.

If stocks reacted on a 30-year timeframe, Nvidia would be up 15% today instead of reaching a trading day nadir of 17%.

What is happening behind the scenes?

American tech companies are moving supply chains or planning to move supply chains out of China.

This is an epochal manifestation of the larger trade war and a decisive development in the eyes of the American administration.

In fact, many industry analysts understand a logjam of failed trade solutions as a bonus to the Chinese.

However, I would argue the complete opposite.

Yes, the Chinese are waiting out the current administration to deal with a new one that might be more lenient.

But that will take another two years and publicly listed companies grappling with the performance of quarterly earnings don’t have two years like the Chinese communist party.

And who knows, the next administration might even seize the baton from the current administration and clamp down even more.

Be careful what you wish for.

Taiwanese company and biggest iPhone assembler Foxconn Technology Group is discussing plans to move production away from China to India.

India is a democratic country, the biggest democracy in Asia, and is a staunch ally of the United States.

CEOs of Google (GOOGL) and Microsoft (MSFT), some of Silicon Valley heavyweights, are from India and American tech companies have been making generational tech investments in India recently.

Warren Buffet even invested $300 million in an Indian FinTech company Paytm.

When you read stories about India being the new China, well it’s happening faster than anyone thought and on a scale that nobody thought, and the underlying catalyst is the overarching trade war fueling this quick migration.

Apple is already constructing low grade iPhones in India in the state of Karnataka since 2017, and these were the first iPhones made in India.

They won’t be the last either.

Wistron, major Taiwanese original design manufacturer, has since started producing the iPhone 6S model there as well.

And it is no surprise that China and its artificially priced smartphones have undercut Samsung and Apple in India grabbing the market share lead.

This is happening all over the emerging world.

And don’t forget if U.S. President Donald Trump revisits banning American chip companies supply channels to Chinese telecom company ZTE. That would be 70,000 Chinese jobs out the window in a nanosecond.

The current administration has drier powder than you think and this would hasten the deceleration of the Chinese economy and also move forward the American recession into 2019 boding negative for tech shares.

Therefore, I would recommend balancing out a trading portfolio with overweights and underweights because it is obvious that tech stocks won’t be coupled to a gondola trajectory to the peak of the summit this year.

It’s a stockpickers market this year with visible losers and winners.

And if China does get their way in the tech war, American chip companies will eventually become worthless squeezed out by mainland competition brought down by their own technology full circle.

They are first on the chopping board because their overreliance on Chinese revenue streams for the bulk of sales.

Among these companies that could go bust are Broadcom (AVGO), Qualcomm (QCOM), Qorvo (QRVO), Skyworks Solutions (SWKS) and as you expected Micron and Nvidia who are one of the main protagonists in this story.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-29 08:06:032019-07-09 04:53:00What’s Behind the NVIDIA Meltdown

Don’t buy the dead cat bounce – that was the takeaway from a recent trading day that saw chips come alive with vigor.

Semiconductor stocks had their best day since March 2009.

The price action was nothing short of spectacular with names such as chip equipment manufacturer Lam Research (LRCX) gaining 15.7% and Texas Instruments (TXN) turning heads, up 6.91%.

The sector was washed out as the Mad Hedge Technology Letter has determined this part of tech as a no-fly zone since last summer.

When stocks get bombed out at these levels - sometimes even 60% like in Lam Research’s case, investors start to triage them into a value play and are susceptible to strong reversal days or weeks in this case.

The semi-conductor space has been that bad and tech growth has had a putrid last six months of trading.

In the short-term, broad-based tech market sentiment has turned positive with the lynchpins being an extremely oversold market because of the December meltdown and the Fed putting the kibosh on the rate-tightening plan.

Fueled by this relatively positive backdrop, tech stocks have rallied hard off their December lows, but that doesn’t mean investors should take out a bridge loan to bet the ranch on chip stocks.

Another premium example of the chip turnaround was the fortune of Xilinx (XLNX) who rocketed 18.44% in one day then followed that brilliant performance with another 4.06% jump.

A two-day performance of 22.50% stems from the underlying strength of the communication segment in the third quarter, driven by the wireless market producing growth from production of 5G and pre-5G deployments as well as some LTE upgrades.

Give credit to the company’s performance in Advanced Products which grew 51% YOY and universal growth across its end markets.

