Global Market Comments

September 29, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOVERNMENT SHUTDOWN IS HERE)

(SPY), ($INDU), (IWM), (V), (MA), (AXP), (UNG),

(CCJ) (XOM), (OXY) (DUK) (TAN), (FSLR)

Global Market Comments

September 29, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOVERNMENT SHUTDOWN IS HERE)

(SPY), ($INDU), (IWM), (V), (MA), (AXP), (UNG),

(CCJ) (XOM), (OXY) (DUK) (TAN), (FSLR)

Global Market Comments

November 28, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LOOKING FOR BIG FOOT),

(NVDA), (VIX), (TLT), (TSLA), (XOM),

(OXY), (TSLA), (SPY), (MA), (V), (AXP)

On October 14, investors finally achieved the portfolios they long desired, not only individuals but institutional ones as well. They got rid of stocks and bonds that had been hobbling them all year and built their cash positions to decade highs.

What happened the next day?

Stocks and bonds went straight up for six weeks. Cash became trash.

For October 14 was the day that the stock market discounted the worst-case economic scenario for 2023, no matter how bad it may get. And it probably won’t get very bad. That’s barring a black swan-type event, like a brand-new global pandemic.

If you think your job can be frustrating, how about mine? If you run with the dumb crowd, the uninformed crowd, the loser crowd, you get your just desserts.

Fortunately, I saw these moves coming a mile off and loaded the boat. I’ve actually made more money on the parabolic move in bonds than some of the enormous moves in stocks. NVIDIA (NVDA) up 50%?

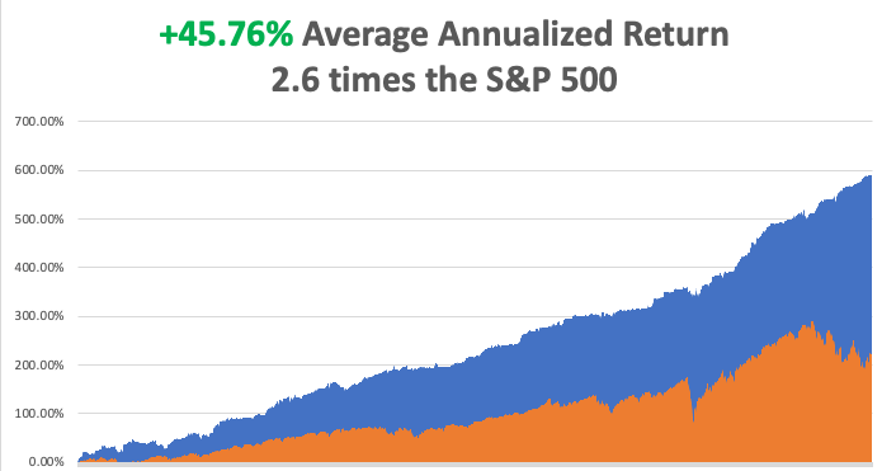

My performance in November has so far tacked on another robust +7.05%. My 2022 year-to-date performance ballooned to +82.42%, a spectacular new high. The S&P 500 (SPY) is down -16.85% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +94.61%.

That brings my 14-year total return to +594.98%, some 2.60 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +45.76%, easily the highest in the industry.

I am going into the month-end surge with a fairly aggressive 40% long, (TLT), (TSLA), 40% short (XOM), (OXY), (TSLA), (SPY), with 20% crash for a totally market-neutral position. We’ve just had a heck of a run, and prices could well stall not far from here for the short term. The post-election rally happened, as predicted in this space.

Like Big Foot, the Yeti, and the Loch Ness Monster, the Fed pivot may soon actually make an appearance. I’m talking months, not years. That’s when our August central bank flips from the most severe tightening of interest rates in history, to a neutral, or one can only pray, an easing stance. This is what the 15% rally in stocks over the last six weeks has been all about.

And here is another old-time worn market nostrum. If investors sense that something is going to happen, they discount it fast, very fast.

Of course, there will be several false starts, denied rumors, and false flags, as there always are. After all, this is my 11th bear market. These will create sudden panic attacks, market selloffs, and Volatility Index (VIX) runs to $30 which are the license to print money for the Mad Hedge Fund Trader. Wait for the market to tell you when to trade. Ignoring it can prove expensive.

As we say here in the west, go off the reservation and you can get a lot of arrows stuck in your back.

How is this even remotely possible with the money supply only at $21.4 trillion, down 2% YOY? That’s a buzz cut from the +30% rate from a year ago.

The answer is that the money is out there, just hiding in different unrecognizable forms. Much of the $4 trillion in pandemic stimulus payments have yet to be spent. Inflation has added $2 trillion in new corporate profits through higher sales prices. Similarly, there is also another $1.5 trillion in pay increases bubbling through the system, also inspired by inflation.

