Mad Hedge Technology Letter

December 6, 2019

Fiat Lux

Featured Trade:

(AUGMENTED REALITY IS HEATING UP),

(AAPL), (LITE), (QCOM), (NVDA), (ADSK), (FB), (MSFT), (SNAP)

Mad Hedge Technology Letter

December 6, 2019

Fiat Lux

Featured Trade:

(AUGMENTED REALITY IS HEATING UP),

(AAPL), (LITE), (QCOM), (NVDA), (ADSK), (FB), (MSFT), (SNAP)

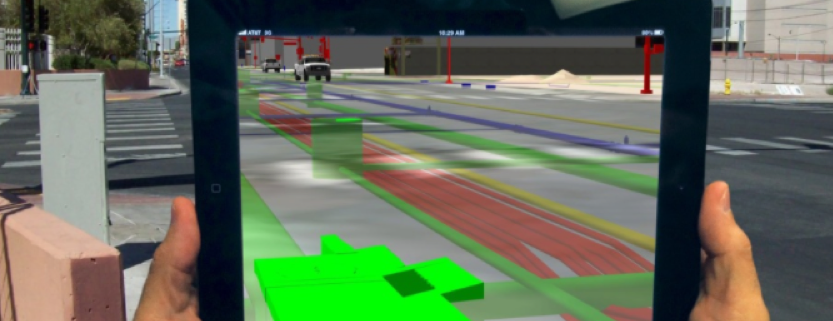

First, what is augmented reality for all the newbies?

Augmented reality is an interactive experience of a real-world environment where the objects that reside in the real world are enhanced by computer-generated perceptual information, sometimes across multiple sensory modalities.

Augmented reality (AR) went rival in 2016 when the Pokemon Go mania captivated everyone from children to adults.

No sooner than 2021, the AR addressable market is poised to mushroom to $83 billion - a sizeable increase from the $350 million in 2018.

Much like machine learning, corporations are learning to marry up this technology with their existing products supercharging the performance.

Ulta Beauty, for example, has acquired AR and artificial intelligence start-ups to help customers digitally test the final appearance of makeup before users purchase the product.

That is just one micro example of what can and will be achieved.

Looking deeper into the guts, Qualcomm (QCOM) is hellbent on making their chips a critical part of the puzzle.

The company is better known for a telecom and a semiconductor play, not often lumped in with a list of AR stocks.

Qualcomm is strategically positioned to capitalize on the integration of augmented reality in mainstream corporate business embedding their chips into the devices.

Maximizing Qualcomm’s future role in the industry, the company announced in 2018 that it would be developing a chipset specifically for AR and VR applications.

This broad-based solution will make it easier for other developers to bring new glasses to the marketplace.

Autodesk (ADSK) is one of my favorite software stocks and a best of breed of industry design.

They sell 3D rendering software to designers and creators by offering a platform in which they can transform 2D designs into digital models that are both interactive and immersive, creating compelling experiences for end-users.

Autodesk has an array of powerful software suites to augment virtually any application, such as 3ds Max, a 3D modeling program; Maya LT game development software; its automotive modeling program VRED; and Forge, a development platform for cloud-based design.

Facebook (FB) has been piling capital into AR for years.

CEO Mark Zuckerberg wants to create an alternative profit-driver and is desperate to wean his brainchild from the digital ad circus.

One example is Facebook’s Portal TV and its Spark AR which is the platform responsible for mobile augmented reality experiences on Facebook, Messenger, and Instagram.

It supplies the virtual effects for consumers to play around with, but it is yet to be seen if consumers gravitate towards this product.

Lumentum (LITE) is the leader in 3D-sensing markets developing cloud and 5G wireless network deployments.

They manufacture 3D sensor lasers that can be used with smartphones to turn handsets into a sort of radar. Sensors are clearly a huge input in how AR functions along with the chips.

CEO of Apple (AAPL) Tim Cook put it best when he earlier said, “I do think that a significant portion of the population of developed countries, and eventually all countries, will have AR experiences every day, almost like eating three meals a day, it will become that much a part of you.”

He said that in 2016 and AR has yet to mushroom into the game-changing sector initially thought partly because the roll-out of 5G is taking longer than first expected.

Apple consumers will need to then adopt a 5G device or phone to really get the AR party started and that won’t happen until the backend of next year.

My initial channel checks hint that the Cupertino firm is planning a 5.4-inch model, two 6.1-inch devices, and one 6.7-inch phone, all of which will support 5G connectivity.

