Remember when Pfizer (PFE) was strutting around Wall Street like a rooster in a henhouse, clucking about their $10 billion-a-year weight-loss wonder drug?

Well, that golden egg turned out to be a dud, with safety issues and side effects sending their experimental pills to the scrap heap faster than you can say "clinical trial failure."

Just when we thought Pfizer had thrown in the towel, they're back in the ring, swinging with a new once-daily version of danuglipron and pushing it towards bigger studies.

But let me tell you, the market's about as excited as I am for a vegan BBQ. Pfizer's shares nudged up a measly 0.4% upon announcement, after a brief 2.9% spike that fizzled faster than a diet soda.

Now, let's talk about the 800-pound gorillas in the room: Eli Lilly's (LLY) Zepbound and Novo Nordisk's (NVO) Wegovy.

These weekly jabs are the current darlings of the weight-loss world, but everyone and their grandmother are scrambling to get an oral GLP-1 to market. It's like watching a gold rush, except instead of pickaxes, they're wielding pipettes.

Lilly's got orfoglipron in Phase 3, with data coming faster than a day trader's heartbeat. Novo's already peddling Rybelsus, though it's about as effective as a chocolate teapot compared to the injectables.

And don't forget the up-and-comers: Viking Therapeutics (VKTX), Gilead Sciences (GILD), and Structure Therapeutics (GPCR) are all elbowing for a spot at the table.

Now, I know Pfizer's trying to convince us that their once-daily danuglipron is the bee's knees, with "encouraging pharmacokinetic data." But they're as tight-lipped about side effects as a politician at a press conference.

The research world’s not completely buying it, and frankly, neither am I. We might be waiting until the cows come home - or at least until 2026 - before we see if this pill's worth its weight in gold.

Meanwhile, Pfizer's stock has been sagging like a bulldog's jowls, down 1.5% this year and a gut-wrenching 21% over the past 12 months.

They're also staring down the barrel of a $17 billion revenue nosedive by 2030 as their patents fly the coop faster than pigeons at feeding time.

So, what has Pfizer been doing to deal with these? In recent months, the company has been on an acquisition bender that'd make a Vegas high-roller blush.

They snagged cancer specialist Seagen for a cool $43 billion, aiming to have eight blockbuster cancer drugs by 2030.

They're also playing footsie with BioNTech (BNTX) again, cooking up mRNA goodies like a COVID/flu combo vaccine. And let's not forget their partnership with Flagship Pioneering in the weight loss arena.

Over the past five years, Pfizer hasn’t been shy about spending money, securing over 20 new medicine approvals.

But Wall Street's been about as impressed as a cat with a new toy - they sniff at it and walk away. The stock took a 40% nosedive in 2023, partly thanks to their obesity program face-planting.

Still, Pfizer is not giving up so easily. In fact, they’ve worked to give their lineup a facelift. New approvals are rolling in faster than a greased pig at a county fair, and their pipeline's deeper than a philosopher on a bender.

Now, here's the million-dollar question: Is Pfizer a diamond in the rough or fool's gold? The market overreacted to their COVID-19 vaccine success, and now they might be overcorrecting in the other direction.

For those of you with nerves of steel and the patience of a Zen master, Pfizer could be a steal at these prices. If you don’t have the stomach for it, then I suggest you look elsewhere.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-07-18 12:00:282024-07-18 12:46:43From Golden Egg To Dud, And Back Again?

Remember when David took down Goliath? Well, history's repeating itself in the biotech arena, and this time, David's got deep pockets and a Ph.D.

Since April, I've been watching a trend on the so-called "next-generation" players in biotech and healthcare world. It reminds me of the massive changes I witnessed in Asian markets back in the '70s.

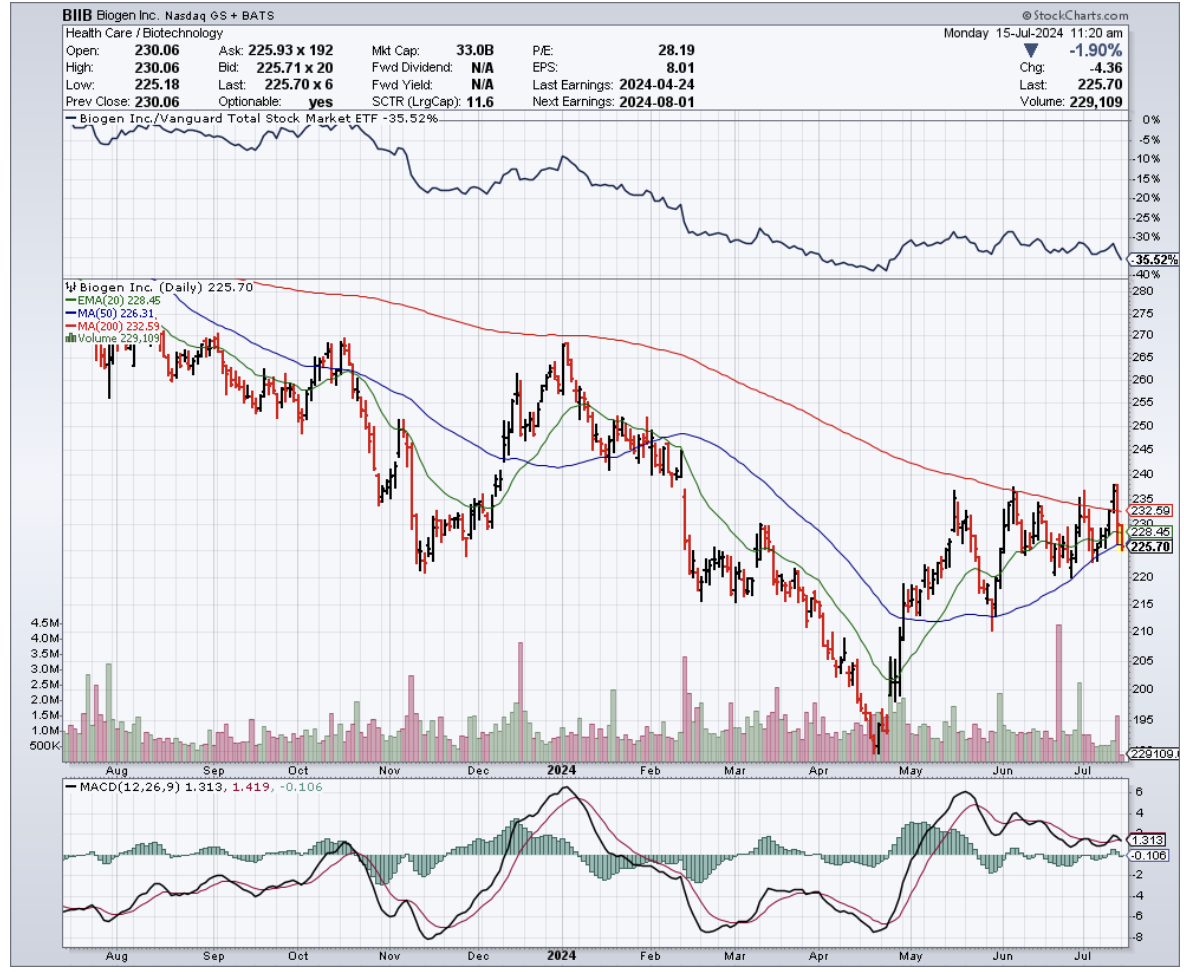

Over the past months, companies like Genmab (GMAB), Ono Pharmaceutical (OPHLY), Vertex (VRTX), Incyte (INCY), Biogen (BIIB), and Asahi Kasei (AHKSY) have been making waves that would impress even the most seasoned surfer. And these next-gen dealmakers aren't just dipping their toes in the M&A pool - they're doing cannonballs.

