Global Market Comments

August 7, 2019

Fiat Lux

Featured Trade:

(WHY I SOLD SHORT MACYS’),

(AMZN), (WMT), (M), (JWN), (KOL)

(TESTIMONIAL)

Global Market Comments

August 7, 2019

Fiat Lux

Featured Trade:

(WHY I SOLD SHORT MACYS’),

(AMZN), (WMT), (M), (JWN), (KOL)

(TESTIMONIAL)

Sorry, the Trade Alert to sell short Macys’ (M) went out late yesterday. I was speaking to a retail expert and his list of things wrong with the marquee name was so long that I couldn't get off the phone. New Yorkers are going to have to find something else to do on Thanksgiving Day than attend their famous parade.

His bottom line? Retail is in a death spiral from which it will never recover. Trying on clothes in a shopping mall will soon become a thing of the past, going the way of the buggy whip, black and white TV, and six-track tapes.

If you had to pick the biggest loser of our ongoing trade wars, which have just been ratcheted up in intensity, it would be the retail industry (XRT). Higher costs and tariffs can’t be passed on, minimum wages are rising in the big cities, lower selling prices are lower, and a massive inventory glut is NOT what money-making is all about.

The stocks have delivered as expected, providing one of the worst-performing sectors of 2019. Half of them probably won’t even make it until 2020.

In fact, Sears (S) and Macy’s (M) have announced more store closings nationwide. The overhead is killing them in a micro margin world.

So, I stopped at a Walmart (WMT) the other day on my way to Napa Valley to find out why.

I am not normally a customer of this establishment. But I was on my way to a meeting where a dozen red long-stem roses would prove useful. I happened to know you could get these for $10 a dozen at Walmart.

After I found my flowers, I browsed around the store to see what else they had for sale. The first thing I noticed was that half the employees were missing their front teeth.

The clothing offered was out of style and made of cheap material. It might as well have been the Chinese embassy. Most concerning, there was almost no one there, customers OR employees.

The Macy’s downsizing is only the latest evidence of a major change in the global economy that has been evolving over the last two decades.

However, it now appears we have reached both a tipping point and a point of no return. The future is happening faster than anyone thought possible. Call it the Death of Retail.

I remember the first purchases I made at Amazon 20 years ago. Even though I personally knew the founder, Jeff Bezos, from my Morgan Stanley days, the idea sounded so dubious that I made my initial purchases with a credit card with only a low $1,000 limit. That way, if the wheels fell off, my losses would be limited.

And how stupid was that name Amazon, anyway? At least, he didn’t call it “Yahoo” because it was already taken.

Today, I do almost all of my shopping at Amazon (AMZN). It saves me immense amounts of time while expanding my choices exponentially. And I don’t have to fight traffic, engage in the parking space wars, or wait in line to pay.

It can accommodate all of my requests, no matter how bizarre or esoteric. A WWII reproduction Army Air Corps canvas flight jacket in size XXL? No problem!

A used 42-inch Sub Zero refrigerator with a front-door icemaker and water dispenser? Have it there in two days, with free shipping at one fifth the $17,000 full retail price.

So I was not surprised when I learned this morning that Amazon accounted for 25% of all new online sales in 2018 in a market that is already growing at a breathtaking 20% YOY.

In 2000, after the great “Y2K” disaster that failed to show, I met with Bill Gates Sr. to discuss his foundation’s investments.

It turned out that they had liquidated their entire equity portfolio and placed all their money into bonds, a brilliant move coming mere months before the Dotcom bust and a 16-year bull market in fixed income.

Mr. Gates (another Eagle Scout) mentioned something fascinating to me. He said that unlike most other foundations their size, they hadn’t invested a dollar in commercial real estate.

It was his view that the US economy would move entirely online, everyone would work from home, emptying out city centers and rendering commuting unnecessary. Shopping malls would become low-rent climbing walls and paintball game centers.

Mr. Gates’ prediction may finally be occurring. Some counties in the San Francisco Bay area now see 25% of their workers telecommuting.

It is becoming common for staff to work Tuesday-Thursday at the office, and from home on Monday and Friday. Productivity increases. People are bending their jobs to fit their lifestyles. And oh yes, happy people work for less money in exchange for personal freedom, boosting profits.

The Mad Hedge Fund Trader itself may be a model for the future. We are entirely a virtual company with no office. Everyone works at home in four countries around the world. Oh, and we all use Amazon to do our shopping.

The downside to this is that whenever there is a snowstorm anywhere in the country, it affects our output. Two storms are a disaster, and at three, such as last winter, we grind to a virtual halt.