You see this is booming credit card spending, much to the joy of Master Card (MA), Visa (V), and American Express (AXP) and their share price surges we have recently seen.

As I keep telling my Concierge customers on the phone, there is no playbook anymore. All the old ones have been rendered useless by the pandemic. To succeed and make windfall profits like me, you basically have to make it up as you go along.

The Fed Favors the Slowing of Rate Hikes, making a December increase of only 50 basis points a sure thing, according to minutes released on Wednesday for the prior meeting. Housing especially is taking a big hit. All interest rate plays, like bonds, rallied strongly.

Equities See Monster Inflows, some $23 billion in 35 weeks according to the Bank of America (BAC) flow of funds survey. There have been huge cash flows out of Europe looking for a stronger dollar, fleeing WWIII, and collapsing home currencies. The big chase is on. Time to go short? I am. It could be a big bull trap.

Leading Economic Indicators Dive, off 0.8% in October, double the decline expected and the weakest since the pandemic low in April 2020. There has only been one positive number in this data series in 2022. You have to go back to the financial crisis to find numbers this bad.

S&P Global Manufacturing PMI Takes a Hit in November, down to 47.6 from an estimate of 50. Services fell from 48 to 46.1. It’s another coincident recession indicator.

Existing Home Sales Plunge 5.9% in October to an annualized rate of 4.43 million units. It is the slowest sales pace in 11 years. It's not as bad as expected but is still down a horrific 28.4% YOY. Inventory fell to just 1.22 million units, only a 3.3-month supply, supporting prices in a major way. In fact, prices are still rising, up 6.6% annually to $379,100. Housing accounts for about 20% of the US economy, so here is your recession threat right here.

New Home Sales Come in Hot at 632,000, a real shocker with the 30-year fixed at 7.4%. Low-ball seller financing incentives must be a factor where they buy down rates to lower levels. Free upgrades, like those cherry wood cabinets, bonus rooms, and marble kitchen counters, also help. Prices are still up 15% YOY and inventories rose to a once unbelievable 8.9 months.

OPEC Plus Considering a 500,000 Barrels a Day Increase at their coming December meeting, which Saudi Arabia vehemently denied. The comments came out just as West Texas intermediate was barreling in on a new nine-month low. Saudi Arabia can talk all they want, but it’s tough to beat a coming recession, which every other hard asset class and commodity is now confirming.

Disney Axes Chairman, dumping Bob Chapek and bringing back Bob Iger from retirement. Losing $1.5 billion on the Disney Plus streaming service and losing its special tax status from the State of Florida has its costs. (DIS) is also not a stock to buy if we are going into recession. Avoid (DIS), despite the 10% move today. Let’s first see if Iger can cut costs.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 28 at 8:00 AM EST, the Dallas Fed Manufacturing Index for November is out.

On Tuesday, November 29 at 8:30 AM, the S&P Case Shiller National Home Price Index is released.

On Wednesday, November 30 at 8:30 AM, the ADP Private Employment Report for November is published. We also get a number on Q3 US GDP.

On Thursday, December 1 at 8:30 AM, the Weekly Jobless Claims are announced. US Personal Income and Spending for October is also out.

On Friday, December 2 at 8:30 AM, the Nonfarm Payroll Report for November is disclosed. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, by the 1980s, my mother was getting on in years. Fluent in Russian, she managed the CIA’s academic journal library from Silicon Valley, putting everything on microfilm.

That meant managing a team that translated over 1,000 monthly publications on topics as obscure as Artic plankton, deep space phenomenon, and advanced mathematics. She often called me to ascertain the value of some of her findings.

But her arthritis was getting to her, and all those trips to Washington DC were wearing her out. So I offered Mom a job. Write the Thomas family history, no matter how long it took. She worked on it for the rest of her life.

Dad’s side of the family was easy. He was traced to a small village called Monreale above the Sicilian port city of Palermo famed for its Byzantine church. Employing a local priest, she traced birth and death certificates going all the way back to an orphanage in 1820. It is likely he was a direct illegitimate descendant of Lord Nelson of Trafalgar.

Grandpa fled to the United States when his brother joined the Mafia in 1915. The most interesting thing she learned was that his first job in New York was working for Orville Wright at Wright Aero Engines (click here). That explains my family’s century-long fascination with aviation.

Grandpa became a tailer gunner on a biplane in WWI. My dad was a tail gunner on a B-17 flying out of Guadalcanal in WWII. As for me, you’ve all heard of plenty of my own flying stories, and there are many more to come.

My Mom’s side of the family was an entirely different story.

Her ancestors first arrived to found Boston, Massachusetts in 1630 during the second Pilgrim wave on a ship called the Pied Cow, steered by a Captain Ashley (click here).

I am a direct descendant of two of the Pilgrims executed for witchcraft in the Salem Witch Trials of 1692, Sarah Good and Sarah Osborne, where children’s dreams were accepted as evidence (click here). They were later acquitted.

