Mad Hedge Technology Letter

January 28, 2019

Fiat Lux

Featured Trade:

(BUY DIPS IN SEMIS, NOT TOPS),

(XLNX), (LRCX), (AMD), (TXN), (NVDA), (INTC), (SOXX), (SMH), (MU), (QQQ)

Mad Hedge Technology Letter

January 28, 2019

Fiat Lux

Featured Trade:

(BUY DIPS IN SEMIS, NOT TOPS),

(XLNX), (LRCX), (AMD), (TXN), (NVDA), (INTC), (SOXX), (SMH), (MU), (QQQ)

Global Market Comments

January 28, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or IT’S FINALLY OVER)

(SPY), (TLT), (FXE), (MSFT), (AAPL),

(PG), (F), (LRCX), (AMD), (XLNX)

Last week, I was too busy to cook dinner for my brood, so I ordered a pizza delivery. When an older man showed up with our dinner, I told the kids to tip him double. After all, he might be an unpaid federal air traffic controller.

It is a good thing I work late on Friday afternoon because that's when the government shutdown ended after 35 days. The bad news? The government stops getting paid again in only 18 more days. If you have to travel, you better do it quick as the open window may be short.

The most valuable thing we learned from all of this is that the weak point in America is the airline transportation system which relies on 4,000 flights to get the country’s business done.

Having once owned a European air charter company, I could have told you as much was coming. Every nut, bolt, and screw that goes into a US registered aircraft has to be inspected by the federal government. They are painted yellow when viewed which is called “yellow tagging”. No inspection, no screw. No screw, no airplane. No airplane, no flight. No flight, no economy. I can’t tell you how many times I have seen a $30 million aircraft grounded by a failed 50-cent part.

And here’s what most investors don’t get. We lost 75 basis points in GDP growth from the shutdown. We may lose another 75 basis points restarting. And if you lose 1.50% from a post-Christmas period that is normally weak anyway, Q1 GDP may well come in negative. Hello recession!

We won’t know for sure until the first advanced estimate of Q1 GDP from the US Department of Commerce’s Bureau of Economic Analysis is published on April 26. That’s when the sushi will hit the fan. That, by the way, is perilously close for the May 10 prediction of the end of the entire ten-year bull market.

How did investors fare during the shutdown? We clocked the best January in 32 years with the Dow Average up 7.55%. Maybe the government should stay closed all the time!

It is not like the government shutdown, the fading Chinese trade talks, and the arrest of the president’s pal were the only things happening last week.

A slowing China is freaking out investors everywhere. Even if a trade deal is cut tomorrow, it may not be enough to pull the economy out of a downward death spiral. Look out below! A 6.6% growth rate for 2018 is the slowest in 30 years.

Existing Home Sales were down a disastrous 6.4%, in December and 10% YOY, the worst read since 2012. The government shutdown is made closings nearly impossible.

The EC’s Mario Draghi said there would be no euro rate rises until 2020 and the US bond market took off like a rocket. Another point or two and we’ll be in short selling territory again. Don’t count on Europe to pull us out of the next recession. Whoever came up with the idea of putting an Italian in charge of Europe’s finances anyway? Like that was such a great idea.

Procter & Gamble (PG) beat with an upside earnings surprise. It must be all those people buying soap to wash their hands of our political system. But Ford (F) disappointed, dragged down by weak foreign earnings. The weakest big car company to get into electric cars is really starting to suffer. The last of the buggy whip makers is taking a swan dive

The semis have bottomed in the wake of spectacular earnings reports from (LRCX), (AMD), and (XLNX). The great artificial intelligence play is back in action after a severe spanking. I never had any doubt they would come back. Now for an entry point.

Farmers are leaving crops to rot in the field as the trade war with China destroys prices and the Mexicans needed to harvest them are trapped at the border. There’s got to be an easier way to earn a living. Avoid the ags and all ag plays. Short tofu stocks!

Investors are now sitting on pins and needles wondering if we get a repeat of the horrific February of 2018, or whether so far great earnings reports will drive us to higher highs. Earnings tail off right when the next government shutdown is supposed to start so our lives will be interesting, to say the least.

