CEO of Uber (UBER) Dara Khosrowshahi earns 200X the salary of the median Uber employee and for that large sum of money, he lost the company $5.9 billion in just the first quarter.

The company is a perennial cash burner, and they haven’t shown us how they will fix this problem.

The company can dish out as many “positive outlooks” as it wants, but rest assured, they usually just move the goalposts and put some lipstick on a pig to dress up even more astronomical losses coming down the pipeline.

Uber’s management obviously did a bad job messaging their “positive outlook” as the share price opened up down 11% in today’s trading.

The time has come to pay the bill for this company and it’s not pretty.

They didn’t come anywhere close to becoming profitable during generational low-interest rates, and now, their prospects look bleak as we barrel towards a world with vastly higher borrowing costs.

Sure, the revenue doubled, but drivers aren’t making any money with such high gas prices and Uber has had to shell out more for labor and that’s not coming down any time soon.

In fact, if there was one tech company that would perform awful in high inflationary conditions, this is the company.

Not only that, but Uber’s service now is also just way too expensive, take a ride, and they charge consumers way more than its worth.

Unless it's 2 in the morning and there is no means back home, consumers won’t rush to order an Uber unless it’s an emergency.

I expect a shortage of drivers to continue as working for Uber as a driver is really bottom-of-the-barrel type of stuff and why do it during a time where labor rights are on the rise?

Remember they had to present a ballot for voters to get them classified as subcontractors and spent $200 million on it.

Investors must have pondered if this $200 million would have been better invested in the actual business instead of ripping off their own employees.

The intensifying competition for labor is also revealing the different ways in which ride-hailing giants are tackling the issue. Uber said it has been making tweaks to the driver app, like unlocking the ability to see upfront fares before accepting a ride, improving maps, and removing bugs.

Uber management touts Uber Eats as the savior of its business but then this company should be valued as a food delivery company with a lower multiple.

Uber eats is still losing money with no end in sight and one must conclude that it appears as if this “tech” firm has no chance of ever becoming profitable based on this current business model.

I fully expect Uber eats to burn more cash as food inflation goes from bad to awful which will mean demand destruction of its customers.

These customers can easily substitute Uber eats services by ordering supermarket delivery and throwing a frozen pizza in the oven.

Uber eats service is a luxury, not a necessity as many Americans cut back on spending because of major economic policy mistakes by the US Central Bank and the current White House administration.

It’s not a shocker to fin

d out that in the 3 years of Uber’s stock being public, shares have gone down 35% since the IPO in dreamy financial conditions with unlimited investment appetite for inferior tech companies.

The stock currently trades at $26 per share, and I would say this stock would be a good short-term trade at around $17.

Lastly, Uber’s way of saying they are a good tech company is by describing themselves as “not Lyft” and that right there is a massive smokescreen.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-05-04 15:02:382022-05-04 15:43:00Ride-Sharing Needs a Facelift

The raging war in Ukraine and Russia will have repercussions for the American tech sector.

Many of these unintended consequences are lurking in the shadows and don’t fully appear until we are further down the road, but one glaring consequence we can expect imminently is higher inflation.

The higher inflation input first revolves around rising energy prices and big moves in the price of crude indicate that prices at the pump will surge throughout the duration of this Eastern European war.

Russia is one of the world's largest exporters of oil and gas. If US, European sanctions and Russia's responses drive up oil and gas prices, Russia's export revenues will rise and help pay the sanctions' costs. In contrast, rising oil and gas prices will feed US inflation.

The more the war is prolonged, the higher likelihood that oil will stay above $100 per barrel and the psychological effect of high gas prices will stay with the consumer for longer.

Even more ironic, the Russian Ruble crashing more than 30% this morning also means that Russia can reduce its energy offerings to the outside world by 25% yet still make a positive 5% nominal return on the energy exports.

Russia could pull back supply as the next chess move on the board and a barrel of oil could launch to upwards of $140 a barrel meaning that Americans could be paying $7 or $8 per gallon in California and Nevada.

People forget that Ukraine is sitting tight and defending while being supplied by Europe from the West.

This includes arms from the US brought down from Latvia, gas from Slovakia, and a smorgasbord of supplies and aid from other European countries.

Logistically, Russia needs to ship everything from mainland Russia including weapons, food, energy, and equipment.

Distances are far in Russia and this will quickly add up to an expensive war for Russia with reports showing that Russia is spending around $20 billion per day to finance this war.

