Below please find subscribers’ Q&A for the Mad Hedge Fund Trader September 18Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What would happen to the United States Treasury Bond Fund (TLT) if the Fed does not lower rates?

A: My bet is that it would immediately have a selloff—probably several points—but after that, recession worries will take bond prices up again and yields down. I don’t think we have seen the final lows in interest rates by a long shot. That’s why I bought the (TLT) last week.

Q: Is it good to buy FedEx (FDX) considering the 13% fall today?

A: I use the 3-day rule on these situations. That's how long it takes for the dust to settle from an earnings shock like this and find the real price. The problem with FedEx is that it’s a great early recession predictor. When the number of delivered packages decreases, it’s always an indicator that the economy as a whole is slowing down, which we know has been happening. It’s one of the most cyclical stocks out there, therefore one of the most dangerous. I wouldn’t bother with FedEx right now. Go take a long nap instead.

Q: Would you be a buyer of Facebook (FB) here, given they seem to have weathered all the recent attacks from Washington?

A: Not here in particular, but I would buy it 20% down when it gets to the bottom edge of its upward channel—it still looks like it’s going crazy. They’re literally renting or buying buildings to hire an additional 50,000 people in San Francisco anticipating huge growth of their business, so that’s a better indicator of the future of Facebook than anything.

Q: Will junk bonds be more in demand now that rates are cratering?

A: Junk bonds (HYG), (JNK) are driven more by the stock market than the bond market, as you can see in the huge rally we just had. Junk bonds are great because their default ratios are usually far below that which the interest rate implies, but you really have to trade them like stocks. Think of them as preferred stocks with really high dividends. When the stock market tops, so will junk bonds. Remember in 2008, junk yields got all the way up to 15% compared to today’s 5.6%.

Q: What will happen to emerging markets (EEM) as rates lower?

A: If lower interest rates bring a weaker US dollar, that would be very positive for emerging markets over the long term and they would be a great buy. However, emerging markets will take the hardest hit if we actually do go into a recession. So, I would pass for now.

Q: What are your thoughts on Alibaba (BABA) and JD.com (JD)?

A: They are great for the long term. However, expect a lot of volatility in the short term. As long as the trade war is going on, these are going to be hard to trade until we get a settlement. (JD) is already up 50% this year but is still down 40% from pre trade war levels. These things will all be up 20-30% when that happens. If you can take the heat until then, they would probably be okay for a long-term portfolio globally diversified.

Q: What do you have to say about the ProShares Ultra Short 20+ Year Treasury ETF (TBT)—the short bond ETF?

A: If you have a position, I’d be selling now. We just had a massive 20%, 4-point rally from $22 to $27 and now would be a good time to take a profit, or at least get out closer to your cost. The zero interest rates story is not over yet.

Q: Would you short the US dollar?

A: I would most likely short it against the euro (FXE), which now has a massive economic stimulus and quantitative easing program coming into play which should be positive for it and negative for the US dollar (UUP). That’s most likely why the euro has stabilized over the last couple of weeks. That said, the dollar has been unexpected high all year despite falling interest rates so I have been avoiding the entire foreign exchange space. I try to stay away from things I don’t understand.

Q: If all our big tech September vertical bull call spreads are in the money, what should we do?

A: You do nothing. They all expire at the Friday close in two trading days. Your broker should automatically use your long call position to cover your short call position and credit your account with the total profit on the following Monday, as well as release the margin for holding that position. After that, we’ll probably wait for another good entry point on all the same names, (AMZN), (FB), (DIS), (MSFT).

Q: If the US fires a cruise missile at Iran, how would the market react?

A: It would selloff pretty big—markets hate wars. And the US wouldn’t send one missile at Iran; it would be more like 100, probably aimed at what little nuclear facilities they have. I doubt that is going to happen. The world has figured out that Trump is a wimp. He talks big but there is never any action or follow through. Inviting the Taliban to Camp David while they were still blowing up our people? Really?

Q: Will the housing market turn on the turbochargers after this dip in rates?

A: It wouldn't turn on the turbochargers, but it might stabilize the market because money is available now at unprecedentedly low interest rates. However, we still have the loss of the SALT deductions—the state and local taxes and real estate taxes that came in with the Trump tax bill. Since then, real estate has been either unchanged or has fallen on both the East and West coast where the highest priced houses are. It’s the most expensive houses that take the loss of the SALT deduction the hardest. Don’t expect any movement in these markets until the SALT deduction comes back, probably in 16 months.

