Since the pandemic started, we’ve had two extremely similar COVID-19 vaccines approved: the mRNA vaccines created by Moderna (MRNA) and Pfizer (PFE) / BioNTech (BNTX).

Now, there’s another coronavirus shot that gained FDA approval: Johnson & Johnson’s (JNJ) adenovirus jab.

In fact, JNJ’s candidate received a unanimous approval from the FDA—a first among the COVID-19 vaccine developers.

Results showed that JNJ’s shot has 66% effectivity at preventing coronavirus infections and 85% effective at blocking severe COVID-19 cases when allowed at least four weeks to take effect.

Taken at face value, the numbers from JNJ’s trials may not seem as impressive as the two-shot vaccines of Moderna or Pfizer, which both demonstrated efficacy results of over 94% in their 2020 reports.

However, it’s important to not make any conclusions based on incomplete data.

After all, drawing comparisons among different vaccine studies performed at different periods is practically comparing apples to oranges.

That’s why Dr. Anthony Fauci and other experts declared that they’ll just take whichever vaccine shot they could avail of.

Actually, the JNJ vaccine may be the ideal option for some people.

Since the JNJ vaccine shows less severe reactions compared to Pfizer and Moderna’s vaccines, this could be preferable for people who couldn’t tolerate the side effects.

Although the side effects of Pfizer and Moderna are temporary, some people need to take days off to recover. Sadly, not everyone has the luxury to do that.

The fact that it’s a single jab vaccine makes it an attractive option for young and healthy individuals, who can’t afford to go back to get a second shot.

It’s also less fragile and can be stored in a regular fridge for three months without the need for any hyper-cold storage system like the mRNA vaccines require. This would make it an attractive option for rural areas.

Plus, JNJ tested its candidate at the height of the pandemic. That means the numbers the company released could have been affected by the situation at the time.

Although JNJ’s vaccine does not completely get rid of the disease, it delivers on the promise of protecting the patients from the worst possible scenarios of COVID-19: hospitalization and death.

Basically, the JNJ vaccine is cheap to manufacture as well as pretty simple to administer and get.

People can get some dependable viral protection within a span of four weeks, without the need to return for a second jab.

As a bonus, the JNJ vaccine could even protect you better from the new variants that are starting to spread fast.

Despite the $410 billion market capitalization of JNJ though, it looks like the New-Jersey-based giant isn’t up for the massive rollout the world expects from its vaccine.

This is where Joe Biden steps in.

With the goal of having every American vaccinated by the end of May, Biden tapped Merck—a fierce rival of JNJ—to help out with the production.

While Merck’s own COVID-19 vaccine program was shut down, this company remains the leading vaccine developer across the globe.

This means it knows a thing or two about fast-moving mass production during outbreaks—and this is exactly the kind of expertise JNJ needs.

If things work out, JNJ should be able to produce 94 million doses by the end of May—roughly 7 million doses ahead of what’s stipulated in its contract—and the full 100 million by June.

This arrangement isn’t anything new. Since the COVID-19 pandemic, competitors have been joining forces to find ways to put an end to the crisis.

In January this year, Sanofi (SNY) announced that it would be collaborating with BioNTech to help manufacture additional doses of the COVID-19 vaccine it developed with Pfizer.

When JNJ receives authorization from the EU as well, Sanofi would also be there to help with the production.

The JNJ vaccine could just be the escape hatch we’ve all been waiting for since the pandemic started.

With this FDA authorization, we’d be able to vaccinate millions more at a breakneck speed.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-04 16:00:552021-03-06 18:20:11Are We There Yet: How the JNJ Vaccine Could Be the Answer

This was the week the stock traders learned there was such a thing as a bond market. They know this because it was bonds that completely demolished their stock trading books.

Suddenly, markets went from zero offered to zero bid. Many strategists labored under the erroneous assumption that ten-year US Treasury yields would never surpass 1.50% in 2021. Yet, here we are only in March and it’s already topped 1.61%. It’s become the one-way trade of the year.

