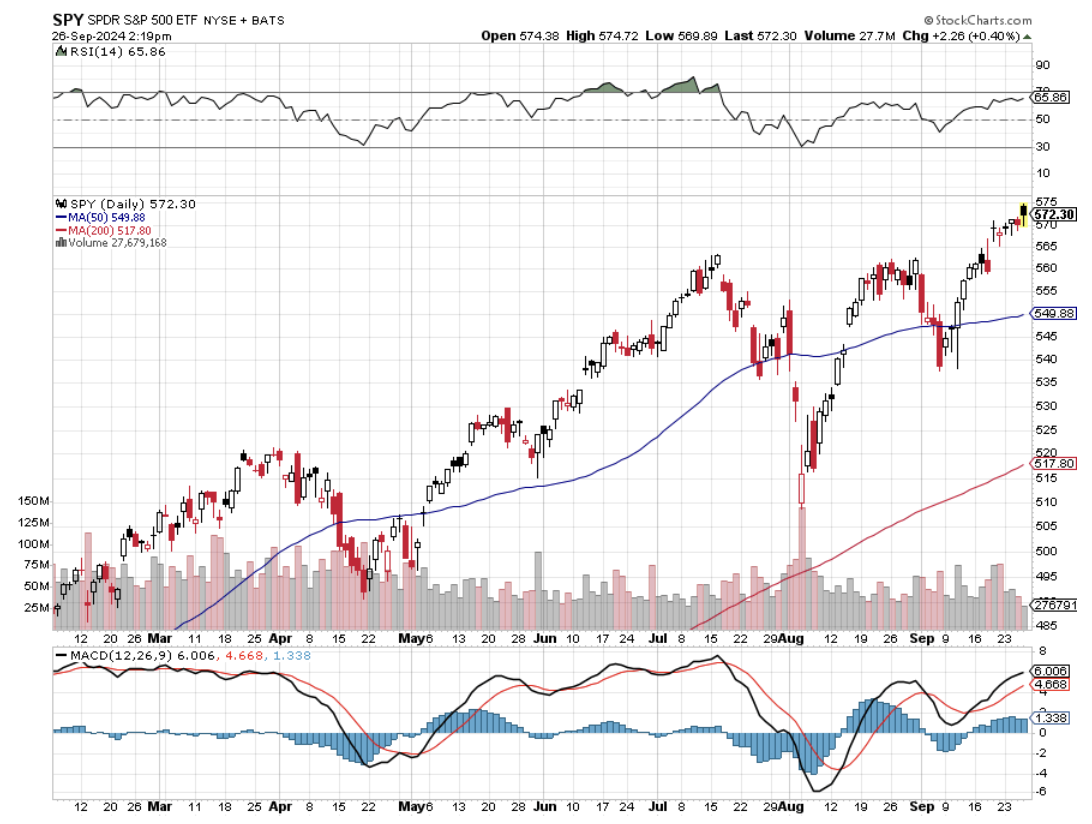

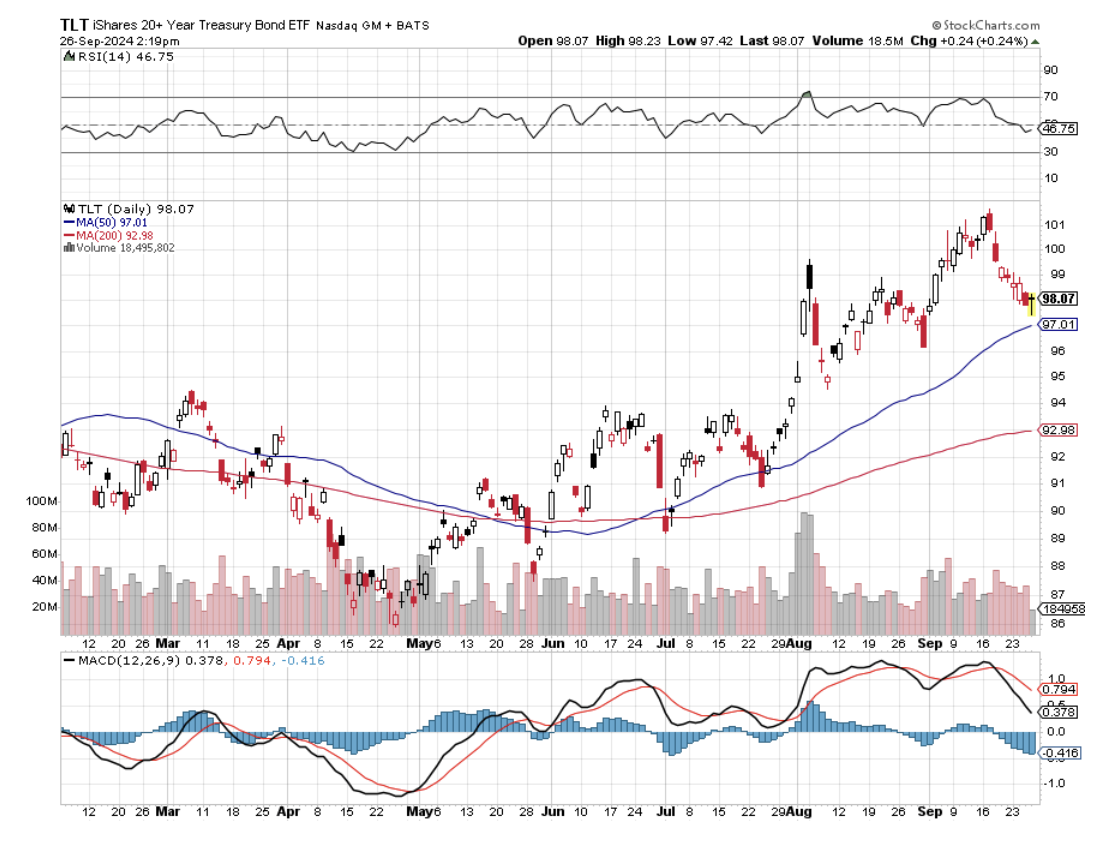

Below please find subscribers’ Q&A for the September 25 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe Nevada.

Q: The iShares 20+ Year Treasury Bond ETF (TLT) is not advancing like I had hoped. I’m not sure why the interest rate cuts have not impacted the 20-year maturity—is it too far out?

A: It’s not an issue of maturity; the fact is that the market has been discounting falling interest rates for six months, all the way back to March. It’s a classic “buy the rumor, sell the news” scenario. (TLT) rose $20 off the low this year, and once the rate cut actually happened, all the news was in. That is why I actually went short the TLT a couple of days ago, and that trade immediately started making money. Here’s the real problem: Fed futures are discounting 250 basis points in rate cuts by June of next year. If you don’t think we’re going to get 250 basis points in rate cuts, which is two 50 basis point rate cuts and five 25 basis point rate cuts, then the market is overbought for the short term and we’re selling short. That’s exactly what I did.

Q: Is it too late to buy Tesla (TSLA) and Nvidia (NVDA)?

A: No, it’s not, I think Tesla could hit $300 this year, and Nvidia could revisit $140. However, the more you wait, the more pain you have to take along the way. Nvidia did drop 40% off its high at one point this year, and Tesla dropped 80% off its high. The price of coming in late is pain, so be ready to take that pain or, even worse, to stop out.

Q: What is your take on Japan’s attempt to take over US Steel (X)?