Q: What catalyst do you think would cause a 10% correction in the next 2-3 months?

A: Trump basically saying “screw you” to the Chinese—a tweet saying he’s going to bring another round of tariff increases. That’s worth a minimum of 2,000 points in the Dow Average (INDU), or about 7% percent. Either that or no move in Fed interest rates—that would also create a big selloff. My guess is that and adverse development in the trade war will be what does it. That’s why my positions are so small now.

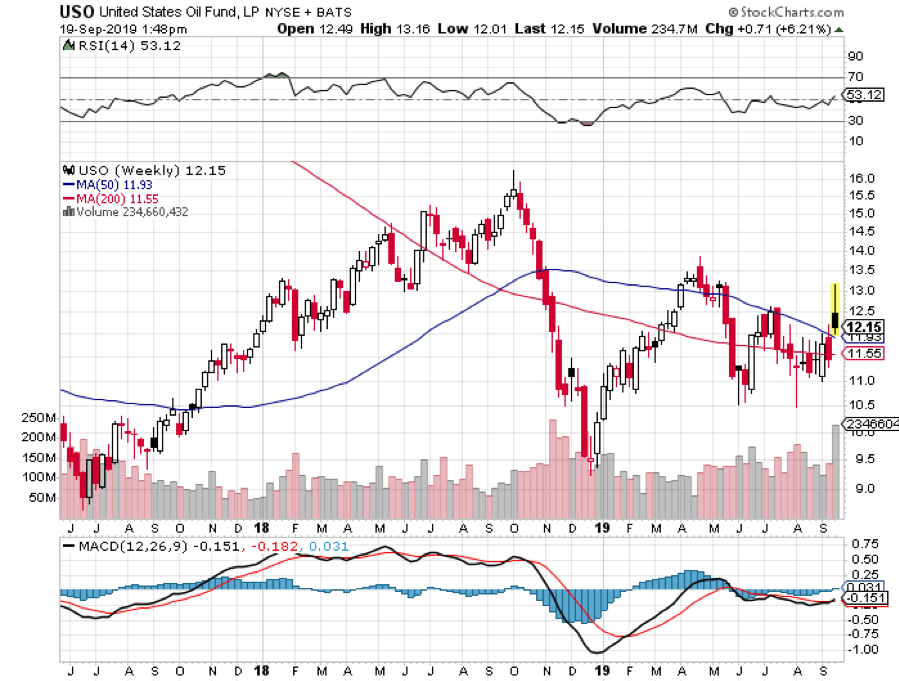

Q: We have a big short position in the United States Oil Fund (USO) now. Are you going to run this into expiration until October $18?

A: Even though oil has already collapsed by 10% since we put this position on last Friday, premiums in oil options are still close to record levels. So, it pays us to hang on for the time decay. The world is still massively oversupplied in oil and the Saudis were able to bring half of the lost production back on in a day. Oil will keep falling unless there is another attack and it is unlikely we will see one again on this scale. And, we only have 20 more days to go to capture the full 14.8% profit.

Good luck and good trading.

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

Ratcheting up the trade tensions, China is pulling the trigger on retaliatory tariffs on $60 billion worth of U.S. goods, just days after the American administration said it would levy higher tariffs on $200 billion in Chinese goods.

American President Donald Trump accused China of reneging on a “great deal.”

The mushrooming friction between the two superpowers gives even more credence to my premise that hardware stocks should be avoided like the plague.

I have stood out on my perch in 2019 and proclaimed to buy software stocks and if you need one name to hide out in then I would confidently choose Microsoft (MSFT).

Microsoft has little exposure to China and will be rewarded the most on a relative basis.

The last place you want to get caught out is buying hardware stocks exposed to China and Apple is quickly turning into the largest piece of collateral damage along with airplane manufacturer Boeing.

Remember that 20% of Apple’s revenue comes from China and Apple bet big to solidify a complex supply chain through Foxconn Technology Group in China.

When history is recorded, CEO of Apple Tim Cook not hedging his bets exposing Apple’s revenue machine could go down as one of the worst ever managerial decisions by tech management.

