Mad Hedge Technology Letter

October 17, 2022

Fiat Lux

Featured Trade:

(THE BIG TALK)

(SOXX), (CHINA), (NVDA), (MU), (LNG)

Mad Hedge Technology Letter

October 17, 2022

Fiat Lux

Featured Trade:

(THE BIG TALK)

(SOXX), (CHINA), (NVDA), (MU), (LNG)

A lot of people haven’t talked about what’s going on in China. Other world events have lessened the focus in the East.

Yet people should be talking about China now.

Authoritarian China is a way bigger deal than what’s happening in the backwaters of Eastern Europe, and I’ll explain.

What on earth could overshadow all of that?

The US administration announced Chinese semiconductor bans, essentially blocking the transfer of intellectual property to China and forcing American executives to quit en masse or face the risk of losing US citizenship.

To say this is escalatory is an understatement.

Remember that previous US president Donald Trump forced the same interests to apply for special licenses, but never ramped up the tension to fever pitch and allowed business to advance.

The result is every American executive and engineer working in China’s semiconductor manufacturing industry resigning, paralyzing Chinese manufacturing overnight.

When combined with a global demand reduction, this is a heavy blow to the short-term prospects of American chip companies (SOXX) that have deep interests in China such as Applied Materials, Intel, Micron (MU), Nvidia (NVDA) and AMD.

US Commerce department also levied a bevy of restrictions on supplying US machinery that’s capable of making advanced semiconductors. It’s going after the types of memory chips and logic components that are at the heart of state-of-the art designs.

For companies with plants in China, including non-US firms, the rules will create additional hurdles and require government signoff.

South Korea’s SK Hynix Inc. is one of the world’s largest makers of memory chips and has facilities in China as part of a supply network that sends components around the world.

The biggest name to be added to the list ban is Yangtze Memory Technologies Co. The memory-chip maker is considered the most successful chip company in China wielding the best technology obviously thanks to American technology.

I found it interesting that at almost the same time, China instructed local resellers to stop selling liquid natural gas (LNG) to Europe as mounting proof China views Europe and America through the same lens.

The rapid escalation means the fragmenting of the United States economy and China will accelerate into the future resulting in the inevitable on-shoring of American chip factories back to the United States which we are already seeing.

Other industries will need to be on-shored back to United States and other friendly countries too.

In the short to mid-term, this means higher costs for the American chip companies as reinvesting into capital projects are a multi-billion dollar proposition.

Also, the pain of losing the large China market hurts badly for the stock and is damaging to the annual revenue outlook.

Expect many revenue downgrades coming down the pipeline.

Inflationary costs is another driver of revenue downgrades too as paying these specialists and keeping the lights on have gotten more expensive.

The chip companies won’t be able to substitute the China demand when we are on the verge of recessions in the United States and Europe.

Ultimately, the infamous boom-bust cycle for the chip stocks will get a more prolonged bust this time around as demand and supply are both painfully reduced.

The boom also will be larger because of coming from a lower cost basis.

However, I would highly doubt a bounce back of any chips stocks in the short-term unless broader market forces drag up stocks which could happen.

We will most likely experience strong bear market rallies met by thundering selloffs.

I would avoid any long term investments into chip companies now and just trade the bounces short-term.

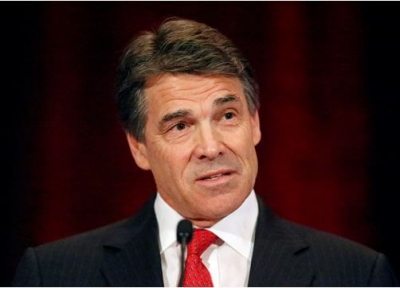

Given that my friend, former Texas Governor, Rick Perry, was nominated for the position of Secretary of Energy yesterday, I thought I would recount a dinner I had with him.

The irony is great since Rick promised to close down the agency while campaigning for president in 2012.

It confirms my suspicion that many of the people Trump is appointing have the mission to destroy the agencies they will head.

As a precondition to joining a dinner with the former Texas governor, I had to promise a few things.

I was not allowed to bring up the fact that he shoots coyotes while jogging. I couldn?t mention statistics proving that 70% of the jobs created in his state during his 12-year tenure as governor were government, not private.

Having agreed to all of that, I was told, ?Sure, come along, we?d love to hear your questions and your insights.?

Perry was making his 12th?visit to the Golden State in the past two years to convince local companies, plagued with onerous taxes, stringent regulations and high operating costs, to pull up stakes and move camp to the Lone Star State.

When I first shook hands with the governor, I was surprised at how short he was. But then he wasn?t wearing the three-inch heeled cowboy boots that normally elevated him at home.

Then I mentioned my secret words: ?Go Aggies.? He recoiled.

?How did you know?? he demanded.

I told him that during the early 1970s, I drove my sister from California to his home state so she could attend Texas A&M University. Perry was a cadet then, and I speculated that they had probably dated.

He answered, ?Nah, I didn?t play around much in those days.?

Probably not.

But after that, he melted, only engaging me in serious conversation, while sticking to canned, stock answers to questions from everyone else.

I was Rick Perry?s new best friend.

As he spoke, I realized that he was much more reasonable in his views than when appealing to his ultra conservative base back home. That is simply the mark of a savvy and successful politician.

Perry said that the country needs both states to lead change and succeed, and that he rooted for California to do well.

