Mad Hedge Biotech and Healthcare Letter

March 7, 2024

Fiat Lux

Featured Trade:

(RALLY CAPS ON)

(VKTX), (LLY), (NVO), (AKRO), (GILD), (BMY), (AMGN), (PFE)

Mad Hedge Biotech and Healthcare Letter

March 7, 2024

Fiat Lux

Featured Trade:

(RALLY CAPS ON)

(VKTX), (LLY), (NVO), (AKRO), (GILD), (BMY), (AMGN), (PFE)

The biotech sector just flipped its rally cap inside out. After a brutal losing streak, it's clawing its way back. The SPDR S&P Biotech (XBI) exchange-traded fund, a barometer for the sector, started to show signs of life when it soared by 5.7% last month, cresting over $100 a share for the first time in two whole years.

While champagne might be premature, this comeback is heating up, and whispers of a full-fledged rally are echoing through Wall Street.

After a rough patch that kicked off in early 2021, seeing the fund take a nosedive of over 60% by late October 2023, the tide began to turn last fall. Initially, whispers of lower interest rates in 2024 sparked interest across small-cap indexes, including our biotech heroes.

Yet, lately, the buzz is all about biotech's own merits — think breakthrough medical trials and the juicy prospect of big pharma playing Pac-Man with smaller but promising biotech firms to beef up their drug pipelines.

And let me tell you, if the current rally's got legs, we might just be witnessing the most thrilling biotech comeback in over half a decade. Especially if the merger and acquisition scene stays hot, we could see biotech stocks climbing even higher.

Take everything that happened in the sector in February as an example. Viking Therapeutics (VKTX) threw down the gauntlet with promising data on its weight loss drug, VK2735, making investors sit up and take notice.

Actually, this candidate is shaping up to be a formidable rival to obesity treatments from Eli Lilly (LLY) and Novo Nordisk (NVO), sending Viking's shares skyward by a jaw-dropping 121% in a single day.

