Global Market Comments

December 8, 2021

Fiat Lux

Featured Trade:

(ON EXECUTING MY TRADE ALERTS),

(TEN REASONS WHY STOCKS CAN’T SELL OFF BIG TIME),

(SPY), (INDU), ($COMPQ), (IWM), (TLT), (GME)

Global Market Comments

December 8, 2021

Fiat Lux

Featured Trade:

(ON EXECUTING MY TRADE ALERTS),

(TEN REASONS WHY STOCKS CAN’T SELL OFF BIG TIME),

(SPY), (INDU), ($COMPQ), (IWM), (TLT), (GME)

Global Market Comments

November 5, 2021

Fiat Lux

Featured Trade:

(NOVEMBER 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(BRKB), (COIN), (IWM), (GOOGL), (MSFT), (MS), (GS), (JPM),

(BABA), (BIDU), (JD), (ROM), (PYPL), (FXE), (FXA), (FXB), (CRSP), (TSLA), (FXI), (BITO), (ETHE), (TLT), (TBT), (BITO), (CGW)

Below please find subscribers’ Q&A for the November 3 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon

Valley.

Q: Have you considered buying Coinbase (COIN)?

A: Yes, we actually recommended it as part of our Bitcoin service in the early days back in July. It’s gone up 62% since then, right along with the Bitcoin move itself. So yeah, buy (COIN) on dips—and there will be dips because it will be at least triple the volatility of the main market. And be sure to dollar cost average.

Q: Do you think the breakout in small caps (IWM) will hold and, if so, should we focus on small-c growth?

A: Yes it will hold, but no I would focus on the big cap barbells, which will lead this rally for the next 6 months. And there you’re talking about the best of tech which is Google (GOOGL) and Microsoft (MSFT), and the best of financials which is Morgan Stanley (MS), Goldman Sachs (GS), and JP Morgan (JPM).

Q: Why not time the webinar for after the FOMC? What will be the market reaction?

A: Well, first of all, we already know what they’re going to say—it’s been heavily leaked in the last week. The market reaction will be initially a potential sharp down move that lasts a few minutes or hours, and then we start a grind up for the next two months. So that's why I wanted to be 80% leverage long going into this. Second, we have broadcast this webinar at the same time for the last 13 years and if we change the time we will lose half our customers.

Q: Why do you always do debit spreads?

A: They’re easier for beginners to understand. That’s the only reason. If you’re sophisticated enough to do a credit spread, the results will be the same but the liquidity will be slightly better, and you can also apply that credit to meet your margin requirements. We have a lot of basic beginners signing up for our service in addition to seasoned pros and I always encourage people to do what they're most comfortable with.

Q: Are you still comfortable with the Morgan Stanley (MS) and Berkshire Hathaway (BRKB) positions?

A: I expect both to go up 10-20% by March, so that’s pretty comfortable. By the way, if you have extremely deep in the money call spreads on Goldman Sachs or Morgan, consider taking profits on those and rolling your strikes up. If you have like the $360-$380 vertical bull call spread in Goldman Sachs, realize that gain and roll up to the $420-$430 March position in Goldman Sachs—that will give you another 100% profit by March. With the $360-$ 380s, you have like 97% of the profit already in the price, there’s no leverage left and no point in continuing, you can only go down.

Q: What should I do with my China position?

A: Sell all your positions in China, realize all the losses now so you can offset those with all the huge profits on all your other positions this year. There I’m talking about Ali Baba (BABA), Baidu (BIDU), and (JD), which have been absolutely hammered anywhere from down 50% to down 70%. And do it now before everyone else does it for the same reasons.

Q: Thoughts on Paypal (PYPL) lately?

A: The stock is out of favor as money is moving out of PayPal into newer fintech stocks. The move down is totally unjustified and screaming long term buy here, but for the short-term investors are going to raid the piggy bank, sell the PayPal, and go into the newer apps. This has been my biggest money-losing trade personally this year because PayPal long-term has a great story.

Q: Will earnings fall off next year due to prior year comparisons or supply chain?

A: No, if anything, earnings are accelerating because supply chain problems mean you can charge customers whatever you want and therefore increase margins, which is why the stock market is going up.

Q: Long term, what would your wrong strikes be?

A: I would say don’t get greedy. I’m doing the ProShares Ultra Technology (ROM) $120-$125 call spread for May expiration—the longest expiration they offer. That gives you about 100% return in 6 months; 100% is good enough for me because then I’ll do the same thing again in May and get another 100%. What’s 100% x 100%? It’s 400% because you’re reinvesting a much larger capital base the second time around. If a 100% profit in six months is not enough for you then you are in the wrong line of business.

Q: Do you think Ethereum (ETHE) has long-term potential upside?

A: Yes, is a 10X move enough? We just had a major new high in Ethereum because they made moves to limit the production of new Ethereum. Ethereum is the superior technology because its architecture avoids the code repeats that Bitcoin does and therefore only uses a third of the electricity to create. But Bitcoin is attracting the big institutional cash flows because they have an early mover advantage. By the way, how much electricity does crypto mining consume? The entire consumption of Washington state in a year, so it’s a big deal.

Q: What should I do about Crisper Therapeutics (CRSP)?

Crispr Therapeutics (CRSP) is my other disaster for this year because ignored the move up to $170—we’re now back into the $90’s again. So, I have 2023 LEAPS on that; I’m going to keep them, I’ve already suffered the damage, but the next time it goes up to $170 I’m selling! Once burned, twice forewarned. And part of the problem with the whole biotech sector is we are now in the back end of the pandemic and anything healthcare-related will get hit, except for the vaccine stocks like Pfizer (PFE) which are still making billions and billions of dollars.

Q: I bought Baidu (BIDU) and Alibaba (BABA) years ago at a much lower price and I'm still up quite a lot; what should I do?

A: If you have the big cushion, I would keep them and look for #1 recovery in the Chinese economy next year and #2 for the government to back off from their idiotic anticapitalism strategy because it’s costing them so much money.

Q: Is Robinhood (HOOD) a good LEAP candidate?

