(TUESDAY, AUGUST 1, 2023 FLORENCE, ITALY GLOBAL STRATEGY LUNCHEON)

(CYBERSECURITY IS ONLY JUST GETTING STARTED)

(PANW), (HACK), (CSCO), (FTNT), (JNPR), (CIBR)

One of the unfortunate aspects of the pandemic has been a tenfold increase in online fraud.

I get a dozen phishing attacks a day pretending to be Walmart, the Bank of America, and Amazon. And I never click on anything from Apple asking me to change my ID and password. The crooks are just getting too good.

However, where there are criminals there is investment gold.

The cybersecurity sector has been spurred upward with the rest of technology in recent months, creating a rare entry point on the cheap side of the longer-term charts.

The near-destruction of Sony (SNE) by North Korean hackers years ago has certainly put the fear of God into corporate America. Apparently, they have no sense of humor whatsoever north of the 38th parallel.

As a result, there is a generational upgrade in cybersecurity underway, with many potential targets boosting spending by multiples.

It’s not often that I get a stock recommendation from an army general. That is exactly what happened the other day when I was speaking to a three-star about the long-term implications of the escalating trade war.

He argued persuasively that the world will probably never again see large-scale armies fielded by major industrial nations. Wars of the future will be fought online, as they have been silently and invisibly over the past 20 years.

All of those trillions of dollars spent on big ticket, heavy metal weapons systems, like submarines and F-35 fighters ($122 million each) are pure pork designed by politicians to buy voters in marginal swing states.

The money would be far better spent where it is most needed, on the cyber warfare front. Needless to say, my friend shall remain anonymous.

The problem is that when wars become cheaper, you fight more of them, as is the case with online combat.

You probably don’t know this, but during the Bush administration, the Chinese military downloaded the entire contents of the Pentagon’s mainframe computers at least seven times.

This was a neat trick because these computers were in stand-alone, siloed, electromagnetically shielded facilities not connected to the Internet in any way. Here are essentially no secrets about anything anymore.

In the process, they obtained the designs of all of our most advanced weapons systems, including our best smart nukes. What have they done with this top-secret information?

Absolutely nothing.

Like many in senior levels of the US military, the Chinese have concluded that these weapons are a useless waste of valuable resources. Far better value for money are more hackers, coders, and servers, which the Chinese have pursued with a vengeance.

You have seen this in the substantial tightening up of the Chinese Internet through the deployment of the Great Firewall, which blocks local access to most foreign websites, including Wikipedia.

Try sending an email to someone in the middle Kingdom with a Gmail address. It is almost impossible. This is why Google (GOOG) closed their offices there years ago.

I know of these because several Chinese readers are complaining that they are unable to open my own Mad Hedge Trade Alerts, or access their foreign online brokerage accounts.

As a member of the Joint Chiefs of Staff recently told me, “The greatest threat to national defense is wasting money on national defense.”

Although my brass-hatted friend didn’t mention the company by name, the implication is that I need to go out and buy Palo Alto Networks (PANW) right now.

Palo Alto Networks, Inc. is an American network security company based in Santa Clara, California just across the water from my Bay area office.

The company’s core products are advanced firewalls designed to provide network security, visibility and granular control of network activity based on application, user, and content identification. To visit their website please click here.

Palo Alto Networks competes in the unified threat management and network security industry against Cisco (CSCO), FireEye (FEYE), Fortinet (FTNT), Check Point (CHKP), Juniper Networks (JNPR), and Cyberoam, among others.

The really interesting thing about this industry is that there really are no losers. That’s because companies are taking a layered approach to cybersecurity, parceling out contracts to many of the leading firms at once, looking to hedge their bets.

To say that top management has no idea what these products really do would be a huge understatement. Therefore, they buy all of them.

This makes a basket approach to the industry more feasible than usual. You can do this by buying the $435 million capitalized Pure Funds ISE Cyber Security ETF (HACK), which boasts CyberArk Software (CYBR and FireEye (FEYE) as its largest positions.

(HACK) has been a hedge fund favorite since the Sony attack.

For more information about (HACK), please click here.