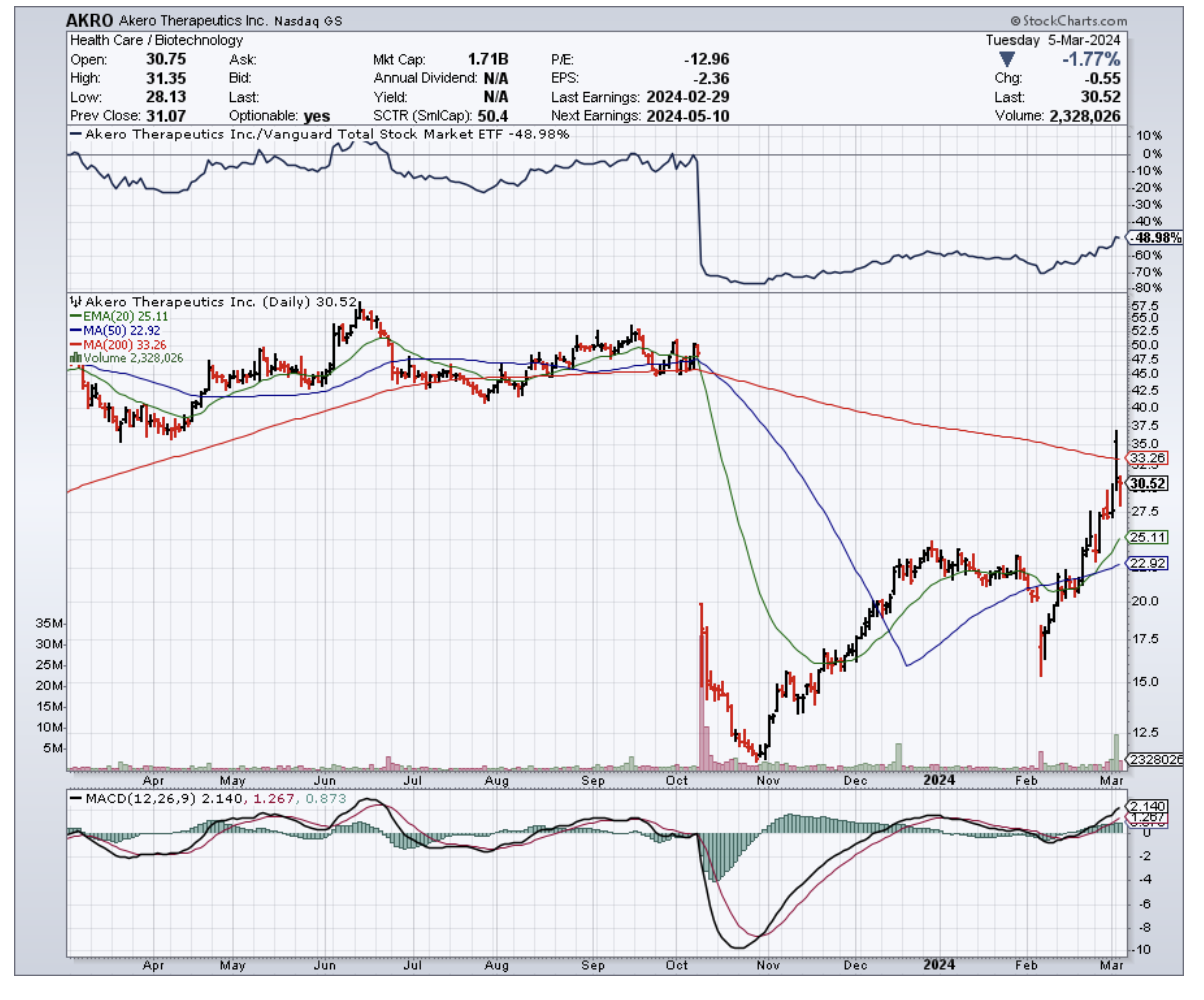

And it's not just Viking stealing the spotlight. Another biotech named Akero Therapeutics (AKRO) also bounced back with some impressive data of its own, challenging the doom and gloom that settled over biotech firms following Eli Lilly's bombshell MASH trial results.

Akero's mid-stage study showed that their drug, efruxifermin, could significantly roll back liver fibrosis in MASH patients — putting a whopping 75% of high-dose recipients on the mend, a stark contrast to the 24% placebo group.

This revelation was a game-changer, especially after Lilly's tirzepatide threw the sector for a loop, hinting at a potential endgame for MASH-specific treatments. But while Lilly's announcement left many details to the imagination, Akero's clear-cut results have reignited excitement over what might be the best MASH treatment yet seen.

As expected, in the midst of this resurgence, the likes of Viking and Akero are catching eyes not just for their groundbreaking treatments but also as tantalizing acquisition targets. Heavyweights like Gilead Sciences (GILD), Bristol Myers Squibb (BMY), Amgen (AMGN), and Pfizer (PFE) are said to be circling, each eyeing a slice of the biotech pie.

As for the biotech investment landscape in general, it's buzzing with renewed vigor. The early months of 2024 have welcomed a smattering of biotech IPOs, a refreshing change after a long drought. CG Oncology's late January debut practically set the market ablaze, doubling in value on its first trading day.

Moreover, public biotechs have found a lifeline in PIPE deals, sidestepping the regulatory hoops of secondary offerings. For instance, Denali Therapeutics' (DNLI) recent PIPE deal, expected to rake in $500 million, is proof of the sector's warming investment climate.

So, dust off those rally caps because the biotech sector isn't just back in the game – it's swinging for the fences.

Breakthrough treatments, a sizzling M&A market, and investors throwing their support behind innovation — this rally has all the ingredients to paint a bright future for the industry. While there will be bumps along the road, one thing's for sure: the biotech sector is poised for a season no one wants to miss.