The bond market seems to be discounting an imminent runaway inflation rate. But at a 1.4% annual figure, it's nowhere to be seen, not with 20 million unemployed and Main Streets everywhere looking like ghost towns.

I still believe that technology is evolving so fast, hyper-accelerated by the pandemic, that it will wipe out any return of inflation. I will not believe in inflation until I see the whites of its eyes, to paraphrase Colonel William Prescott at the Battle of Bunker Hill.

Of course, it is I who has been screaming from the rooftops about the coming crash of the bond markets, since March 20. Being short the bond market has been one of my most profitable trades of 2020 AND 2021. If I am annoyed by anything, it happened too fast, depriving me several more round trips a slower crash would have permitted.

When you have to own stocks, make them financials (JPM), (BAC), (C), which benefit from rising rates. Their loan rates are rocketing while their cost of money is fixed at the Fed overnight cost of funds at 0.25%. Trading volumes at the brokers (MS), (GS) are through the roof, especially for options traders.

It is all a perfect money-making machine. At least, the stock market thinks so.

I’ll tell you something that markets are not paying attention to at all, and it is the tremendous improvement in the pandemic. Since January 20, news cases have cratered from 250,000 a day to only 70,000, down 72%. The best-case scenario which markets discounted by near doubling in 11 months is happening.

With the addition of the Johnson & Johnson (JNJ) vaccine, some 700 million doses will be available by June. We could be back to normal by summer, at least in the parts of the country that don’t believe it is still a hoax.

This breathes life into the blockbuster 7.5% GDP growth scenarios now making the rounds. I think people have no idea how hot the economy is really going to get. Labor and materials shortages may be only three months off, but with no inflation.

So, what does all this mean for the markets? It all sets up the normal 5%-10% correction that I have been predicting. If you have two-year LEAPS on your favorite names, hang on to them. We are going much higher.

I went into the Monday selloff with a rare 100% cash position. The 20% I have now in commodities I picked up on puke out, throw up on your shoe capitulation days.

The barbell is still the winning strategy.

Domestic recovery stocks have been on fire for six months, with small banks up a ballistic 80%. Big tech has gone nowhere. But their earnings are still exploding, in effect, making them 20% cheaper over the same time period.

It’s just a matter of time before markets rotate back into tech and give domestic recovery a break. Think (AAPL), (FB), (AMZN), and (GOOGL). That is where the smart money is going right now. The bond auction was a total disaster. The US Treasury offered $62 billion worth of seven-year US Treasury bonds, double the amount a year earlier. At a 1.95% yield and no one showed. Foreign participation was the worst in seven years. The bid-to-cover ratio was pitiful. Over issuance by the government crushing the market? Who knew? Imagine how high interest rates would be if the Fed wasn’t buying $120 billion a month of bonds?

The insanity is back, with GameStop (GME) doubling in the last 15 minutes of the month. Nobody knows why. It was why stocks tanked at the close on Thursday, scaring away real investors in real stocks. (GME) has become an indicator of all that’s wrong with the market.

Copper demand is rocketing, says Freeport McMoRan (FCX) CEO Richard Adkerson. That’s why he is opening three new US mines this year, adding 250 million pounds in annual output. Biden’s ambitious EV plans are the trigger. You can’t build an EV without a lot of the red metal. The world’s largest copper producer has become a major climate change and ESG play.

NVIDIA blows it away, with sales up a blockbuster 66%. Demand from gamers locked up at home was overwhelming. Purchases by bitcoin miners were through the roof. Even demand from the auto industry was up 16%, even though card sales aren’t. Too bad they picked the wrong day to announce, with the stock off 8.2%. (NVDA) is the one tech stock I would buy on dips.

Fed says business failures will continue at record pace, mostly occurring among small, unlisted local businesses. Biden’s $1.9 trillion rescue budget will come too late for many. Unemployment could stay chronically high for years, as the Weekly Jobless Claims are suggesting.

Housing starts fell in January, down 6.0% to 1.58 million units. A much smaller drop was expected. Rising land and lumber costs are cutting into the economics of new construction. Home prices are going to have to accelerate to suck in more supply. Housing Permits for new construction soared by 10.4% last month, so the future looks bright for builders.