The forced intellectual property transfers in China from western corporations was the worst kept secret in corporate America.

Being an operational guru as he is, and the hordes of data that Apple have access to, this was a no brainer and Cook should have mitigated his risks by investing in a supply chain that was partially outside of China, and not incrementally spreading out the supply chain through other parts of Asia is coming back to bite him.

China's most recent tariffs will come into effect on June 1, adding up to 25% to the cost of U.S. goods that are covered by the new policy from China's State Council Customs Tariff Commission.

The result of these newly minted tariffs is that importers will probably elect to avoid absorbing the costs themselves and pass the price hikes to the consumer sapping demand.

The American consumer still retains its place as the holy grail of the American economic bull case, but this will test the thesis.

For the short term, it would be foolish to hang out to Chinese companies listed in New York through American depository receipts (ADR) such as JD.com (JD), Alibaba (BABA).

Baidu (BIDU) is a company that I am flat out bearish on because of a weakening strategic position versus Alibaba and Tencent in China.

Even with no trade war, I would tell investors to short Baidu, and the chart is nothing short of disgusting.

Wei Jianguo, a former vice-minister at the Chinese Ministry of Commerce who handled foreign trade, said to the South China Morning Post that “China will not only act as a kung fu master in response to U.S. tricks but also as an experienced boxer and can deliver a deadly punch at the end.”

It is clear that any goodwill between the two heavyweight powers has evaporated and the hardliners inside the communist party pulled all the levers possible to back out at the last second.

Many of us do not understand, but there is a complicated political game perpetuating inside the Chinese communist party pitting reformists against staunch traditionalists.

This is not only Chairman Xi’s decision and appearing weak on the global stage is the last concession the communist government will subscribe to.

Along with the iPhone company, semiconductor stocks will be ones to avoid.

The list starts out with the chip companies leveraged the most to Chinese revenue as a proportion of total sales including Qualcomm (QCOM) with 65% of revenue in China, Micron (MU) who has 57% of sales in China, Qorvo who has half of sales from China, Broadcom who has 48% of sales from China, and Texas Instruments rounding out the list with 43% of total revenue from China.

The first 5 months of the year saw constant chatter that the two sides would kiss and makeup and chip stocks benefitted from that tsunami of positive momentum.

The picture isn’t as pretty when you flip the script, and chip stocks could suffer a gut-wrenching summer if the two sides drift further apart.

After Microsoft, other software names I would take comfort in with the added bonus of strong balance sheets are Veeva Systems (VEEV), PayPal (PYPL), and Adobe (ADBE).

The new tariffs will burden American households to up to $2 billion per month going forward, and new purchases for discretionary items like extra electronics will be put on the back burner extending the refresh cycle and saddling chip companies and Apple with a glut of iPhone and chip inventory.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-14 03:02:312019-07-11 13:14:15China's Counterattack

The Mad Hedge Technology Letter has a front-line seat to the carnage wrought by the balkanization of technology that is swiftly descending across all corners of the tech universe.

In technology terms, this is frequently referred to as “splinternet.”

A quick explanation for the novices can be summed up by saying splinternet is the fragmenting of the Internet causing it to divide due to powerful forces such as technology, commerce, politics, nationalism, religion, and interests.

The rapid rise of global splinternet news stories will have an immediate ramification on your tech portfolio and it’s my job to untangle the knots.

What investors are seeing is the bifurcation of the global tech game into a binary world of Chinese and American tech.

Most recently, Central European country Poland, who was thought to be siding with the Chinese because of the growing presence by large-cap Chinese tech in Warsaw, announced government security had arrested a Huawei employee, Chinese national Wang Weijing, for allegedly spying on behalf of the Chinese state.

For all the naysayers that believe the administration’s hope of curtailing the theft of western technology was a bogus endeavor, this recent event buttresses the notion that Chinese state-funded tech companies are truly running nefariously throughout the world.

In fact, Poland has little to gain from this maneuver if you take the current status quo as your guidebook, and I would argue it is a net negative for Poland because Chinese tech is deeply embedded inside of the Poland tech structure bestowing profits and internet capabilities on multiple parties.

Making the case stronger against China, Poland has no flagship tech communications company that would serve as competition to the Chinese or could directly gain from this breach of trust.