With cash reserves that would make Scrooge McDuck blush, these companies are overturning industry norms, already joining the prestigious $100 billion market cap club. At this celebration, the champagne flows freely.

So, what’s the play here?

With IPOs cooling down like day-old coffee, companies eyeing public debuts are now ripe targets for acquisition, more tempting than a juicy peach.

This fresh class of biotechs, unphased by the FTC's scrutiny that acts like kryptonite to pharma giants, are acting more like rocket fuel for these agile consolidators.

They slide through regulatory gaps faster than a greased pig at a county fair, grabbing six out of ten biopharma M&A deals in the second quarter alone. They’re not just taking a slice of the pie—they’re rewriting the recipe.

And if we're talking about firepower? These newcomers boast an average of $3.8 billion in pro forma adjusted cash, which isn't just walking-around money — that's "buy a small country" money.

But don't think for a second that this cash is just sitting pretty in their coffers. These upstarts are putting their money where their mouth is.

Take Incyte, for instance. They flexed their financial muscle with a $2 billion buyback in May 2024, sending a clear message to the market: "We're here to play, and we're playing to win."

And that's just the tip of the iceberg. The industry as a whole is lounging on a cool $1.5 trillion. That's enough liquidity to stretch the imagination — perhaps even to purchase a small planet. Mars, anyone? Elon might give us a discount.

But this financial might isn't just about buying power – it's about survival. As I said before, Big Pharma is teetering on a patent cliff that threatens to erode their revenue streams. To stay competitive, they're scrambling to replenish their pipelines, acquiring promising assets and gobbling up innovative technologies with the voracity of Pac-Man on steroids. And it's not just the usual suspects making moves.

This sense of urgency has created a fertile ground for an emerging cohort of aggressive dealmakers. Companies like Alnylam (ALNY), argenx (ARGX), BeiGene (BGNE), Moderna (MRNA), Neurocrine Biosciences (NBIX), BioNTech (BNTX), and Ipsen (IPSEY) are biting off more than the market expected them to chew, and they're coming to the table hungry.

And these companies aren't just nibbling around the edges. They're making bold moves, acquiring cutting-edge biotech firms with promising pipelines. We're talking oncology, epilepsy, kidney diseases, cardiovascular plays –it's like someone turned a medical textbook into a shopping catalog.

In fact, even the big boys are flexing their muscles.

Novo Holdings (NVO) dropped a jaw-dropping $16.5 billion on Catalent (CTLT). That's not even for a drug - it's for manufacturing. Talk about betting on the picks and shovels in this biotech gold rush.

Eli Lilly (LLY) just plunked down $3.2 billion on Morphic Therapeutic (MORF), betting big on inflammation, immunity, and oncology.

Johnson & Johnson's (JNJ) been on a shopping spree, too, snagging Numab's Yellow Jersey for $1.25 billion and Proteologix for $850 million. Both plays in inflammation and immunity - clearly, they've found their sweet spot.

Biogen's not twiddling its thumbs either, striking a deal with HI-Bio worth up to $1.8 billion.

Not to be outdone, Gilead (GILD) shook hands with CymaBay Therapeutics to the tune of $4.3 billion. Even AbbVie (ABBV), playing it cooler, still dropped a cool $250 million on Celsius.

Meanwhile, Merck's (MRK) set its sights on EyeBio for up to $3 billion, focusing on ophthalmology.

Sanofi (SNY), Bristol Myers Squibb (BMY), GSK (GSK) - they're all in, placing their chips on everything from rare diseases to generics to asthma. Clearly, the Big Pharma giants are also trying to keep up with this shift.

As the biotech field evolves, watching these underdogs will be like watching history in the making — where today's Davids become tomorrow's Goliaths. I suggest you keep a close eye on the names above. Adding them to your portfolio would mean you’re not just watching the giants rise — you’ll be a part of the story.

You know how every golfer dreams of donning the green jacket at the Masters, every chess player longs for the title of Grandmaster, and every football player fantasizes about hoisting the Lombardi Trophy?

Well, healthcare and biotech companies have their own version of the ultimate dream: launching a product that's as successful as the latest weight loss drugs from Eli Lilly (LLY) and Novo Nordisk (NVO).

These two pharma heavyweights have been on an absolute tear, with their shares skyrocketing 611% and 471% respectively over the past five years. It's the kind of rally that'll make your head spin and your wallet sing.

And guess what? The good news just keeps on coming. Analysts have cranked up their forecast for the obesity market. They're now predicting it'll hit a jaw-dropping $130 billion by 2030, up from their previous estimate of $100 billion.

That's an extra $30 billion. I don't know about you, but I call that a pretty sweet cherry on top.

Thanks to this obesity drug frenzy, Lilly has become the world's biggest healthcare company, and Novo Nordisk is now the most valuable company in Europe. It's like watching a couple of underdogs become the kings of the castle overnight.

Now, don't get me wrong, I love a good growth story as much as the next guy, and I wouldn't bet against Lilly or Novo Nordisk. But you know what I like even more? Biotech companies that are flying under the radar. The ones that are quietly innovating and positioning themselves for big things down the road.

That's where Amgen (AMGN) comes in.

I've been singing this company's praises in almost every piece I write, and for good reason. Amgen is one of the most innovative healthcare companies out there, with a massive product portfolio, a robust pipeline, and a balance sheet that's healthier than a triathlete on a kale smoothie diet.

Let me break it down for you. Established biotech companies with strong product portfolios are like fortresses in the business world.

They've got wide moats that are harder to cross than the Strait of Gibraltar. Why? Because bringing a new drug to market costs an arm and a leg.

We're talking anywhere from $314 million to $2.8 billion, depending on who you ask. That's not exactly chump change.

But Amgen? They've got it all figured out. Their portfolio spans a variety of therapeutic areas, including general medicine, oncology, inflammation, and rare diseases.

And in the first quarter of this year, these products helped Amgen rake in a whopping $7.4 billion in revenue, a 22% increase from the same period last year.

Key drugs like Repatha, Evenity, Blincyto, and Tezpire are leading the charge, with growth rates that'll make your head spin.

Repatha alone saw record sales of $517 million, thanks to a 44% increase in volume. And get this: expanded coverage and the removal of prior authorization requirements made the drug more accessible to patients.

It's like Amgen waved a magic wand and made all the red tape disappear.

Still, Amgen isn't just content with dominating the US market. They're taking their show on the road and expanding their international footprint.