And don’t forget to change your password.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Hacker-image-story-3-image-5.jpg177285MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2023-06-28 09:02:232023-06-28 13:20:41Cybersecurity is Only Just Getting Started

(TUESDAY, JUNE 25 SYDNEY, AUSTRALIA STRATEGY LUNCHEON)

(CYBERSECURITY IS ONLY JUST GETTING STARTED),

(PANW), (HACK), (FEYE), (CSCO), (FTNT), (JNPR), (CIBR)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-06-13 04:06:142019-06-13 04:38:16June 13, 2019

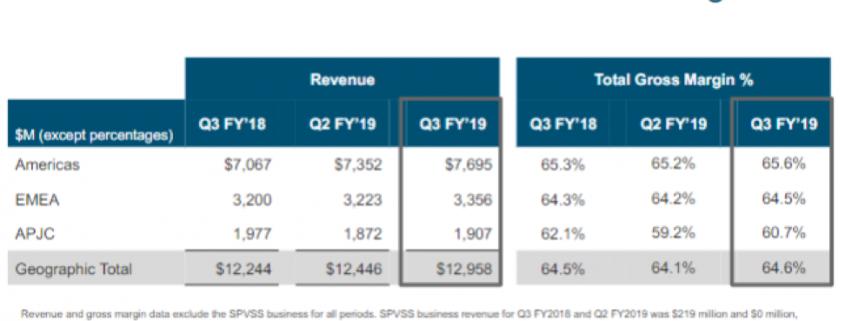

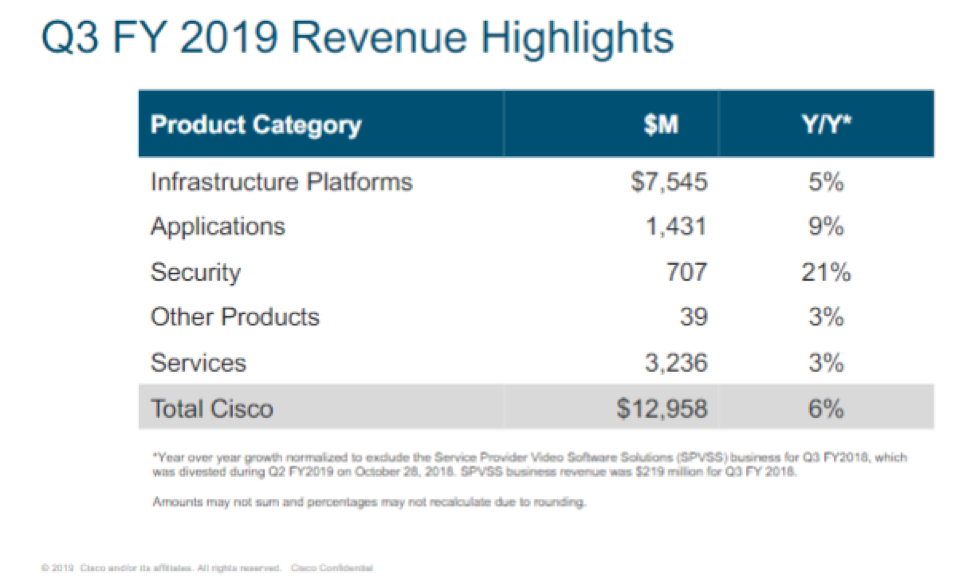

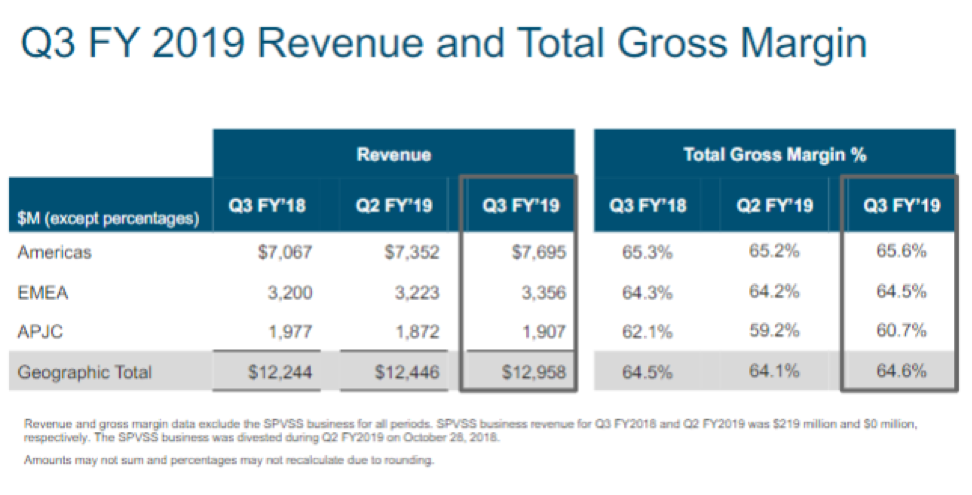

You can’t steal the mojo from the company that sells network software and infrastructure equipment.

