Global Market Comments

June 12, 2020

Fiat Lux

Featured Trade:

(WHEN THE BILL COMES DUE)

(SPY), (TLT), (GD), (USO), (HTZ), (JCP)

Global Market Comments

June 12, 2020

Fiat Lux

Featured Trade:

(WHEN THE BILL COMES DUE)

(SPY), (TLT), (GD), (USO), (HTZ), (JCP)

This was a top you could see coming a mile off. Now, the correction for the greatest rally in stock market history has begun. Will it be the greatest correction in history?

It could be.

It was the awful news that the Coronavirus is starting to run away again that started the panic. New cases in Texas and Arizona are growing so fast that the local hospital systems are getting overwhelmed once again. The Armageddon scenario is back on the table once again.

You knew we were in trouble when the stocks of bankrupt companies, like Hertz (HTZ) and JC Penny (JCP) started doubling in a day, even though they have no equity value whatsoever. They were bid up simply because they had low single-digit prices, as bankrupt companies always do.

They were bid up by greater fools and the market just ran out of them.

It wasn’t just equities that got slammed. Oil (USO) suffered a horrific day, down 8.2%. because of burgeoning inventories leftover from a dead-in-the water economy. Bonds rocketed three points and are up an eye-popping 11 points from last week. Even gold (GLD) failed to move, held back by widespread margin calls.

It seems we have returned to the terrors of February-March, the down 2,000 points a day kind. There was barely a rally all day. It basically went straight down. How much more is there to go? Let’s look at the obvious targets in the S&P 500 (SPY) and the distance from the Monday top.

$299 – Down 7.7% from the top – the 200-day moving average and top of the April - May double top

$288.74 – Down 10.9% - The 50-day moving average

$272 – Down 15% - bottom of the April - May double bottom

$262 – Dow 19.4% - Top of the initial rally off the March 23 bottom and the level where a new bear market is declared. Two bear markets in two quarters?

$219 – Down 32.6% - the March 23 low gets retested.

There is quite a lot to chew on here. In the end, it will depend on how much the first Corona wave ramps up after a far too early re-opening. Even if there are no further shutdowns of the economy, a world where consumers are too afraid to leave their homes doesn’t generate a lot of growth or earnings.

When the president says things are great, but you see 5% of normal traffic in the local shopping mall, you want to run a mile.

Forget about the second wave, we haven’t even gotten out of the first wave yet. Corona deaths topped 114,000 today. We could hit 250,000 by August, not a great mall traffic generator.

If the selloff continues, and it probably will until the Q2 earnings are published starting in mid-July, then this is the dip you want to buy. For if the lows hold, we will be at the beginning of a 400% move in the main indexes over the next decade.

To get the depth of the argument why this will happen, please read about the coming Roaring Twenties and the next American Golden Age by clicking here.

Here is what you want to do on this move down:

*Stocks - buy big dips

*Bonds – sell rallies aggressively

*Commodities - buy dips

*Currencies - sell US dollar rallies

*Precious Metals – buy dips

*Energy – stand aside

*Volatility - sell short over $50

*Real Estate – buy dips

And buy LEAPS (Long Term Equity Anticipation Securities), lots of LEAPS. This is where traders have been picking up 500%-1,000% returns this year.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

May 4, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE NEXT BOTTOM IS THE ONE YOU BUY),

(SPY), (SDS), (TLT), (TBT), (F), (GM), (TSLA), (S), (JCP), (M)

It was only a year ago that I was driving around New Zealand with my kids, admiring the bucolic mountainous scenery, with Herb Albert and the Tijuana brass blasting out over the radio. Believe me, the tunes are not the first choice of a 15-year-old.

Today, it is all a distant memory, with any kind of international travel now unthinkable. For me, that is like a jail sentence. It is all a reminder of how well we had it before and how bleak is the immediate future.

Stock traders have certainly been put through a meat grinder. The best and worst months in market history were packed back to back, down 39% and then up 37%. At the March 23 low, the Dow average had fallen by 11,400 in a mere six weeks. Those who lived through the 1929 crash have lost their bragging rights, if there are any left.

However, like my college professor used to say, “Statistics are like a bikini bathing suit. What they reveal is fascinating, but what they conceal is essential.”

