Global Market Comments

November 29, 2024

Fiat Lux

Featured Trade:

(The Mad DeCEMBER traders & Investors Summit is ON!)

(CHINA’S VIEW OF CHINA),

(FXI), (BIDU), (BABA), (JD)

Global Market Comments

November 29, 2024

Fiat Lux

Featured Trade:

(The Mad DeCEMBER traders & Investors Summit is ON!)

(CHINA’S VIEW OF CHINA),

(FXI), (BIDU), (BABA), (JD)

There was so much enthusiasm for China only a month ago.

A stimulus package was announced, a massive short-covering rally ensured, and finally, after a three-year hiatus, China was back in play. Several hedge funds announced major commitments to the Middle Kingdom.

Here we are only three weeks after the US presidential election, and China now looks so much rubble. Asst prices returned to their starting points. The hedge funds have so much mud on their faces. It’s back to a long wait.

Which gives us all plenty of time to think about what China is really all about.

I ran into Minxin Pei, a scholar at the Carnegie Endowment for International Peace, who imparted to me some iconoclastic, out-of-consensus views on China’s position in the world today.

He thinks that power is not shifting from West to East; Asia is just lifting itself off the mat, with per capita GDP at $12,969, compared to $81,695 in the US.

We are simply moving from a unipolar to a multipolar world. China is not going to dominate the world, or even Asia, where there is a long history of regional rivalries and wars.

China can’t even control China, where recessions lead to revolutions, and 30% of the country, Tibet and the Uighurs want to secede.

China’s military is almost entirely devoted to controlling its own people, which makes US concerns about their recent military build-up laughable.

All of Asia’s progress, to date, has been built on selling to the US market. Take us out, and they’re nowhere.

With enormous resource, environmental, and demographic challenges constraining growth, Asia is not replacing the US anytime soon.

There is no miracle form of Asian capitalism; impoverished, younger populations are simply forced to save more because there is no social safety net.

Try filing a Chinese individual tax return, where a maximum rate of 40% kicks in at an income of $35,000 a year, with no deductions, and there is no social security or Medicare in return.

Ever heard of a Chinese unemployment office or jobs program?

Nor are benevolent dictatorships the answer, with the despots in Burma, Cambodia, North Korea, and Laos thoroughly trashing their countries.

The press often touts the 600,000 engineers that China graduates, joined by 350,000 in India. In fact, 90% of these are only educated to a trade school standard. Asia has just one world-class school, the University of Tokyo.

As much as we Americans despise ourselves and wallow in our failures, Asians see us as a bright, shining example for the world.

After all, it was our open trade policies and innovation that lifted them out of poverty and destitution. Walk the streets of China, as I have done for four decades, and you feel this vibrating from everything around you.

I’ll consider what Minxin Pei said next time I contemplate going back into the (FXI) and (EEM).

China: Not All Its Cracked Up to Be

Mad Hedge Technology Letter

September 30, 2024

Fiat Lux

Featured Trade:

(CHINESE TECH GLITTERS IN THE SHORT-TERM)

(BABA), (JD), (PDD), (BIDU)

The bazookas have been unloaded, and the results are big.

The aftermath is reverberating through the rest of the world’s equity markets.

The Chinese economy is in the dumps and the Chinese communist party is using every tool in the proverbial toolkit to pull them out of their slump.

Juxtapose that in the face of a demographic time bomb and we could say that it is in the nick of time.

Now that we have decades of data on the issue, the Chinese economy has major structural issues and instead of fixing it, they are throwing liquidity at it.

Chinese purchasing power is about to drop through the toilet pipes, but I believe bellwether stocks like Alibaba (BABA), JD.com (JD), Pinduoduo (PDD), and Baidu (BIDU) will perform quite well.

China is all about ecommerce at the retail level anyway and Alibaba will be able to reverse a years-long slump on the back of Beijing’s sweeping stimulus measures.

Flooding the system with liquidity will paper over the cracks and should get consumers out and about instead of eating instant noodles in their little apartments.

Retail is now moving in the right direction again.

Although, long term this does nothing to address the major structural issues in the system, the short-term transfusion should help putting money in consumer’s pockets and liquidity on Chinese corporates will outperform.

Market-support measures initiated by the People’s Bank of China included mortgage rate cuts and an unprecedented $114 billion stock-buying facility.