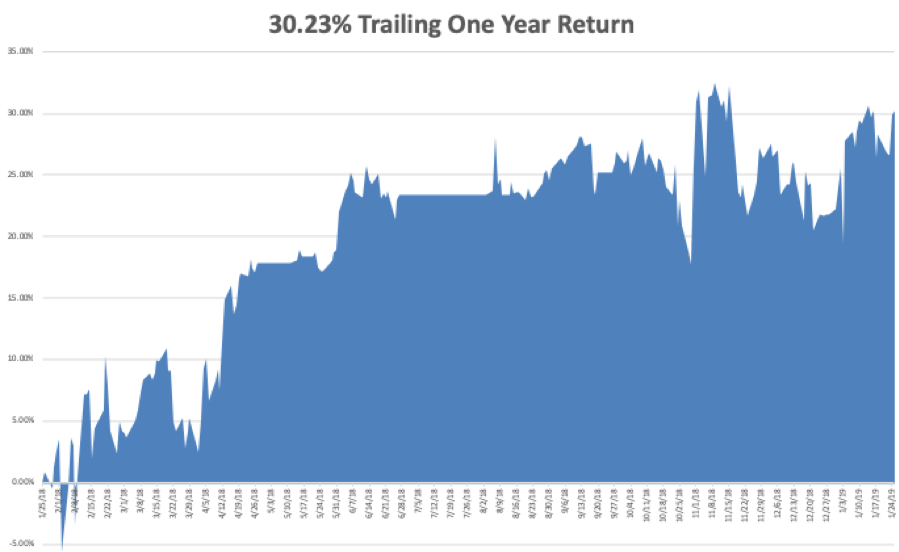

My January and 2019 year to date return soared to +7.24%, boosting my trailing one-year return back up to +30.23%.

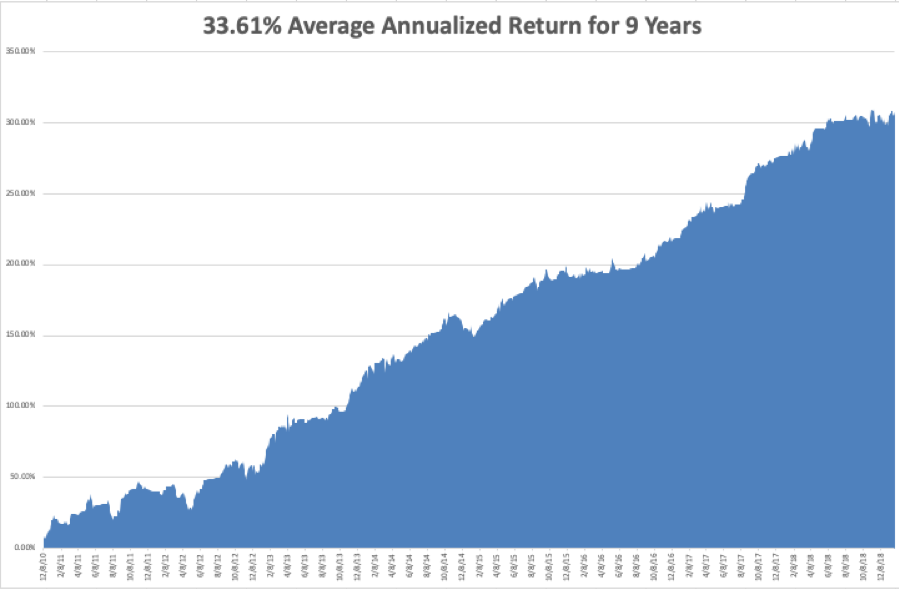

My nine-year return climbed up to +308.14%, a mere 1.72% short of a new all time high. The average annualized return revived to +33.61%.

I have been dancing in between the raindrops using rallies to take profits on longs and big dips to cover shorts.

I started out the week using the 4 1/2 point plunge in the bond market (TLT) to cover the last of my shorts there, bring in a whopper of a $1,680 profit in only 13 trading days. To quote the Terminator (whose girlfriend I once dated, the Terminatrix), I’ll be back.”