Tesla (TSLA) crashed, down $180 in two days. We have just suffered a perfect storm of bad news about Tesla. Interest rates have been soaring, bad for all tech in the mind of the market. Competitor Lucid Motors announced a SPAC valued at $11 billion. And Elon Musk said Bitcoin looked “high” after investing $1.5 billion. Get ready to buy the dip, but not yet.

Quantitative easing to continue, says Fed governor Jay Powell, even if the economy improves. The $120 billion in bond-buying remains, even if the economy improves. He’s doing everything possible to create inflation.

Panic hits the crypto markets, dragging down technology equities with them. The two have been trading 1:1 for four months. Bitcoin suffered an eye-popping 25% plunge from $58,000 to 43,600. The tail is now wagging the dog. All risk-taking may have spiked with the Friday options expiration. Watch Bitcoin for a tech stock revival and vice versa. Stocks have earnings multiple support. Crypto doesn’t. I’ll buy Bitcoin when they post a customer support number.

Australian dollars soars as predicted, from $58 to $79 in 11 months. We could hit parity in 2022. The Aussie is basically a call option on a synchronized global economic recovery. End of the pandemic will also bring a resumption of massive Chinese investment in the Land Down Under. Keep buying the dips in (FXA).

Case-Shiller explodes to the upside, up 10.4% in December. It’s the hottest read in seven years for the National Home Price Index. Phoenix (14.4%), San Diego (13.0%), and Seattle (13.6%) were the strongest cities. The flight from the cities continues.

(TLT) breaks $138, surpassing my end 2021 target of a 1.50% ten-year US Treasury yield. So, I lied. My new yearend target is now $120, which would take ten-year yields to 2.00%. With a $1.9 trillion rescue budget about to kick in after the $900 billion that passed in December, the economy and demand for funds are about to rocket. Better hurry up and buy that house before mortgage rates rise out of reach.

Weekly Jobless Claims sink to 730,000. I can’t believe that 730,000 is now considered a good number, compared to 50,000 a year ago.