Along with navigating higher energy prices at the pump, ride-sharing platform Uber (UBER) and Lyft (LYFT) are testing a new driver earnings algorithm in 24 U.S. cities that allows drivers to see pay and destinations before accepting a trip, and raises the incentives for drivers to take short rides in an effort to attract more drivers.

Labor supply has been a major problem for Uber and Lyft who can’t convince drivers to work for them.

The unit economics simply don’t make sense when inflation has meant expenses have spiked to the detriment of gig economy driver supply.

The changes, which are currently in pilot programs, mark the most wide-ranging updates to Uber's driver pay algorithm in years and come at a time when the company is still trying to win back drivers who left at the start of the pandemic.

Fortunately for Uber, even with headwinds of high energy prices and labor bottlenecks, the post-Omicron economic tailwind should keep Uber shares rangebound in the short-term with a slant towards the upside.

The setup to Uber and Lyft’s next earnings report is also ominous with projections looking hard to beat with the exogenous forces piling up.

Lyft and Uber continue to be a buy the dip and then sell the rally stock on high volatility.

Their lack of quality really suffers in tougher tech market conditions.

It’s true that the painfully delayed response not only to Russia’s offensive in Ukraine will cause higher prices, but the cost will certainly be high as the Western world could have snuffed this out years ago when Russia took over parts of Georgia or annexed Crimea.

The bill is now due, and Germany will initially pay 100 billion euros to liven up their military and this is most likely the beginning of the West finally stopping its policy of turning a blind eye to Eastern European dictators.

More expensive Uber and Lyft rides, higher driving expenses, surging fuel costs will keep the stock in check.

However, considering the stock is way oversold at this level, the tailwinds blowing at their sails means shares will grind up slowly as the Fed raises rates slower than expected.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-02-28 16:02:122022-03-04 00:35:46Mixed Bag for Ride-Sharing Platforms

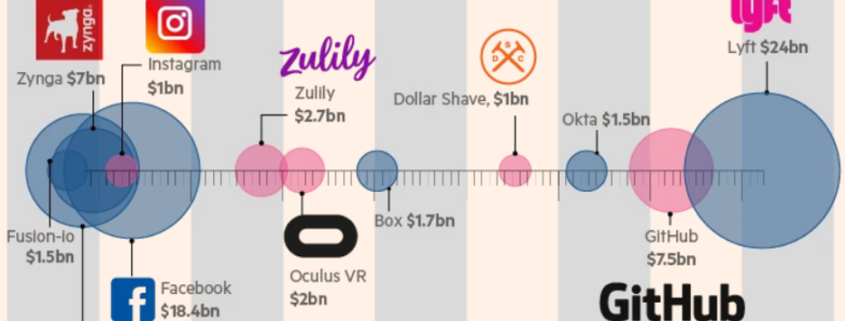

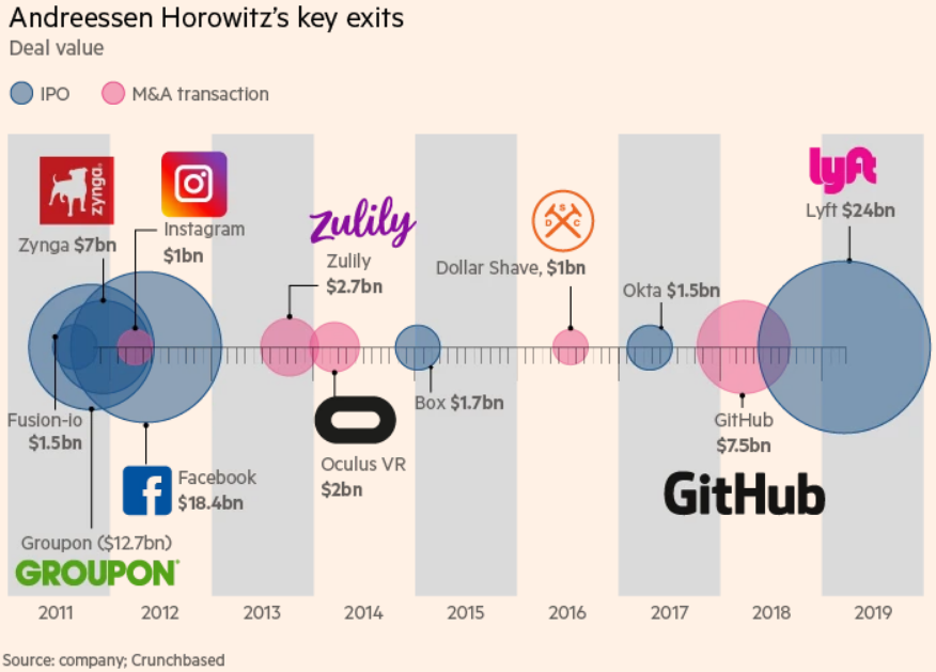

It’s not easy to be the genius who doled out early seed money to Facebook (FB), Foursquare, GitHub, Pinterest (PINS), Lyft (LYFT) and Twitter (TWTR), among others.

