Global Market Comments

November 20, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WEEK THAT WAS)

(SPY), (TLT), (JNK), (NLY) (BA), (UUP),

(TLT), (FCX), (GLD), (GDX), (GOLD)

Global Market Comments

November 20, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WEEK THAT WAS)

(SPY), (TLT), (JNK), (NLY) (BA), (UUP),

(TLT), (FCX), (GLD), (GDX), (GOLD)

In the long history of stock markets, last week will be viewed as one of the pivotal ones of the 21st century. That was when investors flipped from anticipating the end of interest rate rises to the beginning of interest rate cuts.

That is a big deal.

I have been anticipating this for months, putting all my chips on the most interest rate-sensitive sectors: US Treasury bonds (TLT), Junk bonds (JNK), REITS (NLY), and big tech. The payoff has been huge, with some followers calling me up daily with literal tears of joy. They have just made the most money in their lives.

November has been the best month of the year, up 10% from the October low, and it's only half over.

And here is the good news. We are not only in the first inning of a new bull market for all risk assets but also the first pitch of the first at-bat of the first inning. 2024 should be one of the easiest trading years in a decade. This could go on for a decade.

This is how things will play out.

After the hottest quarter of GDP growth in three years at 4.9% in Q3, the economy is slowing. Virtually every business sector is seeing sales weaken, especially real estate and EVs.

That sets up a sharp drop in the inflation rate from the current 3.2% to the Fed’s target of 2%. Get a few months of that and the Fed starts cutting interest rates from the current 5.25%-5.5%. Fed futures are currently indicating a 40% probability that will happen in March.

We could be at 4.0% overnight interest rates by the end of 2024 and 3.0% by the end of 2025 when they stabilize. Stocks and bonds will eat this up.

Better hope that the Fed stays data dependent as promised, because coming data is weak, even if it doesn’t arrive for months. We only need one weak quarter to kill off inflation, and that quarter began on October 1.

Priority One is for the Fed to de-invert the yield curve or get short-term interest rates below long rates. For encouragement, the Fed should look at the most rapidly shrinking money supply in history, which I have been glued to.

There has been no monetary growth for two years, and zero bank deposit growth for three years. The Fed's balance sheet has plunged by $1.5 trillion in 18 months. Fed quantitative tightening continues at $120 billion a month. This is unprecedented in economic history.

The biggest risk to markets is that Powell delays cutting rates as much as he delayed raising rates two years ago. This is a very slow-moving, backward-looking Fed.

If you have a ten-year view of the markets, as I do, this is all meaningless. You need to buy stocks right now. If the Fed does play hardball and rigidly holds to the 2% target it risks causing a recession.

If you see any reasons to shoot down my bull case please, please email me. I’d love to hear them.

It’s not that stocks are expensive. 2024 S&P 500 (SPY) earnings are now 18X. If you take out the Magnificent Seven, they are at 15X earnings, close to the 2008 crash low. Small cap stocks are at a bargain basement 12X earnings and are already priced for recession.

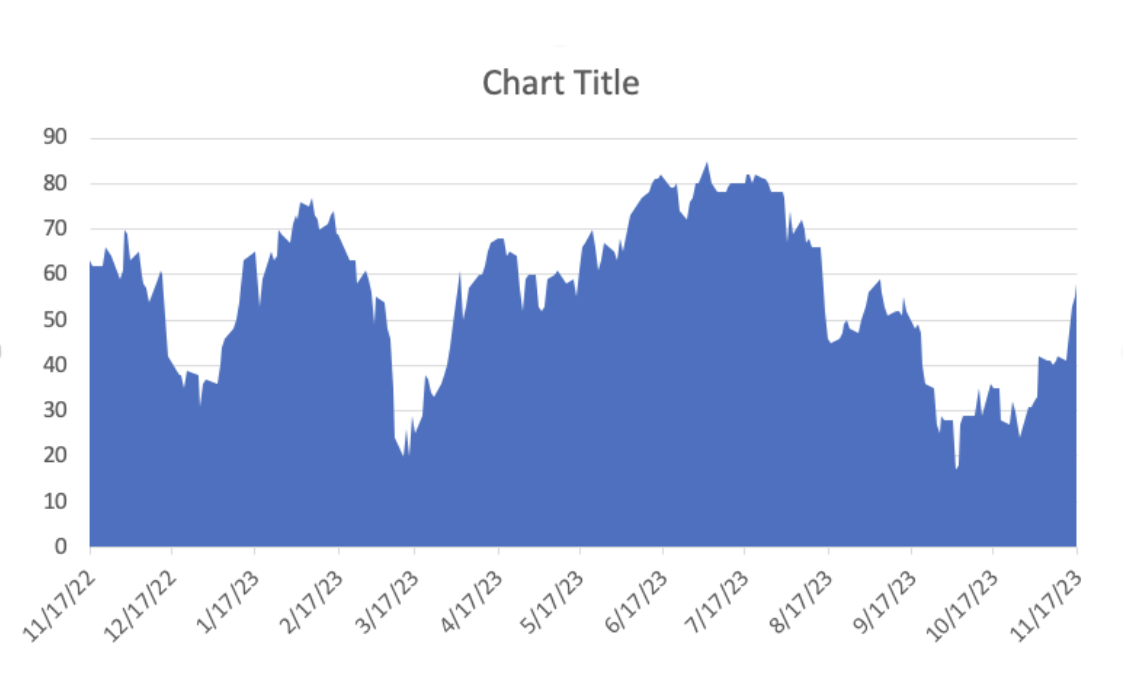

So a strong case for a new decade-long bull market is there. All you have to do is believe it. To see how this will play out look at the chart below as tech stocks are now extremely overbought short term. We no longer have the luxury of waiting for big dips. Small ones will have to do.

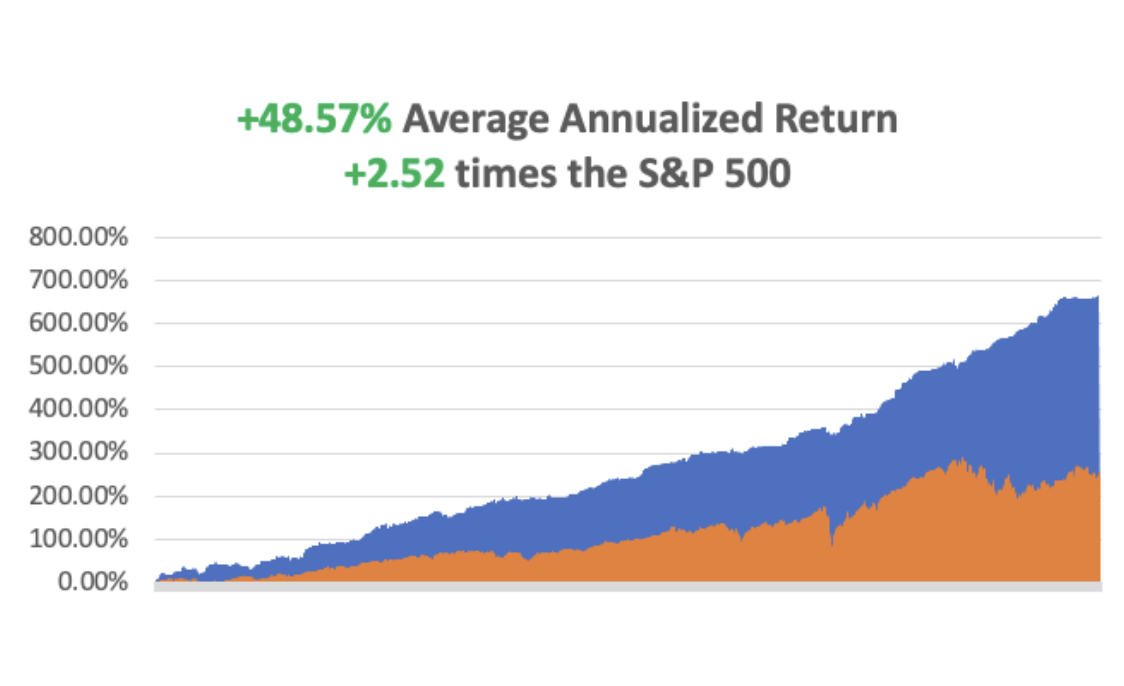

So far in November, we are up a breathtaking +12.59%. My 2023 year-to-date performance is still at an eye-popping +78.76%. The S&P 500 (SPY) is up +18.42% so far in 2023. My trailing one-year return reached +85.42% versus +20% for the S&P 500.