The fringe of the Eurozone Central European nations and Eastern European countries bordering Russia running developing economies rely on Huawei and other low-cost Chinese tech suppliers like ZTE to offer value for money for a populace who cannot afford $1000 Apple (AAPL) iPhones and exorbitant western European telecommunications infrastructure equipment.

The Chinese beelining to this burgeoning area in Europe has given these less developed countries high-speed broadband internet for $10-$15 per month and 4G mobile service for $7 per month, a smidgeon of what westerners fork out for the same monthly service.

Poland rebuffing Huawei is an ominous sign for Chinese tech doing business in the Czech Republic and Hungary as European countries are moving towards denying Huawei in unison.

The last few years saw China create the same recipe of success for fueling economic expansion mimicking the American economy.

The tech sector led the way with outsized gains boosting productivity while analog companies transformed into digital companies to take advantage of the efficiencies high-tech provides.

At the same time, Beijing has initiated a muscular response to the accelerated growth of local tech companies.

The foul play of American tech in Europe has given impetus to Beijing to launch a power grab on local tech structures such as Baidu, Alibaba, and Tencent.

This couldn’t be more evident at Tencent who has failed to secure any new gaming licenses for their best gaming titles.

PlayerUnknown’s Battlegrounds (PUBG), a battle royale multiplayer, has been deprived of massive revenue because of Tencent’s inability to win a proper gaming license from the Chinese authorities to sell in-game add-ons.

In total, lost revenue has already cost Chinese video game companies over $2 billion in revenue since May 2017.

Beijing wants to temper the growing clout of private tech companies who were the recipient of the Chinese consumer’s gorge on technology in the last 20 years.

These companies have never been more infiltrated by the communist party and this can be mainly attributed to the acknowledgment by Beijing that Chinese tech companies are too powerful for their own good now and are a legitimate threat to the powers above.

That is what the sudden retirement of Founder of Alibaba Jack Ma told us who infuriated Chairman Xi because Ma was the first Chinese of note to meet American President Donald Trump at Trump Towers pledging to create a million jobs in America.

Ma later rescinded that statement and was put out to pasture by Beijing.

What does this all mean?

As the broad-based balkanization spreads like wildfire, Chinese and American tech companies’ addressable markets will shrink hamstringing the drive to accelerate revenue.

The potential loss of Europe for the Chinese could give way to Nokia, Siemens, and other western telecommunication companies to move in hijacking a bright spot for Huawei.

If Apple isn’t punching above their weight in China, well that almost certainly means that local tech companies aren’t having a cake walk in the park as well.

The winter sell-off turned the screws on tech first and then the rest of equities obediently, Chinese tech could have a similar domino effect to the Chinese economy boding badly for Chinese ADRs listed on the New York Stock Exchange (NYSE).

Last year, the Shanghai index was one of the worst performing stock markets in the world.

And if the trade wars are really ravaging a few key limbs from local Chinese tech firms, then companies exposed to the Chinese consumer such as Alibaba (BABA), JD.com (JD), Pinduoduo (PDD), Ctrip.com International (CTRP) and Tencent Music Entertainment (TME) could fall off a cliff.

This has already been in the works.

These companies are a good barometer of the health of the Chinese consumer and have had an abysmal last six months of price action.

The vicious cycle will repeat itself with worsening Chinese data drying up the demand for Chinese tech services and the Chinese consumer tightening their purse strings as they try to save money from a cratering economy.

It could become a self-fulfilling prophecy and that is what other indicators such as negative automobile sales and a rapidly failing real estate market are telling us.

The 65 million ghost apartments dotted around China don't help.

This could be the perfect opportunity to instigate wide-ranging reforms to open up the financial, insurance, a tech market to the west, something many analysts thought China would do after joining the World Trade Organization (WTO).

However, Beijing’s retrenchment preferring to pedal mercantilism and cold-blooded power grabs could offer Chairman Xi the prospect of further consolidating his authority by sticking his fingers deeper into the local tech structures giving the state even more control.

I would guess this is a false dawn.

American tech will confront balkanization headwinds of its own evidence in Vietnam as the government blamed Zuckerberg’s Facebook (FB) for failing to root out anti-government rhetoric which is illegal in the communist-based country.