Evenity, for example, has become the segment leader in Japan, capturing a staggering 46% of the bone builder market. And Uplinza, Amgen's fastest-growing biologic for a rare neurological disorder called neuromyelitis optica spectrum disorder (NMOSD), has been launched in multiple markets, including Canada.

Speaking of Uplinza, this little powerhouse came to Amgen via their $27.8 billion acquisition of Horizon last year. And let me tell you, it's paying off in spades.

In the first quarter of 2023, sales of Uplinza shot up by roughly 60%. And its smaller sibling, Tavneos, which targets a rare blood vessel disorder, saw a mind-boggling 122% growth.

The good news doesn't stop there. Amgen just released some hot-off-the-press Phase 3 data for Uplinza in another autoimmune condition, bringing it one step closer to yet another FDA approval.

This could put some serious pressure on competitors like Immunovant (IMVT) and argenx (ARGX), who have hit a few speed bumps lately.

Now, I know what you're thinking. "But John, what about the obesity market? Isn't that where the real action is?" Well, let me tell you, Amgen's got its fingers in that pie too.

They've got a unique obesity drug candidate called MariTide, which I talked about in detail last month, and the early clinical trial data suggests that it could blow Eli Lilly and Novo Nordisk's drugs out of the water.

But Amgen isn't just about cutting-edge drugs and international expansion. They're also rewarding their shareholders with cold, hard cash.

Last December, they hiked their dividend by 5.6%, and they're now paying out $2.25 per share every quarter.

That translates to a juicy 3% yield, and it's backed by a payout ratio that's lower than a limbo stick at a beach party.

Plus, Amgen's been raising its dividend like clockwork, with a five-year compound annual growth rate of 9.6% and 12 consecutive annual hikes. That's the kind of consistency that'll make any investor smile.

Overall, it’s clear that Amgen is a standout in the biotech world, plain and simple.

Besides, this company isn’t some Johnny-come-lately to the biotech game. They've been in this fight since the beginning, and their very name is proof of their founding principles. In fact, “Amgen” is a fancy-pants word for "applied molecular genetics."

That's right, when they picked that name back in 1980, they were already knee-deep in the groundbreaking science of genetic engineering, cooking up new therapies that would change the face of medicine as we know it.

So here’s my advice. When the chips are down and the stakes are high, you can never go wrong to bet on the OG of applied molecular genetics. Buy the dip on Amgen.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-13 12:00:402024-06-13 12:49:32The Tortoise In The Biotech Race That's About To Cross The Finish Line

(The Mad June traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE MALLARD MARKET and ME AND 23 AND ME),

(AAPL), (GOOGL), (AMZN), (TSLA), (MSFT), (META), (AVGO), (LRCX), (SMCI), (NVR), (BKNG), (LLY), (NFLX), (VIX), (COPX), (T), (NVDA), (LEN), (KBH)

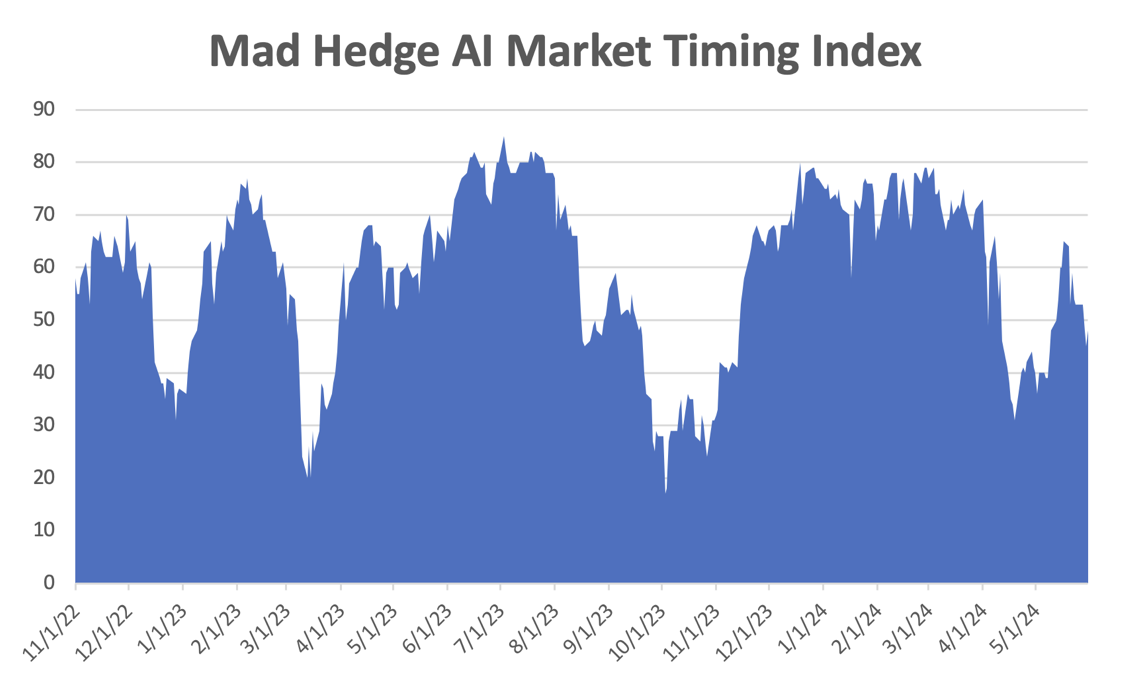

There’s nothing like the comfort and self-satisfaction of having a 100% cash position in a falling market. While everyone else is bleeding red ink, I am happily plotting my next trades.

Of course, the rest of the market isn’t really bleeding red ink, just giving up windfall profits. Still, it’s better to trade from a position of strength than weakness. It makes identifying the next winners easier.

Think of this as the “Mallard Market”. On the surface, it seems calm and peaceful, while underwater, it is paddling along like crazy. The damage has been unmistakable. Dell, the faux AI stock (DELL) crashed by 28%, Salesforce (CRM) got creamed for 34%, and ServiceNow (NOW) got taken to the woodshed for 22%.

