Mad Hedge Technology Letter

May 19, 2021

Fiat Lux

Featured Trade:

(THE CURRENT STATE OF U.S. ECOMMERCE)

(AMZN), (WMT), (KR), (COST)

Mad Hedge Technology Letter

May 19, 2021

Fiat Lux

Featured Trade:

(THE CURRENT STATE OF U.S. ECOMMERCE)

(AMZN), (WMT), (KR), (COST)

Was 2020 a one-hit-wonder for U.S. ecommerce sales?

Hardly so.

US retail ecommerce sales grew 33.6% in 2020, reaching $799.18 billion.

As the public health situation fizzles out, in-store shopping will refresh itself, and a share of consumer spending will revert away from retail and toward services like travel and live entertainment.

Consensus has it that U.S. ecommerce will grow 13.7% this year, reaching $908.73 billion, and although that would be a great year under normal circumstances, annualized growth of 13% appears pitiful compared to the pandemic numbers.

It was only at the beginning of 2020 that ecommerce was expected to grow 13.2% from 2019, but the health crisis ignited ecommerce sales to $799.18 billion.

Ecommerce growth from a much higher base is a hard endeavor as all the low-hanging fruit has been harvested and it’s just harder to push the needle higher.

What does this all mean?

Ecommerce represents a larger piece of the pie than ever before and that comes with greater influence.

I now expect ecommerce sales will account for 15.5% of the $5.856 trillion in total retail sales this year.

Ecommerce sales will surpass $1 trillion next year.

It also means that digital commerce has never been so strong in terms of a percentage growth basis, net total basis, and clout.

However, growth rates will need to moderate first before they can reaccelerate.

Looking at the financial year, look for sales to rise by a low single for the big-box retailer Walmart (WMT) showing that numbers are getting ahead of themselves.

Walmart is an accurate bellwether stock that gives us deep insight into the state of ecommerce, and they said it sees earnings rising by a high single-digit percent.

Guidance aside, Walmart had a great quarter.

Every segment performed well, and I am encouraged by traffic and grocery market share trends.

But customers clearly want to get out and shop which is why growth rates will most likely drop around 13% for ecommerce instead of staying north of 30%.

Walmart’s ecommerce continues to grow and stimulus in the U.S. had an outsized impact, and the second half has more uncertainty than a typical year because the reopening is a once-in-a-lifetime phenomenon and it’s hard to pinpoint the shake out.

Remember, there most likely will not be any broad-based stimulus payments in the 2nd half of 2021 and 2022 that will be rolled into Walmart ecommerce sales.

Walmart is clearly chasing the leader of the pack Amazon.

Amazon is on track to become the largest retailer in the United States within the next four years, followed by the aforementioned Walmart and Kroger.

Kroger has been a fashionable pick amongst hedge fund managers in the beginning of 2021.

Amazon (AMZN) gross merchandise value sales (GMV) will top $631.6 billion by 2025, representing a compound annual growth rate of 14% between 2020 and 2025.

The same report showed us that Walmart’s ecommerce sales are set to grow at a five-year CAGR of 14.9% from $43.6 billion in 2020 to $87.5 billion in 2025, accounting for 16.7% of total retailer sales in 2025.

Ecommerce is the only channel that will grow in the next 5 years, everything else, such as offline retail will contract or go sideways at best.

It’s a death by a thousand cuts type of dilemma for anyone that isn’t in ecommerce.

Costco (COST), the fourth largest U.S. retailer, is expected to invest heavily in its digital business, with its online sales set to increase by 47% over the same period, reaching $15.3bn in 2025.

Over the next few years, Generation Z will age into adulthood and bring with them a digital wallet and firms will need to focus investment online and engage with the digital ecosystem in order to win market share.

Gen Z doesn’t use cash.

Online grocery is set to stay even in healthy times, but the pace of growth for online grocery will level off after the 2020 explosion.

Fresh grocery ecommerce is still expected to grow at 13.3% CAGR between now and 2025 which is why you see many retailers like Walmart investing in the fresh foods’ delivery business.