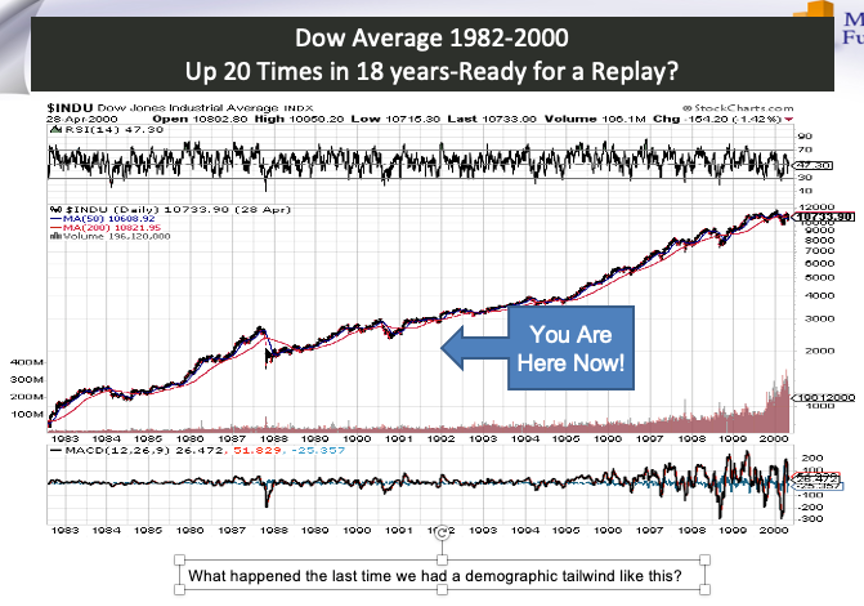

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

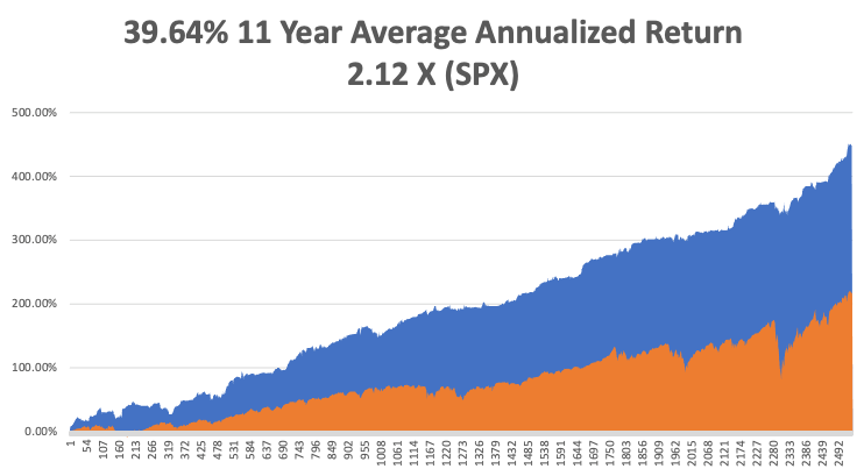

My Mad Hedge Global Trading Dispatch closed out with a 13.28% profit in February after a blockbuster 10.21% in January. The Dow Average is up a miniscule 1.1% so far in 2021.

This is my fourth double-digit month in a row. My 2021 year-to-date performance soared to 23.49%. After the February 19 option expiration, I am now 80% in cash, with longs in (XME) and (FCX).

That brings my 11-year total return to 446.04%, some 2.12 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 39.64%.

My trailing one-year return exploded to 93.48%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 103.31% since the March 20, 2020 low.

We need to keep an eye on the number of US Coronavirus cases at 28 million and deaths topping 510,000, which you can find here.

The coming week will be a boring one on the data front.

On Monday, March 1, at 10:00 AM EST, the ISM Manufacturing Index is out. Zoom (ZM) reports.

On Tuesday, March 2, at 9:00 AM, Total US Vehicle Sales for February are announced. Target (TGT) and Hewlett Packard (HPQ) report.

On Wednesday, March 3 at 8:15 AM, the ADP Private Employment Report is released. Snowflake (SNOW) reports.

On Thursday, March 4 at 9:30 AM, Weekly Jobless Claims are printed. Broadcom (AVG) and Costco (CSCO) report.

On Friday, March 5 at 8:30 AM, The February Nonfarm Payroll Report is announced. Big Lots (BIG) reports. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, the deed is done, I got my first Covid-19 shot, pure Pfizer.

The Marine Corps failed to deliver, as only active duty are getting shots. Washoe County ran out. Incline Village said I couldn’t get a shot until July. My own doctor had no clue.

Then I got an automated call from the doctor who did my stem cell treatment on my knees five years ago. They belonged to a large group that had my birthday in their system and my number came up on the first day the under ’70s opened up.

Going there was a celebration. Everyone was thrilled to death to get their shot. It was like winning the lottery. Our little local hospital operated with machine-like efficiency, inoculating 1,300 a day. It was a straight drive in, dive out. It was an “all hands-on deck” effort, with everyone from the board directors to the billing clerks manning the needles. It took longer to buy a Big Mac than to get my shot.

To make sure I didn’t pass out, I was sent to a holding area, where a person was assigned to each car. I got the CEO and grilled him relentlessly on his business model for 30 minutes.

I haven’t felt this good since I got my polio vaccine sugar cube in 1955.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

January 20 Infection Rate

March 3 Infection Rate

https://www.madhedgefundtrader.com/wp-content/uploads/2021/03/john-thomas-covid-shot.png350468Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-01 10:02:192021-03-01 10:25:44The Market Outlook for the Week Ahead, or Wake Up Call

Below please find subscribers’ Q&A for the February 3 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Incline Village, NV.

Q: Is there a big difference between COVID-19 vaccines?