Cisco (CSCO) is effectively an indirect bet on people using the internet because companies need the network infrastructure to offer all the cool and useful services that tech provides.

Technology and the services that result from it continues to be at the heart of customer strategy and now more than ever, Cisco’s market-leading portfolio and differentiated innovation are resonating with them as they transform their IT infrastructure.

Cisco is also a fabulous bet on 5G as the most recent technologies like cloud, AI, IoT, and WiFi 6 among others are developing together to revolutionize the way business operates and delivers new experiences for customers and teams.

Cisco is fundamentally changing the way customers approach their technology infrastructure to address the rising complexity in their IT environments.

They have constructed the only integrated multi-domain intent-based architecture with security at the foundation.

This is designed to allow customers to securely connect their users and devices over any network to any application.

Enterprise networks today must be optimized for agility and heightened security, leveraging cloud and wireless capabilities with the ability to extract insights from the data and security integrated throughout.

Cisco is in pole position to deliver this to customers.

Last quarter saw the launch of new platforms expanding the enterprise networking assets with the launch of subscription-based WiFi 6 access points and Catalyst 9600 campus core switches purpose-built for cloud-scale networking.

By combining automation and analytics software with a broad portfolio of switches, access points, and controllers, Cisco is creating a seamless end-to-end wireless first architecture.

With the newest Catalyst 9000 additions, Cisco has completed the most comprehensive enterprise networking portfolio upgrade in their history.

Cisco rebuilt their entire access portfolio with intent-based networking across wired and wireless.

Cisco also now have one unified operating system and policy management platform to drive simplicity and consistency across networks all enabled by a software subscription model.

In the data center, their strategy is to deliver multi-cloud architectures that bring policy and operational consistency no matter where applications or data resides by extending Application Centric Infrastructure (ACI) and offering HyperFlex to the cloud.

According to Cisco’s official website, its HyperFlex product is “a converged infrastructure system that integrates computing, networking and storage resources to increase efficiency and enable centralized management.”

Cisco’s partnerships with Amazon Web Services (AWS), Google Cloud, and Microsoft Azure are great examples of how they continue to work with web-scale providers to deliver new innovation.

Some new additions are Cisco’s cloud ACI for AWS, a service that allows customers to manage and secure applications running in a private data center or in Amazon Web Services cloud environments.

They also expanded agreements with Alphabet (GOOGL) by announcing support for their multi-cloud platform Anthos to help customers build secure applications everywhere from private data centers to public clouds with greater simplicity.

Going forward, Cisco will integrate this platform with its broad data center portfolio, including HyperFlex, ACI, SD-WAN, and Stealthwatch cloud to deliver the best multi-cloud experience.

Organic growth has surpassed 4% for five straight quarters and expanded margins and positive guidance for the current quarter will reaccelerate PE multiples, increasing as more investors buy into the strong narrative.

CEO of Cisco CEO Chuck Robbins boasted on the call that “we see very minimal impact at this point based on all the great work the teams have done, and it is absolutely baked into our guide going forward” when referring to the headwinds of the global trade war.

It’s been quite the new normal for chip firms to guide down for the rest of 2019, and Intel’s (INTC) worries are emblematic of the growing challenges facing the tech industry.

Cisco bucked the trend by issuing strong forward guidance of 4.5% to 6.5% revenue growth in its fiscal fourth quarter, and earnings of 80 cents to 82 cents per share.

In an in-house survey, Cisco found that 11% of respondents have upgraded networking infrastructure and 16% expect to do so in the next 12 months.

The “minimal impact” of the trade war indicates to investors that even with negative tech sentiment brooding around the world, Cisco’s best in class tech infrastructure still cannot be sacrificed and the migration of companies to digital directly benefits Cisco who provides the building blocks for software and hardware tech companies to develop around.

Cisco even felt bold enough to hike prices giving consternation to current customers.

Both Juniper (JNPR) and Arista (ANET), lower quality network infrastructure companies, have indicated their enterprise businesses are growing faster than the overall market and Cisco’s price hike was probably a bad time to up margins in the current frosty climate.

Even more worrying is data that suggests a general Enterprise pause in spending at a minimum and could entrap the broader tech market as many capital expenditures could be put on hold in the late economic cycle.

Keep in mind that Cisco’s Catalyst 9000 line had an abnormally strong last fourth quarter due to brisk adoption accelerating meaning comps will be hard to beat in the next earnings report.

However, these are minor bumps on the road at a time when the major narrative is running smoothly and shows no signs of stopping.