When the Revolutionary War broke out in 1776, the original Captain John Thomas, who I am named after, served as George Washington’s quartermaster at Valley Forge responsible for supplying food to the Continental Army during the winter.

By the time Mom completed her research, she discovered 17 ancestors who fought in the War for Independence and she became the West Coast head of the Daughters of the American Revolution. It seems the government still owes us money from that event.

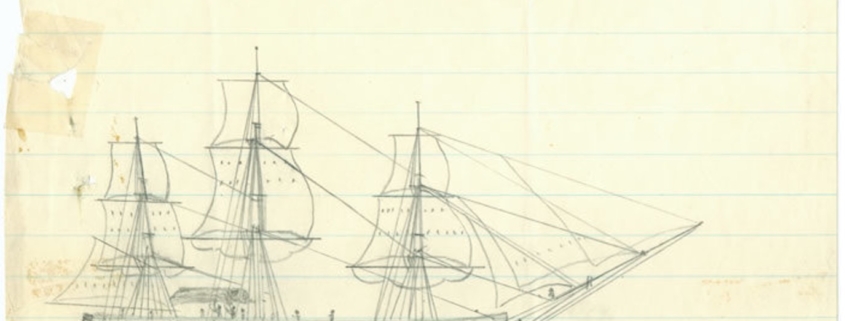

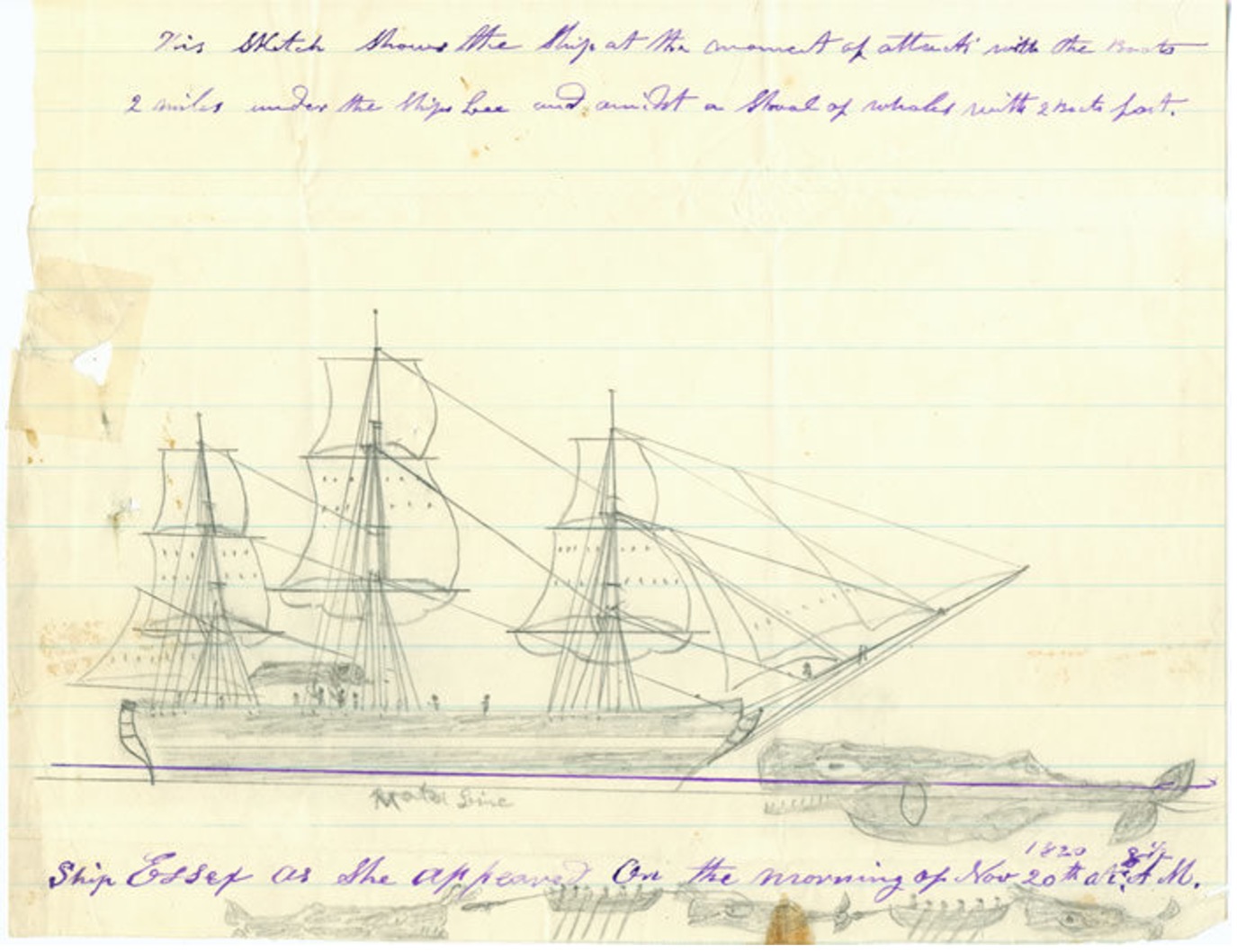

Fast forward to 1820 with the sailing of the whaling ship Essex from Nantucket, Massachusetts, the basis for Herman Melville’s 1851 novel Moby Dick. Our ancestor, a young sailor named Owen Coffin signed on for the two-year voyage, and his name “Coffin” appears in Moby Dick seven times.

In the South Pacific 2,000 miles west of South America, they harpooned a gigantic sperm whale. Enraged, the whale turned around and rammed the ship, sinking it. The men escaped to whaleboats. And here is where they made the fatal navigational errors that are taught in many survival courses today.

Captain Pollard could easily have just ridden the westward currents where they would have ended up in the Marquesas’ Islands in a few weeks. But these islands were known to be inhabited by cannibals, which the crew greatly feared. They also might have landed in the Pitcairn islands, where the mutineers from Captain Bligh’s HMS Bounty still lived. So the boats rowed east, exhausting the men.

At day 88, the men were starving and on the edge of death, so they drew lots to see who should live. Owen Coffin drew the black lot and was immediately shot and devoured. The next day, the men were rescued by the HMS Indian within sight of the coast of Chile, and returned to Nantucket by the USS Constellation.

Another Thomas ancestor, Lawson Thomas, was on the second whaleboat that was never seen again and presumed lost at sea. For more details about this incredible story, please click here.

When Captain Pollard died in 1870, the neighbors discovered a vast cache of stockpiled food in the attic. He had never recovered from his extended starvation.

Mom eventually traced the family to a French weaver 1,000 years ago. Our name is mentioned in England’s Domesday Book, a listing of all the land ownership in the country published in 1086 (click here). Mom died in 2018 at the age of 88, a very well-educated person.

There are many more stories to tell about my family’s storied past, and I will in future chapters. This week, being Thanksgiving, I thought it appropriate to mention our Pilgrim connection.

I have learned over the years that most Americans have history-making swashbuckling ancestors, but few bother to look.

