Mad Hedge Biotech and Healthcare Letter

November 21, 2024

Fiat Lux

Featured Trade:

(TRACE ELEMENTS)

(SNY), (MTZPY), (BIIB), (IONS), (AMLX)

Mad Hedge Biotech and Healthcare Letter

November 21, 2024

Fiat Lux

Featured Trade:

(TRACE ELEMENTS)

(SNY), (MTZPY), (BIIB), (IONS), (AMLX)

In a corner office somewhere in Cambridge, Massachusetts, a team of scientists is attempting something that sounds like it belongs in a sci-fi novel: they're trying to reprogram the genetic instructions that tell our neurons how to behave.

If they succeed, they might help 97% of people with ALS keep their neurons from self-destructing.

Welcome to Trace Neuroscience, where $101 million in venture capital is betting on what amounts to a molecular spell-check for your nervous system.

You might be wondering, as I did, how one starts a company with the audacious goal of tackling one of medicine's most notorious puzzle boxes.

The answer, it turns out, involves three scientists, working in three different labs, who all stumbled upon the same cellular culprit – a protein called UNC13A - the sort of name that makes you wonder if scientists moonlight as license plate generators.

But to understand why UNC13A has everyone buzzing, we need to talk about ALS itself.

ALS, if you're not familiar with it, is the kind of disease that keeps neurologists up at night. Every year, it claims about 5,000 new victims in the US alone, and we still don't know what causes 90% of cases.

Here's a simple way to envision it – think of your nervous system as a complex metropolitan subway system.

ALS is like having someone systematically shut down every station, one by one, until the entire network grinds to a halt. Despite decades of research and millions in funding, we're still mostly watching helplessly as stations go dark.

Sure, the global market for ALS treatments reached $667.3 million in 2023, but that impressive-sounding number masks an uncomfortable truth: we're still barely keeping the lights on, let alone fixing the underlying problem.