Most of the index gains were achieved by just five FANG stocks. Virtually all of the gains were from “stay at home” companies taking in windfalls from cutting-edge online business models. The “recovery” had a good week, and that was about it.

The other obvious development is that if any business was in trouble before the health crisis, you can safely write them off now. That includes retailers like Sears (S), JC Penny’s (JCP), Macy’s (M), almost all brick-and-mortar clothing sellers, and the small and medium-sized energy industry.

The worst economic data points since the black plague are about to hit the tape. Some 30 million in newly unemployed is nothing to dismiss, and that number grows to 40 million if you include discouraged workers.

That is 25% of the workforce, the same as peak joblessness during the great depression. But $14 trillion in QE and fiscal stimulus is about to hit the market too.

Which brings us to the urgent question of the day: What to do now?

It’s a vexing issue because this is not your father’s stock market. This is not even the market we’d grown used to only six months ago. All I can say is that the virology course I took 50 years ago today is worth its weight in gold.

I think you would be mad not to count a second Covid-19 wave into your calculations. This could occur in weeks, or in months, after the summer respite. This makes a second run at the lows a sure thing. I don’t think we’ll make it, but a loss of half the recent gains is entirely possible.

That takes us back down to a Dow Average of 21,000, or an S&P 500 (SPX) of 2,400.

If you are a long term investor looking to rebuild your retirement nest egg, there are only two sectors left in the market, Tech and Biotech & Healthcare. Looking at anything else is both risky and speculative. So, if we do get another meltdown, these are the only areas you should target.

If I am wrong, the market will probably bounce along sideways in a narrow range for months. That is a dream scenario if you pursue a vertical bull and bear call and put option spread strategy that I have been offering up to followers for the past decade.

Pending Home Sales Were Down a Staggering 20.8% in March and off 16.3% YOY. The worst is yet to come. The West, the first into shelter-in-place, was down a monster 26.8%. Prices still aren’t moving because nobody can buy or sell. The way homebuilder stocks like (LEN) and (KBH) are trading, I’d say your home will be worth a lot more in a year when the huge demographic push resumes. I’m not selling.

The 60,000 peak in deaths proposed by the administration only weeks ago is now looking wildly optimistic. Their worst-case scenario of 200,000 deaths, the announcement of which set the March 23 bottom of the Dow Average at 18,200, is now likely.

It will take place when the epidemic peaks in the southern and midwestern states that never sheltered in place or went in late and are coming out early. That second wave may well create a second bottom in stock prices, and that is the one you jump into and buy with both hands.

US Corona Deaths topped 66,000 last week, more than we lost after a decade of the Vietnam War. Total cases exceed one million.

Bank of America sees negative 30% GDP this quarter annualized, so says CEO Brian Moynihan. His economists expect negative 9% in Q3 and plus 30% in Q4. Suffice it to say, this is the ultra-optimistic case. Q4 doesn’t include the millions of businesses that will disappear because the Paycheck Protection Plan is failing so badly. Most government aid will take three to six months to hit the economy.

US GDP crashed 4.8% in Q1, the worst quarter since the depths of the 2008 Great Recession. Q2 will be far worse. We are now officially in recession, which should last 3-4 quarters. But is it already in the price? Next week’s April Nonfarm Payroll report should be a real humdinger.

Ford (F) lost $5 billion in Q2, and there is no guidance about the future. Avoid (F) on pain of death. Late to electric, they may not make it this time. They’re still in the buggy whip business.

Weekly Jobless Claims topped 3.8 million, bringing the six-week total to a staggering 30 million, more than those lost at the peak of the Great Depression. Florida, California, and Georgia led with applications. This implies a U-6 Unemployment rate of 25% with next week’s April Nonfarm Payroll Report. And the Dow Average is up 37% since March 23?

The Bond Market crashed on a Trump threat to default on US Treasury bonds, of which China owns $900 billion. It’s Trump’s retaliation for the Middle Kingdom spawning the Coronavirus, which he calls the “Chinese virus.” The (TLT) dropped three points on the news. Good thing I am triple short a market that is about to get crushed by massive government borrowing.