The renewed positive market sentiment for Alibaba reflects its resilience after struggling in recent years, owing to Beijing’s 32-month crackdown on Big Tech firms and the mainland’s shaky post-pandemic economic recovery.

BABA lost nearly half their value over the past five years.

China’s largest operator of online shopping platforms and a major domestic artificial intelligence (AI) technology player, Alibaba recently won praise from the State Administration for Market Regulation for complying with rectification measures, ending more than three years of regulatory scrutiny that has hung over the company’s operations.

Alibaba’s cloud computing services unit last week announced at an event in Hangzhou the release of more than 100 large language models – the deep-learning technology underpinning generative AI applications like ChatGPT – to the global open-source community and a new text-to-video model, as the company showed its rapid progress in this field.

Earlier this month, Alibaba founder Jack Ma called on employees of the business empire he created 25 years ago to “believe in the future” and “believe in the market” amid stiff competition.

The Chinese Communist Party and their heavy handed approach has a lot to do with many tech companies fizzling out.

It is impossible to really kick start growth when they are suppressing it.

However, now is the time when the government has realized they are overdoing it and have unleashed the animal spirits.

Ultimately, the Chiense government is the arbiter of who gets to do business and how well in China.

In the short-term, Chinese tech stocks will outperform American tech stocks.

Chinese tech stocks are cheap by almost every metric – buy the dip in Chinese tech.

Global Market Comments

November 5, 2021

Fiat Lux

Featured Trade:

(NOVEMBER 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(BRKB), (COIN), (IWM), (GOOGL), (MSFT), (MS), (GS), (JPM),

(BABA), (BIDU), (JD), (ROM), (PYPL), (FXE), (FXA), (FXB), (CRSP), (TSLA), (FXI), (BITO), (ETHE), (TLT), (TBT), (BITO), (CGW)

Below please find subscribers’ Q&A for the November 3 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon

Valley.

Q: Have you considered buying Coinbase (COIN)?

A: Yes, we actually recommended it as part of our Bitcoin service in the early days back in July. It’s gone up 62% since then, right along with the Bitcoin move itself. So yeah, buy (COIN) on dips—and there will be dips because it will be at least triple the volatility of the main market. And be sure to dollar cost average.

Q: Do you think the breakout in small caps (IWM) will hold and, if so, should we focus on small-c growth?

A: Yes it will hold, but no I would focus on the big cap barbells, which will lead this rally for the next 6 months. And there you’re talking about the best of tech which is Google (GOOGL) and Microsoft (MSFT), and the best of financials which is Morgan Stanley (MS), Goldman Sachs (GS), and JP Morgan (JPM).

Q: Why not time the webinar for after the FOMC? What will be the market reaction?

A: Well, first of all, we already know what they’re going to say—it’s been heavily leaked in the last week. The market reaction will be initially a potential sharp down move that lasts a few minutes or hours, and then we start a grind up for the next two months. So that's why I wanted to be 80% leverage long going into this. Second, we have broadcast this webinar at the same time for the last 13 years and if we change the time we will lose half our customers.

Q: Why do you always do debit spreads?

A: They’re easier for beginners to understand. That’s the only reason. If you’re sophisticated enough to do a credit spread, the results will be the same but the liquidity will be slightly better, and you can also apply that credit to meet your margin requirements. We have a lot of basic beginners signing up for our service in addition to seasoned pros and I always encourage people to do what they're most comfortable with.

Q: Are you still comfortable with the Morgan Stanley (MS) and Berkshire Hathaway (BRKB) positions?

A: I expect both to go up 10-20% by March, so that’s pretty comfortable. By the way, if you have extremely deep in the money call spreads on Goldman Sachs or Morgan, consider taking profits on those and rolling your strikes up. If you have like the $360-$380 vertical bull call spread in Goldman Sachs, realize that gain and roll up to the $420-$430 March position in Goldman Sachs—that will give you another 100% profit by March. With the $360-$ 380s, you have like 97% of the profit already in the price, there’s no leverage left and no point in continuing, you can only go down.

Q: What should I do with my China position?

A: Sell all your positions in China, realize all the losses now so you can offset those with all the huge profits on all your other positions this year. There I’m talking about Ali Baba (BABA), Baidu (BIDU), and (JD), which have been absolutely hammered anywhere from down 50% to down 70%. And do it now before everyone else does it for the same reasons.