I did.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Happy Thanksgiving from the Thomas Family

USS Essex

Mad Hedge Biotech and Healthcare Letter

November 8, 2022

Fiat Lux

Featured Trade:

(A GROWTH STOCK POISED TO BREAK RECORDS)

(LLY), (JNJ), (NVDA), (MA), (PG), (NVO), (ABBV)

The stock market has been down in the past couple of months, and the outlook still does not look all that good, considering that the issues with inflation and economic crises are showing no signs of ending anytime soon.

However, as Berkshire Hathaway Vice Chairman Charlie Munger noted, long-term investors should not be too anxious over “when” the markets will recover.

Instead, he advised “to think about ‘what’ will happen versus ‘when’” as a far more efficient way to behave in these challenging times.

Bearing that advice in mind, a particular biotechnology and healthcare stock stands out and is worth considering given its promising future: Eli Lilly (LLY).

Eli Lilly has grown at a fast pace and is considered among the most prominent pharmaceutical businesses in the world, ranking second behind Johnson & Johnson (JNJ).

At the moment, its market capitalization is at about $340 billion, making Eli Lilly more valuable than juggernaut Nvidia (NVDA) and other big names like Mastercard (MA) and Procter & Gamble (PG).

The most promising drug in Eli Lilly’s pipeline right now is Mounjaro, earlier known as tirzepatide, which recently received the green light from the Food and Drug Administration.

This once-a-week injection is an approved therapy that targets Type 2 diabetes. On top of that, Mounjaro can also be used as a potential weight loss drug.

While there are already existing diabetes drugs that double as weight loss treatments, mainly from Novo Nordisk (NVO), what makes Mounjaro distinct is the fact that it’s the first-ever unimolecular dual GIP/GLP-1 receptor agonist. In layman’s terms, this treatment could function in the same way as two completely different hormones that serve to control blood sugar levels.

Now, the question is: How significant an impact is Mounjaro on Eli Lilly?

Based on data from the National Institute of Diabetes and Digestive and Kidney Diseases, about 2 in every 5 adults are classified as obese, while 1 in 11 adults suffer from severe obesity.

That’s a substantial market. More than that, the consequences of obesity are said to have ripple effects throughout the entire healthcare industry.

In fact, the Centers for Disease Control and Prevention estimate the yearly medical costs in the United States due to obesity to be roughly $173 billion in 2019.

Following its approval, Mounjaro raked in $16 million in sales. Given its unique mechanism and the massive market it can target, Mounjaro is estimated to rake in $25 billion in peak revenue annually.