I surmise that Apple’s two premium devices will feature “world-facing” 3D sensing, a technology that could help Apple boost its augmented-reality capabilities and support other feature improvements on its priciest devices.

Apple has had a big hand in Lumentum's growth and will continue to buy their sensors, but other key component suppliers will get contracts such as Finisar, a manufacturer of optical communication components and subsystems.

Apple planned to debut AR glasses by 2020, but the rollout is now delayed until 2022.

They are clearly on the back foot with Microsoft (MSFT) further along in the process.

Microsoft already has a second iteration of its AR headset, HoloLens, and is compatible with several apps and has integration with Azure as well.

The head start of 2 years could really make a meaningful impact and might be hard for Apple to recover.

Facebook isn’t the only social media company going full steam into AR, Snap (SNAP) recently unveiled its newest spectacles, which feature AR elements.

Another application of AR is autonomous driving with Nvidia working on improving the driving experience by fusing AR with artificial intelligence.

Nvidia (NVDA) is already thinking about the next generation of AR technologies with varifocal displays, which improve the clarity of an object for a user.

It will take time to transform our relationship with AR, the infrastructure is still getting built out and many people just don’t have a device that will allow us to tap into the technology.

Investors must know that AR-related stocks will start to appreciate from the anticipation of full sale adoption and there could be a killer app that forces the mainstream user to take notice.

Until then, companies jockey for position and hope to be the ones that take the lion’s share of the revenue once the technology goes into overdrive.

Mad Hedge Technology Letter

December 20, 2018

Fiat Lux

Featured Trade:

(MICRON TECHNOLOGY BOMBS AGAIN)

(MU), (FDX), (UPS), (AAPL), (QRVO), (SWKS), (NXPI), (CRUS), (LITE),

If there was ever a canary in the coal mine, we got one with chipmaker Micron (MU) delivering weak earnings results missing on the top line but squeaking through a one-cent beat on the bottom line.

Love them or hate them, chip companies are susceptible to the boom-bust cycle that is a hallmark of the chip industry.

The beginning of the bust stage of the cycle is upon us with management detailing an “inventory adjustment” that put a damper on revenue.

Micron followed that up by reducing capex for next year and it will take 2-3 quarters to work off this bloated inventory channel.

The perpetrator to the inventory backlog is the smartphone industry.

President and CEO of Micron Sanjay Mehrotra particularly noted “high-end smartphones” as the malefactor tugging down the demand.

This is another damming testament to the prospects of Apple’s (AAPL) suppliers Quorvo (QRVO), Skyworks Solutions (SWKS), NXP Semiconductors (NXPI), Cirrus Logic (CRUS), and Lumentum Holdings (LITE) who can’t catch a break.

The last six months have fired a barrage of poison-tipped arrows at their core business and these stocks are squarely in the no-fly zone until Apple and the trade war can conjure up some good news.

To say these shares are oversold is an understatement, but we are in an extreme trading environment with volatility shooting up the wazoo.

Further reducing the glimmer, Chinese tariffs took up a worrying amount of the conference call dialogue. Investors found out that tariffs pinged half a percent of gross margins.

I have been outright bearish the chip industry from the middle part of the year and Micron is heavily reliant on China for about half of its revenues which is a death sentence in December 2018.

As the China risks have spiked after each head fake détente, so have the execution risks to chip companies with an overly reliant manufacturing process in China.

Not only has the execution risk ratcheted up, but the regulatory risk through costly tariffs is now eroding Micron’s margins.

If you thought that was a downer, then FedEx (FDX) made sure the nail was in the coffin by its ghastly earnings report.

The stock sold off hard confirming fears that global growth is decelerating.

Management did not mince their words about the state of the world and investors usually listen because FedEx is a reliable yardstick of the bigger global economy.

CEO of FedEx Fred Smith offered an olive branch painting a picture of a “solid” US economy, but the conundrum is that the US economy and any other country don't exist in a vacuum and that has been highly evident in Britain who is engaging in economic suicide by disengaging from the globalized world.

Smith cited Europe as a stumbling block and blamed the bulk of weak guidance on “bad political choices”, a thinly veiled dig at the poor level of governance carried out around the world lately.

I might chime in that it is quite strange when political parties and sovereign nations adopt the game of chicken as the leading political strategy applying it to everything and anything.

The side effects to business have been startling with management unable to assuage investor sentiment and business plans shredded apart because of impulsive policy moves.

Politicians aren’t grasping fully that stock market moves are inherently tied to the news cycle and the overwhelming volume of bad news that shouldn’t be as bad as it should be, has a multiplier effect on the stock market algos that go haywire.