Habits are hard to break and it’s clear that digital add-ons are here to stay, and brands must cultivate digital platforms to win.

Mad Hedge Technology Letter

April 12, 2021

Fiat Lux

Featured Trade:

(SHOULD I BUY THE BEYOND MEAT DIP?)

(BYND), (KR), (IMPOSSIBLE FOODS)

Beyond Meat (BYND) will most likely retrace back to $90 from its current share price of $130.

The pandemic was a nightmare for most food companies and for the ones that deliver products to restaurants, it was a catastrophe.

BYNDs net revenues of $101.9 million in the fourth quarter of 2020, an increase of 3.5% compared to the fourth quarter of 2019, were in line with expectations of atrocious numbers.

Growth companies are expected to grow 40% year over year each quarter and in a year where many tech companies experienced 5 years of digital transformation in 1, BYNDs performance was quite pitiful.

It could have been worse for BYND.

The loss they experienced in the food service channel was difficult, but sales were partly made up by growth in net revenues in the fourth quarter driven by a 7% increase in volumes sold largely aided by the retail (this is what they call eating BYND burgers at home) channel.

Q4 retail channel sales were up a full 85% year over year, which helped mitigate the 54% year-over-year decline in Foodservice.

The pandemic’s damaging effect was large on supplying places including amusement parks, sports arenas, academic institutions, hotels, corporate catering services, and others.

The 85% uptick in retail growth couldn’t compensate for the drop off in food service channels much like Uber and the Uber Eats conundrum.

Households continued to buy BYND products, and they bought them more frequently.

On average, they're spending more per household on non-meat products.

Another silver lining is in international retail, they saw a sequential acceleration of growth from Q3 to Q4.

International retail net revenues increased 139% year over year, driven mainly by distribution gains in Canada, including in the club stores, where they had no presence in the prior year.

As 2021 develops, we will see a flip in numbers as consumers start to visit their favorite eateries and are less inclined to grill BYND burgers on the patio grill.

This only injects more uncertainty into the numbers for BYNDs management and the headway they made in the retail channel could be mostly given back.

Naturally, BYND burgers just isn’t that software program that is essential, and the business of food tech is still fighting with the business of normal food like real meat such as cow-based beef and pig-based pork.

Many software programs simply do not have to duel with their analog selves which is why any sort of meaningful investments into a company like BYND is illogical.

Anyone who loves eating plant-based burgers should eat these protein-based burgers and leave the stock alone.

What’s on the horizon for BYND?

One word – competition.

Impossible Foods Inc. is planning to go public in the next year and is exploring either an initial public offering or a merger in a SPAC deal.

This would value the company at around $10 billion.

Once a hard-to-find item available at only expensive, trendy eateries, Impossible products are now on menus at national chains including Burger King.

Fast-food chains have fared significantly better than independent restaurants since the pandemic began, giving Impossible an added boost.

It has also been growing its grocery presence, cutting its suggested retail prices by 20% at U.S. grocery stores in February in its ongoing push to compete with real beef.

BYNDs management downplayed pandemic pressures to the business as “transitory”, but the problem with that is they are transiting right into fierce competition who have signaled willingness to enter into a price war against them.

Others like Kroger (KR) have bigger pockets and will have used the pandemic to plot their path against BYND.

Basically, what I am saying is that the first-mover advantage has disappeared forever, an unfortunate consequence for BYNDs future trajectory, and I don’t see a lot of upside to underlying shares in the short term.

In the short-medium term, Beyond Meat will first, need to rejuvenate their foodservice business and prove to investors that covid didn’t just knock it out.

Second, there is no guarantee that BYNDs food service will come back right away, this could be a hard slog for a few years to reach 2019 numbers and that’s still an if.

And third, they will need to prove they are better than Impossible Foods and the rest of them while most likely lowering the prices of their product.

Unluckily, the pandemic didn’t deliver 5 years of innovation in 1 year for BYND and there are more questions than answers moving forward.

