Below please find subscribers’ Q&A for the November 16 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: What do you see Tesla (TSLA) moving to from here until next year?

A: Not much; I mean if you’re lucky, Tesla won’t move at all. The problem is Twitter is looking like a disaster of huge proportions—firing half the staff on day one? Never good for building a business. Tesla has also been tied to the rest of big tech, which has been in awful condition and may not see a continuous move upward until the Fed actually starts lowering interest rates in the second quarter of next year. Tesla could be dead money here for a while; eventually, a company growing at 50% a year will go up—especially when it’s just had a 50% decline in the share price. As to when that is, I don’t know, and asking me 15 more times will get you just the same answer.

Q: Should we start piling into iShares 20 Plus Year Treasury Bond ETF (TLT) longs now or wait?

A: You go now. Every day you waited meant paying one point more in TLT. I think the bottom is in; we have a 20-30 point move ahead of us. Everybody in the world is now trying to get into this trade, just like I spent all this year trying to get out of it. And if anything, November CPI could be a long term-term top in inflation, especially if we came in with another cold number. So, I would start scaling in now, even though we’re over $100 in the (TLT) today and I first recommended this around $95.

Q: If the Fed keeps raising interest rates, will the US Treasury market fall?

A: Probably not because the Fed only has control of overnight interest rates—the discount rate, the interbank rate—whereas the (TLT) is a 10-to-20-year maturity bond. No matter what short term rates do, the inversion will just keep getting bigger, but in fact, the bond market itself was yielding 4.46%, yielding 8% with junk, has bottomed and will probably start going up from here. So that is the difference between the Fed and what the actual market does.

Q: Do you prefer Junk (JNK), (HYG), or (TLT)?

A: I always go for the highest risk. Junk has about an 8% yield here compared to 3.75% for the TLT. By the way, if you want to do one trade and go to sleep, buy the junk on 2 to 1 margin, get your 16% yield next year, and just take a one-year vacation. That’s what some people do.

Q: When you say the dollar is going to go down what do you mean?

A: I mean the US dollar, while Canadian (FXC) and Australian dollars (FXA) will go up.

Q: What is the best time to buy US dollars?

A: Maybe in five years, as it could go down for five or 10 years from here, now that it’s going to imminently give up its yield advantage.

Q: What's the forecast for casinos?

A: I think casinos do better. Las Vegas was absolutely packed, you couldn’t get into the best hotels—people are spending money like crazy.

Q: What’s the best way to play (TLT)?

A: With a one-year LEAP. I put out the $95/$100 last week for my concierge members. Here, you probably want to do the $100/$105; that’ll still give you a one-year return of 100%.

Q: How do you short the dollar?

A: There are loads of short dollar ETFs out there, or you can just sell short the Invesco DB US Dollar Index Bullish Fund (UUP), which is the dollar basket, or buy the (FXA) or (FXE).

Q: Freeport McMoRan (FCX) just went from 25 to 38; is it time to take a profit and re-enter at a lower point?

A: Short term yes, long term no. My long-term target for (FCX) is $100 because of the exponential growth of copper demand caused by EV production going from 1.5 million to 20 million a year in the next 10 years. Each EV needs 200 pounds of copper, so by 2030, annual copper demand for EVs only will be 20 billion pounds. In 2021, the total annual global copper production was 46.2 billion pounds. In order words, global copper production has to double in eight years just to accommodate EV growth only.

Q: Do you think there’ll be a rail worker strike?

A: I have no idea, but it will be a disaster if there is. There’s your recession scenario.

Q: What strike prices do you like for a Tesla LEAP?

A: Anything above here really. You could be cautious and do something like a $200/$210 two years out—that has a double in it. Or you could be more adventurous and go for a 400% return with like a $250/$260 in two years. I’m almost sure that we’ll have a major recovery in Tesla within two years.

Q: What’s your opinion on PayPal (PYPL) and Albemarle (ALB)?

A: I’m trying to stay away from the fintech area, partly because it’s tech and partly because the banks are recapturing a lot of the business they were losing to fintech a couple of years ago by moving into fintech themselves. That is the story and we’re clearly seeing that in the share prices of both banks and PayPal. I like Albemarle because the demand for lithium going forward is almost exponential.

Q: What’s your thought on the Australian dollar (AUD)?

A: Buy it with both hands as it is going to parity. Australia is a great indirect play on trade with China (FXI), gold (GLD), uranium (CCJ), and iron ore (BHP). It’s a great play on the recovery of the global economy, which will start next year.

Q: What do you think about Royal Caribbean Cruises Ltd (RCL)?

A: Probably a buy but remember all the cruise lines will be impaired to some extent by the massive debts they had to take on to survive two years of shutdown with the pandemic. I took the Queen Victoria last July on their Norwegian Fjord cruise, and it had not been operated for two years. None of the staff had any idea what to do. I had to show them.

Q: Will big tech have a good second half?

A: Probably, but it’s going to be a slow first quarter, and I think if we start getting actual cuts in interest rates, then it’s going to be off to the races for tech and they’ll all go to all-time highs as they always do.

Q: How come you haven’t issued any trade alerts yet on the currencies?

A: Calling a five-year turnaround is a big job. Now that we have the turnaround in play, we’re in dip-buying mode. So, you will see these in the future. But I also have to look at what currency trades are offering compared to other trades in other asset classes. And for the last year or two, the big opportunities have all been in stocks. You had volatility constantly visiting the mid $30s, you didn’t get that in the currencies, and more money was to be made in stock trades than foreign currency trades. That is changing now; let's see if we have a sustainable trend and if we get a good entry point. There’s a lot that goes into these trade alerts that you don’t always get to see. We only get a 95% success rate by being very careful in sending out trade alerts and that means long periods of doing nothing when the risk/reward is mediocre at best, which is right now. The services that guarantee you a trade alert every day all lose money.

Q: What is the recommended minimum portfolio size to amortize the cost of the concierge service?

A: I tell people to have a half a million in assets because we want people who are financially sophisticated to understand what we’re telling them. That said, we do have people with as little as 100,000 in the concierge service and they usually make the money back on the first trade. This is a very sophisticated high-return, very active service. You get my personal cell phone number and all that, plus your own dedicated website, and specific concierge-only research. It’s a much higher level of service. It’s by application only and we currently have no places available for new concierge members. However, if you’re interested, we can put you on the waitlist so that when another millionaire retires, we can open up a space.