A: Only on a really big dip, and then you want to go out two years. With a stock that’s volatile as hell like Robinhood and could drop by half on no notice, so you only buy the big dips. It’s not a slowly grinding upward stock like Goldman Sachs (GS) and Morgan Stanley (MS) where you can add LEAPS now because you know it’s going to keep grinding up.

Q: How can Morgan Stanley go up when the chief strategist is bearish?

A: Their customers aren't listening to their chief strategist—they’re buying. And the volume of the stock, which is where Morgan Stanley makes money, is going through the roof, they’re making record profits there. And I've got Morgan Stanley stock coming out of my ears in LEAPS and so forth.

Q: What are 5 stocks you would buy right now?

A: Easy: Google (GOOGL), Microsoft (MSFT), Morgan Stanley (MS), Goldman Sachs (GS), and JP Morgan (JPM). Buy whatever is down that day. They’re all going up.

Q: Too late to buy Tesla (TSLA) calls?

A: Yes, it is. Tesla has a long history of 40% corrections; we had one that ended in May, and then it doubled (and then some). So yeah, too late to buy the calls here. Go back and read my research from May which said buy the stock and you get a car for free—and that worked again, except this time, you can get three free Tesla’s. A lot of subscribers have sent me pictures of their Teslas they got for free on my advice; I’m probably the largest salesman for Tesla for the last 10 years and all I got out of it was a free Powerwall (the red one)..

Q: How much higher do you think semiconductor companies will go?

A: Higher but it’s impossible to quantify. You’re getting very speculative short-term buying in there. So, I think it continues to the rest of the year, but with chips, you never know.

Q: Would you be buying Crispr Therapeutics (CRSP) at these levels?

A: Yes, but I would either just buy the stock and not be dependent on the calendar or buy a 2 ½ year LEAP and get an easy double on that.

Q: What about the currencies?

A: I don’t see much action in the currencies as long as the US is raising interest rates. I think the Euro (FXE), the Aussie (FXA), and the British pound (FXB) will be dead for the time being. Nobody wants to sell them but nobody wants to buy them either when you’re looking at a potential short term rise in the dollar from rising interest rates.

Q: What stable coins are the right answer for cryptocurrency?

A: The US dollar stable coin, but for price appreciation, you’re really looking at Bitcoin and Ethereum. Stable coins are stable, they don’t move; you want stuff that’s going to go up 5, 10, or 20 times over the next 10 years like Bitcoin (BITO) and Ethereum (ETHE). That is my crypto answer.

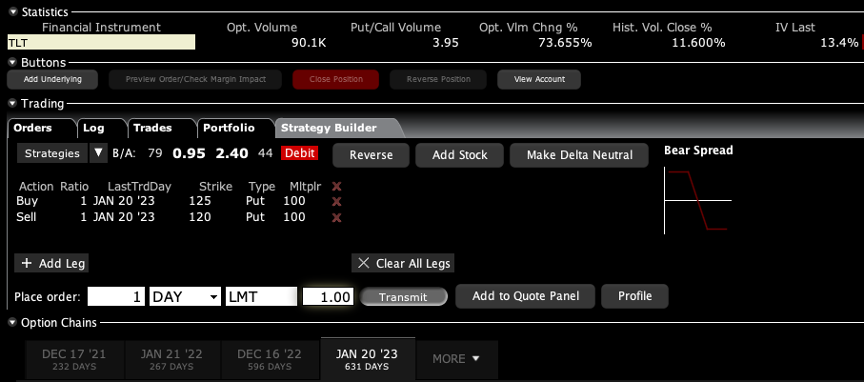

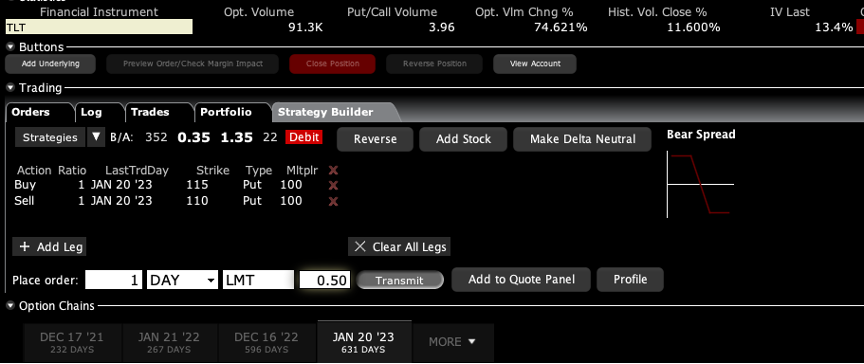

Q: What should I do about the iShares 20 Plus Year Treasury Bond ETF (TLT) $135-$140 put spread expiring in January?

A: If we get another run down to the $141 level that we saw last month, I would come out of all short treasury positions because you’re starting to run into time decay problems with the January expirations. And in case we remain in a range for some reason, I would be taking profits at the bottom end of the range. It was my mistake that I didn’t grab those profits when we hit $141 last time. So don’t let profits grow hair on them, they tend to disappear. We lost six months on this trade due to the delta virus and the mini-recession it brought us.

Q: Will there be accelerated tech selling in December because of the new tax rates?

A: What new tax rates? There has been no new tax bill passed and even if there were, I think people wouldn’t tax sell this year because the profits are enormous. They would rather do any selling in January at higher prices and then defer payment of those taxes by 18 months. I don’t think there will be any tax issues this year at all.

Q: What’s your return on solar power investments?

A: My break-even was four years because our local utility, PG&E, went bankrupt and the only way they're getting out of bankruptcy is raising electricity prices by 10% a year. It turns out that as a result of global warming, the panels have operated at a higher efficiency as well, so we’re getting a lot more power output than originally expected. Now I get free electricity for the remaining 20-year life of the panels which is great because with two Tesla’s and all-electric heating and air conditioning I use a lot of juice. My monthly bill is a sight to behold. I also power the 20 surrounding houses and for that PG&E pays me $1,800 a month.

Q: Do you see China (FXI) invading Taiwan as a potential threat to the market?