That brings my 15-year total return to +675.95%. My average annualized return ballooned to +48.57%, another new high, some 2.52 times the S&P 500 over the same period.

Some 60 of my 65 trades this year have been profitable.

CPI Comes in Flat at 3.2%, much weaker than expected. This is a game-changer. The first Fed rate cut has been moved up to May. Stocks and bonds loved it, taking ten-year US Treasury yield down to a six-week low at 4.44%. Shelter prices, which make up about a third of the overall CPI index, climbed 0.3%, half the prior month’s pace. Taking profits on my long in (TLT).

Fed to Cut Interest Rates as Early as March, or so says the futures market, which gives this a 40% probability. The (TLT) should top $100 and stocks will rocket, especially the interest sensitives. The most recent indications on the CME Group’s FedWatch gauge point to a full percentage point of interest rate cuts by the end of 2024.

Weekly Jobless Claims Hit Three Month High, up 13,000 to 231,000, as the US economy backs off from the superheated Q3. The path for a lower inflation rate is opening up. Do I hear 2%.

PPI Fell by 0.5% in October, a much bigger than expected drop, a three-year low. Inflation is fading fast. YOY came in at 1.3%. Stocks loved the news. 2024 is shaping up to be a great year for risk after two miserable ones.

Government Shutdown Delayed Until 2024, with the passage of a temporary spending bill by the House. It looks like there is a new coalition of the middle of both parties, as the bill passed with 339 votes, topping a two-thirds majority. The Johnson bill would fund some parts of the government through Jan. 19 and others through Feb. 2, setting up the possibility of yet another shutdown deadline on Groundhog Day.

The US Dollar (UUP) Takes a hit as the falling interest rate scenario starts to unfold. Even the Japanese yen rose. This could be a new decade-long trade. Currencies with falling interest rates are always the weakest.

Goldman Sachs Goes Bullish on Gold. The investment bank expects the S&P GSCI, a commodities markets index, to deliver a 21% return over the next 12 months as the broader economic environment improves, OPEC moves to support crude prices as refining is tight and with energy and gold acting as hedges against supply shocks. Buy (GLD), (GDX), and (GOLD) on dips.

Copper Bull Predicts 80% Gain in the Coming Decade, to $15,000 per metric tonne, up from $8,277 says Trafigura’s Kotas Bintas, the world’s largest metal trader. Exploding demand from EV makers is the reason, set to hit 20 million vehicles a year. Electrification of global energy sources is another. Buy (FCX) on dips.

Boeing Lands Monster Order, some $52 billion from Emirates Airlines for 90 new 777x’s and five 787’s. The stock rose 5% on the news. A giant China order is also lurking in the wings. Buy (BA) on dips.

Moody’s Rating Service Downgrades the US, citing deteriorating fiscal conditions and worsening chaos in Washington. However, it maintained its AAA Rating. Oh, and the government shut down on Friday. Buy (TLT) on the dip. Where else are investors going to go for quality?

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, November 20, no data of note were published.

On Tuesday, November 21 at 11:00 AM EST, the Minutes from the previous Fed meeting are released.

On Wednesday, November 22 at 8:30 AM, the Durable Goods are published.

On Thursday, November 23 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, November 24 at 2:30 PM the November S&P Flash PMI’s are published and the Baker Hughes Rig Count is printed.

As for me, I was invited to breakfast last week at the Incline Village Hyatt Hotel and was told to expect someone special, but they couldn’t tell me who for security reasons.

I was nursing a strong black coffee when a bulky figure with white hair wearing a Hawaiian shirt and thermal vest sat down at the table. It was Mike Love, lead singer of the Beach Boys.

During the 1950s, Mike’s dad was a regular visitor to Lake Tahoe, bringing his family up to camp on the then-vacant beaches. My family couldn’t have been far away.

When Mike made his fortune with one of the top rock groups of the 1960s, the natural thing to do was to buy an estate high up the mountain in Incline Village, Nevada with a great lake view. Like me, Mike fell for crystal-clear lake views in summer and spectacular snow-covered mountain vistas in winter. Local real estate agents refer to it as a “poor man’s Aspen.”

Mike ended up raising a family here, his kids eventually growing up and heading out to start their music groups. One was Wilson Phillips, made up of two of Mike’s daughters and the daughter of John Phillips of the Mamas and the Papas, who I taught how to swim at summer camp one year.

But Mike stayed. He loved the lake too much to leave so he made Incline his base for a touring schedule that ran up to a punishing 200 gigs a year.

Mike’s residence was something of a Tahoe insider’s secret. Those who knew where he lived kept the closely guarded secret. We have plenty of celebrities here, Larry Ellison, Mike Milliken, and Peoplesoft’s David Duffield, but Mike is the one everyone loves.

Mike, now 82, is not your typical rock star and I have known many. He is humble, self-effacing, and an alright guy. He avoided drugs and smoking to preserve his voice. He is a health fanatic. He has also been fighting a lifelong battle with depression which kept him off the touring circuit for years at a time and led to contemplations of suicide.

The Beach Boys formed in Hawthorne, California, a beachside suburb of Los Angeles in 1961. The group's original lineup consisted of brothers Brian, Dennis, and Carl Wilson, their cousin Mike Love, and friend Al Jardine. They were the original garage band. Together they created one of the greatest vocal harmonies of all time.

In 1963, the band enjoyed their first national hit with “Surfin USA”, beginning a string of top ten singles that reflected a southern California youth culture of surfing, cars, and teenage romance dubbed the “California sound.”

Those included "I Get Around", "Fun, Fun, Fun", "Help Me Rhonda", "Good Vibrations" and "Don't Worry Baby, which I’m sure you remember well. If you don’t, look them up on iTunes. Their 1966 album “Pet Sounds” was considered one of the most innovative ever produced.

I remember it like it was yesterday. They were one of the few groups that could stand up to the Beatles, who they became friends with. The Beach Boys were regulars on my car’s AM radio.

Buzz kill: the Beach Boys didn’t know how to surf.

All of the early Beach Boys songs were inspired by the Southern California beaches, but only half the country had beaches. So a new manager encouraged them to sing about cars, extending the life of the group by another decade. That is how we got “Little Deuce Coup,” and “409.” After all, the entire country owned cars.

The Beach Boys would eventually sell 100 million records second only to the Beatles. They were also one of the first groups to wrest production control away from the studios, a revolution for the industry that opened doors for generations of successive musicians.

In the late 1960s, the group took a religious bent, traveling to India to study under the celebrity guru Maharishi Mahesh Yogi. Mike has since been practicing transcendental meditation, and it probably saved his life.

By the 1970s, the California sound faded and was eventually killed off by disco. Their last album together was Endless Summer in 1974.

There are only three original Beach Boys left, and Mike Love alone is still touring. In 1983, Dennis Wilson drowned in a boating accident which is thought to be drug-related. In 1998, Carl Wilson died of lung and brain cancer after years of heavy smoking.

Mike was pleased that I recalled his 1980 London concert at Wembley Stadium. I had front-row seats; unaware that I would meet Mike 43 years later. In 1988, Mike was inducted into the Rock and Roll Hall of Fame.

Mike was very annoyed by the pandemic shutdown in 2020 because it prompted the cancelation of over 200 concerts worldwide. He still thinks Covid was fake. He doesn’t need to work as his royalties from 60 years of work are worth a fortune. He tours simply for the love of it.