Q: Thoughts on Paypal (PYPL) lately?

A: The stock is out of favor as money is moving out of PayPal into newer fintech stocks. The move down is totally unjustified and screaming long term buy here, but for the short-term investors are going to raid the piggy bank, sell the PayPal, and go into the newer apps. This has been my biggest money-losing trade personally this year because PayPal long-term has a great story.

Q: Will earnings fall off next year due to prior year comparisons or supply chain?

A: No, if anything, earnings are accelerating because supply chain problems mean you can charge customers whatever you want and therefore increase margins, which is why the stock market is going up.

Q: Long term, what would your wrong strikes be?

A: I would say don’t get greedy. I’m doing the ProShares Ultra Technology (ROM) $120-$125 call spread for May expiration—the longest expiration they offer. That gives you about 100% return in 6 months; 100% is good enough for me because then I’ll do the same thing again in May and get another 100%. What’s 100% x 100%? It’s 400% because you’re reinvesting a much larger capital base the second time around. If a 100% profit in six months is not enough for you then you are in the wrong line of business.

Q: Do you think Ethereum (ETHE) has long-term potential upside?

A: Yes, is a 10X move enough? We just had a major new high in Ethereum because they made moves to limit the production of new Ethereum. Ethereum is the superior technology because its architecture avoids the code repeats that Bitcoin does and therefore only uses a third of the electricity to create. But Bitcoin is attracting the big institutional cash flows because they have an early mover advantage. By the way, how much electricity does crypto mining consume? The entire consumption of Washington state in a year, so it’s a big deal.

Q: What should I do about Crisper Therapeutics (CRSP)?

Crispr Therapeutics (CRSP) is my other disaster for this year because ignored the move up to $170—we’re now back into the $90’s again. So, I have 2023 LEAPS on that; I’m going to keep them, I’ve already suffered the damage, but the next time it goes up to $170 I’m selling! Once burned, twice forewarned. And part of the problem with the whole biotech sector is we are now in the back end of the pandemic and anything healthcare-related will get hit, except for the vaccine stocks like Pfizer (PFE) which are still making billions and billions of dollars.

Q: I bought Baidu (BIDU) and Alibaba (BABA) years ago at a much lower price and I'm still up quite a lot; what should I do?

A: If you have the big cushion, I would keep them and look for #1 recovery in the Chinese economy next year and #2 for the government to back off from their idiotic anticapitalism strategy because it’s costing them so much money.

Q: Is Robinhood (HOOD) a good LEAP candidate?

A: Only on a really big dip, and then you want to go out two years. With a stock that’s volatile as hell like Robinhood and could drop by half on no notice, so you only buy the big dips. It’s not a slowly grinding upward stock like Goldman Sachs (GS) and Morgan Stanley (MS) where you can add LEAPS now because you know it’s going to keep grinding up.

Q: How can Morgan Stanley go up when the chief strategist is bearish?

A: Their customers aren't listening to their chief strategist—they’re buying. And the volume of the stock, which is where Morgan Stanley makes money, is going through the roof, they’re making record profits there. And I've got Morgan Stanley stock coming out of my ears in LEAPS and so forth.

Q: What are 5 stocks you would buy right now?

A: Easy: Google (GOOGL), Microsoft (MSFT), Morgan Stanley (MS), Goldman Sachs (GS), and JP Morgan (JPM). Buy whatever is down that day. They’re all going up.

Q: Too late to buy Tesla (TSLA) calls?

A: Yes, it is. Tesla has a long history of 40% corrections; we had one that ended in May, and then it doubled (and then some). So yeah, too late to buy the calls here. Go back and read my research from May which said buy the stock and you get a car for free—and that worked again, except this time, you can get three free Tesla’s. A lot of subscribers have sent me pictures of their Teslas they got for free on my advice; I’m probably the largest salesman for Tesla for the last 10 years and all I got out of it was a free Powerwall (the red one)..

Q: How much higher do you think semiconductor companies will go?

A: Higher but it’s impossible to quantify. You’re getting very speculative short-term buying in there. So, I think it continues to the rest of the year, but with chips, you never know.