A glut of imported autos is parked at sea, steaming in circles, awaiting a recovery in the US economy. They are no doubt finding company with imported oil tankers. So many unwanted cars coming in the land-based storage areas were overflowing. It’s tough to see (F) and (GM) recovering from this. Keep buying made in the USA (TSLA) on dips, which is headed to $2,500 a share.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had one of the best weeks in years, up a blistering +8.05%. We are now only 6.67% short of a new all-time high. The 100 new subscribers who came in the previous week are sitting pretty and must think I’m some sort of guru.

My aggressive triple weighting in short bond positions came in big time when Trump threatened to default on US debt. My shorts in the S&P 500 (SPY) helped. I took profits on my last long there the previous week. (SDS), another short play, clawed back some losses.

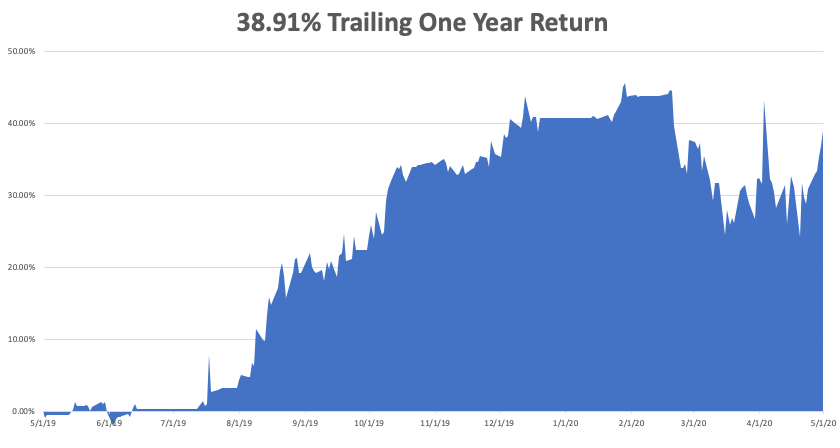

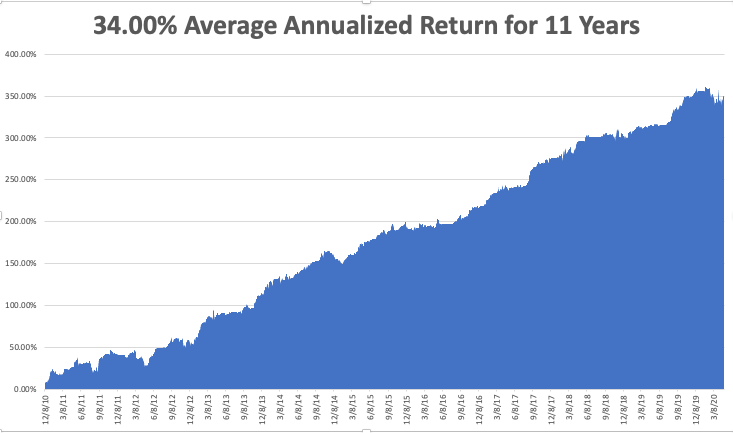

We closed out up a blockbuster +4.55% in April and May is up +2.11%, taking my 2020 YTD return up to only -1.75%. That compares to a loss for the Dow Average of -18.20% from the February top. My trailing one-year return returned to 38.91%. My ten-year average annualized profit returned to +34.00%.

This week, Q1 earnings reports continue and so far, they are coming in much worse than the most dire forecasts. We also get the monthly payroll data, which should be heart-stopping to say the list.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, May 4 at 9:00 AM, the US Factories Orders for March are out and are expected to be disastrous. Berkshire Hathaway (BRK/B) and Eli Lilly (LLY) report.

On Tuesday, May 5 at 11:00 AM, the US Crude Oil Stocks are published and will be another bomb. Netflix (NFLX) and Coca-Cola (KO) report.

On Wednesday, May 6, at 7:15 AM, API Private Sector Employment Report is released. Lan Research (LRCX) and Electronic Arts (EA) announce earnings.

On Thursday, May 7 at 8:30 AM, another horrible Weekly Jobless Claims are out. Bristol Myers Squibb (BMY) reports.