A: China will never invade Taiwan. They own many of the companies they're already in, they de facto control Taiwan government from a distance; they would not risk the international consequences of an actual invasion. And we have the US seventh fleet there to stop exactly that. So, they can make all the noise they want but nothing will come of it. I’ve been watching this for 50 years and nothing has ever happened.

Q: Would you buy ProShares Ultrashort 20+ Treasury ETF (TBT) here?

A: Absolutely, with both hands, all I can get.

Q: Can you recommend any water ETF opportunity?

A: Yes there is one I wrote a piece on last month. It’s the Claymore S&P Global Water Index ETF (CGW).

Q: How long can you hold the (TBT) before time decay hurts?

A: It doesn’t hurt, the cost of the TBT is two times the 10-year rate. So that would be 3%, plus 1% a year for management fees, and that’s your slippage on the TBT in a year right now—it’s 4%. Remember if you’re short the bond market, you have to pay the coupon when you’re short. Double the bond market and you have to pay double the coupon.

Q: Is the ProShares Bitcoin Strategy ETF (BITO) a good alternative to buying bitcoin?

A: I would say yes because I’ve been watching the tracking on that very carefully and it’s pretty damn close. Plus there’s a lot of liquidity there, so yeah, buy the (BITO) ETF on dips and dollar cost average.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 30, 2021

Fiat Lux

Featured Trade:

(APRIL 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(PFE), (MRNA), (USO), (DAL), (TSLA), (CRSP), (ROM), (QQQ), (T), (NTLA),

(EDIT), (FARO), (PYPL), (COPX), (FCX), (IWM), (GOOG), (MSFT), (AMZN)

Below please find subscribers’ Q&A for the April 28 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley, CA.

Q: There is talk of digital currencies being launched in the US. Is there any truth to that? How would that affect the dollar?

A: There is no truth to that; there is not even any serious discussion of digital currency at the US Treasury. My theory has always been that once Bitcoin works and is made theft-proof, the government will take it over and make that the digital US dollar. So far, Bitcoin has existed regulation-free; in fact, the IRS is counting on a trillion dollars in capital gains being taxed going forward in helping to address the budget deficit.

Q: If you have a choice, what’s the best vaccine to get?

A: The best vaccine is the one you can get the fastest. I know you’re a little slow on the rollout in Canada. Go for Pfizer (PFE) if you’re able to choose. You should avoid Moderna (MRNA) because 15% of people getting second shots have one-day symptoms after the second shot. But basically, you don’t get to choose, only kids get to choose because only Pfizer has done trials on people under the age of 21. So, if you take your kids in, they will all get Pfizer for sure.

Q: Should I buy Freeport McMoRan (FCX) here or wait for a bigger dip?

A: Freeport has just had a 25% move up in a week. I wouldn’t touch that. We put out the trade alert when it was in the mid $30s, and it's essentially at its maximum profit point now. So, you don't need to chase—wait for a bigger dip or a long sideways move before you get in.

Q: How do I trade copper if I don't do futures?

A: Buy (FCX), the largest copper producer in the US, and they have call options and LEAPS. By the way, if we do get another $5 dip in Freeport, which we just had, I would really do something like the (FCX) $45-$50 2023 LEAP. You can get 5 times your money on that.

Q: Time to buy oil stocks (USO) for the summer?

A: No, the big driver of oil right now is the pandemic in India. They are one of the world's largest consumers—you find out that most poor countries are using oil right now as they can’t afford the more expensive alternative sources of power. And when your biggest customer is looking at a billion corona cases, that’s bad for business. Remember, when you trade oil, you’re trading against a long-term bear trend.

Q: Would you buy Delta Airlines (DAL) at today’s prices?

A: Yes, I’m probably going to go run the numbers on today's call spread; I actually have 20% of cash left that I could spend. So that looks like a good choice—summer will be incredible for the entire airline industry now that they have all staved off bankruptcy. Ticket prices are going to start rising sharply with an impending severe aircraft shortage.

Q: What are your thoughts on the Buffet index which shows that stocks are more stretched vs GDP at any time vs 2000?

A: The trouble with those indicators is that they never anticipated A) the Fed buying $120 billion a month in US Treasury bonds, B) the Fed promising to keep interest rates at zero for three years, and C) an enormous bounce back from a once-in-a-hundred-year pandemic. That's why not just the Buffet Index but virtually all technical indicators have been worthless this year because they have shown that the market has been overbought for the last six months. And if you paid attention to your indicators, you were either left behind or you went short and lost your shirt. So, at a certain point, you have to ignore your technical indicators and your charts and just buy the damn market. The people who use that philosophy (and know when to use it, and it’s not always) are up 56% on the year.

Q: What trade categories are getting fantastic returns? It’s certainly not tech.

A: Well, we actually rotated out of tech last September and went into banks, industrial plays, and domestic recovery plays. And you can see in the stocks I just showed you in our model portfolio which one we’re getting the numbers from. Certainly, it was not tech; tech has only performed for the last four weeks and we jumped right back in that one also with positions in Microsoft (MSFT). So yes, it’s a constantly changing game; we’re getting rotations almost daily right now between major groups of stocks. The only way to play this kind of market is to listen to someone who’s been practicing for 52 years.

Q: I am 83 years old and have four grandchildren. I want to invest around $20,000 with each child. I was thinking of your bullish view on Tesla (TSLA) on a long-term investment. Do you agree?

A: If those were my grandchildren, I would give them each $20,000 worth of the ProShares Ultra Technology Fund (ROM), the 2x long technology ETF. Unless tech drops 50% from here, that stock will keep increasing at twice the rate of the fastest-growing sector in the market. I did something similar with my kids about 20 years ago and as a result, their college and retirement funds for their kids have risen 20 times. So that’s what I would do; I would never bet everything on a single stock, I would go for a basket of high-tech stocks, or the Invesco QQQ NASDAQ Trust (QQQ) if you don’t want the leverage.

Q: Do you like Amazon (AMZN) splitting?

