Mad Hedge Technology Letter

December 4, 2018

Fiat Lux

Featured Trade:

(THE CHIP STOCKS HAVE BOTTOMED)

(NVDA), (AMD), (INTC)

Mad Hedge Technology Letter

December 4, 2018

Fiat Lux

Featured Trade:

(THE CHIP STOCKS HAVE BOTTOMED)

(NVDA), (AMD), (INTC)

Now that the trade war has officially been put on ice, two short-term trades to scoop up out there for the taking would be chip leaders Advanced Micro Devices (AMD) and Nvidia (NVDA).

Even though I am still bearish on the chip sector as a whole, the mini rapprochement signals a much-needed reprieve to China-sensitive stocks that have been beaten down for most of the year.

The timing is favorable now to jump into some of the avant-garde chip stocks and succinctly two companies that have captured the imagination of the global gaming revolution by constructing the critical GPUs needed to display the mouth-watering graphics that appear life-like.

They are two dominators that have cornered the GPU market and don’t apologize for it.

Even if next year fails to pinpoint a comprehensive détente, China-based supply chains will have more time to make epochal decisions to whether risk the full brunt of a future multilateral spat or mosey on over to greener pastures to insulate themselves from tariff and political fallout.

Most of American tech supply chains are in China now, but that doesn’t mean that can’t change.

Either way, ratcheting down the tone of the jawboning will help chip stocks and the GPU mainstay firms should finish out the year resolutely.

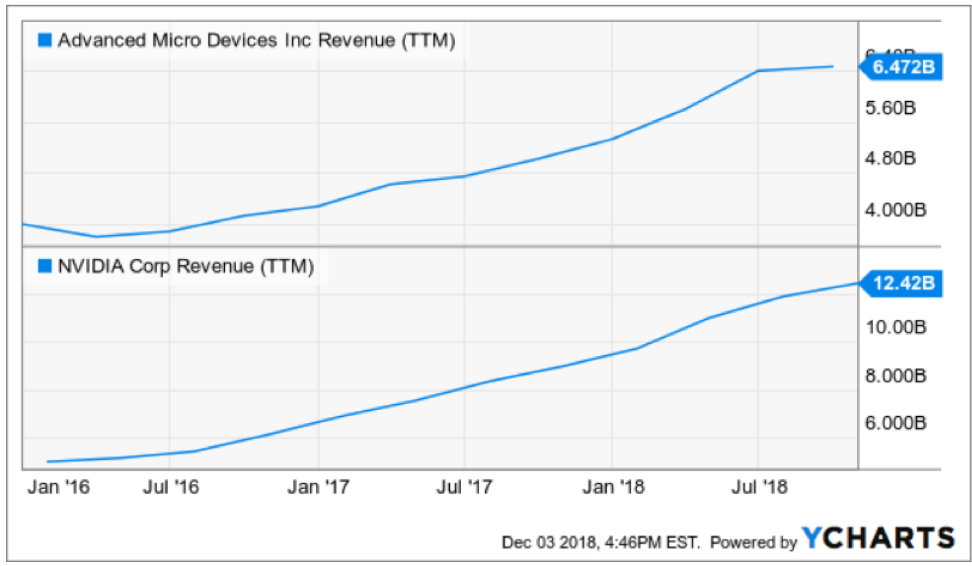

After building an abnormally high amount of inventory due to last year's bitcoin euphoria, Nvidia got ahead of itself drowning in excess GPU units with evaporating crypto mining demand from the bitcoin crash.

It was never imagined that the crypto phenomenon could incite a build-up of inventory channels to the levels that started to erode pricing, but when you consider that two companies and not one were pumping out the GPU units, they simply overdid it.

Conveniently enough, management on both sides blamed each other.

In any case, I believe the spike in inventory says more to the crash and burn of bitcoin pricing than having something to do with these two solidly run companies.

Bitcoin revenue stream only accounted for 10% of revenue at last year’s peak of crypto ecstasy.

The Mad Hedge Technology Letter has steered wide and clear of the crypto phenomenon because even though the blockchain technology is indeed intriguing, there are probably a few more crash and burn scenarios to unfold before it becomes legitimately accepted in mainstream finance.

In any effect, GPU pricing has started to turn the corner up 15% from the September lows, and for the first time since earlier in the year, inventory levels are starting to flush itself out.

