Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE TOP FIVE TECHNOLOGY STOCKS OF 2023),

(RIVN), (ROM), (ARKK), (PANW), (CRM), (FXE), (FXY), (FXA), (LEN), (KBH), (DHI), (TLT), (UUP), (META), (TSLA), (BA), (JNK), (HYG), (BRKB), (USO)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-14 10:04:422022-11-14 11:24:00November 14, 2022

The year 2022 has been driven by rising interest rates, a strong dollar, a weak economy, a bear market in stocks.

A massive reversal is about to take place. 2023 will gain the benefit of gale force macroeconomic tailwinds for the right stocks.

So far this year, Mad Hedge earned an astounding 77.20% profit cashing in on this year’s trends. We could earn the same return taking advantage of next year’s trends.

If you want to ride along on my coattails next year, that is fine with me. But it requires you to take a leap of faith.

I refer you to the motto of Britain’s Special Air Service: “Qui audet adipiscitur,” or “Who dares wins.”

For it only makes sense that the worst stocks of 2022 will be the best performers of 2023.

I have no doubt that tech stocks will bottom out sometime in 2023. Those who get in early will build some of the largest fortunes of this century. Those who miss the boat will spend their retirement years working at Taco Bell.

The reasons are very simple.

*Ultra-high interest rates will force a mild recession in early 2023. Then suddenly, inflation will plummet. We know this has already started because the largest element in the inflation calculation is housing costs, which are in free fall.

*The Fed will panic and deliver 2023 the sharpest DECLINE in interest rates in American history.

*Plunging interest rates will bring a crash in the US dollar.

*Foreign currencies like the Euro (FXE), the Japanese Yen (FXY), and the Australian dollar (FXA) will soar.

*And guess who gets the bulk of their earnings from abroad, sometimes up to two-thirds? The technology industry.

Kaching!

If you think I’m out of my mind, just look at the top performers of the historic stock market rally last week.

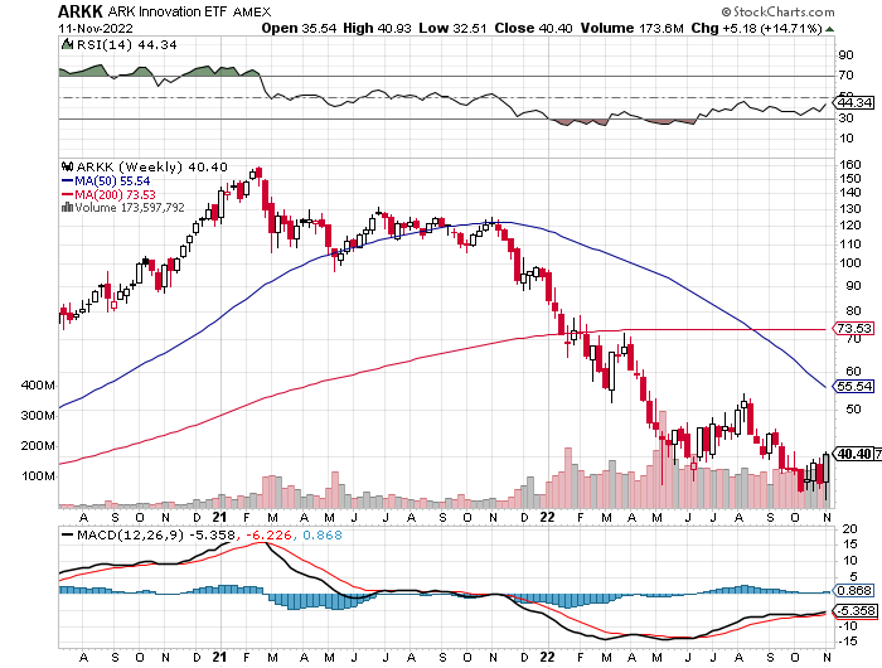

All the interest rate-sensitive sectors caught on fire. Technology stocks took off like a scalded cat, with Cathie Woods’ Ark Innovation Fund (ARKK) up an astounding 14% in a single day.

Bank shares soared. Homebuilders (LEN), (KBH), (DHI) caught a strong bid for the first time in ages. Junk bonds went bid only. US Treasury Bonds had their best day in 20 years (TLT), while the greenback (UUP) had its worst.

The bottom line here is so clear that I’ll write it on a wall for you. Falling interest rates will be the primary driver of stock prices for 2023 and 2024.

Of course, there is a better way to play this than buying the first technology index you stumble across.

So, let me boil this strategy down to just five names, close your eyes, and buy them.

Rivian (RIVN)– ($34) - Rivian is widely believed to be the next Tesla (TSLA). Some 25% owned by its largest customer, Amazon (AMZN), Rivian produces three types of EVs: the R1T pickup truck, the R1S SUV, and Amazon's EDV (electric delivery van). Its R1 vehicles start at under $70,000 and can travel more than 300 miles on a single charge. To learn more about Rivian, please click here.

To say that Rivian is the hot car of the day would be a vast understatement. New cars are trading for double list on the grey market. Owners complain of getting mobbed with gawkers whenever they hit the beach or the ski slopes. The buzz has led to an outstanding order book of an impressive 98,000, or four years of current production. The obvious cool factor allows enormous pricing power.

And here is the key to buying Rivian at this time. At 25,000, it is right at the mass production point where Tesla shares went ballistic all those years ago. And it already has an 80% decline in the price, in the rear-view mirror.

In 2024, Rivian plans to open its second plant in Georgia. After it fully expands its Illinois plant, it expects its annual production capacity to reach 600,000 vehicles.

Inflation Reduction Act passed this summer greatly accelerated rollout of the entire EV industry, which created a $7,500 per vehicle tax credit on top of state benefits.

Yes, this company offers venture capital-type risks. But it offers venture capital-type returns as well, up 10X-50X from here.

Ark Innovation Fund (ARKK) – ($40) – Cathie Woods’ high-tech fund was the proverbial red-headed stepchild of this bear market. It fell a gut-punching 80% from the 2021 top until last week. Just to get back to its old high, likely over the next five years, it has to rise by 400%. Its largest holdings are a real rollcall of the severely abused, Tesla (TSLA), Roku (ROKU), Exact Sciences (EXAS), Intellia (INTL), and Teladoc Health (TDOC), which Woods actively trades. But they are also a valuable insight into the future, EVs, CRISPR technology, robotic surgery, and molecular diagnostics. To learn more about the Ark Innovation Fund, please click here.