You may have noticed that I can work from anywhere and anytime (although sending a Trade Alert from the back of a camel in the Sahara Desert was a stretch), so was sending out an Alert while hanging on the cliff face of a Swiss Alp, but they both made money.

Moroccan cell coverage is better than ours, but the dromedary’s swaying movement made it hard to hit the keys.

The cost of global distribution is essentially zero. Profits go into a bonus pool shared by all. Oh, and we’re hiring, especially in marketing.

It is happening because the entire “bricks and mortar” industry is getting left behind by the march of history.

Sure, they have been pouring millions into online commerce and jazzed up websites. But they all seem to be poor imitations of Amazon with higher prices. It is all “Hour late and dollar short” stuff.

In the meantime, Amazon soared by 49% from December to the May high, and was one of the top performing stocks of 2018. There are now a cluster of Amazon analyst forecasts around the $3,000 mark.

And here is the bad news. Bricks and Mortar retailers are about to lose more of their lunch to Chinese Internet giant Alibaba (BABA), which is ramping up its US operations and is FOUR TIMES THE SIZE OF AMAZON!

There’s a good reason why you haven’t heard much from me about retailers. I made the decision 30 years ago never to touch the troubled sector.

I did this when I realized that management never knew beforehand which of their products would succeed, and which would bomb, and therefore were constantly clueless about future earnings.

The business for them was an endless roll of the dice. That is a proposition in which I was unwilling to invest. There were always better trades.

I confess that I had to look up the ticker symbols for this story as I never use them.

You will no doubt be enticed to buy retail stocks as the deal of the century by the talking heads on TV, Internet research, and maybe even your own brokers, citing how “cheap” they are.

Never confuse a low stock price with “cheap.”

It will be much like buying the coal industry (KOL) a few years ago, another industry headed for the dustbin of history. That was when “cheap” was on its way to zero for almost every company.

So the next time someone recommends that you buy retail stocks, you should probably lie down and take a long nap first. When you awaken, hopefully the temptation will be gone.

Or better yet, go shopping at Amazon. The deals are to die for.

To read “An Evening with Bill Gates Sr.”, please click here.

Global Market Comments

February 1, 2019

Fiat Lux

Featured Trade:

(THE DEATH OF KING COAL),

(KOL), (PEA),

(THE BRAVE NEW WORLD OF ONLINE RETAILING),

(SNAP), (GPRO), (APRN), (SFIX)

Global Market Comments

October 16, 2018

Fiat Lux

Featured Trade:

(WHY COAL IS A SHORT),

(KOL), (BHP), (UNG),

(TESTIMONIAL)

What has been one of the top performing asset classes since the beginning of 2016?

Is it Apple (AAPL), Amazon (AMZN), gold (GLD), oil (USO), or collectible French postage stamps?

If you said “Coal,” you win the kewpie doll.

In fact, the 19thcentury energy source was one of the best investments you could have made over the past three years.

Indeed, the Van Eck Coal ETF (KOL) has picked up an eye-popping 210% since it printed its $5 low the first week of 2016.

Google (GOOG) eat your heart out.

You might give credit to the president for the meteoric move, thanks to policies so overwhelmingly helpful to the industry that they brought tears to the eyes of the owners of coal mining companies.

But you’d be wrong again.

Most of the move took place before the election.

As a result, I have recently been deluged from readers asking if it is time to buy this prehistoric energy source.

My answer is no, not ever, and not even with Donald Trump’s money.

However, my answer relies more on basic market dynamics rather than any environmental sympathies I might have.

You can blame China.

The Beijing government is manipulating its domestic coal industry to prevent them from defaulting on hundreds of billions of dollars with of loans to local banks.

So, it has cut back the number of days the industry can operate from 330 to 276 days a year.

What happens when you restrict supply and increase demand? Prices go through the roof as they have done smartly.

It gets better.

The Middle Kingdom was hit with rainstorms of biblical proportions, flooding many mines and forcing them to close many mines. The sushi hit the fan.

That forced major consumers, the big steel producers, and electric power plants to resort to the international spot market, or the “seaborne market” to cover shortages to avoid shutting down themselves.

Who is the world’s largest supplier to the seaborne market?

That would be BHP Billiton (BHP), the largest capitalized company in Australia, which has seen its shares appreciate by 144% since 2016 bottom.

I have been following coal for 45 years ever since I was the coal correspondent for the Australian Financial Review during the 1970’s.