These investments turned out to be highly successful. If someone even miraculously hit on one of these, your grandchildren would know about it.

This person even acquired a majority stake in Skype for $2.75 billion which was considered highly risky at the time and offloaded it to Microsoft in 2011 for $8.5 billion.

Not everyone can do this like Silicon Valley tech investment maestro Marc Andreessen.

Behind the public markets is angel investing and the data says that these investments fail over 50% of the time for the best of breed like Andreesen.

There are simply too many variables that can derail these profit models which nobody can predict.

To lose over half the time and claim to be an outsized winner means relying on those 10 or 100-baggers or might I even say 1,000-baggers to drag up the portfolio performance.

These are the guys who were buying bitcoin (BTC) at 10 cents on the dollar.

Truthfully, investing in startup companies is not for everyone considering there is over a 50% chance a company will end at a 0 or pennies on the dollar.

However, it can be highly gratifying if and when the investments do pay off and investors get a front seat to the forefront of the tech innovation cycle, which you simply don’t get by trading Facebook and Google from your Fidelity account on your computer screen.

These investors can also get direct access to the chatter while creating a rich network of tech know-how; and I do believe that’s half the value in it too, since it can propel angel investors to the next super app or guy behind the next super app.

I mean who could have ever predicted a global health crisis that’s going into its 3rd year soon? And who will be able to nail the knock-on effects of climate change.

That is why risking losing one’s shirt is a real possibility if they bet the ranch on an unknown entity.

Everybody wants the next Tom Brady to quarterback their team, but who knows who the next Tom Brady is at 18 years old?

Even though Andreessen hits on less than 50% of his ideas, the industry median is around 17%, showing how superior his performance is.

He definitely has this thing figured out on relative terms.

Let’s define Angel Investor.

An angel investor is a high-net-worth individual who provides financial backing for small startups or entrepreneurs, typically in exchange for ownership equity in the company.

The funds that angel investors offer could be one-off investments to help the business get off the ground or in drip injection form to support and carry the company through its difficult early stages, which means burning cash.

Most of these companies don’t make money for the first 10-years and that time is usually a referendum on the quality of the idea; very few stand the test of time.

The potential to make 100-baggers is out there with subsectors like fintech already worth half a trillion dollars in 2020 and with a predicted annual growth rate of 35%.

Angel investors typically require a 35-40% return on the money they invest in a company minus costs and inflation to call it a winner.

But Venture Capitalists may take even more, especially if the product is still in development. For example, an investor may want 50% of the business to compensate for the high risk it is taking by investing in a startup.

Angel investors do the jobs of banks.

Traditional banks would never lend to an entity based on a half-built product or even a genius idea.

Proof of income and debt to income ratios are realities at banks.

When net profits are negative, the balance sheet is too ugly for banks to even think about doing any business with these startups.

Therefore, there are limited pathways for entrepreneurs to find capital, and many turn to Angel investors to help startups take their first steps.

Who Can Be an Angel Investor?

Angel investors are normally individuals who have gained "accredited investor" status, but this isn’t a prerequisite. The Securities and Exchange Commission (SEC) defines an "accredited investor" as one with a net worth of $1M in assets.

Essentially these individuals both have the finances and chutzpah to provide funding for startups. This is welcomed by cash-hungry startups who find angel investors to be far more appealing than other, more predatory, forms of funding.

These private funds usually draw up opportunities for a defined exit strategy, acquisitions or initial public offerings (IPOs).

Liquidity events is what makes everyone happy at the end except for the investors who missed the boat.

It’s even possible that an angel investor only sees growth in the first 5 years and unloads the “idea” to another private investor for a profit.

Private market deals are common because of the excess of liquidity brought on by the U.S. Central Bank lowering interest rates for a prolonged amount of time.

What I do know is that America is the framework within which almost all unicorns prosper, and I do not envision any monumental shift to Europe or China, these other places simply have more problems than the U.S.

How does the normal Joe get it on the action?

Andreesen has said the only way he usually does business is with a “warm” introduction which can be hard to come by if one doesn’t rotate in the same social circles as these heavy hitters.