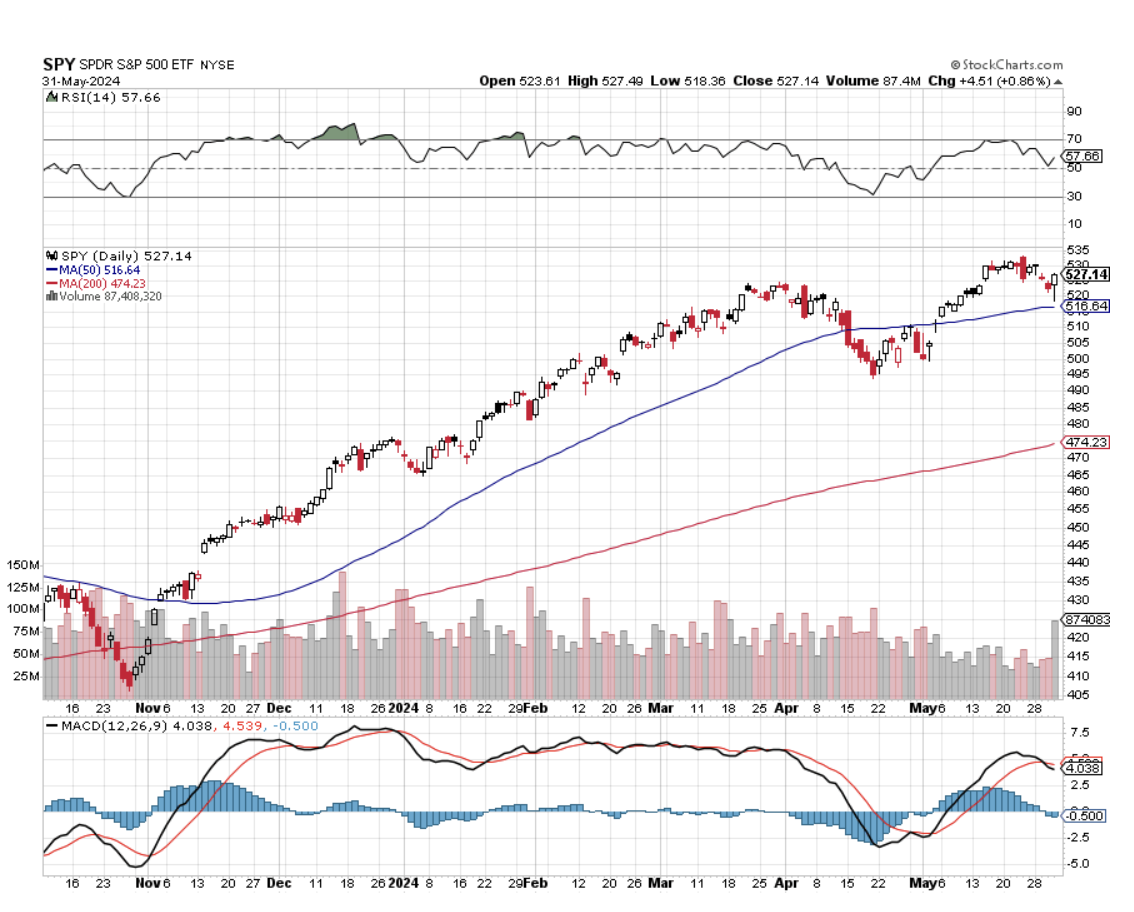

It all belies a market that is incredibly nervous and fast on the trigger. The tolerance for any bad news is zero. Yet there has been no market crash as I expected. The 5,300 level for the (SPX) seems to possess a gravitational field, powered by $250 earnings per share and a multiple of 51X.

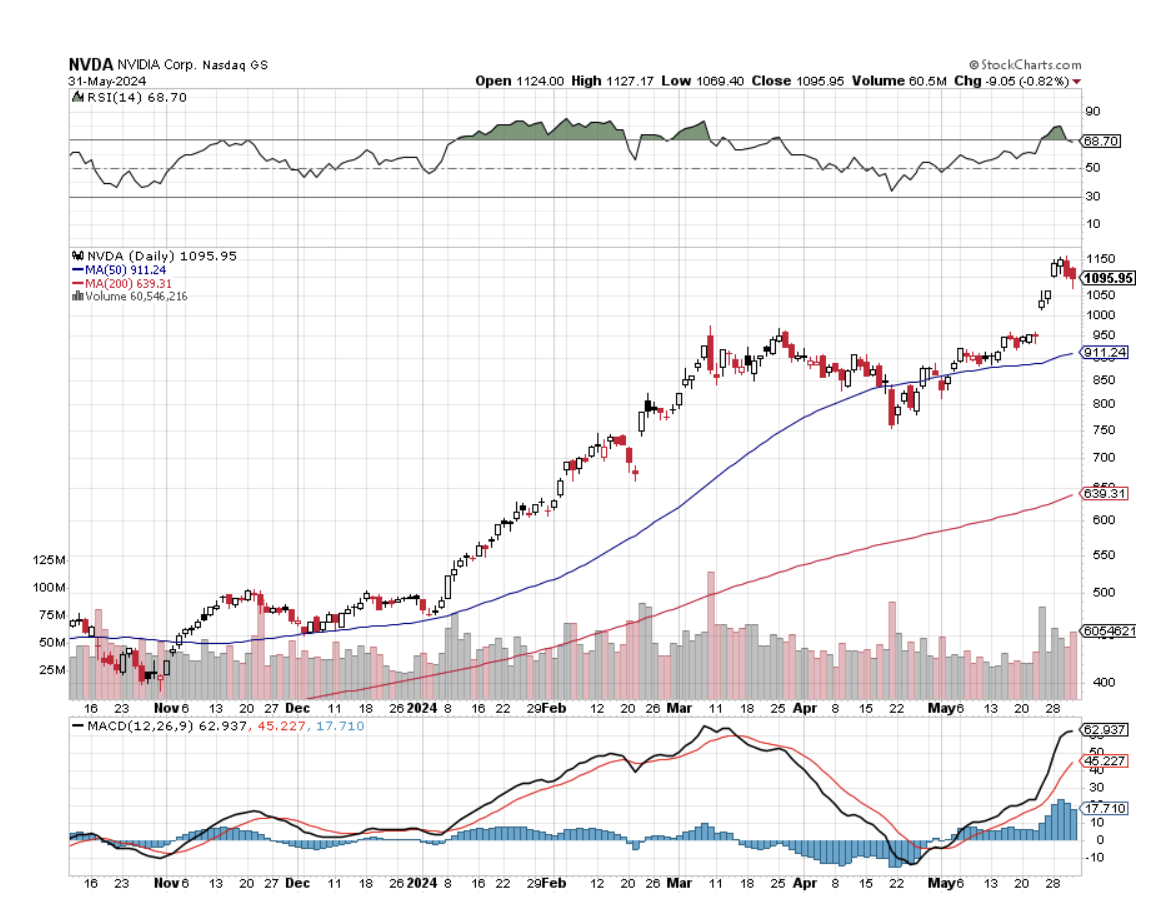

It was NVIDIA that put the writing on the wall by announcing a 10:1 split that has opened the floodgates for similar prosperous and high-priced companies.

There are now 36 stocks with share prices of $500 or more ripe for splits with $7 trillion in market cap, or 16% of the total market. While splits don’t change the value of a company, perceptions are everything, as they prove shareholder-friendly policies. While individual investors are confused by an onslaught of contradictory research recommendations, splits are a great “tell” on what to buy next.

Apple (AAPL), Alphabet (GOOGL), Amazon (AMZN), and Tesla (TSLA) have already carried out splits, some multiple times, to great success. Of the Magnificent Seven, only Microsoft (MSFT) and Meta (META) have yet to split.

In the tech area Broadcom (AVGO), Lam Research (LRCX), Super Micro Computer (SMCI), and Service Now (NOW) have yet to split. In the non-tech area, there are NVR Inc. (NVR), Booking Holdings (BKNG), Eli Lilly (LLY), and Netflix (NFLX). Many of these are well-known Mad Hedge recommended stocks.

History has shown that stocks rise 25% one year after a split compared to 12% for the market as a whole. A stock’s addition to the Dow Average or the S&P 500 (SPY) provides a boost. If both occur, stocks will absolutely explode. Stock splits are also much more attractive than buybacks at these high prices.