ProShares Ultra Technology ETF (ROM) – ($27) – This is a 2X long technology ETF that gives you an extremely aggressive position across the tech sector. It has 19% of its holdings in Apple (AAPL), 16% in Microsoft (MSFT), 10% in Alphabet (GOOGL) and Google (GOOG), at 3.5% in NVIDIA (NVDA), and 120 other smaller names. (ROM) shares are down a breathtaking 67% just in the past year. To learn more about the (ROM), please click here.

Palo Alto Networks (PANW) - $165 – Hacking is one of the fastest-growing sectors in technology, it is recession-proof and immune to the economic cycle. As a result, spending on the defense against hacking is absolutely exploding. Palo Alto Networks, Inc. is an American multinational cybersecurity company with headquarters in Santa Clara, California. Its core products are a platform that includes advanced firewalls and cloud-based offerings that extend those firewalls to cover other aspects of security. I have already earned a tenfold return over the past decade and expect to make another 10X in the coming years. You won’t find any dips in this stock as too many people are trying to get into it. To learn more about the Palo Alto Networks, please click here.

Salesforce (CRM) - $157 – The baby of tech genius Mark Benioff, this company is the dominant player in customer relationship management. If you want to do any business in the cloud, and almost all big companies do, you are up to your eyeballs in customer relationship management. Salesforce is the largest San Francisco-based cloud-oriented software company with virtually all of the Fortune 500 as its customer list. It provides customer relationship management software and applications focused on sales, customer service, marketing automation, analytics, and application development. Salesforce shares have been the target of a haymaker, down 55% in a year. To learn more about Salesforce, please click here.

You know what? I can do better than this.

I can create customized options LEAPS for you that will deliver a tenfold return on whatever performance these ultra-high beta stocks deliver. If the shares of one of my picks rise by 100%, you will make 1,000%.

This is an investment strategy that will enable you to retire early, real early. Tired of punching a time clock or logging into the next Zoom meeting on time?

Those will become a distant memory if you pursue my Mad Hedge Investment strategy for 2023.

As a result, my November month-to-date performance went off to the races, already achieving a hot +2.20%.

That leaves me with a very rare 100% cash position. With midterm election results out on Wednesday and the next report on the Consumer Price Index on Thursday, that sounds like a prudent place to be.

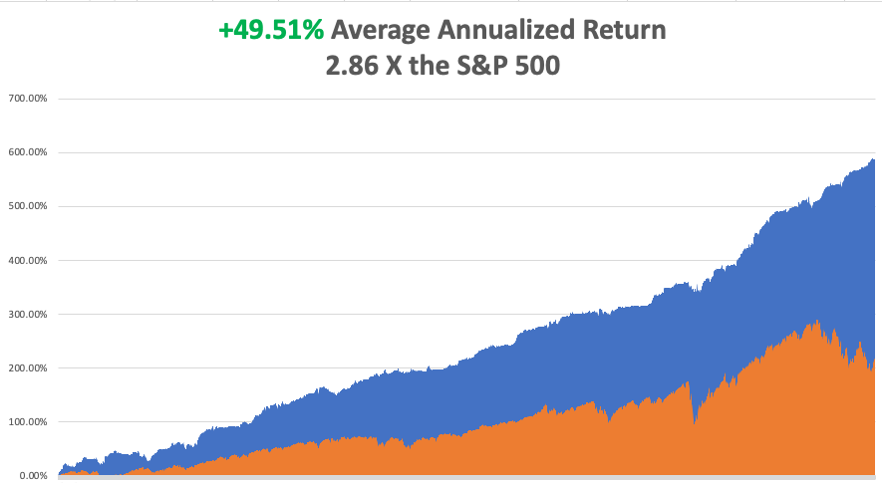

My 2022 year-to-date performance ballooned to +77.57%, a new high. The Dow Average is down -11.85% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +75.53%.

That brings my 14-year total return to +590.13%, some 2.86 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +49.51%, easily the highest in the industry.

Bonds Clock Best Day in Years, taking the ten-year US Treasury bond fund up $3.64. All low interest rate plays had monster days. Junk bond ETFs (JNK) and (HYG) were up two points. 30-year fixed rate mortgages dropped 60 basis points to 6.60%, the biggest drop in history. Long bonds will be THE big trade of 2023.

US Dollar has Worst Day in 20 Years, driven by plunging interest rates. Big tech, which gets a major share from overseas sales, rocketed. Apple alone was up $12. Cathy Wood’s Ark Innovation Fund (ARKK) was up an incredible 14%. It vindicates my view that tech will turn when interest rates and the dollar fall.

Oil Companies (USO) Book Record $200 Million Profit this year, using the Ukraine War to double your cost of gasoline. If we have a recession next year, or the war ends, energy share prices should be peaking around here. Even if they don’t, the risk-reward here is terrible. It means we will have to pay a much higher price to decarbonize the economy at a later date.

Wells Fargo Gets Hit with $1 Billion Fine for its many regulatory transgressions over the last decade. Looting of customer accounts with bogus fees has been a recurring problem. Use any selloffs to buy (WFC) on dips.

Berkshire Hathaway's 20% Profit Increase YOY and buys back another $1 billion worth of stock. However, they did take a $10 billion loss on stocks in Q3 during the market meltdown. Keep buying (BRKB) stock and LEAPS on dips.

$1.5 trillion in Homeowners Equity Lost Since May, thanks to interest rates at 20-year high and a shrinking money supply. Since July, the median home price has dropped by $11,560. The average borrower has lost $30,000 in equity. It’s not a great time to rent either as prices there are soaring. Residential housing could remain weak for another 12-24 months, compared to the six-year drawdown we had from 2006.

Boeing Orders Rise in October, but deliveries fall. The company is finally out of the penalty box, up 40% since October 1. Don’t buy (BA) up here.

The Red Wave Fails to Show, with control of congress still too close to call. Republican House control has shrunk from an expected 60 seats six months ago to maybe two today. Donald Trump threw the election for his party, picking unelectable extremist candidates and campaigning where he wasn’t wanted. A pro-life Supreme Court brought out millions of women voters across the country. If the Republicans can’t win with inflation at 8.7%, they are toast in 2024 when it drops back down to 2%.

Market Dives 646 Points on Democratic Win, with technology stocks taking the biggest hit. The red wave no-show was a black swan traders were not looking for. Energy was the worst performing sector because they aren’t getting the air cover they paid for with a red wave. The result was much as I expected, which is why I went into November 8 with a rare 100% cash position waiting to buy the next low. It turns out that rights are more important than prices.