Q: Would you be buying Crispr Therapeutics (CRSP) at these levels?

A: Yes, but I would either just buy the stock and not be dependent on the calendar or buy a 2 ½ year LEAP and get an easy double on that.

Q: What about the currencies?

A: I don’t see much action in the currencies as long as the US is raising interest rates. I think the Euro (FXE), the Aussie (FXA), and the British pound (FXB) will be dead for the time being. Nobody wants to sell them but nobody wants to buy them either when you’re looking at a potential short term rise in the dollar from rising interest rates.

Q: What stable coins are the right answer for cryptocurrency?

A: The US dollar stable coin, but for price appreciation, you’re really looking at Bitcoin and Ethereum. Stable coins are stable, they don’t move; you want stuff that’s going to go up 5, 10, or 20 times over the next 10 years like Bitcoin (BITO) and Ethereum (ETHE). That is my crypto answer.

Q: What should I do about the iShares 20 Plus Year Treasury Bond ETF (TLT) $135-$140 put spread expiring in January?

A: If we get another run down to the $141 level that we saw last month, I would come out of all short treasury positions because you’re starting to run into time decay problems with the January expirations. And in case we remain in a range for some reason, I would be taking profits at the bottom end of the range. It was my mistake that I didn’t grab those profits when we hit $141 last time. So don’t let profits grow hair on them, they tend to disappear. We lost six months on this trade due to the delta virus and the mini-recession it brought us.

Q: Will there be accelerated tech selling in December because of the new tax rates?

A: What new tax rates? There has been no new tax bill passed and even if there were, I think people wouldn’t tax sell this year because the profits are enormous. They would rather do any selling in January at higher prices and then defer payment of those taxes by 18 months. I don’t think there will be any tax issues this year at all.

Q: What’s your return on solar power investments?

A: My break-even was four years because our local utility, PG&E, went bankrupt and the only way they're getting out of bankruptcy is raising electricity prices by 10% a year. It turns out that as a result of global warming, the panels have operated at a higher efficiency as well, so we’re getting a lot more power output than originally expected. Now I get free electricity for the remaining 20-year life of the panels which is great because with two Tesla’s and all-electric heating and air conditioning I use a lot of juice. My monthly bill is a sight to behold. I also power the 20 surrounding houses and for that PG&E pays me $1,800 a month.

Q: Do you see China (FXI) invading Taiwan as a potential threat to the market?

A: China will never invade Taiwan. They own many of the companies they're already in, they de facto control Taiwan government from a distance; they would not risk the international consequences of an actual invasion. And we have the US seventh fleet there to stop exactly that. So, they can make all the noise they want but nothing will come of it. I’ve been watching this for 50 years and nothing has ever happened.

Q: Would you buy ProShares Ultrashort 20+ Treasury ETF (TBT) here?

A: Absolutely, with both hands, all I can get.

Q: Can you recommend any water ETF opportunity?

A: Yes there is one I wrote a piece on last month. It’s the Claymore S&P Global Water Index ETF (CGW).

Q: How long can you hold the (TBT) before time decay hurts?

A: It doesn’t hurt, the cost of the TBT is two times the 10-year rate. So that would be 3%, plus 1% a year for management fees, and that’s your slippage on the TBT in a year right now—it’s 4%. Remember if you’re short the bond market, you have to pay the coupon when you’re short. Double the bond market and you have to pay double the coupon.

Q: Is the ProShares Bitcoin Strategy ETF (BITO) a good alternative to buying bitcoin?

A: I would say yes because I’ve been watching the tracking on that very carefully and it’s pretty damn close. Plus there’s a lot of liquidity there, so yeah, buy the (BITO) ETF on dips and dollar cost average.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 22, 2021

Fiat Lux

Featured Trade:

(OCTOBER 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(DIS), (TLT), (TBT), (FXI), (BABA), (BIDU), (JD), (USO), (JPM), (MS), (GS), (BITO), ($BTCUSD)

Below please find subscribers’ Q&A for the October 20 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon Valley.

Q: Why are stocks so high? Won’t inflation hurt companies?

A: Inflation hurts bonds (TLT), not companies, which is why we are short the bond market and have been short for most of this year. Inflation actually helps companies because it allows them to raise prices at a faster rate. The ability to raise prices is the best that it’s been in 45 years, and that is enabling them to either maintain or increase profit margins.