The “crypto hangover” headlines roughed up shares of the duopolists but now the light is at the end of the tunnel, and combined with the ceasefire in Washington, has created a positive platform for these two favorites to trade into yearend.

The record-breaking sales volume from Black Friday and Cyber Monday is a minor boost giving credence to the inventory channels clear-up.

Jubilant shoppers were gobbling up GPUs to dish out to gamer friends and family.

At the annual Siggraph conference in Vancouver, Canada, CEO of Nvidia Jensen Huang said, “Turing is Nvidia’s most important innovation in computer graphics in more than a decade.”

The development of real-time ray tracing is the “holy grail” of the GPU industry.

The Turing products render graphics six times faster than their predecessor Pascal-based chip.

Nvidia has rolled out three new graphics cards based on this technology.

In fact, the Turing T4 Cloud GPU has been a massive success in the data center space.

Not only is gaming benefitting from these high-end chips, they can be slotted around offering a diverse set of functionalities.

Ian Buck, Vice President and General Manager of Accelerated Computing at Nvidia said, “We have never before seen such rapid adoption of a data center processor.”

Nvidia’s T4 offers the modern cloud of today the performance and efficiency needed for compute-intensive workloads at scale.

The two companies continue to manufacture top-level GPUs that the competition cannot touch.

The headwinds facing these two titans are of a temporary basis and will eventually dry up.

Both missed on earnings and the stocks sold off badly.

The one-off short-term headwinds will quickly shore up.

The lucky opportunity for investors to get into a best of breed at a cheaper price does not come around too often.

If the near-term fluctuations provide too intense, both companies are great long-term buy and hold stocks.

The bad news has been mostly baked into the pie at this point.

The reset in expectations should factor in the evolving inventory situation and the crypto headwinds.

I fully expect both companies to convincingly beat earnings on the top and bottom line next quarter.

Core gaming demand is robust and by next earnings, the companies will be back to their normal selves – systematically crushing earnings expectations.

This one-off in performance was a curveball, and AMD is a company that I am bullish on with AMD snatching away market share from Intel (INTC).

German’s large tech e-tailer Mindfactory published a survey showing AMD doubling the number of CPUs sold leaving Intel in the dust in November.

Intel’s CPU sales are nosediving quickly because of AMD’s innovative designs and reliable production performance.

Intel has essentially gifted a huge swath of the CPU market to AMD, and AMD has embraced the change and is running with it.

I expect AMD to turn the screws next year on Intel and hoover up more of the CPU market.

Add in that 50% of AMD’s revenue comes from newly launched products and then you can start to cook up why these companies are ahead of the game.

They concoct best in show products leverage with groundbreaking technology and scale up these state-of-the-art offerings to the strongest segments of the chip industry and presto!

You have a magical recipe of success.

At the Mad Hedge Lake Tahoe Conference at the end of October, AMD plummeted to around $17 and I convincingly proclaimed this stock a buy without hesitation.

The stock is up over 25% since then to almost $24, and I believe this stock is in it for the long haul.

Mad Hedge Technology Letter

November 21, 2018

Fiat Lux

Featured Trade:

(FIVE TECH STOCKS TO SELL SHORT ON THE NEXT RALLY)

(WDC), (SNAP), (STX), (APRN), (AMZN), (KR), (WMT), (MSFT), (ATVI), (GME), (TTWO), (EA), (INTC), (AMD), (FB), (BBY), (COST), (MU)

Next year is poised to be a trading year that will bring tech investors an added dimension with the inclusion of Uber and Lyft to the public markets.

It seemed that everything that could have happened in 2018 happened.

Now, it’s time to bring you five companies that I believe could face a weak 2019.

Every rally should be met with a fresh wave of selling and one of these companies even has a good chance of not being around in 2020.

Western Digital (WDC)

I have been bearish on this company from the beginning of the Mad Hedge Technology Letter and this legacy firm is littered with numerous problems.

Western Digital’s structural story is broken at best.

They are in the business of selling hard disk drive products.

These products store data and have been around for a long time. Sure the technology has gotten better, but that does not mean the technology is more useful now.

The underlying issue with their business model is that companies are moving data and operations into cloud-based products like the Microsoft (MSFT) Azure and Amazon Web Services.

Why need a bulky hard drive to store stuff on when a cloud seamlessly connects with all devices and offers access to add-on tools that can boost efficiency and performance?

It’s a no-brainer for most companies and the efficiency effects are ratcheted up for large companies that can cohesively marry up all branches of the company onto one cloud system.

