Global Market Comments

December 13, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BULL AGES),

(BAC), (GS), (JPM), (TLE)

Global Market Comments

December 13, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BULL AGES),

(BAC), (GS), (JPM), (TLE)

I asked a hedge fund friend of mine the other day about his favorite positions for 2022. His answer surprised me: cash.

Maybe it’s just me in my old age, but it seems we are having to work harder and harder to get fewer and fewer returns from the stock market.

Maybe it’s the increasing age of the bull, now 14 months since the last 10% correction. It is not a child anymore, or even a teenager, but more likely thirty something.

Is there a middle age crisis around the corner? While its performance will still be OK, its best years are clearly behind us. In other words, it’s a lot like you and me.

Perhaps it is the recent onslaught of black swans hitting the financial system: oil shocks, threatened Russian invasions, shocking 6.8% inflation, and Fed flip-flopping that are causing the recent reticence.

But here we are with a Dow Average at $35,970, exactly where we were two months ago. There has been a lot of Sturm und Drang, but no net movement.

Maybe this is all to test the faithful and to flush out all the hot money, which we clearly did the previous week. 2022 will be one of the highest growth years in American history, in excess of a 5% real rate.

In a year, the pandemic will be gone, supply chain problems fixed, international trade resumed, corporate profits and the stock market will be at all-time highs, and most workers will have just obtained the biggest pay increases in their lives. The only unknown is how much of this performance has already been pulled forward into 2021.

Still, we have little choice but to press ahead with our longs. With overnight rates still near zero, there are few other high-gaining investments, such as residential real estate. The funny thing is that real estate people are buying stocks because homes have gotten so expensive, while stock market people are buying second and third homes because shares have become so dear.

I call it the “grass is always greener on the other side of the fence” syndrome. It is always a sign of impending trouble.

Cogitating over this, I think I’ll go for my second helping of eggnog and my third mug of hot buttered rum.

CPI Sizzles at 6.8% YOY, the highest since 1982, after a 0.8% pop in November. Virtually everything saw big increases, with used trucks up 30%. The Fed now has more incentive to accelerate the taper and bring forward interest rate hikes. The shock was already priced into the bond market which barely moved.

ADP Soars to 11 Million Job Openings, up 431,000 in October, the most on record. Companies are screaming for new staff. If you are a computer programmer or truck driver, the world is your oyster. Resignations are declining. There are a staggering 254,000 openings in Accommodations and Food Industries, and another 45,000 in nondurable goods manufacturing. State & Local Government shrunk job openings by 115,000. It’s a sign of extreme vigor in the economy.

Weekly Jobless Claims Dive to 184,000, down an amazing 43,000 on the week, a new post-pandemic low and a 52-year low. Things are definitely getting better.

Omicron Fades as a market concern, as a 1,200-point move up in the Dow in two days proves. This was probably the last dip of 2021. Now that the bottom is in, look for volatility to fade from here into yearend. I kept all my positions in the last meltdown, both in financial and tech longs and bond shorts.

Pfizer Says Boosters Work Against Omicron, as I suspected, which is why you saw the biggest two-day rally in stocks this year. The booster increases your immunity 1,000 times. I’d buy (PFE) but it is already up 25% in a month.

Ford Stops Taking Orders for the F-150EV, as demand has been so overwhelming. Now all they have to do is make one. It’s the hottest selling Ford product since the Mustang hit the road in 1964, when the Beatles launched their first US tour. A lot of talk but little output. It’s all PR. Tesla has a 12-year head start, but (F) will probably keep going up as it transforms from a hardware manufacturer to a software company.

Why Elon Musk Hates Hydrogen, which he calls “fool cells”. I tell people to just google the term “Hindenburg”. Electricity is infinitely scalable while hydrogen isn’t, and certainly won’t be able to compete economically after the next tenfold improvement in battery densities.

US Home Prices to Keep Rising, but at only half the 2021 rate. I’ll take another 10% gain in my home value. The generational shortage of housing should keep house prices rising for another decade. Buy (TOL), PHM), and (KBH) on dips, which has resorted to lotteries to halt bidding wars.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With the pandemic-driven meltdown on Friday, my November month-to-date performance bounced back hard to 9.47%. My 2021 year-to-date performance recovered to 86.23%. The Dow Average is up 17.55% so far in 2021.

I used a collapse in bond prices to take profits on my 20% position in bonds. I kept my long in (JPM),(GS), and (BAC). I am 70% in cash. I will be using any further volatility spikes to add positions in the coming week.

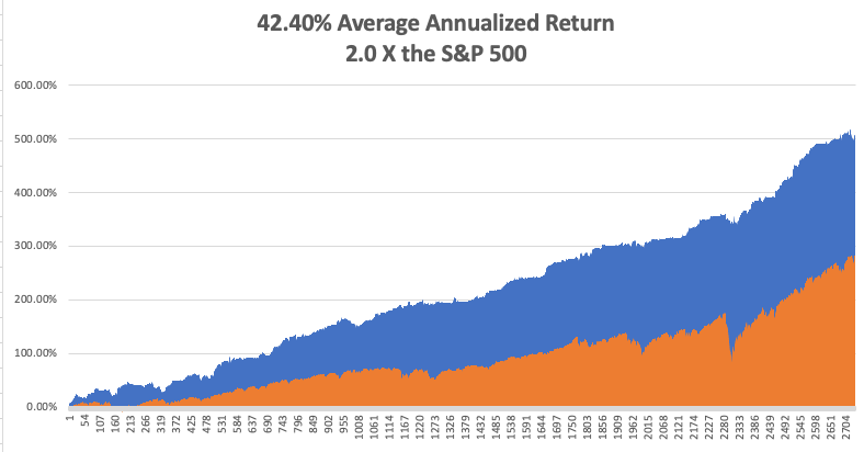

That brings my 12-year total return to 508.78%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 42.40%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 50 million and rising quickly and deaths close to 800,000, which you can find here.

On Monday, December 13 at 8:00 AM, Consumer Inflation Expectations are out.

On Tuesday, December 14 at 8:30 AM, the Producer Price Index for November is published.

On Wednesday, December 15 at 8:30 AM, the Retail Sales for November are printed. At 11:00 AM, the Federal Reserve announces its interest rate decision.

On Thursday, December 16 at 8:30 AM, the Weekly Jobless Claims are disclosed.

On Friday, December 17 at 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, one of the benefits of being married to a British Airways stewardess in the 1970s was unlimited free travel around the world. Ceylon, the Seychelles, and Kenya were no problem.