Outside the internet, the presence of numerous physical inputs has the chance to go haywire which is why I sometimes believe the bore of buying Microsoft or Alphabet until death isn’t such a bad idea.

Investors might want to keep their tech investors from ever exposing themselves to real-world problems even if I think Uber is a great investment for 2021.

I would recommend investors to avoid this crowded space of food tech and let them cudgel each other down to zero. Whoever wins in the end might be worth a flier.

Mad Hedge Technology Letter

January 9, 2019

Fiat Lux

Featured Trade:

(TOP 8 TECH TRENDS OF 2018),

(GOOGL), (FB), (WMT), (SQ), (AMZN), (ROKU), (KR), (FDX), (UPS), (CRM), (TWLO), (ADBE), (PYPL)

As 2019 christens us with new technological trends, building our portfolio and lives around these themes will give us a leg up in battling the algorithms that have upped the ante in our drive to get ahead.

Now it’s time to chronicle some of these trends that will permeate through the tech universe.

Some are obvious, and some might as well be hidden treasures.

American consumers will start to notice that locations they frequent and the proximities around them will integrate more smart-tech.

The hoards of data that big tech possesses and the profiles they subsequently create on the American consumer will advance allowing the possibilities of more precise and useful products.

These products won’t just accumulate in a person’s home but in public areas, and business will jump at the chance to improve services if it means more revenue.

Amazon and Google have piled money into the smart home through the voice assistant initiatives and adoption has been breathtaking.

The next generation will provide even more variety to integrate into daily lives.

The gains in technology have given the consumer broader control over their lives.

The ability to practically manage one’s life from a remote location has remarkably improved leaps and bounds.

The deflation of mobile phone data costs, the advancement of high-speed broadband internet services in developing countries, more cloud-based software accessible from any internet entry point, and the development of affordable professional grade hardware have made life easy for the small business owners.

What a difference a few years make!

This has truly given a headache for traditional companies who have failed to evolve with the times such as television staples who rely on analog advertising revenue.

Millennials are more interested in flicking on their favorite YouTuber channel who broadcast from anywhere and aren’t locally based.

Another example is the quality of cameras and audio equipment that have risen to the point that anybody can become the next Justin Bieber.

Music executives are even using Spotify to target new talent to invest in.

Blockchain technology has the makings of transforming the world we live in.

And the currency based on the blockchain technology had a field day in the press and backyard summer barbecues all over the country.

Well, 2019 will finally put this topic on the backburner even though Bitcoin won’t disappear into irrelevancy, the pendulum will swing the other direction and this digital currency will become underhyped.

The rise to $20,000 and the catastrophic selloff down to $4,000 was a bubble popping in front of us.

It made a lot of people rich like the Winklevoss brothers Cameron and Tyler who took the $65 million from Facebook CEO Mark Zuckerberg and spun it into bitcoin before the euphoria mesmerized the American public.

On the way down from $20,000, retail investors were tearing their hair out but that is the type of volatility investors must subscribe to with assets that are far out on the risk curve.

The volatility that FinTech leader Square (SQ) and OTT Box streamer Roku (ROKU) have are nothing compared to the extreme volatility that digital currency investors must endure.

Video games classified as a spectator sport will expand up to 40% in 2019.

This phenomenon has already captivated the Asian continent and is coming stateside.

This is a bit out of my realm as standard spectator sports don’t appeal to me much at all, and watching others play video games for fun is something I am even further removed from.

But that’s what the youth like and how they grew up, and this trend shows no signs of stopping.

Industry experts believe that the U.S. is at an inflection point and adoption will accelerate.

Remember that kids don’t play physical sports anymore because of the risk to head trauma, blown ligaments, and the sheer distances involved traveling to and from venues turn participants away.

Franchise rights, advertising, and streaming contracts will energize revenue as a ballooning audience gravitates towards popular leagues, tapping into the fanbase for successful video game series such as Overwatch.

The rise of eSports can be attributed to not only kids not playing physical sports but also younger people watching less television and spending more time online.