A: I don’t think they’ll ever split. Jeff Bezos worked on Wall Street (with me at Morgan Stanley) and sees splits as nothing more than a paper shuffle, which it is. It’s more likely that he’ll break up the company into different segments because when they get to a $5 trillion market cap, it will just become too big to manage. Also, by breaking Amazon up into five companies—AWS, the store, healthcare, distribution, etc., —you’re getting a premium for those individual pieces, which would double the value of your existing holdings. So, if you hold Amazon stock, you want it to face an antitrust breakup because the flotation will double the value of your total holdings. That has happened several times in the past with other companies, like AT&T (T), which I also worked on.

Q: When is Tesla going to move and why is it going up with earnings up 74%?

A: Well, the stock moved up a healthy 46% going into the earnings; it’s a classic sell the news market. Most stocks are doing that this quarter and they did so last quarter as well. And Tesla also tends to move sideways for years and then have these explosive moves up. I think the next double or triple will come when they announce mass production of their solid-state batteries, which will be anywhere from 2 to 5 years off.

Q: How can I renew my subscription?

A: You can call customer support at 347-480-1034 or email support@madhedgefundtrader.com and I guarantee you someone will get back to you.

Q: Top gene-editing stock after CRISPR Therapeutics (CRSP)?

A: There are two of them: one is Intellia (NTLA); it’s actually done better than CRISPR lately. The second is Editas (EDIT) and you’ll find out that the same professionals, including the Nobel prize winner Jennifer Doudna here at Berkeley, rotate among all three of these, and the people who run them all know each other. They were all involved in the late 2000's fundamental research on CRISPR, and they’re all frenemies. So yes, it's a three-company industry, kind of like the cybersecurity industry.

Q: What about PayPal (PYPL)?

A: I would wait for the earnings since so many companies are selling off on their announcements. See if they sell off 3-5%, then you buy it for the next leg up. That is the game now.

Q: Do you like any 3D printing stocks like Faro Technologies (FARO)?

A: No, that’s too much of a niche area for me, I’m staying away. And that's becoming a commodity industry. When they were brand new years ago, they were red hot, now not so much.

Q: Do you see the chip companies continuing their bull run for the next few months?

A: I do. If anything, the chip shortage will get worse. Each EV uses about 100 chips, and they’re mostly the low-end $10 chips. Ford (F) said production of a million cars will be lost due to the chip shortage. Ford itself has 22,000 cars sitting in a lot that are fully assembled awaiting the chips. Tesla alone has $300 worth of chips just in its inverters, and there are two inverters in every car. So, when you go from production of 500,000 cars to a million in one year, that's literally billions of chips.

Q: The airlines are packed; what are your thoughts?

A: Yes, one of the best ways to invest is to invest in what you see. If you see airlines are packed, buy airline stocks. If you can’t hire anyone, you know the economy is booming.

Q: What about the Russel 2000 (IWM)?

A: We covered it; it looks like it wants to break out to new highs from here. By the way, there are only 1,500 stocks left in the Russell 2000 after the pandemic, mergers, and bankruptcies.

Q: Are there other ways to play copper out there like (FCX)?

A: Yes; one is the (COPX)— a pure copper futures ETF. However, be careful with pure metal ETFs of any kind because they have huge contangos and you could get a 50% move up in your commodity while your ETF goes down 50% over the same time. This happens all the time in oil and natural gas, and to a lesser degree in the metals, so be careful about that. Before you get into any of these alternative ETFs, look at the tracking history going back and I think you'll see you're much better off just buying (FCX).

Q: How long do you typically hold onto your 2-year LEAPS? Based on my research, the time decay starts to accelerate after about 3 months to one year on LEAPS.

A: Actually, with LEAPS, the reason I go out to two years is that the second year is almost free, there's almost no extra cost. And it gives you more breathing room for this thing to work. Usually, if I get my timing right, my LEAP stocks make big moves within the first three months; by then, the LEAP has doubled in value, and then you have to think about whether you should keep it or whether there are better LEAPS out there (which there almost always are). So, you sell it on a double, which only took a 30% move in the stock, or you may be committed to the company for the long term, like a Microsoft or an Amazon. And then you just run it through the expiration to get a 400% or 500% profit in two years. That is how you play the LEAP game.

Q: Are these recorded?

A: Yes, we record these and we post them on the website after about 2 hours. Just log into the site, go to “my account”, then select your subscription type (Global Trading Dispatch or Technology Letter), and “webinars” will be one of the button choices.

Q: Can you also sell calls on LEAPS?

A: Yes and the only place to do that is the US Treasury market (TLT). There you either want to be short calls far above the market, out two years, or you want to be long puts. And by the way, if you did something like a $120-$125 put spread out to January 2023, then you’re looking at making about a 400% gain. That is a bet that 20-year interest rates only go up a little bit more, to 2.00%. If you really want to bet the ranch, do something like a $120-$122 and you might get a 1000% return.

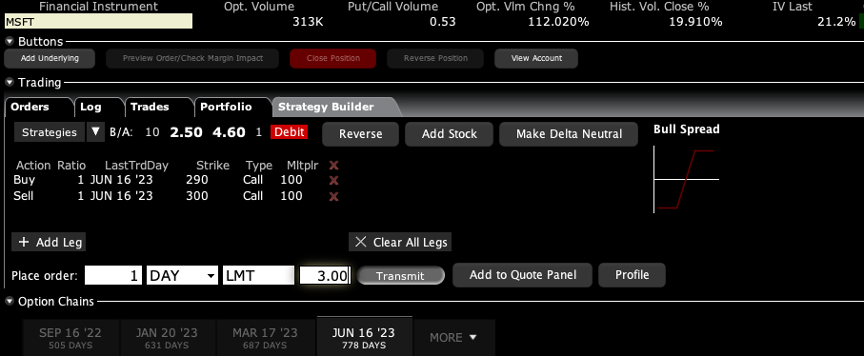

Q: What is the best LEAP to trade for Microsoft (MSFT)?

A: If you want to go out two years, I would do something like a June 2023 $290-$300 vertical bull call spread. There is an easy 67% profit in that one on only a 20% rise in the stock. I do front monthlies for the trade alert service, so we always have at least 10 or 20 trade alerts going out every month. And the one I currently have for is a deep in the money May $230-$240 vertical bull call spread which expires in 12 days.