I had to write a mind-numbing five pieces a week on coal (the AFR was a daily). So it’s safe to say that I know which end of a lump of coal to hold upward.

For a start, you never want to invest in an asset that is dependent on government fiat for rising prices. They can change their minds at any time. The loans in question could get paid off.

And you can count on the world market to suddenly find new supplies whenever a commodity price doubles.

Remember the Rare Earths bubble where we were active players?

After a hyperbolic bubble, prices fell by 90%. Rare earth turned out to be not so rare. Only the cheap labor to extract them free of environmental regulation was.

So you can count on the current coal bubble to deflate eventually. The perfect storm is about to run in reverse.

That leaves us with the long-term fundamentals of coal which are bleak, to say the least.

China is far and away the world’s largest coal consumer at 49%, followed by the US at 11%. This is why China is also the world’s largest producer of greenhouse gases.

China is making every effort to reduce reliance on these cheapest form of energy, thanks to the blinding, choking smog alerts besetting its largest cities.

It is only still using coal because with an economy growing at 6.6% a year plus, it has to rely on every energy form just to keep the lights only. Power brownouts can lead to political instability.

Coal consumption in the US has been in a death spiral for years falling from 50% to 33% of electric power generation over the past decade.

That led to the bankruptcy of several of its largest players such as Arch Coal (ACI) and Peabody Energy (BTU).

The collapse of natural gas prices to $2/btu made a cleaner burning alternative cost-competitive. And gas lacks the nitrous and sulfur oxides and particulate pollution prevalent in coal.

Read the prospectus of any electric power companies and you will find them besieged by lawsuits from consumers claiming that the coal they burned caused their asthma and cancers. Utility companies would love to be rid of it.

And then there’s solar energy.

California governor Jerry Brown has signed the nation’s toughest climate legislation, mandating that all power come from alternative sources by 2030.

On several days this year, alternatives already accounted for 100% of the state’s total power production.

While ambitious, the target is viewed as doable. Solar energy, which now accounts for 5% of the state’s power output, will do the heavy lifting.

Many other states are expected to follow suit. No room for coal here.

The United Kingdom has already taken this path as have many other nations.

It says a lot that a country that ran a coal-based economy for 300 years announces the closing of its last mine which it did a few years ago. It will replace the power output with alternatives.

Having lived in England during the violent miner’s strikes during the early 1980s, it was quite a revelation.

So the writing is on the wall. Another major producer, Anglo American (NGLB.BE) sold two major mines in Australia.

Coal is clearly an energy source whose time has clearly come and gone. So, will the price of coal. The next recession, which may only be a year off, could well drive the entire industry into bankruptcy.

If true, the implications for your stock portfolio could be momentous. So why is the stock market REALLY going down?

The oil industry would far and away be the worst affected. That explains why big companies such as Exxon Mobile (XOM) are hitting new one-year lows, even though the price of Texas tea has risen by an impressive 50% since the summer.

Also taken out to the woodshed for a spanking have been steel and coal. It is fascinating to note that the shares of the supposed beneficiaries of the trade war, coal (KOL) and steel (X), have on average dropped twice as much as the victims, such as technology, since the correction began in February.

China buys some 70% of all US coal exports, which is why the principal US rail routes have shifted from going from North-South to East-West.

Tape readers believe it is a direct outcome of the tit-for-tat trade war with China. But given the small numbers out so far I believe this is being vastly overexaggerated by the media.

The $100 billion out of $1 trillion in two-way trade, generating a total of $25 billion in new tariffs between the two countries, is too small to even affect the GDP numbers.

Academics and Fed watchers argue that the infinitesimal rate of interest rate hikes by our central banks, six in three years, is finally starting to bite. It's just a matter of time before the frog realizes that it has been boiled.

Technology is the lead sector in the market, and it doesn't borrow AT ALL, accounting for 25% of market capitalization, funding growth entirely through cash flow.

In Washington there is a different view.

Plunging share indexes, bringing the biggest intraday swings seen in a decade, can only mean one thing. The Democrats may be about to retake Congress.

The Democrats only need to seize 24 seats in the House and two seats in the Senate to achieve a simple majority.

So far, some 38 House Republicans have announced they are not running for reelection. It's not because they are tired of exercising power. It's because they don't believe they can survive either a Democratic onslaught, or a primary challenge from the far right wing of their own party.

They also are facing the lowest presidential popularity ratings ever seen for a midterm election. Until a few weeks ago, Trump was scraping the basement with a 36% approval, also it has ticked up recently.

So if the Dems take control, what are the investment implications?