Moreover, this treatment could not only be a game changer for the company but also the entire healthcare community.

For context, Eli Lilly’s total revenue in 2021 from all its products combined was $28 billion. Needless to say, Mounjaro would put the company on track for some serious growth.

Looking at this weight loss and diabetes drug's trajectory and potential, Mounjaro can benefit Eli Lilly in the same way AbbVie (ABBV) maximized Humira. For years, Humira was hailed as the top-selling drug in the world.

While it’s set to lose its patent protection by 2023, there’s no doubt that this anti-inflammatory drug boosted the share price and bottom line of AbbVie.

Clearly, this is a business poised to become even more valuable soon. This means its current share price could be considered a bargain in the next few years.

How long it would take for Eli Lilly to make money off its pipeline remains a question mark. However, concentrating on “what” is most likely about to happen instead of “when” makes it easy to make a case for Eli Lilly being an excellent growth investment.

Global Market Comments

October 31, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WAS THAT THE POST-ELECTION RALLY?)

(SPY), (TLT), (VIX), (V), (MA), (AXP)

I have been through 11 bear markets in my lifetime, and I can tell you that the most ferocious rallies always take place in bear markets. This one is no exception. Short sellers always have a limited ability to take pain.

This rally took the Dow Average up 14.4% during the month of October, the biggest such monthly gain since 1976 (hmmm, just out of college and working for The Economist magazine in Tokyo, and dodging bullets in Cambodia).

The Dow outperformed NASDAQ by 9% in October, the most in 20 years. That is a pretty rare event. During the pandemic, the was a tremendous “pull forward” of technology stocks, as only commerce was possible. Now it is time for their earnings to catch up with pandemic valuations, which may take another year.

But first, let me tell you about my performance.

With some of the greatest market volatility in market history, my October month-to-date performance ballooned to +4.87%.

That leaves me with only one short in the (SPY) and 90% cash.

My 2022 year-to-date performance ballooned to +74.55%, a new high. The Dow Average is down -9.47% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +77.95%.

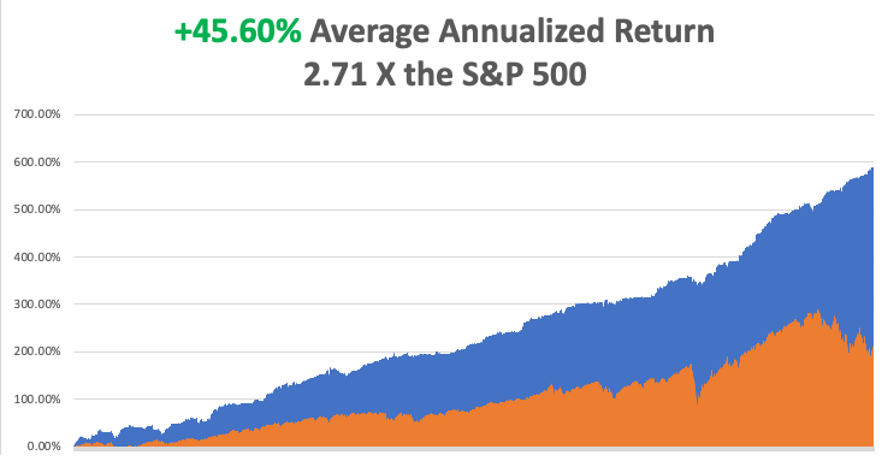

That brings my 14-year total return to +587.88%, some 2.86 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +45.60%, easily the highest in the industry.

And of course, there is no better indicator of the market strength than the Mad Hedge Market Timing Index, which broke above 50 for the first time in six months, all the way to 61.

It's no surprise that investors sold what was expensive (tech) and what was bought that was cheap (banks). It’s basic investing 101. Tech is still trading at a big premium to the market and double the price earnings of banks

The prospect of an end to Fed tightening has ignited a weaker dollar, prompting a stronger stock market that generated the rocket fuel for this month’s move.

All the negatives have gone, the seasonals, earnings reports, a strong dollar, and in 8 days, the election. Don’t forget that the (SPX) has delivered an eye-popping 16.3% return for every midterm election since 1961, all 15 of them.

The put/call spread is the biggest in history, about 1:4, showing that investors are piling in, or at least covering shorts, as fast as they can. Individual stock call options are trading at the biggest premiums ever.

Suffice it to say that I expected all of this, told you about it daily, and we are both mightily prospering as a result.

Much of the selling this year hasn’t been of individual stocks but of S&P 500 Index plays to hedge existing institutional portfolios. The exception is with tax loss selling to harvest losses to offset other gains. That means indiscriminate index selling begets throwing babies out with the bathwater on an industrial scale. And here is your advantage as an individual investor.