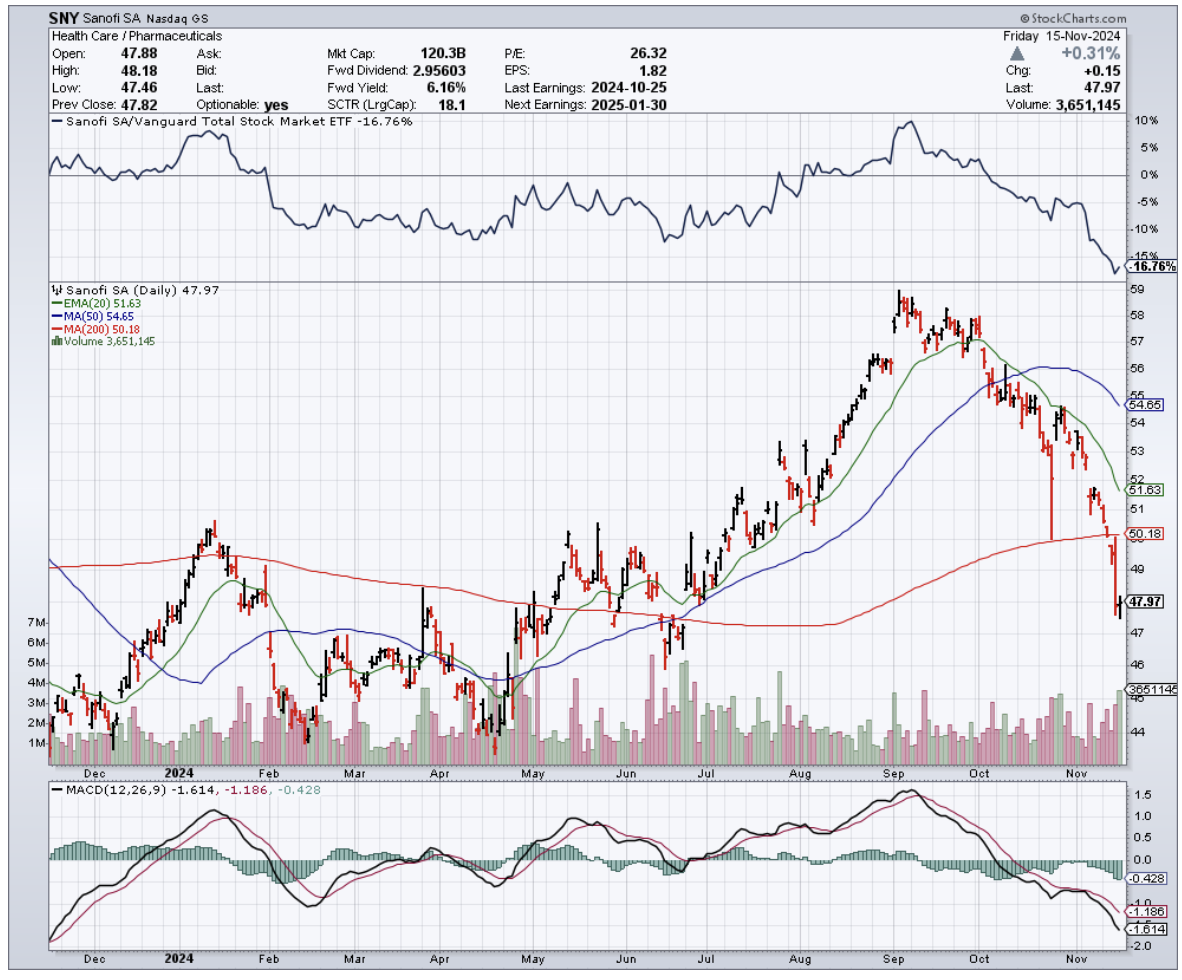

The current FDA-approved medications, Sanofi’s (SNY) Riluzole and Mitsubishi Tanabe Pharma’s (MTZPY) Edaravone (marketed as Radicava), are like trying to stop a flood with a handful of sandbags. They might slow things down a bit, but they're not exactly what you'd call a solution.

So how do you tackle a troublemaker like UNC13A? Enter Trace Neuroscience's bold approach: antisense oligonucleotides, or ASOs for those who don't enjoy tongue twisters.

Think of ASOs as tiny molecular scissors that can edit the body's protein-making instructions with surprising precision - in this case, they're specifically designed to fix how UNC13A behaves when it goes rogue.

The science behind this approach comes from a rather serendipitous confluence of research.

Aaron Gitler at Stanford, Pietro Fratta at University College London, and Michael Ward at the NIH – three scientists who probably should have just gotten a group chat going – independently discovered how certain RNA-processing molecules go haywire in ALS patients.

It's like they each found a different piece of the same puzzle, and when they put them together, the picture suddenly made sense.

And where there's breakthrough science in biotech, money usually follows.

In November 2024, Trace managed to convince some of the biggest names in venture capital – Third Rock Ventures, Atlas Venture, GV (formerly Google Ventures), and RA Capital Management – to part with $101 million.

That's quite a vote of confidence for a company whose main product is still theoretical.

The timing couldn't be more interesting. The ALS treatment market is expected to grow at a rather specific 5.8% per year until 2030, reaching about $1.1 billion.

But in this field, even the success stories come with asterisks.

Take Biogen's (BIIB) Qalsody, which got FDA-approved in May 2024 despite not actually meeting its main trial goals.

It's a rare win in a field where the scoreboard has been mostly zeros, as the rest of the ALS treatment landscape makes painfully clear.

Ionis Pharmaceuticals (IONS) had to shut down their ALS program with Biogen in May 2024, and Amylyx Pharmaceuticals (AMLX) faced the bitter task of pulling their drug Relyvrio from the market in April 2024, laying off 70% of their staff in the process.

These setbacks illuminate an uncomfortable truth about ALS drug development: the path from lab bench to pharmacy shelf is paved with perfectly logical theories that simply didn't work in real bodies.