The governor was still basking in the glow of Toyota?s recent announcement that it was moving 3,000 jobs from Long Beach, California to Texas.?

It has been a controversial win for him, as his state is paying $10,000 in subsidies per person to lure the white-collar work force.

I spoke to Toyota USA CEO, Jim Lentz, about this recently. He said the real reason had to do with working in the same time zone as the company?s large manufacturing facilities in Kentucky and Tennessee.

A lower cost of living, cheaper rents, and discount labor costs were also issues. Lower taxes were at the bottom of a list of ten priorities.

Past experience has shown that most departing workers, fleeing from California, return after three years. It seems the summer heat and humidity kill them.?

Thus chastened, they are more than willing to pay a premium for the lifestyle here, despite the higher taxes and earthquakes.

Perry says the US needs an ?all of the above? solution to its energy problems. It is not a good idea to be dependent on foreign energy sources, especially from unstable countries.

Despite its stereotype as an oil-based economy, Texas was now the top producer of wind power in the country. The installed base there now exceeds 12 gigawatts, making it the fifth largest in the world.

My friend, T. Boone Pickens, has been a major investor in wind power generation there.

An aggressive approvals process made possible the construction of long distance transmission lines needed to send it to other states and eventually to California itself, thus creating a national market for wind power.

The governor says that Texas will become a major exporter for liquefied natural gas within the next two years. Cheniere Energy (LNG), the front-runner in the field, has been a favorite recommendation of mine for the past five years, and? Trade Alert followers have chased the shares up from $6 to $70.

Despite the controversy over fracking wells polluting fresh water supplies, Perry says there has not been a single incidence of this occurring in Texas. This is no doubt a result of the state?s ferocious regulation of the energy industry, of which I, myself, have no small amount of experience.

Thanks in part to new federal regulations, air pollution has fallen dramatically in Texas. Ozone emissions have dropped by 23% since 2000, while nitrous oxides are off by 57%.

These, and other measures have enabled the US to cut its dependence on foreign oil imports from 33% to 15% since 2000. During the same period, natural gas production, which produces half the carbon of oil based fuels, has soared by 57%.

At that point, another guest raised his hand and asked his stance on gay rights. Perry opined that sexuality was a choice that could be controlled, and that gay marriage would never get his support. An audible hiss was heard in the roomwhich Perry stonily ignored.

That invited the question about the legalization of marijuana. He simply said that it would never be legalized in his state, and, ?If people want to get high, they can go to Colorado.?

Finally, a woman at the table asked about reproductive rights. When Perry said that he was proud to sign a Texas law limiting termination to the first five months of pregnancy, murmurs were heard. The law is not expected to survive a pending challenge at the Supreme Court.

Another attendee queried his view of Hillary Clinton. I braced myself. He then surprised me by saying that he thought she was ?a very capable Secretary of State and a great public servant.?

That spoke volumes to me. It meant that with access to all his private polling data, Rick Perry thought that Hillary would win the 2016 presidential election. As the astute politician that he is, Perry doesn?t want to burn his bridges.

Perry likes to tell people that he is probably the last governor who used an outhouse on a dry cotton farm near Abilene, West Texas.

He became an Eagle Scout and I confirmed this with the secret scout handshake.

He earned a degree in animal science at Texas A&M where he was also a Corps Cadet and a yell leader. His first part-time job was as a door-to-door salesman. When he graduated, he joined the Air Force and became a C-130 pilot.

Perry originally started in politics as a Democrat, getting elected to the Texas House of Representatives in 1984.

He worked on Al Gore?s presidential campaign in 1988. This was back when Southern Democrats were more conservative than the right wing of the Republican Party.Perry became a Republican in 1989.

He moved up to the governorship in 2000, when sitting governor George W. Bush was elected president. Perry has been reelected three times, making him the longest tenured Texas governor in history.

Perry said that his time spent as the front runner in the 2012 presidential election ?were the three most exhausting hours of my life.?

He then repeated his ?Oops? moment when, if elected, he couldn?t remember the third government department he would close (it was the Department of Commerce, in addition to Energy and Education). That was probably to head off someone else bringing it up first.

I told the governor I knew two facts about our respective states which I bet he didn?t know. He asked what they were.

I responded that California and Texas were the only two states that had been independent countries before joining the Union. California had been the Bear Flag Republic for six months until mid 1848, while the Republic of Texas stood on its own for a decade, until 1846. Texans have been regretting joining the Union ever since.

Today, the two states make up 19.1% of America?s GDP, and 20.4% of its population.

The other mystery fact was that while Texas was independent, it maintained an embassy in London, England on St. James Street.Today, the space is occupied by a pub and is across the street from the Ritz Hotel and next door to my old office at The Economist?magazine headquarters. Perry said he?d check it out on his next visit there.

As the dinner wound down, I asked the governor if he had ever driven a Tesla Model S-1. He said he hadn?t. I asked if he would like to because my own high performance model was conveniently parked out front. He said he?d love to.

At that point, the plain clothed Texas Rangers who accompany him as bodyguards noticeably tensed up.

I have some experience providing quick tutorials for the uninitiated on how to drive this incredible electric car from the future. My chassis number is 125 out of a fleet of 45,000 and is one of the oldest S-1s around.

Newcomers invariably underestimate the car?s power and acceleration, which works out to about 450 horsepower in the carbon world. This can be unexpectedly dangerous for newbies.