Mad Hedge Biotech and Healthcare Letter

March 5, 2024

Fiat Lux

Featured Trade:

(THE SKINNY ON ECONOMIC GROWTH)

(LLY), (NVO), (AMGN)

What might just give economies a bigger jolt than the frenzy of the Super Bowl or a jampacked Taylor Swift world tour? If you guessed the recent buzz around weight-loss drugs, take a bow. You see, it's not just about slimming waistlines anymore – these breakthrough medications could be a game-changer for the whole economy.

But first, a sobering reality check: health issues have been nibbling away at the U.S. labor force like a sneaky termite over the last 30 years, shaving off two to three percentage points.

Then there's the matter of early departures from this mortal coil, chipping away another 0.2 percentage points from annual labor growth.

Not to mention the legion of unsung heroes caring for the ailing, effectively benched from the workforce, leading to a 3% labor force deficit.

Among all the health issues affecting the labor force, obesity has been identified as a sneaky little gremlin, dragging down productivity and participation in the workforce.

With obesity affecting 40% of the U.S. population, we're talking about a hefty 1% slash in total output.

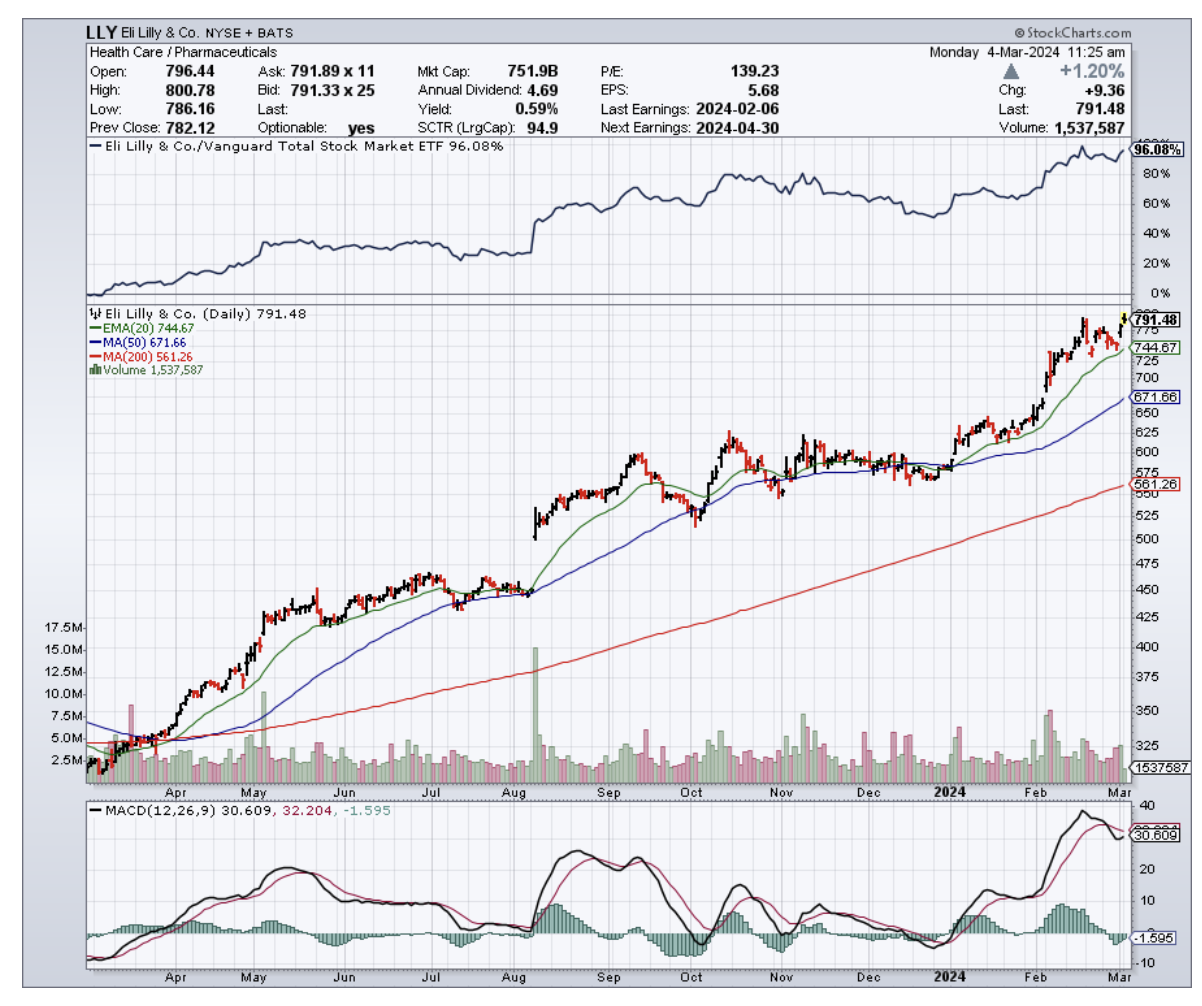

But what if there was a way to combat this? Enter stage left: Eli Lilly (LLY). Sure, you might know them as a big-league player in the pharma world, but did you know they're the brains behind blockbuster medications like Trulicity, Mounjaro, and cancer-battling Verzenio?

And the story gets even more exciting – it's not just their existing all-star lineup that's sent their stock soaring 180% since 2021. Their latest weight-loss marvel, Zepbound, got the FDA's green light last November. Think of it as Mounjaro's twin, sporting the same molecule but with a different name to keep things clear for their existing diabetes patients.

This breakthrough signals a massive shift in the obesity treatment landscape. The global anti-obesity market is projected to explode to a staggering $100 billion annually by 2030 – a dramatic leap from last year's $6 billion. To put that in perspective, global spending on cancer treatments is estimated at $220 billion this year.

Naturally, Lilly is poised to grab a big slice of that pie. Analysts are predicting a healthy 21.4% revenue boost this year, and nearly 24% by 2025. Talk about a growth spurt.

As for earnings? They're looking at nearly tripling in that timeframe. The future's so bright, Lilly might need shades.