I used the big 500-point swoon in the Dow on Monday to come out of my (SPY) short at cost. An unfortunate comment on interest rates by the European Central Bank forced me to stop out of my long in the Euro (FXE), also at cost.

That has whittled my portfolio down to only two positions, a long in Microsoft (MSFT) and a short in Apple (AAPL). As a pairs trade you could probably run this position for years. I am now 80% in cash.

The goal is to go 100% into cash into the February option expiration in 14 trading days, wait for a big breakout, and then fade it. Essentially, I am waiting for the market to tell me what to do. That will enable me to bank double-digit profits for the start of 2019, the best in a decade.

The upcoming week is very iffy on the data front because of the government shutdown. Some government data may be delayed and other completely missing. Private sources will continue reporting on schedule. All of the data will be completely skewed for at least the next three months. You can count on the shutdown to dominate all media until it is over.

Jobs data will be the big events over the coming five days along with some important housing numbers. We also have several heavies reporting earnings.

On Monday, January 28 at 8:30 AM EST, we get the Chicago Fed National Activity Index.

On Tuesday, January 29, 9:00 AM EST, the Case Shiller National Home Price Index for November is released. The ever important Apple (AAPL) earnings are out after the close, along with Juniper Networks (JNPR).

On Wednesday, January 30 at 8:15 AM EST, the ADP Private Employment Report is announced. Pending Home Sales for December follows. Boeing Aircraft (BA) and Facebook (FB), and PayPal (PYPL) announce.

Thursday, January 31 at 8:30 AM EST, we get Weekly Jobless Claims. We also get the all-important Consumer Spending Index for December. Amazon (AMZN) and General Electric (GE) announce.

On Friday, February 1 at 8:30 AM EST, the January NonFarm Payroll Report hits the tape.

The Baker-Hughes Rig Count follows at 1:00 PM. Schlumberger (SLB) announces earnings. Home Sales is released. AbbVie Inc (ABBV) and DR Horton (DHI) report.

As for me, I will be celebrating my birthday. Believe me, lighting 67 candles creates a real bonfire. I received the best birthday card ever from my daughter which I have copied below

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Don’t buy the dead cat bounce – that was the takeaway from a recent trading day that saw chips come alive with vigor.

Semiconductor stocks had their best day since March 2009.

The price action was nothing short of spectacular with names such as chip equipment manufacturer Lam Research (LRCX) gaining 15.7% and Texas Instruments (TXN) turning heads, up 6.91%.

The sector was washed out as the Mad Hedge Technology Letter has determined this part of tech as a no-fly zone since last summer.

When stocks get bombed out at these levels - sometimes even 60% like in Lam Research’s case, investors start to triage them into a value play and are susceptible to strong reversal days or weeks in this case.

The semi-conductor space has been that bad and tech growth has had a putrid last six months of trading.

In the short-term, broad-based tech market sentiment has turned positive with the lynchpins being an extremely oversold market because of the December meltdown and the Fed putting the kibosh on the rate-tightening plan.

Fueled by this relatively positive backdrop, tech stocks have rallied hard off their December lows, but that doesn’t mean investors should take out a bridge loan to bet the ranch on chip stocks.

Another premium example of the chip turnaround was the fortune of Xilinx (XLNX) who rocketed 18.44% in one day then followed that brilliant performance with another 4.06% jump.

A two-day performance of 22.50% stems from the underlying strength of the communication segment in the third quarter, driven by the wireless market producing growth from production of 5G and pre-5G deployments as well as some LTE upgrades.

Give credit to the company’s performance in Advanced Products which grew 51% YOY and universal growth across its end markets.

With respect to the transformation to a platform company, the 28-nanometer and 16-nanometer Zynq SoC products expanded robustly with Zynq sales growing 80% YOY led by the 16-nanometer multiprocessor systems-on-chip (MPSoC) products.

Core drivers were apparent in the application in communications, automotive, particularly Advanced Driver Assistance Systems (ADAS) as well as industrial end markets.

Zynq MPSoC revenues grew over 300% YOY.

These positive signals were just too positive to ignore.