A: Well, it’s entirely political. They definitely picked the wrong year to take a run at US steel because it’s headquartered in Pittsburgh, Pennsylvania, and neither political party can win their election without winning Pennsylvania. Nippon Steel is now 3x larger than US Steel (I covered the company for ten years when I lived in Japan.) It’s the steel factor Jimmy Doolittle bombed in the Pearl Harbor movie. US Steel is using 140-year-old technology—Open Hearth Technology—which hasn’t been updated since the Great Depression. Nippon Steel, meanwhile, is promising to scrap all of that and bring the Steel Industry into the 21st Century. All great ideas for Nippon Steel and their shareholders, but not so great for Unions; all of these takeovers always result in massive layoffs of Union workers. So, that is the issue. That’s where a large part of the added value comes from.

Q: What are the chances that interest rates drop to zero?

A: Zero. I don’t think we’ll ever see 0% interest rates again because people now understand the massive damage that causes to the economy and to savers. So, on the next interest rate cycle, we’ll go down maybe to 2% if we get a recession, but probably not much more than that.

Q: Is it a good time to buy FedEx Corp (FDX)?

A: Yes, it probably is. If there was one rule of trading this year, you buy everything on top of these monster selloffs that are caused by weak guidance. We did it on Palo Alto Networks (PANW) earlier this year—people made a fortune on that. FedEx just did the same thing, so yes, I’m looking very carefully at FedEx calls, call spreads, and LEAPS two years out.

Q: I recently saw a recommendation to buy California Utility Company PG&E (PGE) because of recent revenue gains. Should I take a look?