A president from one party and a congress from the other is a fairly common occurrence. That was the state of affairs during the past six years of the Obama administration, and the past two years of George Bush's.

In other words, it's a survivable situation.

It has long been said that markets love gridlocked government. At the end of the day, they wish Washington would go away so everyone can get on with the important business of making money.

For a start, a Democratic win would assure that no important legislation would be passed into law for two years.

But it goes beyond that. Majority control means that the Democrats would get control of the chairmanships of every committee. That means that the investigation of Trump's various actions would escalate from a slow burn to a full-fledged flash fire.

While this may occupy the headlines of newspapers, it will have minimal impact on the markets or the economy. Only the hard cases will even notice.

And now for a quickie civics lesson, which I understand they don't teach in high school anymore.

A Democratic win in the Senate would almost certainly bring an impeachment trial, where only a simple major majority of 51 is required. That would stall markets for about three months.

And no matter how rosy the prospects are for Democratic gains, they are unlikely to reach the two-thirds majority needed for an actual conviction.

For that the Dems would have to win 94 seats, a near impossibility in this heavily gerrymandered country. Just to get a simple majority in the House, the Democrats have to win 58% of the popular vote. But they could reach a tipping point.

In short, it's all looking like 1975 all over again. What happened after 1975? After collapsing 45%, then rallying from a Nixon resignation low of a Dow Average of 550 to 1,000, it then took EIGHT YEARS for stocks to rally another 1,000 points.

Wall Street shrank dramatically, and many brokers become taxi drivers. It's not a pleasant prospect, except that today they would become Uber drivers.

I remember it like it was yesterday.

The endless bear market was a major reason why I started my career as a financial journalist for The Economist magazine in London rather than heading straight for Wall Street.

Once the new bull market started in 1983, I was inside Morgan Stanley (MS) within a year, while it was still private.

And thanks to Bob Baldwin for the job, a Navy man and Ivy Leaguer who lived to 95!

If the election was held tomorrow, the Democrats would almost certainly get control. But the election is not tomorrow, it is in seven months, and in politics that could be seven lifetimes.

Polls could improve for Trump. But then they could get a whole lot worse, too. And then there is Robert Mueller constantly lurking at the periphery.

In the end, markets might not do much of anything in a gridlocked government.

Much of the prosperity of America has occurred independent of the goings on in the nation's capital. It has taken place in spite of, not because of government policies.

Technology companies, now 25% of the economy (it was 26% two weeks ago) will continue to push the envelope forward at a hyperaccelerating rate, creating trillions of dollars in new shareholder value.

Thank goodness for that!

However, the volatility to get to nothing could be extreme, as we now are witnessing.

Dow Average 1972-83

A reader emailed me yesterday to tell me that while visiting his daughter at a college in North Carolina, he refilled his rental car with gas for $1.39 a gallon.

So I got the idea that something really big is going on here that no one is yet seeing. I processed the possibilities in my snowshoe up to the 10,000-foot level above Lake Tahoe last night.

By the way, the view of the snow covered High Sierras under the moonlight was incredible.

For decades, I have dismissed the hopes of my environmentalist friends that alternatives will soon replace oil (USO) as our principal source of energy.

I have long agreed with the views of my fracking buddies in the Texas Barnett Shale that it will be decades before wind, solar, and biodiesel make any appreciable dent in our energy makeup.

It took 150 years to build our energy infrastructure, and you don?t replace that overnight. The current weakness in oil prices is a simple repeat of a predictable cycle that has continued for a century and a half. In a couple years, Texas tea will be posting triple digits once again.

I always thought that oil had one more super spike left in it. After that, it will fade into history, reduced to limited applications, like making plastics and asphalt, probably sometime in the 2030?s.

The price for a barrel of oil should then vaporize to $5.

But given the price action for energy and all other commodities I?m starting to wonder if this time I?m wrong.

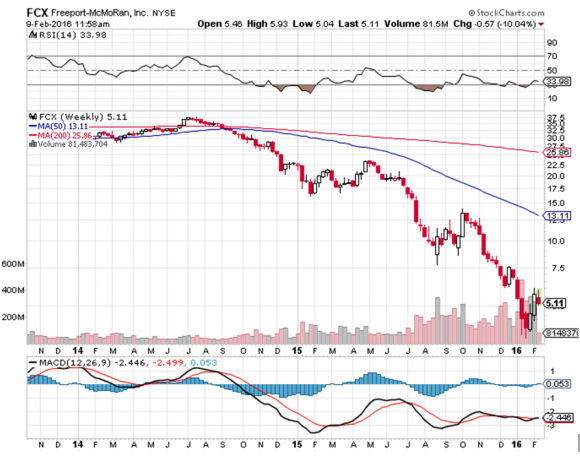

I have watched with utter amazement while Freeport McMoRan (FCX) plunged from $38 to $3. I was gob smacked to see Linn Energy (LINE), admittedly a leveraged play, crater from $32 to 30 cents.