Usually, you rode in first class, which was half empty, as the British Empire was then rapidly fading. Or you could fly in the cockpit where, on long flights, the pilot usually put the plane on autopilot and then went to sleep on the floor, asking me to watch the controls.

That’s how I got to fly a range of larger commercial aircraft, from a Vickers Viscount VC-10 to a Boeing 747. Nothing beats flying a jumbo jet over the North Pole on a clear day, where the unlimited view ahead is nothing less than stunning.

When gold peaked in 1979 at $900 an ounce, up from $34, The Economist magazine asked me to fly from Japan to South Africa and write about the barbarous relic. That I did with great enthusiasm, bringing along my new wife, Kyoko.

Sure enough, as soon as I arrived, I noticed long lines of South Africans cashing in their Krugerrands, which they had been saving up for years in the event of a black takeover.

There was only one problem. My wife was Japanese.

While under the complicated apartheid system, Chinese were relegated to second class status along with Indians, Japanese were treated as “honorary whites” as Japan did an immense amount of trade with the country.

The confusion came when nobody could tell the difference between Chinese and Japanese, not even me. As a result, we were treated as outcasts everywhere we went. There was only one hotel in the country that would take us, the Carlton in Johannesburg, where John and Yoko Lennon stayed earlier that year.

That meant we could only take day tips from Joberg. We traveled up to Pretoria, the national capital, to take in the sights there. For lunch, we went to the best restaurant in town. Not knowing what to do, they placed us in an empty corner and ignored us for 45 minutes. Finally, we were brought some menus.

The Economist asked me to check out the townships where blacks were confined behind high barbed-wire fences in communities of 50,000. I was given a contact in the African National Conference, then a terrorist organization. Its leader, Nelson Mandela, had spent decades rotting away in an island prison.

My contact agreed to smuggle us in. While blacks were allowed to leave the townships for work, whites were not permitted in under any circumstances.

So, we were somewhat nonplussed Kyoko and I were asked to climb into the trunk of an old Mercedes. Really? We made it through the gates and into the center of the compound. On getting out of the trunk, we both burst into nervous laughter.

Some honeymoon!

After meeting the leadership, we were assigned no less than 11 bodyguards as whites in the townships were killed on sight. The favored method was to take a bicycle spoke and sever your spinal cord.

We drove the compound inspecting plywood shanties with corrugated iron roofs, brightly painted and packed shoulder to shoulder. The earth was dry and dusty. People were friendly, waving as we drove past. I interviewed several. Then we were smuggled out the same way we came in and hastily dropped on a corner in the city.

Apartheid ended in 1990 when the ANC took control of the country, electing Nelson Mandela as president. A massive white flight ensued which brought people like Elon Musk’s family to Canada and then to Silicon Valley.

Everyone feared the blacks would rise up and slaughter the white population.

It never happened.

Today, South Africa offers one of the more interesting investment opportunities on the continent. The end of apartheid took a great weight off the shoulders of the country’s economy. Check out the (EZA), which nearly tripled off of the 2020 bottom.

Kyoko passed away in 2002 at age 50.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

December 6, 2021

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT IS ON FOR DECEMBER 7-9) (MARKET OUTLOOK FOR THE WEEK AHEAD, or THE TRIPLE VIRUS ATTACK),

(SPY), (TLT), (BAC), (GS), (JPM), (VIX)

Those who were bemoaning the lack of market volatility certainly had their wishes fulfilled last week and then some. Volatility attacked the $30 level remorselessly like a hoard of barbarians. But it didn’t close there.

We actually got three Omicrons last week, the virus kind, the Fed kind, and the jobs variety, with the November Nonfarm Payroll report coming in at a paltry 210,000. Yet, the Headline unemployment rate cratered to a new post-pandemic low, from 4.6% to 4.2%. Go figure.

The Fed’s move amounts to a sudden dramatic lean towards a hawkish stance. The word “transitory” has hopefully been banished from the Fed lexicon for good.

The final flush on Friday no doubt cleansed the market like a colonoscopy, vaporizing any bad positions from yearend reports. That’s why the reopening stocks like hotels, cruise lines, airlines, and casinos were sold down so hard and bounced back with equal vigor.

Last week’s violence cleared the way for the yearend rally to continue, with the final destination a close at the year’s top tic all-time high.

Of course, everyone knows interest rates are rising except the bond market, where prices seemed to magically levitate, keeping interest rates low. Rumors of hedge funds covering shorts to bury losses abound. This is the trade that everyone universally got wrong.

I think the incredible move on Friday was due to hedge funds stampeding to cover money-losing short positions ahead of embarrassing yearend reports.

From here on, trading should get easier as the smarter money departs for Hawaii, the Caribbean, Aspen, or in this case Lake Tahoe, where the pristine waters and ski slopes beckon. Volume and volatility should bleed out from here.

I’m sticking with my long tech, long financials, and short bond strategy until payday, which should be soon.

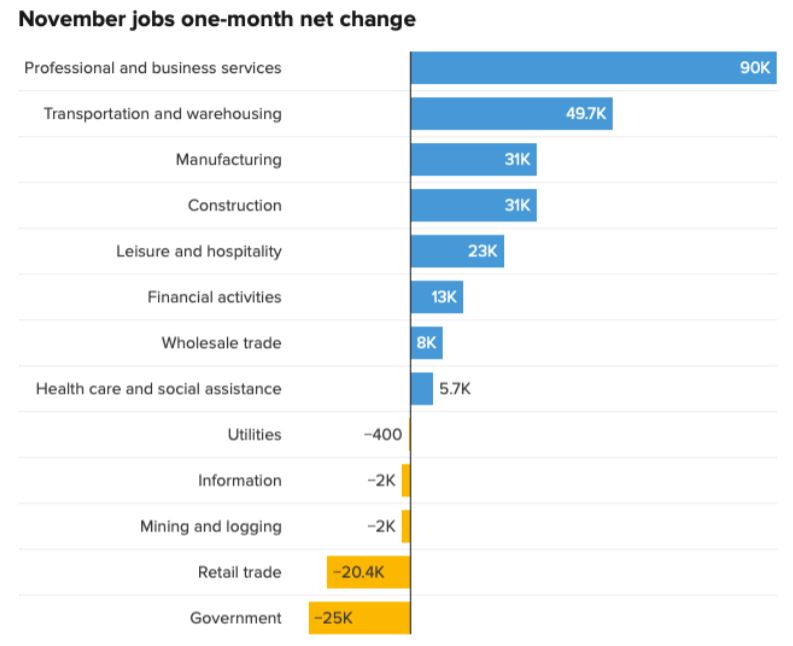

The Nonfarm Payroll Report Disappoints in November, coming in at 210,000. Over 600,000 was expected. The Headline Unemployment Rate fell to 4.2%, a new post pandemic low. There was a lot of confusing and contradictory data this month. Professional & Business Services added 90,000, Couriers & Messengers 26,800, and Leisure & Hospitality 23,000. But total Employment added 1.1 million. Government lost 25,000 jobs.