A: The best vaccine is the one you can get. It’s better than being dead. But there are important differences. The Pfizer (PFE) and Moderna (MRNA) vaccines are RNA vaccines, they’re very safe, and getting similar results. But the evidence shows that about 15% of Moderna recipients are coming down with flu-like symptoms on their second shot. Nobody knows why, as the two are almost biochemically identical. AstraZeneca is a killed virus type vaccine, which means if they have a manufacturing error, you end up giving the disease to people by accident, as with the original polio vaccine. So that's the less safe vaccine. So far, that one has only been used in Europe and Australia, as it is made in England. There isn’t enough data about the John & Johnson (JNJ) single-shot vaccine.

Q: Is Moderna (MRNA) a long term buy?

A: The trouble with all the vaccine plays is that we’re heading for a global vaccine glut in about 4 months when we’ll have something like 12 companies around the world making them. The rush for everyone to get a vaccination as soon as possible is leading to inevitable overproduction and falling stock prices. Moderna is already a 12 bagger for us. I’m not really looking to overstay my welcome, so to speak. Time to cash in and say, “Thank you very much, Mr. Market.” There will be another cycle down the road for (MRNA) as its technology is used to cure cancer, but not yet.

Q: Would you recommend a silver (SLV) LEAP?

A: Yes, silver was run up 35% for a day by the GameStop (GME) crowd and crashed the next day, which was to be expected because there are no short positions in silver. Everything was just hedged to look like there were short positions because the big banks had huge open short options positions that were public and hedges in the futures and silver bars that were private. The (GME) people only saw the public short positions. Long term, I would go for a $30-$32 vertical call spread expiring in 2023. Go out 2 years, and I think you could get silver at $50. So, a good LEAP might get you a 1000% return in two years. Those are the kinds of trades I like to do.

Q: What do you think of Amazon now that Jeff Bezos is retiring?

A: Buy the daylights out of it. That was the great unknown overhanging the stock for years, Jeff’s potential retirement. Now it's no longer unknown, you want to buy (AMZN). Even before the retirement, I was targeting $5,000 a share in two years. Now we have everybody under the sun raising their targets to $5,000 or more— we even had one upgrade today to $5,200. There are at least half a dozen businesses that Amazon can expand into, like healthcare, which will be multibillion-dollar earners. And then if you break it up because of antitrust, it doubles in value again, so that's a screaming buy here. We have flatlined for six months, so this could be a trigger for a long-term breakout.

Q: Is there anything else left after GameStop? Another short play?

A: Well, this was the worst short squeeze in 25 years, and everyone else covered their other shorts because they don't want to get wiped out like the one Melvin Capital. There were only around a dozen potential single-digit heavily shorted stocks out there, and those are mostly gone. So, the GameStop crowd will have to roll up their sleeves and do some hard work finding stocks the old fashion way—by doing research. I’m guessing that GameStop was a one-hit-wonder; we probably won’t be surprised again. At the same time, you should never underestimate the stupidity of other investors.

Q: What do you think of the cloud plays like Cloudera and Snowflake?

A: I love cloud plays and there will be more coming. The entire US economy is moving on to the cloud. But everyone else loves them too. Snowflake (SNOW) doubled on its first day, and Cloudera (CLDR) doubled over the last three months, so they're incredibly expensive and high risk. But you can't argue with their business models going forward—the cloud is here to stay.

Q: Would you buy LEAPS in financials?

A: Absolutely yes; go out two years for your maturity and 30% on your strike prices, you will get a ten bagger on the trade. If I’m wrong, it only goes to zero.

Q: Is US Steel (X) a buy?

A: Yes. They are being dragged up by the global commodity boom triggered by the global synchronized recovery. (X) took a hit today because they just priced a $700 million secondary share issue which the flippers dumped like a hot potato. If given the choice, I’d rather do a copper play with Freeport McMoRan (FCX) which is seeing much more buying from China. I bought it on Monday.

Q: Any chance you can include one-, three-, and five-year price targets?

A: No chance whatsoever. I’ve never heard of a fund manager that could do that and be right. Stocks are just too imprecise an instrument with all the emotion that’s involved. But for the better stocks, you can with confidence predict at least a double. And by the way, all my predictions for the last 13 years have been way, way on the low side, so I tend to be conservative. Like, remember when Amazon was at $10? I said it would go to $20. Boy was I right!

Q: How can you say the next four years will be good for the stock market?