Elon Musk Sells More Tesla Shares and Warns of a Twitter Bankruptcy, some $3.9 billion worth, bringing this year’s total to $36 billion. Musk is raising money to head off a bankruptcy of Twitter now that major advertisers are fleeing en masse. This certainly is a distress sale. If Musk was looking to build a real business, re-tweeting fringe conspiracy theories was the worst thing he could have done. Endorsing the Republican party will cost him half of his customers. Is this Musk’s Waterloo, or his Dien Bien Phu?

Facebook to Lay Off 11,000, about 13% of its total employees. Zuckerberg admits the error of pushing the company into the metaverse too far too fast. With the stock down 77%, there are not a lot of happy campers at One Hacker Way. Avoid (META) for now, but it may be a 2023 play when we get closer to a new final product.

FTX Becomes an Epic Bankruptcy, with $9.5 billion missing from its balance sheet, in one of the biggest blowups of the crypto age. Losses are expected to reach $50-$60 billion, with the bankruptcy of 130 affiliated companies. It is also a potential Dept of Justice target. All affiliated tokens and coins have gone to zero. So, placing your money with a fresh-faced kid in the Bahamas wearing baggy shorts and with no financial background was not such a great idea after all. It’s amazing how many serious people were sucked in on this one. At least Sam Bankman-Fried said he was sorry.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 14 at 8:00 AM, the Consumer Inflation Expectations for October are released.

On Tuesday, November 15 at 8:30 AM, the Producer Price Index for October is released.

On Wednesday, November 16 at 8:30 AM, Retail Sales for October are published.

On Thursday, November 17 at 8:30 AM, Weekly Jobless Claims are announced. Housing Starts and Permits for October are also out.

On Friday, November 18 at 10:00 AM, the Housing Starts for October are printed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I am often told that I am the most interesting man people ever met, sometimes daily. I had the good fortune to know someone far more interesting than myself.

When I was 14, I decided to start earning merit badges if I was ever going to become an Eagle Scout. I decided to start with an easy one, Reading Merit Badge, where you only had to read four books and write one review.

I was directed to Kent Cullers, a high school kid who had been blind since birth. During the late 1940s, the medical community thought it would be a great idea to give newborns pure oxygen. It was months before it was discovered that the procedure caused the clouding of corneas and total blindness. Kent was one of these kids.

It turned out that everyone in the troop already had Reading Merit Badge and that Kent had exhausted our supply of readers. Fresh meat was needed.

So, I rode my bicycle over to Kent’s house and started reading. It was all science fiction. America’s Space Program had ignited a science fiction boom and writers like Isaac Asimov, Jules Verne, Arthur C. Clark, and H.G. Welles were in huge demand. Star Trek came out the following year, in 1966. That was the year I became an Eagle Scout.

It only took a week for me to blow through the first four books. In the end, I read hundreds to Kent. Kent didn’t just listen to me read. He explained the implications of what I was reading (got to watch out for those non-carbon-based life forms).

Having listened to thousands of books on the subject, Kent gave me a first class education and I credit him with moving me towards a career in science. Kent is also the reason why I got an 800 SAT score in math.

When we got tired of reading, we played around with Kent’s radio. His dad was a physicist and had bought him a state-of-the-art high-powered short-wave radio. I always found Kent’s house from the 50-foot-tall radio antenna.

That led to another merit badge, one for Radio, where I had to transmit in Morse Code at five words a minute. Kent could do 50. On the badge below the Morse Code says “BSA.” In those days, when you made a new contact, you traded addresses and sent each other postcards.

Kent had postcards with colorful call signs from more than 100 countries plastered all over his wall. One of our regular correspondents was the president of the Palo Alto High School Radio Club, Steve Wozniak, who later went on to co-found Apple (AAPL) with Steve Jobs.

It was a sad day in 1999 when the US Navy retired Morse Code and replaced it with satellites. However, it is still used as beacon identifiers at US airfields.

Kent’s great ambition was to become an astronomer. I asked how he would become an astronomer when he couldn’t see anything. He responded that Galileo, the inventor of the telescope, was blind in his later years.

I replied, “good point”.

Kent went on to get a PhD in Physics from UC Berkely, no mean accomplishment. He lobbied heavily for the creation of SETI, or the Search for Extra Terrestrial Intelligence, once an arm of NASA. He became its first director in 1985 and worked there for 20 years.

In the 1987 movie Contact written by Carl Sagan and starring Jodie Foster, Kent’s character is played by Matthew McConaughey. The movie was filmed at the Very Large Array in western New Mexico. The algorithms Kent developed there are still in widespread use today.

Out here in the west aliens are a big deal, ever since that weather balloon crashed in Roswell, New Mexico in 1947. In fact, it was a spy balloon meant to overfly and photograph Russia, but it blew back on the US, thus its top secret status.

When people learn I used to work at Area 51, I am constantly asked if I have seen any spaceships. The road there, Nevada State Route 375, is called the Extra Terrestrial Highway. Who says we don’t have a sense of humor in Nevada?

After devoting his entire life to searching, Kent gave me the inside story on searching for aliens. We will never meet them but we will talk to them. That’s because the acceleration needed to get to a high enough speed to reach outer space would tear apart a human body. On the other hand, radio waves travel effortlessly at the speed of light.

Sadly, Kent passed away in 2021 at the age of 72. Kent, ever the optimist, had his body cryogenically frozen in Hawaii where he will remain until the technology evolves to wake him up. Minor planet 35056 Cullers is named in his honor.

There are no movies being made about my life…. yet. But there are a couple of scripts out there under development.

Watch this space.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/11/boy-scouts.png625418Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-14 10:02:212022-11-14 11:26:31The Market Outlook for the Week Ahead, or The Top Five Technology Stocks of 2023

Lately, my inbox has been flooded with emails from subscribers asking if the housing market is about to crash as a result of the recent bubble and if they should panic and sell their homes.

They have a lot to protect.

Since prices hit rock bottom in 2011 and foreclosures crested, the national real estate market has risen by 100%.

The hottest markets, like those in Seattle, San Francisco, and Reno, are up by more than 200%, and certain neighborhoods of Oakland, CA have shot up by 500%.

Looking at the recent housing statistics, I can understand their concern. In February, the data were the hottest on record across the board:

* Housing prices are still exploding to the upside with S&P Case Shiller Rising 21%, the one-month biggest spike in history

*Your Check is in the Mail, with the passage of the $1.9 trillion rescue package. A big chunk of this went into housing upgrades

* Goldman Sachs is Forecasting a Jobs Boom, that will take the headline Unemployment Rate down to 3.5% by yearend. Employed people buy houses.