A: Absolutely, you should. PG&E has gone bankrupt twice in the last 25 years, and the current new management seems to know what they’re doing. They borrowed $20 billion to underground all the long-distance power lines in the state so they won’t be liable for any of these gigantic wildfires that caused the last bankruptcy. Also, you kind of want to own utilities when interest rates are falling because utilities are among the biggest borrowers in the country.

Q: Is Global X Uranium ETF (URA) a good proxy for Cameco Corp (CCJ)?

A: Yes, another one is Consolidation Energy Corp. (CEG), but they’ve all had absolutely astronomical moves ever since the announcement came out that Microsoft was reopening the Three Mile Island nuclear power plant. So, wait for a dip, but the thing is just going up every day right now.

Q: Is it time to buy iShares 20+ Year Treasury Bond ETF (TLT) LEAPS?

A: No, LEAPS territory was last year or the beginning of this year when we were in the $80s (and we issued a ton of (TLT) LEAPS last year.) LEAPS are what you do at market bottoms, not at new all-time highs or two-year highs. Remember, if LEAPS don’t work, they can go to zero, and you want to avoid the zero outcome as much as possible.

Q: Should I look at Visa Inc (V)?

A: Yes, this is another one of those poor guidance situations leading to 20% selloffs. In Visa’s case, they’re being sued by the US government for antitrust because they own 47% of the credit card market. So, I would maybe wait a little bit more, let the market fully digest that, and then Visa’s probably a really strong buy because they’re still growing at 15% a year and minting money like crazy.

Q: Do you see gold going to $3,000 next year?

A: Absolutely, yes, unless it goes to $3,000 this year, which raises a better question: what happens when gold hits $3,000? It goes to 4$,500, because Chinese savers have no other place to put their money except gold. The real estate has crashed and isn’t coming back, they don’t trust their own banks or currency—there really is nowhere else for them to put their own money. They don’t even buy gold miners, they just buy the gold metal and coins. So I think we could see much higher highs than gold, and I’m sticking to my longs.

Q: Will silver continue to lag?

A: No. In fact, in the last couple of weeks, silver has done a big catch-up that is happening because recession fears are going away. Even the soft-landing fears are starting to vaporize—we may have no landing at all. The economy may just keep going, and silver is far more sensitive to the economy than gold is; and that is all silver positive. When we get to the metals, you’ll see how much silver has actually caught up. Silver is probably the better buy here because it tends to outperform gold by two to one.

Q: Do you think the Japanese will cross 100 yen to the dollar in the near future?

A: No, but I think it may cross 100 to the dollar in two years. You’re looking at a permanently weak US dollar from now on. As long as we’re cutting interest rates faster than anyone else, our currency will be the weakest. Japan’s rates are at zero, so they’re not going to cut interest rates at all, which is why we've had this enormous move in the Japanese yen.

Q: Can you give me some good renewable energy stocks and reasons why they are good buys?

A: Well, my favorite renewables are the Canadian Uranium stock Cameco Corporation (CCJ), First Solar (FSLR), which has been the leading industrial-scale solar producer for a long time, and NextEra Energy (NEE), which is very heavily dependent on producing electric power from renewables and also have a 3% dividend.

Q: Why is the euro going up even though their economy is in such terrible shape?

A: Europe has much lower interest rates than the US, and therefore, much less ability to cut interest rates than the US; it is the interest rate cuts that are driving currencies down, and we are the world’s greatest interest rates cutter right now. So, that is why you’re getting outperformance of the euro (FXE).

Q: Financials have moved up over the last two weeks; what’s your take on year-end and beyond? Should I buy Goldman Sachs (GS), JP Morgan (JPM) and Morgan Stanley (MS)?

A: Yes on all three. They’re all big beneficiaries of falling interest rates, improving economies, declining default rates, and rising stock markets. So, you have a triple play on all three of those. I’d be buying the dips on all financials.

Q: When will the sell volatility come back?

A: When you get the Volatility Index ($VIX) over $30. That seems to be the sweet spot for selling volatility. We are now at $15.

Q: If the US sharply increases tariffs, what will be the impact on the economy?

A: It would basically amount to a 20% price increase on everything you buy—from clothes to electronic parts to everything else—and the stock market would crash. Probably 90% of the non-food items Walmart (WMT) sells is from China. That’s why they call it the Chinese embassy. Tariffs are a tremendous restraint of trade and never, ever work, except for targeted items like cars or solar panels. For instance, I am in favor of a 100% tariff on Chinese cars to keep them from demolishing our own car industry as they are currently doing in Europe.