Soon, there will be no difference in terms of pay and stature of pro athletes and video gaming athletes.

The amount of money being thrown at the world’s best gamers makes your spine tingle.

The era of digital data regulation is upon us and whacked a few companies like Google and Facebook in 2018.

Well, this is just the beginning.

The vacuum that once allowed tech companies to run riot is no more, and the government has big tech in their cross-hairs.

The A word will start to reverberate in social circles around the tech ecosphere – Antitrust.

At some point towards the end of 2019, some of these mammoth technology companies could face the mother of all regulation in dismantling their business model through an antitrust suit.

Companies such as Amazon and Facebook are praying to the heavens that this never comes to fruition, but the rhetoric about it will slowly increase in 2019 because of the mischievous ways these tech companies have behaved.

The unintended consequences in 2018 were too widespread and damaging to ignore anymore.

Antitrust lawsuits will creep closer in 2019 and this has spawned an all-out grab for the best lobbyists tech money can buy.

Tech lobbyists now amount to the most in volume historically and they certainly will be wielded in the best interest of Silicon Valley.

Watch this space.

The demand for smart consumer devices will fall off a cliff because most of the people who can afford a device already are reading my newsletter from it.

The stunting of smart device innovation has made the upgrade cycle duration longer and consumers feel no need to incrementally upgrade when they aren’t getting more bang for their buck.

The late-cycle nature of the economy that is losing momentum because of a trade war and higher interest rates will see companies look to add to efficiencies by upgrading software systems and processes.

This bodes well for companies such as Microsoft (MSFT), Salesforce (CRM), Twilio (TWLO), PayPal (PYPL), and Adobe (ADBE) in 2019.

This is where Amazon has gotten so good at efficiently moving goods from point A to point B that it is threatening to blow a hole in the logistic stalwarts of UPS and FedEx.

Robots that help deploy packages in the Amazon warehouses won’t just be an Amazon phenomenon forever.

Smaller businesses will be able to take advantage of more robotics as robotics will benefit from the tailwind of deflation making them affordable to smaller business owners.

Amazon’s ramp-up in logistics was a focal point in their purchase of overpriced grocer Whole Foods.

This was more of a bet on their ability to physically deliver well relative to competition than it was its ability to stock above average quality groceries.

If Whole Foods ever did fail, Amazon would be able to spin the prime real estate into a warehouse located in wealthy areas serving the same wealthy clientele.

Therefore, there is no downside short or long-term by buying Whole Foods. Amazon will be able to fine-tune their logistics strategy which they are piling a ton of innovation into.

Possible new logistical innovations include Amazon attempting to deliver to garages to avoid rampant theft.

This is all happening while Amazon pushes onto FedEx’s (FDX) and UPS’s (UPS) turf by building out their own fleet.

Innovative logistics is forcing other grocers to improve fast giving customers better grocery service and prices.

Kroger (KR) has heavily invested in a new British-based logistics warehouse system and Walmart (WMT) is fast changing into a tech play.

Current Chair of the Federal Reserve Jerome Powell unleashed a dragon when he boxed himself into a corner last year and had to announce a rate hike to preserve the integrity of the institution.

Markets whipsawed like a bull at a rodeo and investors lost their pants.

Tech companies who have been leading the economy and trot out robust EPS growth out of a whole swath of industries will experience further volatility as geopolitics and interest rate rhetoric grips the world.

Apple’s revenue warning did not help either and just wait until semiconductors start announcing disastrous earnings.

The short volatility industry crashed last February, and the unwinding of the Fed’s balance sheet mixed with the Chinese avoiding treasury purchases due to the trade war will insert even more volatility into the mix.

Powell attempted to readjust his message by claiming that the Fed “will be patient” and tech shares have had a monstrous rally capped off with Roku exploding over 30% after news of positive subscriber numbers and news of streaming content platform Hulu blowing past the 25 million subscriber mark.

Volatility is good for traders as it offers prime entry points and call spreads can be executed deeper in the money because of the heightened implied volatility.