Q: Despite recent moves, the algo looks bearish. There are lots of mixed signals.

A: Yes, it does. And yes, that’s often the case when the market timing index hangs around 50.

Q: Do concierges go for short term moves?

A: No, concierges are looking for the big, long-term trades that they can just buy and forget about. That is where the big money is made. At least 90% of the people that try day trading lose money but make all the brokers rich.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or Technology Letter, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/John-with-fish-story-3-e1524263315551.jpg378300Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-18 10:02:302022-11-18 11:44:34November 16 Biweekly Strategy Webinar Q&A

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE TOP FIVE TECHNOLOGY STOCKS OF 2023),

(RIVN), (ROM), (ARKK), (PANW), (CRM), (FXE), (FXY), (FXA), (LEN), (KBH), (DHI), (TLT), (UUP), (META), (TSLA), (BA), (JNK), (HYG), (BRKB), (USO)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-14 10:04:422022-11-14 11:24:00November 14, 2022

The year 2022 has been driven by rising interest rates, a strong dollar, a weak economy, a bear market in stocks.

A massive reversal is about to take place. 2023 will gain the benefit of gale force macroeconomic tailwinds for the right stocks.

So far this year, Mad Hedge earned an astounding 77.20% profit cashing in on this year’s trends. We could earn the same return taking advantage of next year’s trends.

If you want to ride along on my coattails next year, that is fine with me. But it requires you to take a leap of faith.

I refer you to the motto of Britain’s Special Air Service: “Qui audet adipiscitur,” or “Who dares wins.”

For it only makes sense that the worst stocks of 2022 will be the best performers of 2023.

I have no doubt that tech stocks will bottom out sometime in 2023. Those who get in early will build some of the largest fortunes of this century. Those who miss the boat will spend their retirement years working at Taco Bell.

The reasons are very simple.

*Ultra-high interest rates will force a mild recession in early 2023. Then suddenly, inflation will plummet. We know this has already started because the largest element in the inflation calculation is housing costs, which are in free fall.

*The Fed will panic and deliver 2023 the sharpest DECLINE in interest rates in American history.

*Plunging interest rates will bring a crash in the US dollar.

*Foreign currencies like the Euro (FXE), the Japanese Yen (FXY), and the Australian dollar (FXA) will soar.

*And guess who gets the bulk of their earnings from abroad, sometimes up to two-thirds? The technology industry.

Kaching!

If you think I’m out of my mind, just look at the top performers of the historic stock market rally last week.

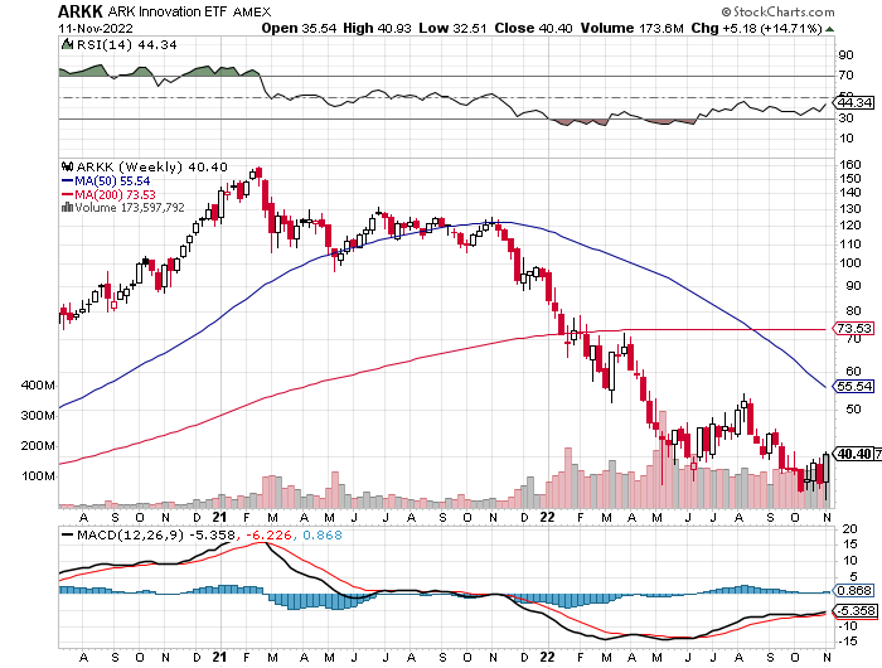

All the interest rate-sensitive sectors caught on fire. Technology stocks took off like a scalded cat, with Cathie Woods’ Ark Innovation Fund (ARKK) up an astounding 14% in a single day.

Bank shares soared. Homebuilders (LEN), (KBH), (DHI) caught a strong bid for the first time in ages. Junk bonds went bid only. US Treasury Bonds had their best day in 20 years (TLT), while the greenback (UUP) had its worst.

The bottom line here is so clear that I’ll write it on a wall for you. Falling interest rates will be the primary driver of stock prices for 2023 and 2024.

Of course, there is a better way to play this than buying the first technology index you stumble across.

So, let me boil this strategy down to just five names, close your eyes, and buy them.

Rivian (RIVN)– ($34) - Rivian is widely believed to be the next Tesla (TSLA). Some 25% owned by its largest customer, Amazon (AMZN), Rivian produces three types of EVs: the R1T pickup truck, the R1S SUV, and Amazon's EDV (electric delivery van). Its R1 vehicles start at under $70,000 and can travel more than 300 miles on a single charge. To learn more about Rivian, please click here.

To say that Rivian is the hot car of the day would be a vast understatement. New cars are trading for double list on the grey market. Owners complain of getting mobbed with gawkers whenever they hit the beach or the ski slopes. The buzz has led to an outstanding order book of an impressive 98,000, or four years of current production. The obvious cool factor allows enormous pricing power.

And here is the key to buying Rivian at this time. At 25,000, it is right at the mass production point where Tesla shares went ballistic all those years ago. And it already has an 80% decline in the price, in the rear-view mirror.