*Workforce at home will double post-pandemic, maintaining demand for large homes. One-third of new stay-at-home workers are never going back.

*We are all now mortgage prisoners, trapped by our 2.75% fixed rate mortgages refied last year. Selling your home and rolling into a 7.5% mortgage isn’t that appealing. Selling so far has been minimal, the markets just shut down.

I have a much better indicator of future housing prices than the depressing numbers above. With the way homebuilder stocks like Lennar (LEN), KB Homes (KBH), and Pulte Homes (PHM) are trading since June, I’d say your home will be worth a lot more in a year, and possibly double in another five years. Many of these stocks are up nearly 35% since then, beating the market by far.

What I call “intergenerational arbitrage” will be the principal impetus. The main reason that we have just endured two “lost decades” of economic growth over the last 20 years is that 85 million baby boomers are retiring to be followed by only 65 million “Gen Xers”. When you are losing 20 million consumers, economies don’t grow very fast. For more about millennial investing habits, please click here.

When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and “RISK ON” assets like equities, and more buyers of assisted living facilities, healthcare, and “RISK OFF” assets like bonds. That’s what got us to a 0.32% yield in the ten-year at the low.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward to the other side of the pandemic and the reverse happens. The baby boomers will be out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home.

That is when you have 65 million Gen Xers being chased by 85 million of the “Millennial” generation trying to buy their assets!

By then, we will not have built new homes in appreciable numbers for 15 years and a severe scarcity of housing starts. Even before the pandemic, new home construction was taking place at half the 2008 peak. Residential real estate prices will naturally soar. Labor shortages will force wage hikes.

The middle-class standard of living will then reverse a 40-year decline. Annual GDP growth will return from the subdued 2% rate of the past many years to near the torrid 4% seen during the 1990s. It all leads to my “Return of the Roaring Twenties” scenario which you can learn about by clicking here.

It gets better.

It is certain that the current administration will restore tax deductions for state and local real estate taxes (SALT) lost in the 2017 tax bill. The cap on home mortgage interest rate deductions will also rise.

These two events will trigger an immediate 10% increase in the value of your home on an after-tax basis, and more on the coasts.

So, if someone approaches you with a discount offer for your home, I would turn around and run a mile the other way.

You should also pile into the stocks, options, and LEAPS of housing stocks in any future market dip.

Not to Worry

https://www.madhedgefundtrader.com/wp-content/uploads/2022/11/open-house-signs.png256576Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-02 09:04:082022-11-02 14:46:17Why There Won’t be a Housing Crash

There is no doubt whatsoever that the stock market tried to break down last week and failed. At worst, the Dow Average double bottomed at $29,600, the same level it reached on September 28.

And even that low was a mere 800 points lower than the one we set on June 14.

And that’s how it’s going to go.

Incremental new lows, followed by violent “rip your face off” rallies on enormous volume.

Until it ends.

That happens when markets start speculating about coming interest rate cuts sometime in 2023. And remember, you’re buying stocks for not what the economy is doing today, but for how well it will be performing in six to nine months.

You’re buying the future, not the present, or heaven forbid, the past.

That means you should use these throw-up-on-your-shoes days to scale into your favorite long-term companies. When markets inevitably rally, you can either sell for a short-term profit and rewind the video once again or keep it as part of a long-term holding.

It's a nice choice to have. I’ve been doing it all year.

With some of the greatest market volatility in market history, my October month-to-date performance ballooned to +5.00%.

I used last week’s extreme volatility to roll down strike prices for Tesla (TSLA) and JP Morgan (JPM) option spreads to manage my risk. I was still able to hang on to a 40% long position and threw out a new short in the S&P 500 at the end of Thursday.

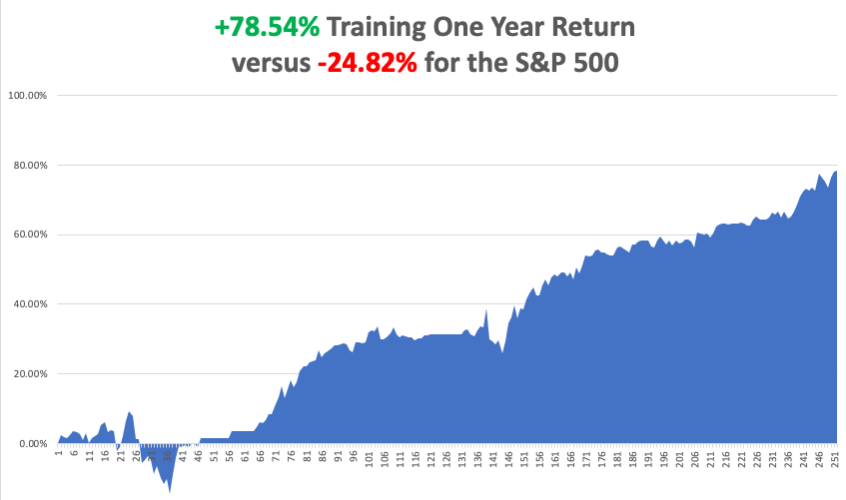

My 2022 year-to-date performance ballooned to +75.06%, a new high. The Dow Average is down -18.48% so far in 2022. With the coming Friday options expiration, I will be up +76.49%.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +78.54%.

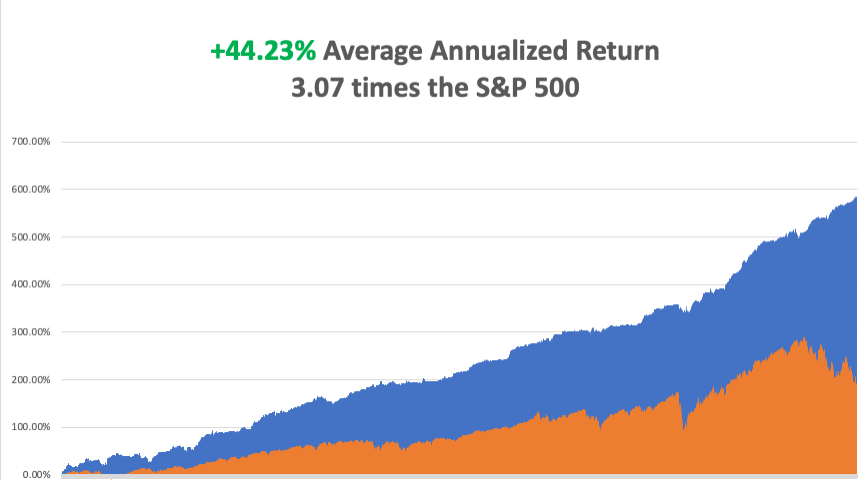

That brings my 14-year total return to +587.62%, some 3.03 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +44.23%, easily the highest in the industry.