Long term, the trade war complications threaten to corrode a substantial chunk of chip revenues at mainstay players like Intel (INTC) and Nvidia (NVDA).

Not only has the execution risk ratcheted up, but the regulatory risk of operating in China is rising higher than the nosebleed section because of the Huawei extradition case and paying costly tariffs to import back to America is a punch in the gut.

This fragility was highlighted by Intel (INTC) who brought the semiconductor story back down to earth with a mild earnings beat but laid an egg with a horrid annual 2019 forecast.

Intel telegraphed that they are slashing projections for cloud revenue and server sales.

Micron (MU) acquiesced in a similar forecast calling for a cloud hardware slowdown and bloated inventory would need to be further digested creating a lack of demand in new orders.

Then the ultimate stab through the heart - the 2019 guide was $1 billion less than initially forecasted amounting to the same level of revenue in 2018 - $73 billion in revenue and zero growth to the top line.

Making matters worse, the downdraft in guidance factored in that the backend of the year has the likelihood of outperforming to meet that flat projection of the same revenue from last year offering the bear camp fodder to dump Intel shares.

How can firms convincingly promise the back half is going to buttress its year-end performance under the drudgery of a fractious geopolitical set-up?

This screams uncertainty.

Love them or crucify them, the specific makeup of the semiconductor chip cycle entails a vulnerable boom-bust cycle that is the hallmark of the chip industry.

We are trending towards the latter stage of the bust portion of the cycle with management issuing code words such as “inventory adjustment.”

Firms will need to quickly work off this excess blubber to stoke the growth cycle again and that is what this strength in chip stocks is partly about.

Investors are front-running the shaving off of the blubber and getting in at rock bottom prices.

Amalgamate the revelation that demand is relatively healthy due to the next leg up in the technology race requiring companies to hem in adequate orders of next-gen chips for 5G, data servers, IoT products, video game consoles, autonomous vehicle technology, just to name a few.

But this demand is expected to come online in the late half of 2019 if management’s wishes come true.

To minimize unpredictable volatility in this part of tech and if you want to squeeze out the extra juice in this area, then traders can play it by going long the iShares PHLX Semiconductor ETF (SOXX) or VanEck Vectors Semiconductor ETF (SMH).

In many cases, hedge funds have made their entire annual performance in the first month of January because of this v-shaped move in chip shares.

Then there is the other long-term issue of elevated execution risks to chip companies because of an overly reliant manufacturing process in China.

If this trade war turns into a several decades affair which it is appearing more likely by the day, American chip companies will require relocating to a non-adversarial country preferably a democratic stronghold that can act as the fulcrum of a global supply chain channel moving forward.

The relocation will not occur overnight but will have to take place in tranches, and the same chip companies will be on the hook for the relocation fees and resulting capex that is tied with this commitment.

That is all benign in the short term and chip stocks have a little more to run, but on a risk reward proposition, it doesn’t make sense right now to pick up pennies in front of the steamroller.

If the Nasdaq (QQQ) retests December lows because of global growth falls off a cliff, then this mini run in chips will freeze and thawing out won’t happen in a blink of an eye either.

But if you are a long-term investor, I would recommend my favorite chip stock AMD who is actively draining CPU market share from Intel and whose innovation pipeline rivals only Nvidia.

Mad Hedge Technology Letter

November 13, 2018

Fiat Lux

Featured Trade:

(NO BIWEEKLY STRATEGY WEBINAR FOR WEDNESDAY NOVEMBER 14)

(WHY I HATE CHIP STOCKS)

(AAPL), (CY), (TXN), (LRCX), (KLAC), (LITE), (QCOM), (MU), (SWKS), (LSCC)

Now that the midterm elections are behind us, Congress will be gridlocked for the next two years portending well for tech stocks as a whole.

However, the gridlock will exacerbate negative sentiment in one small group of technology – the semiconductor chip sector.

I have been staunchly bearish on this cohort since the outset of the trade logjam with China and I recommend readers to avoid these stocks like the plague.

The split Congress could fuel an even more rigid stance towards the complicated tech situation, further clamping down on foreign IP theft and technological forced transfers.