On Friday, May 8, the April Nonfarm Payroll Report is printed, the worst unemployment rate since the Great Depression. AbbVie (ABBV) reports.

As for me, to battle cabin fever, I am setting up a tent in my back yard and staying there tonight, just to change the scenery. The girls need one more campout to qualify for camping merit badge, an important Eagle Scout one, and this will qualify.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

February 28, 2019

Fiat Lux

Featured Trade:

(WHY ETSY KNOCKED IT OUT OF THE PARK),

(ETSY), (AMZN), (WMT), (TGT), (JCP), (M)

I wrote to readers that I expected online commerce company Etsy to “smash all estimates” in my newsletter Online Commerce is Taking Over the World last holiday season, and that is exactly what they did as they just announced quarterly earnings.

To read that article, click here.

I saw the earnings beat a million miles away and I will duly take the credit for calling this one.

Shares of Etsy have skyrocketed since that newsletter when it was hovering at a cheap $48.

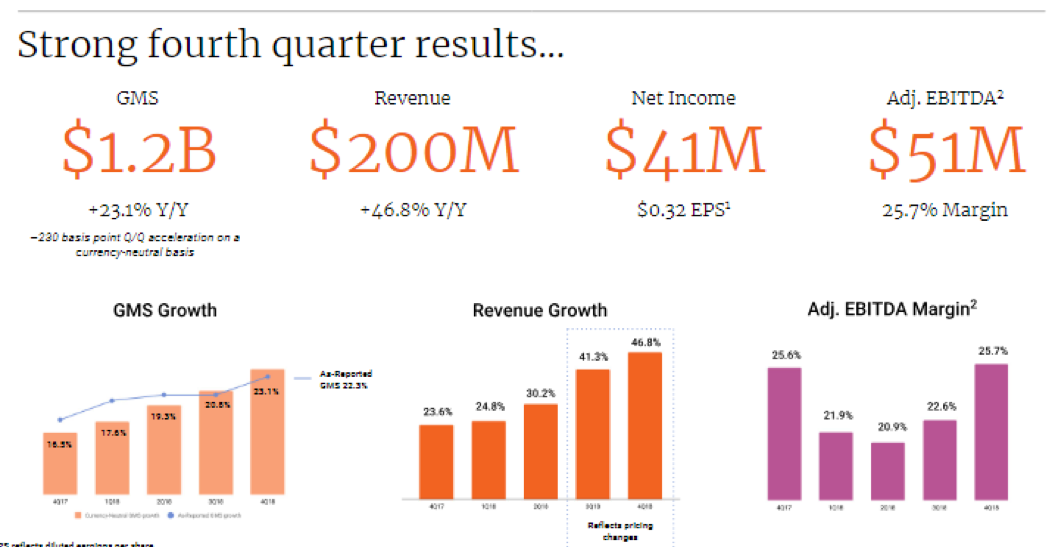

The massive earnings beat spawned a rip-roaring rally to over $71 - the highest level since the IPO in 2015.

Three catalysts serving as Etsy’s engine are sales growth, strength in their core business, and high margin expansion.

Sales growth was nothing short of breathtaking elevating 46.8% YOY – the number sprints by the 3-year sales growth rate of 27% signaling a firm reacceleration of the business.

The company has proven they can handily deal with the Amazon (AMZN) threat by focusing on a line-up of personalized crafts.

Some examples of products are stickers or coffee mugs that have personalized stylized prints.

This navigates around the Amazon business model because Amazon is biased towards high volume, more likely commoditized goods.

Clearly, the personalized aspect of the business model makes the business a totally different animal and they have flourished because of it.

Active sellers have grown by 10% while active buying accounts have risen by 20% speaking volumes to the broad-based popularity of the platform.

On a sequential basis, EPS grew 113% QOQ demonstrating its overall profitability.

Estimates called for the company to post EPS of 21 cents and the 32 cents were a firm nod to the management team who have been working wonders.

Margins were healthy posting a robust 25.7%.

The holiday season of 2018 was one to reminisce with Amazon, Target (TGT), and Walmart (WMT) setting online records.

Pivoting to digital isn’t just a fad or catchy marketing ploy, online businesses harvested the benefits of being an online business in full-effect during this past winter season.