Remember that old 60/40 equity/bond investment strategy? The idea was that whenever stocks went down, the losses would be offset by the profits from rising bonds.

This year, it delivered the worst performance in 100 years, down 34.4% year-to-date. That is the inevitable end result of a decade of zero interest rates and free money that took everything up.

So what is the best strategy you could probably employ right now? A 60/40 strategy. Even I find myself checking out bond yields these days, where I got my start in life as a trader 50 years ago. Yes, before there were stocks, there were bonds. Junk is now yielding 10%. Remember, that means a holding doubles in value every six years. The market is clearly in a mood to throw out the babies with the bathwater. I would be remiss not to mention the recent decline of Tesla posing one of its periodic tests of the faithful, now approaching a once unheard-of price earnings multiple of 30X.

Up until September 20, Elon Musk’s creation was almost immune to the bear market.

Then Twitter (TWTR) happened.

Musk agreed to take majority control of a $44 billion company, of which Elon himself is only contributing $16 billion. He sold Tesla shares last July to fund this. But the market wiped $333 billion, or 34.6%, off the market capitalization of the company. It is a wild overreaction to the move.

This has nothing to do with Tesla itself, as the richest man in the world is buying Twitter with his own pocket change. But it is undeniable that it will be a distraction of management time.

And here is all you need to know about Tesla. Tesla is the fastest growing large company in the world. Profit margins are increasing, thanks to the recent collapse of commodity prices. Unit sales will rise by 40% this year. Every time Tesla opens a new factory at a cost of $7 billion, it generates $15 billion of profit per year, forever!

Remember also, that the stock market gets an 800-pound gorilla off its back with the end of the midterm elections on November 8. It makes no difference who wins, a major uncertainty will be gone. That much IS certain.

And what happens when the Fed keeps interest rates too low for long, then raises them too much? It lowers them again too much, igniting a monster bull market in stocks. That’s also what you’re buying down here. That's what you get when you appoint a central bank governor with a political science major rather than PhDs and Nobel Prizes in Economics like the last ones.

Call it blunder 3.0.

Consumer Price Index Rockets Up to 8.6%, up 0.4% on the month and a new 40-year high. Stocks, bonds, crypto, and currencies were crushed and the US Dollar Soared. Look for new lows in stocks. Growth really took it on the nose. Expect another month of volatility until the next CPI report comes out.

Stocks Mount Historic Rally, gaining $1,420 points, or 5% of the intraday low. Stocks were down 500 in the wake of the CPI report, then up $1,420. It was mostly hedge short covering, as most institutions are too slow to react. Still, we now have a low to trade against.

The Fed Minutes are Out, and our central bank is clearly worried about doing too little than too much, when they are doing too much. At least they did six weeks, or 4,000 Dow points ago. The inflation goal is still 2.0%. Interest rates will go higher before they go lower.

Equity Inflows Hit a Record Last Week, the third highest week since 2008. Long term investors are willing to bottom fish here, even if the final bottom isn’t found for months.

Bond Liquidity Issues Haunting the Fed, and bids dry up in an endlessly falling market. The matter has been greatly exacerbated by a Fed that is now selling $95 billion a month as part of its quantitative tightening policy. It’s becoming increasingly difficult to move big blocks of bonds in a zero-bid market. Spreads are widening and size is shrinking. The bad news is that the worst is yet to come.

You Just Got an 8.7% Raise, if you are older than 61 and collecting Social Security. That is the payment increase that kicks in from January. Fortunately, some thoughtful person eons ago tied payments to the CPI, which is now going through the roof. I’m going to Hawaii with my money, even if the increase means that Social Security goes bankrupt by 2034, when I’m 82.

PC Sales Dive 19.5% in Q3, reaching only 68 million units. It’s the steepest decline since PC data collection began 30 years ago. And you wonder why they are selling the chip stocks so aggressively. High inventories are also a big problem. Lenovo was the top seller in the world at 20.2 million units, followed by Hewlett Packard’s (HPE) 17.6 million, and Dell (DELL) at 15.2 million.

Applied Materials Cuts Estimates, in line with everyone else in the industry. The new government export restrictions will cost it $250-$500 million in the current quarter. But how much is already in the price? Buy (AMAT) on dips.

Home Financing Pours into 5/1 ARMS, which can be had for a doable 5.56%. That compares to over 7.0% for the 30-year fixed, the highest since 2006. It will be low enough to keep homebuilders on life support for a couple of years Avoid (LEN) and (KBH).

REITS are Still Getting Slaughtered, with the plunge in the bond market today to multidecade lows. The REIT Index is down 30% this year, while the (SPY) is off only 21%. Real Estate Investment Trusts do best when interest rates are low. Too many investors piled into REITS in a desperate reach for yield. There’s a great trade here someday, but not yet.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil in a sharp decline and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, October 17 at 8:30 AM, the New York Empire State Manufacturing Index for September is released.

On Tuesday, October 18 at 7:00 AM, the D for September is out.

On Wednesday, October 19 at 8:30 AM, Housing Starts and Permits for September are published.

On Thursday, October 20 at 8:30 AM, Weekly Jobless Claims are announced. At 10:00 AM, we get Existing Home Sales for September. On Friday, October 21 at 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, it was in 1986 when the call went out at the London office of Morgan Stanley for someone to undertake an unusual task. They needed someone who knew the Middle East well, spoke some Arabic, was comfortable in the desert, and was a good rider.

The higher-ups had obtained an impossible-to-get invitation from the Kuwaiti Royal family to take part in a camel caravan into the Dibdibah Desert. It was the social event of the year.

More importantly, the event was to be attended by the head of the Kuwait Investment Authority, who ran over $100 billion in assets. Kuwait had immense oil revenues, but almost no people, so the bulk of their oil revenues were invested in western stock markets. An investment of goodwill here could pay off big time down the road.

The problem was that the US had just launched air strikes against Libya, destroying the dictator, Muammar Gaddafi’s royal palace, our response to the bombing of a disco in West Berlin frequented by US soldiers. Terrorist attacks were imminently expected throughout Europe.

Of course, I was the only one who volunteered.

My managing director didn’t want me to go, as they couldn’t afford to lose me. I explained that in reviewing the range of risks I had taken in my life, this one didn’t even register. The following week found me in a first-class seat on Kuwait Airways headed for a Middle East in turmoil.

A limo picked me up at the Kuwait Hilton, just across the street from the US embassy, where I occupied the presidential suite. We headed west into the desert.