If you haven’t figured it out yet – there is an underlying suitability issue with western tech services that tie up with authoritarian governments.

It many times leads the western tech companies to be a pawn in a political game that later turns into a bloody mess.

The weak rule of law has spawned a convenient practice of blaming western tech to distract from internal disputes strengthening the nationalist case of a purported western tech firm gone rogue.

This could lead Facebook to be removed in Vietnam, and the $238 million in ad revenue that will vanish.

Headaches are sprouting up across Europe with Facebook clashing with more stringent data privacy rules through General Data Protection Regulation (GDPR).

German’s largest national Sunday newspaper Bild am Sonntag claimed from sources that the Federal Cartel Office will summon Facebook to halt collecting some user data.

This could take a machete to ad revenue in a critical lucrative market for Facebook, and this experience is being echoed by other American tech companies who are running full speed into complicated regulatory quagmires outside of America.

Adding benzine to the flames, Deputy Attorney General Rod Rosenstein speaking at a cybercrime symposium at Georgetown University’s Law Center in Washington added to the tech misery explaining that to “secure devices requires additional testing and validation—which slows production times — and costs more money.”

This is not bullish to the overall tech picture at all.

Hamstringing tech is not ideal to promoting economic growth, but the decades of unchecked growth is finally reverting back to the mean with regulation rearing its unpretty head and the balkanization of tech forcing countries to pick between China or America.

The silver lining is that the American economy remains resilient taking the body blows of a government shutdown, interest rate drama, and trade war uncertainty in full stride.

The net-net is that American and Chinese tech firms could experience decelerating revenue growth far dire than any worst-case scenario forecasted by industry analysts.

Therefore, I forecast that American tech shares have limited upside for the next 6-10 weeks and Chinese tech is dead money in that same time span.

Any rally is ripe for another sell-off if there are no meaningful breakthroughs in the trade war and if China’s economic data continues to falter.

The global growth scare could actually come home to roost.

The supposed narrowing of trade differences has been nothing more than tactical, and procuring any fundamental victories is a hard ask in the short term.

In an ideal world, China would open the floodgates and allow the world to join them in an economic détente, however, based on Chairman Xi’s record of purging his mainland enemies and the military, slamming the gates shut and padlocking them seems more likely at this point.

Seizing the rights to an untimed Chairmanship term has its perks – this is one of them and he is using the entire assortment of options available to him.

Traders should look at deep in-the-money vertical bear put spreads on any sharp rally to specific out-of-fashion tech names saddled with regulatory and data balkanization headwinds, or tech firms with a large footprint in mainland China.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/01/battlegrounds.png412808Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-15 04:06:582019-07-09 04:57:18The Balkanization of the Internet

As a bolt from the blue, Google search is headed back to China.

The project coined Dragonfly commenced in early 2017 as Google sought a way back into the lucrative Chinese market to sell its products.

The retracement to China then later sped up after Google CEO Sundar Pichai secretly met with a top Chinese official in December 2017.

The censored Google search application could be launched in the next six months to a year upon approval from the communist party.

Why China?

There are three times more smartphones in China than in the U.S. This market represents celestial scale unfounded in any other country.

The Chinese Internet population has roughly 772 million people with Internet penetration levels at about 55%.

The U.S. has maxed out its penetration level at 89% and there is little room to snatch up a new group of mass users. This is not the case in China, which has ample amounts of room to run.

In addition, Google hopes to roll out a news aggregation app mirrored on Chinese newsfeed app Jinri Toutiao that implements personalized artificial intelligence to cater toward each unique user's needs.

As of December 2017, users spent an average of 73 minutes per day on this app.

Jinri Toutiao has 120 million daily active users and has been given a valuation of around $35 billion.

The unbridled potential for American large cap tech companies in China is unrivaled.

But navigating around China's murky business environment under the comprehensive controls of the Great Firewall has proved cumbersome highlighting the executional prowess of Apple's (AAPL) iPhone business in China.

Why did Google leave in the first place?

The issue of censorship was the catalyst leading Google search to the exits.

Google was stunned by the exploits of the Chinese communist government, which maneuvered around Google's system targeting human rights activists among other things.

Operating abroad, companies do not always have complete control over the systems they build and the business processes that revolve around it.

Beijing continued to press Google to filter its search results in 2010, and anything but compliance spelled doom for Google's future in China.