Mike is now touring with a reconstituted Beach Boys. For their tour schedule, please click here. On November 17, 2023, Love released a special double album entitled “Unleash the Love” featuring 13 previously unreleased songs and 14 Beach Boys classics.

It was a pleasant way to spend a morning recalling the 1960s. It’s a miracle we both survived. It’s all proof that if you live long enough, you meet everyone.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

We’ve just seen our last interest rate rise in the economic cycle. Yes, I know that our central bank took no action at their last meeting in September. The market has just done its work for it.

And the markets are no shrinking violet when it comes to taking bold action. The 50 basis points it took bond yields up over the last two weeks is far more than even the most aggressive, economy-wrecking, stock market-destroying Fed was even considering.

And that doesn’t even include the rate hikes no one can see, the deflationary effects of quantitative tightening, or QT. That is the $1 trillion a year the Fed is sucking out of the economy with its massive bond sales.

It really is a miracle that the US economy is growing as fast as it is. After a warm 2.4% growth rate in Q2, Q3 looks to come in at a blistering 4%-5%. That is definitely NOT what recessions are made of.

Where is all this growth coming from?

Some of the credit goes to the pandemic spending, the free handouts we call got to avoid starvation while Covid ravaged the country. You probably don’t know this, but nothing happens fast in Washington. Government spending is an extremely slow and tedious affair.

By the time that contracts are announced, bids awarded, permits obtained, men hired, and the money spent, years have passed. That means money approved by Congress way back in 2020 is just hitting the economy now.

But that is not the only reason. There is also the long-term structural push that is a constant tailwind for investors:

Hyper-accelerating technology.

Yes, I know, there goes John Thomas spouting off about technology again. But it is a really big deal.

I have noticed that the farther away you get from Silicon Valley, the more clueless money managers are about technology. You can pick up more stock tips waiting in line at a Starbucks in Palo Alto than you can read a year’s worth of research on Wall Street.

What this means is that most large money managers, who are based on the east coast are constantly chasing the train that is leaving the station when it comes to tech.

On the west coast, managers not only know about the new tech, but the tech that comes after that and another tech that comes after that, if they are not already insiders in the current hot deal. This is how artificial intelligence stole a march on almost everyone, until a year ago, unless you were on the west coast already working in the industry. Mad Hedge has been using AI for 11 years.

You may be asking, “What does all of this mean for my pocketbook?” a perfectly valid question. It means that there isn’t going to be a recession, just a recession scare. That technology will bail us out again, even though our old BFF, the Fed, has abandoned us completely.

Which brings me to the current level of interest rates. I have also noticed that the farther away you get from New York and Washington, the less people know about bonds. On the west coast mention the word “bond” and they stare at you cluelessly. Indeed, I spent much of this year explaining the magic of the discount 90-day T-bill, which no one had ever heard of before (What! They pay interest daily?).

In fact, most big technology companies have positive cash balances. Look no further than Apple’s $140 billion cash hoard, which is invested in, you guessed it, 90-day T-bills when it isn’t buying its own stock, and is earning a staggering $7.7 billion a year in interest.

The great commonality in the recent stock market correction is easy to see. Any company that borrows a lot of money saw its stock get slaughtered. Technology stocks held up surprisingly well. That sets up your 2024 portfolio.

Put half your money in the Magnificent Seven stocks of Apple (AAPL), Amazon (AMZN), Meta (META), Microsoft (MSFT), Tesla (TSLA), (NVIDIA), and Salesforce (CRM).

Put your other half into heavy borrowers that benefit from FALLING interest rates, including bonds (TLT), junk bonds (JNK), (HYG), Utilities (XLU), precious metals (GOLD), (WPM), copper (FCX), foreign currencies (FXA), (FXE), (FXY), emerging markets (EEM).

As for me, I never do anything by halves. I’m putting all my money into Tesla. If I want to diversify, I’ll buy NVIDIA. Diversification is only for people who don’t know what is going to happen.

I just thought you’d like to know.

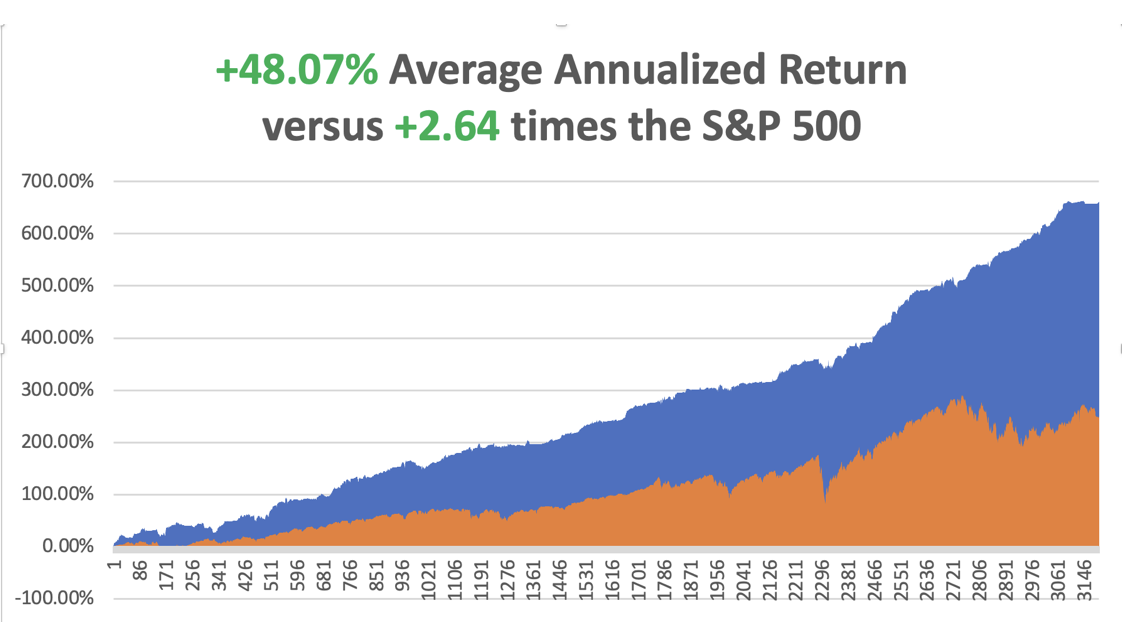

So far in October, we are up +2.96%. My 2023 year-to-date performance is still at an eye-popping +63.76%. The S&P 500 (SPY) is up +12.89% so far in 2023. My trailing one-year return reached +76.46% versus +22.57% for the S&P 500.

That brings my 15-year total return to +660.95%. My average annualized return has fallen back to +48.07%, another new high, some 2.64 times the S&P 500 over the same period.

Some 44 of my 49 trades this year have been profitable.

Chaos Reigns Supreme in Washington, with the firing of the first House speaker in history. Will the next budget agreement take place on November 17, or not until we get a new Congress in January 2025? Markets are discounting the worst-case scenario, with government debt in free fall. Definitely NOT good for stocks, which are reaching for a full 10% correction, half of 2023’s gains.

September Nonfarm Payroll Report Rockets, to 336,000, and August was bumped up another 50,000. The economy remains on fire. The headline Unemployment Rate remains steady at an unbelievable 3.8%. And that’s with the UAW strike sucking workers out of the system. This is supposed to by impossible with 5.5% interest rates. Throw out you economics books for this one!

JOLTS Comes in Hot at 9.61 million job openings in August, 700,000 more than the July report. The record labor shortage continues. Will the Friday Nonfarm Payroll Report deliver the same?

ADP Rises 89,000 in September, down sharply from previous months, showing that private job growth is growing slower than expected. August was revised down. It’s part of the trifecta of jobs data for the new month. The mild recession scenario is back on the table, at least stocks think so.

Weekly Jobless Claims Rise to 207,000, still unspeakably strong for this point in the economic cycle. Continuing claims were unchanged at 1.664%.

Traders Pile on to Strong Dollar, headed for new highs, propelled by rising interest rates. There is a heck of a short setting up for next year.