Either way, there is no end in sight and as this administration is concretely in place for the next two years, doubling down on foreign policy wins could be the Republican party’s path to victory heading into the 2020 election.

This could mean the rhetoric towards China could ratchet up a few levels.

Soon enough, the tariffs levied on Chinese imports is set to increase to 25% in January.

Even before January, a planned meeting between Trump and Chairman Xi in Buenos Aires on Nov. 29 will take place and is creating a swirling tornado of uncertainty around chip sentiment that is on tenterhooks.

Any chance to resuscitate the sentiment in the industry could come and go with another gut-churning leg down in chip shares.

Unfortunately, the sword of Damocles hanging over the chip sector could drop in 2019 slashing profit margins, revenue, and damaging the all-important guidance.

Even if individual chip companies determine that the trade friction is too much to stomach, it would be expensive and lengthy to transfer an entire supply chain to Vietnam or Indonesia, hitting current R&D budgets and damaging future innovation affecting the pipeline of fresh products.

Time is not a friend to the chip sector.

If the China leveraged chip companies were to wait out this trade war, they risk further being enveloped into the eye of the trade storm if no quick agreements can be made.

They might have to wait a while as Beijing views waiting out Trump and dealing with the next administration in charge as the ideal option.

Chairman Xi conveniently removed term limits in the last congress, meaning he is in his job until death which could be another 40 years or so.

That is the time horizon the Chinese are playing with.

The timing couldn’t have been worse for the chip sector after a slew of weak guidance from upper management painted a downbeat picture for the sector as we inch towards 2019.

Texas Instruments (TXN) Chief Executive Rich Templeton started off his earnings report admitting, “demand for our products slowed across most markets.”

He later admitted that the semiconductor market is grappling with an imminent “softer” market.

Following up a growing chorus of chip executives flashing dangerous warnings signs, Lattice Semiconductors (LSCC) lamented that it was seeing slowness in the industrial and consumer markets in Asia as a result of macroeconomic conditions and tariffs.

Cypress Semiconductor (CY) also chimed in saying it was coping with “softness across the board.”

Making matters worse, Beijing has been showering capital on the local chip sector aimed at nurturing and developing Chinese chip companies poised to compete on the global stage.

Recently, Chinese state-backed semiconductor maker Fujian Jinhua Integrated Circuit was indicted by the U.S. Justice Department for industrial espionage.

The company allegedly stole trade secrets from Boise-based Micron (MU).

Micron could now become the first piece of collateral damage to the snarky trade war threatening huge swaths of American chip company's revenue.

And with the affected American chip companies waded in a quagmire, and chip market softness on the near horizon, semiconductor equipment firms have borne a good amount of the damage this year with Applied Materials Inc (AMAT), KLA-Tencor Corp (KLAC), and Lam Research Corp (LRCX) getting hammered.

Chips tied to Apple’s (AAPL) iPhone are also in for a drubbing with Apple suddenly announcing in their most recent report they would stop offering the unit sales of iPhones, creating more uncertainty around units sold for a massive end-market for global chip companies, adding to the swirling uncertainties overall Chinese chip revenue face.

Apple proxy chip stocks who lean on Apple for a big chunk of revenue such as Skyworks Solutions (SWKS) are getting crushed.

Skyworks was downgraded last week by Citigroup based on underperforming iPhone XR sales.

The rapid rush of chip downgrades has been fast and furious.

Skyworks will have pockets of strength when 5G is fully rolled out because they will supply critical components installed in this new technology for the new era of internet speed and performance.

But that pocket of strength is not now and will not happen tomorrow.

It’s time to duck out of Skyworks and I have been convincingly downbeat on this particular name since the inception of the trade war.

Today crawled in the next batch up negative chip news from Lumentum Holdings (LITE) who supplies 3D chips for Apple iPhone's facial recognition system.

Management reported that sales would be $20 million lower than originally forecasted because of a sudden reduction in shipments from an unnamed customer.

Another ongoing headache is the Qualcomm (QCOM) versus Apple marriage or divorce, depending on how you look at it.

They have been mired in a prolonged court case against each other, and Qualcomm’s share price has been dismal as of late.