Mad Hedge Technology Letter

November 21, 2018

Fiat Lux

Featured Trade:

(FIVE TECH STOCKS TO SELL SHORT ON THE NEXT RALLY)

(WDC), (SNAP), (STX), (APRN), (AMZN), (KR), (WMT), (MSFT), (ATVI), (GME), (TTWO), (EA), (INTC), (AMD), (FB), (BBY), (COST), (MU)

Next year is poised to be a trading year that will bring tech investors an added dimension with the inclusion of Uber and Lyft to the public markets.

It seemed that everything that could have happened in 2018 happened.

Now, it’s time to bring you five companies that I believe could face a weak 2019.

Every rally should be met with a fresh wave of selling and one of these companies even has a good chance of not being around in 2020.

Western Digital (WDC)

I have been bearish on this company from the beginning of the Mad Hedge Technology Letter and this legacy firm is littered with numerous problems.

Western Digital’s structural story is broken at best.

They are in the business of selling hard disk drive products.

These products store data and have been around for a long time. Sure the technology has gotten better, but that does not mean the technology is more useful now.

The underlying issue with their business model is that companies are moving data and operations into cloud-based products like the Microsoft (MSFT) Azure and Amazon Web Services.

Why need a bulky hard drive to store stuff on when a cloud seamlessly connects with all devices and offers access to add-on tools that can boost efficiency and performance?

It’s a no-brainer for most companies and the efficiency effects are ratcheted up for large companies that can cohesively marry up all branches of the company onto one cloud system.

Even worse, (WDC) also manufactures the NAND chips that are placed in the hard drives.

NAND prices have faltered dropping 15% of late. NAND is like the ugly stepsister of DRAM whose large margins and higher demand insulate DRAM players who are dominated by Micron (MU), Samsung, and SK Hynix.

EPS is decelerating at a faster speed and quarterly sales revenue has plateaued.

Add this all up and you can understand why shares have halved this year and this was mainly a positive year for tech shares.

If there is a downtown next year in the broader market, watch out below as this company is first on the chopping block as well as its competitor Seagate Technology (STX).

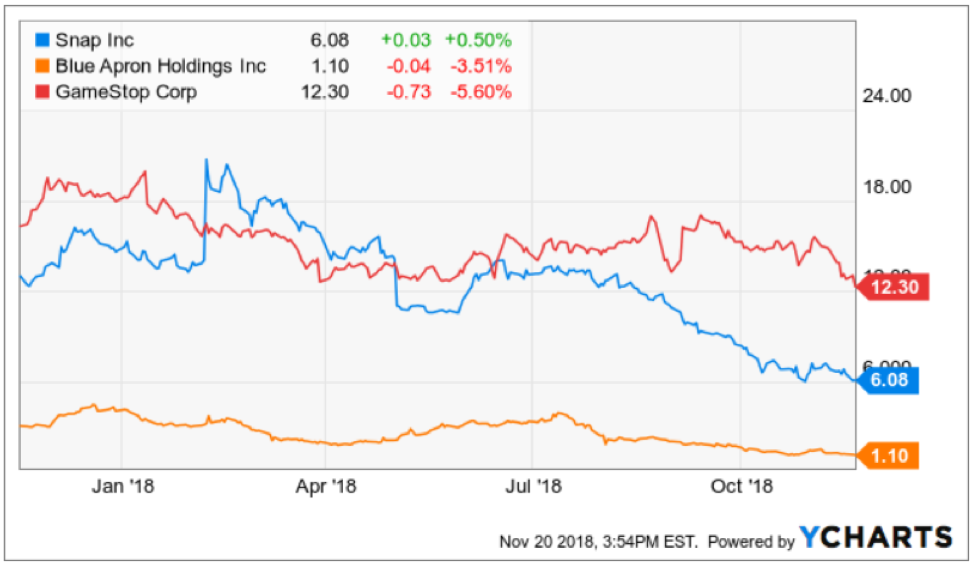

Snapchat (SNAP)

This company must be the tech king of terrible business models out there.