Q: Do we expect commodities like copper (FCX) and foodstuffs to go up as rates are cut?

A: I do. They’re big beneficiaries of falling rates, but more importantly, they’re even bigger beneficiaries of a stimulated Chinese economy, and that’s why we see these monster moves over the last two days.

Q: If you had to invest in one rideshare company, would it be Lyft (LYFT) or Uber (UBER)?

A: Uber—they have far superior management, they’ll be the first into robo-taxis, and they are constantly evolving their model, with Lyft always struggling to catch up.

Q: How will antitrust regulation affect the Magnificent Seven?

A: The bottom line is it will double the value of the Magnificent Seven. If these companies are broken up, the individual parts are worth far more than the whole companies, and we saw this when we broke up AT&T (T) 50 years ago, and the resulting seven companies within a year had a combined market value that vastly exceeded the original AT&T. I actually participated in that deal when I was at Morgan Stanley (since I am 6’4” I was asked to carry the ballots from one floor to another). Expect the same to happen with the Magnificent Seven. They will be worth double or triple more.

Q: If China has a falling population, how will a stimulus program help?

A: Well, it will fill in for the 600 million consumers who were never born as a result of the one-child policy. Not many others are talking about this besides me, but the fact is that the current economic weakness comes entirely from the one-child policy, and there is no way out of that, so they are going to have to keep stimulating again and again, much like the US did through the pandemic.

Q: If you can buy gold and silver on the UK market in sterling, does that make more sense for a UK resident?

A: Yes, it does, since your home currency is in sterling. You will actually get a double play or a “hockey stick effect” because not only is gold going up against the US dollar, but sterling (FXB) is going up against the US dollar, so you’ll get a multiplied effect relative to the pound. We used to play this all day long in Europe in the 1970s and 1980s, back when you had individual currencies to trade and the euro hadn’t been invented yet.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

It’s hard to believe that Uber (UBER), the ride-sharing company, is where it’s at now and by that, I mean delivering profits.

It was just only a few years ago when burning money was something they were known for and beginning the next lender to fund them was a common request.

That was the era of cheap money where 0% interest rates created companies like Uber and this capital was the oxygen they needed to keep trying until they could make it work.

Much of the early years were characterized by a fierce competition with competitor Lyft (LYFT) offering subsidies to drivers.

Fast forward to today and they also have a sparkling food delivery business and are projected to continue to grow in the first quarter of 2024.

The company carved out a profit of $1.43 billion in the final three months of 2023, which included a $1 billion benefit from its equity investments as well as income from its operations.

The company has turned an annual profit once before, in 2018 on the back of its investments, but it wasn’t earning money from its operations until now.

The company’s performance in the last three months of 2023 suggests that demand for its ride-sharing and food-delivery services remains robust.

From 2016 through the first quarter of 2023, Uber bled cash close to $30 billion in operating losses.

The company posted its first quarterly operating profit in the second quarter of 2023. The company was founded in 2009.

It was also better than Lyft at responding to a sudden driver shortage after the economy reopened from lockdowns. That helped Uber gain market share.

Lyft is still twisting in the wind of mediocrity and has yet to post its first operating profit.

Uber expanded advertising on its app over the past year. It says it has continued to become more disciplined about spending on discounts to consumers and incentives to drivers. It says it has also become better at combining deliveries and reducing errors, which has improved its operational efficiency.

In the last three months of 2023, the company’s mobility revenue grew 34% and its delivery revenue expanded 6%, while its revenue from freight declined 17%.

After bottoming around $19 per share in the middle of 2022, the stock has been on a rampage and now sits nicely at over $81 per share.

No doubt the stock benefited from last year's slew of capital betting on the Fed to drop interest rates.

I even anointed Uber as my number 1 stock of 2023 and their performance delivered in spades.

What we are witnessing is the maturity of the company and I am not saying they are going to deliver profit back to the shareholder like a FANG, but the conversation will start and that should carry momentum.

The US economy is still going strong growing a few percentage points per quarter and that means US consumers are still spending and that is good for ride-sharing and food delivery.

Uber is sitting nicely as they are a monopoly in this area of technology services.

I am bullish Uber.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-02-16 14:02:212024-02-16 11:45:59The Ride Sharing King of Tech

Who is responsible when artificial intelligence harms someone?

The California jury may soon have to make a decision. In December 2019, a man driving a Tesla (TSLA) with an AI navigation system killed two people in an accident. The driver faces up to 12 years in prison.