Scoring a warm introduction also means getting boots on the ground in California which is ebbing and flowing between its colossal wildfires and public health issues like many other places.

Honestly speaking, if might be difficult to get the best of the best angel opportunities even if the gunpowder is loaded.

It’s accurate to believe that probably guys like Andreesen get the best of the best ideas in front of them and if they pass on it, the likes of Sequoia, Benchmark, and Softbank have very smart people as well who get similar type of presentations and opportunities.

Like you correctly guessed, this private group of capital is quite incestuous and tight-knit. It’s a copycat league of the ages.

The one avenue that might be of interest is a platform that has democratized angel investing who on the last count had close to 1,000 companies looking for start-up capital.

I won’t stand here saying this is the cream of the crop because it’s not, but I will say that sometimes companies are overlooked, or the industry consensus has shifted too far in one direction offering undiscovered dark horses a chance.

Lastly, this forum of angel companies on offer does give analysts insight into where money is funneled to and the current hot sub-sector of the tech industry.

This platform even offers an Angel index fund if a reader wants to take the aggregate performance of 150-200 companies with a $50,000 minimum.

If a reader wants access to facilitate angel investing by a deal-by-deal offer from the Angel list as a professional investor, then $500,000 is required.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/andreessen.png672936Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-16 15:02:112021-08-24 17:28:36How To Be A Tech Angel Investor

Below please find subscribers’ Q&A for the June 16 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Lake Tahoe, NV.

Q: Does Copper (FCX) look like a buy now or wait for it to drop?

A: I would buy ⅓ now, ⅓ lower down, ⅓ lower down still. Worst case we get down to $30 in Freeport McMoRan (FCX) from $37 today. A new internal combustion engine requires 40 lbs. of copper for wiring, but new EVs require 200 lbs. per car, and the number of EV cars is about to go from 700,000 last year to 25 million in 10 years. So, you can do the math here. It's basically 24.3 million times 200 lbs., or 1.215 billion tons, and that's the annual increase in demand for copper over the next 10 years. There aren’t enough mines in the world to accommodate that, so the price has to go up. However, (FCX) has gone up 12 times from its 2020 low and was overdue for a major rest. So short term it's a sell, long term it's a double. That's why I put the LEAPS out on it.

Q: Lumber prices are dropping fast, should I bet the ranch that it’ll drop big?

A: No, I think the big drop has happened; we’re down 40% from the highs, the next move is probably up. And that is a commodity that will remain more or less permanently in short supply due to the structural impediments put into the lumber market by the Trump administration. They greatly increased import duties from Canada and all those Canadian mills shut down as a result. It’s going to take a long time to bring those back up to speed and get us the wood we need to build houses. Another interesting thing you’re seeing in the bay area for housing is people switching over to aluminum and steel for framing because it’s cheaper, and of course in an earthquake-prone fire zone, you’d much rather have steel or aluminum for framing than wood.

Q: I didn’t catch the (FCX) LEAP, can you reiterate?

A: With prices at today's level, you can buy the 35 calls in (FCX), sell short the 40 calls, and get nearly a 177% return by January 2022. That's an absolute screamer of a LEAPS.

Q: How do you see the working from home environment in the near future after Morgan Stanley (MS) asked everyone to return?

A: Well that’s just Morgan Stanley and that’s in New York. They have their own unique reasons to be in New York, mostly so they can meet and shake down all their customers in Manhattan—no offense to Morgan Stanley, but I used to work there. For the rest of the country, those in remote places already, a lot of companies prefer that people keep working from home because they are happier, more productive, and it’s cheaper. Who can beat that? That’s why a lot of these productivity gains from the pandemic are permanent.

Q: Is there a recording of the previous webinar?

A: Yes, all of the webinars for the last 13 years are on the website and can be accessed through your account.

Q: What makes Microsoft (MSFT) a perfect-looking chart?

A: Constant higher lows and higher highs. They also have a fabulous business which is trading relatively cheaply to the rest of tech and the rest of the main market. Of course, they were a huge pandemic winner with all the people rushing out to buy PCs and using Microsoft operating software. I expect those gains to improve. The new game now is the “wide moat” strategy, which is buying companies that have near monopolies and can’t be assailed by other companies trying to break into their businesses. The wide moat businesses are of course Microsoft (MSFT), Amazon (AMZN), Facebook (FB) and Alphabet (GOOGL). That's the new investment philosophy; that's why money has been pouring back into the FANGs for a month now.