Snapchat is part of an industry the whole western world is attempting to burn down.

Social media has gone for cute and lovable to destroy at all cost. The murky data-collecting antics social media companies deploy have regulators eyeing these companies daily.

More successful and profitable firm Facebook (FB) completely misunderstood the seriousness of regulation by pigeonholing it as a public relation slip-up instead of a full-blown crisis threatening American democracy.

Snapchat is presiding over falling daily active user growth at such an early stage that usership doesn’t even pass 100 million DAUs.

Management also alienated the core user base of adolescent-aged users by botching the redesign that resulted in users bailing out of Snapchat.

Snapchat has been losing high-level executives in spades and fired a good chunk of their software development team tagging them as the scapegoat that messed up the redesign.

Even more imminent, Snapchat is burning cash and could face a cash crunch in the middle of next year.

They just announced a new spectacle product placing two frontal cameras on the glass frame. Smells like desperation and that is because this company needs a miracle to turn things around.

If they hit the lottery, Snap could have an uptick in its prospects.

GameStop (GME)

This part of technology is hot, benefiting from a generational shift to playing video games.

Video games are now seen as a full-blown cash cow industry attracting gaming leagues where professional players taking in annual salaries of over $1 million.

Gaming is not going away but the method of which gaming is consumed is changing.

Gamers no longer venture out to the typical suburban mall to visit the local video games store.

The mushrooming of broad-band accessibility has migrated all games to direct downloads from the game manufacturers or gaming consoles’ official site.

The middleman has effectively been cut out.

That middleman is GameStop who will need to reinvent itself from a video game broker to something that can accrue real value in the video game world.

The long-term story is still intact for gaming manufactures of Activision (ATVI), EA Sports (EA), and Take-Two Interactive (TTWO).

The trio produces the highest quality American video games and has a broad portfolio of games that your kids know about.

GameStop’s annual revenue has been stagnant for the past four years.

It seems GameStop can’t find a way to boost its $9 billion of annual revenue and have been stuck on this number since 2015.

If you do wish to compare GameStop to a competitor, then they are up against Best Buy (BBY) which is a better and more efficiently run company.

Then if you have a yearning to buy video games from Best Buy, then you should ask yourself, why not just buy it from Amazon with 2-day free shipping as a prime member.

The silver lining of this business is that they have a nice niche collectibles division that hopes to deliver over $1 billion in annual sales next year growing at a 25% YOY clip.

But investors need to remember that this is mainly a trade-in used video game company.

Ultimately, the future looks bleak for GameStop in an era where the middleman has a direct path to the graveyard, and they have failed to digitize in an industry where digitization is at the forefront.

Blue Apron

This might be the company that is in most trouble on the list.

Active customers have fallen off a cliff declining by 25% so far in 2018.

Its third quarter earnings were nothing short of dreadful with revenue cratering 28% YOY to $150.6 million, missing estimates by $7 million.

The core business is disappearing like a Houdini act.

Revenue has been decelerating and the shrinking customer base is making the scope of the problem worse for management.

At first, Blue Apron basked in the glory of a first mover advantage and business was operating briskly.

But the lack of barriers to entry really hit the company between the eyes when Amazon (AMZN), Walmart (WMT), and Kroger (KR) rolled out their own version of the innovative meal kit.

Blue Apron recently announced it would lay off 4% of its workforce and its collaboration with big-box retailer Costco (COST) has been shelved indefinitely before the holiday season.

CFO of Blue Apron Tim Bensley forecasts that customers will continue to drop like flies in 2019.

The company has chosen to focus on higher-spending customers, meaning their total addressable market has been slashed and 2019 is shaping up to be a huge loss-making year for the company.

The change, in fact, has flustered investors and is a great explanation of why this stock is trading at $1.

The silver lining is that this stock can hardly trade any lower, but they have a mountain to climb along with strategic imperatives that must be immediately addressed as they descend into an existential crisis.

Intel (INTC)

This company is the best of the five so I am saving it for last.