Yen Soars on suspected Bank of Japan intervention in the foreign exchange markets to defend the 150 line against the US dollar. The currency is down 35% in three years and could be the BUY of the century.

Kaiser Goes on Strike with 75,000 health care workers walking out on the west coast. The issue is money. The company has a long history of labor problems. This seems to be the year of the strike.

Oil (USO)Gets Slammed on Recession Fears, down 5% on the day to $85, in a clear demand destruction move and worsening macroeconomic picture. Europe and China are already in recession. It’s the biggest one-day drop in a year. Is the top in?

Tesla Delivers 435,059 Vehicles in September, down 5% from forecast, but the stock rose anyway. The Cybertruck launch is imminent, where the company has 2 million new orders. Keep buying (TSLA) on Dips. Technology is accelerating.

EVs have Captured an Amazing 8% of the New Car Market. They have been helped by a never-ending price war and generous government subsidies. EV sales are now up a miraculous 48% YOY and are projected to account for a stunning 23% of all California sales in Q3. Tesla is the overwhelming leader with a 52% share in a rapidly growing market, distantly followed by Ford (F) at 7% and Jeep at 5%. However, a slowdown may be at hand, with EV inventories running at 97 days, double that of conventional ICE cars. This could create a rare entry point for what will be the leading industry of this decade, if not the century. Buy more Tesla (TSLA) on bigger dips, if we get them.

Apple Upgrades New iPhone 15 to deal with overheating from third-party gaming. It will shut down some of its background activity, including some of the new AI functions, which were stressing the central processor. Third-party apps were adding to the problem, such as Uber and games from (META). This is really cutting-edge technology.

Moderna (MRNA) Bags a Nobel Prize in Chemistry. Katalin Kariko and Drew Weissman’s work helped pioneer the technology that enabled Moderna and the Pfizer Inc.-BioNTech SE partnership to swiftly develop shots. I got four and they saved my life when I caught Covid. I survived but lost 20 pounds in two weeks. It was worth it.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, October 9, there is no data of note released.

On Tuesday, October 10 at 8:30 AM EST, the Consumer Inflation Expectations is released.

On Wednesday, October 11 at 2:30 PM, the Producer Price Index is published.

On Thursday, October 12 at 8:30 AM, the Weekly Jobless Claims are announced. The Consumer Price Index is also released.

On Friday, October 13 at 1:00 PM the September University of Michigan Consumer Expectations is published. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, one of the many benefits of being married to a British Airways senior stewardess is that you get to visit some pretty obscure parts of the world. In the 1970s, that meant going first class for free with an open bar, and occasionally time in the cockpit jump seat.

To extend our 1977 honeymoon, Kyoko agreed to an extra round trip for BA from Hong Kong to Colombo in Sri Lanka. That left me on my own for a week in the former British crown colony of Ceylon.

I rented an antiquated left-hand drive stick shift Vauxhall and drove around the island nation counterclockwise. I only drove during the day in army convoys to avoid terrorist attacks from the Tamil Tigers. The scenery included endless verdant tea fields, pristine beaches, and wild elephants and monkeys.

My eventual destination was the 1,500-year-old Sigiriya Rock Fort in the middle of the island which stood 600 feet above the surrounding jungle. I was nearly at the top when I thought I found a shortcut. I jumped over a wall and suddenly found myself up to my armpits in fresh bat shit.

That cut my visit short, and I headed for a nearby river to wash off. But the smell stayed with me for weeks.

Before Kyoko took off for Hong Kong in her Vickers Viscount, she asked me if she should bring anything back. I heard that McDonald’s had just opened a stand there, so I asked her to bring back two Big Macs.

She dutifully showed up in the hotel restaurant the following week with the telltale paper bag in hand. I gave them to the waiter and asked him to heat them up for lunch. He returned shortly with the burgers on plates surrounded by some elaborate garnish and colorful vegetables. It was a real work of art.

Suddenly, every hand in the restaurant shot up. They all wanted to order the same thing, even though the nearest stand was 2,494 miles away.

We continued our round-the-world honeymoon to a beach vacation in the Seychelles where we just missed a coup d’état, a safari in Kenya, apartheid South Africa, London, San Francisco, and finally back to Tokyo. It was the honeymoon of a lifetime.

Kyoko passed away in 2002 from breast cancer at the age of 50, well before her time.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Sigiriya Rock Fort

Kyoko

Global Market Comments

August 18, 2023

Fiat Lux

Featured Trades:

(WEDNESDAY, SEPTEMBER 6, 2023 SAN DIEGO, CALIFORNIA GLOBAL STRATEGY LUNCHEON)

(TESTIMONIAL)

(AUGUST 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(SNOW), (PANW), (AMZN), (FCX), (WPM), (CCI), (GOLD), (WEAT), (JNK), (TLT), (X), (XOM), (HD), (AA), (UNG), (TSLA)

CLICK HERE to download today's position sheet.

Below please find subscribers’ Q&A for the August 16 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: Did you hear that Michael Burry was putting on a big short (the guy who made a fortune shorting housing in 2009)?

A: Yes, I heard that, but I never, ever trade-off of those kinds of comments. First of all, I think he’s wrong; and often, what happens in those situations is you hear about them going into the trade, but you never hear about them getting out, which might be tomorrow or next week. Also, there’s a nasty habit of big hedge fund managers telling you the opposite of what they’re actually doing. We hear big hedge fund traders like Bill Ackman getting super bearish at market bottoms, and then a few months later learn that they were buying with both hands, as was the case with the pandemic bottom. Be careful about other people’s opinions—they can be hazardous to your wealth. Just look at the data and the facts. That’s what I do.

Q: Would you buy Snowflake (SNOW) around current prices?

A: Yes—first of all Snowflake is a Warren Buffet favorite, which I always tend to follow. However, Warren can wait 5 years for a stock to work, and you can’t. So, I would wait for a bigger dip before getting into SNOW. So far, we are down 25% from the recent peak. One thing’s for sure, cybersecurity is a long-term winner, as seen by the ballistic move in Palo Alto Networks (PANW) since we started recommending it about 8 years ago.

Q: Why are US consumers so strong, and will that hold up for the rest of 2023?

A: US consumers are so strong because they banked so much money during 10 years of QE and all the pandemic stimulus, that they have a lot saved. They are now happy to spend to make up for the spending they couldn’t do during the pandemic. They’re basically in spending catch-up mode or revenge spending.

Q: How far do you see the iShares 20 Plus Year Treasury Bond ETF (TLT) go?

A: My worst-case scenario has it going to $90 down from $94—that’s a yield of about 4.50%. And that's where a lot of bond investors see fair value, and will start piling in. But as long as the momentum is against it, I’m not touching it. As soon as I am convinced there is a real bottom in the (TLT), I’m going to jump in with both hands and buy long-term LEAPS, where you can get a 100% or 200% return pretty quickly.

Q: Time to buy the Tesla (TSLA) dip?

A: We’re getting close. My guess is you might get a spike down to $200 from the recent $300 high. That’s also going to be LEAPS territory for us because the long-term outlook for this company is spectacular.

Q: What do you think of Freeport McMoRan (FCX), Silver (WPM), and United States Natural Gas Fund (UNG)?

A: I think they are all strong buys; I have LEAPS out on all of them. I think we start to get a big move in the 4th quarter of this year that’ll go well into next year—so big money just sitting on the table begging for you to take it.

Q: What are we to make of the crash of the Chinese Yuan?

A: The Chinese economy is weak and looks like it’s getting weaker. They still have a pandemic hangover. We don’t know what their real pandemic numbers are—they adopted our pandemic policy 2 years after we did, and they’re suffering as a result. They also insist on using their own vaccine, Sinovac, for nationalist reasons which is only 30% effective. But, when the Chinese economy does come back on stream, that’ll be the gasoline on the fire for the global economy, and that’s why we like commodities, industrials, energy, and so on.

Q: What does an 8% mortgage rate mean for the housing sector?