But here's the catch: Lilly's stellar rise has its stock priced at a premium, and then some. We're talking 60 times this year's expected earnings. And while the company's profit train is set to chug along, not every stock can keep up those lofty valuations in the long haul.

And let's not forget about the competition. Novo Nordisk (NVO), with its own contenders Ozempic and Wegovy, is nipping at Lilly's heels, even as Amgen (AMGN) and others are hot on the trail with promising candidates of their own.

Yet, Lilly's not sweating it. With Zepbound (aka Mounjaro for the weight-conscious) already making waves as a go-to for obesity treatment, they're sitting pretty. It's like they've already won half the battle, with doctors and patients already in the know about this not-so-secret weapon.

Still, as tempting as it might be to hop on the Lilly bandwagon after seeing those numbers, we need to do a quick reality check before investing. It's important to remember that every stock has its ups and downs.

For starters, Lilly's stellar rise means their stock is trading at a premium – a hefty 60 times this year's expected earnings. And while the company's profit train is definitely chugging along, that kind of lofty valuation might be a bit too spicy for some investors' taste, especially in the long run.

So, what's the takeaway for those who want in on the action? Lilly's current price tag might give you pause, especially if you're looking for a bargain.

It's been a wild ride for this stock, and sometimes the best moves involve waiting for the market to catch its breath.

However, their dominant position in a rapidly expanding market definitely makes them a player worth watching closely. I suggest to buy on the dip.

Switching gears for a second, let’s take a look at the big picture. It turns out that widespread use of GLP-1 medications like Lilly's could deliver way more than just individual weight loss. We're talking about a potential shot in the arm for the entire U.S. economy.

Think about it: if 30 million Americans hop on the GLP-1 train with drugs like Mounjaro and Zepbound, and a conservative 70% of them see benefits, we could see a 0.4% boost in the U.S. GDP. And that's just the starting line.

In a best-case scenario, where 60 million Americans embrace these treatments and a whopping 90% benefit, the GDP could potentially surge by a full 1%. Even with more modest projections, with 15 million users and a 50% success rate, the economic impact would still be noteworthy.