With some careful coaching, Perry gingerly drove the car a few times around San Francisco?s Huntington Park, atop Nob Hill with two nervous, but heavily armed, Rangers in the back seat.

When we carefully turned back onto California Street and came to a stop in front of the Mark Hopkins Hotel, Perry pronounced the vehicle ?a marvelous piece of technology?.

With that, Perry invited me to visit the governor?s mansion the next time I visited Austin, Texas.

I said I?d be honored, and silently drove my Tesla off into the night, thus christened by a true Texan.

You Want Me to Do What?

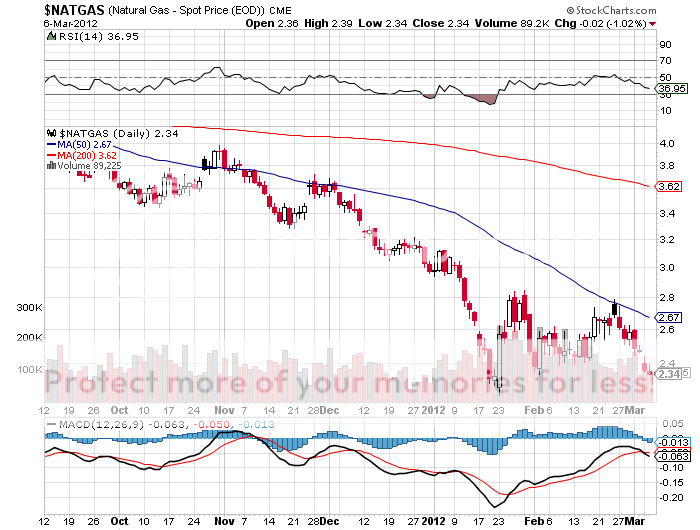

I am constantly asked if there are any ways investors can take advantage of the current collapse in natural gas prices.

You don?t want to touch the gas producing companies, like Chesapeake (CHK) and Devon (DVN), because prices for natural gas are probably going to stay down for years.

Good firms that benefit from the increased volume of gas pumped are few and far between. Unless you are a large consumer of this despised molecule, such as an electric power company or a petrochemical plant, it is tough to find a profitable niche.

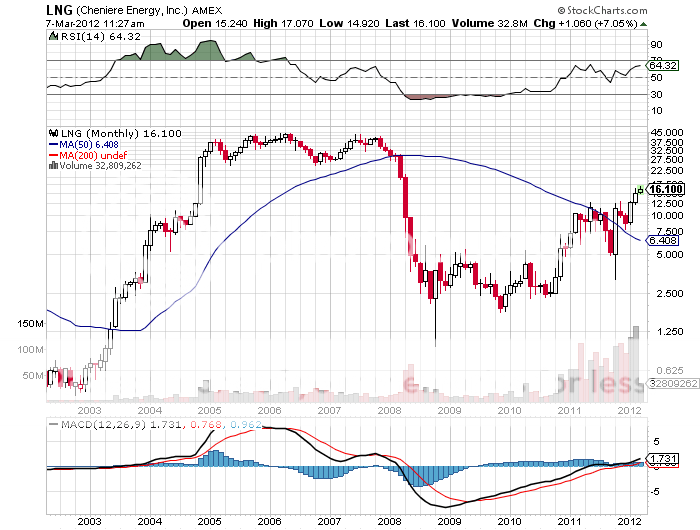

However, there is one company that delivers a narrow rifle shot that will do extremely well in coming years, and that is Cheniere Energy (LNG).

I first started following (LNG) two decades ago when I was still wildcatting for CH4 in the Texas Barnet Shale.

Back when natural gas was trading at a lofty $5/MBTU, Qatar invested $50 billion in developing its own massive gas resources.

The plan was to liquefy the gas at -256 degrees Fahrenheit in the Middle East, ship it to the US in a fleet of specialized LNG carriers, and have Cheniere convert it back into gas at its Sabine River plant for distribution to an energy hungry US market through the Creole Trail pipeline.

It all looked like a great plan, and (LNG) shares traded up to $45.

Then ?fracking? technology came along and blew up the entire model. The discovery of a new 100-year supply of gas under our feet caused gas prices to crash from a post Amaranth peak of $17/MMBTU down to $2/MMBTU.

Any plans to import LNG from the other side of the world were rendered utterly worthless. Qatar ended up selling its gas to Europe insteadto help offset that continent's over reliance on imports from Russia.

Chenier?s billion-dollar investment in a gasification plant was now worth only so much scrap metal. (LNG) shares plumbed to low single digits as the firm flirted with bankruptcy.

Enter China.

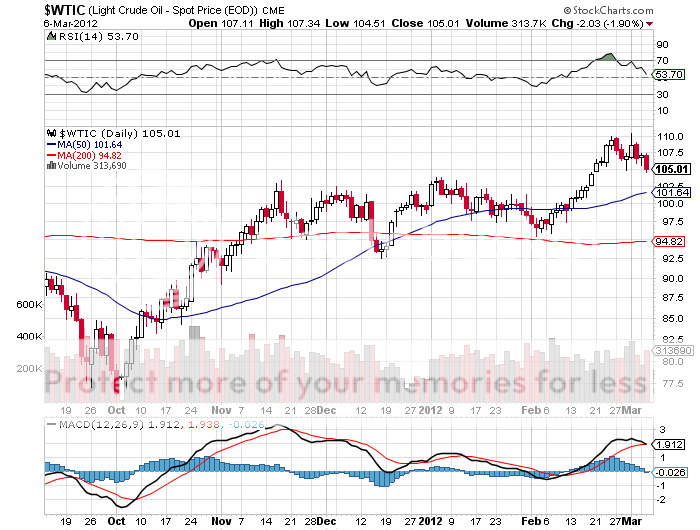

The Middle Kingdom?s voracious demand for energy in this recovery has caused the price of oil (USO) to soar from a 2008 low of $30 to $112.