The math is brutal - only 6.2% of neurological drugs survive the journey from Phase I to approval. Trace's response to these odds? Assemble a team that's seen enough clinical trial failures to know how to (hopefully) avoid them.

Their CEO, Eric Green, M.D., Ph.D., leads a squad that includes Chief Medical Officer Irina Antonijevic and Chief Operating Officer Megan Baierlein.

They're aiming to start clinical trials by early 2026, which in drug development terms is practically tomorrow.

For investors, timing like this transforms Trace from a scientific curiosity into a near-term catalyst.

Their approach - anchored in genetic evidence and measurable biomarkers - stands out in a field where most companies are still shooting in the dark with better bullets.

The story of Trace Neuroscience reads like molecular medicine's version of going from medieval star-gazing to GPS navigation.

While traditional ALS treatments chase symptoms, Trace is tracking proteins with the precision of an atomic clock.

They've transformed one of medicine's most frustrating puzzles into something remarkably concrete: either their molecular markers will move, or they won't.

In the biotech world, that kind of clarity is worth watching.

Mad Hedge Biotech and Healthcare Letter

April 4, 2024

Fiat Lux

Featured Trade:

(A HIGH RISK, HIGH REWARD BIOTECH)

(VYGR), (SNY), (ABBV), (NBIX), (NVS), (AZN), (SGMO), (BIIB), (RHHBY), (IONS)

Voyager Therapeutics (VYGR) has put investors through the wringer. Since going public in 2015, their chips have swung wildly, from a high-rolling $30 down to a "you've got to be kidding me" $2.50. Why? Well, their early bet on curing neurological diseases hit some snags.

But, things seem to be turning around for them these days. Word on the street is Voyager's new Alzheimer's drug could be a total game-changer. If those clinical trials get the FDA's blessing, their stock could skyrocket from its current $9.30 to $22 a share.

Before anything else, let's take a stroll down memory lane.

Voyager started out with big dreams – using fancy gene therapies to tackle tough brain diseases like Parkinson's and Huntington's. Sadly, those early programs didn't quite deliver.

But hey, they caught the eye of some big pharma players. Sanofi (SNY) came knocking with a sweet deal – $100 million upfront and promises of up to $745 million if things worked out. Unfortunately, the science wasn't cooperating, and Sanofi bailed in 2019. Ouch.

Not to be discouraged, Voyager hooked another giant, AbbVie (ABBV), with a $1.2 billion deal for Alzheimer's and Parkinson's drugs. But then, more bad luck – their Parkinson's drug stumbled, and their Huntington's disease trials got put on hold. So, AbbVie decided to cut their losses in 2020. Double ouch.

And while the pandemic may have cured our boredom, it killed investor patience with unproven biotechs. Voyager's stock price cratered, leaving them worth about as much as a used napkin – barely more than their own $500 million cash pile.

But Voyager, bless their stubborn hearts, refused to become a biotech graveyard.

Despite having zero products actually making money, they have a secret weapon: their TRACER capsid tech. Think of it as a tiny Trojan Horse that can sneak drugs past that blood-brain barrier and deliver them directly to their target. Pretty impressive, right?

This tech, along with Voyager's brainpower, caught the eye of some pharma giants.

We're talking big names like Neurocrine Biosciences (NBIX), Novartis (NVS), AstraZeneca (AZN), and Sangamo (SGMO). If everything goes according to plan, these partnerships could be worth a whopping $8 billion. Now that's what I call a vote of confidence — or maybe just a collective case of gambling fever.

For Voyager, however, its biggest gamble is on Alzheimer's – and they're going all-in. Their star player is an antibody that tackles those nasty tau tangles that mess up brain cells.

Here’s a bit of context to understand why treatments for this are crucial.

Tau is like the scaffolding inside your neurons, keeping everything organized. But in Alzheimer's, that tau goes rogue, clumping into nasty tangles. Think of it like a giant hairball clogging up the brain's communication system. These tangles are called neurofibrillary tangles (NFTs) if you want to sound super smart.