It truly is the world of the algos and humans are living in their world and not the other way around.

The most important takeaway from FedEx is what they didn’t say.

Early development of the de-facto Amazon Airlines has already cost FedEx up to 3% of total volume growth.

And this is just the beginning.

Amazon is still feeling around for the rocks at the bottom while it tries to cross the river.

Once it masters logistics, expect a radical swivel towards the integration of their own airline into the bulk of Amazon.com’s package deliveries.

And when FedEx’s management claims that the market has gotten it wrong about the Amazon threat, that means the market is completely correct.

The market is always right.

Amazon’s master plan is to vertically integrate every last process down to the last mile, the doorbell, and now the microwave as Amazon has rolled out a myriad of smart home products.

FedEx management has to be blind to understand this won’t damage future sales.

It is materially false if FedEx thinks Amazon is not competing with them, and the sad part of this is there is not much FedEx can do about it.

The shipping giant cut its 2019 earnings forecast between $15.50 and $16.60 per share — from $17.20 to $17.80 a share.

FedEx’s goal of eclipsing $1.5 billion in operating income by fiscal 2020 has been shelved disappointing investors. FedEx cratered 12% on a day that saw the Fed do its best body slam imitation on the market.

The first phase of the logistics swivel is taking delivery of 40 planes and constructing a hub that will be able to operate 100 planes, then it will do as Amazon does with everything – scale it to the hills.

FedEx and UPS have a few years to figure out how to counteract this existential crisis and not decades.

Technology moves that fast now in this interconnected world.

Domestic volume comprises 17% of revenues at UPS and 19% at FedEx, management won’t be able to hide this problem under the carpet as the drag becomes highly visible like a sore thumb.

Analysts expect Amazon Air to offer more than slim savings to its business model saving between $2 to $4 per package next year.

The annual savings add up from $1 billion to $2 billion or 3% to 6% of its global shipping costs.

It is spot-on to admit that over the last few years, the explosion of packages during the holiday shopping season has put higher levels of stress on the U.S. Postal Service, UPS (UPS), and FedEx.

Even though overloaded with business, all three carriers have posted record levels of on-time deliveries and they appear to be handling the surge in volume.

But there will come a moment in time when an inflection point will give Amazon the keys to the car.

They will suddenly stop offering their e-commerce packages to these three carriers and business will drop off a cliff for them.

That is the future these three are confronted with and there is nothing they can do unless they build their own Amazon.com which is a pie in the sky dream at this point.

Amazon is out to prove they can execute the logistic part of their business cheaper and faster than anyone else because of the superior management and mountain of data they can act on.

I believe it will happen.

Part of stretching themselves with a new army of minions in Washington D.C., New York, and Nashville is partly about fulfilling the job of comprehensively and vertically integrating their e-commerce platform.

It will take a horde of workers to make this happen.

If the prophecy from FedEx management comes true and the global economy indeed softens next year, the stock will bear the brunt of the downside momentum and UPS too.

Stay away from the trio of deliverers. There are healthier fishes in the sea.

And as for the chip sector and Apple, wait on the sidelines for some good news.

Mad Hedge Technology Letter

November 13, 2018

Fiat Lux

Featured Trade:

(NO BIWEEKLY STRATEGY WEBINAR FOR WEDNESDAY NOVEMBER 14)

(WHY I HATE CHIP STOCKS)

(AAPL), (CY), (TXN), (LRCX), (KLAC), (LITE), (QCOM), (MU), (SWKS), (LSCC)

Now that the midterm elections are behind us, Congress will be gridlocked for the next two years portending well for tech stocks as a whole.

However, the gridlock will exacerbate negative sentiment in one small group of technology – the semiconductor chip sector.

I have been staunchly bearish on this cohort since the outset of the trade logjam with China and I recommend readers to avoid these stocks like the plague.

The split Congress could fuel an even more rigid stance towards the complicated tech situation, further clamping down on foreign IP theft and technological forced transfers.

Either way, there is no end in sight and as this administration is concretely in place for the next two years, doubling down on foreign policy wins could be the Republican party’s path to victory heading into the 2020 election.

This could mean the rhetoric towards China could ratchet up a few levels.

Soon enough, the tariffs levied on Chinese imports is set to increase to 25% in January.

Even before January, a planned meeting between Trump and Chairman Xi in Buenos Aires on Nov. 29 will take place and is creating a swirling tornado of uncertainty around chip sentiment that is on tenterhooks.

Any chance to resuscitate the sentiment in the industry could come and go with another gut-churning leg down in chip shares.