A classic example is Visa (V) which I’m’ liking more than ever right now, which I aggressively bought on the last two market downturns. The company has ample cash flow, carries no net debt, and with high inflation, is a guaranteed double-digit sales and earnings compounder.

It clears a staggering $10 trillion worth of transactions a year. With $29.3 billion in revenues in 2022 and $16 billion in net income, it has a technology-like 55% profit margin. Visa is also an aggressive buyer of its own shares, about 3% a year. That’s because it trades at a discount to other credit card processors, like Master Car (MA) and American Express (AXP).

The only negative for Visa is that it gets 55% of its earnings from aboard, which have been shrunken by the strong dollar. That is about to reverse.

It turns out that digital finance never made a dent in Visa’s prospects, as the dreadful performance of PayPal (PYPL) and Square (SQ) shares amply demonstrate.

Remember, however, that the Fed is raising interest rates by 0.75% to a 3.75%-4.00% range on Wednesday, November 2, and may do so again in December. It has been the fastest rate rise of my long and illustrious career, and also the best telegraphed.

That may give us one more dip in the stock market that will enable us to buy in on the coming Roaring Twenties.

We’ll see.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, October 31 at 6.45 AM, the Chicago PMI for October is released.

On Tuesday, November 1 at 7:00 AM, the JOLTS job opening report for September is out.

On Wednesday, November 2 at 8:30 AM, ADP Private Employment Report for October is published. The Fed raises interest rates at 11:00 AM and follows with a press conference at 11:30.

On Thursday, November 3 at 8:30 AM, Weekly Jobless Claims are announced.

On Friday, November 4 at 8:30 AM the Nonfarm Payroll Report for October is printed. At 2:00, the Baker Hughes Oil Rig Count is out.

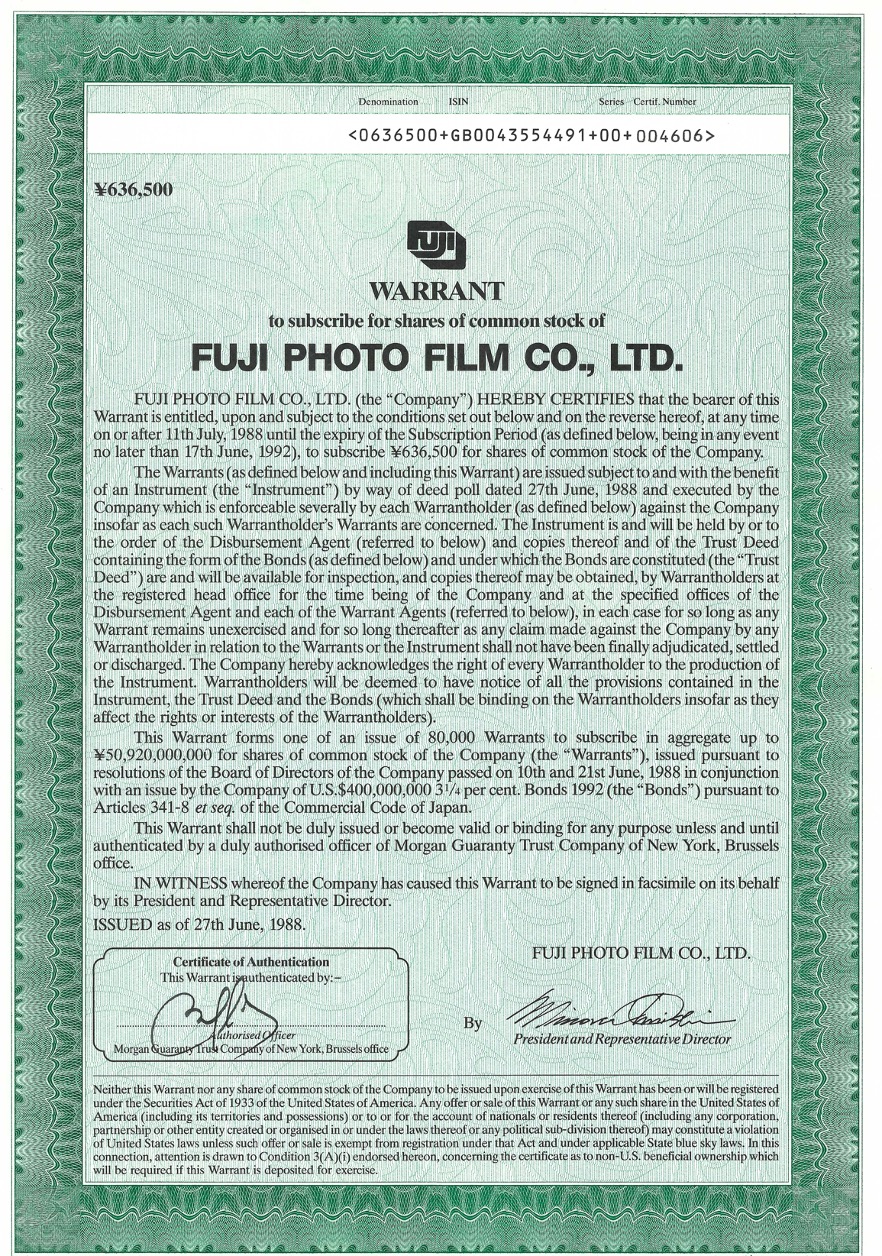

As for me, during the late 1980s, the demand for Japanese bonds with attached equity warrants was absolutely exploding.