Q: Where is all this liquidity coming from to drive the stocks high after the Fed ends Quantitative easing?

A: In the last 20 years, the liquidity of the US has gone from 6% of GDP to 47% of GDP. That is an enormous increase, and most of that money has gone into stocks and real estate, which is why both have been on a tear for the last 11 years. And I expect that to continue; the Fed isn’t even hinting at taking liquidity out of the system until well into 2023. On top of that, you have corporate profit exploding from $2 trillion last year to $10 trillion this year, adding another $8 trillion to the system, and outpacing any Fed taper by a five to one margin. Corporations alone are using these profits to buy back more than $1 trillion of their own stock this year.

Q: I’m hearing so much about the supply chain problems these days. Is that just a short-term fixable problem or a long-term structural one?

A: Absolutely it’s short-term. This actually isn’t a pandemic-related problem but a private capital investment one. It’s being caused by the record growth of the US economy which is sucking in more imports than it has ever seen before. We’ve actually exceeded pre-pandemic levels of imports a while ago. Import infrastructure isn’t big enough to handle it. If it was there wouldn’t be enough truckers to handle it. We had a shortage of 50,000 truckers before the pandemic, now we’re short 100,000. Some of these guys are making up to $100,000 a year, not bad for a high school level education. Expect it to get worse before it gets better, but it will get better eventually. That is why Amazon is having trouble, because supply chain problems may bring a weak Christmas, which is the most profitable time of year for them. If we get any big selloff at Amazon for this reason, you want to buy that bottom because it’ll double again in 3 years.

Q: Walt Disney (DIS) has pretty much sideways the whole year around $70, is this going down or should I buy?

A: I would look to buy but I would buy an in-the-money LEAPS, like a $150-$170 one year out. Disney’s been hit with a lot of slowdowns lately, slowdowns with park reopening, movie releases, new streaming customers. But these are all temporary slowdowns and will pick up again next year. Disney is the classic reopening play, so you will get another bite at the apple with a second reopening. Maybe “bite of the mouse” is a better metaphor.

Q: Global growth is down because of China (FXI) with their PMI under 50; do you think they will drag down the entire global economy in 2022?

A: No, if we recover, their largest customer, they will recover too. Remember their pandemic cases are only a tiny fraction of what ours were, some 4,000 or so, and their economy is still export-driven. You can't have major port congestion in Los Angeles and a weak economy in China, those are just two ends of one chain. I would look for a recovery in China next year. As for the stocks, I don’t know because that’s an entirely political issue; Baidu (BIDU), (JD), and Alibaba (BABA) are still getting beaten like a redheaded stepchild. We don’t know when that’s going to end; it’s an unknown. So, stand aside on Chinese plays, especially when the stuff at home is so much better with all these financials and tech stocks to invest in.

Q: What do you think about meme stocks?

A: I think you should avoid them like the plague. When there are so many good quality stocks with long term uptrends, why bother dumpster diving? You’re better off buying a lottery ticket.

Q: Which US bank should I invest in?

A: If you want the gold standard, you buy JP Morgan (JPM) which just announced blowout earnings. If you want a broker, go for Morgan Stanley (MS), which also just announced blowout earnings last week. And I want you to make my monthly pension payment secure, as it comes from Morgan Stanley. Keep those checks coming!