In 2024, Rivian plans to open its second plant in Georgia. After it fully expands its Illinois plant, it expects its annual production capacity to reach 600,000 vehicles.

Inflation Reduction Act passed this summer greatly accelerated rollout of the entire EV industry, which created a $7,500 per vehicle tax credit on top of state benefits.

Yes, this company offers venture capital-type risks. But it offers venture capital-type returns as well, up 10X-50X from here.

Ark Innovation Fund (ARKK) – ($40) – Cathie Woods’ high-tech fund was the proverbial red-headed stepchild of this bear market. It fell a gut-punching 80% from the 2021 top until last week. Just to get back to its old high, likely over the next five years, it has to rise by 400%. Its largest holdings are a real rollcall of the severely abused, Tesla (TSLA), Roku (ROKU), Exact Sciences (EXAS), Intellia (INTL), and Teladoc Health (TDOC), which Woods actively trades. But they are also a valuable insight into the future, EVs, CRISPR technology, robotic surgery, and molecular diagnostics. To learn more about the Ark Innovation Fund, please click here.

ProShares Ultra Technology ETF (ROM) – ($27) – This is a 2X long technology ETF that gives you an extremely aggressive position across the tech sector. It has 19% of its holdings in Apple (AAPL), 16% in Microsoft (MSFT), 10% in Alphabet (GOOGL) and Google (GOOG), at 3.5% in NVIDIA (NVDA), and 120 other smaller names. (ROM) shares are down a breathtaking 67% just in the past year. To learn more about the (ROM), please click here.

Palo Alto Networks (PANW) - $165 – Hacking is one of the fastest-growing sectors in technology, it is recession-proof and immune to the economic cycle. As a result, spending on the defense against hacking is absolutely exploding. Palo Alto Networks, Inc. is an American multinational cybersecurity company with headquarters in Santa Clara, California. Its core products are a platform that includes advanced firewalls and cloud-based offerings that extend those firewalls to cover other aspects of security. I have already earned a tenfold return over the past decade and expect to make another 10X in the coming years. You won’t find any dips in this stock as too many people are trying to get into it. To learn more about the Palo Alto Networks, please click here.

Salesforce (CRM) - $157 – The baby of tech genius Mark Benioff, this company is the dominant player in customer relationship management. If you want to do any business in the cloud, and almost all big companies do, you are up to your eyeballs in customer relationship management. Salesforce is the largest San Francisco-based cloud-oriented software company with virtually all of the Fortune 500 as its customer list. It provides customer relationship management software and applications focused on sales, customer service, marketing automation, analytics, and application development. Salesforce shares have been the target of a haymaker, down 55% in a year. To learn more about Salesforce, please click here.

You know what? I can do better than this.

I can create customized options LEAPS for you that will deliver a tenfold return on whatever performance these ultra-high beta stocks deliver. If the shares of one of my picks rise by 100%, you will make 1,000%.

This is an investment strategy that will enable you to retire early, real early. Tired of punching a time clock or logging into the next Zoom meeting on time?

Those will become a distant memory if you pursue my Mad Hedge Investment strategy for 2023.

As a result, my November month-to-date performance went off to the races, already achieving a hot +2.20%.

That leaves me with a very rare 100% cash position. With midterm election results out on Wednesday and the next report on the Consumer Price Index on Thursday, that sounds like a prudent place to be.

My 2022 year-to-date performance ballooned to +77.57%, a new high. The Dow Average is down -11.85% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +75.53%.

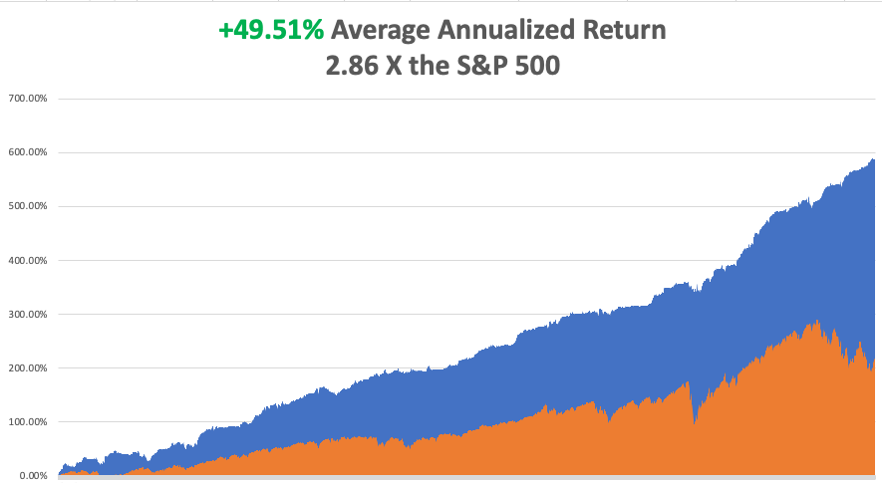

That brings my 14-year total return to +590.13%, some 2.86 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +49.51%, easily the highest in the industry.

Bonds Clock Best Day in Years, taking the ten-year US Treasury bond fund up $3.64. All low interest rate plays had monster days. Junk bond ETFs (JNK) and (HYG) were up two points. 30-year fixed rate mortgages dropped 60 basis points to 6.60%, the biggest drop in history. Long bonds will be THE big trade of 2023.

US Dollar has Worst Day in 20 Years, driven by plunging interest rates. Big tech, which gets a major share from overseas sales, rocketed. Apple alone was up $12. Cathy Wood’s Ark Innovation Fund (ARKK) was up an incredible 14%. It vindicates my view that tech will turn when interest rates and the dollar fall.

Oil Companies (USO) Book Record $200 Million Profit this year, using the Ukraine War to double your cost of gasoline. If we have a recession next year, or the war ends, energy share prices should be peaking around here. Even if they don’t, the risk-reward here is terrible. It means we will have to pay a much higher price to decarbonize the economy at a later date.

Wells Fargo Gets Hit with $1 Billion Fine for its many regulatory transgressions over the last decade. Looting of customer accounts with bogus fees has been a recurring problem. Use any selloffs to buy (WFC) on dips.