Despite accounting for an overwhelming share of the world?s new energy purchases, Chinese cities are suffering from brown outs due to power shortages.

This is why China is resisting immense American pressure to quit buying Texas tea from Iran.

Enter the arbitrage. While oil has been plummeting, gas has been falling even more. Gas is now selling at 25% of the cost of oil on an adjusted BTU basis.

Another way of saying this is that you can buy oil for $12 a barrel instead of $48. It only takes a second with an abacus to understand the appeal of such a disparity.

Gas also has the additional benefits in that it is much cleaner burning than crude, lacks the sulfur and nitrogen dioxides, and produces half the carbon dioxide. That?s a big deal in Beijing where the air is so thick you can cut it with a knife on a bad day.

It is also important to know that many states, like California have decided to use natural gas as a bridge fuel until more economic and scalable alternatives are developed.

Enter the long-term contracts. During the 1960?s and 1970?s Japan entered into huge long term contracts to buy LNG from Australia and Indonesia to feed their own economic miracle of the day.

Because it is very expensive and hard to get, offshore supplies were tapped, the price was set at $16/MBTU. Those contracts are now expiring.

Do you think they?ll renew at the old price, or go to Cheniere for the $4 stuff? Gee, let me think about that one for a bit.

Enter Fukushima. The nuclear meltdown on March, 2011 prompted Japan to shut down 49 of 54 nuclear power plants that accounted for 25% of the country?s electric power generation. The brownouts that followed forced a sweltering summer on millions as the government urged consumers to shut off air conditioners to save juice.

Power companies there have been scrambling to obtain conventional energy supplies, and cheap gas supplies from the US would meet this demand nicely.

The trigger.

Cheniere obtained US government permission to export 2.2 billion cubic feet a day for 20 years. That would require it to convert the existing gasification plant to a liquefaction plant, something that can be done with some expensive re-engineering. A second plant is in the approval process.

It has already found several large international buyers to take delivery of the new end product. All that was missing was the money to finish the plant.

My hedge fund buddies have been accumulating this stock when it bottomed at $3, expecting an angel investor to appear. But it was one of those ?someday, it might happen? kind of stories better left to long-term players.

Then Blackstone jumped in with a beefy $2 billion investment in Cheniere. That will enable them to obtain an additional $3 billion in debt financing needed to finish the first of two export facilities. They are now expected to come online in 2016.

How does Cheniere stack up as an investment? Frankly, it is kind of scary. The market cap is only $11.3 billion, it has no earnings yet, and it pays no dividend. When the current spate of deals are done, it will have $5 billion in debt.

I first got followers into (LNG) at $5. We then had a great run all the way up to $85, and we took profits. In the current melt down, it has backed off all the way down to $45, a 47% hickey.

And these facilities are dangerous to operate. One blew up in Texas in 1937 and killed 300 schoolchildren.

As a result, local permits for these are very hard to come by. Anyone who thinks Texas is an unregulated paradise should try drilling for natural gas.

But as you can see a whole host of geopolitical, technology and economic strands reach a nexus in this one company, all of which are extremely positive for the share price.

If the story comes true, as Blackstone hopes, then there could be a double or triple in the shares for the patient. To learn more about Cheniere Energy, please go to their website: http://www.cheniere.com.

Did Somebody Light a Match?

Did Somebody Light a Match?

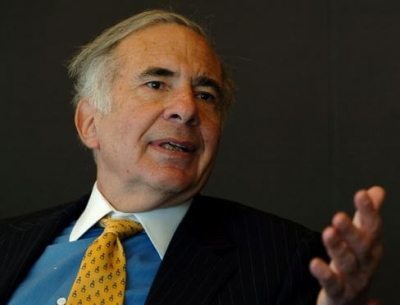

Many ascribe Monday?s 312 point plunge in the Dow Average to an informational webinar posted by legendary corporate raider and hedge fund manager, Carl Icahn.

I have known Carl for 30 years, and I once owned and apartment in his building on the Upper East Side of Manhattan, near Sutton Place (which I later sold for a quick double).

Even then, he was opinionated, cantankerous, and never hesitated to make the bold move. Wall Street hated him.

At 79, he is nothing less than a force of nature. Whenever I see Carl, I say I want to be like him when I grow up.

I just watched the controversial video, entitled ?Danger Ahead ? A Message From Carl Icahn?, which has ruffled more than a few feathers in the establishment. But that has always been Carl?s strong suite.

Here are the high-points:

1) We should end the ?carried interest? treatment of hedge fund profits, which lets billionaire managers get off scot-free, while sticking a big tax bill with the little guy.

2) Foreign profits of US multinationals, some $2.2 trillion, should be brought home, taxed, and put to work.

3) Corporate inversions, whereby American companies reincorporate overseas to beat taxes, should be banned.