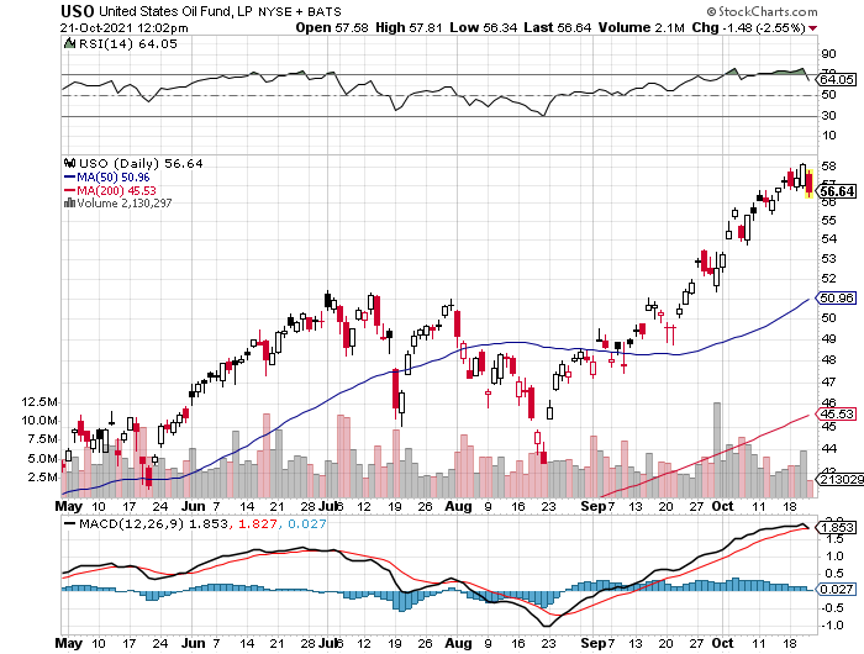

Q: Are we headed to $150 oil (USO)?

A: No, what we’re seeing here is a short-term spike in prices due to supply chain problems, OPEC discipline, a booming economy, and Russia trying to squeeze Europe on energy supplies. I don’t see it continuing much per year as the stocks could be popping out, so avoid oil and energy plays. The solar plays, like (TAN), (FSLR), and (SPWR) on the other hand, all look like they have miles to go.

Q: You said in your Webinar that you can still get a 50% Return on the United States Treasury Bond Fund (TLT) LEAPS. Can you give me the specifics?

A: If you went a year out on Tuesday when I recorded this webinar, you could buy the (TLT) October 2022 $150-$150 vertical bear put spread for $3.40 for a maximum profit on expiration at $5.00 of $47%. That’s where you buy the $155 put and sell short the $150 put against it. Since then, bonds have fallen by $3.00, and it is now trading at $3.60 giving you a 39% return. Try to establish this position on the next (TLT) rally.

Q: What is your yearend target for Bitcoin?

A: Now that we have broken the old high at $66,000, we should be able to make it to $100,000 by January. The SEC approving that new ProShares Bitcoin Strategy ETF (BITO) ETF unlocks trillions of dollars which can now go into Bitcoin, those regulated by the Investment Company Act of 1940. Crypto is now the fastest-growing segment of the financial markets. It’s inflation that driving this, and the Fed is throwing fuel on the fire by taking no action in the face of a red hot 5.4% Consumer Price Index. Even if the Fed does taper, the action will be more than offset by the massive $8 trillion increase in corporate profits. Companies are not only buying their own stocks, they are also using these profits to buy Bitcoin. I see this as a Bitcoin node myself. Be sure to dollar cost average your position by putting in a little bit of money every day because Bitcoin is wildly volatile, up 140% since August 1. By the way, it’s not too late to subscribe to the Mad Hedge Bitcoin Letter, which we are taking down from the store on Monday for a major upgrade by clicking here. We are raising prices after that.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on the paid service you are currently in (GLOBAL TRADING DISPATCH, TECH LETTER, or BITCOIN LETTER), then select WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good luck and stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

March 26, 2021

Fiat Lux

Featured Trade:

(AVOID THIS KOREAN ECOMMERCE COMPANY)

(CPNG), (AMZN), (GRUB), (UBER), (JD), (SHOP), (MELI)

I might characterize Coupang (CPNG) as something akin to China’s JD.com.

It's an e-commerce company that has fulfillment solutions, not dissimilar to Amazon (AMZN) Fulfillment. They also have storefronts that they provide for businesses, which isn't dissimilar to say, a Shopify (SHOP).

Even combining aspects of Amazon and Shopify are there but they don’t have the powerful AWS cloud business.

Similar to JD.com (JD), which is a Chinese e-commerce platform, Coupang has differentiated itself by owning its entire logistics and delivery system.

What is different about Coupang versus the other players in Korean e-commerce is that they own their own inventory for the most part.

That means that they have inventory sitting on their balance sheets.

They have responsibility for pushing that through. But it also means, since they directly negotiate with the manufacturers of these items, they're able, for the most part, to get lower prices.