These events were bound to happen as teething pains are quite common with new technology especially one that is ambitious enough to transport machines in a human world.

Multiple federal agencies are investigating Tesla crashes, and The California Department of Motor Vehicles is investigating the use of AI-controlled driving functions.

Our current liability system used to determine liability and compensation for injuries is not AI-friendly.

Liability rules were designed for a time when humans caused most injuries.

However, with AI, errors can occur without direct human intervention. The liability system must be adjusted accordingly. Poor accountability won't just stifle AI innovation. It will also harm patients and consumers.

It's time to start thinking about accountability as AI becomes ubiquitous but remains under-regulated. AI-based systems have already contributed to injuries.

The right accountability approach is critical to unlocking the potential of AI. Uncertain regulations and the prospect of costly litigation will deter investment, development, and deployment of AI in industries ranging from healthcare to autonomous vehicles.

Currently, liability claims typically begin and end with the person using the algorithm. Of course, if someone abuses the AI system or ignores its warnings, that person should be held accountable.

But AI errors are often not the user's fault. Who can blame an emergency doctor for letting an AI algorithm miss papilledema — a swelling of part of the retina?

AI's failure to detect the disease could delay care and potentially cause the patient to lose their eyesight. Papilledema is difficult to diagnose without an ophthalmologist.

AI is constantly self-learning, which means it takes in information and looks for patterns in it. This is a "black box" that makes it difficult to understand which variables affect the outcome.

The key is to ensure that everyone involved - users, developers, and everyone else in the chain - has been vetted to keep AI safe and effective.

First, insurers should protect policyholders from AI injury litigation costs by testing and validating new AI algorithms before deploying them.

Car insurers have also been comparing and testing cars for years. An independent security system can provide AI stakeholders with a predictable system of accountability that adapts to new technologies and practices.

Second, some AI errors should be challenged in courts that specialize in uncommon cases. These tribunals may specialize in particular technologies or topics.

Third, proper regulatory standards from federal agencies can offset the excessive liability of developers and users. For example, some forms of medical device liability have been superseded by federal regulations and laws. Regulators should focus on standard AI development processes early on.

Regulation can make or break AI in the upcoming years and I lean towards the laissez-faire attitude of deregulation.

Too many regulations will stifle development and bring about undue costs.

No company will continue with loss-making operations unless they see a light at the end of the tunnel.

If allowed to develop with light regulation, AI will be that supercharger to tech stocks that investors dreamed of.

Transportation-based tech stocks such as Uber and Lyft will be one of the largest winners from the widespread implementation of driverless technology.

Also, throw in there the food delivery companies like DoorDash (DASH).

Another group with immense expense-saving possibilities is all the airline firms around the world because theoretically, self-driving technology will become good enough to deploy in short and long-haul flights.

Getting to the point of consumers and regulators fully trust self-driving technology is still a long and windy path, but I do believe we will arrive there.

When we do get there, the tech companies underwriting these benefits will feel a 10X boost to their share price.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-11-29 14:02:042023-11-29 14:49:41Dealing With A Black Box

Who is responsible when artificial intelligence harms someone?

The California jury may soon have to make a decision. In December 2019, a man driving a Tesla (TSLA) with an AI navigation system killed two people in an accident. The driver faces up to 12 years in prison.

These events were bound to happen as teething pains are quite common with new technology especially one that is ambitious enough to transport machines in a human world.

Multiple federal agencies are investigating Tesla crashes, and The California Department of Motor Vehicles is investigating the use of AI-controlled driving functions.

Our current liability system, used to determine liability and compensation for injuries, is not AI-friendly.

Liability rules were designed for a time when humans caused most injuries.

But with AI, errors can occur without direct human intervention. The liability system must be adjusted accordingly. Poor accountability won't just stifle AI innovation. It will also harm patients and consumers.

It's time to start thinking about accountability as AI becomes ubiquitous but remains under-regulated. AI-based systems have already contributed to injuries.

The right accountability approach is critical to unlocking the potential of AI. Uncertain regulations and the prospect of costly litigation will deter investment, development, and deployment of AI in industries ranging from healthcare to autonomous vehicles.

Currently, liability claims typically begin and end with the person using the algorithm. Of course, if someone abuses the AI system or ignores its warnings, that person should be held accountable.

But AI errors are often not the user's fault. Who can blame an emergency doctor for letting an AI algorithm miss papilledema — a swelling of part of the retina?