4) Corporate share buybacks, which amount to 4.5% of the outstanding float per year, are a short-term fix for company share prices only at the long-term price of a weaker balance sheets.

5) Some $4.5 trillion in borrowing by the Federal Reserve has crowded out the little guy. On this one, I disagree with Carl. With overnight rates at zero and ten year Treasury bonds yielding 2.06%, nobody is getting crowded out from anything.

6) Artificially low interest rates are fueling an unwarranted takeover boom and encouraging risky financial engineering.

7) Junk bonds (HYG), (JNK) are a bubble begging to pop. They are the result of a runaway Wall Street selling machine that saw big firms selling short their own issues to unwary customers.

Carl sums up by saying that while the Fed saved the US economy during 2008-09, they created the problem in the first place with Greenspan?s excessive easing in 2002-03.

He believes that the candidacy of outsider Donald Trump is a natural reaction to peoples? dissatisfaction with Washington and Wall Street.

I have to admit that Carl has brought up some serious points here. I agree with all, except the above-mentioned ?crowding out? issue. Combined, they are a detrimental tax on the long-term economic health of America.

Could this be an attempt by Carl to throw his hat into the political ring? Treasury Secretary in a future Trump administration was mentioned in later media interviews.

But at his age, even for Carl, that would be a reach.

While Icahn has been ringing the alarm bell on the stock market and junk bonds all year, he has been aggressively acquiring major stakes in in the energy and commodities sectors all year, while they are trading at generational lows.

He has zeroed in on two of my own favorite trades, Freeport McMoRan (FCX) and Cheniere Energy (LNG).

Carl is also holding a major position in Apple (AAPL), which he acquired two years ago just after I jumped in at $395. He believes the shares are absurdly cheap.

To watch the 15 minute video in full, please click: http://carlicahn.com.

Good for you, Carl Icahn!

Sell the shovels to the gold miners. That was the lesson of the 1849 California gold rush.

How many individual gold miners can you name today? How about none, unless you are an expert on the obscure street names of San Francisco.

And the companies that sold supplies and services to them? Try Wells Fargo (WFC), Bank of America (BAC), Union Pacific (UNP), and Levi Strauss. Some 165 years later, they not only survive, they thrive. This is the lesson that I remind readers of when they flock to me for advice on where to make money in the current natural gas fracking boom (UNG), (USO).

They do so because I was a pioneer in this revolutionary technology 15 years ago, driving down the endless washboard roads of the Barnet Shale in West Texas to lock up leases on depleted fields for pennies on the dollar. It turns out that there was still more gas and oil down there than had ever been extracted from the original wells. Kaching!

The problem, as it always is in radical new emerging technologies, is that it is tough for the outsider to participate. Fracking still only accounts for a tiny share of the profits of majors like Exxon Mobil (XOM) and Chevron (CVX).

The small plays have already risen tenfold, such as my recommendation for Cheniere Energy (LNG) (click here to read ?Revisiting Cheniere Energy (LNG)?). Much of the rest is privately held and closed to outside investors.

The last thing in the world you want to do is go out and buy natural gas itself. Why buy a commodity just when the supply is massively ramping up? So, how is the ordinary guy to get in on the ground floor of this modern day bonanza?

The other day I got a call from one of my old drilling buddies, who has since moved on to the Eagle Ford Shale in East Texas. You know, the one with the oil permanently stuck under his fingernails and a deeply tanned face that looks like an old saddle?

He said that the industry is facing a major problem in that the new fields are often in the middle of nowhere, lacking even the most basic infrastructure. Housing is non-existent and workers in scarce supply. Civilization in Texas, like the towns, is found around the geology of traditional oil, usually under giant underground salt domes. Oil shale is a different story.

Their choice now is to tell workers to bring their own recreational vehicles to live in the boondocks, or endure four-hour daily commutes. When you are paying your blue-collar workers $200,000 a year, you don?t want them spending half of their day on a bus listening to an iPod, watching videos, or staring blankly out at the desolate landscape. Obviously, families don?t fit anywhere in this picture.

My friend told me about a company called InVision Housing Solutions Management LLC that had come up with a great means for solving this vexing problem, carving out a highly lucrative niche for themselves. It is in the business of building and leasing out temporary housing for oil workers.

These are not the dreaded, ticky tacky mobile home parks of old, but high-end affairs, complete with pleasant grounds, high-end finishes, and generous common amenities. When workers are earning well into triple digits, they expect better accommodations.

Their primary customers are leading companies you all know and love, like Chesapeake (CHK) and Halliburton (HAL), which are opening up new oil and gas fields as fast as they can get the permits. These firms are more than happy to pay lease rates of $100 a day or more, or what you might expect to pay for a mid level hotel in a major city.

Then my friend really got my attention. He said that InVision?s existing facility, the ?Double C Resort,? was getting occupancy rates of 75% or more, usually on long-term leases, something a major hotel chain would kill for. This was enabling it to earn net returns on its investment for outside investors up to an eye popping 20% a year, or better.

The story gets better. The project is scalable. The Double C Resort is just one of 20 locations in Texas where the supply/demand dynamics favor similar developments. Beyond that, it could expand nationally to service fields as far away as North Dakota and California.

InVision can build a town with 300 units for $15 million, including the roads, utilities, sewers, Wi-Fi, etc. Operational expenses are minimal, so after the initial build out you are left with a big cash flow machine on your hands. You do the math.