This isn't just pocket change – it's serious economic muscle. With the right push, these weight-loss drugs could be the breakthrough prescription our economy needs, adding some serious pep to our growth alongside countless individual health transformations. Now, isn't that a story worth following?

Mad Hedge Biotech and Healthcare Letter

February 27, 2024

Fiat Lux

Featured Trade:

(CASHING IN ON CURES)

(LLY), (NVO), (JNJ), (PFE), (MRK), (BIIB)

In the biotechnology and healthcare industry, reaching a $1 trillion market cap is akin to scaling Mount Everest without oxygen. Yet, Eli Lilly (LLY) has emerged as an unexpected contender, catching the investing world’s attention by not just climbing the mountain but being on the verge of planting its flag at the summit.

A year ago, if you'd whispered in my ear that Eli Lilly's stock was about to skyrocket nearly 140%, I might have choked on my coffee. But here we are, and the buzz isn't just about the rocket ride — it's whether Eli Lilly can be the first biopharma behemoth to hit the $1 trillion market cap. Wild, right?

So, what's cooking at Eli Lilly that's got everyone so revved up? Well, they've got a couple of aces up their sleeve.

Sure, they've been making waves with Verzenio for breast cancer and Jardiance for diabetes, but the real game-changer? Tirzepatide, sold under their brand name Mounjaro for type 2 diabetes and is now strutting the stage as Zepbound for weight loss. This isn't just any old drug; it's the blockbuster that's got everyone from Wall Street to Main Street talking.

But what makes tirzepatide so darn special? It's the first of its kind, a dual GLP-1/GIP agonist, making it a heavyweight champion in the fight against obesity. With sales already blasting past the $5 billion mark in record time, it's like watching a rocket take off without any signs of slowing down.

Now, I know what you're thinking. "But hey, aren't there other big fish in the sea?" Sure, Johnson & Johnson (JNJ), Pfizer (PFE), and Merck (MRK) are doing their thing, but next to Eli Lilly's recent performance, they're looking a bit like they're running in slow motion.

And while Novo Nordisk (NVO) has been gaining traction in the diabetes market with its own version of the treatment, Eli Lilly’s tirzepatide is in a league of its own. In fact, this drug is projected to become the top-selling treatment in history, with the potential to rake in sales north of $25 billion.

For context, AbbVie (ABBV) Humira had an annual record of $21.2 billion, and that’s already the recorded highest-selling therapy in history. But, the road to hitting these goals demands many more new indications.

That’s why it comes as no surprise that tirzepatide is eyeing a new target: metabolic dysfunction-associated steatohepatitis, or MASH for short. It's a fancy way of saying "a really bad liver problem," and it's a growing issue globally.

Beyond tirzepatide, Eli Lilly's expanding in a few other markets. Alzheimer's, for one, where their potential therapy, donanemab, is making waves and presents a potential competitor to Biogen’s (BIIB) Leqembi.

And let's not overlook their recent wins with cancer medicine Jaypirca and ulcerative colitis therapy Omvoh. It's like Eli Lilly's hitting bingo on every card.

With all these in mind, can Eli Lilly truly reach that $1 trillion valuation? With their current market cap already north of $715 billion, it looks like the company is ready to take home the title. Assuming a modest compound annual growth rate of about 7%, that trillion-dollar dream could become reality quicker than you can say "biopharma giant."

As investors, industry watchers, and, frankly, anyone with a pulse on the future of medicine keep their eyes glued to this unfolding story, the message is clear: Eli Lilly is not just about the numbers. It's about setting new benchmarks, pushing boundaries, and cashing in on cures in the most spectacular way possible.

So, if you're wondering where the smart money is heading in the biotechnology arena, following Eli Lilly's trail might just lead you to a treasure trove of opportunities. I suggest you buy the dip.

Global Market Comments

February 9, 2024

Fiat Lux

Featured Trade:

(FEBRUARY 7 BIWEEKLY STRATEGY WEBINAR Q&A),

(LLY), (FXI), (TSM), (BABA), (PLTR), (MSBHF), (SMCI), (JPM), (INDY), (INDA), (TSLA), (BYDDF), (NFLX), (META), (UNG)

Below please find subscribers’ Q&A for the February 7 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: Have you ever flown an ME-262?