Intel has fallen behind unable to keep up with upstart Advanced Micro Devices (AMD) led by stellar CEO Dr. Lisa Su.

Advanced Micro Devices is planning to launch a 7-nanometer CPU in the summer while Intel plans to roll out its next-generation 10-nanometer CPUs in early 2020.

The gulf is widening between the two with Advanced Micro Devices with the better technology.

As the new year inches closer, Intel will have a tough time beating last year's comps, and investors will need to reset expectations.

This year has really been a story of missteps for the chip titan.

Intel dealt with the specter security vulnerability that gave hackers access to private data but later fixed it.

Executive management problems haven’t helped at all.

Former CEO of Intel Brian Krzanich was fired soon after having an inappropriate relationship with an employee.

The company has been mired in R&D delays and engineering problems.

Dragging its feet could cause nightmares for its chip development for the long haul as they have lost significant market share to Advanced Micro Devices.

Then there is the general overhang of the trade war and Intel is one of the biggest earners on mainland China.

The tariff risk could hit the stock hard if the two sides get nasty with each other.

Then consider the chip sector is headed for a cyclical downturn which could dent the demand for Intel chip products.

The risks to this stock are endless and even though Intel registered a good earnings report last out, 2019 is set up with landmines galore.

If this stock treads water in 2019, I would call that a victory.

Amazon’s reign doesn’t touch everything – there are still nooks and crannies of the business world it still doesn’t dominate.

Hard to believe, right?

As Amazon (AMZN) branches off into every known and unknown crevice of the economy to excavate fresh growth drivers, it’s hard to fathom where they won’t be in the future.

Supermarkets are one of the most innovative parts of technology right now, and even with Amazon’s grocery prize of Whole Foods, they are yet to rule over a broad-based grocer empire.

It might behoove you to discover that Kroger (KR) is on the brink of constructing a high-tech, cutting edge supermarket business that could juice up their crusade against Amazon.

In May, Kroger decided on partnering up with British-based online grocer Ocado (LON: OCDO) to build out a full-fledged, automated warehouse acting as the launching pad to their high-tech supermarket aspirations.

Kroger just announced they will identify 3 of the 20 new warehouse sites by the end of 2018 and the search is “making good progress.” These three warehouses should be functional within a year.

This is the best investment Kroger has ever made in the history of the company.

The deal also gave Kroger a 5% stake in Ocado which has no brick and mortar stores.

Even more brilliant, the deal bans Ocado from selling the technology to other American competitors.

Ocado has been voted the best online U.K. grocer by Consumers' Association magazine Which? every year since 2010.

The company went public on the London Stock Exchange in 2010 and its share price has had a banner year.

Shares were trading at £245 just 11 months ago.

The stock has been a battleground company with massive short interest because a contingent of investors believe this is just a simple grocer company.

Some investors value Ocado as a high-tech company and it is obvious which group has won out as this online grocer saw shares catapult to a tad below £1200 only to slightly retrace and consolidate.

Ocado shares are still hovering around £900 giving credence to this high-tech grocer amidst a country that is bereft of technology companies.

Softbank’s buy of Arm Holdings was the crown jewel of British tech companies to be pocketed and taken off the public markets.

Imagination Technologies was also a blockbuster name that went private after Apple infamously announced it would stop incorporating Imagination Technologies’ system-on-a-chip accounting for over half of total revenue.

Shares cratered by 70% and the company was picked up on the cheap like hawks swooping on prey by private equity fund Canyon Bridge, who is backed by the Chinese communist government.

Ocado is the torch bearer for Britain now and the smorgasbord of deals signed with France, Sweden, Canada and America indicate their intent to be a major tech player.

The breathtaking short-squeeze has put bears on alert shying away from their oversized sell button as they have been epically burnt on this trade.

This love them or hate them online grocer plans to license out its industry leading proprietary technology to revolutionize legacy supermarkets such as Kroger.

The stellar performance by Amazon has fueled its competition’s ambition to up its game in any way possible, boding well for the consumer who will benefit from better services and lower prices.