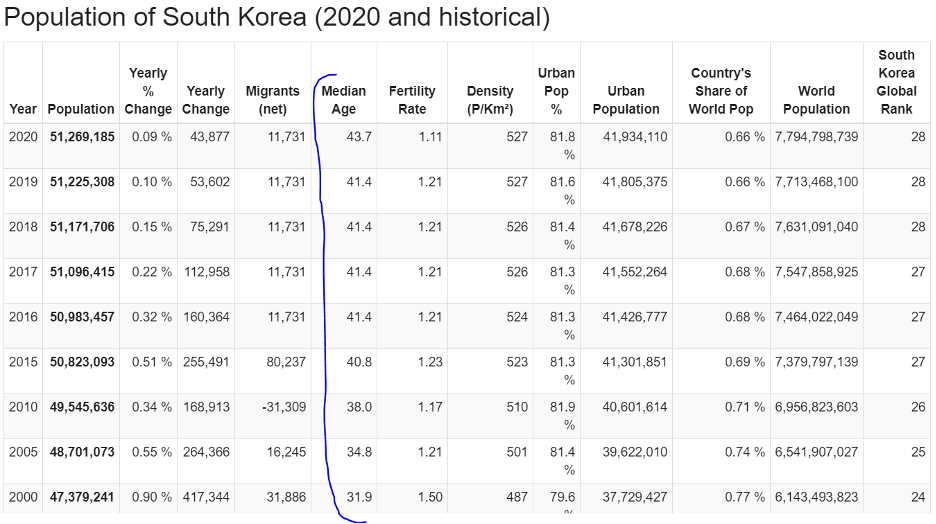

Total Korean e-commerce spend was $128 billion in 2019, which is expected to grow to $206 billion by 2024, implying a CAGR of approximately 10%.

This is where Coupang has a chance but in a rising interest rate environment and with competition on the New York exchanges from Amazon (AMZN), Shopify (SHOP), even MercadoLibre (MELI), I don’t believe Coupang is more attractive than these 3 in its current form as it relates to American investors pouring money into their stock.

Is it an advantage if 70% of Koreans live within seven miles of the Coupang logistic centers?

Certainly, there is that train of thought.

The massive investments into fulfillment centers mean they can surpass the delivery speed of many of its competitors because South Korea is essentially one capital city with millions upon millions hovering on top of each other like many other parts of Asia.

The problem I can have with this scenario is that margins could suffer because a busy Korean lifestyle doesn't lend itself to things like in-store shopping as readily as it does in the United States, and it could manifest itself with Koreans tapping into higher frequency in which they buy online which will push up total spend, but margins will decrease because you are buying stuff that won’t move the needle higher because you've paid for the service.

I can easily see someone just buying one item for delivery in the morning and doing that seven days per week.

Now I need a set of tweezers, I'm going to order that. Tomorrow, I need cotton pads, I’m going to order that.

Over time, operating margin will get butchered with a business like this.

And what do you know? I’m right, they have been losing billions upon billions the past few years with no end in sight.

How long will the external investors subsidize their losses?

At a broader level, mobile phone penetration is already at 96% of Koreans and 40% of Koreans order groceries online, so it’s hard for me to digest where the addressable market can expand from here because they have already collected so much of the available harvest.

This IPO does feel a little bit like an ex-growth dump on the retail investor and that’s not saying shares can’t appreciate at all, but investors believing this is the next Amazon are sorely mistaken.