Restricting speech is commonplace for many undeveloped countries with brutal regimes.

The U.S. has one of the most lenient free press laws in the world underlying the backbreaking hassle of operating in a country that actively and aggressively suppresses free speech deemed negative to the people in powerful positions.

After Google started rerouting mainland Chinese Google search to its filter-less Hong Kong servers, Google search was unceremoniously shut down within months.

A comeback is in the works at a time when China and America are at each other's throats in a tit-for-tat trade war, complicating the move to reinsert itself back in the Middle Kingdom.

Let's make no bones about it, this is a high-risk, high-reward strategy for Alphabet, which seeks to add yet another growth driver to its profit-making machine.

Out of the FANG group, only Apple has emerged to unlock the Chinese market with outstanding success.

All other American tech competition was rooted out. Only chip names such as Micron (MU) and Intel (INTC) latched onto the Chinese market largely because of the Chinese demand for chips.

This unfortunate development opened the path for the BATs to dominate in China, which is comprised of Baidu (BIDU), Alibaba (BABA), and Tencent.

Rewind back to 2010, Google search was directly competing against China's Baidu headed up by founder Robin Li.

Google had just 14% market share in search and was trailing far behind Baidu, which had 79% of market share.

In 2010, the difference in the quality of the search algorithms between the two couldn't have been larger.

When comparing these search engines, 85% of Google searches would populate vastly different results compared to Baidu's search platform.

Upon further inspection, Google search was deemed far more accurate than the market share leader Baidu, and that has not changed.

China's inferior technological abilities are well noted. The shortage of talent has forced them to institute forced technological transfers from western companies working in China, outright theft of technical know-how by state sponsored hackers, and the use of government loans to finance M&A activity in technological advanced countries.

In fact, Google leaving China robbed the Chinese tech sector of legitimate competition crushing the innovation trajectory or any remnants of one.

This led to the BATs running riot making money hand over fist but still trailing American tech by a country mile in terms of technical ability and innovation.

A lack of competition breeds complacency.

The reintegration of Google search into China will bring a whole new level of top-class ad technology into China.

This could be the beginning of a monumental ramp up in digital ad spend in China, which trails far behind North America and Europe in average revenue per person.

Discretionary spending is robust in China and advertisers want a piece of the action.

As much as this could be an opportunity for Alphabet to invigorate its cash-making enterprise, it is also a chance to enhance the overall Chinese tech sector.

Upon hearing Google will return, Baidu's Li laid down the gauntlet retorting that Baidu will "win one more time."

Having the communist party on your side as a tag team partner goes a long way in China and has been the main reason of foreign firms fleeing in droves in the past.

Alphabet won't have the same help.

Yet, it could learn a great deal from heading into this sensitive opportunity that could also lay the groundwork to operate in other countries with repressive governments bent on destroying freedom of speech.

Naturally, Alphabet employees weren't impressed with this new direction.

Silicon Valley is centered on left-wing social mores and adjusting its model to accommodate a totalitarian regime does not sit well with many workers.

Google saw a mini employee revolt because of Project Maven, a national defense program marrying artificial intelligence with combat operations in the United States.

Allowing Google's technology to possibly fall into the hands of Beijing would be unforgivable and a national embarrassment.

This idea is definitely not part of the low hanging fruit initiative.

This fruit is 20 feet high dangling from a distant branch.

If Alphabet pulls this off, it could add another surging driver to its portfolio, which prints money because of its digital ad segment.

It could potentially increase revenue by 30%.

Alphabet's successfully bringing in its Google search engine back from the cold, albeit censored search engine, could lay the groundwork for other American tech companies to enter the Chinese market, which would crush Alibaba, JD.com (JD), Tencent, and Baidu's share price.

Baidu dropped more than 6% upon this announcement.

The tech expertise level would naturally rise in China if American tech companies were permitted to set up shop, enhancing the total Chinese tech sector.

It would also apply pressure on China's communist government to open up its industries and do away with the protectionist stance that has been a bedrock policy fueling China's unbelievable rise from rags to riches.

China's top-level politicians must understand inward policies of this ilk do not mesh with the status of a country that is the world's second biggest economy. And it was only a matter of time before unyielding backlash ensued.