Qualcomm recorded zero licensing revenue in the quarter from Apple who is withholding royalty payments from Qualcomm in a dispute over the company's licensing practices.

The move damaged quarterly licensing sales sliding 6% to $1.14 billion.

Qualcomm has lashed back at Apple pointing the finger at Apple for transferring its intellectual property to Intel (INTC) who is supplying chips for new-model iPhones which is possibly part of the reason they lost this contract.

Losing the iPhone contract to Intel is the main factor in Qualcomm expecting modem chip shipments to decline 22% to about 185 million units.

The fight has no end in sight but like Skyworks Solution, Qualcomm is on the forefront of the 5G revolution and provides a silver lining to embattled revenue growth that has been dragged down with the China mess.

At the end of the day, companies have less resistance when they aren’t belligerently brawling with their biggest purchasers.

Biting the hand that feeds you is a poor strategy that cuts across any industry.

Avoid chip companies for the short term and wait for sentiment to reverse course.

Global Market Comments

October 5, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY OCTOBER 17 HOUSTON STRATEGY LUNCHEON INVITATION),

(OCTOBER 3 BIWEEKLY STRATEGY WEBINAR Q&A)

(SPY), (VIX), (VXX), (MU), (LRCX), (NVDA), (AAPL), (GOOG), (XLV), (USO), (TLT), (AMD), (LMT), (ACB), (TLRY), (WEED)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 3 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Will the market keep increasing for the rest of the year?

A: We haven’t had the pullback yet, so the short answer is yes. My yearend target of and S&P 500 (SPY) for the end of 2018 still stands. You can’t argue with the immediate price action. That said, the market is wildly overbought for the medium term and is approaching valuation levels we haven’t seen since the Dotcom peak in 2000. That why I am running a 70% cash trading book now.

Q: Should I be buying the Volatility Index (VIX) here?

A: Look at the bottom where we broke back in August, if we go down there and sit for a couple of days, then go out and buy the March 2019 $40 iPath S&P 500 VIX Short-Term Futures ETN (VXX) calls—way out of the money, way far in the future—and that way if you get any bounce in the (VIX) in the next 6 months, you’ll make a ton of money on that. You can buy them today for 50 cents. Plus, we could get one of these situations where there’s a major selloff once we’re into the new year, so a 6-month (VXX) call option would hedge that.

Q: Given the choice of Apple (AAPL) or Google (GOOG), which would you buy?

A: If you’re a conservative, old lady, widow and orphan type, you’d probably want to buy Apple— it’s almost turned into a utility, it’s so reliably safe, going up and has a nice dividend. If you want to be aggressive, swinging for the fences young stud and are looking for a double, I would go with Google—much higher growth pattern, pays no dividend and has had a 3-month consolidation going sideways. The only thing that could hurt this company would be government regulation, but with the Democrats possibly taking control of Congress in November, the prospect of government regulation of the entire technology sector could rapidly fade away.

Q: When should I get into Health Care (XLV)?

A: I think you have to wait at this point. To me, it’s tremendously overbought at the moment, but is still enjoying a long-term bull move. This is one of my two favorite sectors in the entire market. It has been rising for four months now, even though the Trump threat of price cuts are constantly overhanging the market.

Q: Is oil (USO) going to 100?

A: Because of the disruptions caused by the Iran sanctions and the tearing up of the Iran Nuclear Treaty, Trump has created a short squeeze in oil prices. He is threatening to boycott any country that buys oil from Iran, so Iran is shipping their oil through China, which is already under sanctions itself. However, that is easier said than done. The oil business is much more complicated than people realize. For China to take Iranian oil, they literally have to build new refineries from scratch to process the crude from Iran; no two crudes are alike. When you build a major supply, you have to build refineries to match that, and you have to get it there. This market will eventually stabilize, but in the meantime, there is a big short squeeze going on in Europe.

Q: Do you see the economy going strong into the end of the year?

A: Yes, I do—we still have the tax cuts, global liquidity, and deregulation kicking in, and those things will all work until the end of the year. I think we close at the highs of the year, and after that we’re going to have to start to work hard for our money once again in 2019. The US economy is like a supertanker; it takes a long time to turn it around.