How Real is Omicron? On Friday, the market viewed it as a delta variant 2.0. I don’t think so. If anything, it shows how effective the global early response system has become to new variants. South Africa caught omicron with only a handful of cases and the borders started closing immediately. There is no indication that Omicron can’t be stopped by vaccination. It will only kill the anti-vaxers. It means we’re safer, not more at risk, and the economic recovery and the bull market should continue.

Oil Plunges Down 13% in a Day, breaking $70, as fears of a new variant-caused recession run rampant. It was a “sell everything” selloff.

Biden Says No Travel Restrictions or Lockdowns, in response to the new Covid Omicron variant. Therefore, no negative response for the stock market. It was worth a 350-point rally yesterday.

Pending Home Sales Soar by 7.5% in October. The Midwest showed the strongest sales, reflecting a mass migration to cheaper homes from the coasts.

ADP Comes in Red Hot at 534,000. Services dominated and Leisure & Hospitality picked up a massive 136,000. Large companies led the hiring binge. It augers well for the Friday Nonfarm Payroll Report.

More Taper Sooner was the bottom line on Powell’s comments last week. The Fed governor said in testimony in front of the Senate Banking Committee that inflation is no longer “transitory”, implying that hotter inflation numbers are to come. Yikes! Finally, a nod to reality! Stocks tanked 600 points on the comment. Bonds should crash but strangely are holding up. Watch this space. The news could give us a tradable bottom for all asset classes.

ISM Manufacturing Improves, from 60.8 to 61.1 in November. It’s more proof that the economy is expanding.

Weekly Jobless Claims Still Hot at 222,000, and continuing claims fell below 2 million, a new post-pandemic low. No recession here.

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With the pandemic-driven meltdown on Friday, my December month-to-date performance plunged to -4.58%. My 2021 year-to-date performance took a haircut to 72.18%. The Dow Average is up 13.00% so far in 2021.

I used the collapse in interest rates to add a 20% position in financial stocks, Goldman Sachs (GS), and Bank of America (BAC). I got hammered with my existing short in bonds, with the ten-year yield plunging to an eye-popping 1.37%.

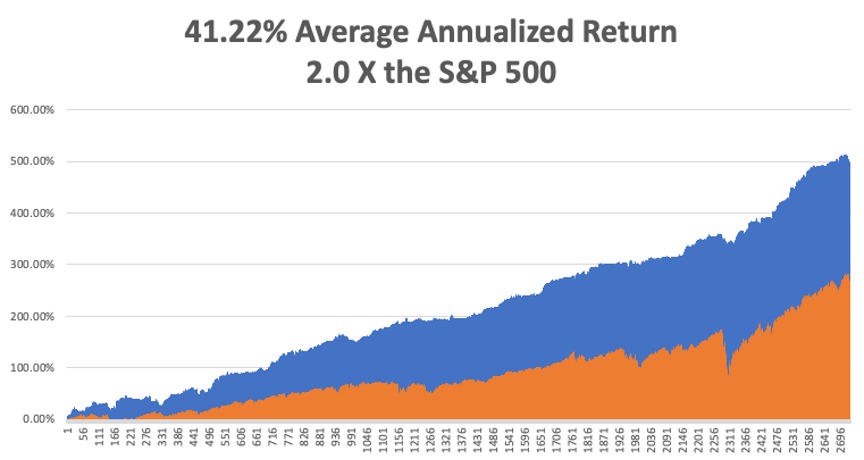

That brings my 12-year total return to 494.73%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 41.22% easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 49 million and rising quickly and deaths topping 788,000, which you can find here.

The coming week will be all about the inflation numbers.

On Monday, December 6, nothing of note takes place as we move into the yearend slowdown.

On Tuesday, December 7 at 5:30 AM EST, the US Balance of Trade is released for October. We will remember Pearl Harbor Day when the US Navy lost 3,000 men.

On Wednesday, December 8 at 5:15 AM, the JOLTS Job Openings for October are published.

On Thursday, December 9 at 8:30 AM, the Weekly Jobless Claims are disclosed.

On Friday, December 10 at 5:30 AM EST the US Inflation Rate for November is printed. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, occasionally I tell close friends that I hitchhiked across the Sahara Desert alone when I was 16 and am met with looks that are amazed, befuddled, and disbelieving, but I actually did it in the summer of 1968.

I had spent two months hitchhiking from a hospital in Sweden all the way to my ancestral roots in Monreale, Sicily, the home of my Italian grandfather. My next goal was to visit my Uncle Charles, who was stationed at the Torreon Air Force base outside of Madrid, Spain.

I looked at my Michelin map of the Mediterranean and quickly realized that it would be much quicker to cut across North Africa than hitching all the way back up the length of Italy, cutting across the Cote d’Azur, where no one ever picked up hitchhikers, then all the way down to Madrid, where the people were too poor to own cars.

So one fine morning found me taking deck passage on a ferry from Palermo to Tunis. From here on, my memory is hazy and I remember only a few flashbacks.

Ever the historian, even at age 16, I made straight for the Carthaginian ruins where the Romans allegedly salted the earth to prevent any recovery of a country they had just wasted. Some 2,000 years later, it worked as there was nothing left but an endless sea of scattered rocks.

At night, I laid out my sleeping bag to catch some shut-eye. But at 2:00 AM, someone tried to bash my head in with a rock. I scared them off but haven’t had a decent night of sleep since.

The next day, I made for the spectacular Roman ruins at Leptus Magna on the Libyan coast. But Muamar Khadafi pulled off a coup d’état earlier and closed the border to all Americans. My visa obtained in Rome from King Idris was useless.

I used to opportunity to hitchhike over Kasserine Pass into Algeria, where my uncle served under General Patton in WWII. US forces suffered an ignominious defeat until General Patton took over the army 1n 1943. Some 25 years later, the scenery was still littered with blown-up tanks, destroyed trucks, and crashed Messerschmitt’s.

Approaching the coastal road, I started jumping trains headed west. While officially the Algerian Civil War ended in 1962, in fact, it was still going on in 1968. We passed derailed trains and smashed bridges. The cattle were starving. There was no food anywhere.

At night, Arab families invited me to stay over in their mud brick homes as I always traveled with a big American Flag on my pack. Their hospitality was endless, and they shared what little food they had.