Berkshire Hathaway's 20% Profit Increase YOY and buys back another $1 billion worth of stock. However, they did take a $10 billion loss on stocks in Q3 during the market meltdown. Keep buying (BRKB) stock and LEAPS on dips.

$1.5 trillion in Homeowners Equity Lost Since May, thanks to interest rates at 20-year high and a shrinking money supply. Since July, the median home price has dropped by $11,560. The average borrower has lost $30,000 in equity. It’s not a great time to rent either as prices there are soaring. Residential housing could remain weak for another 12-24 months, compared to the six-year drawdown we had from 2006.

Boeing Orders Rise in October, but deliveries fall. The company is finally out of the penalty box, up 40% since October 1. Don’t buy (BA) up here.

The Red Wave Fails to Show, with control of congress still too close to call. Republican House control has shrunk from an expected 60 seats six months ago to maybe two today. Donald Trump threw the election for his party, picking unelectable extremist candidates and campaigning where he wasn’t wanted. A pro-life Supreme Court brought out millions of women voters across the country. If the Republicans can’t win with inflation at 8.7%, they are toast in 2024 when it drops back down to 2%.

Market Dives 646 Points on Democratic Win, with technology stocks taking the biggest hit. The red wave no-show was a black swan traders were not looking for. Energy was the worst performing sector because they aren’t getting the air cover they paid for with a red wave. The result was much as I expected, which is why I went into November 8 with a rare 100% cash position waiting to buy the next low. It turns out that rights are more important than prices.

Elon Musk Sells More Tesla Shares and Warns of a Twitter Bankruptcy, some $3.9 billion worth, bringing this year’s total to $36 billion. Musk is raising money to head off a bankruptcy of Twitter now that major advertisers are fleeing en masse. This certainly is a distress sale. If Musk was looking to build a real business, re-tweeting fringe conspiracy theories was the worst thing he could have done. Endorsing the Republican party will cost him half of his customers. Is this Musk’s Waterloo, or his Dien Bien Phu?

Facebook to Lay Off 11,000, about 13% of its total employees. Zuckerberg admits the error of pushing the company into the metaverse too far too fast. With the stock down 77%, there are not a lot of happy campers at One Hacker Way. Avoid (META) for now, but it may be a 2023 play when we get closer to a new final product.

FTX Becomes an Epic Bankruptcy, with $9.5 billion missing from its balance sheet, in one of the biggest blowups of the crypto age. Losses are expected to reach $50-$60 billion, with the bankruptcy of 130 affiliated companies. It is also a potential Dept of Justice target. All affiliated tokens and coins have gone to zero. So, placing your money with a fresh-faced kid in the Bahamas wearing baggy shorts and with no financial background was not such a great idea after all. It’s amazing how many serious people were sucked in on this one. At least Sam Bankman-Fried said he was sorry.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 14 at 8:00 AM, the Consumer Inflation Expectations for October are released.

On Tuesday, November 15 at 8:30 AM, the Producer Price Index for October is released.

On Wednesday, November 16 at 8:30 AM, Retail Sales for October are published.

On Thursday, November 17 at 8:30 AM, Weekly Jobless Claims are announced. Housing Starts and Permits for October are also out.

On Friday, November 18 at 10:00 AM, the Housing Starts for October are printed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I am often told that I am the most interesting man people ever met, sometimes daily. I had the good fortune to know someone far more interesting than myself.

When I was 14, I decided to start earning merit badges if I was ever going to become an Eagle Scout. I decided to start with an easy one, Reading Merit Badge, where you only had to read four books and write one review.

I was directed to Kent Cullers, a high school kid who had been blind since birth. During the late 1940s, the medical community thought it would be a great idea to give newborns pure oxygen. It was months before it was discovered that the procedure caused the clouding of corneas and total blindness. Kent was one of these kids.

It turned out that everyone in the troop already had Reading Merit Badge and that Kent had exhausted our supply of readers. Fresh meat was needed.

So, I rode my bicycle over to Kent’s house and started reading. It was all science fiction. America’s Space Program had ignited a science fiction boom and writers like Isaac Asimov, Jules Verne, Arthur C. Clark, and H.G. Welles were in huge demand. Star Trek came out the following year, in 1966. That was the year I became an Eagle Scout.

It only took a week for me to blow through the first four books. In the end, I read hundreds to Kent. Kent didn’t just listen to me read. He explained the implications of what I was reading (got to watch out for those non-carbon-based life forms).

Having listened to thousands of books on the subject, Kent gave me a first class education and I credit him with moving me towards a career in science. Kent is also the reason why I got an 800 SAT score in math.

When we got tired of reading, we played around with Kent’s radio. His dad was a physicist and had bought him a state-of-the-art high-powered short-wave radio. I always found Kent’s house from the 50-foot-tall radio antenna.

That led to another merit badge, one for Radio, where I had to transmit in Morse Code at five words a minute. Kent could do 50. On the badge below the Morse Code says “BSA.” In those days, when you made a new contact, you traded addresses and sent each other postcards.

Kent had postcards with colorful call signs from more than 100 countries plastered all over his wall. One of our regular correspondents was the president of the Palo Alto High School Radio Club, Steve Wozniak, who later went on to co-found Apple (AAPL) with Steve Jobs.

It was a sad day in 1999 when the US Navy retired Morse Code and replaced it with satellites. However, it is still used as beacon identifiers at US airfields.

Kent’s great ambition was to become an astronomer. I asked how he would become an astronomer when he couldn’t see anything. He responded that Galileo, the inventor of the telescope, was blind in his later years.

I replied, “good point”.

Kent went on to get a PhD in Physics from UC Berkely, no mean accomplishment. He lobbied heavily for the creation of SETI, or the Search for Extra Terrestrial Intelligence, once an arm of NASA. He became its first director in 1985 and worked there for 20 years.

In the 1987 movie Contact written by Carl Sagan and starring Jodie Foster, Kent’s character is played by Matthew McConaughey. The movie was filmed at the Very Large Array in western New Mexico. The algorithms Kent developed there are still in widespread use today.

Out here in the west aliens are a big deal, ever since that weather balloon crashed in Roswell, New Mexico in 1947. In fact, it was a spy balloon meant to overfly and photograph Russia, but it blew back on the US, thus its top secret status.