A: There's only nine of the original German jet fighters left from WWII in museums. One hangs from the ceiling in the Deutsches Museum in Munich (click here for the link), I have been there and seen it and it is truly a thing of beauty. You would have to be out of your mind to fly that plane, because the engines only had a 10 hour life. That's because during WWII, the Germans couldn't get titanium to make jet engine blades and used steel instead, and those fell apart almost as soon as they took off. So, of the 1,443 ME-262’s made there’s only nine left. The Allies were so terrified of this plane, which could outfly our own Mustangs by 100 miles per hour, that they burned every one they found. That’s also why there are no Japanese Zeros.

Q: Thoughts on Palantir (PLTR) long term?

A: I love it, it’s a great data and security play. Right now, markets are revaluing all data plays, whatever they are. But it is also overvalued having almost doubled in a week.

Q: What do you make of all these layoffs in Silicon Valley? What does this mean for tech stocks?

A: It means tech stocks go up. The tech stocks for a long time have practiced over-employment. They were growing so fast, they always kept a reserve of about 10% of extra staff so they could be put them to work immediately when the demand came. Now they are switching to a new business model: fire everybody unless you absolutely have to have them right now, and make everybody you have work twice as hard. That greatly increases the profitability of these companies, as we saw with META (META), which had its profits triple—and that seems to be the new Silicon Valley business model. If you're one of the few 100,000 that have been laid off in Silicon Valley, eventually the economy will grow back to where they can absorb you. That's how it's going to play out. In the meantime, go take a vacation somewhere, because you're not going to get any vacations once you get a new job.

Q: I have had shares of Alibaba (BABA) since 2020 and the stock has been in free fall since. Should I take the 80% loss or hold?

A: Well, number one, you need to learn about risk control. Number two, you need to learn about stop losses. I stop out when things go 10% against me; that's a good level. At 80%, you might as well keep the stock. You've already taken the loss and who knows, China may recover someday. It's not recovering now because no foreigners want to invest in China with all the political risk and invasion risk of Taiwan. After all, look at what happened to Russia when they invaded Ukraine—that didn't work out so well for them.

Q: On the Chinese economy (FXI), is the poorer performance due to the decision to move to a war economy? The move in the economic front was described in Xi's speech to the CCP in January of 2023.

A: The real reason, which no one is talking about except me, is the one child policy, which China practiced for 40 years. What it has meant is you now have 40 years of missing consumers that were never born. And there is no solution to that, at least no short-term solution. They're trying to get Chinese people to have more kids now, and you're seeing three and four child families for the first time in 40 years in China. But there is no short-term fix. When you mess with demographics, you mess with economic growth. We warned the Chinese this would happen at the time, and they ignored us. They said if they hadn't done the one child policy, the population of China today would be 1.8 billion instead of 1.2 billion. Well, they’re kind of damned no matter what they do so there was no good solution for them. Of course, threatening to invade your neighbors is never good for attracting foreign investment for sure. Nobody here wants to touch China with a 10-foot pole until there’s a new leader who is more pacifist.

Q: What do you think of Eli Lilly (LLY)?

A: I absolutely love it. If there's a never-ending bull market in fat Americans, which is will go on forever, they're one of two companies that have the cure at $1,000 a month. On the other hand, the stock has tripled in the last 18 months, so it’s kind of late in the game to get in.

Q: Are there any stocks that become an attractive short in the event of a Taiwan invasion, such as Taiwan Semiconductor (TSM)?

A: All stocks become attractive shorts in the event of another war in China. You don't want to be anywhere near stocks and the semis will have the greatest downside beta as they always do. You don't want to be anywhere near bonds either, because the Chinese still own about a trillion dollars’ worth of our bonds. Cash and T-bills suddenly looks great in the event of a third war on top of the two that we already have in Gaza and Ukraine.