This is something that Big Pharma like Biogen (BIIB), AbbVie, and Roche (RHHBY) are trying to target, too. But Voyager claims theirs is a precision weapon, zeroing in on just the bad stuff. If clinical trials prove that, their drug could blow the competition out of the water.

Plus, Voyager's got another trick up their sleeve: a gene therapy that hits the “off” switch on those tau tangles. They've shown it works in animals, and Biogen and Ionis (IONS) are already testing something similar in humans. But Voyager's got the edge – theirs is a one-time shot, so no more of those painful spinal taps.

That’s not all. Voyager is also tinkering with these new virus capsules that can sneak gene therapies straight into brain cells. And get this – they're even working on ways to ditch the viruses altogether and target nerves directly. Pretty cutting-edge stuff.

So, is Voyager a surefire win? Heck no.

Let's be realistic. It's going to be a while before Voyager actually makes money from these drugs. But there'll be exciting news along the way—science proving their ideas work.

Remember, the tricky thing with gene therapies is that everyone's chasing the same dream: how to get these treatments where they need to go quickly, cheaply, and safely. It's tough to predict who'll crack the code, even for the experts.

What's noteworthy about Voyager is that they keep reeling in those big pharma partners. Sure, the first two deals fizzled out, but not before Voyager pocketed a ton of cash. That kept them afloat, and now their stock's not such a dumpster fire.

But, let’s face it. Voyager's track record isn't exactly a parade of victories. Progress has been slow, and that's just the way it is in this industry.

If they pull off a miracle cure, they'll be worth billions, maybe tens of billions. Remember when Intellia Therapeutics (INTL) hit that $10 billion mark? That's the kind of payoff we're talkin' about.

Still, Voyager needs to deliver some serious wins, or those partners will vanish again. However, it’s worth considering that when a big player like Novartis, who knows this gene therapy game, partners up... that's gotta mean something, right? Even without results from human trials, it's a sign Voyager might be onto something big.

I know it's hard to justify investing in small biotechs with a losing streak, especially when they're tackling the toughest diseases out there. But after digging into Voyager, I can see its potential.

Worst case scenario? Their drugs flop. But that can happen to any biotech, even those with huge valuations and decades of trying.

As for Voyager, this biotech has been around the block. They've clearly got some promising science, and their stock is cheap. For me, that's enough to take a small position and see what happens.

Mad Hedge Biotech and Healthcare Letter

September 22, 2022

Fiat Lux

Featured Trade:

(GOOD THINGS COME TO THOSE WHO WAIT)

(NTLA), (IONS), (TAK), (CRSP), (EDIT), (CRBU), (BEAM), (ALNY), (PFE), (REGN)

CRISPR technology has been receiving so much hype over the past years. However, the promise of this gene editing platform has yet to be realized.

Crispr gene-editing therapies can apply permanent modifications to our DNA by zeroing in on specific genes and then incapacitating them or reworking harmful segments of their genetic instructions.

While this could change in the coming years, investors have become impatient with the progress and lack of any major breakthrough in genomics. Some are losing confidence that this sector could experience explosive growth.

This is what happened with Intellia Therapeutics (NTLA).

Earlier this week, the company showed data that patients who received a one-time gene-editing infusion exhibited sustained improvement in a genetic condition that can result in fatal swelling when left untreated.

To be more specific, Intellia’s update means it could deliver a potentially permanent solution for hereditary angioedema. In this condition, a patient has a miswritten gene in their liver cells that produces a specific protein that triggers a dangerous swelling throughout the body.

Applying the treatment to 6 patients, Intellia’s one-time treatment lowered blood levels of the harmful proteins by more than 90% and decreased the swelling.

This is a more notable effect than the results from existing drugs like Takhzyro from Ionis Pharmaceuticals (IONS) and Takeda Pharmaceutical (TAK).

Despite the encouraging update, Wall Street still spurned the stock, and its price fell.

It looks like investors have lost patience with the slow progress of clinical studies in genetic treatments, pushing some to take advantage of the positive news from Intellia to abandon their positions.