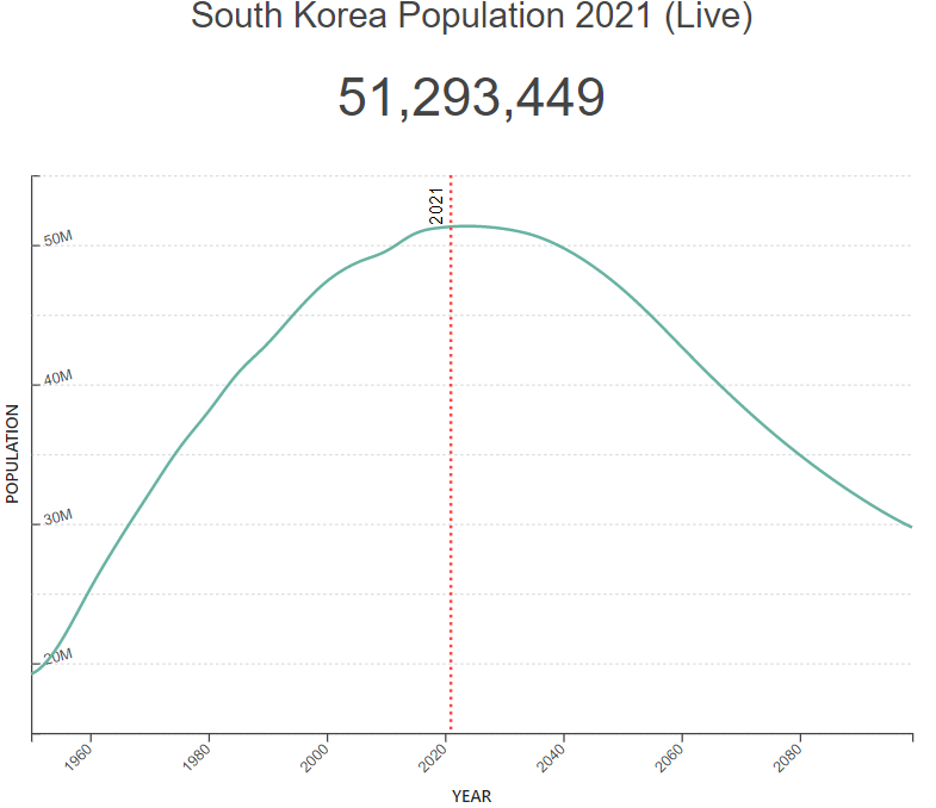

They are not Amazon, not even close, and they are also confined to one small market where the population has peaked and will start decreasing in numbers.

The population is only 15% of the U.S. and incomes in the U.S. are vastly higher, so how does Coupang become an Amazon without the AWS business?

Just as disturbing, the median age in Korea has ballooned from 31.9 in 2000 to 43.7 in 2020 and this cohort doesn’t strike me as the group in the glory years of family formation, peak spend, or technological know-how.

As the Korean population starts to decline in 2025 and the median age creeps up from 43.7 to 50, then aside from adult diapers, where does the incremental growth come from in Korea?

I just don’t see it.

Personal incomes are going to rise at an annualized rate of about 3% every year and I believe much of the total spend will be fought out attempting to woo the big buyers which offer a point of attack for competition that should come around in the next 2 to 3 years.

They also have Coupang Eats, not dissimilar to Grubhub (GRUB) or Uber (UBER) Eats. They have grocery delivery, and even an integrated payment processor. All of these things that took Amazon much longer to build out, admittedly, were a little before their time there, Coupang has already integrated that into the platform.

For this, I give them credit, but they are still nothing like Amazon in terms of potency and scale.

In 2019, active customers rose 34% and that’s what a prototypical growth company should do.

It’s not shocking.

Then an analyst would think that with covid and all that public chaos pinning consumers at home, surely, Coupang would grow active customers by 50% of even 60% in 2020, right?

But active customers only grew 18% in 2020, and they provided zero insight about why active customer growth slowed nearly in half year-over-year, and that for me shows, Coupang is severely limited by what Korea can offer in terms of growth and total spend.

If readers want to get into the Korean economy then I would advise to wait on other Korean homegrown entrepreneur-led startups with IPOs in the pipeline by Krafton Inc., the creator of hit game PUBG, and the country’s biggest mobile-only bank Kakao Bank. Unlike Coupang, those firms are profitable.

Ultimately, total e-commerce spend for all Internet buyers in Korea is expected to grow from approximately $2,600 in 2019 to approximately $4,300 in 2024 on a per buyer basis and Coupang will take advantage of that but I don’t foresee the 30% annual rise in underlying shares that others do.

I can definitely visualize a grind up with periodical substantial selloffs because of missed targets and disappointing forecasts.

That’s not the type of price action I want to see.

The signs point to Coupang maturing immediately and the executive management creating a special clause to allow them to dump shares right after the IPO illustrates that this tech company will stall out moving forward.

Normally, management must wait 6 months after going public before the lock-up period ends.

Highly unusual and can you believe it? They even gave stock shares to their courier drivers at the IPO, making me pause, then come to the conclusion that I rather invest in a tech company returning incremental value to the shareholders and not the manual labor that is paid by an hourly wage. How bizarre!

Avoid Coupang like the plague.