When people learn I used to work at Area 51, I am constantly asked if I have seen any spaceships. The road there, Nevada State Route 375, is called the Extra Terrestrial Highway. Who says we don’t have a sense of humor in Nevada?

After devoting his entire life to searching, Kent gave me the inside story on searching for aliens. We will never meet them but we will talk to them. That’s because the acceleration needed to get to a high enough speed to reach outer space would tear apart a human body. On the other hand, radio waves travel effortlessly at the speed of light.

Sadly, Kent passed away in 2021 at the age of 72. Kent, ever the optimist, had his body cryogenically frozen in Hawaii where he will remain until the technology evolves to wake him up. Minor planet 35056 Cullers is named in his honor.

There are no movies being made about my life…. yet. But there are a couple of scripts out there under development.

Watch this space.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/11/boy-scouts.png625418Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-14 10:02:212022-11-14 11:26:31The Market Outlook for the Week Ahead, or The Top Five Technology Stocks of 2023

The rip-roaring rally that started in October, with which we made so much money on, vaporized in a heartbeat. Traders lulled into a false sense of security with happy talk among themselves were suddenly throwing up on their shoes.

Fed governor Powell clearly indicated that interest rates will remain higher for longer, and therefore, stock prices lower. Powell promised us pain last summer and is delivering big time. Powell’s job is NOT to defend the stock market.

Personally, I’m looking for another 75 basis points on December 14, followed by 50 basis points on February 1 and another 25 basis points on March 22. This will bring us 4.75%-5.00% range for overnight Fed funds. After that, rates will fall for years as the Fed rushes to repair the damage it inflicted on the economy. Stocks will deliver the 800% return I have been promising.

I went into the Fed meeting short and used the ensuing meltdown to take profits.

As a result, my November month-to-date performance went off to the races, already achieving a hot +2.20%.

That leaves me with a very rare 100% cash position. With midterm election results out on Wednesday and the next report on the Consumer Price Index on Thursday, that sounds like a prudent place to be.

My 2022 year-to-date performance ballooned to +77.57%, a new high. The Dow Average is down -11.85% so far in 2022.

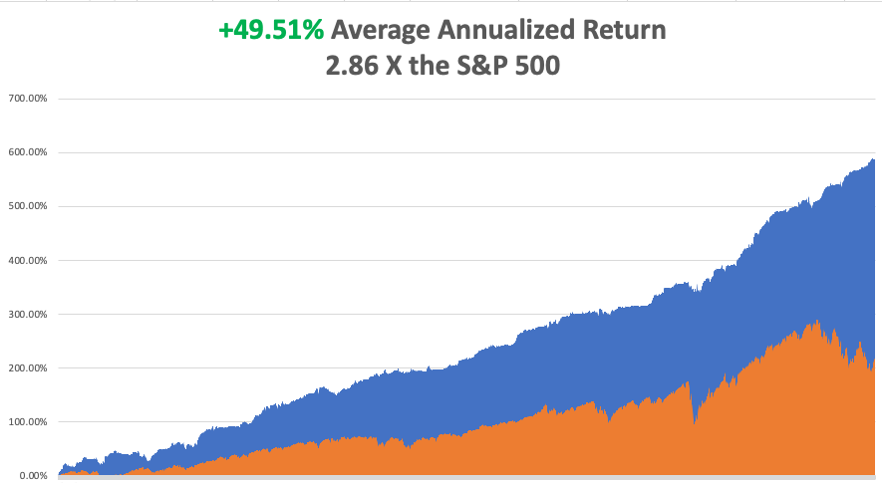

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +49.51%.

That brings my 14-year total return to +590.13%, some 2.86 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +49.51%, easily the highest in the industry.

There is no doubt that the greatest buying opportunity of the century is setting up. Those who bought the Dotcom Crash bottom in 2003 snapped up Apple (AAPL) at 20 cents on its way to $186, split adjusted. During the 2009 Financial Crisis bottom, the savvy snapped up Microsoft (MSFT) at $11. Its top tick last year was $23.

A similar golden opportunity is setting up in the next year and will create immense wealth. Just remember that things always go down more than you think, and then rise far more than you believe possible.

However, one of the greatest questions of all time has finally been resolved. Can stock markets rise without big tech? The answer has been an overwhelming “YES.” Financial, where we have been very heavily involved, rose up to 25% while tech was falling 20%. Healthcare has been on fire as well. It all gives us a place to earn our crust of bread until the long-term trend up in tech resumes, however long that may take.

The turn will be called by the prospect of Fed interest rate CUTS sometime in 2023, and good luck calling that.

Further complicating matters near term is that this could be the greatest tax loss selling year of all time, with some stocks down up to 80% sold to offset gains elsewhere, such as in energy. But the mutual funds are already done, their tax year already ended. Whatever is left must be wound up by December 31.

Nonfarm Payroll Comes in at a Hot 261,000 in October, higher than hoped. The Headline Unemployment Rate crawled up to 3.7%, the highest since February. Average hourly earnings are up 4.7% YOY, far below the inflation rate. The U-6 “Discourage worker” rate rose from 6.7% to 6.8%. Anyone who thinks these numbers will lead to an earlier end to the Fed interest rate rises has a hole in their head.

JOLTS Beats Bigtime, with 10.7 million jobs opening, a million more than expected. No cooling of labor demand here.

ADP Rises 239,000, more than expected, nailing the coffin shut on the 75-basis point rate hike. The strong industries, like Airlines and Leisure & Hospitality, are still hiring like crazy.

Is Big Tech Dead Money? It may be for months, or even years, but Big Tech always comes back. It’s just a matter of how long it takes big double-digit earnings to return with the onset of the next robust economic recovery. Until then, expect a lot of differentiation. Apple (AAPL) will hold up best, followed by Amazon (AMZN) and Google (GOOGL). As for Meta (META), the old Facebook, it may never come back.

Tech Austerity Accelerates, with Apple (AAPL) announcing an unheard-of hiring freeze. The rest of big tech is following suit. The knees are about to be cut from under the market’s safest stock.