Etsy’s management has been laser-like focusing on key initiatives such as developing the overall product experience for both sellers and buyers, enhancing customer support and infrastructure, and tested new marketing channels.

Context-specific search ranking, signals and nudges, personalized recommendations, and a host of other product launches were built using machine learning technology that aided towards the improved customer experience.

New incremental buyers were led to the site and returning customers were happy enough to buy on Etsy’s platform multiple times voting with their wallet.

The net effect of the deep customization of products results in unique inventory you locate anywhere else, differentiating itself from other e-commerce platforms that scale too wide to include this level of personalization.

Backing up my theory of a hot holiday season giving online retailers a sharp tailwind were impressive Cyber Monday numbers with Etsy totaling nearly $19,000 in Gross Merchandise Sales (GMS) per minute marking it the best single-day performance in the company’s history.

Logistics played a helping hand with 33% of items on Etsy capable to ship for free domestically during the holidays which is a great success for a company its size.

This wrinkle drove meaningful improvements in conversion rate which is evidence that product initiatives, seller education, and incentives are paying dividends.

Overall, Etsy had a fantastic holiday season with sellers’ holiday GMS, the five days from Thanksgiving through Cyber Monday, up 30% YOY.

Forecasts for 2019 did not disappoint which calls for sustained growth and expanding margins with GMS growth in the range of 17% to 20% and revenue growth of 29% to 32%.

Execution is hitting on all cylinders and combined with the backdrop of a strong domestic economy, consumers are likely to gravitate towards this e-commerce platform.

Expanding its marketing initiatives is part of the business Josh Silverman explained during the conference call with Etsy dabbling in TV marketing for the first time in the back half of 2018, and finding it positively impacting the brand health metrics particularly around things like intending to purchase.

However, Etsy has a more predictable set of marketing investments through Google that offers higher conversion rates and the firm can optimize to see how they can shift the ROI curve up.

Etsy can invest more at the same return or get better returns at the existing spend from Google, it is absolutely the firm's bread and butter for marketing, particularly in Google Shopping, and some Google product listing ads.

With all the creativity and reinvestment, it’s easy to see why Etsy is doing so well.

Online commerce has effectively splintered off into the haves and have-nots.

Those pouring resources into innovating their e-commerce platform, customer experience, marketing, and social media are likely to be doing quite well.

Retailers such as JCPenney (JCP) and Macy’s (M) have borne the brunt of the e-commerce migration wrath and will go down without a fight.

Basing a retail model on mostly physical stores is a death knell and the models that lean feverishly on an online presence are thriving.

At the end of the day, the right management team with flawless execution skills must be in place too and that is what we have with Etsy CEO Josh Silverman and Etsy CFO Rachel Glaser.

Buy this great e-commerce story Etsy on the next pullback - shares are overbought.

Mad Hedge Technology Letter

November 14, 2018

Fiat Lux

Featured Trade:

(I NAILED IT)

(AMZN), (GOOGL), (FDX), (UPS), (JCP)

Having been in this market for yonks, ages, and even a coon?s age, I have seen trading strategies come and go.

First, there was the nifty fifty during the 1960?s. Junk bonds had their day in the sun. Then portfolio insurance was all the rage.

Oops!

While the dollar was weak, international diversification was the flavor of the day. After foreign stocks turned bitter, the IPO mania and the Dotcom bubble of the nineties followed.

Macro trading dominated the new Millennium until the high frequency traders took over.

What is the cutting edge management strategy today?

According to my friend, Anthony Scaramucci, of Skybridge Capital, activist shareholder trading now has the unfair advantage.

Anthony, known as the ?Mooch? to his friends, is so convinced of the merit of this bold, in-your-face approach that he has devoted nearly 40% of his assets to this aggressive posture.

That is no accident.

Have you ever heard the term ?unintended consequences?? Scaramucci argues that The Financial Stability Act of 2010, otherwise known as Dodd-Frank produced that effect with a turbocharger.

The Act brought in a raft of new shareholder rights intended to help Mom & Pop. But activist investors have, so far, been the prime beneficiaries of the reform, using the new regulations to shake down companies for quick profits.