Cisco shares will continue to rise if they continue to upgrade their products and back it up with their best of breed reputation that could spur more price hikes.

Investors should wait for dips to buy in this name until there are any signs of product quality erosion which I believe will not happen in 2019.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/05/cisco-margin.png495972Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-20 01:02:162019-07-11 13:04:10The Big Play in Cisco

I bet you are wondering where all that money from the tax cuts is going.

Believe it or not, the No. 1 destination of this new windfall is technology companies, not just the stocks, but entire companies.

In fact, the takeover boom in Silicon Valley has already started, and it is rapidly accelerating.

The only logical conclusion in 2018 is that tech firms are about to get a lot more expensive. I'll explain exactly why.

The corporate cash glut is pushing up prices for unrealized M&A activity in 2018. U.S. firms accumulated an overseas treasure trove of around $2.6 trillion and the capital is spilling back into the States with a herd-type mentality.

I have chewed the fat with many CEOs about their cash pile road map. All mirrored each other to a T: strategic acquisition and share buybacks, period. The acquisition effect will be felt through all channels of the tech arterial system in 2018.

As the global race to acquire the best next generation technology heats up, domestic mergers could pierce the 400-deal threshold after a lukewarm 2017.

Spend or die.

Apple alone boomeranged back more than $250 billion with hopes of selective mergers and share buybacks. Cisco (CSCO), Microsoft (MSFT), and Google (GOOGL) were also in the running for most cash repatriated.

The tech behemoths are eager to make transformative injections into security, big data, semiconductor chips, and SaaS (service as a software) among others.

Hint: You want to own stocks in all of these areas.

Even non-traditional tech companies are getting in on the act with Walmart concentrating the heart of its strategic future on the pivot to technology.

Walk into your nearest Walmart every few months.

You'll notice major changes and not for decorative measures.

U-turns from legacy technology firms hawking desktop computers and HDD's (Hard Disk Drive) suddenly realize they are behind the eight ball.

M&A activity will naturally tilt toward firms dabbling in earlier-stage software and 5G supported technology. This flourishing trend will reshape autonomous vehicles and IoT (Internet of Things) products.

The dilemma in waiting to splash on a potential new expansion initiative is that the premium grows with the passage of time. Time is money.

It's a sellers' market and the sellers know this wholeheartedly.

Unleashing the M&A beast comes amid a seismic shift of rapid consolidation in the semiconductor sector. Cut costs to compete now or get crushed under the weight of other rivals that do. Ruthless rules of the game cause ruthless executive decisions.

The best way to cut costs is with immense scale to offer nice shortcuts in the cost structure. Buying another company and using each other's dynamism to find a cheaper way to operate is what Microchip Technology's (MCHP) culling of Microsemi Corporation (MSCC) in a deal worth $10bn was about.

Microsemi, based in Aliso Viejo, California, focuses on manufacturing chips for aerospace, military, and communications equipment.

Microchip's focal point is industrial, automobile and IoT products.

Included in the party bag is a built-in $1.8 billion annual revenue stream and more than $300 million of dynamic synergies set to take effect within three years. The bonus from this package is the ability to cross-sell chips into unique end markets opposed to selling from scratch.

Each business hyper-targets different segments of the chip industry and is highly complementary.

Benefits of a relatively robust credit market create an environment ripe for mergers. Some 57% of tech management questioned intend to go on the prowl for marquee pieces to add to their arsenal.

Then we have chip company Broadcom (AVGO) led by CEO Hock Tan, whose entire strategy is based on M&A and minimal capital spending.

His low-quality strategy of buying market share will ultimately fritter out. His lack of capital spending was also a salient reason for blocking Broadcom's purchase of Qualcomm (QCOM), which if stripped of its capital spending budget would have fallen behind China's Huawei to develop critical 5G infrastructure.

Tan's strategy flies in the face of the most powerful tech companies that are using M&A to enhance their products expanding their halo effect around the world.

Gutting innovation and skimming profits off the top is an entirely self-serving, myopic strategy to the detriment of long-term shareholders.

Investors punished Broadcom for it's latest investment of CA Technologies (CA) for $18.9 billion, even though this pickup signals a different tack.

CA Technologies is a leading provider of information technology (IT) management software, which suggests a belated move into the enterprise software market dominated by incumbents such as Salesforce (CRM).

Better late than never.

No need to mince words here as 2018 won't see any discounts of any sort. Nimble buyers should prepare for price wars as the new normal.

Not only are the plain vanilla big cap tech firms dicing up ways to enter new markets, alternative funds are looking to splash the cash, too.