A: It is a disaster. I don’t think prices will drop very much—it’ll just cease all new buying because nobody qualifies for an 8% mortgage. They are going to either be only cash buyers out there or people waiting for the next drop in interest rates, and we’re already seeing that with the mortgage rate at 7.24%. If we do get a move up to 8%, it’ll just be a short-term spike that won’t last very long.

Q: Aren’t high-interest rates pushing rents higher?

A: Yes, absolutely. Since people can’t afford to buy houses, they are renting until they can, which pushes rental prices up and adds to the inflation numbers.

Q: When do you think the tech sector will rebound? It’s had a really bad three weeks.

A: End of August or sometime in September. I think. When people come back from the beach, they’re going to look at the long-term future of these companies and think “holy smokes,” why don’t I own more of these?” And we may even be doing LEAPS at high prices, which I almost never do, but the growth rate in tech next year is looking to be spectacular, and I think if we do a conservative at-the-money, we should at least double our money in a few months, similar to how US Steel (X) LEAPS did.

Q: Is Amazon (AMZN) a buy? They’re starting to develop their pharmacy rather well.

A: Yes, Amazon is on the buy list—it’s already up 50% this year. Jassy, the new CEO, is doing a great job. They also have a massive investment in AI which they can monetize anytime they want, and online pharmacies are a great place to start. They’ve been talking about doing that for at least 10 years.

Q: Are gold (GLD), wheat (WEAT), and precious metals a buy?

A: Yes, those are all strong buys on the dip.

Q: What about Tesla (TSLA) LEAPS?

A: Yes Tesla is definitely a LEAPS candidate $30 down from where it is now.

Q: What about Crown Castle International (CCI)?

A: CCI took a major hit from Verizon, canceling a contract with them (which is their biggest customer), so I want to wait for that to digest before I do anything yet. However, we are definitely approaching “BUY” territory; I think the yield is up to about 6.5% now.

Q: Should I take profits on the next jump up in United States Steel Corporation (X)?

A: Yes, it’s not worth hanging on 16 more months to maturity when there’s only 30% of the profit left. And, if all the takeover bids fail for some reason, the stock goes back to $20, and then your LEAPS becomes worthless. So, I would take profits; 100% profit in 2 months is nothing to turn up your nose at.

Q: How confident are you in (TLT) going to $110 by the end of the year?

A: Very confident; by then we will start seeing more hints of Fed interest rate cuts, inflation should be lower, and Goldman Sachs is in fact forecasting that the first rate cut will happen in March. So you’ll certainly start discounting that in the (TLT) by December. We could see the high in yields and the low in prices at the central bankers conference in Jackson Hole next week.

Q: What do you think about cruise lines and hotels right now?

A: The business is great, they’re all packed. However, during the pandemic, these sectors had to take on massive amounts of debt to keep from going under when their ships were tied up with zero revenue for two years; same with the hotels. So, the balance sheets are terrible in all of these areas including airlines. That’s why I’ve been avoiding them, too many better plays. Don’t go away from your core trades looking for trouble.

Q: When do we finally start seeing the Fed stop raising rates?

A: I think they already have; I think the most recent rate rise was the last one. If I’m wrong, they’ll do one more quarter—it’s totally dependent on the numbers.

Q: Won’t falling rates be bullish for bonds and gold?

A: Yes, that's why we’re buying them; but I’m waiting on the bond LEAPS—I want to see a firm bottom before getting back in there. 2024 will be all about falling interest rates plays.

Q: What’s causing the volatility in the United States Natural Gas Fund (UNG)?

A: A Strike in Australia, collapsing supplies in Europe (where prices are up 40%), and expectation of a global economic recovery in China. Ultimately, it’ll be China that takes this thing up to $10, $12, or $14 for the UNG, but you need them to recover first. That’ll probably happen next year, which is why we have the two-year LEAPS on there.

Q: With junk (JNK), have we seen the high rates?

A: Yes. If not, we’re very close, so it’s worth starting to scale in here.

Q: Should I short Home Depot (HD), as US consumers are holding back on home upgrades?

A: No, you should not short anything because you’re going against a long-term bull market trend that probably continues for another 10 years. So, any shorts should be measured in days and not weeks.

Q: Should I start chasing oil, because it’s been on quite a run, and should I buy Exxon (XOM)?

A: Yes, if we get an economic recovery next year, oil goes over 100 easily and will take all the oil companies up with it.

Q: Is (UNG) a domestic or foreign gas ETF?

A: It’s mostly domestic, and it’s a mix of the top natural gas producers in the US.

Q: Are the BRIC countries going to bring down the dollar?

A: You’ve got to be out of your mind. Would you rather store your money in China and Indonesia or the US? That’s your choice. I know there’s a lot of internet conspiracy theories out there—I get about a question a day on this. It’s Never going to happen; not in my lifetime. But it does attract internet traffic, which is the purpose of putting out these ridiculous stories like a BRIC-engineered digital currency replacing the dollar as a reserve currency. It’s just clickbait.

Q: Why is there a short squeeze in copper?

A: EV production is going from 2 million to 10 million a year in 2030, and every EV needs 200 pounds of copper. By the way, there are now 527 EV models on the market, but only one company makes money doing this, and that’s Tesla (TSLA).

Q: We’ve been waiting for a recession in the US for years, and US consumers are still going strong. What gives? I want rates to drop so I can invest in real estate again.

A: Well, yes. This recession has been predicted for 2 years. The problem is we have a certain political party telling us every day that the economy is the worst it’s ever been when, in actuality, the health of the economy is amazingly strong, and certainly the strongest economy in the world. So, I don't think we get a real recession until well into the 2030s because of massive technological development and a huge demographic tailwind—that’s an absolute winning combination, last seen in the 1990s. Plus, now we have AI accelerating everything. So, look at the numbers; don’t listen to opinions. Opinions can be fatal to your wealth.

Q: Does the use of an adjustable-rate loan make sense for the purchase of a second home?

A: Yes, it does. During the great interest rate spike of the 1980s, I bought my home in New York with an adjustable-rate loan. The initial interest rate was 18%, but when rates dropped to 11%, the value of the home tripled. Not a bad trade—and I bet the same kind of opportunity is out there now, provided you can get another adjustable-rate loan. By the way, in Europe, they only have adjustable-rate loans. The 30-year fixed anomaly only exists in the US and Canada because you have the US government as the unlimited buyer of last resort for 30-year fixed mortgages.

Q: Thoughts on other steel companies and aluminum?

A: I like them all. The country needs 200,000 miles of new long-distance transmission lines to accommodate the electrification of the economy, and those are all made out of aluminum except for the last mile—most people don’t know that. Buy Alcoa (AA).

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 17, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GOING AGAINST THE CONSENSUS),

(TLT), (MUB), (JNK), (HYG), (GLD), (SLV), (GOLD), (WPM), (FCX), (BHP), (EEM), (MS), (GS), (JPM), (BAC), (C), (BRK/B), (SPY), (QQQ), (IWM), (VIX)

Going against the market consensus has been working pretty well lately.

When the world prayed for a Santa Claus rally, I piled on the shorts. When traders expected a New Year January crash, I filled my boots with longs.

That’s how you earn an eye-popping 19.83% profit in a mere nine trading says, or 2.20% a day.

The other day, someone asked me how it is possible to get mind-blowing results like these. It’s very simple. Get insanely aggressive when everyone else is terrified, which I did on January 3. I also knew that with the Volatility Index (VIX) falling to $18, pickings would quickly get extremely thin. It was make money now, or never.

To quote my favorite market strategist, Yankees manager Yogi Berra, “No one goes to that restaurant anymore because it’s too crowded.”

My performance in January has so far tacked on a welcome +19.83%. Therefore, my 2023 year-to-date performance is also +19.83%, a spectacular new high. The S&P 500 (SPY) is up +3.78% so far in 2023.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 15 years ago. My trailing one-year return maintains a sky-high +103.30%.