Actually, it’s not only Intellia that suffered from this mistreatment by the market. Investors have also been dumping other stocks utilizing the Nobel-prize-winning technology, Crispr-Cas9, including CRISPR Therapeutics (CRSP), Editas Medicine (EDIT), Caribou Biosciences (CRBU), and Beam Therapeutics (BEAM).

Intellia was hailed the top CRISPR stock in 2021 when the company and its co-collaborator, Regeneron (REGN), shared their promising interim results from a Phase 1 study assessing NTLA-2001, a treatment for a rare genetic disease called transthyretin (ATTR) amyloidosis.

This Crispr infusion candidate managed to knock out rogue genes in the liver cells of 12 patients, halting ATTR’s poisonous effects on their hearts or nerves. Based on clinical data, Intellia’s therapy caused an over 90% drop in the fatal protein triggered by the genetic condition.

If successful, this one-and-done ATTR treatment from Intellia would go head-to-head against other chronic drug therapies like Onpattro by Alnylam Pharmaceuticals (ALNY) or Pfizer’s (PFE) Vyndagel, which generates $2 billion in sales every year.

Many companies use Crispr technology to edit human genomes in an effort to treat and possibly even cure rare genetic diseases. Their treatments typically utilize either an ex vivo or an in vivo approach. With ex vivo therapies, the genes are altered outside the patient’s body.

However, Crispr’s use is not only limited to targeting genetic conditions. There are also gene-editing companies that are working on leveraging the technology to come up with treatments for various kinds of cancer.

In particular, Crispr technology has been a biotech favorite in the development of chimeric antigen receptor T-cell or CAR-T therapies. There are used to genetically engineer immune cells to target specific tumors.

Apart from these, some biotech companies are using Crispr technology to conduct screening. This is different from genetic testing, though.

When using Crispr for screening, the genes are modified in a manner that makes them nonfunctional or inoperative. Crispr screening allows biotechs to explore which genes take on particular functions, which can be critical in the development of drugs and treatments.

Intellia’s recent updates are clear indications that Crispr technology works. Since this will be applied to humans, we should expect the timeline and adaptation to take longer.

I have become more and more thrilled with developments in the gene editing space. Moreover, I believe it’s no longer about “if” but when it will happen.

Overall, the gene editing sector is not for fast-paced investors. This is for those willing to wait for a very long time, particularly for stocks like Intellia Therapeutics.

Mad Hedge Biotech and Healthcare Letter

April 21, 2022

Fiat Lux

Featured Trade:

LET’S GET READY TO RUMBLE)

(MRNA), (PFE), (BNTX), (AZN), (ABBV), (MRK), (BMY), (TAK), (GILD),

(SNY), (ALNY), (NVS), (REGN), (IONS), (GSK), (BIIB), (CRSP)

As we gradually reach the pinnacle of biotechnology formation, a war is brewing in the life sciences world.

This can be one of the most exciting times for medical innovations for patients. Meanwhile, investors can be picky when picking where to put their money.

Even up-and-coming scientists can seize the opportunities to lay the groundwork for their own dream organizations.

At the same time, those aspiring to climb the corporate ladder have better chances at becoming CEO without the need to slog through the biopharma sector and scramble for whatever opening is available.

However, as more and more companies launch practically every day, claiming to offer groundbreaking and revolutionary breakthroughs, it’s critical to keep in mind that not all biotechs will succeed.

Actually, the number of biotech companies has been steadily rising since 2015.

In that year, 177 firms were formed, with biotech birth rates breaching the 200-per-annum mark by 2017 and 2018.

Seeing as many more have emerged even during the pandemic, it looks like the biotech world won’t be slowing down anytime soon.

Even funding hasn’t been deterred by economic downturns.

From 2015 to 2018, the total funding for biotech companies averaged between $68.6 million to roughly $90.2 million.

After a bustling, record-breaking 2020, the bar leading to 2021 was expectedly high.

Surprisingly, 2021 blew those figures out of the water as private investors opted to raise the bar even higher.