From the political side, it could possibly offer additional ammunition to the American administration if China wholeheartedly rejects Google's foray into the mainland, even if it complies with every miniscule, arcane rule Beijing throws at them.

It will prove that China is not willing to compromise or make a deal with the deal-obsessed American administration. And it will signal a dead-end road for any large cap American tech company with China aspirations.

The U.S. administration would use this as an "I told you so" moment, highlighting a history of perpetual unfair trade practices. Hopefully, it never gets to this point.

As it stands, many American large cap tech companies won't touch the Chinese market with a 10-foot pole, but the breathless scale is hard to pass up for others.

If Google is stonewalled, expect an even tougher response from the American administration hell-bent on preventing technological transfers to China.

Currently, the Committee on Foreign Investment in the United States (CFIUS) is attempting to recreate the rules to counteract the China threat.

The trade war is ultimately about global supremacy and being able to harness the biggest tool to achieve world hegemony, which is high caliber technology.

The treatment of Chinese and American tech companies by each other's government will give investors deep insight into how this all plays out.

This is Alphabet's last gasp chance at entering China. If it evolves into a spectacular failure, it always has its digital ad business to fall back on and the upcoming mass rollout of Waymo, its autonomous self-driving taxi business.

"If Google re-enters the market, it gives us the opportunity to player kill with real swords and spears and win one more time," - said founder and CEO of Baidu Robin Li.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-13 01:05:132018-08-13 01:05:13Google's New Chinese Play

The administration's attempts to stick China with the bill is a waste of time.

The stock market is forward-looking and that is what I focus on when writing the Mad Hedge Technology Letter.

American tech companies want to turn over this bitter page of history and construct a fruitful future.

Ironically, it could be no other than American large tech companies that solves this trade misunderstanding by embracing Chinese tech instead of dragging them through the embers of political chaos.

That is what this groundbreaking partnership between Alphabet (GOOGL) and China's second largest e-commerce company JD.com (JD) is telling us.

If American and Chinese tech agree to fuse together through different M&A activity, strategic partnerships, and engineering projects, slapping penalties on your own interests would be without basis.

Albeit gone are the yesteryears of complete ownership on the other's turf, a medium ground could be found to satisfy both parties.

Alphabet's $550 million investment will give it 27 million shares of JD.com Class A shares equating to a 1% stake in JD.com.

JD.com products will now be hawked on Google Shopping, a platform giving users a chance to compare different price points from various sellers.

JD.com's fresh links with Silicon Valley's original powerhouse is timely because its business-to-consumer retail sales have slightly dipped in form from 27% last year to an underwhelming 25% in the first quarter of 2018.

Alibaba (BABA), the Amazon of China, is the 800-pound gorilla in the room and has a stranglehold on this market, carving out a robust 60% of sales from business to consumer retail.

Chinese companies have never worried about foreign companies seizing market share in China because they know the rigid operating environment mixed with "cultural" barriers will lead to a rapid demise.

Chinese firms are channeling their distress toward local competitors that understand the market as well as they do and number in the 100s in any one industry.

This is also a huge bet on the Chinese consumer who has put the world economy on its back creating the lions' share of global growth for the past 10 years.

Do not bet against China and the Chinese consumer.

Alphabet is taking this sentiment to the bank by integrating part of a premium Chinese tech firm into its own top line performance.

This investment would not happen if Alphabet believed the trade war could turn draconian cannibalizing each other's profit engines.

Alphabet has obviously been reading the tea leaves from the Mad Hedge Technology Letteras I identified China's huge competitive advantage in Southeast Asia and the huge potential for Chinese companies that migrate there.

The pivot toward Southeast Asia was the deal clincher for Alphabet and rightly so.

Alphabet has also invested in opening an A.I. (artificial intelligence) lab in Beijing showing its determination to extract a piece of the pie from China and ensuring their brand power is maintained in the Middle Kingdom.

Google search has been shut down on mainland China since 2010. Therefore, Alphabet needs to find alternative ways to benefit from the Chinese consumer and increase its presence.

The writing on the wall was when Baidu (BIDU) came to the fore with its own Chinese version of Google search.

Opportunities on the mainland have been scarce ever since the appearance of Baidu.

Apple (AAPL) has been the premier role model in China successfully juggling the complexities of the Chinese market. A big part of its staying power is offering local Chinese jobs.