Q: Do you have any concerns about Facebook’s (FB) advertising ability, given the recent reduction of tracking capabilities of IOS 4.5 users?

A: Well first of all, IOS 4.5 users, the Apple operating system, are only 15% of the market in desktops and 24% of mobile phones. Second, every time one of these roadblocks appears, Facebook finds a way around it, and they end up taking in even more advertising revenue. That’s been the 15-year trend and I'm sticking to it.

Q: Is Caterpillar (CAT) a LEAP candidate right now?

A: Not yet, but we’re getting there. Like many of these domestic recovery plays, it is up 200% from the March lows where we recommended it. The best time to do LEAPS is after these big capitulation selloffs, and all we’ve really seen in most sectors this year is a slow grind down because there's just too much money sitting under the market trying to get into these stocks. Let’s see if (CAT) drops to the 50-day moving average at $185 and then ask me again.

Q: If you have the (FCX) LEAPS, should you keep them?

A: I would keep them since I'm looking for the stock to double from here over the next year. If you have the existing $45-$50 LEAPS, I would expect that to expire at its max profit point in January. But you may need to take a little pain in the interim until it turns.

Q: Should I bet the ranch on meme stocks like (AMC) and GameStop GME)?

A: Absolutely not, I’m amazed you haven't lost everything already.

Q: Do you think Exxon-Mobile (XOM) could rise 30% from here?

A: Yes, if we get a 30% rise in oil. We are in a medium-term countertrend rally in oil which will eventually burn out and take us to new lows. Trade against the trend at your own peril.

Q: Disneyland (DIS) in Paris is set to open. Is Disneyland a buy here?

A: Yes, we’re getting simultaneous openings of Disneyland’s worldwide. I’ve been to all of them. So yes, that will be a huge shot in the arm. Their streaming business is also going from strength to strength.

Q: How long will the China (FXI) slowdown last?

A: Not long, the slowdown now is a reaction to the superheated growth they had last year once their epidemic ended. We should get normalized growth in China at around 6% a year, and I expect China to rally once that happens.

Q: Have you changed your outlook on inflation, real or imagined?

A: I don’t think we’re going to have inflation; I buy the Fed's argument that any hot inflation numbers are temporary because we’re coming off of a one-on-one comparisons from when the economy was closed and the prices of many things went to zero. If you look at that inflation number, it had trouble written all over it. Some one third of the increase was from rental cars. One of the hottest components was used cars. You’re not going to get 100% year on year increases next year in rental or used cars.

Q: When you issue a trade alert, it’s always in the form of a call spread like the Microsoft (MSFT) $340-$370 vertical bull call spread. What are the pros and cons of doing this trade on the put side, like shorting a vertical bear put spread?

A: It’s six of one, half a dozen of the other. There are algorithms that arbitrage between the two positions that make sure that they’re never out of line by more than a few cents. I put out call spreads because they’re easier for beginners to understand. People get buying something and watching it go up. They don’t get borrowing something, selling it short, and buying it back cheaper.

Q: Will gold (GLD) prices go up?

A: Yes, when inflation goes up for real.

Q: What is the future of the gig economy? How will that affect Uber (UBER) and Lyft (LYFT)?

A: I like both, because they just got a big exemption from California on part time workers, and that is very positive for their business models.

Q: Do you think the government doesn’t want to cancel student debt because it will unleash inflation?

A: It’s the exact opposite. The government wants to forgive student debt because it will unleash inflation. If you add 10 million new consumers to the economy, that is very positive. As long as former students have tons of debt, horrible credit ratings, and are unable to buy homes or get credit cards, they are shut out of the economy. They can’t participate in the main economy by buying homes, shopping, or getting credit. The fact that the US has so many college grads is why businesses succeed here and fail in every other country. That should be encouraged.

Q: Where is the United States US Treasury Bond Fund (TLT) headed?

A: Short term up, long term down.

Q: Options premiums are not melting away much today; I hope they start decaying after the Fed announcement.

A: In these elevated volatility periods—believe it or not, the (VIX) is still elevated compared to its historic levels—they hang on all the way to the very last day, before expiration, before they really melt the time value on options. It really does pay to run these into expiration now. When the VIX was down at like $9-$10, that was not the case.

Q: I bought a short term expiration going long the (TLT) to hedge my position; was this smart?