Japan was Number One, the engine of technological innovation. Everyone in the world owned a Sony Walkman. They were trouncing the United States with 45% of its car market.

The most conservative estimate for the Nikkei Average for the end of 1990 was 50,000, or up 27%. The high end was at 100,000. Why not? After all, the Nikkei had just risen tenfold in ten years and the Japanese yen had tripled in value.

In 1989, my last full year at Morgan Stanley, the Japanese warrant trading desk accounted for 80% of the firm’s total equity division profits.

The deals were coming hot and heavy. Since Morgan Stanley had the largest Japanese warrant trading operation in London, a creation of my own, we were invited to join so many deals that the firm ran out of staff to attend the signings.

Since I was the head of trading, I thought it odd that the head of investment banking wanted to speak to me. It turned out that Morgan Stanley was co-managing two monster $3 billion bond deals on the same day. Could I handle the second one? Our commission for the underwritings was $10 million for each deal!

I thought, why not, better to see how the other half lived. So, I said “yes.”

The attorneys showed up minutes later. I was given a power of attorney to sign on behalf of the entire firm and commit our capital to the underwriting $3 billion five-year bond issue for the Industrial Bank of Japan. The deal was especially attractive as the bonds carried attached put options on the Nikkei which institutional investors could buy to hedge their Japanese stock portfolios.

Since the Industrial Bank of Japan thought the stock market would never see a substantial fall, they happily sold short the put options. Only the Industrial Bank of Japan could have pulled this off as it was one of the largest and highest-rated banks in Japan. I knew the CEO well.

It turned out that there was a lot more to a deal signing than I thought, as it was done in the traditional British style. We met at the lead manager’s office in the City of London in an elegant wood-paneled private dining room filled with classic 18th century furniture.

First, there was a strong gin and tonic which you could have lit with a match. A five-course meal accompanied with a 1977 deep Pouilly Fuse white and a 1952 Bordeaux red with authority. I had my choice of elegant desserts. Sherry and a 50-year-old port followed, along with Cuban cigars, which was a problem since I had just quit smoking (my wife recently bore twins).

The British were used to these practices. Any American banker would have been left staggering, as drinking during business hours back then was illegal in New York.

Then out came the paperwork. I signed with my usual flourish and the rest of the managers followed. The Industrial Bank of Japan provided the Dom Perignon as they were about to receive $3 billion in cash the following week.

Then an unpleasant thought arose in the back of my mind. Morgan Stanley assumed the complete liability for their share of the deal. But did I just incur a massive personal liability as well?

Then I thought, naw, why pee on someone’s parade. Morgan Stanley’s been doing this for 50 years. Certainly, they knew what they were doing.

Besides, the Japanese stock market is going up forever, right? No harm, no foul. In any case, I left Morgan Stanley to start my own hedge fund a few months later.

Some seven months later, one of the greatest stock market crashes of all time began. The Nikkei fell 50% in six months and 85% in 20 years. Some 32 years later the Nikkei still hasn’t recovered its old high.

For a few years, that little voice in the back of my mind recurred. The bonds issued by the Industrial Bank of Japan fell by half in months on rocketing credit concerns. The IBJ’s naked short position in the Nikkei puts completely blew up, costing the bank $10 billion. The Bank almost went bankrupt. It was one of the worst timed deals in the history of finance. The investors were burned bigtime.

Did I ever hear about the deal I signed on again? Did process servers show up and my front door in London with a giant lawsuit? Did Scotland Yard chase me down with an arrest warrant?

Nope, nothing, nada, bupkis. I never heard a peep from anyone. It turns out you CAN lose $12 billion worth of other people’s money and face absolutely no consequences whatsoever.

Welcome to Wall Street.

Still, when the five-year maturity of the bonds passed, I breathed a sigh of relief.

My hedge fund got involved in buying Japanese equity warrants, selling short the underlying stock, thus creating massive short positions with a risk-free 40% guaranteed return. My investors loved the 1,000% profit I eventually brought in doing this.

Unlike most managers, I insisted on physical delivery of the warrant certificates, as the creditworthiness of anyone still left in the business was highly suspect. Others who took delivery used warrants to wallpaper their bathrooms (really).