It’s the type of climb that’s truly hard to believe.

Biotechs raised over $22 billion in private funds in 2020 following a sluggish 2019. In 2021, that figure rose to $28.5 billion.

The top earner in these funding rounds last year was China’s Abogen, which took $1 billion in private investors’ money across two rounds.

Abogen is an mRNA-centered firm that’s currently working on a COVID-19 vaccine.

What makes its product different and possibly better than Moderna (MRNA), Pfizer (PFE), BioNTech (BNTX), and AstraZeneca (AZN) is that it would be thermostable. That is, it could be used in areas without access to refrigeration.

Another big winner in 2021 is Massachusetts-based biotech ElevateBio, which aims to be a one-stop shop for cell and gene therapies.

The idea is to develop a technology that fuses its gene-editing platform, cell engineering structure, and manufacturing warehouse into one system to ease and accelerate the drug development process.

Although not entirely the same, this plan has similarities with the strategies of Big Pharma names like AbbVie (ABBV) and Merck (MRK).

Amid the growing number of biotechs, a key challenge is how to stand out among companies that target the same disease areas. This kind of competition could hamper innovation.

The clearest indicator of success would be receiving approval and being able to launch the products commercially.

Ultimately, the goals are to offer safe and effective treatments and provide value to their shareholders.

Unfortunately, the reality is only a handful of startups do make it all the way to the top.

The more feasible scenario is that bigger businesses would acquire these companies—and that seems to be the case these days.

Alongside the booming biotech formation rate are the increasingly aggressive biotech buyout deals.

We’ve seen this before.

It started in 2019, with Bristol Myers Squibb (BMY) buying Celgene, followed by AbbVie splurging on Allergan and Takeda (TAK) merging with Shire.

In 2020, AstraZeneca bought biotech superstar Alexion Pharmaceuticals while Gilead Sciences (GILD) snapped up Immunomedics.

Meanwhile, Sanofi (SNY) stacked its deck with the $3.2 billion acquisition of Translate Bio. As for Merck, this biopharma sneaked in a massive win with an $11.5 billion buyout of Acceleron.

For this year, several names have already been eyed by Big Pharmas.

There’s Alynlam Pharmaceuticals (ALNY), an RNA-centered company, which seems to be the target of both Novartis (NVS) and Regeneron (REGN).

Another RNA-focused company, Ionis Pharmaceuticals (IONS), appears to be a key target as well, with the likes of GlaxoSmithKline (GSK), Bayer, and even Biogen (BIIB) waiting for an opportunity to pounce.

After all, acquisitions form an integral lifeline of the biotech world. Huge businesses with the resources swoop up promising buyout candidates to bolster their own pipelines.

However, M&A isn’t the only option for biotechs. There’s also the path where they can seek companies with similar focus and consolidate to become larger and more competitive entities.

This has been the expected plan for CRISPR Therapeutics (CRSP) for a long time. Hence, it is no surprise if other biotechs with their own groundbreaking technologies decide to follow the same route.

Overall, the biotech industry is booming amid its recent struggles with the market.

The faster growth rate of companies can be attributed to more investors seeing the industry's potential and, of course, better access to technology and scientific advancement.

Moreover, the world has become more interested in the biotech world and what the industry can offer due to the pandemic.

COVID-19 has shone a light on this sector following the quick and effective results of the vaccines and treatments.

That is, people have finally caught on to the idea that there is an incredible opportunity in biotech.

While a correction is to be expected at some point, the critical thing to bear in mind is that great ideas will always generate funding no matter what.

Mad Hedge Biotech & Healthcare Letter

August 19, 2021

Fiat Lux

FEATURED TRADE:

A LOW-PROFILE BIOTECH WINNER

(VRTX), (ACAD), (SRPT), (FGEN), (MRK), (MRNA), (NVS), (XLRN), (PTGX), (IONS), (BLUE), (EDIT), (ABBV)

Choosing winners among biotechnology and healthcare stocks these days isn’t easy.