Not just a few jobs, but millions.

As of April 2017, an Apple press release stated, "Apple has created and supported 4.8 million jobs in China" which is almost three times more than in America.

Apple deploys much of its supply chain around the mainland and taking down Apple in a trade war would strip millions of Chinese jobs in one fell swoop.

Not only that, Apple has deeply invested in data centers located in China and opened research centers in Shanghai and Suzhou.

Foxconn, a company responsible for assembling iPhones in mainland China, employs 1.2 million alone.

Alphabet would be smart to follow in the same footsteps, effectively, morphing into a hybrid Chinese company employing locals in droves and allowing millions of Chinese to earn their crust of bread through local factories.

Let me be clear: This would not hurt its business back at home.

It is also wrong to say that China is saturating because the 6.8% annual growth rate in China is a firm vote of confidence for Chinese discretionary spenders.

However, instead of competing head to head under the scrutiny of Chinese regulators, it is much more sensical to copy SoftBank's Masayoshi Son's lead when he invested $25 million in Jack Ma's Alibaba in 1999.

SoftBank's 1999 investment is now valued at more than $30 billion as of the current share price today.

Yahoo later joined the party in 2005, investing $1 billion into Alibaba and that stake is worth many times over.

Instead of fighting through cultural norms and fighting against the throes of an exotic business environment, paying for a stake and leaving its nose out of it has shown to be demonstrably effective.

Partnerships complicate the relationship, but if management can lock down each side's commitment to the very T, collaboration could spur even more innovation benefiting both countries and bottom lines.

China has draconian Internet controls put in place. American tech companies aren't up to snuff with cultural maneuverability to navigate through these shark-infested waters.

Better to pay for a stake and pick up the check after the market close.

Another winner in this deal is tech valuations, which has been the Cinderella story of 2018.

Although American tech companies will probably never be able to own 100% of a Chinese BAT. However, allowing these types of investments to go ahead is certainly bullish for equities.

Tech is still the sector lifting the heavy weight stateside and promoting innovation through collaboration will do a great deal to win the hearts and minds of Chinese people, companies and government.

As much as China hates the stain to its image of this nebulous trade war, it still deeply respects and admires large-cap American tech companies.

Chinese Millennials particularly have a deep love affair with Tesla's Elon Musk. They are captivated by his braggadocio, which they find appealingly exotic and captivatingly un-Chinese.

Through this partnership, JD.com will learn heaps about cutting-edge ad-tech and is guaranteed to apply the know-how to its home user base. In return, Alphabet will get deep insights of how JD.com controls the entire logistical experience and how a Chinese tech behemoth operates its supply chain.

The nuggets of information pocketed will help Alphabet compete more with Amazon back at home.

This is a win-win proposition.

Adding even more cream on top, enhanced brand awareness by joining together with Google could catapult JD.com into the shop window of America's consciousness.

Up until today, JD.com is hardly known about in the West except for specialists that avidly follow technology like the Mad Hedge Technology Letter.

I reiterate my stance of not buying into Chinese tech companies, and readers would be better served buying Microsoft (MSFT), Amazon (AMZN), and Netflix. (NFLX)

It makes no sense to trade stocks mired in the heart of a trade war.

As much as I love Alibaba as a company, it has been trading in a range because of the whipsawing headlines released in the press.

However, I can stand from afar and admire how the Chinese BATs have advanced in such a short amount of time.

If American tech and Chinese tech merge to the point of unrecognizability, consolidation could create a super tech power comprising of mixed Chinese and American interests.

Instead of bickering at each other, other solutions look to be more compelling.

The world's economy needs a healthy Chinese economy and vibrant Chinese consumer.

If the Chinese economy ever fell off a cliff, you can kiss this nine-year equity bull market goodbye, and the Mad Hedge Technology Letter would turn extremely bearish in a blink of an eye.

Therefore, America has a large stake in not alienating the Mandarins to the point of disgust.

I am still bullish on equities, but vigilance is the name of the game for short-term traders.

"My belief is that one plus one equals three. The pie gets larger, working together," Apple CEO Tim Cook said about its operations in mainland China and working with the Chinese Communist government.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-06-20 01:05:122018-06-20 01:05:12Google's Grand China Play

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visist to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.