With respect to the transformation to a platform company, the 28-nanometer and 16-nanometer Zynq SoC products expanded robustly with Zynq sales growing 80% YOY led by the 16-nanometer multiprocessor systems-on-chip (MPSoC) products.

Core drivers were apparent in the application in communications, automotive, particularly Advanced Driver Assistance Systems (ADAS) as well as industrial end markets.

Zynq MPSoC revenues grew over 300% YOY.

These positive signals were just too positive to ignore.

Long term, the trade war complications threaten to corrode a substantial chunk of chip revenues at mainstay players like Intel (INTC) and Nvidia (NVDA).

Not only has the execution risk ratcheted up, but the regulatory risk of operating in China is rising higher than the nosebleed section because of the Huawei extradition case and paying costly tariffs to import back to America is a punch in the gut.

This fragility was highlighted by Intel (INTC) who brought the semiconductor story back down to earth with a mild earnings beat but laid an egg with a horrid annual 2019 forecast.

Intel telegraphed that they are slashing projections for cloud revenue and server sales.

Micron (MU) acquiesced in a similar forecast calling for a cloud hardware slowdown and bloated inventory would need to be further digested creating a lack of demand in new orders.

Then the ultimate stab through the heart - the 2019 guide was $1 billion less than initially forecasted amounting to the same level of revenue in 2018 - $73 billion in revenue and zero growth to the top line.

Making matters worse, the downdraft in guidance factored in that the backend of the year has the likelihood of outperforming to meet that flat projection of the same revenue from last year offering the bear camp fodder to dump Intel shares.

How can firms convincingly promise the back half is going to buttress its year-end performance under the drudgery of a fractious geopolitical set-up?

This screams uncertainty.

Love them or crucify them, the specific makeup of the semiconductor chip cycle entails a vulnerable boom-bust cycle that is the hallmark of the chip industry.

We are trending towards the latter stage of the bust portion of the cycle with management issuing code words such as “inventory adjustment.”

Firms will need to quickly work off this excess blubber to stoke the growth cycle again and that is what this strength in chip stocks is partly about.

Investors are front-running the shaving off of the blubber and getting in at rock bottom prices.

Amalgamate the revelation that demand is relatively healthy due to the next leg up in the technology race requiring companies to hem in adequate orders of next-gen chips for 5G, data servers, IoT products, video game consoles, autonomous vehicle technology, just to name a few.

But this demand is expected to come online in the late half of 2019 if management’s wishes come true.

To minimize unpredictable volatility in this part of tech and if you want to squeeze out the extra juice in this area, then traders can play it by going long the iShares PHLX Semiconductor ETF (SOXX) or VanEck Vectors Semiconductor ETF (SMH).

In many cases, hedge funds have made their entire annual performance in the first month of January because of this v-shaped move in chip shares.

Then there is the other long-term issue of elevated execution risks to chip companies because of an overly reliant manufacturing process in China.

If this trade war turns into a several decades affair which it is appearing more likely by the day, American chip companies will require relocating to a non-adversarial country preferably a democratic stronghold that can act as the fulcrum of a global supply chain channel moving forward.

The relocation will not occur overnight but will have to take place in tranches, and the same chip companies will be on the hook for the relocation fees and resulting capex that is tied with this commitment.

That is all benign in the short term and chip stocks have a little more to run, but on a risk reward proposition, it doesn’t make sense right now to pick up pennies in front of the steamroller.

If the Nasdaq (QQQ) retests December lows because of global growth falls off a cliff, then this mini run in chips will freeze and thawing out won’t happen in a blink of an eye either.

But if you are a long-term investor, I would recommend my favorite chip stock AMD who is actively draining CPU market share from Intel and whose innovation pipeline rivals only Nvidia.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-28 01:06:352019-07-09 04:54:41Buy Dips in Semis, Not Tops

This is the most important research piece you will ever read, bar none. But you have to finish it to understand why. So, I will get on with the show.

I have been hammering away at my followers at investment conferences, webinars, and strategy luncheons this year about one recurring theme. Things are good, and about to get better, a whole lot better.

The driver will be the exploding rate of technological innovation in electronics, biotechnology, and energy. The 2020s are shaping up to be another roaring twenties, and asset prices are going to go through the roof.