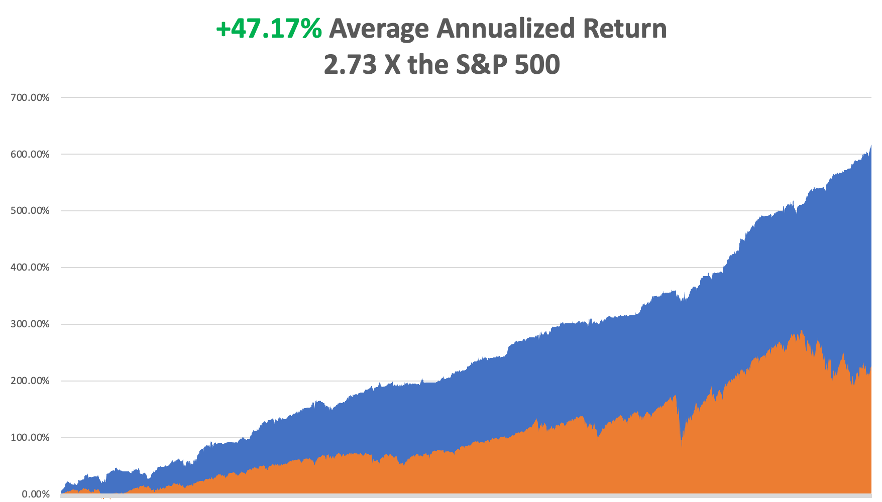

That brings my 15-year total return to +617.03%, some 2.73 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +47.17%, easily the highest in the industry.

I took profits in my February bonds last week (TLT), taking advantage of a $5 pop in the market. All my remaining positions are profitable, including longs in (GOLD), (WPM), (TSLA), (BRK/B), and (TLT), with 30% in cash for a 10% net long position.

Since my New Year forecasts have worked out so well, I will repeat the high points just in case you were out playing golf or bailing out from a flood when they were published.

Buy Falling Interest Rate Plays, as I expect the yield on the ten-year US Treasury yield to fall from 3.50% to 2.50% by yearend. That means Hoovering up any kind of bond, like (TLT), (MUB), (JNK), and (HYG). Falling interest rates also shine a great spotlight on precious metals like (GLD), (SLV), (GOLD), and (WPM).

The US Dollar Will Continue to Fall. Commodities love this scenario, including (FCX), (BHP), and emerging markets (EEM).

Inflation Will Decline All Year and should go below 4% by the end of 2023. In fact, we have had real deflation for the past six months. Financials do well here, like (MS), (GS), (JPM), (BAC), (C), and (BRK/B).

Which creates another headache for you, if not an opportunity. We may have a situation where the main indexes, (SPY), (QQQ), and (IWM) go nowhere, while individual stocks and sectors skyrocket. That creates a chance to outperform benchmarks…and everyone else.

There has been a lot of discussion among traders lately about the collapse of the Volatility Index ($VIX) to $18, a two-year low and what it means.

They are distressed because a ($VIX) this low greatly shrinks the availability of low risk/high return trading opportunities. A ($VIX) this low is basically shouting at you to “STAY AWAY!”

Does it mean that an explosion of volatility is following? Or are markets going to be exceptionally boring for the next six months?

Beats me. I’ll wait for the market to tell me, as I always do.

Current Positions

Risk On

(TSLA) 1/$75-$80 call spread 10.00%

(GOLD) 1/$15.50-$16.50 call spread. 10.00%

(WPM) 1/$$36-$39 call spread. 10.00%

(BRKB) 1/$290-$300 call spread 10.00%

Risk Off

(TLT) 1/$96-$99 call spread - 10.00%

(TLT) 1/$95-$98 call spread -20.00%

Total Net Position 10.00%

Total Aggregate Position 70.00%

Consumer Price Index Falls 0.1% in December, continuing a trend that started in June. Stocks popped and bonds rallied. YOY inflation has fallen to 6.5%. “RISK ON” continues. Now we have to wait another month to get a new inflation number. The economy has now seen de facto deflation for six months. Gas prices led the decline, now 9.4%. We might get away with only a 0.25% interest rate hike at the February 1 Fed meeting.

Bond Default Risk Rises, as well as a government shutdown, as radicals gain control of the House. This is the group that lost the most seats in the November election. Bonds are the only asset class not performing today, and paper with summer maturities is trading at deep discounts. It certainly casts a shadow over my 50% long bond position. However, I don’t expect it to last more than a month and my longest bond maturity is in February.

The US Consumer is in Good Shape, according to JP Morgan’s Jamie Diamond. Spending is now 10% greater than pre covid, and balance sheets are healthy. No sign of an impending deep recession here.

Boeing Deliveries Soar from 340 to 480 in 2022, and 479 new orders. A sudden aircraft shortage couldn’t have happened to a nicer bunch of people. The 737 MAX has shaken off all its design problems after two crashes four years ago. Cost-cutting here can be fatal. Europe’s Airbus is still tops, with 663 deliveries last year. Don’t chase the stock up here, up 79% from the October lows, but buy (BA) on dips.

Small Business Optimism Hits Six-Month Low to from 91.9 to 89.8, adding to the onslaught of negative sentiment indicators, so says the National Federation of Independent Business (NFIB).

Copper Prices Set to Soar Further with the post-Covid reopening of China, according to research firm Alliance Bernstein. After a three-year shutdown, there is massive pent-up demand. Copper prices are at seven-month highs. Keep buying (FCX) on dips.

Australian Metals Exports Soar, as the new supercycle in commodities gains steam. Shipments topped $9 billion in November, 20% higher than the most optimistic forecasts. Keep buying copper (FCX), aluminium (AA), iron ore (BHP), gold (GLD) and silver (SLV) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, January 16, markets are closed for Martin Luther King Day.

On Tuesday, January 17 at 8:30 AM EST, the New York Empire State Manufacturing Index is out

On Wednesday, January 18 at 11:00 AM, the Producer Price Index is announced, giving us another inflation read.

On Thursday, January 19 at 8:30 AM, the Weekly Jobless Claims are announced. US Housing Starts and Building Permits are printed.

On Friday, January 20 at 7:00 AM, the Existing Home Sales are disclosed. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, the University of Southern California has a student jobs board that is positively legendary. It is where the actor John Wayne picked up a gig working as a stagehand for John Ford which eventually made him a movie star.

As a beneficiary of a federal work/study program in 1970, I was entitled to pick any job I wanted for the princely sum of $1.00 an hour, then the minimum wage. I noticed that the Biology Department was looking for a lab assistant to identify and sort Arctic plankton.

I thought, “What the heck is Arctic plankton?” I decided to apply to find out.

I was hired by a Japanese woman professor whose name I long ago forgot. She had figured out that Russians were far ahead of the US in Arctic plankton research, thus creating a “plankton gap.” “Gaps” were a big deal during the Cold War, so that made her a layup to obtain a generous grant from the Defense Department to close the “plankton gap.”

It turns out that I was the only one who applied for the job, as postwar anti-Japanese sentiment then was still high on the West Coast. I was given my own lab bench and a microscope and told to get to work.

It turns out that there is a vast ecosystem of plankton under 20 feet of ice in the Arctic consisting of thousands of animal and plant varieties. The whole system is powered by sunlight that filters through the ice. The thinner the ice, such as at the edge of the Arctic ice sheet, the more plankton. In no time, I became adept at identifying copepods, euphasia, and calanus hyperboreaus, which all feed on diatoms.

We discovered that there was enough plankton in the Arctic to feed the entire human race if a food shortage ever arose, then a major concern. There was plenty of plant material and protein there. Just add a little flavoring and you had an endless food supply.

The high point of the job came when my professor traveled to the North Pole, the first woman ever to do so. She was a guest of the US Navy, which was overseeing the collection hole in the ice. We were thinking the hole might be a foot wide. When she got there, she discovered it was in fact 50 feet wide. I thought this might be to keep it from freezing over but thought nothing of it.

My freshman year passed. The following year, the USC jobs board delivered up a far more interesting job, picking up dead bodies for the Los Angeles Counter Coroner, Thomas Noguchi, the “Coroner to the Stars.” This was not long after Charles Manson was locked up, and his bodies were everywhere. The pay was better too, and I got to know the LA freeway system like the back of my hand.