Fed Raises Interest Rates by 75 Basis Points but changed their language to be slightly more accommodative. Stocks rallied 500 points on the news. If this is bullish, it’s a stretch. They are still targeting a 2% inflation rate and will take into account cumulative tightening to date. Acknowledging they have already raised rates a lot is something. That is more dovish than expected.

Chicago PMI is Still Falling, from 47 estimated to 45.2 in October. Under 50 indicates a recessionary economy.

Morgan Stanley Says Rising Rates to End Soon, according to strategist Mike Wilson. The big pivot will happen sooner than later. I agree.

Twitter Hate Speech Spikes 500%, since Elon Musk took over the company, as racists and conspiracy theorists test his looser limits. The entire senior staff has been fired as they are still subject to fraud accusations from Musk. Musk thinks he can resell the company for a big premium in five years. Is this the end of democracy, or just Twitter (TWTR) whose stock no longer trades? More advertisers will bail after Musk paraded conspiracy theories in the wake of the Pelosi assassination attempt.

US Treasury to Borrow $550 Billion in Q4. It means the bond short (TLT) and (TBT) may have one more gasp to go.

Japan Spends $42 Billion to Support the Yen in October to no avail, as it threatens new lows. The yen will remain weak as long as interest rates remain near zero.

First Starshipto Launch in December, the largest rock ever launched. The super heavy booster will return to earth while the capsule will land off the coast of Hawaii. Space X has a $3 billion contract from NASA to return to the moon by 2025.

US Banks Processed $1.2 Billion in Ransomware Payments this Year, triple the previous year’s level. Russia is the source of many of the attacks. And you wonder why we are supporting Ukraine?

Russian EconomyShrinks by 5% YOY in September as the sanctions take their toll. Only 45% to go. The call-up of 300,000 reservists has yet to hit the economy.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 7 at 12:00 PM, the Consumer Credit for September is released.

On Tuesday, November 8, the US Midterm elections take place with 532 House and 34 Senate seats up for grabs.

On Wednesday, November 9 the entire day will be spent analyzing election results and tracking the ties.

On Thursday, November 10 at 8:30 AM, Weekly Jobless Claims are announced. We also get the US Core Inflation Rate for October.

On Friday, November 11 at 8:30 AM the University of Michigan Consumer Sentiment for November is printed. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, I was recently in Los Angeles visiting old friends, and I am reminded of one of the weirdest chapters of my life.

There were not a lot of jobs in the summer of 1971, but Thomas Noguchi, the LA County Coroner, was hiring. The famed USC student jobs board had delivered! Better yet, the job included hours at night and free housing at the coroner's department.

I got the graveyard shift, from midnight to 8:00 AM. All I had to do was buy a black suit from Robert Halls, for $25.

Noguchi was known as the “coroner to the stars” having famously done the autopsies on Marilyn Monroe and Jane Mansfield. He did not disappoint.

For three months, whenever there was a death from unnatural causes, I was there to pick up the bodies. If there was a suicide, gangland shooting, or horrific car accident, I was your man.

Charles Manson had recently been arrested and I was tasked with digging up the victims. One, cowboy stuntman Shorty Shay, had his head cut off and neatly placed in between his ankles.

The first time I ever saw a full set of women’s underclothing, a girdle, and pantyhose, was when I excavated a desert roadside grave that the coyotes had dug up. She was pretty far gone.

Once, I and another driver were sent to pick up a teenage boy who had committed suicide in Beverly Hills. The father came out and asked us to take the mattress as well. I regretted that we were not allowed to do favors on city time. He then said, “can you take it for $200”, then an astronomical sum.

A few minutes later found a hearse driving down the Santa Monica Freeway on the way to the dump with a double mattress expertly tied on the roof with Boy Scout knots with a giant blood spot in the middle.

Once, I was sent to a cheap motel where a drug deal gone wrong had produced several shootings. I found $10,000 in a brown paper bag under the bed. The other driver found another ten grand and a bag of drugs and kept them. He went to jail. I didn’t.

The worst pick-up of the summer was also the most disgusting and even made the old veterans sick. A 300-pound man had died of a heart attack and was not discovered for a month. We decided to each grab an arm or leg and all tug on the count of three. One, two, three, and all four limbs came off!

Eventually, I figured out that handling dead bodies could be hazardous to your health, so I asked for rubber gloves. I was fired.

Still, I ended up with some of the best summer job stories ever.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/11/average-nov722.png484882Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-07 10:02:102022-11-07 11:05:56The Market Outlook for the Week Ahead, or the Fed Giveth and the Fed Taketh Away

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT IS ON FOR JUNE 14-16)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or PUTIN’S DEAD END),

(VIX), (HYG), (JNK), (PTON), (W), (MSTR), (RDFN), (BYND), (F), (TSLA), (NVDA)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-06-06 10:06:412022-06-06 11:37:16June 6, 2022

The current consensus for market strategists is that volatility will remain high.

Please pinch me because I think I died and went to heaven. For every time the Volatility Index (VIX) tops $30, I make another 10%-15% for my followers.

The bulk of market players are now obsessing whether we are entering a recession or not, as if their investment faith depended on it.

Recession, resmession.

As long as I can keep making a 65.40% trailing one-year return, while the Dow Average is off -4.2% during the same time period, I could care less what the economy is actually going to do.

After an impressive 380-point, 10% rally in the S&P 500, it now looks like the stock market is failing once again. Best case, we revisit this year’s low at 3,800. Worst case, we break to new lows at 3,600. The very worst case, we break below 3,500 and wish you had never heard of the stock market.

If you are a trader, there is a fantastic opportunity here to buy low, sell high, and retire early. If you are disciplined, you still have a ton of cash left over from the end of 2021 (I was 100% cash) and will be cherry-picking on the big down days.

It's really very simple. The longer you have been doing this, the easier it gets and the more money you will make. After 52 years of practice, I can do this in my sleep.

As the bear market worsens, we are seeing old asset classes return from the dead like the revived dinosaurs of Jurassic Park. Call convertible bonds are the velociraptors of the bunch.

Take the main junk bond ETF like the iShares iBoxx High Yield Corporate Bond Fund (HYG) and the SPDR Barclays High Yield Bond Fund (JNK), which have seen yields double from 3% to over 6% in only six months.