Q: What is the best way to play Google (GOOG)?

A: Go 20% out of the money and buy a January 2023 $2,900-$3,000 vertical bull call spread for $20—that should make about 400%. If you want more specific advice on LEAPS, we have an opening for the Mad Hedge Concierge Service so send an email to support@madhedgefundtrader.com with subject line “concierge,” and we will reach out to you.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

I Think I See Another Winner

Global Market Comments

March 22, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ENTERING TERRA INCOGNITA),

(TLT), (TSLA), (JPM), (VIX), (QQQ), (IWM), (BAC), (C), (SPY)

During the Middle Ages, when explorers sought new lands and their rich treasures, large sections of their navigational charts were marked with the term “terra incognita.”

That meant what lays beyond was unknown and that they should enter only at their own risk. Often there was a picture of a dragon or a sea monster to mark the spot.

There was also often a warning that you might even sail off of the edge of the earth.

Financial markets have entered a “terra incognita” of their own recently.

Here is the big unknown: How high can ten-year US Treasury bond yields soar when the Federal Reserve is promising to keep overnight interest pegged at 25 basis points until 2024 in the face of essentially unlimited monetary and fiscal stimulus?

So far, the answer is: more.

That is a really big question because we’ve never really been here before.

In fact, some Cassandras from the right are even predicting such a policy will cause us to sail off of the edge of the earth. The modern-day equivalent of running into dragons is inviting runaway inflation.

I can tell you from my own vast, almost immeasurable navigational experience (I am licensed by the US government) that “terra incognita” does not invite inordinate risk-taking or betting of ranches by traders or investors. Instead, they tend to sit on their hands, work on their golf swing, or update their Facebook pages.

That is what the Volatility Index (VIX) last week is essentially screaming at us by touching the $19 handle for the first time in a year.

Almost everyone I know has made more money in the markets than at any time in their lives. That is what a near doubling of the stock market in a year gets you.

And the new wealth was not attained because their intelligence and market insight have suddenly doubled, although a strong case for such can be made for readers of Mad Hedge Fund Trader.

So I used the Friday, March 19 option expiration to go into a rare 100% cash position. I really have gotten away with too much lately.

Then feeling guilty, I slapped on a single long in Tesla (TSLA), that old reliable money-maker. It’s worked for me since it was $3.50 a share. After all, a gigantic green energy infrastructure bill is about to pass in Congress. What better to own than the world’s largest EV car maker.

And what a tear it has been.

After bringing in a ballistic 66.64% profit in 2020, I reeled in another 40.38% gain in the first 2 ½ months of 2021. I did this via 40 trades which generated 38 wins and only two losses. That’s a success rate of an incredible 95%. I have to pinch myself when I read these numbers.

I am concerned because numbers any higher than this will look fake. It’s a rule of thumb in the investment business that when managers claim a 100% success rate, they are either high-frequency traders back by super-fast mainframe computers or running a scam.

So, I have been advising clients to pare back their biggest positions that became massively overweight purely through capital appreciation. Financials come to mind. JP Morgan (JPM) up 81% in three months? Sounds like a Ponzi Scheme.

So let me give you some upside targets in the bond market. We doubled bottomed in 2012 and 2016 at a 1.37% yield in the ten-year Treasury bond yield. We have already surpassed that level like a hot knife through butter.

At the depths of the 2008-2009 Great Recession, rates bottomed at 2.0% yield, which now seems within easy reach. The lowest yield we saw after the 2003 Dotcom Crash was a 3.0%.

When the upside targets in interest rates in this cycle are the lows of the previous economic cycles, that augurs pretty well for the future of stock prices. That is the guaranteed outcome of the tidal wave of cash now sweeping the global financial system.

The permabears are warning that the “Roaring Twenties” have already happened. I argued that they are only just getting started and that the indexes have another 4X of upside in them over the rest of the decade. When the last “Roaring Twenties” occurred, you didn’t sell in 1921.

It also reminds me of the huge “rip your face off” rally we saw from March 2009 to 2010. A lot of market gurus said then that was the peak. They were wrong. Today, they are driving for Uber and Lyft.

So when a talking head warns you that higher interest rates will cause the stock market to crash, just turn off the boob tube and go back to practicing your golf swing.

The Mad Hedge Summit Videos are Up, from the March 9,10, and 11 confab. Listen to 27 speakers opine on the best strategies, tactics, and instruments to use in these volatile markets. The product discounts offered last week are still valid. Start, stop, and pause the videos at your leisure. Best of all, access to the videos is FREE. Access them all by clicking here at www.madhedge.com, click on CURRENT SUMMIT REPLAYS in the upper right-hand corner, and then choose the speaker of your choice.

Ten Year Bond Yields (TLT) soar to a 1.75%, setting financials on fire and demolishing tech (QQQ). We are rapidly approaching a 2.00% yield, which could trigger a huge round of profit-taking on bond shorts, a domestic stock selloff, and a tech rally. The next great rotation may be just ahead of us.

Oil (USO) dives 8% on fears of an imminent Saudi production increase and a worsening Covid-19 outlook in Europe. Are we next with all these early reopening’s? Gone 100% cash at the close with the March quadruple witching option expiration.

A Tax Hike is next on the menu. Corporate tax rates are returning from 21% to 28% for the small proportion of companies that actually PAY tax. Raising taxes on earnings of more than $400,000. Pass through entities to get a haircut. Increasing estate taxes. You better die soon if you want your kids to stay rich. Increase in capital gains taxes over $1 million. I want my SALT deduction back! The grand negotiation begins on who needs bridges, rail lines, and subway extensions. Hint: for some reason, there have been no new federal projects started in California for the past four years and all the existing ones were cut back.

Value Stocks (IWM) are beating growth ones, reversing a decade-long trend. The Russell Value Index is up 11% this year, while growth is unchanged. It’s a total flip from last year when growth was tech-led. This could continue for years, or until the tech becomes the new value stocks. Big winners include Boeing (BA), JP Morgan (JPM), and Morgan Stanley (MS), all Mad Hedge moneymakers.