As a train pulled into Algiers, a conductor caught me without a ticket. So, the railway police arrested me and on arrival took me to the central Algiers prison, not a very nice place. After the police left, the head of the prison took me to a back door, opened it, smiled, and said “si vou plais”. That was all the French I ever needed to know. I quickly disappeared into the Algiers souk.

As we approached the Moroccan border, I saw trains of camels 1,000 animals long, rhythmically swaying back and forth with their cargoes of spices from central Africa. These don’t exist anymore, replaced by modern trucks.

Out in the middle of nowhere, bullets started flying through the passenger cars splintering wood. I poked my Kodak Instamatic out the window in between volleys of shots and snapped a few pictures.

The train juddered to a halt and robbers boarded. They shook down the passengers, seizing whatever silver jewelry and bolts of cloth they could find.

When they came to me, they just laughed and moved on. As a ragged backpacker I had nothing of interest for them.

The train ended up in Marrakesh on the edge of the Sahara and the final destination of the camel trains. It was like visiting the Arabian nights. The main Jemaa el-Fna square was amazing, with masses of crafts for sale, magicians, snake charmers, and men breathing fire.

Next stop was Tangiers, site of the oldest foreign American embassy, which is now open to tourists. For 50 cents a night, you could sleep on a rooftop under the stars and pass the pipe with fellow travelers which contained something called hashish.

One more ferry ride and I was at the British naval base at the Rock of Gibraltar and then on a train for Madrid. I made it to the Torreon base main gate where a very surprised master sergeant picked up half-starved, rail-thin, filthy nephew and took me home. Later, Uncle Charles said I slept for three days straight. Since I had lice, Charles shaved my head when I was asleep. I fit right in with the other airmen.

I woke up with a fever, so Charles took me to the base clinic. They never figured out what I had. Maybe it was exhaustion, maybe it was prolonged starvation. Perhaps it was something African. Possibly, it was all one long dream.

Afterwards, my uncle took for to the base commissary where I enjoyed my first cheeseburger, French fries, and chocolate shake in many months. It was the best meal of my life and the only cure I really needed.

I have pictures of all this which are sitting in a box somewhere in my basement. The Michelin map sits in a giant case of old, used maps that I have been collecting for 60 years.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Mediterranean in 1968

Global Market Comments

November 29, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or NOW IT’S THE OMICRON VARIANT)

(TSLA), (NVDA), (VIX), (SPX), (JPM)

Rioting in Holland and Austria, protests in France, the new lockdowns prompted by the new Omicron Variant of the Covid virus had only one message for American Investors: SELL!

The end result was the biggest down day in 15 months, with the Dow exceeding a 1,000-point bruise at the lows, not bad for a half-day holiday session.

While the market was bidless for most stocks, that wasn’t true for the best quality fastest growers. Tesla (TSLA) gave up only 3%, Microsoft 2.4%., and NVIDIA (NVDA) 3.5%. I tried to buy several at the close and failed, even though I kept raising my bid.

We also saw one of the sharpest declines in the history of the Mad Hedge Market Timing Index, from an overbought 85 to a bargain basement 31 in mere days.

This is exactly what the market needed.

I went into last week 100% in cash because I was leery of a market that traded sideways on declining volume after a historic run. In fact, we needed some kind of selloff before the market could go higher.

As I never tire of telling followers, cash is a position and has option value. A dollar at a market top is worth $10 at a market bottom. I had to endure only 50 market corrections before I figured this out, wishing I had cash at the bottom.

At the Friday low, stocks had sold off 1,850 points, or exactly 5.0% from the November 8 high. Heard that number before?

Before stock could rise, they had to fall first. The fears over Omicron are complete nonsense. It will not affect the US economy or stock markets one iota. Some 90% of the US population is now immune to Covid. There is no evidence that Omicron can overcome vaccines. When the variant comes here, and you can’t stop it, it will only kill anti-vaxers, as it did in Europe.

The fact is that the US continues to grow at a prolific 7% rate, with no sign of slowing in sight. As the port congestion fades, supply chains will repair and the inflation that is incited will fade. US companies are making more money than ever.

We still have a second reopening trade on for 2022. In a year, the economy will be booming, we will be at full employment, inflation will have faded, the pandemic will be over, and stocks will be at new all-time highs.

While some of next year’s performance has been pulled forward into 2021, much of it remains in the future.

So, when next time we take another run at a Volatility Index (VIX) of $29, I’ll be in there with guns blazing picking up all the usual suspects.

Global Stock on Pandemic Fears Smashes Markets, with Dow futures down 800 and ten-year yields off 13 basis points. New mandatory lockdowns in Austria and Holland have triggered rioting. It’s just another less than 5% correction.

The farther we go down now, the more we can go up in December and January. America’s 90% immunity will hold at bay any variants. There is no evidence this new one can’t be stopped by vaccines. Africa is another story. I went into this 80% cash. Wait for the selling to burn out in a day or two then use the high volatility to add front-month call spreads and LEAPS in your favorites.

Biden Appoints Jay Powell for a second time in a major lurch to the middle by the president. It’s the opening shot in the 2022 mid-term elections. I’ll approve your Fed governor if you pass my social safety net. It turned out to be impossible to find anyone more dovish than Jay Powell. The stock market loves it, especially interest rate-sensitive financials. The yearend rally continues.

Another $1.75 trillion Social Spending Bill passes the House, but most won’t see the light of day in the Senate. At best, maybe a few hundred million in spending gets through. Expect to hear a lot about socialism and deficits. No market impact here.

New Home Sales lag, up only 0.8% in October versus 1.4% expected. Some 6.34 million units were shifted. Only 1.25 million homes are for sale, down 12% YOY, representing only a 2.4-month supply.

The median price for a home rose to $353,900, up 13.1% YOY, but local markets like Phoenix and Seattle are seeing far greater gains. Million-dollar homes are seeing the greatest gains, with institutional investors pouring into the market to lock in historic low-interest rates.

Rents soar by 36% in New York and Florida against a national average of 13% in October is another sign of reopening and a return to normal.

Biden Taps the SPR, releasing some 50 million barrels, or two days’ worth of consumption. The president is throwing the gauntlet down at OPEC. Oil rallied on the news, as it was not more. This is largely a symbolic gesture and will have a minimal impact on gasoline prices. Now that the US is a net energy exporter it should close down the SPR as it is simply a subsidy for a dying fuel source that is going to zero and a bribe for Texas and Louisiana voters.