In an hour, I came across the most amazing sight - a collection of large tents accompanied by about 100 camels. Everyone was wearing traditional Arab dress with a ceremonial dagger. I had been riding horses all my life, camels not so much. So, I asked for the gentlest camel they had.

The camel wranglers gave me a tall female, which was more docile and obedient than the males. Imagine that! Getting on a camel is weird, as you mount them while they are sitting down. My camel had no problem lifting my 180 pounds.

They were beautiful animals, highly groomed, and in the pink of health. Some were worth millions of dollars. A handler asked me if I had ever drunk fresh camel milk, and I answered no, they didn’t offer it at Safeway. He picked up a metal bowl, cleaned it out with his hand, and milked a nearby camel.

He then handed me the bowl with a big smile across his face. There were definitely green flecks of manure floating on the top, but I drank it anyway. I had to lest my host to lose face. At least it was white. It was body temperature warm and much richer than cow’s milk.

The motion of a camel is completely different from a horse. You ride back and forth in a rocking motion. I hoped the trip was short, as this ride had repetitive motion injuries written all over it. I was using muscles I had never used before. Hit your camel with a stick and they take off at 40 miles per hour.

I learned that a camel is a super animal ideally suited for the desert. It can ride 100 miles a day, and 150 miles in emergencies, according to TE Lawrence, who made the epic 600-mile trek to Aquaba in only four weeks in the heat of summer. It can live 15 days without water, converting the fat in its hump.

In ten miles, we reached our destination. The tents went up, clouds of dust rose, the camels were corralled, and the cooking began for an epic feast that night.

It was a sight to behold. Elaborately decorated huge five wide bronze platers were brought overflowing with rice and vegetables, and every part of a sheep you can imagine, none of which was wasted. In the center was a cooked sheep’s head with the top of the skull removed so the brains were easily accessible. We all ate with our right hands.

I learned that I was the first foreigner ever invited to such an event, and the Arabs delighted in feeding me every part of the sheep, the eyes, the brains, the intestines, and gristle. I pretended to love everything, and lied back and thought of England. When they asked how it tasted, I said it was great. I lied.

As the evening progressed, the Johnny Walker Red came out of hiding. Alcohol is illegal in Kuwait, and formal events are marked by copious amounts of elaborate fruit juices. I was told that someone with a royal connection had smuggled in an entire container of whiskey and I could drink all I wanted.

The next morning I was awoken by a bellowing camel and the worst headache in the world. I threw a rock at him to get him to shut up and he sauntered over and peed all over me.

The things I did for Morgan Stanley!

Four years later, Iraq invaded Kuwait. Some of my friends were kidnapped and held for ransom, while others were never heard from again.

The Kuwaiti government said they would pay for the war if we provided the troops, tanks, and planes. So they sold their entire $100 million investment portfolio and gave the money to the US.

Morgan Stanley got the mandate to handle the liquidation, earning the biggest commission in the firm’s history. No doubt, the salesman who got the order was considered a genius, earned a promotion, and was paid a huge bonus.

I spent the year as a Marine Corps captain, flying around assorted American generals and doing the odd special opp. I got shot down and still set off airport metal detectors. No bonus here. But at least I gained insight and an experience into a medieval Bedouin lifestyle that is long gone.

They say success has many fathers. This is a classic example.

You can’t just ride out into the Kuwait desert anymore. It is still filled with mines planted by the Iraqis. There are almost no camels left in the Middle East, long ago replaced by trucks. When I was in Egypt in 2019, I rode a few mangy, pitiful animals held over for the tourists.

When I passed through my London Club last summer, the Naval and Military Club on St. James Square, who’s portrait was right at the front entrance? None other than that of Lawrence of Arabia.

It turns out we were members of the same club in more ways than one.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

John Thomas of Arabia

Checking Out the Local Camel Milk

This One Will Do

Traffic in Arabia

https://www.madhedgefundtrader.com/wp-content/uploads/2022/10/john-thomas-camel-milk-e1666022569371.jpg357450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-10-17 11:02:592022-10-17 13:42:19The Market Outlook for the Week Ahead, or Blunder 3.0

Lately, my inbox has been flooded with emails from subscribers asking if the housing market is about to crash as a result of the housing bubble and if they should sell their homes.

They have a lot to protect.

Since prices hit rock bottom in 2011 and foreclosures crested, the national real estate market has risen by 50%.

The hottest markets, like those in Seattle, San Francisco, and Reno, are up by more than 125%, and certain neighborhoods of Oakland, CA have shot up by 500%.

Looking at the recent housing statistics, I can understand their concern. The data are the hottest on record across the board:

* Housing prices are still exploding to the upside with S&P Case Shiller Rising 10.4% in December, the one-month biggest spike in history

*Your Check is in the Mail, with the passage of the $1.9 trillion rescue package. A big chunk of this is going into housing upgrades

* Goldman Sachs is Forecasting a Jobs Boom, which will take the headline Unemployment Rate down to 4.1% by yearend. Employed people buy houses.

*Rising rates haven’t touched the housing market, and won’t for years.

*Workforce at home will double post-pandemic, maintaining demand for large homes

*30-year fixed-rate mortgages still a mere 3.26%, still near a historic low

*$45 billion in rental assistance is now available, thanks to Biden’s Rescue Package.

I have a much better indicator of future housing prices than the depressing numbers above. The way homebuilder stocks like Lennar (LEN), KB Homes (KBH), and Pulte Homes (PHM) are trading I’d say your home will be worth a lot more in a year, and possibly double in another five years. Many of these stocks are up nearly 200% since the March 23 bottom.

What I call “intergenerational arbitrage” will be the principal impetus. The main reason that we are just endured two “lost decades” of economic growth over the last 20 years is that 85 million baby boomers are retiring to be followed by only 65 million “Gen Xers”. When you are losing 20 million consumer economies, don’t grow very fast. For more about millennial investing habits,x please click here.

When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and “RISK ON” assets like equities, and more buyers of assisted living facilities, healthcare, and “RISK OFF” assets like bonds. That’s what got us to a 0.32% yield in the ten-year.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward to the other side of the pandemic and the reverse happens. The baby boomers will be out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home.

That is when you have 65 million Gen Xers being chased by 85 million of the “millennial” generation trying to buy their assets!

By then, we will not have built new homes in appreciable numbers for 14 years, and a severe scarcity of housing hits. Even before the pandemic, new home construction was taking place at half the 2008 peak. Residential real estate prices will naturally soar. Labor shortages will force wage hikes.