Even worse, (WDC) also manufactures the NAND chips that are placed in the hard drives.

NAND prices have faltered dropping 15% of late. NAND is like the ugly stepsister of DRAM whose large margins and higher demand insulate DRAM players who are dominated by Micron (MU), Samsung, and SK Hynix.

EPS is decelerating at a faster speed and quarterly sales revenue has plateaued.

Add this all up and you can understand why shares have halved this year and this was mainly a positive year for tech shares.

If there is a downtown next year in the broader market, watch out below as this company is first on the chopping block as well as its competitor Seagate Technology (STX).

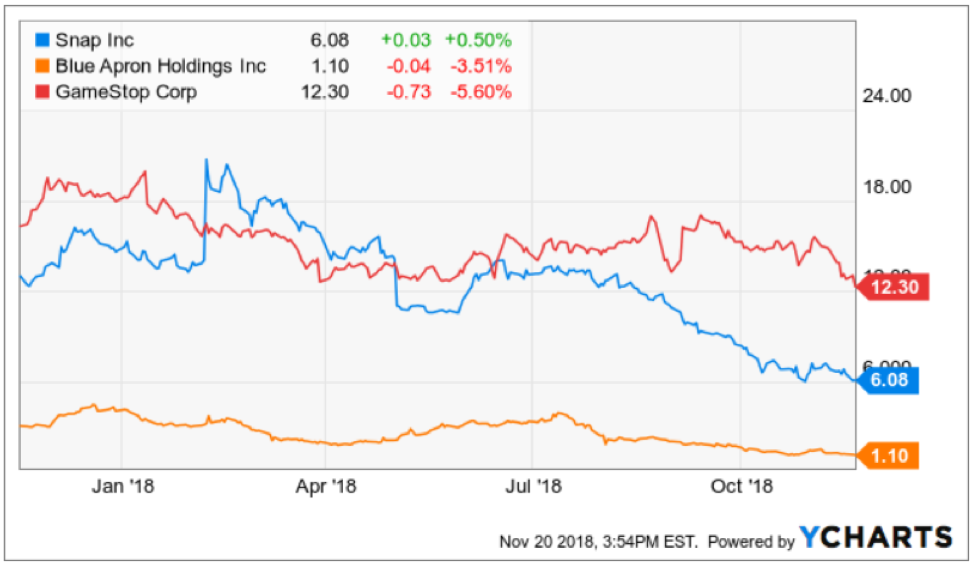

Snapchat (SNAP)

This company must be the tech king of terrible business models out there.

Snapchat is part of an industry the whole western world is attempting to burn down.

Social media has gone for cute and lovable to destroy at all cost. The murky data-collecting antics social media companies deploy have regulators eyeing these companies daily.

More successful and profitable firm Facebook (FB) completely misunderstood the seriousness of regulation by pigeonholing it as a public relation slip-up instead of a full-blown crisis threatening American democracy.

Snapchat is presiding over falling daily active user growth at such an early stage that usership doesn’t even pass 100 million DAUs.

Management also alienated the core user base of adolescent-aged users by botching the redesign that resulted in users bailing out of Snapchat.

Snapchat has been losing high-level executives in spades and fired a good chunk of their software development team tagging them as the scapegoat that messed up the redesign.

Even more imminent, Snapchat is burning cash and could face a cash crunch in the middle of next year.

They just announced a new spectacle product placing two frontal cameras on the glass frame. Smells like desperation and that is because this company needs a miracle to turn things around.

If they hit the lottery, Snap could have an uptick in its prospects.

GameStop (GME)

This part of technology is hot, benefiting from a generational shift to playing video games.

Video games are now seen as a full-blown cash cow industry attracting gaming leagues where professional players taking in annual salaries of over $1 million.

Gaming is not going away but the method of which gaming is consumed is changing.

Gamers no longer venture out to the typical suburban mall to visit the local video games store.

The mushrooming of broad-band accessibility has migrated all games to direct downloads from the game manufacturers or gaming consoles’ official site.

The middleman has effectively been cut out.

That middleman is GameStop who will need to reinvent itself from a video game broker to something that can accrue real value in the video game world.

The long-term story is still intact for gaming manufactures of Activision (ATVI), EA Sports (EA), and Take-Two Interactive (TTWO).

The trio produces the highest quality American video games and has a broad portfolio of games that your kids know about.

GameStop’s annual revenue has been stagnant for the past four years.