To flesh out some hard numbers about growth rates that are realistically possible and which industries will be the leaders, I hooked up with my old friend, Ray Kurzweil, one of the most brilliant minds in computer science.

Ray is currently a director of Engineering at Google (GOOG) heading up a team that is developing stronger artificial intelligence. He is an MIT grad with a double major in computer science and creative writing. He was the principal inventor of the CCD flatbed scanner, first text-to-speech synthesizer, and the commercially marketed large-vocabulary speech recognition.

When he was still a teenager, Ray was personally awarded a science prize by President Lyndon Johnson. He has received 20 honorary doctorates and has authored 7 books. It was upon Ray’s shoulders that many of today’s technological miracles were built.

His most recent book, The Singularity is Near: When Humans Transcend Biology, was a New York Times bestseller. In it, he makes hundreds of predictions about the next 100 years that will make you fall out of your chair.

I met Ray at one of my favorite San Francisco restaurants, Morton’s on Sutter Street. I ordered a dozen oysters, a filet mignon wrapped in bacon, and drowned it all down with a fine bottle of Duckhorn merlot. Ray had a wedge salad with no dressing, a giant handful of nutritional supplements, and a bottle of water. That’s Ray, one cheap date.

The Future of Man

A singularity is defined as a single event that has monumental consequences. Astrophysicists refer to the big bang and black holes in this way. Ray’s singularity has humans and machines merging to become single entities, partially by 2040 and completely by 2100.

All of our thought processes will include built-in links to the cloud making humans super smart. Skin that absorbs energy from the sun will eliminate the need to eat. Nanobots will replace blood cells, which are far more efficient at moving oxygen. A revolution in biotechnology will enable us to eliminate all medical causes of death.

Most organs can now be partially or completely replaced. Eventually, they all will become renewable by taking one of your existing cells and cloning it into a completely new organ. We will become much more like machines, and machines will become more like us.

The first industrial revolution extended the reach of our bodies, and the second is extending the reach of our minds.

And, oh yes, prostitution will be legalized and move completely online. Sounds like a turn-off? How about virtually doing it with your favorite movie star? Your favorite investment advisor? Yikes!

Ironically, one of the great accelerants towards this singularity has been the war in Iraq. More than 50,000 young men and women came home missing arms and legs (in Vietnam these were all fatalities, thanks to the absence of modern carbon fiber body armor).

Generous government research budgets have delivered huge advances in titanium artificial limbs and the ability to control them only with thoughts. Quadriplegics can now hit computer keystrokes merely by thinking about them.

Kurzweil argues that exponentially growing information technology is encompassing more and more things that we care about, like healthcare and medicine. Reprogramming of biology will be the next big thing and is a crucial part of his “singularity.”

Our bodies are governed by obsolete genetic programs that evolved in a bygone era. For example, over millions of years, our bodies developed genes to store fat cells to protect against a poor hunting season in the following year. That gave us a great evolutionary advantage 10,000 years ago. But it is not so great now with obesity becoming the country’s number one health problem.

We would love to turn off these genes through reprogramming, confident that the hunting at the supermarket next year will be good. We can do this in mice now which, in experiments, can eat like crazy but never gain weight.

The happy rodents enjoy the full benefits of caloric restriction with no hint of diabetes or heart disease. A product like this would be revolutionary, not just for us, health care providers, and the government, but, ironically, for fast food restaurants as well.

Within the last five years, we have learned how to reprogram stem cells to rebuild the hearts of heart attack victims. The stem cells are harvested from skin cells, not human embryos, ducking the political and religious issue of the past.

And if we can turn off genes, why not the ones in cancer cells that enable them to pursue unlimited reproduction until they kill its host? That development would cure all cancers, and is probably only a decade off.

The Future of Computing

If this all sounds like science fiction, you’d be right. But Ray points out that humans have chronically underestimated the rate of technological innovation.

This is because humans evolved to become linear thinking animals. If a million years ago we saw a gazelle running from left to right, our brains calculated that one second later it would progress ten feet further to the right. That’s where we threw the spear. This gave us a huge advantage over other animals and is why we became the dominant species.

However, much of science, technology, and innovation grows at an exponential rate and is where we make our most egregious forecasting errors. Count to seven, and you get to seven. However, double something seven times and you get to a billion.