Historic low interest rates are allowing them to leverage up at minimal cost, increasing their firepower.

These include known sharks (once spurned as ?green mailers?) like my former neighbor, Carl Icahn, and his younger, more agile competitor, Bill Ackman.

They can simply buy a small number of shares in a target company and demand a management change, share buy backs, the spinning off of assets, several seats on the board, and even making allegations of criminal activity, which are often unfounded.

A message from Icahn on the voicemail is not something management is eager to hear.

He even shook down Apple (AAPL) last year, with great success, harvesting a near double on the trade.

This is why names like Herbalife (HLF), Netflix (NFLX), and JC Penny?s (JCP) are constantly bombarding the airwaves.

The net result of this is that savvy activist shareholders have effectively replaced the traditional ?buy and hold? strategy as a way to add alpha, or outperformance.

This has enabled activist oriented hedge funds to beat the pants off of traditional macro hedge funds because many historical cross asset relationships they follow have broken down.

Tell me about it!

Suddenly, the world no longer makes sense to them and has apparently gone mad, at the investors? expense. Long/short equity managers, which comprise 43% of the funds out there, are also underperforming for the sixth consecutive year.

The activist managers themselves justify their often harsh actions by arguing that individual shareholders can ride to riches on their coattails. Shaking up management can result in better-run companies, even if it is at the point of a gun.

Activism accelerates evolution, breaks up clubby boards of insiders, and enhances the bottom line. Corporations can be forced to retool and restructure.

How does the individual investor get involved in the new wave of activist investors? The short answer is that they don?t. There are few, if any, such exchange traded funds (ETFs) in existence.

Doing the quantitative screens to generate short lists of potential activist targets, and then listening to the jungle telegraph regarding who is coming into play, are well beyond the resources of your average Joe.

You can try to give your money to the best activist managers. But they are either closed to new investors, or have very high minimum initial investments, often in the $1-$10 million range.

If you are lucky enough to get your dosh in, you will find the talent very expensive. Activist funds are one of the last redoubts of the old 2%/20% management fee and performance bonus structure. And ?hockey stick? bonus schedules are not unheard of.

When I ran my old hedge fund, we made 40% a year like clockwork. I took the first 10%, the limited partners the remaining 30% and they were thrilled to get it.

And you wonder why the small guys feel the market is rigged.

The activist trend won?t last forever. Interest rates will inevitably rise, making the strategy expensive to finance. If the stock market keeps rising, as I expect, then cheap targets will become as scarce as hen?s teeth.

Eventually, gobs of money will pour into the strategy, compressing returns as the Johnny-come-latelys pile in. In the end, trading around activist shareholders will get tossed into the dustbin of history, along with all the other investment fads.

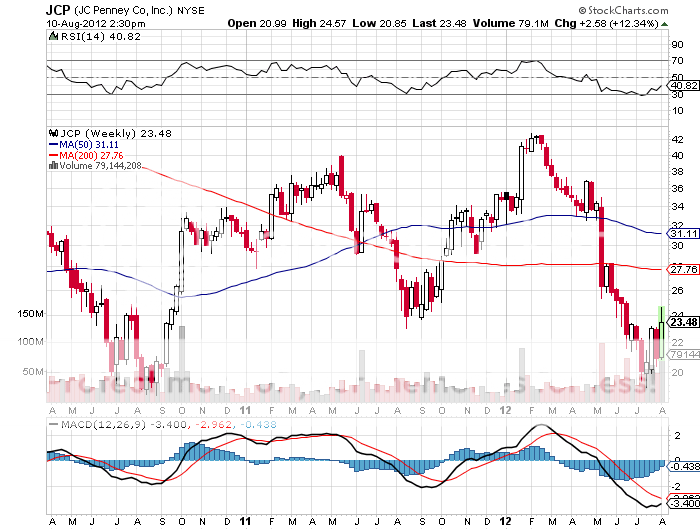

Checking in With the ?Mooch?The stock of the day last Friday was, no doubt, JC Penny (JCP), one of the most heavily shorted stocks in the market, which announced Q2, 2012 earnings. Despite a huge miss, the stock soared by 20% because the losses were not as bad as many expected. This leads to the question of whether traders should double up or bail on the existing short positions.