Bitcoin tops 61,000. Nothing else to say but that because there are no fundamentals. It’s up 80% in 2021 and 540% YOY. But it is becoming a good risk-taking indicator thought, and right now it is shouting a loud and clear “Risk On.”

It’s going to be All About Stock Picking for the Rest of 2021, says Morgan Stanley strategist Mike Wilson. Dragging on the index from here on will be the prospects of rising rates, tax hikes, and inflation. Mike especially dislikes small caps (IWM) which have already had a terrific run, with a 19% YTD gain. Stock picking? Boy, did you come to the right place!

Fed to hold off on rates hikes through 2023, said Governor Jay Powell after the open Market Committee Meeting. Bonds rallied a full half-point on the news and then crashed again, taking yields to a new 1.70% high. It sees inflation reaching a positively stratospheric 2.0% sometime this year, after which it will die, so nothing to do here. This is what a 100% dovish FOMC gets you. Let the games begin!

New Housing Starts Collapse, from an expected +2.5% to -10.3%, as high lumber, land, labor, and interest rates take their toll. This will only drive new home prices high at a faster rate and the little remaining supply dries up. Millennials need some place to live.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

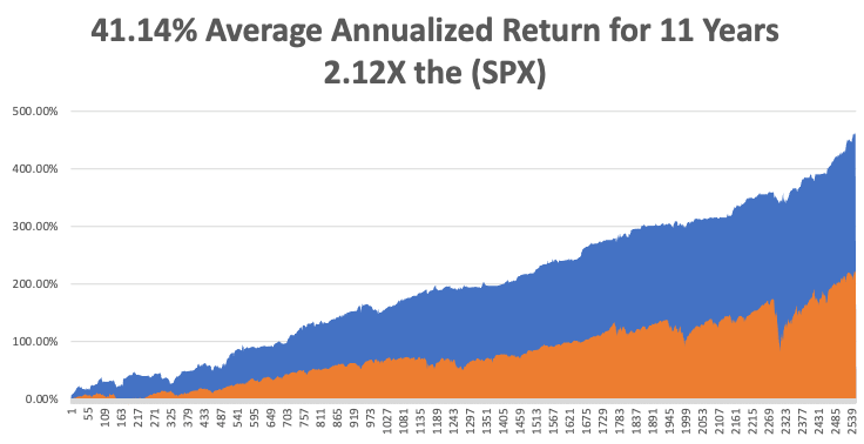

It’s amazing how well patience can help your performance. My Mad Hedge Global Trading Dispatch profit reached a super-hot 16.89% during the first half of March on the heels of a spectacular 13.28% profit in February.

It was a tough week in the market, so I held fire and ran my seven remaining profitable positions into the March 19 options expiration. I took advantage of a meltdown in Tesla (TSLA) shares to put on my only new position of the week with a very deep-in-the-money long. That leaves me with 90% cash and a barrel full of dry powder.

This is my fifth double-digit month in a row. My 2021 year-to-date performance soared to 40.38%. The Dow Average is up a miniscule 7.7% so far in 2021.

That brings my 11-year total return to 462.93%, some 2.12 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 41.14%.

My trailing one-year return exploded to 121.60%, the highest in the 13-year history of the Mad Hedge Fund Trader. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 29.8 million and deaths topping 542,000, which you can find here. Thankfully, death rates have slowed dramatically, but Obituaries are still the largest sector in the newspaper.

The coming week will be a boring one on the data front.

On Monday, March 22, at 9:00 AM, Existing Home Sales for February are released.

On Tuesday, March 23, at 9:00 AM, New Home Sales are published.

On Wednesday, March 24 at 8:30 AM, we learn US Durable Goods for February are printed.

On Thursday, March 25 at 8:30 AM, Weekly Jobless Claims are out. We also get the final read of US Q4 GDP.

On Friday, March 26 at 8:30 AM, US Personal Income & Spending for February are released. At 2:00 PM, we learn the Baker-Hughes Rig Count.

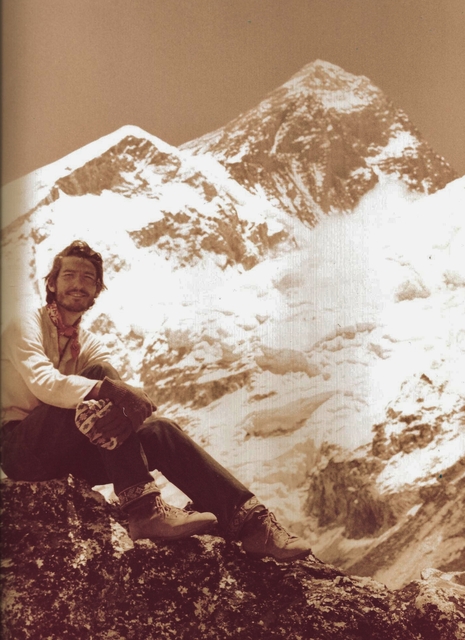

As for me, I have been doing a lot of high altitude winter mountain climbing lately, and with the warm spring weather, the risk of avalanches is ever present. It takes me back to the American Bicentennial Everest Expedition, which I joined in 1976.

It was led by my old friend, instructor, and climbing mentor Jim Whitaker, who pulled an ice ax out of my nose on Mt. Rainer in 1967 (you can still see the scar). Jim was the first American to summit the world’s highest mountain. I tried to break a high-speed fall and an ice ax kicked back and hit me square in the face. If I hadn’t been wearing goggles I would have been blinded.

I made it up to 22,000 feet on Everest, to Base Camp II without oxygen because there were only a limited number of canisters reserved for those planning to summit. At that altitude, you take two steps, and then break to catch your breath.

There is a surreal thing about that trip that I remember. One day, a block of ice the size of a skyscraper shifted on the Khumbu Ice Fall and out of the bottom popped a body. It was a man who went missing on the 1962 American expedition. Everyone recognized him as he hadn’t aged a day in 15 years, since he was frozen solid.

I boiled my drinking water, but at that altitude, water can’t get hot enough to purify it. So I walked 100 miles back to Katmandu with amoebic dysentery. By the time I got there, I’d lost 50 pounds, taking my weight to 120 pounds.