The history of the progress of communications is a good example of an exponential effect. The spoken language took hundreds of thousands of year to develop. Written language emerged thousands of years, books in 100 years, the telegraph in a century, and telephones 50 years later.

Some ten years after Steve Jobs brought out his Apple II personal computer, the growth of the Internet went hyperbolic. Within three years of the iPhone launch, social media exploded out of nowhere.

At the beginning of the 20th century, $1,000 bought 10 X -5th power worth of calculations per second in our primitive adding machines. A hundred years later a grand got you 10 X 8th power calculations, a 10 trillion-fold improvement. The present century will see gains many times this.

The iPhone itself is several thousand times smaller, a million times cheaper, and billions of times more powerful than computers of 40 years ago. That increases the price per performance by the trillions. More dramatic improvements will accelerate from here.

Moore’s law is another example of how fast this process works. Intel (INTC) founder Gordon Moore published a paper in 1965 predicting a doubling of the number of transistors on a printed circuit board every two years. Since electrons had shorter distances to travel, speeds would double as well.

Moore thought that theoretical limits imposed by the laws of physics would bring this doubling trend to end by 2018 when the gates become too small for the electrons to pass through. For decades, I have read research reports predicting that this immutable deadline would bring an end to innovation and technological growth, and bring an economic Armageddon.

Ray argues that nothing could be further from the truth. A paradigm shift will simply allow us to leapfrog conventional silicon-based semiconductor technologies and move on to bigger and better things. We did this when we jumped from vacuum tubes to transistors in 1949, and again in 1959 when Texas Instruments (TXN) invented the first integrated circuit.

Paradigm shifts occurred every ten years in the past century, every five years in the last decade, and will occur every couple of years in the 2020s. So fasten your seatbelts!

Nanotechnology has already allowed manufacturers to extend the 2018 Moore’s Law limit to 2022. On the drawing board are much more advanced computing technologies including calcium-based systems using the alternating direction of spinning electrons, and nanotubes.

Perhaps the most promising is DNA-based computing, a high research priority at IBM and several other major firms. I earned my own 15 minutes of fame in the scientific world 40 years ago as a member of the first team ever to sequence a piece of DNA which is why Ray knows who I am.

DeoxyriboNucleic Acid makes up the genes that contain the programming that makes us who we are. It is a fantastically efficient means of storing and transmitting information. And it is found in every single cell in our bodies, all 10 trillion of them.

The great thing about DNA is that it replicates itself. Just throw it some sugar. That eliminates the cost of building the giant $2 billion silicon-based chip fabrication plants of today.

The entire human genome is a sequential binary code containing only 800 MB information which after you eliminate redundancies, has a mere 30-100 MB of useful information, about the size of an off-the-shelf software program like Word for Windows. Unwind a single DNA molecule and it is only six feet long.

What this means is that, just when many believe that our computer power is peaking, it is in fact just launching on an era of exponential growth. Supercomputers surpassed human brain computational ability in 2012, about 10 to the 16th power (ten quadrillion) calculations per second.

That power will be available on a low-end laptop by 2020. By 2050, this prospective single laptop will have the same computing power of the entire human race, about 9 billion individuals. It will also be small enough to implant in our brains.

The Future of the Economy

Ray is not really that interested in financial markets or, for that matter, making money. Where technology will be in a half-century and how to get us there are what get his juices flowing. However, I did manage to tease a few mind-boggling thoughts from him.

At the current rate of change, the 21st century will see 200 times the technological progress that we saw in the 20th century. Shouldn’t corporate profits, and therefore share prices, rise by as much?

Technology is rapidly increasing its share of the economy and increasing its influence on other sectors. That’s why tech has been everyone’s favorite sector for the past 30 years and will remain so for the foreseeable future. For two centuries, technology has been eliminating jobs at the bottom of the economy and creating new ones at the top.

Stock analysts and investors make a fatal flaw in estimating future earnings based on the linear trends of the past, instead of the exceptional growth that will occur in the future.

In the last century, the Dow appreciated from 100 to 10,000, an increase of 100 times. If we grow at that rate in this century, the Dow should increase by 10,000% to 1 million by 2100. But so far, we are up only 6%, even though we are already 18 years into the new century.

The index is seriously lagging but will play catch up in a major way during the 2020s when economic growth jumps from 2% to 4% or more, thanks to the effects of massively accelerating technological change.