As the dispassionate analyst that I am, who only looks at numbers in the cold, harsh light of reality, the figures could not have been more disappointing. Q2 EPS showed a loss of $0.37/shares versus an expected loss of $0.25. Revenues came in at $3 billion compared to an estimate of $3.2 billion.

Worst of all, same store sales cratered by -21.7% YOY while traffic was off -12%. This is despite offering kids free haircuts. Gross margins shrank and Internet sales were off 30%. To top it all, the company announced that it would no longer provide future guidance. Moody?s immediately followed with a downgrade of the company?s debt from Ba1 to Ba3.

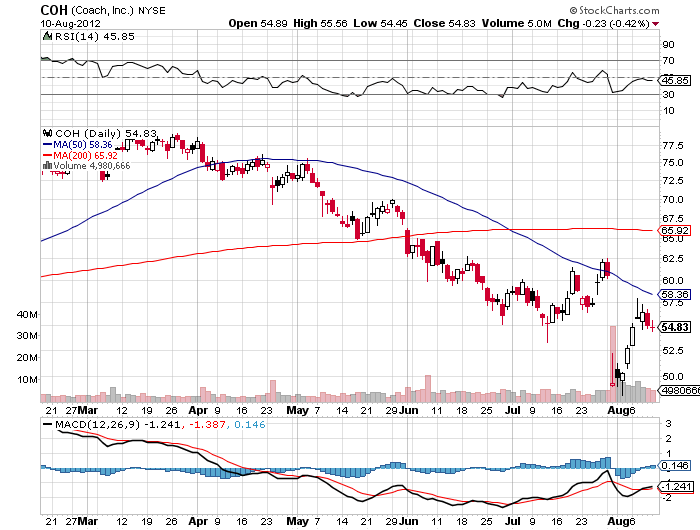

The new CEO, Ron Johnson, has no retail experience and says he needs 4 years for a turnaround. In the meantime, competitor Macys is making good money and selling at 11X earnings with the best CEO in business. Well established luxury brand Coach (COH) sells for a 14X multiple. If you fall in love with retail and absolutely have to be in this sector, there are far better fish to fry. Personally, I would rather lie down and take a long nap.

The hedgies still in this name are clearing gunning for a chapter 11. So a chance to sell again 20% higher than yesterday in the face of bad news has to be attractive. But with such a huge share of the company?s outstanding shares already sold short, the risk reward here is not great. I would have ridden the stock down from $40 to $20 and then said, ?Thank you very much?, rather than chase the last few dollars just to prove I?m right.

The company only has to get a little right to trigger a bigger short squeeze. Technicians were clearly focused on a potential multiyear double bottom on the charts. Besides, I was never one for sloppy seconds, and don?t need a haircut.

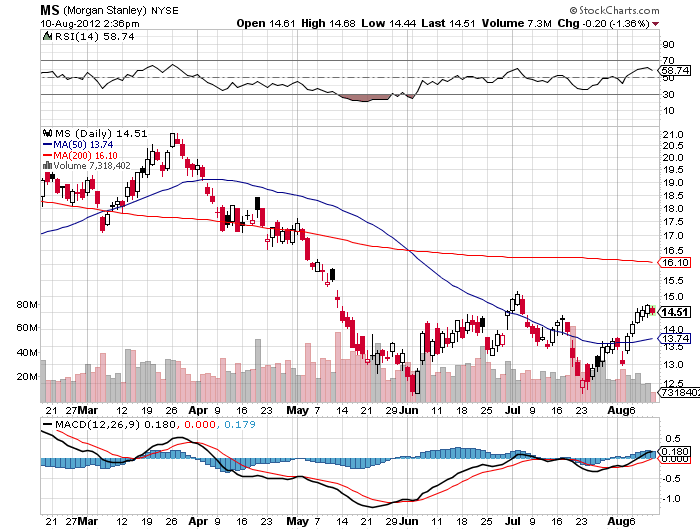

Looking for a better stock to sell short at the top of the recent range with dire fundamentals? I?d rather short Morgan Stanley on an up day.

JC Penny: Better Fish to Fry