A: Well, $10 trillion in fiscal stimulus, $10 trillion in QE; stocks tend to like that. Oh, and technology exponentially accelerating on all fronts and far more broadly than what we saw in the 1990s. Also, there is a certain person who is no longer president, so add about 10-20% on top of all stock valuations. Companies can finally do long term planning again, after being unable to do so for four years because policies were anti-trade, anti-business, and flip-flopping every other day. So yes, I think that's enough to make the next 4 four years good; and actually, I think the next 8 years could be good—I'm predicting Dow 120,000 by 2030, if you recall.

Q: When do you expect the next 5% correction if there is one? February is always very volatile.

A: With an unlimited liquidity market like we have, it is really tough to see negatives of any kind. What kind of negatives are out there? The pandemic doesn’t stop—that's the main one. There’s another one people aren't talking about: the reason we got all these vaccines so fast is they took all regulation and threw it out the window. What if one of these vaccines kill off a million people? That would be pretty negative for the market. Interest rates could rocket faster than expected. But I’m always short there so that would be a moneymaker. But these are pretty out there possibilities, and that is why the market is not backing off, and when it does, it only gives us 5%.

Q: Is the Fed stimulating the economy too much?

A: The bond market says no with a ten-year yield of 1.10%, and the bond market is always the ultimate arbiter of when the stimulus ends. That’s because the Fed can’t directly control bond market interest rates, only overnight rates. But when we get bonds up to, say, a 3% yield (which is probably 2 or 3 years off), that’s when we’re getting too much stimulus, and we’ll probably take our foot off the pedal way before then. I know Janet Yellen and she agrees with me on this point. She’ll be throttling back well before we see a 3% yield in the Treasury market.

Q: Do you manage other people’s money?

A: No, because it costs a million dollars in legal fees to set up even a small fund these days. When I set up my hedge fund 30 years ago, there were no regulatory costs because no one knew what a hedge fund was; they all thought they were doing something illegal, so they didn't have to register for anything. That’s why it’s changed now.

Q: What is your target on NVIDIA (NVDA), and will it split?

A: It’s an easy double, with a global chip shortage running rampant. They make the best graphics cards in the world, bar none. These big tech companies tend not to split until they get share prices into the thousands, which is what Apple (AAPL) and what Tesla (TSLA) did three or four times.

Q: If we get 3.25% in bonds, is that going to hurt gold?

A: Yes, and that’s one of the reasons I bailed on my gold positions a couple of weeks ago. It effectively turned into a bond long. A sharp rise in interest rates is bad for gold because we all know that gold yields to zero.

Q: What about Fireye (FEYE)?

A: Yes, we also love Fireye in addition to Palo Alto Networks (PANW) because there is a near-monopoly—there are only about six players in the entire cybersecurity industry and hacking is getting worse by the day. Look at the Solar Winds (SWI) fiasco and the national Russian hack there.

Q: What about copper as a recovery play?

A: Well, I voted with my feet on Monday when I bought a position in Freeport McMoRan, after it just sold off 15%. I think (FCX) could double at some point in the coming economic recovery. So, copper is an absolute winner, and when having to choose between copper and steel, I’ll pick copper all day long.

Q: What do you recommend for gold (GLD)?

A: Gold is a trading range for the time being. Buy the dips, sell the rallies; you won’t get more than about 10% or 15% range on that. And there are just better fish to fry right now, like financials, which benefit from rising interest rates as opposed to being punished. Bitcoin is stealing gold’s thunder and the markets keep creating more Bitcoins.

Q: Should high-frequency trading be banned?

A: I don’t think it should be. It does create liquidity; the effect on the market is wildly overexaggerated. They’re basically trading for pennies or tenths of pennies, so they do provide buying on selloffs and selling at huge price spikes. They do have a positive effect and they’re probably only taking about $10 or $20 billion in profit a year out of the market.

Q: Should I buy Wynn Resorts (WYNN) here?