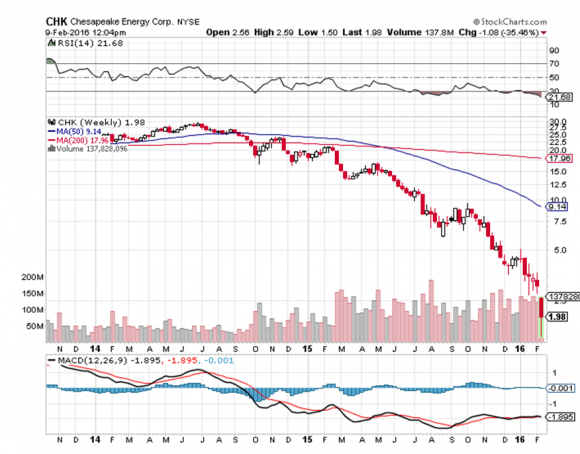

And I was totally befuddled to see gas major Chesapeake Energy (CHK) implode from $65 to $1.

Has the world gone mad?

When the data don?t match your view, it?s time to change your view.

Maybe there won?t be another spike in oil prices. Could its disappearance from the modern industrialized economy have already begun?

That would certainly explain a lot of the recent eye-popping price action in the markets. In five short years oil has dropped 82%. It did this while global GDP grew by 20% and auto sales, and therefore gasoline demand, has been booming.

Of course, you could just call all of this a big giant reversion to the mean.

Over the past 150 years, the average, inflation adjusted price of oil has been $35 a barrel. The price for gasoline has been $2.25 a gallon, exactly where it was in 1932, and where it now is in much of the country.

I know all of these numbers because I once did a study to see if oil prices are rigged (conclusion: they are). How can the price of a commodity stay the same for 150 years?

Wait, the naysayers announce. Things don?t happen that fast.

But they do, my friends, they do, especially in energy.

Until 1849, my ancestors were the largest producers of whale oil on Nantucket Island. (Our family name,? Coffin, was mentioned in ?Moby Dick? seven times, and was a focus of the just released film, ?In the Heart of the Sea.?)

Then this stuff called petroleum came along, wrested from the ground with new technology by men like Drake and Rockefeller. The whale oil market crashed, dropping in price by 90%, and virtually disappeared in two years.

My relatives were wiped out and moved to San Francisco, which they already knew from their whaling days, and where gold had just been found.

A half-century later, this thing called an ?automobile? came along meant to replace the ubiquitous horse and buggy. People laughed. It was loud, noisy, smelly, inefficient, and expensive. Only the rich could afford them.

You had to go to a drug store to buy high priced fuel in one-gallon tins. And it scared the horses. England passed a national automobile speed limit of 5 miles per hour, as cars were considered dangerous.

Then huge oil discoveries were made in Texas and California (watch ?There Will Be Blood?), the Hughes drill bit came along, and gasoline prices fell sharply. Suddenly cars were everywhere. The horse population declined from 100 million to only 1 million today.

All of this is a long-winded, history packed way of saving ?This time it may be different?.

I have on my desktop a Trade Alert already written up to buy the (USO) May, 2016 $9 calls. Today, they traded at $1.00. I?m just waiting for another melt down in oil to take a low risk punt on the long side.

If we rocket back up to $100, as many are predicting, these calls will be worth a fortune. But you know what, oil may only peak out at $44 this time. The trade will still make money, but not as much as in past cycles.

So, you better think hard about loading up on too many oil stocks at these distressed levels. Look what has already happened to the coal industry (KOL), which has essentially gone bankrupt.

You could well be buying into the buggy whip industry circa 1900.

If I warned them once, I warned them 1,000 times!

The Australian dollar (FXA) is going to fall.

That?s why I cautioned my Aussie friends to sell their homes, get the money the hell out of the country, and pay for their overseas vacations in advance.

As long as it is a de facto colony of China, the fortunes of the Land Down Under are completely tied to economic prospects there.

It is almost a waste of time looking at the Reserve Bank of Australia?s data releases. They have become a deep lagging, and really irrelevant indicators. You are better off going to the source, and that is in Beijing.