Some 100 years ago, one-third of jobs were in farming, one third were in manufacturing, and one third in services. If you predicted then that in a century farming and manufacturing would each be 3% of total employment and that something else unknown would come along for the rest of us, people would have been horrified. But that’s exactly what happened.

Solar energy use is also on an exponential path. It is now 1% of the world’s supply but is only seven doublings away from becoming 100%. Then we will consume only one 10,000th of the sunlight hitting the earth. Geothermal energy offers the same opportunities.

We are only running out of energy if you limit yourself to 19th-century methods. Energy costs will plummet. Eventually, energy will be essentially free when compared to today’s costs, further boosting corporate profits.

Hyper-growth in technology means that we will be battling with deflation for the rest of the century, as the cost of production and price of everything fall off a cliff. That makes our 10-year Treasury bonds a steal at a generous 2.60% yield, a full 460 basis points over the real long-term inflation rate of negative 2% a year.

US Treasuries could eventually trade down to the 0.40% yields seen in Japan only a couple of years ago. This means that the bull market in bonds is still in its early stages, and could continue for decades.

The upshot for all of this these technologies will rapidly eliminate poverty, not just in the US but around the world. Each industry will need to continuously reinvent its business model, or disappear.

The takeaway for investors that stocks, as well as other asset prices, are now wildly undervalued given their spectacular future earnings potential. It also makes the Dow target of 1 million by 2100 absurdly low, and off by a factor of 10 or even 100. Will we be donning our “Dow 100 Million” then?

Other Random Thoughts

As we ordered dessert, Ray launched into another stream of random thoughts. I asked for Morton’s exquisite double chocolate mousse. Ray had another handful of supplements. Yep, Mr. Cheap Date.

The number of college students has grown from 50,000 to 12 million since the 1870s. A kid in Africa with a cell phone has more access to accurate information than the president of the United States did 15 years ago.

The great superpower, the Soviet Union, was wiped out by a few fax machines distributing information in 1991.

Company offices will become entirely virtual by 2025.

Cows are very inefficient at producing meat. In the near future, cloned muscle tissue will be produced in factories, disease free, and at a fraction of the present cost without the participation of the animal. PETA will be thrilled.

Use of nanomaterials to build ultra light but ultra strong cars cuts fuel consumption dramatically. Battery efficiencies will improve by 10 to 100 times. Imagine powering Tesla Model S1 with a 10-pound battery! Advances in nanotube construction mean the weight of the vehicle will drop from the present 3 tons to just 100 pounds but will be far safer.

Ray is also on a scientific advisory panel for the US Army. Uncertain about my own security clearance, he was reluctant to go into detail. Suffice it to say that the weight of an M1 Abrams main battle tank will shrink from 70 tons to 1 ton, but will be 100 times stronger.

A zero tolerance policy towards biotechnology by the environmental movement exposes their intellectual and moral bankruptcy. Opposing a technology with so many positive benefits for humankind and the environment will inevitably alienate them from the media and the public who will see the insanity of their position.

Artificial intelligence is already far more prevalent than you understand. The advent of strong artificial intelligence will be the most significant development of this century. You can’t buy a book from Amazon, withdraw money from your bank, or book a flight without relying on AI.

Ray finished up by saying that by 2100 humans will have the choice of living in a biological, or in a totally virtual, online form. In the end, we will all just be files.

Personally, I prefer the former, as the best things in life are biological, and free!

I walked over to the valet parking, stunned and disoriented by the mother load of insight I had just obtained, and it wasn’t just the merlot talking, either! Imagine what they talk about at Google all day.

To buy The Singularity is Near at discount Amazon pricing, please click here. It is worth purchasing the book just to read Ray’s single chapter on the future of the economy.

Did You Say "BUY" or "SELL"

The Future is Closer than You Think

https://www.madhedgefundtrader.com/wp-content/uploads/2014/05/Borg.jpg343442DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2018-12-28 01:06:452018-12-27 16:45:52Peeking Into the Future with Ray Kurzweil

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

S&P Top 10 Holdings 3-4-2019

S&P Top 10 Holdings 3-4-2019

Did You Say "BUY" or "SELL"

Did You Say "BUY" or "SELL" The Future is Closer than You Think

The Future is Closer than You Think