Q: What do you think about the prospects of the Japanese stock market now?

A: I think the big move is done; it finally hit a new high after a 34-year wait. The next big move in Japan is when the Yen gets stronger, and that is bad for Japanese stocks, so I would be a little cautious here unless you have some great single name plays like Warren Buffett does with Mitsubishi Corp. (MSBHF). So that's my view on Japan—I'm not chasing it after being out for 34 years. Why return? The companies in the US are better anyway.

Q: What is the deal with Supermicro Computer (SMCI)? It went up 23 times in a year to $669 after not clear $30 for a decade.

A: The answer is artificial intelligence. It is basically creating immense demand for the entire chip ecosystem, including high end servers, which Supermicro makes. It also has the benefit of being a small company with a small float, hence the ballistic move. It was too small to show up on my radar. I’ll catch the next one. There are literally thousands of companies like (SMCI) in Silicon Valley.

Q: Will JP Morgan (JPM) bank shares keep rising, or will they fall when the Fed cuts rates?

A: (JPM) will keep rising because recovering economies create more loan demand, allow wider margins, and cause default rates to go down. It becomes a sort of best case scenario for banks, and JP Morgan is the best of the breed in the banking sector. It also benefits the most from the concentration of the US banking sector, which is on its way from 4,000 banks to 6 with help from the US government.

Q: Is India a good long-term play? Which of the two ETFs I recommend are the better ones?

A: Yes, India is a good long-term play. You buy both iShares India 50 (INDY) and the iShares MSCI India (INDA), which I helped create yonks ago. India is the new China, and the old China is going nowhere. So, yes, India definitely is a play, especially if the dollar starts to weaken.

Q: Do you expect to pull back in your market timing index?

A: Yes, probably this month. Have I ever seen it go sideways at the top for an extended period? No, I haven't. On the other hand, we’ve never had a new thing like artificial intelligence hit the market, nor have we seen five stocks dominate the entire market like we're seeing now. So, there are a lot of unprecedented factors in the market now which no one has ever seen before, therefore they don't know what to do. That is the difficulty.

Q: Does India have an in-country built EV, and what is their favorite EV in India?

A: No, but Tesla (TSLA) is talking about building a factory there. And I would have to say BYD Motors (BYDDF) because they have the world’s cheapest EV’s. There is essentially no car regulation in India except on imports. Car regulation and safety requirements is what keeps the BYDs out of the United States, and it's kept them out for the last 15 years. So that is the issue there.

Q: What do you think about META as a dividend play?

A: I think META will go higher, but like the rest of the AI 5, it is desperately in need of a pull back and a refresh to allow new traders to come in.

Q: Why does Netflix (NFLX) keep going up? I thought streaming was saturated—what gives?

A: Netflix won the streaming wars. They have the best content and the best business strategy; and they banned sharing of passwords, which hit my family big time since it seemed like the whole world was using my Netflix password. And no, I'm not going tell you what my password is. I’ve already paid for Griselda enough times. Seems there is a lot of demand for strong women in my family. Netflix they seem to be enjoying a near monopoly now on profits.

Q: Has the NASDAQ come too far too fast, and does it have more to run?

A: Well it does have more to run, but needs a pull back first. I'm thinking we'll get one this month, but I'm definitely not shorting it in the meantime.

Q: Have you ordered your Tesla (TSLA) Cybertruck?

A: I actually ordered it two years ago and it may be another two year wait; with my luck the order will come through when I'm in Europe and I'll miss it. Some of my friends have already gotten deliveries because they ordered on day one. They love it.

Q: What happened to United States Natural Gas (UNG)?