And therein lies the problem.

It is highly unlikely that the government in China has any idea what their economy is actually doing. Sure, they pump out the usual figures on a reliable basis like clockwork. These are educated guesses, at best.

Even in a perfect world, collecting numbers from 1.3 billion participants is a hopeless task. The US is unable to do these with any real accuracy, and we have one quarter of their population and vastly superior technology.

For what it is worth, Chinese President Xi Jinping has promised that his country?s GDP growth will not fall below a 6.5% annual rate for the next five years. At this pace, China is still creating more economic activity that any other country in the world.

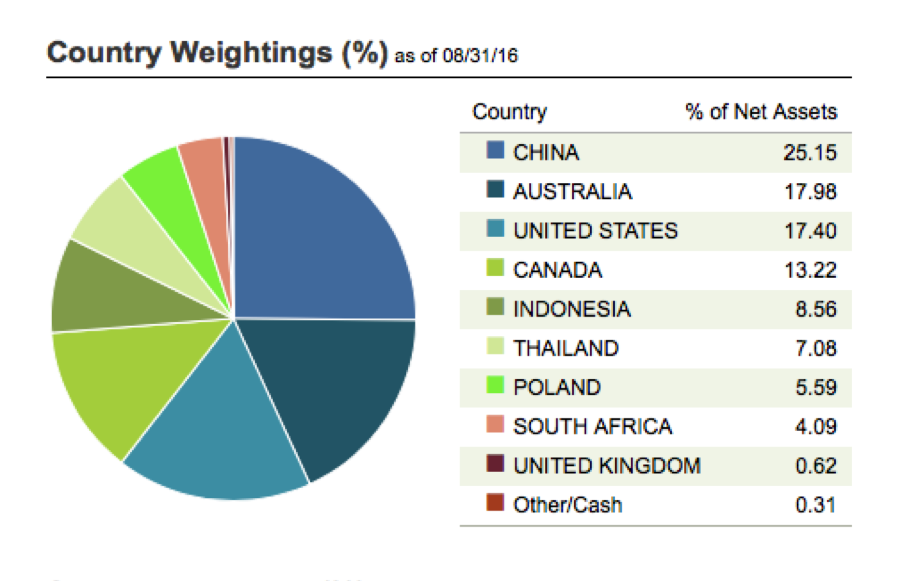

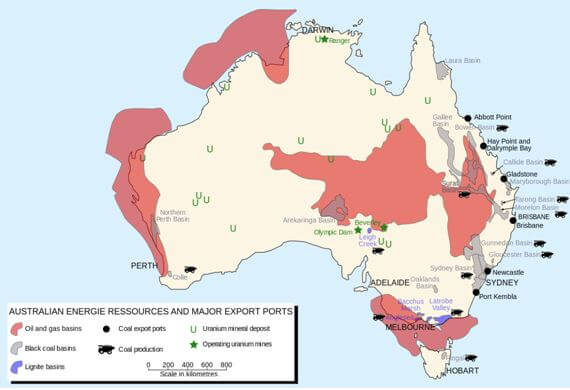

Which leaves us nothing else to rely on but commodity prices to look at, far an away Australia?s largest earner. These are suggesting that the worst has yet to come.

Virtually the entire asset class hit new six year lows yesterday. I had to go to the weekly charts to see how ugly things really are.

Australia?s largest exports are iron ore (26%, or $68.2 billion worth), coal (KOL) (16%), gold (GLD) (8.1%), and petroleum (USO) (5.7%). When the world?s largest consumer of these slows down, so does demand for these commodities.

BHP Billiton Ltd. (BHP), the largest producer of iron ore, has seen its shares plunge 57% from last year?s high.

But wait! It gets worse.

I have written at length about the transition of China from an industrial to a services based economy. You would expect this, as the Middle Kingdom has virtually no commodity resources of its own, but lots of smart people.

In a nutshell, they wish they had America?s economy. Where services now account for a staggering 68% of all economic activity.

This is why China?s future lies with Alibaba (BABA), Baidu (BIDU), and JD.com (JD). It does NOT lie with its steel factories and coalmines, which by the way, recently announced layoffs of 100,000, the largest in history.

To learn more about the structural remaking of China, please click here for ?End of the Commodities Super Cycle?.

There is one bright spot to mention. Australia is making a transition to a services based economy of its own. Tourism is rocketing, as is the influx of flight capital from the Middle Kingdom.

Walk the streets of Brisbane these days, and you are overwhelmed by the abundance of Asians coming here to learn English, attain a high education, or start a new business. When I came here 40 years ago, they were virtually absent.