The middle-class standard of living will then reverse a 40-year decline. Annual GDP growth will return from the subdued 2% rate of the past four years to near the torrid 4% seen during the 1990s. It all leads to my “Return of the Roaring Twenties” scenario which you can learn about by clicking here.

It gets better.

It is certain that the current administration will restore tax deductions for state and local real estate taxes (SALT) lost in the 2017 tax bill. The cap on home mortgage interest rate deductions will also rise.

These two events will trigger an immediate 10% increase in the value of your home on an after-tax basis and more on the coasts.

So, if someone approaches you with a discount offer for your home, I would turn around and run a mile the other way.

You should also pile into the stocks, options, and LEAPS of housing stocks in any future market dip.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-13 20:04:042022-01-13 20:36:30Why a US Housing Boom Will Continue

I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini could navigate it.

I am anything but Houdini, so I go downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up-to-date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 12X pro.

Here is the bottom line which I have been warning you about for months. In 2022, you are going to have to work twice as hard to earn half as much money with double the volatility.

It’s not that I’ve turned bearish. The cause of the next bear market, a recession, is at best years off. However, we are entering the third year of the greatest bull market of all time. Expectations have to be toned down and brought back to earth. Markets will no longer be so strong that they forgive all mistakes, even mine.

2022 will be a trading year. Play it right, and you will make a fortune. Get lazy and complacent and you’ll be lucky to get out with your skin still attached.

If you think I spend too much time absorbing conspiracy theories or fake news from the Internet, let me give you a list of the challenges I see financial markets are facing in the coming year:

The Ten Key Variables for 2022

1) How soon will the Omicron wave peak?

2) Will the end of the Fed’s quantitative easing knock the wind out of the bond market?

3) Will the Russians invade the Ukraine or just bluster as usual?

4) How much of a market diversion will the US midterm elections present?

5) Will technology stocks continue to dominate, or will domestic recovery, and value stocks take over for good?

6) Can the commodities boom get a second wind?

7) How long will the bull market for the US dollar continue?

8) Will the real estate boom continue, or are we headed for a crash?

9) Has international trade been permanently impaired or will it recover?

10) Is oil seeing a dead cat bounce or is this a sustainable recovery?

The Thumbnail Portfolio

Equities – buy dips Bonds – sell rallies Foreign Currencies – stand aside Commodities – buy dips Precious Metals – stand aside Energy – stand aside Real Estate – buy dips Bitcoin – Buy dips

1) The Economy

What happens after a surprise variant takes Covid cases to new all-time highs, the Fed tightens, and inflation soars?

Covid cases go to zero, the Fed flip flops to an ease and inflation moderates to its historical norm of 3% annually.

It all adds up to a 5% US GDP growth in 2022, less than last year’s ballistic 7% rate, but still one of the hottest growth rates in history.

If Joe Biden’s build-back batter plan passes, even in diminished form, that could add another 1%.

Once the supply chain chaos resolves inflation will cool. But after everyone takes delivery of their over orders conditions could cool.

This sets up a Goldilocks economy that could go on for years: high growth, low inflation, and full employment. Help wanted signs will slowly start to disappear. A 3% handle on Headline Unemployment is within easy reach.

The weak of heart may want to just index and take a one-year cruise around the world instead in 2022 (here's the link for Cunard).

So here is the perfect 2022 for stocks. A 10% dive in the first half, followed by a rip-roaring 20% rally in the second half. This will be the year when a big rainy-day fund, i.e., a mountain of cash to spend at market bottoms, will be worth its weight in gold.

That will enable us to load up with LEAPS at the bottom and go 100% invested every month in H2.

That should net us a 50% profit or better in 2022, or about half of what we made last year.

Why am I so cautious?

Because for the first time in seven years we are going to have to trade with a headwind of rising interest rates. However, I don’t think rates will rise enough to kill off the bull market, just give traders a serious scare.

The barbell strategy will keep working. When rates rise, financials, the cheapest sector in the market, will prosper. When they fall, Big Tech will take over, but not as much as last year.

The main support for the market right now is very simple. The investors who fell victim to capitulation selling that took place at the end of November never got back in. Shrinking volume figures prove that. Their efforts to get back in during the new year could take the S&P 500 as high as $5,000 in January.

After that the trading becomes treacherous. Patience is a virtue, and you should only continue new longs when the Volatility Index (VIX) tops $30. If that means doing nothing for months so be it.

We had four 10% corrections in 2021. 2022 will be the year of the 10% correction.

Energy, Big Tech, and financials will be the top-performing sectors of 2022. Big Tech saw a 20% decline in multiples in 2022 and will deliver another 30% rise in earnings in 2022, so they should remain at the core of any portfolio.

It will be a stock pickers market. But so was 2021, with 51% of S&P 500 performance coming from just two stocks, Tesla (TSLA) and Alphabet (GOOGL).

However, they are already so over-owned that they are prone to dead periods as long as eight months, as we saw last year. That makes a multipronged strategy essential.

Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, and dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites are returning home by train because their religion forbade automobiles or airplanes.

The national debt ballooned to an eye-popping $30 trillion in 2021, a gain of an incredible $3 trillion and a post-World War II record. Yet, as long as global central banks are still flooding the money supply with trillions of dollars in liquidity, bonds will not fall in value too dramatically. I’m expecting a slow grind down in prices and up in yields.

The great bond short of 2021 never happened. Even though bonds delivered their worst returns in 19 years, they still remained nearly unchanged. That wasn’t good enough for the many hedge funds, which had to cover massive money-losing shorts into yearend.

Instead, the Great Bond Crash will become a 2022 business. This time, bonds face the gale force headwinds of three promised interest rates hikes. The year-end government bond auctions were a complete disaster.

Fed borrowing continues to balloon out of control. It’s just a matter of time before the last billion dollars in government borrowing breaks the camel’s back.

That makes a bond short a core position in any balanced portfolio. Don’t get lazy. Make sure you only sell a rally lest we get trapped in a range, as we did for most of 2021.

For the first time in ages, I did no foreign exchange trades last year. That is a good thing because I was wrong about the direction of the dollar for the entire year.

Sometimes, passing on bad trades is more important than finding good ones.

I focused on exploding US debt and trade deficits undermining the greenback and igniting inflation. The market focused on delta and omicron variants heralding new recessions. The market won.

The market won’t stay wrong forever. Just as bond crash is temporarily in a holding pattern, so is a dollar collapse. When it does occur, it will happen in a hurry.

5) Commodities (FCX), (VALE), (DBA)

The global synchronized economic recovery now in play can mean only one thing, and that is sustainably higher commodity prices.