Weekly Jobless Claims plunge to a 52-year low, to 199,000. People are finally coming out of hiding and going back to work. It makes the upcoming November Nonfarm Payroll Report pretty interesting. Mark it on your calendar.

Tesla sales are on fire in California, the largest market in the US. The newest small SUV Model Y is leading the charge. No other company is close to mass production of a competitor yet. Tesla has a 5% market share in the Golden State ranking it no five among all car sales. A $7,500 tax credit that started last week is a big tailwind, but you have to tax taxes to benefit. Buy (TSLA) on dips, a Mad Hedge 380 bagger. My target is $10,000, 8X from here.

The Ports Log Jam is breaking. 24-hour shifts at Los Angeles and Long Beach, which handle 40% of all US unloadings, are making a big difference. Once the supply chain problems go away, so will inflation.

My Ten Year-View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With the pandemic-driven meltdown on Friday, my November month-to-date performance plunged to -10.74%. My 2021 year-to-date performance took a haircut to 77.82%. The Dow Average is up 14.05% so far in 2021.

I used a spike on bond prices to add a 20% position in bonds and the Friday dive to go long JP Morgan (JPM), so I am 70% in cash. I will be using any further volatility spikes to add positions in the coming week.

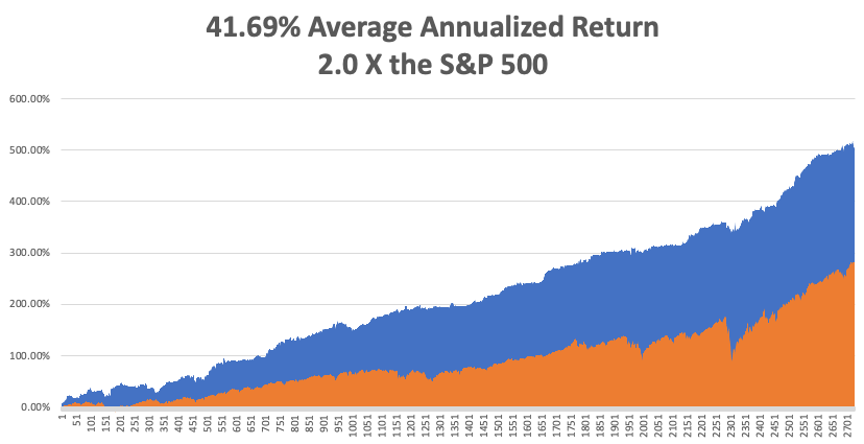

That brings my 12-year total return to 500.37%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 41.69% easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 48.2 million and rising quickly and deaths topping 780,000, which you can find here.

The coming week will be all about the inflation numbers.

On Monday, November 29 at 7:00 AM, Pending Homes Sales for October are released.

On Tuesday, November 30 at 6.45 AM, the S&P Case Shiller National Home Price Index is announced.

On Wednesday, December 1 at 5:15 AM, the ADP Private Employment Report is printed.

On Thursday, December 2 at 8:30 AM, the Weekly Jobless Claims are disclosed.

On Friday, December 3 at 8:30 AM EST, the November Nonfarm Payroll Report is published. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, with all the recent violence in the Middle East, I am reminded of my own stint in that troubled part of the world. I have been emptying sand out of my pockets since 1968, when I hitchhiked across the Sahara Desert, from Tunisia to Morocco.

During the mid-1970s, I was invited to a press conference given by Yasser Arafat, founder of the Al Fatah terrorist organization and leader of the Palestine Liberation Organization, at the Foreign Correspondents Club of Japan. His organization then rampaged throughout Europe, attacking Jewish targets everywhere.

Japan recognized the PLO to secure their oil supplies from the Persian Gulf, on which they were utterly dependent.

It was a packed room on the 20th floor of the Yurakucho Denki Building, and much of the world’s major press was represented, as the PLO had few contacts with the west.

Many placed cassette recorders on Arafat’s table in case he said anything quotable. Then Arafat ranted and raved about Israel in broken English.

Mid-sentence, one machine started beeping. A journalist jumped up to turn his tape over. Suddenly, four bodyguards pulled out Uzi machine guns and pointed them directly at us.

The room froze.

Then a bodyguard deftly set his Uzi down on the table flipped over the offending cassette, and the remaining men stowed their weapons. Everyone sighed in relief. I thought it was interesting that the PLO was using Israeli firearms.

The PLO was later kicked out of Jordan for undermining the government there. They fled Lebanon for Tunisia after an Israeli invasion. Arafat was always on the losing side, ever the martyr.

He later shared a Nobel Prize for cutting a deal with Israel engineered by Bill Clinton in 1993, recognizing its right to exist. He died in 2004.

Many speculated that he had been poisoned by the Israelis. My theory is that the Israelis deliberately kept Arafat alive because he was so incompetent. That is the only reason he made it until 75.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 5, 2021

Fiat Lux

Featured Trade:

(NOVEMBER 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(BRKB), (COIN), (IWM), (GOOGL), (MSFT), (MS), (GS), (JPM),

(BABA), (BIDU), (JD), (ROM), (PYPL), (FXE), (FXA), (FXB), (CRSP), (TSLA), (FXI), (BITO), (ETHE), (TLT), (TBT), (BITO), (CGW)

Below please find subscribers’ Q&A for the November 3 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon

Valley.

Q: Have you considered buying Coinbase (COIN)?

A: Yes, we actually recommended it as part of our Bitcoin service in the early days back in July. It’s gone up 62% since then, right along with the Bitcoin move itself. So yeah, buy (COIN) on dips—and there will be dips because it will be at least triple the volatility of the main market. And be sure to dollar cost average.

Q: Do you think the breakout in small caps (IWM) will hold and, if so, should we focus on small-c growth?

A: Yes it will hold, but no I would focus on the big cap barbells, which will lead this rally for the next 6 months. And there you’re talking about the best of tech which is Google (GOOGL) and Microsoft (MSFT), and the best of financials which is Morgan Stanley (MS), Goldman Sachs (GS), and JP Morgan (JPM).

Q: Why not time the webinar for after the FOMC? What will be the market reaction?

A: Well, first of all, we already know what they’re going to say—it’s been heavily leaked in the last week. The market reaction will be initially a potential sharp down move that lasts a few minutes or hours, and then we start a grind up for the next two months. So that's why I wanted to be 80% leverage long going into this. Second, we have broadcast this webinar at the same time for the last 13 years and if we change the time we will lose half our customers.

Q: Why do you always do debit spreads?