Q: Will the interest rate spike kill the market?

You think? Investors are so used to ultra-low interest rates that a transition to normal rates will be traumatic. Next Friday, we get Core CPI, and if that comes in hot we could see another spike to 3.35% in the ten-year US Treasury bond (TLT). There are now a ton of people desperate to get out of their bond holdings at last week’s prices. This is why I have been selling short the bond market for the past three years and selling as recently as Monday. The next leg down in a 30-year bear market has begun.

Q: Advanced Micro Devices (AMD) has shot over $30—would you sell it?

A: We love the company long term but short term it is just way overdone; take the double and run, and then buy back on the next dip.

Q: Are you still bearish on the chip company?

A: Short term yes, long term no. This sector is now totally driven by the trade war with China. This includes NVIDIA (NVDA), Micron Technology (MU) and LAM Research (LRCX). Lam is particularly exposed because they had ordered to sell ten entire chip factories to China which is now on hold. That said, the day the trade way ends these stocks will all start a 50% run up. If China gets the same free pass and symbolic treaty that Canada did, that could happen sooner than later. If you can’t sleep at night until then, cut your position in half. If you still can’t sleep, cut it again.

Q: Do you think Lockheed Martin (LMT) is a buy Here at $350?

A: No, there is a double top risk for the stock right here. And if the Democrats get control of congress, the whole Trump trade could unwind. That would give the opposition the purse strings and the first thing they’ll do is cut defense spending, which Trump bumped up by $50 billion.

Q: Do you have any views on pot stocks like Aurora Cannabis (ACB), Tilray (TLRY) and (WEED)?

Stay away in droves. They’re this year’s bitcoin stocks. It’s still illegal. That’s why these companies are all based in Canada. And after all it’s a weed. How hard is it to grow? The barriers to entry are zero.

Mad Hedge Technology Letter

September 24, 2018

Fiat Lux

Featured Trade:

(BAD NEWS FROM MICRON TECHNOLOGY (MU),

(MU), (BABA), (KLAC), (LRCX), (INTC), (AMD), (NVDA), (HPQ)

If your stomach was on edge before, then you must feel quite queasy now.

That’s only if you didn’t get rid of your chip stocks when I told you to.

The chip sector has been rife with issues for quite some time now, and I’ve been firing off bearish chip stories the past few months.

Intel (INTC) was one of the last chip companies I told you to avoid like the plague, please click here to review that story.

The contagion has spread wider.

Micron (MU), the Boise, Idaho-based chip giant, delivered poor guidance from its latest earnings report, adding more carnage to this trouble sector.

It’s been rough sailing for many American-based chip companies lately that are not named Advanced Micro Devices (AMD) and Nvidia (NVDA).

The protracted ongoing trade war between America and China that sees no end in sight is the fundamental reason to stay away from these chip companies that are the meat and potatoes inside of all electronic devices.

Cofounder of Alibaba (BABA) Jack Ma, who recently stepped down from his position as chairman, told news outlets that this trade war could last “20 years” and is “going to be a mess.”

Micron is affected by this trade war more than any other American company, with half of its annual revenue derived from the Middle Kingdom.

Out of the $20.32 billion in annual revenue last year, more than $10 billion was from China alone.

Micron is a leader in selling DRAM chips, which are placed in most portable electronic devices such as smartphones, video game consoles, and laptop computers.

The commentary coming out from chip executives has been overly negative and spells doom and gloom - supporting my view to be cautious on chips through the end of the year.

At the Citi 2018 Global Technology Conference in New York, KLA-Tencor (KLAC) chief financial officer Bren Higgins characterized the winter season DRAM market as “little less than what we thought,” describing margins as “modestly weaker.”

Lam Research (LRCX), once one of my favorite chip plays, offered bearish rhetoric about the state of chip investments, saying on its earnings call that is expected “lower spending on new equipment by some of its memory customers.”

It doesn’t take a rocket scientist to know that “memory customer” is Intel, which is in the throes of a CPU chip shortage rocking the overall personal computer market.