It seems GameStop can’t find a way to boost its $9 billion of annual revenue and have been stuck on this number since 2015.

If you do wish to compare GameStop to a competitor, then they are up against Best Buy (BBY) which is a better and more efficiently run company.

Then if you have a yearning to buy video games from Best Buy, then you should ask yourself, why not just buy it from Amazon with 2-day free shipping as a prime member.

The silver lining of this business is that they have a nice niche collectibles division that hopes to deliver over $1 billion in annual sales next year growing at a 25% YOY clip.

But investors need to remember that this is mainly a trade-in used video game company.

Ultimately, the future looks bleak for GameStop in an era where the middleman has a direct path to the graveyard, and they have failed to digitize in an industry where digitization is at the forefront.

Blue Apron

This might be the company that is in most trouble on the list.

Active customers have fallen off a cliff declining by 25% so far in 2018.

Its third quarter earnings were nothing short of dreadful with revenue cratering 28% YOY to $150.6 million, missing estimates by $7 million.

The core business is disappearing like a Houdini act.

Revenue has been decelerating and the shrinking customer base is making the scope of the problem worse for management.

At first, Blue Apron basked in the glory of a first mover advantage and business was operating briskly.

But the lack of barriers to entry really hit the company between the eyes when Amazon (AMZN), Walmart (WMT), and Kroger (KR) rolled out their own version of the innovative meal kit.

Blue Apron recently announced it would lay off 4% of its workforce and its collaboration with big-box retailer Costco (COST) has been shelved indefinitely before the holiday season.

CFO of Blue Apron Tim Bensley forecasts that customers will continue to drop like flies in 2019.

The company has chosen to focus on higher-spending customers, meaning their total addressable market has been slashed and 2019 is shaping up to be a huge loss-making year for the company.

The change, in fact, has flustered investors and is a great explanation of why this stock is trading at $1.

The silver lining is that this stock can hardly trade any lower, but they have a mountain to climb along with strategic imperatives that must be immediately addressed as they descend into an existential crisis.

Intel (INTC)

This company is the best of the five so I am saving it for last.

Intel has fallen behind unable to keep up with upstart Advanced Micro Devices (AMD) led by stellar CEO Dr. Lisa Su.

Advanced Micro Devices is planning to launch a 7-nanometer CPU in the summer while Intel plans to roll out its next-generation 10-nanometer CPUs in early 2020.

The gulf is widening between the two with Advanced Micro Devices with the better technology.

As the new year inches closer, Intel will have a tough time beating last year's comps, and investors will need to reset expectations.

This year has really been a story of missteps for the chip titan.

Intel dealt with the specter security vulnerability that gave hackers access to private data but later fixed it.

Executive management problems haven’t helped at all.

Former CEO of Intel Brian Krzanich was fired soon after having an inappropriate relationship with an employee.

The company has been mired in R&D delays and engineering problems.

Dragging its feet could cause nightmares for its chip development for the long haul as they have lost significant market share to Advanced Micro Devices.

Then there is the general overhang of the trade war and Intel is one of the biggest earners on mainland China.

The tariff risk could hit the stock hard if the two sides get nasty with each other.

Then consider the chip sector is headed for a cyclical downturn which could dent the demand for Intel chip products.

The risks to this stock are endless and even though Intel registered a good earnings report last out, 2019 is set up with landmines galore.

If this stock treads water in 2019, I would call that a victory.

Mad Hedge Technology Letter

September 24, 2018

Fiat Lux

Featured Trade:

(BAD NEWS FROM MICRON TECHNOLOGY (MU),

(MU), (BABA), (KLAC), (LRCX), (INTC), (AMD), (NVDA), (HPQ)

If your stomach was on edge before, then you must feel quite queasy now.

That’s only if you didn’t get rid of your chip stocks when I told you to.

The chip sector has been rife with issues for quite some time now, and I’ve been firing off bearish chip stories the past few months.

Intel (INTC) was one of the last chip companies I told you to avoid like the plague, please click here to review that story.

The contagion has spread wider.

Micron (MU), the Boise, Idaho-based chip giant, delivered poor guidance from its latest earnings report, adding more carnage to this trouble sector.

It’s been rough sailing for many American-based chip companies lately that are not named Advanced Micro Devices (AMD) and Nvidia (NVDA).

The protracted ongoing trade war between America and China that sees no end in sight is the fundamental reason to stay away from these chip companies that are the meat and potatoes inside of all electronic devices.