What happens when the new fields get fully developed? For a start, these new natural gas fields are much larger than people realize. Once the primary gas pocket at 5,000 feet is emptied, there are more at 7,000, 9,000, 11,000, 13,000, 15,000 feet and more.

The same fields will get drilled over and over again for years to come. When they say that a century?s worth of cheap energy has just been discovered, they?re not kidding.

There will also always be continuing demand for housing to service the new infrastructure, such as the pipelines. After that, the housing is so portable that it can simply be placed on a flatbed trailer and moved elsewhere.

InVision is not a public company, but is accepting outside investors with a minimum $50,000 stake. Besides the generous cash flow, if the company ever does go public at some point in the future, you would then get the earnings multiple bump up in the value of your asset.

To get more information about InVision Housing Solutions Management LLC please, visit their website at http://invisionhousing.com . You can also contact, Tom Tamrack, directly at info@invisionhousing.com, or call him at 888-516-2221.

Perhaps an Investment Opportunity?

Perhaps an Investment Opportunity?

If there is one complaint about the Diary of a Mad Hedge Fund Trader, it is that I am too short term in my orientation. My response is that this is the only way you can obtain a 138% trading return in 3 ? years. I can skim off the cream when others can?t.

There is a reason why we are the only investment newsletter that publishes our performance on a daily basis. Basically, all our competitors lose money for their readers. It?s a lot like those Japanese restaurants that display plastic models of their food in the front window.

Still, I like to throw readers ten baggers when I find them. Long-term followers get that warm and fuzzy feeling when I mention Baidu (BIDU) ($12 to $190), Cheniere Energy (LNG) ($5 to $68), Molycorp ($12 to $80), and Tesla (TSLA) ($16 to $260) for a good reason.

Well, I found another ten bagger, one you can just buy and forget about for the next three to five years. I discovered this jewel at the SALT conference in Las Vegas last month organized by my friend, Anthony Scaramucci (click here for ?The Report on the 6th Annual Skybridge Alternatives (SALT) Conference?).

At the keynote dinner, I randomly picked a table near the stage. One of the couples next to me wore a UCLA pin from where she graduated, prompting a discussion of the Golden age of Bruin basketball and the salad days of? legends John Wooden and Bill Walton (four perfect 30-0 seasons and an 88 game winning streak!).

I casually mentioned I was there as a cancer researcher and DNA scientist during the early 1970?s, and graduated in biochemistry. The ears perked up, and the dam broke.

The gentleman I was dining with turned out to be the CEO of CytRx Corp. (CYTR) a revolutionary innovator in the chemotherapy field. Through a top secret, patented chemical reaction, their chemists can add an acid sensitive linker molecule to pre existing generic chemotherapy drug.

That enables the drug to only kill the cancer cells and not the rest of you as well, eliminating side effects, and permitting a substantial ramping up of the dosage. I worked out the chemistry in my mind, and quickly figured out that it would work.

The net effect is to install a turbocharger on existing drugs, greatly enhancing their curative effects. Stage three trials will be completed by 2016, when the company expects full FDA approval. The company has $125 million in cash and no debt.

I lost a wife to cancer 12 years ago, and received a crash update on the state of the science then. I have been following it ever since, awaiting my turn. If CytRx is able to pass the FDA gauntlet, then they have found the Holy Grail. Best of all, the shares have just suffered a 67% pullback, thanks to the spring biotech meltdown.

To learn more about the company and obtain the details, please visit their website: ?http://www.cytrx.com .

Curing of cancer during the 2020?s is a major part of my Golden Age scenario for the coming decade (click here for ?Here Comes the Next Golden Age?).

The kicker here is that there is not just one, but hundreds of companies developing ground-breaking treatments that will come out in the years ahead, many of them just across the bridge from me. This should collapse the cost of health care for the government, and the rest of us as well.

I knew I would live forever!

Remember that buying the shares of a drug company before final approval is always a crapshoot. The last time I did this was with Genentech?s (DNA) Avastin, because I was dating the senior researcher there at the time (tall, long legs, brilliant).

The shares doubled the day they got the green light, and Bank of America flipped from a ?SELL? to a ?BUY? recommendation for the stock on top of a $30 move, tail between legs. That was good.

As we parted ways, the CEO even pushed over his desert, from which his doctor forbade him for health reasons. I gobbled that up as well.

Is CytRx (CYTR) Another Ten Bagger?

Is CytRx (CYTR) Another Ten Bagger?

Occasionally, I so totally knock the ball out of the park that I qualify for a place in the stock picker?s Hall of Fame. That was the case when I put out a recommendation to buy LNG exporter, Cheniere Energy (LNG), a year ago (click here? for Take a Look at Cheniere Energy (LNG).

Since then, the stock has soared an eye popping 85%. The great thing here is that I think the stock is still a buy. An upside target of $30 is a chip shot, and the all time high at $45 is within range. So get a 10%-20% dip in the price, and you might shovel some into your long-term portfolio. I quote below the entire original piece:

?I am constantly asked if there are any ways investors can take advantage of the collapse of the natural gas market, where at $2.34/MMBTU prices are plumbing decade lows. I have recently made good money buying puts on the ETF (UNG), but these are not for the faint of heart. They call this contract the ?widow maker? for a good reason.