So, I’ll be trolling the market for split-happy candidates.

You should too.

Since it may be some time before we capitulate and take a worthwhile run at new highs, I thought I’d update you on the global demographic outlook, which is always a long-term driver of economies and markets.

People are now living longer than ever before. But postponing death is only a part of the demographic story. The other is the decline in births. The combination of the two is creating huge changes in the global economy.

The notion of a “demographic transition” is almost a century old. Human societies used to have roughly stable populations, with high mortality matched by high fertility. Families had eight kids and 3-5 usually died in childhood, barely maintaining population growth.

In England and Wales in the 18th and 19th centuries, death rates suddenly plummeted. But fertility did not. The result was a population explosion. As the benefits of economic growth and advances in medicine and public health spread, most of the world has followed a similar transition, but far faster. As a result, human numbers rose fourfold over the last hundred years, from 2 billion to 8 billion.

In time, fertility followed mortality on a downward path across most of the world. As a result, fertility rates in more than half of all countries and territories in 2021 fell below the replacement level. For the world as a whole, the fertility rate was 2.3 in 2021, barely above the replacement of 2.1, down from 4.7 in 1960.

For high-income countries, the fertility rate was a mere 1.6, down from 3.0 in 1960. In general, poor countries still have higher fertility rates than richer ones, but they have been falling there, too.

What explains this collapse in fertility rates? An important part of the answer is the wonderful surprise that more children survived than expected. So, people started to practice various forms of birth control.

But the desire to have many children also shrank sharply. When husbands realized that smaller families meant high standards of living for themselves, family sizes dropped sharply. Even in ultra-conservative Iran, the fertility rate has collapsed from 6.6 in 1980 to only 1.7 in 2021.

A big reason for this shift was that, for their parents, children have moved from being a valuable productive asset in the 19th century to an expensive luxury today. That was back when 50% of our population worked on farms. Today it’s only 2%.

In the meantime, female participation in the economy rose dramatically in the 20th century, including in highly skilled careers. That raised the “opportunity cost” of producing children, especially for mothers. So, they have children later, or even not at all.

Where public childcare is more generous women are encouraged to combine careers with having children. The absence of such help helps explain the exceptionally low fertility rates in much of East Asia and Southern Europe, where parental support is limited.

This global shift towards very low fertility, with the exception (so far) of sub-Saharan Africa, is among the most important events driving the global economy. One implication is that the population of Africa is forecast to be larger than that of all today’s high-income countries, plus China by 2060, thanks to the elimination of many diseases there.

Why is all this important?

Because rising populations create larger markets, more profits for corporations, and rising share prices. Shrinking populations have the opposite effect, as China is learning about its distress now. One reason the US is growing faster than the rest of the world is that a continuous stream of new immigrants since its foundation has created endless numbers of new workers and customers. Dow 240,000 here we come!

Just thought you’d like to know.

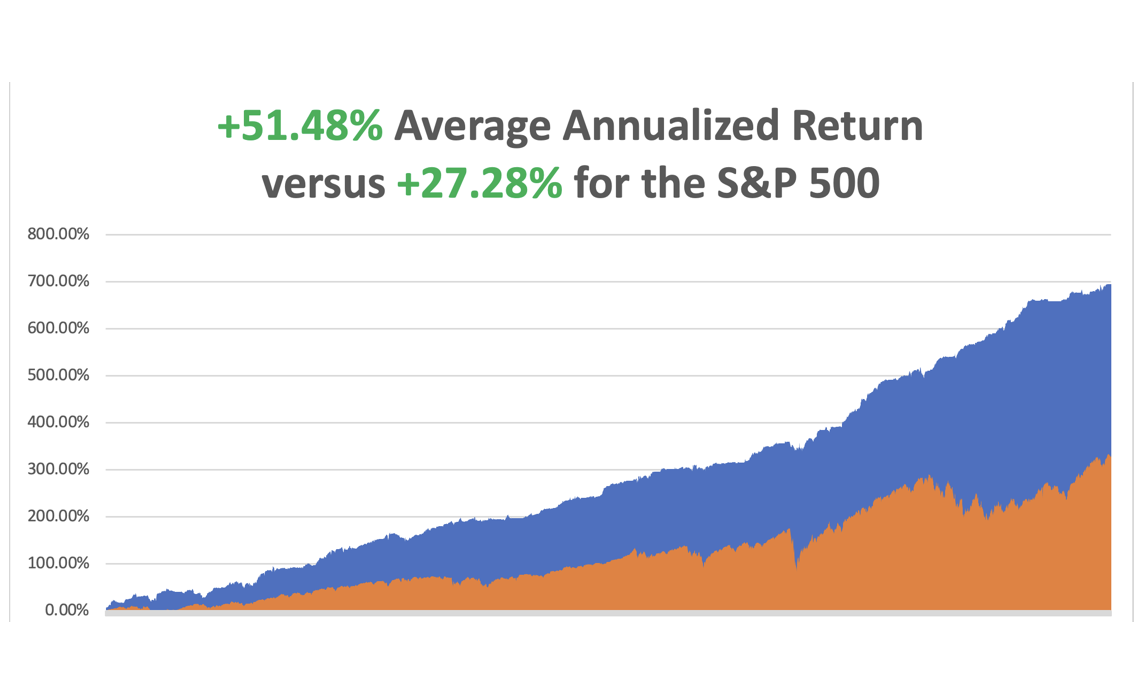

So far in May, we are up +3.74%. My 2024 year-to-date performance is at +18.35%.The S&P 500 (SPY) is up +10.48%so far in 2024. My trailing one-year return reached +35.74%. That brings my 16-year total return to +694.78%.My average annualized return has recovered to +51.48%.

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I bailed on my last position early in the week, covering a short in Apple for a profit.

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

The Fed’s Favorite Inflation Gauge Cools by 0.2% in April, with the PCE, or the Personal Consumer Inflation Expectations Price Index. This one strips out the volatile food and energy components. It gives more credibility to a September rate cut and gave bonds a good day. NVIDIA Shares Continues to Go Ballistic, creating another $800 billion in market capitalization in three trading days. That is the most in history. That took NASDAQ to a new all-time high at 17,000. At $2.8 trillion (NVDA) could become the largest publicly traded company in the world in another day. Today’s tailwind came from an Elon Musk comment that his new xAI start-up would buy the company's high-end H100 graphics cards. Buy (NVDA) on the next 20% dip.

Pending Home Sales Dive, down 7.7% in April, the worst since the Covid market three years ago. The impact of escalating interest rates throughout April dampened home buying, even with more inventory in the market. But the anticipated rate cuts later this year should lead to better conditions, with improved affordability and more supply. Buy (LEN) and (KBH) on dips.

Money Supply Rises for the First Time in More than a Year. Remember money supply? As measured by M2, it sums up the currency, coins, and savings deposits held by banks, balances in retail money-market funds, and more. Data for April released on Tuesday afternoon showed an increase of 0.6% from a year ago. The Fed balance sheet has shrunk by $1.5 trillion in two years, the fastest decline in history, slowing the economy.