The twin Covid variants put commodities on hold in 2021 because of recession fears. So did the Chinese real estate slowdown, the world’s largest consumer of hard commodities.

The heady days of the 2011 commodity bubble top are now in play. Investors are already front running that move, loading the boat with Freeport McMoRan (FCX), US Steel (X), and BHP Group (BHP).

Now that this sector is convinced of an eventual weak US dollar and higher inflation, it is once more the apple of traders’ eyes.

China will still demand prodigious amounts of imported commodities once again, but not as much as in the past. Much of the country has seen its infrastructure build out, and it is turning from a heavy industrial to a service-based economy, like the US. Investors are keeping a sharp eye on India as the next major commodity consumer.

And here’s another big new driver. Each electric vehicle requires 200 pounds of copper and production is expected to rise from 1 million units a year to 25 million by 2030. Annual copper production will have to increase 11-fold in a decade to accommodate this increase, no easy task, or prices will have to ride.

The great thing about commodities is that it takes a decade to bring new supply online, unlike stocks and bonds, which can merely be created by an entry in an excel spreadsheet. As a result, they always run far higher than you can imagine.

Accumulate commodities on dips.

Snow Angel on the Continental Divide

6) Energy (DIG), (RIG), (USO), (DUG), (UNG), (USO), (XLE), (AMLP)

Energy may be the top-performing sector of 2022. But remember, you will be trading an asset class that is eventually on its way to zero.

However, you could have several doublings on the way to zero. This is one of those times.

The real tell here is that energy companies are drinking their own Kool-Aid. Instead of reinvesting profits back into their new exploration and development, as they have for the last century, they are paying out more in dividends.

There is the additional challenge in that the bulk of US investors, especially environmentally friendly ESG funds, are now banned from investing in legacy carbon-based stocks. That means permanently cheap valuations and shares prices for the energy industry.

Energy stocks are also massively under-owned, making them prone to rip-you-face-off short squeezes. Energy now counts for only 3% of the S&P 500. Twenty years ago it boasted a 15% weighting.

The gradual shut down of the industry makes the supply/demand situation more volatile. Therefore, we could top $100 a barrel for oil in 2022, dragging the stocks up kicking and screaming all the way.

Unless you are a seasoned, peripatetic, sleep-deprived trader, there are better fish to fry.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly, that it blew a passenger train over on its side.

In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year.

We also see countless abandoned 19th century gold mines and the broken-down wooden trestles leading to them, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

Fortunately, when a trade isn’t working, I avoid it. That certainly was the case with gold last year.

2021 was a terrible year for precious metals. With inflation soaring, stocks volatile, and interest rates going nowhere, gold had every reason to rise. Instead, it fell for almost all of the entire year.

Bitcoin stole gold’s thunder, sucking in all of the speculative interest in the financial system. Jewelry and industrial demand was just not enough to keep gold afloat.

This will not be a permanent thing. Chart formations are starting to look encouraging, and they certainly win the price for a big laggard rotation. So, buy gold on dips if you have a stick of courage on you.

Would You Believe This is a Blue State?

8) Real Estate (ITB), (LEN)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the transcontinental railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley.

Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

There is no doubt a long-term bull market in real estate will continue for another decade, although from here prices will appreciate at a 5%-10% slower rate.

There is a generational structural shortage of supply with housing which won’t come back into balance until the 2030s.

There are only three numbers you need to know in the housing market for the next 20 years: there are 80 million baby boomers, 65 million Generation Xer’s who follow them, and 86 million in the generation after that, the Millennials.

The boomers have been unloading dwellings to the Gen Xers since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That’s what caused the financial crisis.

If they have prospered, banks won’t lend to them. Brokers used to say that their market was all about “location, location, location.” Now it is “financing, financing, financing.” Imminent deregulation is about to deep-six that problem.

There is a happy ending to this story.

Millennials now aged 26-44 are now the dominant buyers in the market. They are transitioning from 30% to 70% of all new buyers of homes.

The Great Millennial Migration to the suburbs and Middle America has just begun. Thanks to Zoom, many are never returning to the cities. So has the migration from the coast to the American heartland.

That’s why Boise, Idaho was the top-performing real estate market in 2021, followed by Phoenix, Arizona. Personally, I like Reno, Nevada, where Apple, Google, Amazon, and Tesla are building factories as fast as they can.

As a result, the price of single-family homes should rocket during the 2020s, as they did during the 1970s and the 1990s when similar demographic forces were at play.

This will happen in the context of a coming labor shortfall, soaring wages, and rising standards of living.

Rising rents are accelerating this trend. Renters now pay 35% of their gross income, compared to only 18% for owners, and less, when multiple deductions and tax subsidies are taken into account. Rents are now rising faster than home prices.

Remember, too, that the US will not have built any new houses in large numbers in 13 years. The 50% of small home builders that went under during the crash aren’t building new homes today.

We are still operating at only a half of the peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

That makes a home purchase now particularly attractive for the long term, to live in, and not to speculate with.

You will boast to your grandchildren how little you paid for your house, as my grandparents once did to me ($3,000 for a four-bedroom brownstone in Brooklyn in 1922), or I do to my kids ($180,000 for a two-bedroom Upper East Side Manhattan high rise with a great view of the Empire State Building in 1983).

That means the major homebuilders like Lennar (LEN), Pulte Homes (PHM), and KB Homes (KBH) are a buy on the dip.

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now. It’s also a great inflation play.

If you borrow at a 3.0% 30-year fixed rate, and the long-term inflation rate is 3%, then, over time, you will get your house for free.

How hard is that to figure out? That math degree from UCLA is certainly earning its keep.

Crossing the Bridge to Home Sweet Home

9) Bitcoin

It’s not often that new asset classes are made out of whole cloth. That is what happened with Bitcoin, which, in 2021, became a core holding of many big institutional investors.

But get used to the volatility. After doubling in three months, Bitcoin gave up all its gains by year-end. You have to either trade Bitcoin like a demon or keep your positions so small you can sleep at night.

By the way, right now is a good place to establish a new position in Bitcoin.

10) Postscript

We have pulled into the station at Truckee in the midst of a howling blizzard.

My loyal staff has made the ten-mile trek from my beachfront estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 50 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my Macbook Pro and iPhone 13 Pro, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above.

Good luck and good trading in 2022!

John Thomas

The Mad Hedge Fund Trader

The Omens Are Good for 2022!

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-05 13:00:512022-01-05 18:26:592022 Annual Asset Class Review

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.