Unfortunately, the sword of Damocles hanging over the chip sector could drop in 2019 slashing profit margins, revenue, and damaging the all-important guidance.

Even if individual chip companies determine that the trade friction is too much to stomach, it would be expensive and lengthy to transfer an entire supply chain to Vietnam or Indonesia, hitting current R&D budgets and damaging future innovation affecting the pipeline of fresh products.

Time is not a friend to the chip sector.

If the China leveraged chip companies were to wait out this trade war, they risk further being enveloped into the eye of the trade storm if no quick agreements can be made.

They might have to wait a while as Beijing views waiting out Trump and dealing with the next administration in charge as the ideal option.

Chairman Xi conveniently removed term limits in the last congress, meaning he is in his job until death which could be another 40 years or so.

That is the time horizon the Chinese are playing with.

The timing couldn’t have been worse for the chip sector after a slew of weak guidance from upper management painted a downbeat picture for the sector as we inch towards 2019.

Texas Instruments (TXN) Chief Executive Rich Templeton started off his earnings report admitting, “demand for our products slowed across most markets.”

He later admitted that the semiconductor market is grappling with an imminent “softer” market.

Following up a growing chorus of chip executives flashing dangerous warnings signs, Lattice Semiconductors (LSCC) lamented that it was seeing slowness in the industrial and consumer markets in Asia as a result of macroeconomic conditions and tariffs.

Cypress Semiconductor (CY) also chimed in saying it was coping with “softness across the board.”

Making matters worse, Beijing has been showering capital on the local chip sector aimed at nurturing and developing Chinese chip companies poised to compete on the global stage.

Recently, Chinese state-backed semiconductor maker Fujian Jinhua Integrated Circuit was indicted by the U.S. Justice Department for industrial espionage.

The company allegedly stole trade secrets from Boise-based Micron (MU).

Micron could now become the first piece of collateral damage to the snarky trade war threatening huge swaths of American chip company's revenue.

And with the affected American chip companies waded in a quagmire, and chip market softness on the near horizon, semiconductor equipment firms have borne a good amount of the damage this year with Applied Materials Inc (AMAT), KLA-Tencor Corp (KLAC), and Lam Research Corp (LRCX) getting hammered.

Chips tied to Apple’s (AAPL) iPhone are also in for a drubbing with Apple suddenly announcing in their most recent report they would stop offering the unit sales of iPhones, creating more uncertainty around units sold for a massive end-market for global chip companies, adding to the swirling uncertainties overall Chinese chip revenue face.

Apple proxy chip stocks who lean on Apple for a big chunk of revenue such as Skyworks Solutions (SWKS) are getting crushed.

Skyworks was downgraded last week by Citigroup based on underperforming iPhone XR sales.

The rapid rush of chip downgrades has been fast and furious.

Skyworks will have pockets of strength when 5G is fully rolled out because they will supply critical components installed in this new technology for the new era of internet speed and performance.

But that pocket of strength is not now and will not happen tomorrow.

It’s time to duck out of Skyworks and I have been convincingly downbeat on this particular name since the inception of the trade war.

Today crawled in the next batch up negative chip news from Lumentum Holdings (LITE) who supplies 3D chips for Apple iPhone's facial recognition system.

Management reported that sales would be $20 million lower than originally forecasted because of a sudden reduction in shipments from an unnamed customer.

Another ongoing headache is the Qualcomm (QCOM) versus Apple marriage or divorce, depending on how you look at it.

They have been mired in a prolonged court case against each other, and Qualcomm’s share price has been dismal as of late.

Qualcomm recorded zero licensing revenue in the quarter from Apple who is withholding royalty payments from Qualcomm in a dispute over the company's licensing practices.

The move damaged quarterly licensing sales sliding 6% to $1.14 billion.

Qualcomm has lashed back at Apple pointing the finger at Apple for transferring its intellectual property to Intel (INTC) who is supplying chips for new-model iPhones which is possibly part of the reason they lost this contract.

Losing the iPhone contract to Intel is the main factor in Qualcomm expecting modem chip shipments to decline 22% to about 185 million units.

The fight has no end in sight but like Skyworks Solution, Qualcomm is on the forefront of the 5G revolution and provides a silver lining to embattled revenue growth that has been dragged down with the China mess.

At the end of the day, companies have less resistance when they aren’t belligerently brawling with their biggest purchasers.

Biting the hand that feeds you is a poor strategy that cuts across any industry.

Avoid chip companies for the short term and wait for sentiment to reverse course.