AT&T’s (T) Copper is Worth More Than the Company, and with plans to convert half its copper network to fiber by 2025 could free up billions of tons of the red metal to sell on the market. Copper prices have doubled over the past two years, and they could double again by next year. Worldwide there are 7 trillion tons of copper wire in place. Fiber is cheaper and exponentially more efficient than copper, which is facing huge demands from AI, EVs, and the electrification of the grid. Buy copper (COPX) on dips.

Markets are Underpricing Low Volatility (VIX), not a good thing at all-time highs. Volatility across equity and currency markets is low. The Volatility Index (VIX) at $12.46 compares with an average over five years of $21.5 and over the longer term of $19.9. Markets are heavily discounting good news and a disinflationary environment. It is not only stocks. There is also low volatility across currency markets. The DB index of foreign exchange volatility is at $6.3 versus an average of $7.6 over five years and $9.3 over the longer term. This will end in tears.

S&P Case Shiller Jumps to New All-Time High, with its National Home Price Index. The index rose by 1.29%, the fastest growth since April 2023. All 20 major metro cities were up last month and gained 6.5% YOY. Four cities are currently at all-time highs: San Diego, Los Angeles, Washington, D.C., and New York. Prices in San Diego saw the biggest gain, up 11.4% from February of 2023. Both Chicago and Detroit reported 8.9% annual increases. Portland, Oregon, saw the smallest gain in the index of just 2.2%. Unaffordability is the big story in the market right now. The sunbelt is seeing the most weakness, thanks to a post-pandemic construction boom.

Space X’s Starlink Tops 3 million Subscribers, and is rapidly moving towards a global WiFi network. I set up a dozen of these in Ukraine last October and even the Russians couldn’t hack them. It sets a global 200 Mb standard usable in most countries, even the remote Galapagos Islands in the Pacific. It’s only a VC investment now but could become Elon Musk’s next trillion-dollar company.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 3, the ISM Manufacturing PMI is released.

On Tuesday, June 4 at 7:00 AM, the JOLTS Job Openings Report will be published.

On Wednesday, June 5 at 7:00 AM, the ISM Services PMI is published.

On Thursday, June 6 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Challenger Job Cuts Report.

On Friday, June 7 at 8:30 AM, the Nonfarm Payroll and headline Unemployment Rate are announced. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when Anne Wojcicki founded 23andMe in 2007, I was not surprised. As a DNA sequencing pioneer at UCLA, I had been expecting it for 35 years. It just came 70 years sooner than I expected.

For a mere $99 back then they could analyze your DNA, learn your family history, and be apprised of your genetic medical risks. But there were also risks. Some early customers learned that their father wasn’t their real father, learned of unknown brothers and sisters, that they had over 100 brothers and sisters (gotta love that Berkeley water polo team!), and other dark family secrets.

So, when someone finally gave me a kit as a birthday present, I proceeded with some foreboding. My mother spent 40 years tracing our family back 1,000 years all the way back to the 1086 English Domesday Book (click here)

I thought it would be interesting to learn how much was actually fact and how much fiction. Suffice it to say that while many questions were answered, alarming new ones were raised.

It turns out that I am descended from a man who lived in Africa 275,000 years ago. I have 311 genes that came from a Neanderthal. I am descended from a woman who lived in the Caucuses 30,000 years ago, which became the foundation of the European race.

I am 13.7% French and German, 13.4% British and Irish, and 1.4% North African (the Moors occupied Sicily for 200 years). Oh, and I am 50% less likely to be a vegetarian (I grew up on a cattle ranch).

I am related to King Louis XVI of France, who was beheaded during the French Revolution, thus explaining my love of Bordeaux wines, women wearing vintage Channel dresses, and pate foie gras.

Although both my grandparents were Italian, making me 50% Italian, I learned there is no such thing as pure Italian. I come out only 40.7% Italian. That’s because a DNA test captures not only my Italian roots, plus everyone who has invaded Italy over the past 250,000 years, which is pretty much everyone.

The real question arose over my native American roots. I am one-sixteenth Cherokee Indian according to family lore, so my DNA reading should have come in at 6.25%. Instead, it showed only 3.25% and that launched a prolonged and determined search.

I discovered that my French ancestors in Carondelet, MO, now a suburb of Saint Louis, learned of rich farmland and easy pickings of gold in California and joined a wagon train headed there in 1866. The train was massacred in Kansas. The adults were all killed, and the young children were adopted into the tribe, including my great X 5 Grandfather Alf Carlat and his brother, then aged four and five.

When the Indian Wars ended in the 1880s, all captives were returned. Alf was taken in by a missionary and sent to an eastern seminary to become a minister. He then returned to the Cherokees to convert them to Christianity.By then, Alf was in his late twenties so he married a Cherokee woman, baptized her, and gave her the name of Minto, as was the practice of the day.

After a great effort, my mother found a picture of Alf & Minto Carlat taken shortly after. You can see that Alf is wearing a tie pin with the letter “C” for his last name Carlat. We puzzled over the picture for decades. Was Minto French or Cherokee? You can decide for yourself.

Then 23andMe delivered the answer. Aha! She was both French and Cherokee, descended from a mountain man who roamed the western wilderness in the 1840s. That is what diluted my own Cherokee DNA from 6.50% to 3.25%. And thus, the mystery was solved.