A: They’re easier for beginners to understand. That’s the only reason. If you’re sophisticated enough to do a credit spread, the results will be the same but the liquidity will be slightly better, and you can also apply that credit to meet your margin requirements. We have a lot of basic beginners signing up for our service in addition to seasoned pros and I always encourage people to do what they're most comfortable with.

Q: Are you still comfortable with the Morgan Stanley (MS) and Berkshire Hathaway (BRKB) positions?

A: I expect both to go up 10-20% by March, so that’s pretty comfortable. By the way, if you have extremely deep in the money call spreads on Goldman Sachs or Morgan, consider taking profits on those and rolling your strikes up. If you have like the $360-$380 vertical bull call spread in Goldman Sachs, realize that gain and roll up to the $420-$430 March position in Goldman Sachs—that will give you another 100% profit by March. With the $360-$ 380s, you have like 97% of the profit already in the price, there’s no leverage left and no point in continuing, you can only go down.

Q: What should I do with my China position?

A: Sell all your positions in China, realize all the losses now so you can offset those with all the huge profits on all your other positions this year. There I’m talking about Ali Baba (BABA), Baidu (BIDU), and (JD), which have been absolutely hammered anywhere from down 50% to down 70%. And do it now before everyone else does it for the same reasons.

Q: Thoughts on Paypal (PYPL) lately?

A: The stock is out of favor as money is moving out of PayPal into newer fintech stocks. The move down is totally unjustified and screaming long term buy here, but for the short-term investors are going to raid the piggy bank, sell the PayPal, and go into the newer apps. This has been my biggest money-losing trade personally this year because PayPal long-term has a great story.

Q: Will earnings fall off next year due to prior year comparisons or supply chain?

A: No, if anything, earnings are accelerating because supply chain problems mean you can charge customers whatever you want and therefore increase margins, which is why the stock market is going up.

Q: Long term, what would your wrong strikes be?

A: I would say don’t get greedy. I’m doing the ProShares Ultra Technology (ROM) $120-$125 call spread for May expiration—the longest expiration they offer. That gives you about 100% return in 6 months; 100% is good enough for me because then I’ll do the same thing again in May and get another 100%. What’s 100% x 100%? It’s 400% because you’re reinvesting a much larger capital base the second time around. If a 100% profit in six months is not enough for you then you are in the wrong line of business.

Q: Do you think Ethereum (ETHE) has long-term potential upside?

A: Yes, is a 10X move enough? We just had a major new high in Ethereum because they made moves to limit the production of new Ethereum. Ethereum is the superior technology because its architecture avoids the code repeats that Bitcoin does and therefore only uses a third of the electricity to create. But Bitcoin is attracting the big institutional cash flows because they have an early mover advantage. By the way, how much electricity does crypto mining consume? The entire consumption of Washington state in a year, so it’s a big deal.

Q: What should I do about Crisper Therapeutics (CRSP)?

Crispr Therapeutics (CRSP) is my other disaster for this year because ignored the move up to $170—we’re now back into the $90’s again. So, I have 2023 LEAPS on that; I’m going to keep them, I’ve already suffered the damage, but the next time it goes up to $170 I’m selling! Once burned, twice forewarned. And part of the problem with the whole biotech sector is we are now in the back end of the pandemic and anything healthcare-related will get hit, except for the vaccine stocks like Pfizer (PFE) which are still making billions and billions of dollars.

Q: I bought Baidu (BIDU) and Alibaba (BABA) years ago at a much lower price and I'm still up quite a lot; what should I do?

A: If you have the big cushion, I would keep them and look for #1 recovery in the Chinese economy next year and #2 for the government to back off from their idiotic anticapitalism strategy because it’s costing them so much money.

Q: Is Robinhood (HOOD) a good LEAP candidate?

A: Only on a really big dip, and then you want to go out two years. With a stock that’s volatile as hell like Robinhood and could drop by half on no notice, so you only buy the big dips. It’s not a slowly grinding upward stock like Goldman Sachs (GS) and Morgan Stanley (MS) where you can add LEAPS now because you know it’s going to keep grinding up.

Q: How can Morgan Stanley go up when the chief strategist is bearish?

A: Their customers aren't listening to their chief strategist—they’re buying. And the volume of the stock, which is where Morgan Stanley makes money, is going through the roof, they’re making record profits there. And I've got Morgan Stanley stock coming out of my ears in LEAPS and so forth.

Q: What are 5 stocks you would buy right now?

A: Easy: Google (GOOGL), Microsoft (MSFT), Morgan Stanley (MS), Goldman Sachs (GS), and JP Morgan (JPM). Buy whatever is down that day. They’re all going up.

Q: Too late to buy Tesla (TSLA) calls?

A: Yes, it is. Tesla has a long history of 40% corrections; we had one that ended in May, and then it doubled (and then some). So yeah, too late to buy the calls here. Go back and read my research from May which said buy the stock and you get a car for free—and that worked again, except this time, you can get three free Tesla’s. A lot of subscribers have sent me pictures of their Teslas they got for free on my advice; I’m probably the largest salesman for Tesla for the last 10 years and all I got out of it was a free Powerwall (the red one)..

Q: How much higher do you think semiconductor companies will go?

A: Higher but it’s impossible to quantify. You’re getting very speculative short-term buying in there. So, I think it continues to the rest of the year, but with chips, you never know.

Q: Would you be buying Crispr Therapeutics (CRSP) at these levels?

A: Yes, but I would either just buy the stock and not be dependent on the calendar or buy a 2 ½ year LEAP and get an easy double on that.

Q: What about the currencies?

A: I don’t see much action in the currencies as long as the US is raising interest rates. I think the Euro (FXE), the Aussie (FXA), and the British pound (FXB) will be dead for the time being. Nobody wants to sell them but nobody wants to buy them either when you’re looking at a potential short term rise in the dollar from rising interest rates.

Q: What stable coins are the right answer for cryptocurrency?

A: The US dollar stable coin, but for price appreciation, you’re really looking at Bitcoin and Ethereum. Stable coins are stable, they don’t move; you want stuff that’s going to go up 5, 10, or 20 times over the next 10 years like Bitcoin (BITO) and Ethereum (ETHE). That is my crypto answer.

Q: What should I do about the iShares 20 Plus Year Treasury Bond ETF (TLT) $135-$140 put spread expiring in January?

A: If we get another run down to the $141 level that we saw last month, I would come out of all short treasury positions because you’re starting to run into time decay problems with the January expirations. And in case we remain in a range for some reason, I would be taking profits at the bottom end of the range. It was my mistake that I didn’t grab those profits when we hit $141 last time. So don’t let profits grow hair on them, they tend to disappear. We lost six months on this trade due to the delta virus and the mini-recession it brought us.