If you are willing to take on more risk, individual busted convertible bonds yield infinitely more. You know all the names. Peloton (PTON) converts are paying a 10.4% yield to maturity, Wayfair (W) 11.0%, MicroStrategy (MSTR) 13.1%, Redfin (RDFN) 14.5%, and Beyond Meat (BYND) 19.5%. Buy ten of these and even if one goes under, you still earn a decent double-digit return.

Having run a convertible bond trading desk for ten years, I can tell you that the risk/reward balance for many individuals with this investment class is just right.

As my summer military duty approaches, information about the Ukraine War is pouring into me. I will share with you what I can, what has been declassified for the war is still a major factor in your investment outcomes. I have been able to use my “top secret” status for 50 years,= to your benefit.

The amazing thing is that in this modern age, information goes from “top secret” to declassified in only a day. It is a new strategy used by the current administration that is working incredibly well. Information is more valuable shared than locked up.

I have been getting a lot of questions from readers as to why Vladimir Putin committed such a disastrous error by invading Ukraine as he is considered a smart guy. My initial response was that he surrounded himself with “yes” men who only told him what he wanted to hear, leading to terrible outcomes, which I have seen happen many times.

The costs of the war for Putin have so far been enormous; 50,000 casualties, 1,000 tanks, 1,300 armored vehicles, banishment from the western economy, the loss of $1 trillion in foreign held assets, and the decline of the national GDP from $1.5 trillion to $1 trillion.

The costs are about to substantially rise. The US is now sending over its most advanced artillery systems, the MRLS, or Multiple Rocket Launch System, which can hit any target within 300 miles with an accuracy of one meter. All you have to do is dial in the latitude and longitude of the target and it never misses. This one weapon will certainly bring the war to a stalemate and consign it to page three of the newspapers.

But after doing a ton more research, my view has evolved. Putin has in fact launched a Resource War against the entire rest of the world. The result has been to boost the price of practically everything Russia produces, including oil ($123 billion), refined petroleum products ($63 billion), iron & steel ($28 billion), coal ($17 billion), fertilizer ($13 billion), wood ($12 billion), wheat ($9 billion), aluminium ($8 billion), platinum, palladium, uranium.

There is also the inflation angle. While the US benefits from many of these high prices as well, they have raised the US inflation rate from 5% to 8.3%. That damages the election prospects of Biden and the Democrats. High inflation improves the election of prospects of a former president who Putin seems to vastly prefer for whatever reason.

After covering Russia for 50 years, flying their front-line fighters, springing a wife out of jail in Moscow, I can tell you that everything there is a chess game, and they play a very long game.

Nonfarm Payroll Report comes in at 390,000, better than expected. Leisure & Hospitality led the gains with 84,000, and Professional & Business Services by 75,000. Manufacturing fell to only 18,000, largely because of a shortage of workers. The Headline Unemployment Rate remained the same at 3.6%. Average hourly earnings rose by an inflationary 5.2% YOY. The U6 “discouraged worker” rate rose back to 7.1%.

Weekly Jobless Claims jump 19,000 to 200,000, a two-month high, according to the Department of Labor. Compensation for American workers has hit a 30-year high. New York showed the largest increase followed by Illinois.

OPEC+ raises oil output to meet surging energy demand caused by the Ukraine War. Up 648,000 barrels a month for July and August. They could easily do a lot more. The cartel is aiming for the pre-pandemic 10 million barrels a day. No dent in prices at the pump yet.

Hedge Funds were slaughtered in May, with the flagship Tiger Global Fund down a massive 14%. Gee, Mad Hedge Fund Trader was UP 11% in May and am up 44% on the year. Maybe there’s something in the water here at Lake Tahoe. Or, maybe it’s the “Mad” that is giving me my edge?

S&P Case Shiller National Home Price Index tops 20.6%, a new all-time high. Tampa (34.8%), Miami (32.4%), and Phoenix (32.0%) lead the gains. Incredible as it may seem, price rises are accelerating. But expect that to cool off once current prices start feeding into the index.

Home Listings soar, with homes for sale up 9% YOY as homeowners fear missing getting out at the top. New listings have doubled in a year, according to Redfin. Outrageous over-market bids have definitely ended in California. So far, no hint of price drops….yet.

A Ford (F) Electric Pickup can power your house for ten days, but only if you live in a tiny house. Ford is the first company to introduce bidirectional charging that lets your home run off the vehicle’s 1,300-pound lithium-ion battery. All you need is a $3,895 hardware upgrade from Sunrun. The range is 320 miles, not as much as the latest Tesla Model X (TSLA). Good luck getting one. Ford isn’t taking any new orders until it fills the 200,000 it already has. Expect Tesla to copy the move.

The Fed may overshoot on raising interest rates if Fed governor Christopher Waller has his way. That’s because going too tight may be necessary to break the back of inflation. That’s what happened in 1980, when Fed Funds hit 17%, and ten-year bond yields hit 15.84%. My first home mortgage interest rate for a coop in Manhattan back then was 17%.

China Covid Cases fade, prompting a big Bitcoin rally. This could be the impetus for a sudden global economic recovery that will deliver a big US stock market rally. Good thing I loaded the boat with tech stocks two weeks ago.

The Fed Minutes were not so horrible, downplaying the risk of a full 1% rate rise, triggering a 1,000-point rally in the Dow. With five up days in a row this is starting to look like THE bottom. Is this the light at the end of the tunnel?

NVIDIA (NVDA) rips, surprising to the upside on almost every front, sending the stock up $30, or 18.75%. Mad Hedge followers bought (NVDA) last week. This is one of the best run companies in the world. I expect the shares to rise from the current $178.51 to $1,000 in five years. Buy (NVDA) on dips.

Q1 GDP dives 1.5%, in its final read. It’s the worst quarter since the pandemic began during Q2 2022. Weekly Jobless Claims dropped 8,000 to 210,000. My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyperaccelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With some of the greatest market volatility seen since 1987, my June month-to-date performance recovered to +2.49%.