They all expired worthless, I made fortunes on the short positions, and still have them by the thousands (see below).

In September 2000, the Industrial Bank of Japan, its shares down 90%, merged with the Dai-Ichi Kangyō Bank and Fuji Bank to form the Mizuho Financial Group. It was a last-ditch effort to save the Japanese financial system after ten years of recession engineered by the government.

Morgan Stanley shut down their worldwide Japanese equity warrant trading desk, losing about $20 million and laying off 200. Some staff were outright abandoned as far away as Hong Kong. Morgan Stanley was not a good firm for running large losses, as I expected.

I learned a valuable trading lesson. The greater the certainty that people have that an investment will succeed, the more likely its failure. Think of it as Chaos Theory with a turbocharger.

But we sure had a good time while the Japanese equity warrant boom lasted.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

January 7, 2022

Fiat Lux

Featured Trade:

(THE DEATH OF VISA AND MASTERCARD)

(MA), (V), (SQ), (PYPL), (AFTPY), (AFRM), (AMZN)

Visa and Mastercard’s card networks are a relic of the past, not in terms of reach or footprint, but the technology of it.

This will cost their stock price and we are already seeing it play out in the market.

The canary in the coal mine was fintech players Square (SQ) and PayPal (PYPL) whose share prices were pummeled at the back end of last year.

PYPL is down 40% from its 2021 peak and SQ experienced a similar 42% drop.

This fierce competition and the crowded marketplace have investors paying less of a premium than ever before.

In a tightening rate environment, it’s clear the wolves are out for more flesh and the contagion will spread to those further up the food chain.

Fintech business models aren’t as robust or foundational as the bulwarks of MA and V, but questions must be asked if small businesses aren’t willing to pay an extra 2% on sales for outdated technology.

The fintech space has moved a long way in a short amount of time causing investors to be concerned about secular growth sustainability.

Among them are concerns that consumers are shifting to debit, away from higher-margin credit cards.

Consumers are also using more alternative payment methods that may bypass the card networks, including “buy now pay later” services offered by companies like Klarna, Afterpay (AFTPY), and Affirm (AFRM).

Visa has also come under pressure from a recent announcement by Amazon.com (AMZN) that next year it will stop accepting Visa-branded credit cards issued in the United Kingdom and this could be the beginning of a narrowing of Visas’ moat that could trigger a domino effect in other rich western countries.

The bulls would say that the stocks could undergo a reversal if the Omicron variant is not as bad as initially thought creating a tsunami of consumer spending massaging the bottom line for Visa and Mastercard.

But it’s looking more like V and MA are the victims of tightening travel restrictions around the globe and elevated positive cases that are immobilizing consumers.

The big card networks rely heavily on revenues related to cross-border travel as consumers and businesses use their cards for airfare, Airbnb’s, and Ubers, as well as duty-free gifts in foreign countries.

Multiples may need to come down if the Omicron variant puts the shackles on travel as countries reimpose bans or quarantine rules.

Investors had been counting on a recovery in cross-border travel to boost revenues for the card networks. This is definitely a kick in the nuts after initially seeing momentum as countries in general trended to loosening restrictions.

International transactions brought in $1.9 billion, or 21%, of Visa’s $8.9 billion in revenues for the 2021 fourth quarter.

The segment is highly profitable due to steep transaction and foreign-exchange fees. Cross-border margins come in around 69%, contributing significantly to Visa’s overall earnings per share.

The Christmas season has been confronted by a bevy of new restrictions as many places consider other measures to curb the spread of the Omicron variant.

Ultimately, even if MA and V can get positive reinforcement from increased short-term travel which seems unlikely, alternative business models are breathing down their neck as the technology of money has advanced.

The “buy now, pay later” phenomenon, although risky, is a rapid gut punch to the incumbents.

Then consider there is speculative technology like Bitcoin out there that bypasses these dinosaur networks altogether.

I believe 2022 is the year that MA and V get exposed as a luxury in a frugal world where small businesses can’t afford to give away 2% of revenue.

There’s too much money being invested into the technology of money for small businesses to reach for MA and V’s network.

Even open banking and digital networks can really dent the traditional payment networks.

Basically, I believe these companies have hit the high-water mark, and the likes of Zelle and Venmo will start to put pressure on these high fees.

Places like China don’t even use them by bypassing them through digital wallets like Wechat pay and Alipay.

Pie shrinkage and revenue decelerate — I believe this is one of the seminal trends we will see in fintech in 2022.

Global Market Comments

December 3, 2021

Fiat Lux

Featured Trade:

(DECEMBER 1 BIWEEKLY STRATEGY WEBINAR Q&A),

(PYPL), (MA), (AXP), (SQ), (TLT), (TBT), (TSLA), (AAPL), (FB), (MSFT), (AA), (FCX), (BITO), (COPA.L)