Cofounder of Alibaba (BABA) Jack Ma, who recently stepped down from his position as chairman, told news outlets that this trade war could last “20 years” and is “going to be a mess.”

Micron is affected by this trade war more than any other American company, with half of its annual revenue derived from the Middle Kingdom.

Out of the $20.32 billion in annual revenue last year, more than $10 billion was from China alone.

Micron is a leader in selling DRAM chips, which are placed in most portable electronic devices such as smartphones, video game consoles, and laptop computers.

The commentary coming out from chip executives has been overly negative and spells doom and gloom - supporting my view to be cautious on chips through the end of the year.

At the Citi 2018 Global Technology Conference in New York, KLA-Tencor (KLAC) chief financial officer Bren Higgins characterized the winter season DRAM market as “little less than what we thought,” describing margins as “modestly weaker.”

Lam Research (LRCX), once one of my favorite chip plays, offered bearish rhetoric about the state of chip investments, saying on its earnings call that is expected “lower spending on new equipment by some of its memory customers.”

It doesn’t take a rocket scientist to know that “memory customer” is Intel, which is in the throes of a CPU chip shortage rocking the overall personal computer market.

Personal computers face a steep 7% drop in sales volume for the rest of the year, and the knock-on effect is rippling throughout the industry.

The lower volume of produced computers means less memory needed, adding up to less sales for Micron.

This rationale forced Micron to guide down its revenue growth from 22% to 16% for the last quarter of 2018.

Intel’s monumental lapse has offered a golden opportunity for competitor Advanced Micro Devices (AMD) to steal market share from Intel in broad daylight.

This was the exact thesis that provoked me to urge readers to pile into AMD shares like a Tokyo rush-hour subway car.

Shares have gone ballistic to say the least.

(AMD) is poised to seize and reposition itself in the global CPU market with a 70/30 market share, up from the paltry 90/10 market share before Intel’s debacle.

To make matters worse for Intel, widespread reports indicate its shortage problems are “worsening.”

Such is a dog-eat-dog world out there when a company can triple market share in a blink of an eye.

The rotation is real with HP (HPQ) planning to integrate AMD chips into 30% of its consumer PCs, and Dell already mentioning it will use AMD chips to make up for the shortages.

The resilience in chip demand remains the silver lining for this industry as price weakness and production shortages will be finite.

Server demand remains particularly robust.

Google, Amazon, Facebook, and Microsoft coughed up $34.7 billion on data centers to serve cloud-based operation in the first half of the year in 2018, a sharp increase of 59% YOY.

Investors have been paranoid of the boom-bust nature of the chip industry for decades.

Each cycle sees spending and chip pricing rocket, only for inventories to build up and demand to evaporate in an instant.

The beginning of the end always starts with lower guidance, followed up with missed earnings the next quarter.

This playbook has repeated itself over and over.

Micron guided first quarter revenue of 2019 in a range between $7.9 billion to $8.3 billion, lower than the consensus of $8.45 billion.

And, if all of this horrid chip news wasn’t reason to rip your hair out - here is the bombshell.

To wean itself off the reliance of American chips, Alibaba has created a subsidiary to produce its own chips called Pingtouge Semiconductor Company.

Pingtouge refers to honey badger in the Chinese language, symbolic for its tenacity in the face of adversity – perhaps a thinly-veiled dig at the American political system.

Former Chairman Ma pocketed this chip company Hangzhou C-SKY Microsystems last year. It will will be given ample leeway and resources to team up with Alibaba to roll out its first commercial chip next year.

Alibaba has rapidly grown into the third-largest cloud player in the world, and require an abundant source of chips moving forward.

Chips tricked out with artificial intelligence will be adopted by not only its data centers, but integrated with its autonomous driving technology and IoT products, which are markets that Alibaba is proud to be part.

You can find Alibaba’s cloud products present in more than 20 countries. And the company that Jack Ma built forecasts to generate more than 50% of its revenue from overseas markets soon.

It could be Jack Ma laughing all the way to the bank.

Ultimately, Micron produced fair results last quarter, but like Facebook found out, if investors believe the company is about to fall off a cliff, it offers little resistance to the share price on a short-term basis.

Could the cyclicality demons start to awake to drag this company down?

Partially, yes, but there are still many positives to take away from this leading chip company.

China will need years to remedy its addiction of American chips.