You don?t want to touch the gas producing companies, like Chesapeake (CHK) and Devon (DVN), because prices are probably going to stay down for years. Good firms that benefit from the increased volume of gas pumped are few and far between. Unless you are a large consumer of this despised molecule, such as an electric power company or a petrochemical plant, it is tough to find a profitable niche.

However, there is one company that delivers a narrow rifle shot that could do extremely well in coming years, and that is Cheniere Energy (LNG). I first started following (LNG) a decade ago when I was still wildcatting for CH4 in the Texas Barnet Shale.

Back when natural gas was trading at a loft $5/MBTU, Qatar invested $50 billion in in developing its own substantial gas resources. The plan was to liquefy the gas at -256 degrees Fahrenheit in the Middle East, ship it to the US in a fleet of specialized LNG carriers, and have Cheniere convert it back into gas at its Sabine River plant for distribution to an energy hungry US market through the Creole Trail pipeline. It all looked like a great plan, and (LNG) shares traded up to $45.

Then ?fracking? technology came along and blew up the entire model. The discovery of a new 100-year supply of gas under our feet caused gas prices to crash from a post Amaranth peak of $17/MMBTU down to $2/MMBTU. Any plans to import LNG from the other side of the world were rendered utterly worthless. Chenier?s billion-dollar investment in a gasification plant was now worth only so much scrap metal. (LNG) shares plumbed low single digits as the firm flirted with bankruptcy.

Enter China. The Middle Kingdom?s voracious demand for energy in this recovery has caused the price of oil (USO) to soar from a 2008 low of $30 to $110. Despite accounting for an overwhelming share of the world?s new energy purchases, Chinese cities are suffering from brown outs due to power shortages. This is why China is resisting immense American pressure to quit buying Texas tea from Iran.

Enter the arbitrage. While oil has been spiking, gas has been crashing. Gas is now selling at 15% of the cost of oil on an adjusted BTU basis. Another way of saying this is that you can buy oil for $16 a barrel instead of $110. It only takes a second with an abacus to understand the appeal of such a disparity.

Gas also has the additional benefits in that it is much cleaner burning than crude, lacks the sulfur and nitrogen dioxides, and produces half the carbon dioxide. That?s a big deal in Beijing where the air is so thick you can cut it with a knife on a bad day.

Enter the long-term contracts. During the 1960?s and 1970?s Japan entered into huge long term contracts to buy LNG from Australia and Indonesia to feed their own economic miracle of the day. Because very expensive and hard to get, offshore supplies were tapped, the price was set at $16/MBTU. Those contacts are now expiring. Do you think they?ll renew at the old price, or go to Cheniere for the $2 stuff? Gee, let me think about that one for a bit.

Enter Fukushima. The nuclear meltdown last March prompted Japan to shut down 49 of 54 nuclear power plants that accounted for 25% of the country?s electric power generation. The brownouts that followed forced a sweltering summer on millions as the government urged consumers to shut off air conditioners to save juice. Power companies there have been scrambling to obtain conventional energy supplies, and have been a major factor in driving oil up from $75 to $100 since the fall. Cheap gas supplies from the US would meet this demand nicely.

The trigger. Last May, Cheniere got US government permission to export 2.2 billion cubic feet a day for 20 years. That would require it to convert the existing gasification plant to a liquifaction plant, something that can be done with some expensive re-engineering. It has already found several large international buyers to take delivery of the new end product. All that was missing was the money to finish the plant. My hedge fund buddies have been accumulating this stock since October, when it bottomed at $3, expecting an angel investor to appear. But it was one of those ?someday, it might happen? kind of stories better left to long term players.

Then last week, Blackstone jumped in with a beefy $2 billion investment in Cheniere. That will enable them to obtain an additional $3 billion in debt financing needed to finish the first of two export facilities. They are now expected to come online in 2016.

How does Cheniere stack up as an investment? Frankly, it is kind of scary. The market cap is only $2 billion, and it pays no dividend. When the current spate of deals are done, it will have $5 billion in debt. The Stock has just run up from $3 to $17. And these facilities are dangerous to operate. One blew up in Texas in 1937 and killed 300 schoolchildren. As a result, local permits for these are very hard to come by.

But as you can see, a whole host of geopolitical, technology and economic strands tie together in this one company, all of which are positive for the share price. If the story comes true, as Blackstone hopes, then there could be a double or triple in the shares for the patient. To learn more about Cheniere Energy, please click here for their website at http://www.cheniere.com/default.shtml .?

I have been pounding the table on the attractions of Cheniere Energy (LNG) since last spring. Yesterday, the stock hit a new all time high of $21.50.

There is never any guarantee that a government agency will not do something idiotic. Last year it didn?t, thankfully. The Federal Energy Regulatory Commission (FERC) granted the final license needed by Cheniere Energy (LNG) to build the first of two liquefaction plants at Sabine Pass on the Texas Louisiana border on the Gulf of Mexico. These will be the first such plants built in the US in 40 years.

FERC gave to go ahead despite vocal opposition from the Sierra Club, which claimed that fracking caused environmental damage. This, of course, is complete bunk. MIT recently published a study of 50 incidents where gas made it into local water supplies. In every case, it was shown to be the cause of subcontractor incompetence and inexperience, not because of any fundamental flaws with the technology.