A: Yes, but only if you are a professional short-term trader. If you are in front of your screen all day and are able to catch these short term moves in (TLT), that is smart. My experience is that most individual investors don’t have the experience to do that, don’t want to sit in front of a screen all day, and would rather be playing golf. Such hedging strategies end up costing them money. Also, remember that half of the moves these days are at the opening; they’re overnight gap openings and you can’t catch that intraday trading—it’s not possible. So over time, the people who take the most risk make the most money. And that means the people who don’t hedge make the most money. But you have to be able to take the pain to do that. So that’s my philosophy talk on risk taking.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trade

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/john-beer.png437510Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-06-18 10:02:382021-06-18 14:13:32June 16 Biweekly Strategy Webinar Q&A

Uber (UBER) is a solid tech investment for the remainder of 2021, and this is me saying that when I don’t even like their company business model.

The biggest gap up in shares usually occurs when a company goes from flat-out terrible to the level just above that and that’s what is happening to Uber in 2021.

Why have they been so bad lately?

Uber’s Mobility gross bookings, or ride-sharing revenue, was $6.8 billion, which was down 47% year on year and revenue of only $1.5 billion.

Uber was never profitable, to begin with, not even close, and for COVID to gut their main business in 2020, investing in shares became even less appetizing.

Or were they?

Ironically enough, the California ride-sharing company was able to compensate during the pandemic by delivering food, a very non-tech type of business.

Delivery revenue of $1.4 billion, up 220%, significantly outpaced gross bookings growth and delivery revenues take rate was 13.5%, up 391 basis points year on year and up 21 basis points quarter on quarter.

Not only did the delivery revenue become almost equal to its ride-sharing revenue in such a short time span, but their “take rate” nudged up which is measured as the percentage of what they accrue from each $1 in delivery.

The momentum allowed Uber to triple its shares from March 2020 lows on the back of a reinvigorated delivery service, trillions of printed money, and a broad-based rally that swept up Uber.

Trust me, Uber doesn’t own any worthwhile intellectual property that is going to differentiate itself from the competition, but they are part of a duopoly with Lyft (LYFT) that makes 2021 so intriguing.

Reading the 2021 tea leaves, it's hard not to love this company as tourism, outdoor mobility, and intercity mobility will reverse and people will start paying uber for rides to go to bars and house parties.

Uber indicated just that with a teaser report before the real earnings come out showing that total gross bookings as of March 2021 reached the highest monthly level in the company's nearly 12-year history.

Mobility posted its best month since the pandemic started in March 2020, passing a $30B annualized gross bookings run rate. Average daily gross bookings were up 9% month-over-month.

Delivery set another all-time record, crossing $52B annualized gross bookings run rate in March, up over 150% on the year.

Uber says the rideshare business recovery and continuing Eats demand have customers outpacing the number of drivers and couriers.

The company ended the Form 8-K on a down note, letting investors know that after a court order, Uber must reclassify UK drivers as employees.

The company expects to record a “significant accrual” due to higher British employment costs in Q1 with the majority expected to reduce total and mobility revenues and revenue take rates but will be excluded from adjusted EBITDA results.

I must say that it’s quite irresponsible of management to just slide this “significant accrual” off the balance sheet as it could turn into something major if other big markets similar to London force Uber to reclassify workers as employees.

This is by far the biggest risk moving forward in 2021, but I doubt that other European locales will have the balls to say no to Uber.

Management reiterated that they remain on track to turn the EBITDA profitable in 2021, but then again, the EBITDA is quite substantial which is a management trick that needs to be banned in corporate America.

I believe that management keeps moving the goalposts by trying hard to please the incremental investor with alternative metrics, but that doesn’t take away from the immense potential of the back half of 2021.

Uber is poised to seriously outperform as people have been quarantined inside for over a year now and are waiting to explode out of their front door.

The company has burnt through over $15 billion in cash since 2019 and the stock has tripled, after stripping out a decline in food deliveries later this year, I believe the strength in rideshare revenue will end up with Uber having some quite rosy numbers.

Call it a net positive after you minus out the delivery revenue which is poised to shrink in the latter half of the year.

Thus, I will stamp Uber with a short-term and medium-term conviction buy, but a long-term sell because I just don’t see a pathway yet to become a heavy hitter, and Uber’s accounting gimmicks are a red flag.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/04/uber.png406812Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-14 14:02:062021-04-20 00:00:10A 2021 Tech Darling

Mad Hedge Technology Letter November 9, 2020 Fiat Lux

Featured Trade:

(UBER BACK FROM PURGATORY) (UBER), (LYFT), (GRUB)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-11-09 11:04:252020-11-09 11:37:07November 9, 2020

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.