Since the year started, the sector has been marred with several unexpected disappointments like the 50% decline of crowd favorites Acadia Pharmaceuticals (ACAD) and Sarepta Therapeutics as well as the 33% fall of the ever-dependable FibroGen (FGEN).

So, how can investors pick a winner?

One tactic is taking a peek at what Wall Street analysts are doing, noting which among the companies they’re following are trading the farthest below the estimated price points.

Among the names on the list, a particular stock stands out as a strong contender these days: Vertex Pharmaceuticals (VRTX).

Although it’s one of the most widely known biotechnology companies today, Vertex actually started in a garage of a Harvard-trained chemist, Joshua Bogner, who left his cushy job at one of the most illustrious big pharma companies at that time, Merck (MRK), to pursue his vision.

The company’s raison d’être was a major selling point for a lot of talented and idealistic scientists in that era.

That is, Vertex wanted to find cures for the most challenging diseases and do this in an unbureaucratic setting.

Since then, Vertex’s goal has been straightforward: tackle the most complex and toughest diseases and deliver breakthrough treatments that offer tangible benefits to patients.

Over the years, the company has managed to keep this goal at the forefront of its efforts, starting with its work on the devastating genetic disorder called cystic fibrosis (CF).

Vertex’s work on CF took over a decade, but it eventually led to an impressive franchise that helped with the treatment of patients.

In the first quarter of 2021 alone, sales in this segment reached $1.7 billion.

Expanding on its work, Vertex has explored genetic therapies and set up a collaboration with Moderna (MRNA) in 2016.

Using the latter’s well-established expertise in messenger RNA technology, the companies are expected to come up with more aggressive and advanced CF treatments in the coming years.

Given these developments, Vertex reiterated its 2021 sales guidance to be somewhere in the range of $6.7 and $6.9 billion. Meanwhile, sales of its CF franchise are estimated to peak at $9 to $10 billion—if not higher—by 2024.

Aside from its work on CF, Vertex has also been pouring resources on developing treatments for severe sickle cell anemia and beta thalassemia, a rare blood disorder.

In fact, the company has been looking into these developments as the next major revenue stream, as seen in its bolstered collaboration deal with CRISPR Therapeutics (CRSP).

In this deal, Vertex paid the smaller biotechnology company $900 million upfront plus a potential addition of $200 million following the first regulatory approval of their therapy, CTX001.

While this may sound like a hefty deal to some, Vertex actually values CTX001 at roughly $11 billion.

CTX001, which is a one-time therapy, is priced at roughly $1 million per patient. At this point, the market for beta thalassemia is valued at $32 billion.

Needless to say, this would make CTX001 a massive income generator in the next few years.

Considering the lucrative market for beta thalassemia, though, it’s no surprise that several competitors have emerged to grab their share as well.

Some companies, such as Novartis (NVS) and Acceleron (XLRN), offer maintenance drugs for the disease.

Meanwhile, others like Protagonist Therapeutics (PTGX) and Ionis Pharmaceuticals (IONS) are attempting to develop treatments that would become direct competitors of CTX001.

However, the closest rivals of the Vertex-CRISPR candidate are from Bluebird Bio (BLUE) and Editas Medicine (EDIT).

While this has become a crowded space, Vertex and CRISPR remain the leaders in this segment, as most of the other candidates are still in the investigation phase.

Since it was founded in the 1980s, Vertex has remained true to its vision of tackling some of the toughest diseases out there.

While big pharmaceutical companies, such as AbbVie (ABBV), decided to expand their portfolio through acquisitions, Vertex leveraged its talent pool and maximized its funds by establishing strategic collaborations instead.

This tactic provided the company with enough elbow room that eventually led to its dominance in the CF space, where it now enjoys a virtual monopoly until at least the next decade.

Meanwhile, it has forged strong relationships with promising biotechnology companies and can very well be on its way to becoming the most dominant force in the rare blood disorder segment.

Overall, Vertex Pharmaceuticals is an attractive stock with an impressive portfolio and an even more impressive pipeline.