How low is low?

It doesn?t help that the governor of the Reserve Bank of Australia, Australia?s central bank, Glenn Stevens, despises his nation?s currency.

He has used every rally this year to talk down the Aussie, threatening interest rate cuts and quantitative easing.

The hope is that a deep discount currency will allow the exporters to maintain some pricing edge on the commodities front.

The market chatter is that the Aussie will take a run as low as $0.55, the 2008-09 Great Recession low.

Whether we actually get that far or not is a coin toss.

And will even $0.55 below enough for Glenn Stevens?

So far in 2015 the Indian stock market has handily beaten that of the US, by 10.6% compared to 5.3%.

?The India election result is the biggest development to affect emerging markets over the last 30 years.? That is what retired chairman of Goldman Sachs Asset Management and originator of the ?BRIC? term, Jim O?Neal, told me last week.

Indeed, the stunning news has sent long term country specialists scampering. In my long term strategy lectures I have been titillating listeners for years with predictions that India was about to become the next China.

With half the per capita income of the Middle Kingdom, India was lacking the infrastructure needed to compete in the global marketplace. All that was needed was the trigger.

This is the trigger.

With a new party taking control of the government for the first time in 50 years, the way is now clear to carry out desperately needed sweeping political and economic reforms. At the top of the list is a clean sweep of corruption, long endemic to the subcontinent. I once spent four months traveling around India on the Indian railway system, and the demand for ?bakshish? was ever present.

A reviving and reborn India has massive implications for the global economy, which could see growth accelerate as much at 0.50% a year for the next 30 years. This will be great news for stocks everywhere. It will help offset flagging demand for commodities from China, like coal (KOL), iron ore (BHP), and the base metals (CU).

Demand for oil (USO) grows, as energy starved India is one of the world?s largest importers.

A strengthening Rupee, higher standards of living, and relaxed import duties should give a much needed boost for gold (GLD). India has always been the world?s largest buyer.

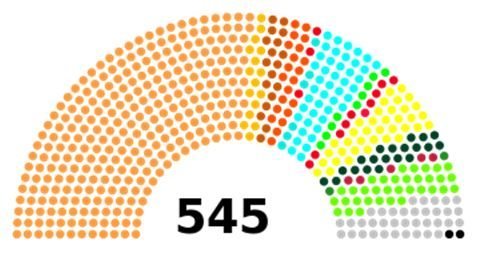

The world?s largest democracy certainly delivers the most unusual of elections, a blend of practices from today?.and a thousand years ago. It was carried out over five weeks, and a stunning 541 million voted, out of an eligible 815 million, a turnout of 66.4%. That is far higher than elections seen here in the United States.

Of the 552 members in the Lok Sabha, the lower house (or their House of Representatives), a specific number of seats are reserved for scheduled castes, scheduled tribes, and women. Gee, I wonder which one of these I would fit in?

Important issues during the campaign included rising prices, the economy, security, and infrastructure such as roads, electricity and water. About 14% of voters cited corruption as the main issue.

Some 12 political parties ran candidates. The winner was Hindu Nationalist Narendra Modi of the Bharatiya Janata Party (BJP), who led a diverse collection of lesser parties to take an overwhelming majority. For more details on this fascinating election, please click here at http://www.ndtv.com/elections.

It is still early days for the Bombay stock market, which has already rocketed by a stunning 20% since the election results became obvious last week.

This could be the beginning of a ten-bagger move over coming decades. Managers are hurriedly pawing through stacks of research on the subcontinent they have been ignoring for the past four years, the last time emerging markets peaked.

In the meantime, the action has spilled over into other emerging markets (EEM), their currencies (CEW), and their bonds (ELD), which have all punched through to new highs for the year.

I?ll be knocking out research o specific names when I find them. Until then, use any dip to pick up the Indian ETF?s (INP), (PIN), and (EPI).

After the market closes every night, I usually don a 60 pound backpack and climb the 2,000 foot mountain in my back yard.

To pass the time, I listen to audio books on financial and historical topics, about 200 a year (I?ve really got President Grover Cleveland nailed!). That?s if the howling packs of coyotes don?t bother me too much.

I also engage in mental calisthenics, engaging in complex mathematical calculations. How many grains of sand would you have to pile up to reach from the earth to the moon? How many matchsticks to circle the earth?

For last night?s exercise, I decided to quantify the impact of this year?s oil price crash on the global economy.