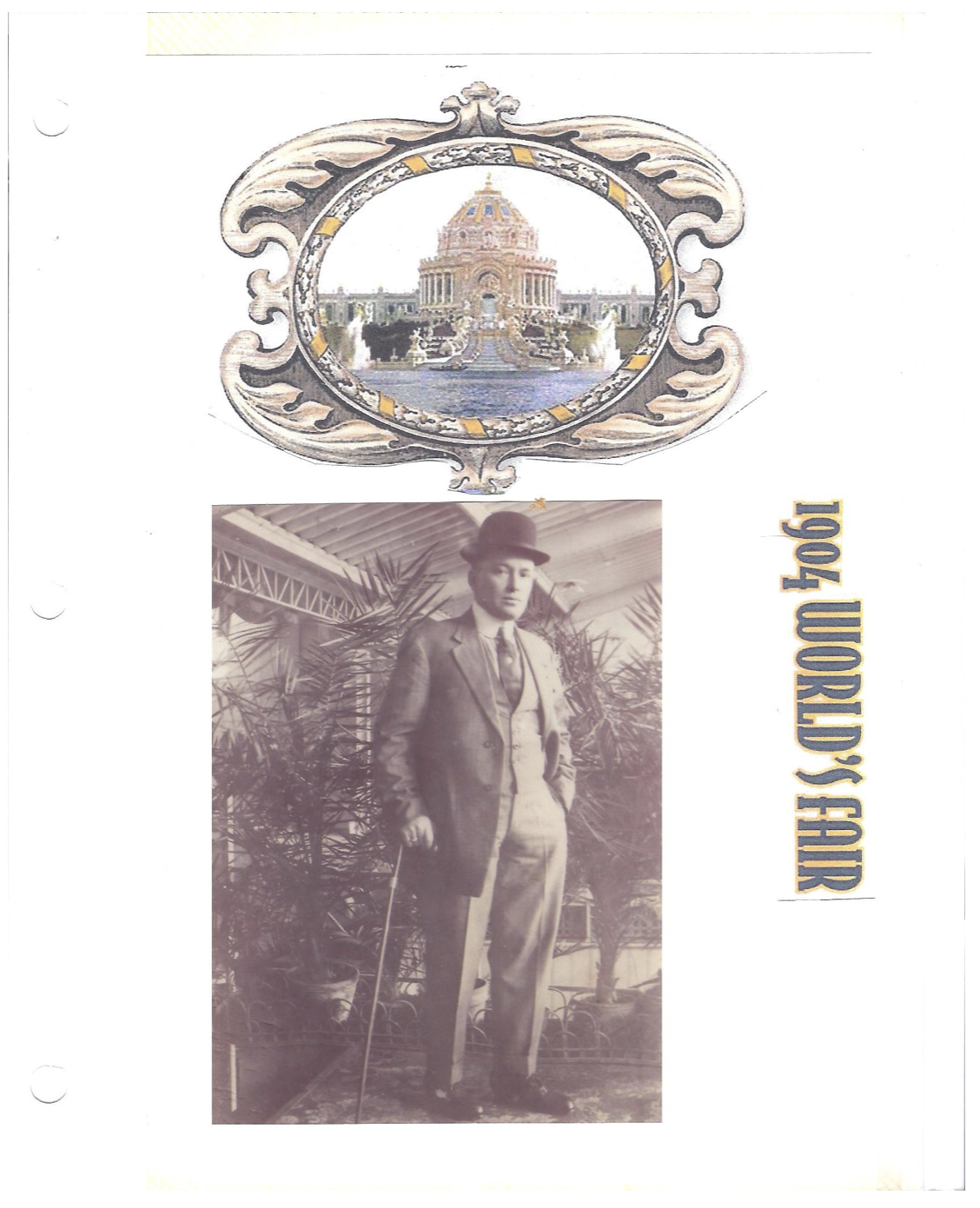

The story has a happy ending. During the 1904 World’s Fair in St. Louis (of Meet Me in St. Louis fame), Alf, then 46, placed an ad in the newspaper looking for anyone missing a brother from the 1866 Kansas massacre. He ran the ad for three months and on the very last day, his brother answered and the two were reunited, both families in tow.

Today, getting your DNA analyzed starts from $119, but with a much larger database, it is far more thorough. To do so, click here.

My DNA Has Gotten Around

It All Started in East Africa

1880 Alf & Minto Carlat, Great X 5 Grandparents

The Long-Lost Brother

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2023/01/alf-minto.jpg252293april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-03 09:02:142024-06-03 11:56:52The Market Outlook for the Week Ahead, or Welcome to the Mallard Market

Hang on to your Geiger counters because we're about to dive deep into the world of radiopharmaceutical therapy. I bet even Marie Curie would be impressed by the mind-blowing leaps we've made since her ground-shattering discoveries a century ago.

Now, don't get me wrong, she's a tough act to follow. But the big guns in pharma have taken up the challenge, piling up billions on the roulette table of targeted radiopharmaceutical therapy.

And from where I'm sitting, the odds are looking pretty darn exciting.

Just picture the scene: Radiation that directly takes the fight to those nasty tumor cells, like a microscopic missile strike that zaps cancer cells while ignoring the innocent bystanders.

How? By hitching a radioactive particle to a targeting molecule - think Uber, but for cancer therapy.

This healthcare game-changer, dubbed radiopharmaceutical therapy is projected to become a whopping $25 billion goldmine.

Forget the clunky radiation therapy your grandparents endured – this is precision, it's innovation, and it could potentially enrich your investment portfolio.

Actually, everyone seems to be piling into the radiopharma race. Experts say we're merely at the start line and these next-gen technologies could bring a windfall.

Evidence? The recent flurry of acquisitions, with no less than four deals being sealed just these past months.

Now, let's put some names to this game.

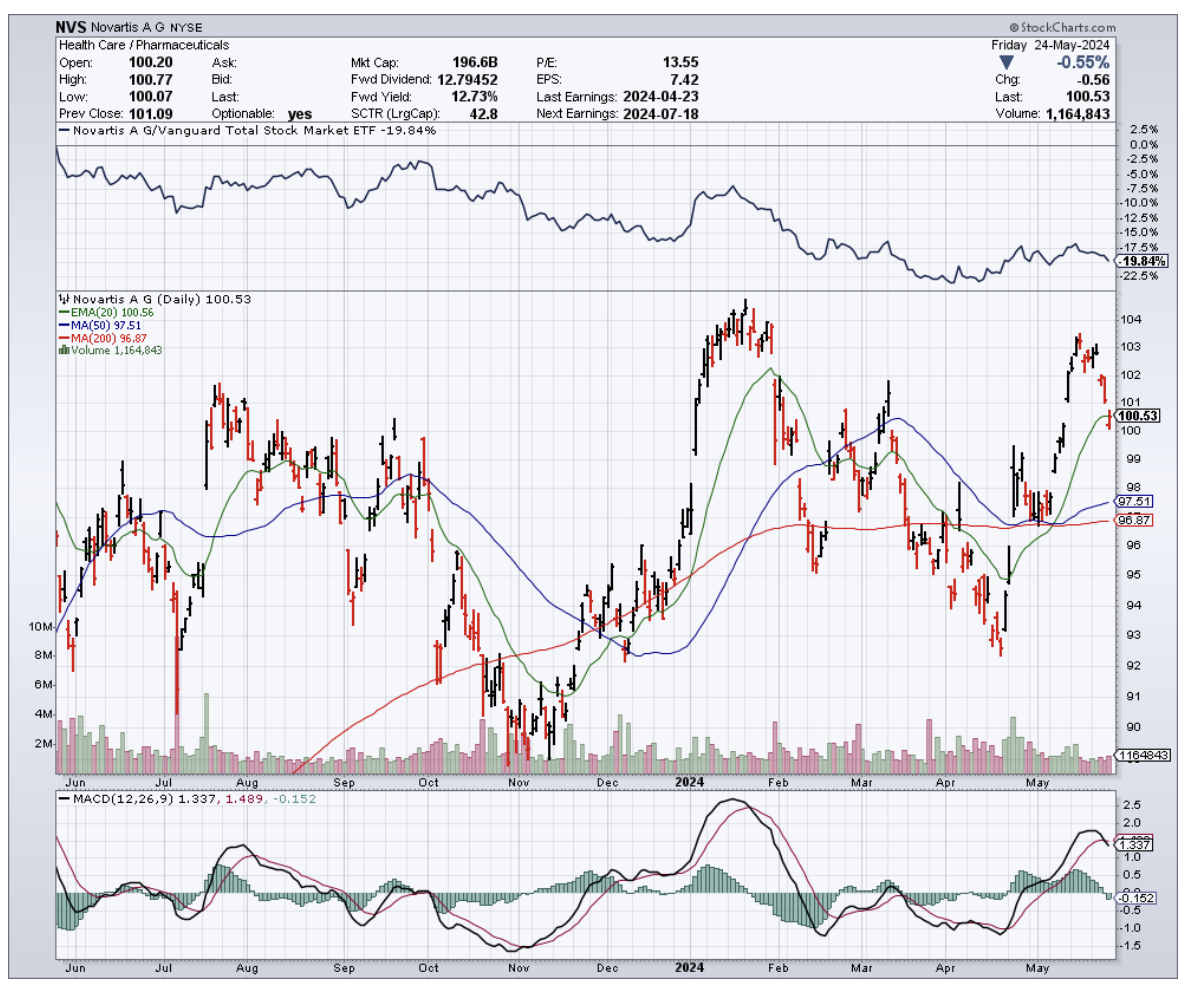

Novartis (NVS) is leading the pack with two radiopharmaceutical showstoppers under its belt. With their drugs Pluvicto and Lutathera, they're forecasted to rake in a whopping $5 billion by 2028 – that's more zeros than I can count on two hands.