Sovereign wealth funds and private equity firms are ambitiously circling around like vultures above waiting for the prey to show itself.

Private equity firms dove head first into the M&A circus already tripling output for tech firms.

Highlighting the synchronized show of force is none other than Travis Kalanick, the infamous founder of Uber. He christened his own venture capital fund that hopes to invest in e-commerce, real estate, and companies located in China and India.

The new fund is called 10100 and is backed by his own money. All this is possible because of SoftBank CEO Masayoshi Son's investment in Uber, which netted Kalanick a cool $1.4 billion representing Kalanick's 30% stake in Uber.

It is undeniable that valuations are exorbitant, but all data and chip related companies are selling for huge premiums. The premium will only increase as the applications of 5G, A.I., autonomous cars start to pervade deeper into the mainstream economy.

Adding fuel to the fire is the corporate tax cut. The lower tax rate will rotate more cash into M&A instead of Washington's tax coffers enhancing the ability for companies to stump up for a higher bill. Sellers know firms are bloated with cash and position themselves accordingly.

Highlighting the challenges buyers face in a sellers' market is Microsemi Corp.'s (MSCC) purchase of PMC-Sierra Inc. Even though PMC-Sierra had been looking to get in bed with Skyworks Solutions Inc. (SWKS) just before the MSCC merger, PMC-Sierra reneged on the acquisition after (SWKS) refused to bump up its original offer.

(SWKS) manufactures radio frequency semiconductors facilitating communication among smartphones, tablets and wireless networks found in iPhones and iPads.

(SWKS) is a prime takeover target for Apple. (SWKS) estimates to have the highest EPS growth over the next three to five years for companies not already participating in M&A. Apple (AAPL) could briskly mold this piece into its supply chain. Directly manufacturing chips would be a huge boon for Apple in a chip market in short supply.

In 2013, Japan's Tokyo Electron and Applied Materials (AMAT) angled to become one company called Eteris. This maneuver would have created the world's largest supplier of semiconductor processing equipment.

After two years of regulatory review, the merger was in violation of anti-trust concerns according to the United States. (AMAT), headquartered in Santa Clara, California, is a premium target as equipment is critical to manufacturing semiconductor chips. (AMAT) competes directly with Lam Research (LRCX), which is an absolute gem of a company.

Juniper Networks (JNPR) sells the third-most routers and switches used by ISP's (Internet Service Providers). It is also No. 2 in core routers with a 25% market share. Additionally, (JNPR) has a 24.8% market share of the firewall market.

In 2014, Palo Alto Networks (PANW), another takeover target focusing on cybersecurity, paid a $175 million settlement fee for allegedly infringing (JNPR)'s application firewall patents.

In data center security applications, (JNPR) routinely plays second fiddle to Cisco Systems (CSCO). Cisco, the best of breed in this space would benefit by snapping up (JNPR) and integrating its expertise into an expanding network.

Unsurprisingly, health care is the other sector experiencing a tidal wave of M&A, and it's not shocking that health care firms accumulated cash hoards abroad too. The dots are all starting to connect.

Firms want to partner with innovative companies. Companies hope to focus on customer demands and build a great user experience that will lead the economy. Health care costs are outrageous in America, and Jeff Bezos could flip this industry on its head.

Amazon (AMZN) pursuing lower health costs ultimately will bind these two industries together at the hip and is net positive for the American consumer.

Ride-sharing company Uber embarked on a new digital application called Uber Health that book patients who are medically unfit for regular Uber and shuttle them around to hospital facilities.

Health care providers can hail a ride for sick people immediately and are able to make an appointment 30 days in advance. It is a little difficult to move around in a wheel chair, and tech solves problems that stir up zero appetite for most business ventures. Apple is another large cap tech titan keeping close tabs on the health care space.

It's a two-way street with health care companies looking to snap up exceptional tech and vice versa.

It's practically a game of musical chairs.

Ultimately, Tech M&A is the catch of the day, and boosting earnings requires cutting-edge technology no matter how expensive it is. Investors will be kicking themselves for waiting too long. Buy now while you can.

Featured Trade:

(FRIDAY, JUNE 15, 2018, DENVER, CO, GLOBAL STRATEGY LUNCHEON)

(ANATOMY OF A GREAT TRADE)

(TLT), (TBT), (SPY), (GLD), (USO),

(CYBERSECURITY IS ONLY JUST GETTING STARTED),

(PANW), (HACK), (FEYE), (CSCO), (FTNT), (JNPR), (CIBR)

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.