AI's failure to detect the disease could delay care and potentially cause the patient to lose their eyesight. Papilledema is difficult to diagnose without an ophthalmologist.

AI is constantly self-learning, which means it takes in information and looks for patterns in it. This is a "black box" that makes it difficult to understand which variables affect the outcome.

The key is to ensure that everyone involved - users, developers, and everyone else in the chain - has been vetted to keep AI safe and effective.

First, insurers should protect policyholders from AI injury litigation costs by testing and validating new AI algorithms before deploying them.

Car insurers have also been comparing and testing cars for years. An independent security system can provide AI stakeholders with a predictable system of accountability that adapts to new technologies and practices.

Second, some AI errors should be challenged in courts that specialize in uncommon cases. These tribunals may specialize in particular technologies or topics.

Third, proper regulatory standards from federal agencies can offset the excessive liability of developers and users. For example, some forms of medical device liability have been superseded by federal regulations and laws. Regulators should focus on standard AI development processes early on.

Regulation can make or break AI in the upcoming years and I definitely lean towards the laissez faire attitude of deregulation.

Too many regulations will stifle the development and bring about undue costs.

No company will continue with loss-making operations unless they see a light at the end of the tunnel.

If allowed to develop with light regulation, AI will be that supercharger to tech stocks that investors dreamed of.

Transportation-based tech stocks such as Uber and Lyft will be one of the largest winners from the widespread implementation of driverless technology.

Also, throw in there the food delivery companies like DoorDash (DASH).

Another group with immense expense-saving possibilities is all the airlines around the world because theoretically, self-driving technology will become good enough to deploy in short and long-haul flights.

Getting to the point of consumers and regulators fully trusting self-driving technology is still a long and windy path, but I do believe we will arrive there.

When we do get there, the tech companies exposed to these great benefits will feel a 10X boost to their share price.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-03-06 16:02:202023-03-28 15:01:56Dealing With a Black Box

They are and will continue to be the largest influencer in tech share price action in the short-term and the last 2 days has proved it.

Whatever you think or say about the equity market, we can’t hide from the truth that liquidity will either wreak havoc on short-term price action or shoot it to the moon like we saw post-Fed announcement about the latest rate hike.

Tech shares lifted off like an Elon Musk spaceship to Mars and the Mad Hedge Technology Letter was tactical enough to take profits on a DocuSign (DOCU) put spread and stomp out in Meta (META) before the earnings report.

I was able to add some additional long tech as Friday is proving to benefit from the spillover effect.

No matter how we view it, volatility isn’t going anywhere any time soon.

Why?

Since January 2020, the US has printed nearly 80% of all US dollars in existence.

Lots of fiat paper sloshing around in the system has many unintended consequences.

When pushed into certain asset classes, the hot money polarizes price action. That’s how we got all the meme stock craziness.

This phenomenon won’t be going away anytime soon and the Fed slowly reducing their asset sheet pales in comparison to the liquidity hanging around on the sidelines.

The Fed hike means short-term rates now stand at between 4.5%-4.75%, the highest since October 2007.

The move marked the eighth increase in a process that began in March 2022. By itself, the fund's rate sets what banks charge each other for overnight borrowing, but it also spills through to many consumer debt products.

Tech shares took off because Chairman Powell acknowledged that “the disinflationary process” had started.

In a blink of an eye, the Nasdaq was up 2% and growth stocks were up 5%.

Powell intentionally didn’t pour cold water on the rally when he had a chance to smash it down with more hawkish rhetoric or a 50 basis point hike.

It appears highly likely that Powell isn’t interested in tech stocks or any equities for that matter experiencing another bloodbath like 2022.

There might be pitchforks out for him if there is a 30% loss in major indexes this year and perhaps he is scared that Washington would bring the heat. He likes his cushy job and the benefits that come with it.

I do believe this is only the first of a series of Powell Houdini acts where he is willing to disappear behind any sort of opportunity to smash down the markets and let them run wild.

Tech stocks will be a natural buy-the-dip opportunity during this deflation narrative.

We have a clear runway from 6.5% inflation to around 4% and during this 2.5% deflation drop, I can easily see the Nasdaq lurching higher.

I used Friday to add a bullish position in Lyft (LYFT) and Amazon (AMZN) after their terrible earnings while I took almost maximum profit in our Netflix (NFLX) call spread.

It was almost as if Powell announced a new round of QE or, well, sort of.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-03 16:02:302023-03-02 00:24:52Hi Beta Is Suddenly Hot

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.