Personal computers face a steep 7% drop in sales volume for the rest of the year, and the knock-on effect is rippling throughout the industry.

The lower volume of produced computers means less memory needed, adding up to less sales for Micron.

This rationale forced Micron to guide down its revenue growth from 22% to 16% for the last quarter of 2018.

Intel’s monumental lapse has offered a golden opportunity for competitor Advanced Micro Devices (AMD) to steal market share from Intel in broad daylight.

This was the exact thesis that provoked me to urge readers to pile into AMD shares like a Tokyo rush-hour subway car.

Shares have gone ballistic to say the least.

(AMD) is poised to seize and reposition itself in the global CPU market with a 70/30 market share, up from the paltry 90/10 market share before Intel’s debacle.

To make matters worse for Intel, widespread reports indicate its shortage problems are “worsening.”

Such is a dog-eat-dog world out there when a company can triple market share in a blink of an eye.

The rotation is real with HP (HPQ) planning to integrate AMD chips into 30% of its consumer PCs, and Dell already mentioning it will use AMD chips to make up for the shortages.

The resilience in chip demand remains the silver lining for this industry as price weakness and production shortages will be finite.

Server demand remains particularly robust.

Google, Amazon, Facebook, and Microsoft coughed up $34.7 billion on data centers to serve cloud-based operation in the first half of the year in 2018, a sharp increase of 59% YOY.

Investors have been paranoid of the boom-bust nature of the chip industry for decades.

Each cycle sees spending and chip pricing rocket, only for inventories to build up and demand to evaporate in an instant.

The beginning of the end always starts with lower guidance, followed up with missed earnings the next quarter.

This playbook has repeated itself over and over.

Micron guided first quarter revenue of 2019 in a range between $7.9 billion to $8.3 billion, lower than the consensus of $8.45 billion.

And, if all of this horrid chip news wasn’t reason to rip your hair out - here is the bombshell.

To wean itself off the reliance of American chips, Alibaba has created a subsidiary to produce its own chips called Pingtouge Semiconductor Company.

Pingtouge refers to honey badger in the Chinese language, symbolic for its tenacity in the face of adversity – perhaps a thinly-veiled dig at the American political system.

Former Chairman Ma pocketed this chip company Hangzhou C-SKY Microsystems last year. It will will be given ample leeway and resources to team up with Alibaba to roll out its first commercial chip next year.

Alibaba has rapidly grown into the third-largest cloud player in the world, and require an abundant source of chips moving forward.

Chips tricked out with artificial intelligence will be adopted by not only its data centers, but integrated with its autonomous driving technology and IoT products, which are markets that Alibaba is proud to be part.

You can find Alibaba’s cloud products present in more than 20 countries. And the company that Jack Ma built forecasts to generate more than 50% of its revenue from overseas markets soon.

It could be Jack Ma laughing all the way to the bank.

Ultimately, Micron produced fair results last quarter, but like Facebook found out, if investors believe the company is about to fall off a cliff, it offers little resistance to the share price on a short-term basis.

Could the cyclicality demons start to awake to drag this company down?

Partially, yes, but there are still many positives to take away from this leading chip company.

China will need years to remedy its addiction of American chips.

It will not be able to produce the scope of quality or quantity to just stop buying from American companies for the foreseeable future.

The authorized $10 billion share buyback gave Micron shares a nice lift earlier this year, but the industry dynamics are now deteriorating rapidly.

Chip sentiment is at its lowest ebb for some time, and I reaffirm my call to avoid this sector completely unless it’s the two cornerstone chip companies showing systematic resiliency - (AMD) or Nvidia (NVDA).

The administration initially slapped on a tariff rate of 10% on $200 billion worth of goods with intentions to scale it up.

If nothing is solved, the increase to 25% will cause another 5% to 10% drop in Micron and Intel.

Then if the administration plans to go after the rest of the $250 billion of Chinese imports, expect another dive in chip shares.

Either way, each jawboning tweet as we head deeper into this trade conflict will damage Micron’s shares.

This sector is getting squeezed from many sides now, and if you don’t go outright short chip companies, then stay away until the storm clouds pass over and you can reassess the situation.