It will not be able to produce the scope of quality or quantity to just stop buying from American companies for the foreseeable future.

The authorized $10 billion share buyback gave Micron shares a nice lift earlier this year, but the industry dynamics are now deteriorating rapidly.

Chip sentiment is at its lowest ebb for some time, and I reaffirm my call to avoid this sector completely unless it’s the two cornerstone chip companies showing systematic resiliency - (AMD) or Nvidia (NVDA).

The administration initially slapped on a tariff rate of 10% on $200 billion worth of goods with intentions to scale it up.

If nothing is solved, the increase to 25% will cause another 5% to 10% drop in Micron and Intel.

Then if the administration plans to go after the rest of the $250 billion of Chinese imports, expect another dive in chip shares.

Either way, each jawboning tweet as we head deeper into this trade conflict will damage Micron’s shares.

This sector is getting squeezed from many sides now, and if you don’t go outright short chip companies, then stay away until the storm clouds pass over and you can reassess the situation.

Mad Hedge Technology Letter

September 19, 2018

Fiat Lux

Featured Trade:

(IBM’S SELF DESTRUCT),

(IBM), (BIDU), (BABA), (AAPL), (INTC), (AMD), (AMZN), (MSFT), (ORCL)

International Business Machines Corporation (IBM) shares do not need the squeeze of a contentious trade war to dent its share price.

It is doing it all by itself.

Stories have been rife over the past few years of shrinking revenue in China.

And that was during the golden years of China when American tech ran riot on the mainland before the dynamic rise of Baidu (BIDU), Alibaba (BABA), and Tencent, otherwise known as the BATs.

Then the Oracle of Omaha Warren Buffett drove a stake through the heart of IBM shares earlier this year by announcing he was fed up with the company’s direction and dumped a 35-year position.

Buffett unloaded all of his shares in favor of putting down an additional 75 million shares in Apple (AAPL) in the first quarter of 2018.

Topping off his Apple position now sees Buffett owning a mammoth 165.3 million total shares in the resurgent tech company.

Buffett’s shrewd decision has been rewarded, and Apple’s stock has rocketed more than 20% since he jovially declared his purchase in May.

IBM has been a rare misstep for Buffett, who took a moderate loss on his IBM position disclosing an average cost basis of $170 on 64 million shares that Berkshire bought in 2011.

IBM has flatlined since that Buffett interview, and slid around 25% since its peak in mid-2014.

IBM is grappling with the same conundrum most legacy companies deal with – top line contraction.

In 2014, IBM registered a tad under $93 billion in annual revenue, and followed up the next three years with even lower revenue.

A horrible recipe for success to say the least.

In an era of turbo-charged tech companies whose value now comprise over a quarter of the S&P, IBM has really fluffed its lines.

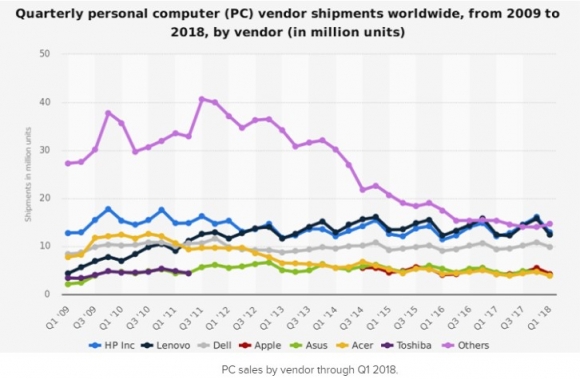

IBM’s prospects have been stapled to the PC market for years.

A recent JP Morgan note revealed the PC market could contract by 5% to 7% in the fourth quarter because of CPU shortages from Intel (INTC).

The report’s timing couldn’t have been worse for IBM.

The PC industry has been tanking for the past six consecutive years unable to shirk shrinking volume.

Intel is another company I have been lukewarm on lately because it is being outmaneuvered by chip competitor Advanced Micro Devices (AMD).

Even worse, this year has been a bad one for Intel’s management, which saw former CEO Brian Krzanich resign for sleeping with a coworker.

The poor management has had a spillover effect with Intel needing to delay new product launches as well.

To read more about my timely recommendation to pile into AMD in mid-August at $19, please click here.

Meanwhile, AMD shares have gone parabolic and surpassed an intraday price of $34 recently.

Investors should ask themselves, why invest in IBM when there are so many other tech companies that are growing, and growing revenue by 20% or more per year?

