You can’t watch a game without a program, and the lineup for biotech and healthcare is truly astonishing. No surprise then that the fields account for more or less than 17% of US GPD.

Here is a listing of the biggest $100 billion plus products you have never heard of. The good news is that you have just stumbled across a sector that will generate no less than a staggering $1.4 trillion in sales over the next five years.

That means it’s certainly worth your time getting to know this field. With this amount at stake, it’s no wonder companies manufacturing these blockbuster drugs are sparing no expense to fight off patent vultures.

A good example is Amgen (AMGN), which recently won its case to extend the patent life of rheumatoid arthritis biological Enbrel against Novartis AG’s (NOVN) biosimilar arm Sandoz. Since each extra hour added to patent life means millions of dollars (and sometimes billions) in sales, the additional 10 years of exclusivity for Enbrel is a massive victory for Amgen.

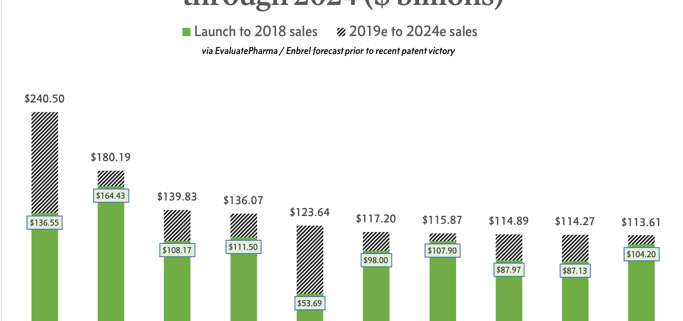

In a recent study released by Evaluate Pharma, Enbrel was ranked third in the top 10 biggest sellers up to 2024. The forward-looking consensus projection anticipates Amgen’s golden goose to hit roughly $140 billion in total revenues in five years – a truly impressive performance particularly for a drug that has been around for more than 20 years. However, Enbrel’s longevity pales in comparison to the other behemoths in the biopharma realm.

Up until 2018, Pfizer’s (PFE) Lipitor held the title of earning the highest lifetime sales in the industry. Since its launch in 1997, the cholesterol drug has raked in $164.4 billion in revenues so far with the number estimated to reach $180 billion by 2024. Lipitor’s success is highlighted more by the fact that it's under a small molecule status and holds approval for a very narrow indication.

Overtaking Lipitor to take the top spot is AbbVie’s (ABBV) rheumatoid arthritis treatment Humira, which closed with $20 billion in sales in 2018 alone. While some AbbVie investors frown upon the over-reliance of the company on Humira, it appears that the efforts to protect the drug has paid off big time.

With patent protection (132 approved patents!) safeguarding its exclusivity in the market, Humira is projected to reach a total of $240 billion in revenues by 2024. Clearly, the rewards they’ve been reaping show no signs of abating anytime soon.

More importantly, Humira’s robust sales, which makes up almost 70% of the company’s profits, has provided AbbVie with the financial capacity to finally get out of the shadow of parent company Abbott Laboratories (ABT) and come up with its own pipeline. As it happens, AbbVie’s efforts towards this direction have already started with the massive purchase of Allergan (AGN) for $63 billion this year.

Apart from Lipitor, Humira, and Enbrel, there are three more blockbuster products with sales that hit the $100 billion mark as of 2018 -- a figure that would make Ecuador proud to claim as their annual GDP. These are Roche Holding Ltd. Genussscheine’s (ROG) chemotherapy drug Rituxan, Amgen’s anemia treatment Epogen, and GlaxoSmithKline’s (GSK) asthma medication Advair.

One biopharma bestseller that leapfrogged a lot of other drugs in the market is multiple myeloma medication Revlimid -- aka the drug that built Celgene (CELG). With an entry date of 2008, this drug is the newest one on the list. While Revlimid’s sales are impressive, what’s actually quite exciting is the fact that its projected revenues easily outstrip its already notable sales of $53.69 billion.

By 2024, this Celgene blockbuster is estimated to reach $123.64 billion in sales. There’s a caveat to this though as Revlimid’s success in the years to come is dependent on how Celgene plans to deal with generic competition chomping at the bit and ready to attack once the drug reaches its 2022 patent expiration date.

Another big-ticket drug that might see a bit of a decline in sales soon is from Johnson & Johnson (JNJ). While the company has always been aggressive when it comes to dominating the market for its Crohn's Disease drug Remicade, an investigation by the Federal Trade Commission (FTC) might put a damper on things soon. According to recent reports, JNJ has been suspected of contracting payers to ensure market control and stave off competitors.

Meanwhile, the three horsemen of Roche, namely, Rituxan, cancer and eye disease medication Avastin, and breast cancer treatment Herceptin, reached a collective amount of $365 billion in total sales. These three are anticipated to stay put on top of the industry in the next five years as well, thanks to their competitive pricing and aggressive strategies to protect their patents.

Rounding out the list is Amgen’s Epogen, which is expected to add $107.90 billion to the already astounding $115.87 billion it generated for the company. Meanwhile, GSK’s Advair, which brought in $113.61 billion, is expected to pour in an additional $104.20 billion by 2024.

Interestingly, the majority of the top 10 franchise drugs are biologics except for Sanofi’s (SAN) ulcer treatment Zantac, Bristol-Myers Squibb Co’s (BMY) heart medication Plavix, Advair, and of course, Lipitor. In fact, this is considered as the primary reason for their capability to fight off potential copycats for years.

In some cases, their monopoly of the market has allowed them to expand to include various other indications in their coverage. The massive sales of biologics are also rooted in their ability to demand big-ticket reimbursements. Unlike their generic competitors, brand recognition alone makes it more convenient for patients to ask for compensation.

Needless to say, the success stories of these drugs make it quite obvious why these biopharma companies employ a battalion of legal experts to fend off the rise of generics. While the onslaught of biosimilars cannot be helped, these lawyers ensure that patients opting for these versions of the medication would find it incredibly difficult to ask for biosimilar reimbursements.