Not just resting on their pile of success, they've scooped up Mariana Oncology in a $1 billion deal. This strategic move solidifies Novartis' dominion in the radiopharmaceutical arena – and you can quote me on that.

Inspired by Novartis' success, other pharmaceutical titans are catching the FOMO fever.

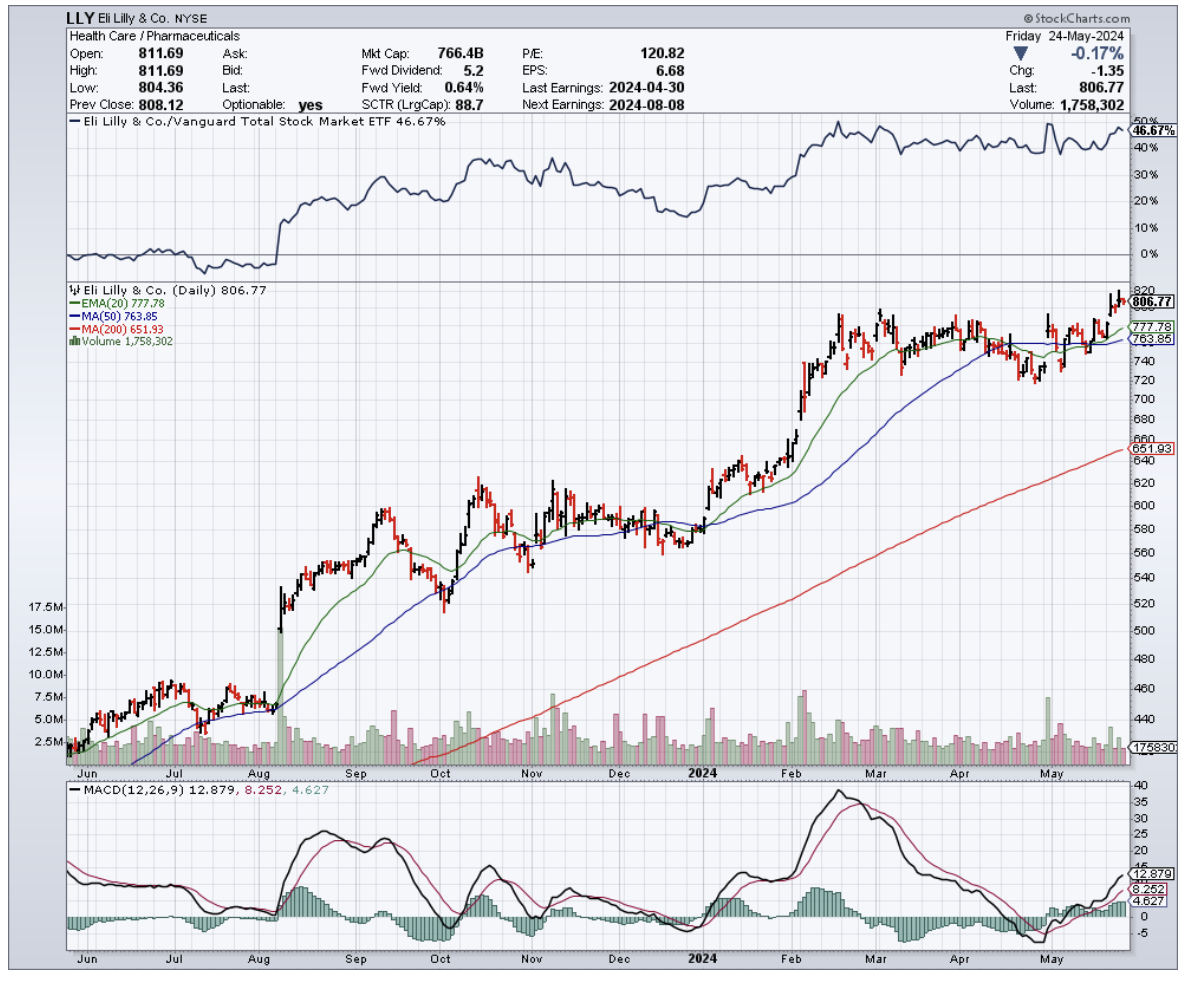

Eli Lilly (LLY), for instance, handed over $1.4 billion to acquire Point Biopharma and its promising radiation drug, PNT2002.

The investors’ darling this year with a near 38% surge in stock price (thanks to the overwhelming success of its obesity drugs), Eli Lilly is set to maintain its upward trajectory by venturing into the radiopharmaceutical space.

Bristol-Myers Squibb (BMY) isn't about to be left out of the radiopharmaceutical race either.

They ponied up a cool $4.1 billion for RayzeBio, snagging a promising pipeline of treatments. One standout is RYZ101, a late-stage targeted radiopharma therapy already making waves in trials for gastroenteropancreatic neuroendocrine tumors and small-cell lung cancer.

This acquisition followed closely on the heels of their $14 billion buyout of schizophrenia drug developer Karuna Therapeutics. Clearly, they’re feeling the heat as patents on some of their older cash cows are set to expire.

So, sure, BMY’s stock has been a bit sluggish lately, but this radiopharmaceutical gamble could be the shot in the arm they need.

And the acquisition spree doesn't stop there. AstraZeneca (AZN) also dove headfirst into the radiopharmaceutical pool, shelling out $2.4 billion for Fusion Pharmaceuticals in March.

Fusion's pipeline, including their Phase 2 candidate FPI-2265 for metastatic castration-resistant prostate cancer, adds another potential blockbuster to the mix.

Meanwhile, several biopharma companies are still standing tall, catching the eye of investors.

In fact, the venture capital poured into radiopharmaceutical drugs surged to $518 million last year, a cool 722% increase from 2017.

The race isn't slowing down anytime soon either. Researchers are exploring the use of radiopharmaceuticals alongside other treatments like immunotherapy, and even envision a future where this technology could be applied to any cancer, including ovarian, breast, or brain tumors.

And with only two products currently in the market, the potential for growth in targeted radiotherapies seems almost infinite.

So, I'll say it one more time – get your Geiger counters ready. The radiopharmaceutical revolution is just getting started, ladies and gentlemen. It’s time to zero in on this hotbed of innovation and watch your investments go nuclear.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-05-28 12:00:522024-05-28 11:59:05Get Your Geiger Counters Ready

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.