If IBM does manage to eke out top line growth in 2018, it will be by 1% to 2%, similar to Oracle’s recent performance.

Unsurprisingly, the price action of Oracle (ORCL) for the past year has been flatter than a bicycle ride around Beijing.

Live by the sword and die by the sword.

Thus, the Mad Hedge Technology Letter has been ushering readers into high-performance stocks that will bring technological and societal changes.

If you put a gun to my head and forced me to give sage investment advice, then the answer would be straightforward.

Buy Amazon (AMZN) and Microsoft (MSFT) on the dip and every dip.

This is a way to print money as if you had a rich uncle writing you checks every month.

Legacy tech is another story.

The IBMs and the Oracles of the world are bringing up the tech sector’s rear.

To add insult to injury, the lion’s share of IBM’s revenue is carved out from abroad, and the recent surge in the dollar is not doing IBM any favors.

IBM’s Watson initiative was billed as the savior for Big Blue.

The artificial intelligence initiative would integrate health care data into an actionable app.

The expectations were high hoping this division would drag up IBM from its long period of malaise.

IBM bet big on this division ploughing more than $15 billion into it from 2010-2015, predicting this would be the beginning of a new renaissance for the historic American company.

This game changing move fell on deaf ears and has been a massive bust.

IBM swallowed up three companies to ramp up this shift into the AI world - Phytel, Explorys, and Truven.

The treasure trove of health care data and proprietary analytics systems these companies came with were what this division needed to turn the corner.

These three companies were strong before the buy out and engineers were upbeat hoping Watson would elevate these companies to another level.

Wistfully, IBM Management led by CEO Ginni Rometty grossly mishandled Watson’s execution.

Phytel boasted 160 engineers at the time of IBM’s purchase and confusingly slashed half the workforce earlier this year.

Engineers at the firm even lamented that now, even smaller firms were “eating them alive.”

Unimpressed with the direction of the artificial intelligence division at IBM, many of these three companies’ best and brightest engineers jumped ship.

The inability for IBM to integrate Watson reared its ugly head in plain daylight when MD Anderson Cancer Center in Texas halted its Watson project after draining $62 million.

This was one of many errors that Watson AI accrued.

The failure to quicken clinical decision-making to match patients to clinical trials was an example of how futile IBM had become.

In short, a spectacular breakdown in execution mixed with an abrupt brain drain of AI engineers quickly imploded the prospect of Watson ever succeeding.

In 2013, IBM confidently boasted that Watson would be its “first killer app” in health care.

Internal leaks shined a brighter light on IBM’s subpar management skills.

One engineer described IBM’s management as having “no idea” what they were doing.

Another engineer said they were uncertain of a “road map” and “pivoted many times.”

Phytel, an industry leader at the time focusing on population health management, was bleeding money.

The engineers explained further, chiming in that IBM’s management had zero technical experience that led management wanting to create products that were “simply impossible.”

Not only were these products impossible, but they in no way took advantage of the resources these three companies had at their disposal.

Do you still want to invest in IBM?

Fast forward to today.

IBM is being sued in federal court with the plaintiff’s, former employees at the firm, claiming the company unfairly discriminated against elderly employees, firing them because of their age.

The documents submitted by the plaintiff’s state that “IBM has laid off 20,000 employees who were over the age of 40” since 2012.

This prototypical legacy company has more problems than the eye can see in every nook and cranny of the company.

If you have IBM shares now, dump them as soon as you can and run for cover.

It’s a miracle that IBM shares have eked out a paltry gain this year. And this thesis is constant with one of my overarching themes – stay away from all legacy tech firms with no cutting-edge proprietary technologies and stagnating growth.

________________________________________________________________________________________________

Quote of the Day

“Some say Google is God. Others say Google is Satan. But if they think Google is too powerful, remember that with search engines unlike other companies, all it takes is a single click to go to another search engine,” said Alphabet cofounder Sergey Brin.

Global Market Comments

August 23, 2018

Fiat Lux

Featured Trade:

(WHY THE DOW IS GOING TO 120,000),

(X), (IBM), (GM), (MSFT), (INTC), (DELL),

($INDU), (NFLX), (AMZN), (AAPL), (GOOGL),

(THE MAD HEDGE CONCIERGE SERVICE HAS AN OPENING),

(TESTIMONIAL)

For years, I have been predicting that a new Golden Age was setting up for America, a repeat of the Roaring Twenties. The response I received was that I was a permabull, a nut job, or a conman simply trying to sell more newsletters.