Jim was an Eagle Scout, the first full-time employee of Recreational Equipment Inc. (REI), and last climbed Everest when he was 61. Today, he is 92 and lives in Seattle, WA.

Jim reaffirms my belief that daily mountain climbing is a great life extension strategy, if not an aphrodisiac.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 15, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LISTEN TO THE (VIX),

(SPY), (IWM), (QQQ), (TLT), (VIX), (DAL), (BA), (ALK)

I decided to take a day off over the weekend and see what was happening in the real economy.

As I drove over the Bay Bridge, I spotted over 30 very large container ships from China loaded to the gills. They were diverted from Los Angeles where the delay to unload ships has extended to two months.

The San Francisco farmers market was jammed with a mask-wearing crowd. Standing in front of me in the line to buy lavender salt was former 49ers quarterback Joe Montana, who took his team to the Super Bowl four times. He was in great shape, looking at least 30 pounds lighter than in his heyday.

Leaving Half Moon Bay after picking up some driftwood for my garden, the traffic to get into town was at least an hour long.

It all underlies a theme for the economy and the markets that I have been expounding upon for the last year.

The Roaring Twenties have begun, the number of consumers and investors who believe this is increasing every day, and the impact on business and stocks is still being wildly underestimated.

You can see this in the Volatility Index (VIX), which has made a rare two roundtrips over the past month, and that means two possible things. Markets are undecided. When they make up their minds, they will either crash, or make a new leg up.

I vote for the latter.

I keep especially close attention on the (VIX) these days because it tells me when I can turn on or off my printing press for $100 bills. Anywhere over a (VIX) of $30 and I can strap on “free money” trades where the chances of losing money are virtually nil.

You can see this in my performance this year, where 40 roundtrips trade alerts in 11 weeks generated 38 wins and only two losses. That’s a success rate of an unprecedented 95%.

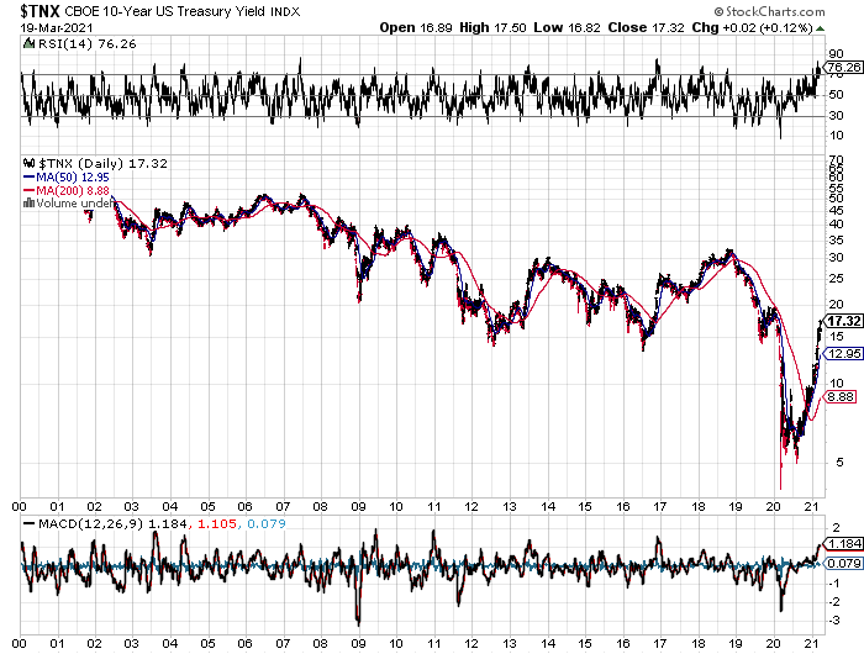

The indecision in the markets is obvious in the charts below. The large cap S&P 500 (SPX) and the small cap Russell 2000 (IWM) clawed their way to new highs last week, but the tech heavy NASDAQ (QQQ) made a feeble, halfhearted effort at best. Technology alone is being punished for rising interest rates as the ten-year US Treasury yield hit 1.62%.

This makes absolutely no sense as the larger tech companies are massive cash generators, run huge cash balances, and are enormous let lenders to the financial system. That means they make millions in interest payments from rising rates. What they are really being punished for is doubling from the pandemic low a year ago.

But never argue with Mr. Market.

Biden signs, with a record $1.8 trillion hitting the economy immediately. Money could start hitting your bank account this weekend if you are signed up for electronic payments with the IRS. Let the party begin! I already spent my money a long time ago. The Fed is forecasting a 10% GDP growth rate in Q2. Money is about to come raining down upon the economy….and the stock market. The big question is how much of this is already in the market. “Buy the rumor, sell the news”. Given the wild swings in the market, and multiple visits to a $32 (VIX), it’s clear that markets don’t know….yet.

The Next Battle is over infrastructure, which the democrats want to have an environmental. “green” slant. Look for a big gas tax rise to pay for it. They may get what they want with Senate control. Look for a September target. The economy needs $2 trillion a year in new government spending to keep the stock market rising and it will probably happen.

Nonfarm Payroll comes in at a blockbuster 379,000 in February, far better than expected. It's a preview of explosive numbers to come as the US economy crawls out of the pandemic. That’s with a huge drag from terrible winter weather. The headline Unemployment Rate is 6.2%. The U-6 “discouraged worker” rate of still a sky high 11%, those who have been jobless more than six months. Leisure & Hospitality were up an incredible 355,000 and Retail was up 41,000. Government lost 86,000 jobs. See what employers are willing to do when they see $20 trillion about to hit the economy?

Weekly Jobless Claims dive to 712,000 has pandemic restrictions fall across the country, the lowest since November. However, ongoing claims still stand at an extremely high 4.1 million. Total US joblessness still stands at 18 million. Will the pandemic come back to haunt us from these early reopenings?

California Disneyland (DIS) to reopen April 1, lifting a very dark cloud and huge expenses off the company. Cases on the west coast have fallen so dramatically that the state feels it can get away with this. Maybe this is an effort to derail the recall movement against the government. Stock is up 2% in the after-market, which Mad Hedge followers are long. Time to dig out my mouse ears. Keep buying (DIS) on dips.