Q: Will there be accelerated tech selling in December because of the new tax rates?

A: What new tax rates? There has been no new tax bill passed and even if there were, I think people wouldn’t tax sell this year because the profits are enormous. They would rather do any selling in January at higher prices and then defer payment of those taxes by 18 months. I don’t think there will be any tax issues this year at all.

Q: What’s your return on solar power investments?

A: My break-even was four years because our local utility, PG&E, went bankrupt and the only way they're getting out of bankruptcy is raising electricity prices by 10% a year. It turns out that as a result of global warming, the panels have operated at a higher efficiency as well, so we’re getting a lot more power output than originally expected. Now I get free electricity for the remaining 20-year life of the panels which is great because with two Tesla’s and all-electric heating and air conditioning I use a lot of juice. My monthly bill is a sight to behold. I also power the 20 surrounding houses and for that PG&E pays me $1,800 a month.

Q: Do you see China (FXI) invading Taiwan as a potential threat to the market?

A: China will never invade Taiwan. They own many of the companies they're already in, they de facto control Taiwan government from a distance; they would not risk the international consequences of an actual invasion. And we have the US seventh fleet there to stop exactly that. So, they can make all the noise they want but nothing will come of it. I’ve been watching this for 50 years and nothing has ever happened.

Q: Would you buy ProShares Ultrashort 20+ Treasury ETF (TBT) here?

A: Absolutely, with both hands, all I can get.

Q: Can you recommend any water ETF opportunity?

A: Yes there is one I wrote a piece on last month. It’s the Claymore S&P Global Water Index ETF (CGW).

Q: How long can you hold the (TBT) before time decay hurts?

A: It doesn’t hurt, the cost of the TBT is two times the 10-year rate. So that would be 3%, plus 1% a year for management fees, and that’s your slippage on the TBT in a year right now—it’s 4%. Remember if you’re short the bond market, you have to pay the coupon when you’re short. Double the bond market and you have to pay double the coupon.

Q: Is the ProShares Bitcoin Strategy ETF (BITO) a good alternative to buying bitcoin?

A: I would say yes because I’ve been watching the tracking on that very carefully and it’s pretty damn close. Plus there’s a lot of liquidity there, so yeah, buy the (BITO) ETF on dips and dollar cost average.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 1, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LET THE GAMES BEGIN!)

(MS), (GS), (BLK), (JPM), (BAC), (TLT), (TSLA), (AAPL), (MSFT), (GOOGL), (AMZN), (ROM)

Welcome to the first day of November, when the seasonals swing from negative to positive. The hard six months are over. The next six should be like shooting fish in a barrel.

At least that’s what happened in the past. The period from November 1 to May 31 has delivered the highest stock returns for the past 75 years.

So how do we play a hand that we have already been dealt full of aces and kings?

Load the boat with financials, like (MS), (GS), (BLK), (JPM), and (BAC). Notice that when we had the sharpest rise in interest rates in a year, financials barely moved when they should have crashed? That means they will soon start going up again.

You might have also observed that technology stock has been flat-lining when rising rates should have floored them. That means their torrid 20% earnings growth will keep floating their boats.

It gets better. We just learned that the GDP growth rate plunged in Q3 from a rip-roaring 6% rate to only 2%. What happens next? That 4% wasn’t lost, just deferred into 2022. The rip-roaring 6% growth rate returns. That’s why stocks are pushing up to new all-time highs right now.

So, buy the dips. We may have seen our last 5% correction of 2021. The only unknown is how markets will react to a Fed taper, which could come as early as Wednesday. But on the heels of that, we will get a $1.75 billion rescue package, the biggest in 50 years. One will cancel out the other, and then some.

Take a look at the ProShares Ultra Technology Fund (ROM), the 2X long ETF. I just analyzed its 30 largest holdings. Half are tech stocks that have been trash and are down 30% or more. The other half are at all-times highs, like Microsoft (MSFT) and Alphabet (GOOGL).

What happens next when the seasonals are a tailwind? The tech stocks that are down will rally because they are cheap, while the high stocks keep going because they are best of breed. I think (ROM) has $150 written all over it by March.

You’ve got to love Elon Musk, whose net worth is approaching $300 billion. When the pandemic broke, every automaker cancelled their chip orders for the rest of the year while Tesla took them all. Today, Detroit has millions of cars built but in storage because they are all missing chips. In the meantime, Tesla is snagging orders for 100,000 cars at a time.

Like I say, you gotta love Musk. Hey, Elon, call me! Why don’t you just buy the entire US coal industry and shut it down. It would only cost $5 billion, as market caps are so low. That would have more impact on the environment than another million Teslas. Worst affected would be China, where 70% of US coal now goes.

A continued major driver of the bull case for stocks is profit margins of historic proportions.

Q1 saw a 13% margin, Q2 13.5% and Q3 12.3%, and Q3 had to carry the dead weight of a delta impaired GDP growth rate of only 2.0%. Imagine what companies can do in Q4 when the growth rate is returning to a torrid 6% rate.

This has been one of my basic assumptions for the entire year and it seems it was I was alone in having it. This is where the 90% year-to-date performance comes from.

Inflation is Here to Stay, says top investing heavyweights, at least 4% through 2022. That means high inflation, higher financial shares, and higher Bitcoin prices. It’s going to take two years to unwind the mess at the ports that is driving prices.

Covid is Getting Knocked Out by a One-Two Punch, via a new round of booster shots and imminent childhood vaccinations. It could take new cases to zero in a year and give us a booming economy.

S&P Case Shiller is Still Rocketing, the National Home Price Index up 19.8% YOY in August. Phoenix (33.3%), San Diego (26.2%), and Tampa (25.9%) were the hot cities. This will continue for a decade but as a slower rate.

New Home Sales Pop, to 800,000. Annual median prices jump at an annual 18.7% to $408,000. The share of homes selling over $1 million increased from 5% to 9% in a year. It cost $500,000 to get a starter home in an Oakland slum these days. Homebuilders Sentiment Soars to 80. Buy (KBH), (PUL), and (LEN) on dips.

Bonds Melt Up, creating one of the best trade entry points of the year. A successful 30-year auction this week that took yields from 1.71% down to 1.52% in a heartbeat. It makes no sense. Buying bonds here is like buying oil in the full knowledge that someday it will go to zero. I am doubling my short position here. Look at the (TLT) December 2022 $150-$155 vertical bear put spread LEAPS which is offering a 14-month return of 54%. This is the month when the Fed has promised to begin the first of six interest rate hikes. Just buy it and forget about it.