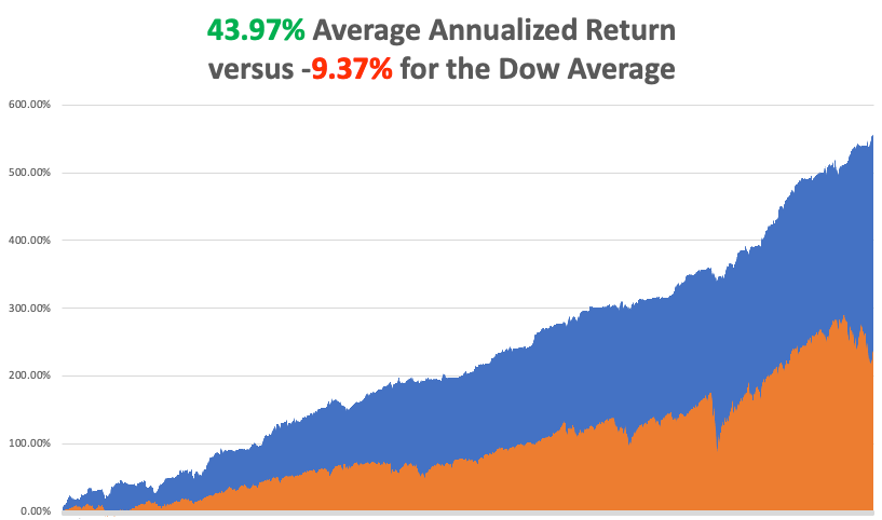

My 2022 year-to-date performance exploded to 44.36%, a new all-time high. The Dow Average is down -9.37% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky high 65.40%.

That brings my 14-year total return to 556.92%, some 2.37 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 43.97%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 84.7 million, up 300,000 in a week and deaths topping 1,000,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, June 6 is the 78th anniversary of the D-Day invasion of Normandy. All of the veterans I knew have long since passed. I’ll miss the memorial this year. On Tuesday, June 7 at 8:30 AM, the US Balance of Trade for April is released.

On Wednesday, June 8 at 10:30 AM, US Crude Inventories are published.

On Thursday, June 9 at 8:30 AM, Weekly Jobless Claims are out.

On Friday, June 10 at 8:30 AM, the blockbuster US Core Inflation Rate is announced. More importantly, the new dinosaur movie, Jurassic World: Dominion, is released. At 2:00 the Baker Hughes Oil Rig Count are out.

As for me, this is not my first Russian invasion.

Early in the morning of August 20, 1968, I was dead asleep at my budget hotel off of Prague’s Wenceslas Square when I was suddenly awoken by a burst of machine gun fire. I looked out the window and found the square filled with T-54 Russian tanks, trucks, and troops.

The Soviet Union was not happy with the liberal, pro-western leaning of the Alexander Dubcek government so they invaded Czechoslovakia with 500,000 troops and overthrew the government.

I ran downstairs and joined a protest demonstration that was rapidly forming in front of Radio Prague trying to prevent the Russians from seizing the national broadcast radio station. At one point, I was interviewed by a reporter from the BBC carrying this hulking great tape recorder over his shoulder, as I was the only one who spoke English.

It seemed wise to hightail it out of the country, post haste, as it was just a matter of time before I would be arrested. The US ambassador to Czechoslovakia, Shirley Temple Black (yes, THE Shirley Temple), organized a train to get all of the Americans out of the country.

I heard about it too late and missed the train.

All borders with the west were closed and domestic trains shut down, so the only way to get out of the country was to hitch hike to Hungary where the border was still open.

This proved amazingly easy as I placed a small American flag on my backpack. I was in Bratislava just across the Danube from Austria in no time. I figured worst case, I could always swim it, as I had earned both, the Boy Scout Swimming, and Lifesaving merit badges.

Then I was picked up by a guy driving a 1949 Plymouth who loved Americans because he had a brother living in New York City. He insisted on taking me out to dinner. As we dined, he introduced me to an old Czech custom, drinking an entire bottle of vodka before an important event, like crossing an international border.

Being 16 years old, I was not used to this amount of high-octane 40 proof rocket fuel and I was shortly drunk out of my mind. After that, my memory is somewhat hazy.

My driver, also wildly drunk, raced up to the border and screeched to a halt. I staggered through Czech passport control which duly stamped my passport. I then lurched another 50 yards to Hungary, which amazingly let me in. Apparently, there is no restriction on entering the country drunk out of your mind. Such is Eastern Europe.

I walked another 100 yards into Hungary and started to feel woozy. So, I stumbled into a wheat field and passed out.

Sometime in the middle of the night, I felt someone kicking me. Two Hungarian border guards had discovered me. They demanded my documents. I said I had no idea what they were talking about. Finally, after their third demand, they loaded their machine guns, pointed them at my forehead, and demanded my documents for the third time.

I said, “Oh, you want my documents!”

I produced my passport, When they got to the page that showed my age they both started laughing.

They picked me and my backpack up and dragged me back to the road. While crossing some railroad tracks, they dropped me, and my knee hit a rail. But since I was numb, I didn’t feel a thing.

When we got to the road, I saw an endless stream of Russian army trucks pouring into Czechoslovakia. They flagged down one of them. I was grabbed by two Russian soldiers and hauled into the truck with my pack thrown on top of me. The truck made a U-turn and drove back into Hungary.

I contemplated my surroundings. There were 16 Russian Army soldiers in full battle dress holding AK-47s between their legs and two German Shepherds all looking at me quizzically. Then I suddenly felt the urge to throw up. As I assessed that this was a life and death situation, I made every effort to restrain myself.

We drove five miles into the country and then stopped at a small church. They carried me out of the truck and dumped me and my pack behind the building. Then they drove off.

The next morning, I woke up with the worst headache of my life. My knee bled throughout the night and hurt like hell. I still have the scar. Even so, in my enfeebled condition, I realized that I had just had one close call.

I hitch-hiked on to Budapest, then to Romania, where I heard that the beaches were filled with beautiful women. My Italian let me get by passably in the local language.

It all turned out to be true.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

One More Off to College

If You Don’t Like the Price, Don’t Use it

https://www.madhedgefundtrader.com/wp-content/uploads/2022/06/John-thomas-daughter-grad.png354472Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-06-06 10:02:082022-06-07 14:40:00The Market Outlook for the Week Ahead, or Putin’s Dead End

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-05 18:26:392022-01-05 18:26:39January 5, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.