A: Buy the dips for sure; this is a major recovery play. We here in Nevada are expecting an absolute tidal wave of people to hit the casinos once the pandemic ends, and (WYNN), (MGM), and (LVS) would be a great play in those areas.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/lake-tahoe-sunrise.png460612Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-05 09:34:282021-02-05 08:16:16February 3 Biweekly Strategy Webinar Q&A

Stocks are tumbling on the back of substandard vaccine updates, with investors growing more wary of the whole COVID-19 vaccine narrative.

January ended with Novavax (NVAX) announcing that its COVID-19 vaccine candidate is roughly 90% effective, but doesn’t work as well against other more contagious strains in South Africa.

Johnson & Johnson (JNJ) reported that its candidate is only 66% effective at stopping moderate to severe strains of the coronavirus, but is 100% effective in preventing hospitalizations and even death 28 days after it gets administered.

However, the real kicker is Merck’s (MRK) decision to completely drop out of the COVID-19 vaccine race when both its candidates showed disappointing results in the early stages.

This is disappointing news considering that Merck is one of the biggest vaccine developers in the world today.

Nonetheless, Merck’s still not out of the COVID-19 race yet as it appears to be following the lead of Gilead Sciences (GILD) instead.

That is, it plans to focus on developing COVID-19 treatments in the hopes of benefiting from it the same way Gilead did in the past months.

Since the pandemic started, Gilead has been at the forefront of the fight – so much that its COVID-19 treatment, Remdesivir, is evidently having a major impact on the company’s top line.

In its third-quarter earnings report in 2020, Gilead reported $6.6 billion in total revenue, showing off a 17% jump from its performance during the same period last year.

If you exclude its COVID-19 sales, Gilead would have only earned $5.6 billion, with the increase in its year over year performance changing from 17% to just 2%.

As for its overall performance in 2020, Gilead announced that it’s raising its previous guidance from the $23 billion and $23.35 billion range to be somewhere between $24.3 billion and $24.35 billion.

This new guidance indicates a 10% year over year growth, but without Remdesivir, its product sales would actually show a slight decline compared to 2019.

Outside Remdesivir, Gilead has been active in searching for additional growth drivers.

So far, the most promising segment is its HIV lineup led by its top-selling product, Biktarvy, also known as "the gold standard in HIV treatment."

In the third quarter of 2020, sales of Gilead’s HIV line climbed by 8% to reach $4.5 billion.

While generic competition has entered the market, Biktarvy is expected to continue to gain steam in 2021.

Another catalyst in its HIV line is the drug Lenacapavir, which can either be developed as a twice-a-year injection or a weekly pill.

If successful, Lenacapavir can bring an additional $9 billion in revenue for Gilead.

Aside from HIV, Gilead has also been working toward becoming a leader in the oncology sector.

To achieve this, the company spent $21 billion for the acquisition of Immunomedics.

Specifically, Gilead bought the New Jersey-based company for its new breast cancer treatment, Trodelvy.

Gilead’s massive bet on Trodelvy raised a lot of eyebrows, but the product offers a very real chance for an enormous payoff for its shareholders.

Trodelvy lowers the risk of death among breast cancer patients by an impressive 52% when compared to those who receive standard care.

Annually, Trodelvy is estimated to rake in at least $1.8 billion in revenue for Gilead --- and that’s only for breast cancer application.

Gilead also intends to expand Trodelvy’s application to include more complex fields of oncology and even for some viral diseases.

Beyond its COVID-19 program, Gilead has an impressive portfolio of diverse assets that the company is focused on developing.

It currently has 42 clinical programs queued in its pipeline and at least a handful of these are anticipated to become steady sources of revenue.

As expected, it spent 2020 acquiring the necessary partners for its big picture plans, making 2021 a year of milestones for the company.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-02 14:00:562021-02-03 19:10:472021: Gilead Sciences’ Year of Milestones

Tesla (TSLA) has been sizzling hot for months now, and it looks like its Midas touch has reached the biotechnology world.

It seems that almost everything linked to Tesla achieves success. That could indicate terrific news for a particular biotech: CureVac (CVAC).

CureVac, an under-the-radar biotech stock, is closing in on the leading COVID-19 vaccine developers today.