The move was a crucial step towards turning the US into a major natural gas (UNG) exporter. The company has already contracted to sell 89% of the plants? planned annual output of 16 million tons. Buyers include BG Group of the UK, Gas Natural Fenosa of Spain, Gail of India, and Kogas of South Korea. Initial deliveries are expected to commence at the end of 2015.

You may recall that I recommended this stock to readers back on March 7 when it was trading at $16.10 a share (click here for ?Take a Look at Cheniere Energy (LNG)? at http://madhedgefundradio.com/take-a-look-at-cheniere-energy-lng/). I think it is just a matter of time before the stock surpasses its next hurdle at $30, especially if natural gas continues to stabilize here around $2/MM BTU.

Now, We?re Cooking With Gas

I am constantly asked if there are any ways investors can take advantage of the collapse of the natural gas market, where at $2.34/MBTU prices are plumbing decade lows. I have recently made good money buying puts on the ETF (UNG), but these are not for the faint of heart. They call this contract the ?widow maker? for a good reason.

You don?t want to touch the gas producing companies, like Chesapeake (CHK) and Devon (DVN), because prices are probably going to stay down for years. Good firms that benefit from the increased volume of gas pumped are few and far between. Unless you are a large consumer of this despised molecule, such as an electric power company or a petrochemical plant, it is tough to find a profitable niche.

However, there is one company that delivers a narrow rifle shot that could do extremely well in coming years, and that is Cheniere Energy (LNG). I first started following (LNG) a decade ago when I was still wildcatting for CH4 in the Texas Barnet Shale.

Back when natural gas was trading at a loft $5/MBTU, Qatar invested $50 billion in in developing its own substantial gas resources. The plan was to liquefy the gas at -256 degrees Fahrenheit in the Middle East, ship it to the US in a fleet of specialized LNG carriers, and have Cheniere convert it back into gas at its Sabine River plant for distribution to an energy hungry US market through the Creole Trail pipeline. It all looked like a great plan, and (LNG) shares traded up to $45.

Then ?fracking? technology came along and blew up the entire model. The discovery of a new 100 year supply of gas under our feet caused gas prices to crash from a post Amaranth peak of $17/MBTU down to $2/MBTU. Any plans to import LNG from the other side of the world were rendered utterly worthless. Chenier?s billion dollar investment in a gasification plant was now worth only so much scrap metal. (LNG) shares plumbed low single digits as the firm flirted with bankruptcy.

Enter China. The Middle Kingdom?s voracious demand for energy in this recovery has caused the price of oil to soar from a 2008 low of $30 to $110. Despite accounting for an overwhelming share of the world?s new energy purchases, Chinese cities are suffering from brown outs due to power shortages. This is why China is resisting immense American pressure to quit buying Texas tea from Iran.

Enter the arbitrage. While oil has been spiking, gas has been crashing. Gas is now selling at 15% of the cost of oil on an adjusted BTU basis. Another way of saying this is that you can buy oil for $16 a barrel instead of $110. It only takes a second with an abacus to understand the appeal of such a disparity.

Gas also has the additional benefits in that it is much cleaner burning than crude, lacks the sulfur and nitrogen dioxides, and produces half the carbon dioxide. That?s a big deal in Beijing where the air is so thick you can cut it with a knife on a bad day.

Enter the long term contracts. During the 1960?s and 1970?s Japan entered into huge long term contracts to buy LNG from Australia and Indonesia to feed their own economic miracle of the day. Because very expensive, hard to get or offshore supplies were tapped, the price was set at $16/MBTU. Those contacts are now expiring. Do you think they?ll renew at the old price, or go to Cheniere for the $2 stuff. Gee, let me think about that one for a bit.

Enter Fukushima. The nuclear meltdown last March prompted Japan to shut down 49 of 54 nuclear power plants that accounted for 25% of the country?s electric power generation. The brownouts that followed forced a sweltering summer on millions as the government urged consumers to shut off air conditioners to save juice. Power companies there have been scrambling to obtain conventional energy supplies, and have been a major factor in driving oil up from $75 to $100 since the fall. Cheap gas supplies from the US would meet this demand nicely.

The trigger. Last May, Cheniere got US government permission to export 2.2 billion cubic feet a day for 20 years. That would require it to convert the existing gasification plant to a liquifaction plant, something that can be done with some expensive re-engineering. It has already found several large international buyers to take delivery of the new end product. All that was missing was the money to finish the plant. My hedge fund buddies have been accumulating this stock since October, when it bottomed at $3, expecting an angel investor to appear. But it was one of those ?someday, it might happen? kind of stories better lead to long term players.

Then last week, Blackstone jumped in with a beefy $2 billion investment in Cheniere. That will enable them to obtain an additional $3 billion in debt financing needed to finish the first of two export facilities. They are now expected to come online in 2016.

How does Cheniere stack up as an investment? Frankly, it is kind of scary. The market cap is only $2 billion, and it pays no dividend. When the current spate of deals are done, it will have $5 billion in debt. The Stock has just run up from $3 to $17. And these facilities are dangerous to operate. One blew up in Texas in 1937 and killed 300 schoolchildren. As a result, local permits for these are very hard to come by.

But as you can see, a whole host of geopolitical, technology and economic strands tie together in this one company, all of which are positive for the share price. If the story comes true, as Blackstone hopes, then there could be a double or triple in the shares for the patient. To learn more about Cheniere Energy, please click here for their website at http://www.cheniere.com/default.shtml.

Did Somebody Light a Match?