Proof that the Roaring Twenties is Here. It’s demand that is spiking, the greatest ever seen, not supplies that are drying up in the supply chain issue. It should continue for a decade and the bull market in stocks that follows it. You heard it here first. Dow 240,000 here we come.

Apple Blows it in Q3, with millions of its phones lost at sea and no idea when unloads are possible, costing it $6 billion in sales. Revenues were up a ballistic 29% YOY. Buy (AAPL) on dips. I see $200 a year next year.

Amazon Craters, with both shrinking revenues and profits. Supply chain problems about with several billion of inventory trapped at sea off the coast of Long Beach. It plans to hire 275,000 to handle the Christmas rush. The stock hit a one year low. There is a time to buy (AMZN) on the dip, but not quite yet.

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a massive +8.95% gain in =October. My 2021 year-to-date performance maintained 88.55%. The Dow Average is up 17.06% so far in 2021.

After the recent ballistic move in the market, I am continuing to run my longs in Those include (MS), (GS), (BAC), and a short in the (TLT). All are approaching their maximum profit point and we have nothing left but time decay to capture. So, I am going to run these into the November 19 expiration in 14 trading days. It’s like have a rich uncle write you a check one a day.

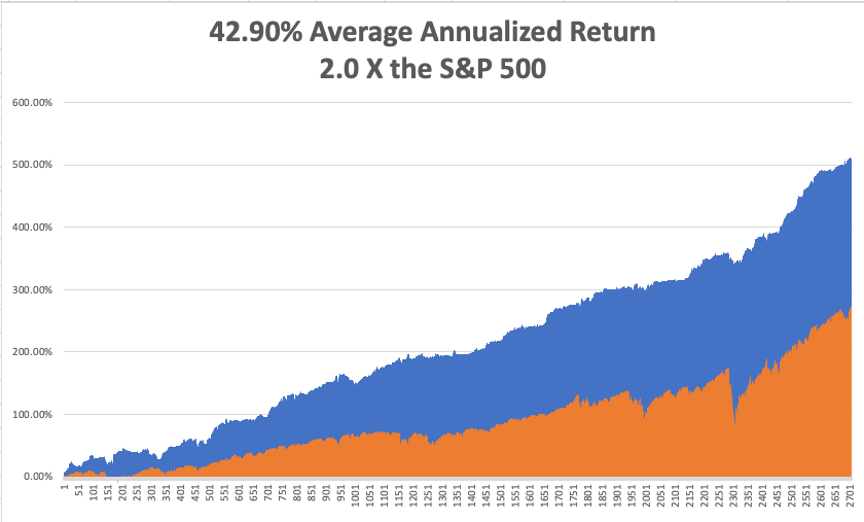

That brings my 12-year total return to 511.10%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.90%, easily the highest in the industry.

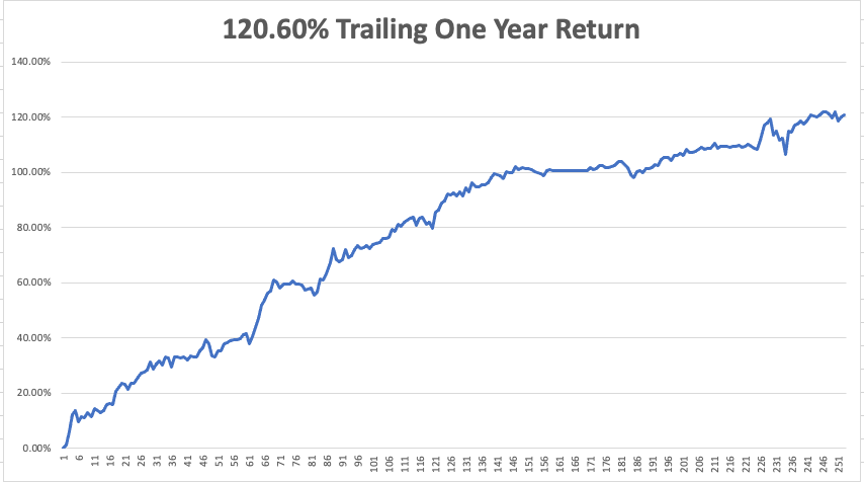

My trailing one-year return popped back to positively eye-popping 120.60%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 46 million and rising quickly and deaths topping 746,000, which you can find here.

The coming week will be slow on the data front.

On Monday, November 1 at 7:00 AM, the ISM Manufacturing PMI for October is out. Avis (CAR) Reports.

On Tuesday, November 2 at 1:30 PM, the API Crude Oil Stocks are released. Pfizer (PFE) reports.

On Wednesday, November 3 at 7:30 AM, the Private Sector Payroll Report is published. Etsy (ETSY) reports. At 11:00 AM, the Federal Reserve interest rate decision is announced, followed by a press conference.

On Thursday, November 4 at 8:30 AM, Weekly Jobless Claims are announced. Airbnb reports (ABNB).

On Friday, November 5 at 8:30 AM, The October Nonfarm Payroll Report is released. DraftKings (DKNG) reports. At 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

As for me, I have been known to occasionally overreach myself, and a trip to the bottom of the Grand Canyon a few years ago was a classic example.

I have done this trip many times before. Hike down the Kaibab Trail, follow the Colorado River for two miles, and then climb 5,000 feet back up the Bright Angle Trail for a total day trip of 27 miles.

I started early, carrying 36 pounds of water for myself and a companion. Near the bottom, there was a National Park sign stating that “Being Tired is Not a Reason to Call 911.” But I wasn’t worried.

The scenery was magnificent, the colors were brilliant, and each 1,000 foot descent revealed a new geologic age. I began the long slog back to the south rim.

As the sun set, it was clear that we weren’t going to make to the top. I was passed by a couple who RAN the entire route who told me “better hurry up.” I realized that I had erred in calculating the sunset, it'staking place an hour earlier in Arizona than in California.

By 8:00 PM it was pitch dark, the trail had completely iced up, and it was 500 feet straight down over the side. I only had 500 feet to go but the batteries on my flashlight died. I resigned myself to spending the night on the cliff face in freezing temperatures.

Then I saw three flashlights in the distance. Some 30 minutes later, I was approached by three Austrian Boy Scouts in full dress uniform. I mentioned I was a Scoutmaster and they offered to help us up.

I grabbed the belt of the last one, my companion grabbed my belt, and they hauled us up in the darkness. We made it to the top and I said, “thank you”, giving them the international scout secret handshake.

It turned out that I wasn’t in great shape as I thought I was. In fact, I hadn’t done the hike since I was a scout myself 30 years earlier. I couldn’t walk for three days.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Happy Halloween!