A differentiating factor it has from the likes of Pfizer (PFE), BioNTech (BNTX), and Moderna (MRNA) is its bonafide tie-in with Tesla. Although it sounds like quite a stretch for an electric car company to have any involvement with a biotech stock, the connection actually makes sense.

Like Moderna and BioNTech, CureVac has also been working on utilizing messenger RNA (mRNA) technology to develop various vaccines and other treatments. If all goes well, this could even lead to finding a way to immunize people against cancer.

Where does Tesla come in?

It all started in 2019 when CureVac was awarded $34 million in funding by the Coalition for Epidemic Prepared Innovations (CEPI).

The goal was to create and eventually build a prototype of an mRNA “printer.” This high-tech tool would be used to produce mRNA doses in areas that suffer from viral outbreaks. It could be used by hospitals to create personalized medicines.

Having an mRNA printer would be groundbreaking in fighting off viral diseases, particularly in remote regions. As expected, this project faced many technology obstacles along the way.

Here’s where Tesla can offer a solution since one of the companies it acquired in the past years is Grohmann Engineering, which specializes in automated manufacturing.

This makes Tesla Grohmann Automation the logical partner for CureVac to turn for help in building its mRNA printer prototype.

What we know so far is that the two companies have been working closely on the project.

It’s only a matter of time before we find out if Tesla’s magic would once again blow our expectations out of the water and we are presented with yet another breakthrough.

Other than its alliance with Tesla in the mRNA race, CureVac has forged another partnership to transform itself into a stronger candidate in the COVID-19 vaccine competition.

CureVac has tapped into the global reach of Bayer (BAYN) to help it distribute its vaccine once it gains approval.

In terms of its own COVID-19 vaccine candidate, CureVac is anticipated to release positive results.

This is because its technology closely mirrors that used by Moderna and BioNTech, which strongly indicates that the efficacy levels could be just as good.

However, CureVac’s vaccine candidate offers a competitive advantage over the others: it doesn’t require cold storage.

This means it would be easier and more convenient to distribute it compared to Moderna’s and Pfizer’s.

It also requires a much smaller dose compared to Moderna’s COVID-19 vaccine candidate. This translates to cheaper manufacturing costs.

CureVac has secured a deal with the EU to deliver an initial 405 million doses for half of the year plus 300 million doses more in 2021 alone. It also agreed to produce 600 million doses in 2022.

Meanwhile, its alliance deal with Bayer indicates that it has secured a powerful distribution partner.

Therefore, we could expect CureVac to leverage Bayer’s global supply network to deliver its vaccines worldwide.

However, CureVac and Bayer are thinking way ahead of 2022.

The alliance formed by the two companies sees to it that the CureVac vaccine candidate would become the strongest contender in the post-pandemic years.

As per Bayer’s projection, the companies estimate 12 billion to 14 billion vaccine doses just to bring this pandemic under control.

Considering that COVID is expected to become an endemic disease, annual or even bi-annual vaccination programs would become the norm.

While Pfizer, Moderna, and AstraZeneca have been well ahead of the vaccine race, the door is still firmly open for other developers like Novavax (NVAX), Johnson & Johnson (JNJ), GlaxoSmithKline (GSK), Sanofi (SNY), and, of course, CureVac to launch their own COVID-19 vaccines.

Only going public in August 2020, this German biotech company already has $18.2 billion in market capitalization.

Its public offering of 15.3 million shares sold at $16 each generated $245.3 million for the company back in August.

By early December 2020, CureVac shares were already being traded somewhere around $150 as investors quickly began to realize the value proposition.

If I am to look to invest in a COVID-19 vaccine developer at this point, CureVac would surely be one of my choices.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-01-26 12:00:182021-01-27 20:09:34Emerging COVID-19 Alliances

Mad Hedge Biotech & Healthcare Letter January 21, 2021 Fiat Lux

FEATURED TRADE:

(IS JOHNSON & JOHNSON THE BEST CORONAVIRUS STOCK?) (JNJ), (MRNA), (PFE), (AZN), (NVAX)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-01-21 14:02:222021-01-21 14:20:19January 21, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.