It wasn’t until years later when I had obtained a high-security clearance from the Defense Department that I learned of the true military interest in plankton by both the US and the Soviet Union.

It turns out that the hole was not really for collecting plankton. Plankton was just the cover. It was there so a US submarine could surface, fire nuclear missiles at the Soviet Union, then submarine again under the protection of the ice.

So, not only have you been reading the work of a stock market wizard these many years, you have also been in touch with one of the world’s leading experts on Artic plankton.

Live and learn.

CLICK HERE to download today's position sheet.

1981 On Peleliu Island in the South Pacific

Global Market Comments

January 4, 2023

Fiat Lux

2023 Annual Asset Class Review

A Global Vision

FOR PAID SUBSCRIBERS ONLY

Featured Trades:

(SPX), (QQQ), (IWM) (AAPL), (XLF), (BAC) (JPM), (BAC), (C), (MS), (GS),

(X), (CAT), (DE),(TLT), (TBT), (JNK), (PHB), (HYG), (MUB), (LQD), (FXE), (EUO),

(FXC), (FXA), (YCS), (FXY), (CYB), (DIG), (RIG), (USO), (DUG), (UNG), (USO),

(XLE), (AMLP),(GLD), (DGP), (SLV), (PPTL), (PALL), (ITB), (LEN), (KBH), (PHM)

I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini could navigate it.

I am anything but Houdini, so I foray downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up to date with the onboard gossip.

The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 14 Pro Max.

Here is the bottom line which I have been warning you about for months. In 2023, we will probably top the 84.63% we made last year, but you are going to have to navigate the reefs, shoals, and hurricanes. Do it and you can laugh all the way to the bank. I will be there to assist you to navigate every step.

The first half of 2023 will be all about trading. After that, I expect markets to go straight up.

And here is my fundamental thesis for 2023. After the Fed kept rates too low for too long, then raised them too much, it will then panic and lower them again too fast to avoid a recession. In other words, a mistake-prone Jay Powell will keep making mistakes. That sounds like a good bet to me.

Let me give you a list of the challenges I see financial markets are facing in the coming year:

The Ten Key Variables for 2023

1) When will the Fed pivot?

2) How much of a toll will the quantitative tightening take?

3) How soon will the Russians give up on Ukraine?

4) When will buyers return to technology stocks from value plays?

5) Will gold replace crypto as the new flight to safety investment?

6) When will the structural commodities boom get a second wind?

7) How fast will the US dollar fall?

8) How quickly will real estate recover?

9) How fast can the Chinese economy bounce back from Covid-19?

10) How far will oil prices keep falling?

The Thumbnail Portfolio

Equities – buy dips

Bonds – sell buy dips

Foreign Currencies – buy dips

Commodities – buy dips

Precious Metals – buy dips

Energy – stand aside

Real Estate – buy dips

1) The Economy – Bouncing Along the Bottom

Whether we get a recession or not, you can count on markets fully discounting one, which it is currently doing with reckless abandon.

Anywhere you look, the data is dire, save for employment, which may be the last shoe to fall. Technology companies seem to be leading us in the right direction with never-ending mass layoffs. Even after relentless cost-cutting though, there are still 1.5 tech job offers per applicant, which is down from last year’s three.

The Fed is currently predicting a weak 0.5% GDP growth rate for 2023, the same feeble rate we saw for 2022. What we might get is two-quarters of negative growth in the first half followed by a sharp snapback in the second half.

Whatever we get, it will be one of the mildest recessions or growth recessions in American economic history. There is no hint of a 2008-style crash. The banking system was shored up too well back then to prevent that. Thank Dodd/Frank.

So far, so good.

2) Equities (SPX), (QQQ), (IWM) (AAPL), (XLF), (BAC) (JPM), (BAC), (C), (MS), (GS), (X), (CAT), (DE)

Since my job is to make your life incredibly easy, I am going to narrow my equity strategy for 2023.

It's all about falling interest rates.

When interest rates are high, as they are now, you only look at trades and investments that can benefit from falling interest rates.

In the first half, that will be value plays like banks, (JPM), (BAC), (C), financials (MS), (GS), homebuilders (KBH), (LEN), (PHM), industrials (X), capital goods (CAT), (DE).

As we come out of any recession in the second half, growth plays will rush to the fore. Big tech will regain leadership and take the group to new all-time highs. That means the volatility and chop we will certainly see in the first half will present a generational opportunity to get into the fastest-growing sectors of the US economy at bargain prices. I’m talking Cadillacs at KIA prices.

A category of its own, Biotech & Healthcare should do well on their own. Not only are they classic defensive plays to hold during a recession, technology and breakthrough new discoveries are hyper-accelerating. My top three picks there are Eli Lily (ELI), Abbvie (ABBV), and Merck (MRK).

Block out time on your calendars because whenever the Volatility Index (VIX) tops $30, I am going pedal to the metal, and full firewall forward (a pilot term), and your inboxes will be flooded with new trade alerts.

There is another equity subclass that we haven’t visited in about a decade, and that would be emerging markets (EEM). After ten years of punishment by a strong dollar, (EEM) has also been forgotten as an investment allocation. We are now in a position where the (EEM) is likely to outperform US markets in 2023, and perhaps for the rest of the decade.

3) Bonds (TLT), (TBT), (JNK), (PHB), (HYG), (MUB), (LQD)

Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, and dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites are returning home by train because their religion forbade automobiles or airplanes.

The national debt ballooned to an eye-popping $30 trillion in 2021, a gain of an incredible $3 trillion and a post-World War II record. Yet, as long as global central banks are still flooding the money supply with trillions of dollars in liquidity, bonds will not fall in value too dramatically. I’m expecting a slow grind down in prices and up in yields.

The great bond short of 2021 never happened. Even though bonds delivered their worst returns in 19 years, they still remained nearly unchanged. That wasn’t good enough for the many hedge funds, which had to cover massive money-losing shorts into yearend.

Instead, the Great Bond Crash will become a new business. This time, bonds face the gale force headwinds of three promised interest rate hikes. The year-end government bond auctions were a complete disaster.

Fed borrowing continues to balloon out of control. It’s just a matter of time before the last billion dollars in government borrowing breaks the camel’s back.

That makes a bond short a core position in any balanced portfolio. Don’t get lazy. Make sure you only sell a rally lest we get trapped in a range, as we did for most of 2021.

A Visit to the 19th Century

4) Foreign Currencies (FXE), (EUO), (FXC), (FXA), (YCS), (FXY), (CYB)

With a major yield advantage over the rest of the world, the US dollar has been on an absolute tear for the past decade. After all, we have the world’s strongest economy.

That is about to end.

If your primary assumption is that US interest rates will see a sharp decline sometime in 2023, then the outlook for the greenback is terrible.

Currencies are driven by interest rate differentials and the buck is soon going to see the fastest shrinking yield premium in the forex markets.

That shines a great bright light on the foreign currency ETFs. You could do well buying the Australian Dollar (FXA), Euro (FXE), Japanese yen (FXE), and British Pound (FXB). I’d pass on the Chinese yuan (CYB) right now until their Covid shutdowns end.

5) Commodities (FCX), (VALE), (DBA)

Commodities are the high beta play in the financial markets. That’s because the cost of being wrong is so much higher. Get on the losing side of commodities and you will be bled dry by storage costs, interest expenses, contangos, and zero demand.

Commodities have one great attribute. They predict recessions earlier than any other asset class. When they peaked in March of 2022, they were screaming loud and clear that a recession would hit in early 2023. By reversing on a dime on October 14, they also told us that the recovery would begin in July of 2023.

You saw this in every important play in the sector, including Broken Hill (BHP), Peabody Energy (BTU), Freeport McMoRan (TCX), and Alcoa Aluminum (AA). Excuse me for using all the old names.