Oil (USO) soars 3% on an attack on Saudi oil facilities and a building US economic recovery. $69 a barrel is printed. This is setting up as a great short. High prices in a decarbonizing economy have no future. A (USO) $34-$36 put LEAP with a January 2023 maturity might make all the sense in the world here.

Boeing (BA) announced Fist Positive Deliveries, in 14 months, finally turning around the mess with the 737 MAX. United Airlines was the biggest buyer. The perfect storm is finally over. And Boeing is about to snag another giant order, this time from Southwest (LUV). This comes on the heels of similar big order from Alaska Air (ALK). Keep buying (BA) on dips. An upside breakout is imminent.

Consumer Price Index Comes in at 0.4%, and 0.1% ex food and energy. It’s still at a nonexistent level. Rising gasoline prices were a factor, but airline ticket prices remain at all-time lows. I’ll worry about inflation when I see the whites of its eyes. Commodity prices have doubled in a year but show nowhere in the inflation numbers. With a headline Unemployment Rate at 6.1% and a U-6 at 18 million, it's unlikely we’ll see wage any time soon, which is 70% of the inflation calculation.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

It’s amazing how well selling tops and buying bottoms can help your performance. My Mad Hedge Global Trading Dispatch profit reached a super-hot 16.32% during the first half March on the heels of a spectacular 13.28% profit in February. The Dow Average is up a miniscule 8.2% so far in 2021.

It was a total rip your face off rally in the markets last week, so I took off my hedged and covered shorts in the S&P 500 (SPY) and the NASDAQ (QQQ). That leaves me to run my seven remaining profitable positions into the March 19 options expiration.

I also had my hands full running the three-day Mad Hedge Traders & Investors Summit, introducing some 27 speakers to a global audience of 10,000. The speakers’ videos go up on Tuesday at www.madhedge.com.

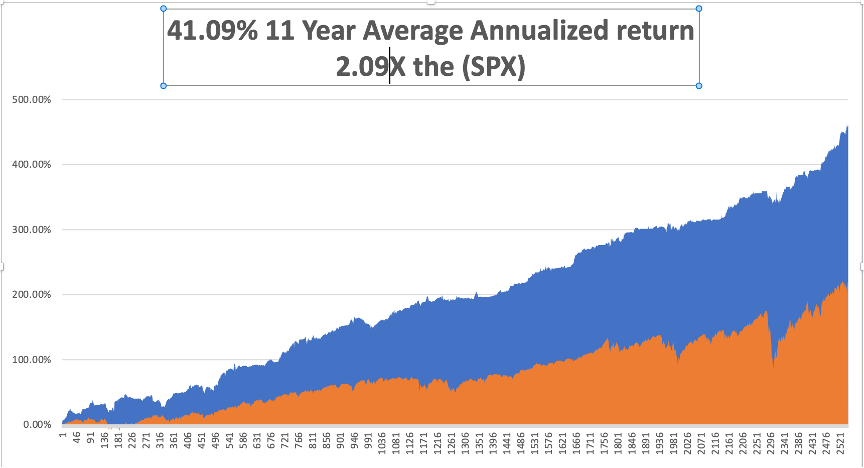

This is my fifth double-digit month in a row. My 2021 year-to-date performance soared to 39.81. That brings my 11-year total return to 465.36%, some 2.12 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 41.09%. I am concerned because numbers any higher than this will look fake.

My trailing one-year return exploded to 122.6%, the highest in the 13-year history of the Mad Hedge Fund Trader. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 29.5 million and deaths topping 535,000, which you can find here. Thankfully, death rates have slowed dramatically, but Obituaries are still the largest sector in the newspaper.

The coming week will be a boring one on the data front.

On Monday, March 15, at 7:30 AM EST, the New York Empire State Manufacturing Index for March is released.

On Tuesday, March 16, at 8:30 AM, US Retail Sales for February are published.

On Wednesday, March 17 at 8:30 AM, we learn Housing Starts for February. At 2:00 PM we get the Federal Reserve interest rate decision and press conference.

On Thursday, March 18 at 8:30 AM, Weekly Jobless Claims are out. We also obtain the Philadelphia Fed Manufacturing Index.

On Friday, March 19 at 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I was saddened to learn of the death of George Schultz, Treasury Secretary and Secretary of State under president Ronald Reagan. He was 101.

George graduated from Yale at the outbreak of WWII and immediately joined the US Marine Corps (Semper Fi) where he used his ample math background to become an anti-aircraft officer. He issued my dad’s unit the useful advice to always lead an attacking Zero fighter by four plane lengths to hit the engine with a machine gun. It’s simple ballistics.

After the war, he used the GI bill to get a PhD from MIT, and later worked for President Eisenhower. He then became the Dean of the Chicago Business School.

I first met George when The Economist magazine sent me to interview him in San Francisco as the CEO of Bechtel Corp, a major engineering and construction company in 1982. The following week, he was drafted by the incoming Reagan administration, where he stayed for eight years. We kept in touch ever since.

When the Soviet Union collapsed in 1991, Schultz as Secretary of State was instrumental in managing the event so that it stayed peaceful….and moved forward. I later flew to Berlin to watch the Russian Army pull its troops out of my former home.

In his later years, George was very active in the Marines Memorial Association where I got to know him very well, he often was wearing his full-dress blues looking as new as if they came out of the factory that day, bringing a fascinating series of military speakers.

As Schultz got older, he couldn’t remember what he knew was top-secret or classified, and what wasn’t. I benefited greatly from that, but kept my mouth shut. However, I learned some amazing things.

He was also very active in arms control and flew to Moscow as recently as 2019. In recent years, I help him to the podium, George grasping my arm and walking his slow shuffle.

George Schultz was a great example of the best leaders that American can produce. He will be missed.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 9, 2021

Fiat Lux

Featured Trade:

(ON EXECUTING MY TRADE ALERTS),

(TEN REASONS WHY STOCKS CAN’T SELL OFF BIG TIME),

(SPY), (INDU), ($COMPQ), (IWM), (TLT), (GME)