The world is currently consuming about 92 million barrels a day of Texas tea, or 33.6 billion barrels a year. In May, at the $107.50 high, that much oil cost $3.6 trillion. At today?s $53.60 low you could buy that quantity of oil for a bargain $1.8 trillion.

Buy a barrel of crude, and you get one for free!

This means that $1.8 trillion has suddenly been taken out of the pockets of oil producers, and put into the pockets of oil consumers. Over the medium term, this is fantastic news for oil consumers. But for the short term, things could get very scary.

$1.8 trillion is a lot of money. If you had that amount in hundred dollar bills, it would rise to 180 million inches, 15 million feet, or 2,840 miles, or 1.2% of the way to the moon (another mental exercise).

The global financial system cannot move this amount of money around on short notice without causing some pretty severe disruptions.

For a start, there is suddenly a lot less demand for dollars with which to buy oil. This has triggered short covering rallies in the long beleaguered Japanese Yen (FXY) and the Euro (FXE), which are just now backing off of long downtrends. The fundamentals for these currencies are still dire. But the short term trend now appears to be an upward one.

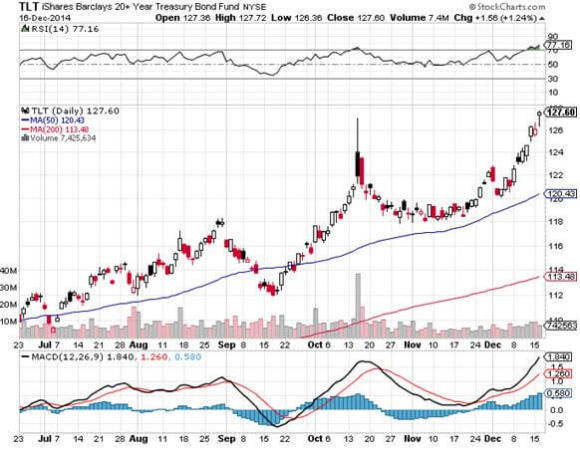

The US Federal Reserve certainly sees the oil crash as an enormously deflationary event. The use of energy is so widespread that it feeds into the cost of everything. That firmly takes the chance of any interest rate rise off the table for 2015. The Treasury bond market (TLT) has figured this out and launched on a monster rally.

Traders are also afraid that the disinflationary disease will spread, so they have been taking down the price of virtually all other hard commodities as well, like coal (KOL), iron ore (BHP), and copper (CU). For more depth on this, see yesterday?s piece on ?The End of the Commodity Super Cycle?.

The precipitous fall in energy investments everywhere will be felt principally in the 15 US states involved in energy production (Texas, Oklahoma, Louisiana, and North Dakota, etc.). So, the consumers in the other 35 states should be thrilled.

However, the plunge in energy stocks is getting so severe, that it is dragging down everything else with it. ALL shares are effectively oil shares right now. In fact, all asset classes are now moving tic for tic with the price of oil.

Throw on top of that the systemic risk presented by the ongoing collapse of the Russian economy. The Ruble has now fallen a staggering 70% in six months, and there is panic buying of everything going on in Moscow stores. The means that the dollar denominated debt owed by local firms has just risen by 70%. Any foreign banks holding this debt are now probably regretting ever watching the film, Dr. Zhivago.

Russian interest rates were just skyrocketed from 10.50% to 17%. The Russian stock market (RSX) is the world?s worst performing bourse this year. How do you spell ?depression? in the Cyrillic alphabet?

And guess what the new Russian currency is?

IPhone 6.0?s, of which Apple is now totally sold out in Alexander Putin?s domain!

Thankfully, this is more of a European than an American problem. But nobody likes systemic risks, especially going into illiquid yearend trading conditions. It?s a classic case of being careful what you wish for.

Of the $1.8 trillion today, about $430 billion is shifting between American pockets. That amounts to a hefty 2.5% of GDP.

Money spent on oil is burned. However, money spent by newly enriched consumers has a multiplier effect. Spend a dollar at Wal-Mart, and the company has to hire more workers, who then have more money to spend, and so on. So a shifting of funds of this magnitude will probably add 1% to U.S. economic growth next year.

Unfortunately, we will lose a piece of this from the obvious slowdown in housing. Deflation means that home prices will stagnate, or even fall. This is a major portion of the US economy which, for the most part, has been missing in action for most of this recovery.

Ultimately, cheap energy as far as the eye can see is a key element of my ?Golden Age? scenario for the 2020?s (click here for ?Get Ready for the Coming Golden Age? ).

But you may have to get there by riding a roller coaster first.

Oil at $53?

Oil at $53?