Ocado’s 20 automated warehouses dotted around America will take three years to complete.

Simply put, Ocado is best in show at building these supermarket automated warehouses and could receive a windfall of revenue around the world as grocers from all corners of the world revolutionize logistical processes.

Of the 260,000 orders they receive per week in Britain, error rates have plummeted to a subterranean level of less than 1%.

The whole process is closely monitored by algorithms, scanning, identifying and optimizing each step of the process.

Ocado’s algorithms are quite masterful – they have been programmed to even sort a bag of groceries so the eggs aren’t squashed at the bottom of the order by a sack of potatoes.

The insides are placed for perfection like the interior of Château de Malmaison straddling the suburbs of Paris, France.

These ideally placed items can travel up to 20 miles in Ocado’s boxes.

This might be fine for a land-challenged country like Britain, but distances are grotesquely larger in America, and making sure perishables arrive fit as a fiddle offers complexities to Ocado’s engineering team.

To root out any bugs, Ocado’s phalanx of engineers create digital clones of a functional warehouse mimicking the location-specific conditions and operations to eradicate any faulty processes that crop up.

This has allowed Ocado to refine different models adding to the team’s scope of versatility.

Each set of geographies will present unique challenges and adapting to local needs of each grocer will be a key to harness profitability.

Ultimately, Ocado is not new to this – they have been cultivating this type of technology for 15 years.

Drench Ocado’s model with more technology and it has become faster, more efficient, and systematically accurate.

Humans have been shipped out in favor of a bagging robot that separates out the orders needing to be placed in certain crates.

Humans are redeployed up the value chain of work and retrained as management delegates the lower grade tasks to be taken over by machines.

Ocado’s delivery vehicles are tricked out with telemetry systems, an automated communications process by which measurements and other data are collected remotely in order to ameliorate the delivery time schedules.

Betting the ranch on enhancing the technology, Ocado has rolled out a freshly designed robot that can stack and sort boxes in stacks of up to 21 boxes high.

And here is the kicker – the artificially intelligence-based technology has outsized cross-over effect applicable to a myriad of industries that require warehouses as a main input in an operation which could spawn massive layers of potential profits.

The deep commitment to innovation is costly and investors will always be anxious about the margin story, but that should not be reason to jump ship.

There is no seat at the table if a company is not armed and wielding the best technology current engineering can create.

Top-class engineers aren’t cheap, and like their brethren in Silicon Valley, engineers continue to be tech firm’s largest cost but their best asset.

Machine learning is also deployed across the customer service support platforms to ensure any complaints do not repeat.

Eventually, Ocado hopes to automate everything and once self-driving technologies become customary, they will do away with the human driver too.

They have already carried out tests showing their capabilities of functioning with this technology and did a stint of 2 weeks with little problem.

This May was the first time Ocado netted a nations big fish supermarket business with 1,300-store strong ICA Sweden.

ICA has carved out Swedish market share approaching a third.

Ocado is capitalizing on the new sense of urgency from legacy supermarkets to pivot towards technology to bolster profits.

Online supermarkets were once discarded but now seek to seize 15% of the grocery market share on the way to 20%.

Assuming that 10% is the peak is wrong especially with Ocado’s supermarket warehouse technology.

Most recently, Instacart partnered with German discount supermarket Aldi to offer delivery service.

Ocado has absolutely started to spread its wings by licensing its robot-laden supermarket warehouse technology and this is just the beginning.

More deals will be in the pipeline and consumers will much rather shop for groceries online now.

To admire the scope of Ocado’s pioneering expertise, this is their revolutionary warehouse system controlled by air traffic control technology with R2-D2-like robots careening around on a grid set-up fulfilling orders – click here to watch the video.

Mad Hedge Technology Letter

October 2, 2018

Fiat Lux

Featured Trade:

(TAKE A LOOK AT ENGLAND’S AMAZON),

(LON: OCDO), (KR), (AMZN)

(WE'RE MAKING SOME CHANGES HERE AT THE MAD HEDGE FUND TRADER)