A: A super cold spell hit the Midwest, froze all the pipes, and nobody could deliver natural gas just when the power companies were screaming for more gas. That created the double in the price which you should have sold into! Usually, people don't need to be told to take a profit when something doubles in 2 weeks, but apparently there are some out there as I've been here getting emails from them. Further confusing matters further is that (UNG) did a 4:1 reverse split right at this time. They have to do this every few years or the 35% a year contango takes the price below $1.00 and shares can’t trade below $1.00 on the New York Stock Exchange.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech and Healthcare Letter

February 8, 2024

Fiat Lux

Featured Trade:

(THE WEIGHT IS OVER)

(REGN), (NVO), (LLY), (RHHBY)

Let's look into something that's been buzzing in the healthcare sector, and no, I'm not just talking about the latest diet fad. I’m talking about obesity treatments — specifically, those groundbreaking drugs that are reshaping the market and, quite literally, the patients using them.

Yes, I'm looking at you, GLP-1 agonists. These bad boys have been making waves for their significant role in weight loss, but let's face it, there's always room for a bit of an upgrade, right?

Despite all the cheers and positive vibes around GLP-1 agonists, a little detail has been creeping up that's somewhat less than ideal — muscle loss.

It turns out, up to a whopping 40% of the weight shed isn't just fat saying goodbye, but muscle bidding adieu as well. Not exactly the parting gift patients were hoping for, and frankly, it's stirring up some concerns that could ripple through public health in the not-so-distant future.

This is where Regeneron (REGN) comes in.

This biotechnology company isn’t new to the scene, but it’s taking a fresh angle on the whole ordeal. Their game plan? A dynamic duo approach, combining trevogrumab or garetosmab with the well-known semaglutide (hello, Wegovy), aiming to refine the weight loss journey for those embarking on it.

Regeneron’s goal is clear: let's keep the muscle, lose the fat, and change the narrative on obesity treatments.

Now, for a little context, the obesity treatment arena has been somewhat monopolized by Novo Nordisk (NVO) and Eli Lilly (LLY), with their respective champions, Wegovy and Zepbound, leading the charge.

But here's where Regeneron is looking to carve out its niche, not just in improving the now but in eyeing the future post-treatment landscape. The million-dollar question they're tackling: once the weight's off, how do you keep it from coming back without those weekly jab appointments?

To know the answer to that question, I suggest you mark your calendars for May 2024 because that's when the magic starts. It will commence Phase 2 of the study aiming to test Regeneron’s combo and hopefully offer better results to the weight loss game.

Ultimately, the company aims to preserve, or even boost, muscle mass. Imagine that, weight loss without the unwanted goodbye to your gains.

While it's worth noting that while Regeneron is making waves with its innovative approach, they're not alone in the quest for muscle preservation. Other players are also in the mix, each with their own strategies to combat the side effects of GLP-1 agonists.

Roche (RHHBY), for instance, has set its sights on combining their anti-myostatin antibody with incretin treatments, expanding the battlefield into new territories.

However, Regeneron’s plans don’t end in the weight loss world.

Earlier this month, Regeneron threw another curveball with the acquisition of 2seventy bio's cell therapy pipeline. This move isn't just about expanding their arsenal; it's about integrating and innovating in ways that could redefine cancer treatment as we know it.

By blending Regeneron's antibody expertise with 2seventy's cell therapy prowess, they're transforming into a potential oncology powerhouse.

Now, let's look at the numbers. Regeneron's market cap is flirting with the $100 billion mark, proof of their performance and potential. With revenues dancing around the $13 billion mark for 2023 and a price-to-sales ratio that's eye-catching, to say the least.

Yet, with every high, there's a looming challenge. The patent cliff for Eylea, their golden goose, is on the horizon, threatening to shake up the status quo.

But if there's one thing Regeneron has shown us, it's their knack for innovation. Given everything the company has embarked on over the past months, it’s safe to say that they’ve got this issue covered.

Does that mean it’s time to yell "screaming buy" from the rooftops? I usually keep such big words under lock and key, but Regeneron? They're onto something. They're not just surviving; they're plotting a course to new horizons without putting all their eggs in one basket. That strategy? It's more than just good—it's golden.

So while the cautious among us might wait for the market to blink first, there's something to be said for getting ahead of the curve. After all, in the world of pharma, timing is everything, and Regeneron seems to have its clock set just right.