Now some strategists are finally starting to agree with me. They too are recognizing that a ganging up of three generations of investment preferences will combine to drive markets higher during the 2020s, much higher.

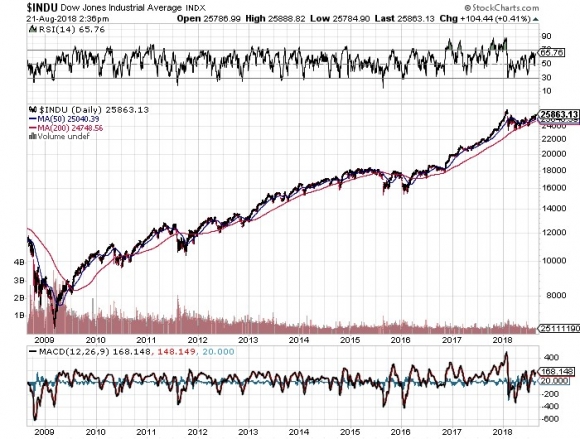

How high are we talking? How about a Dow Average of 120,000 by 2030, up another 465% from here? That is a 20-fold gain from the March 2009 bottom.

It’s all about demographics, which are creating an epic structural shortage of stocks. I’m talking about the 80 million Baby Boomers, 65 million from Generation X, and now 85 million Millennials. Add the three generations together and you end up with a staggering 230 million investors chasing stocks, the most in history, perhaps by a factor of two.

Oh, and by the way, the number of shares out there to buy is actually shrinking, thanks to a record $1 trillion in corporate stock buybacks.

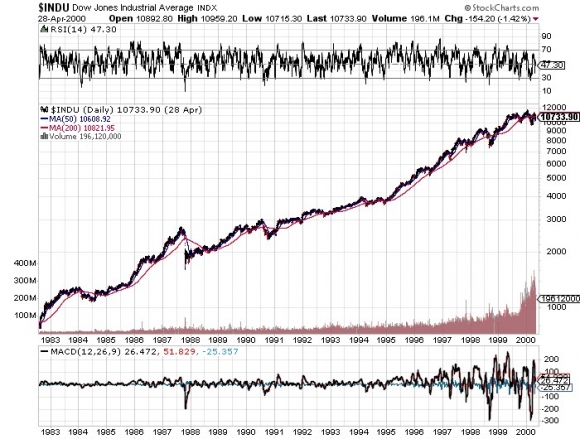

I’m not talking pie in the sky stuff here. Such ballistic moves have happened many times in history. And I am not talking about the 17th century tulip bubble. They have happened in my lifetime. From August 1982 until April 2000 the Dow Average rose, you guessed it, exactly 20 times, from 600 to 12,000, when the Dotcom bubble popped.

What have the Millennials been buying? I know many, like my kids, their friends, and the many new Millennials who have recently been subscribing to the Diary of a Mad Hedge Fund Trader. Yes, it seems you can learn new tricks from an old dog. But they are a different kind of investor.

Like all of us, they buy companies they know, work for, and are comfortable with. During my Dad’s generation that meant loading your portfolio with U.S. Steel (X), IBM (IBM), and General Motors (GM).

For my generation that meant buying Microsoft (MSFT), Intel (INTC), and Dell Computer (DELL).

For Millennials that means focusing on Netflix (NFLX), Amazon (AMZN), Apple (AAPL), and Alphabet (GOOGL).

That’s why these four stocks account for some 40% of this year’s 7% gain. Oh yes, and they bought a few Bitcoin along the way too, to their eternal grief.

There is one catch to this hyper-bullish scenario. Somewhere on the way to the next market apex at Dow 120,000 in 2030 we need to squeeze in a recession. That is increasingly becoming a topic of market discussion.

The consensus now is that an impending inverted yield curve will force a recession sometime between August 2019 to August 2020. Throwing fat on the fire will be a one-time only tax break and deficit spending that burns out sometime in 2019. These will be a major factor in U.S. corporate earnings growth dramatically slowing down from 26% today to 5% next year.

Bear markets in stocks historically precede recessions by an average of seven months so that puts the next peak in top prices taking place between February 2019 to February 2020.

When I get a better read on precise dates and market levels, you’ll be the first to know.

To read my full research piece on the topic please click here to read “Get Ready for the Coming Golden Age.”