The heady days of the 2011 commodity bubble top are about to replay. Now that this sector is convinced of a substantially weaker US dollar and lower inflation, it is once more a favorite target of traders.

China will still demand prodigious amounts of imported commodities once its pandemic shutdown ends, but not as much as in the past. Much of the country has seen its infrastructure built out, and it is turning from a heavy industrial to a service-based economy, much like the US. Investors are keeping a sharp eye on India as the next major commodity consumer.

And here’s another big new driver. Each electric vehicle requires 200 pounds of copper and production is expected to rise from 1 million units a year to 25 million by 2030. Annual copper production will have to increase three-fold in a decade to accommodate this increase, no easy task, or prices will have to rise.

The great thing about commodities is that it takes a decade to bring new supply online, unlike stocks and bonds, which can merely be created by an entry in an excel spreadsheet. As a result, they always run far higher than you can imagine.

Accumulate all commodities on dips.

6) Energy (DIG), (RIG), (USO), (DUG), (UNG), (XLE), (AMLP)

Energy was the top-performing sector of 2022. But remember, you will be trading an asset class that is eventually on its way to zero sooner than you think. However, you could have several doublings on the way to zero. This is one of those times.

The real tell here is that energy companies are bailing on their own industry. Instead of reinvesting profits back into their future exploration and development, as they have for the last century, they are paying out more in dividends and share buybacks.

Take the money and run.

There is the additional challenge in that the bulk of US investors, especially environmentally friendly ESG funds, are now banned from investing in legacy carbon-based stocks. That means permanently cheap valuations and share prices for the energy industry.

Energy now counts for only 5% of the S&P 500. Twenty years ago, it boasted a 15% weighting.

The gradual shutdown of the industry makes the supply/demand situation infinitely more volatile.

Unless you are a seasoned, peripatetic, sleep-deprived trader, there are better fish to fry.

And guess who the world’s best oil trader was in 2022? That would be the US government, which drew 400 million barrels from the Strategic Petroleum Reserve in Texas and Louisiana at an average price of $90 and now has the option to buy it back at $70, booking a $4 billion paper profit.

The possibility of a huge government bid at $70 will support oil prices for at least early 2023. Whether the Feds execute or not is another question. I’m advising them to hold off until we hit zero again to earn another $18 billion. Why we even have an SPR is beyond me, since America has been a large net energy producer for many years now. Do you think it has something to do with politics?

To understand better how oil might behave in 2023, I’ll be studying US hay consumption from 1900-1920. That was when the horse population fell from 100 million to 6 million, all replaced by gasoline-powered cars and trucks. The internal combustion engine is about to suffer the same fate.

7) Precious Metals (GLD), (DGP), (SLV), (PPTL), (PALL)

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly that it blew a passenger train over on its side.

In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year.

We also see countless abandoned 19th century gold mines and the broken-down wooden trestles leading to huge piles of tailings, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

Fortunately, when a trade isn’t working, I avoid it. That certainly was the case with gold last year.

2022 was a terrible year for precious metals until we got the all-asset class reversal in October. With inflation soaring, stocks volatile, and interest rates soaring, gold had every reason to fall. Instead, it ended up unchanged on the year, thanks to a 15% rally in the last two months.

Bitcoin stole gold’s thunder until a year ago, sucking in all of the speculative interest in the financial system. Jewelry and industrial demand were just not enough to keep gold afloat. That is over now for good and that is why gold is regaining its luster.

Chart formations are starting to look very encouraging with a massive head-and-shoulders bottom in place. So, buy gold on dips if you have a stick of courage on you, which I hope you do.

Higher beta silver (SLV) will be the better bet as it already has been because it plays a major role in the decarbonization of America. There isn’t a solar panel or electric vehicle out there without some silver in them and the growth numbers are positively exponential. Keep buying (SLV), (SLH), and (WPM) on dips.

8) Real Estate (ITB), (LEN), (KBH), (PHM)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the Transcontinental Railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley.

Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

Those in the grip of a real estate recession take solace. We are in the process of unwinding 2022’s excesses, but no more. There is no doubt a long-term bull market in real estate will continue for another decade, once a two year break is completed.

There is a generational structural shortage of supply with housing which won’t come back into balance until the 2030s. You don’t have a real estate crash when we are short 10 million homes.

The reasons, of course, are demographic. There are only three numbers you need to know in the housing market for the next ten years: there are 80 million baby boomers, 65 million Generation Xers who follow them, and 86 million in the generation after that, the Millennials.

The boomers (between ages 58 and 76) have been unloading dwellings to the Gen Xers (between ages 46 and 57) since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That’s what caused the financial crisis. That has created a massive shortage of housing, both for ownership and rentals.

There is a happy ending to this story.

Millennials now aged 26-41 are now the dominant buyers in the market. They are transitioning from 30% to 70% of all new buyers of homes. They are also just entering the peak spending years of middle age, which is great for everyone.

The Great Millennial Migration to the suburbs and Middle America has just begun. Thanks to the pandemic and Zoom, many are never returning to the cities. That has prompted massive numbers to move from the coasts to the American heartland.

That’s why Boise, Idaho was the top-performing real estate market, followed by Phoenix, Arizona. Personally, I like Reno, Nevada, where Apple, Google, Amazon, and Tesla are building factories as fast as they can.

As a result, the price of single-family homes should continue to rise during the 2020s, as they did during the 1970s and the 1990s when similar demographic forces were at play.

This will happen in the context of a labor shortfall, soaring wages, and rising standards of living.

Rising rents are accelerating this trend. Renters now pay 35% of their gross income, compared to only 18% for owners, and less, when multiple deductions and tax subsidies are considered. Rents are now rising faster than home prices.

Remember, too, that the US will not have built any new houses in large numbers in 16 years. The 50% of small home builders that went under during the Financial Crisis never came back.

We are still operating at only a half of the 2007 peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

There is a new factor at work. We are all now prisoners of the 2.75% 30-year fixed rate mortgages we all obtained over the past five years. If we sell and try to move, a new mortgage will cost double today. If you borrow at a 2.75% 30-year fixed rate, and the long-term inflation rate is 3%, then, over time, you will get your house for free. That’s why nobody is selling, and prices have barely fallen.

This winds down towards the end of 2023 as the Fed realizes its many errors and sharply lowers interest rates. Home prices will explode…. again.

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now after you throw in all the tax breaks. It’s also a great inflation play.

That means the major homebuilders like Lennar (LEN), Pulte Homes (PHM), and KB Homes (KBH) are a buy on the dip.

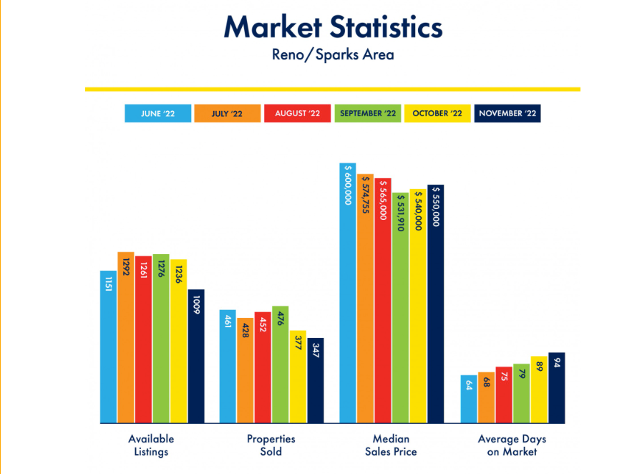

Recent Reno Real Estate Statistics

9) Postscript

We have pulled into the station at Truckee amid a howling blizzard.

My loyal staff has made the ten-mile trek from my estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 50 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my MacBook Pro and iPhone, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above, which should be soon.

Good luck and good trading in 2023!

John Thomas

The Mad Hedge Fund Trader

Global Market Comments

November 18, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (JNK), (HYG) or (TLT), (UUP), (FXE), (FXC), (FXA), (ALB), (FCX), (PYPL), (FXI), (GLD), (CCJ), (BHP), (RCL)