Mad Hedge Bitcoin Letter

April 21, 2022

Fiat Lux

Featured Trade:

(SHOPIFY BOOSTS DIGITAL GOLD)

(BTC), (SHOP), (MCD), (WMT)

Mad Hedge Bitcoin Letter

April 21, 2022

Fiat Lux

Featured Trade:

(SHOPIFY BOOSTS DIGITAL GOLD)

(BTC), (SHOP), (MCD), (WMT)

People aren’t going to wake up the next day and find that Bitcoin (BTC) is suddenly the de-facto global payment system.

There are steps that need to be taken for it to get to that point.

How I see it – the path to further adoption will go through the e-commerce systems in digitized form.

This makes sense on a lot of fronts.

It’s no secret that e-commerce is usurping the status quo of brick-and-mortar shops.

That process was accelerated by the health phenomenon over the past two years.

If Bitcoin get can the likes of Amazon to allow Bitcoin payment, then that would be considered a massive victory.

That needs to happen before government services or utility payments allow Bitcoin payments.

It also needs to happen before big government install regulations too onerous that it won’t come to fruition.

The short-term positive news is that payment network Strike has announced integrations with Shopify (SHOP), an alternative payment processor Blackhawk Network, which will make it easier for global merchants to accept Bitcoin payments.

Bitcoin Lightning Network, a second layer built on top of the Bitcoin blockchain, will convert BTC payments into dollars quickly, relieving merchants of complexities associated with actually holding Bitcoin.

I must admit, Shopify is no Amazon, but baby steps need to happen somewhere and Shopify is a reputable e-commerce company as it stands.

Yet Shopify’s $4.5 billion of annual sales is dwarfed by Amazon’s $450 billion in annual sales and that matters.

Scale is everything in tech and hitting singles doesn’t make quite the dent or simply will take too long for the results to become meaningful.

Shopify will be able to take advantage of previously untapped global markets and purchasing power, as well as save money with low-cost payment processing through accepting Bitcoin payments.

Merchants will be able to interact with the Bitcoin network, and users will be able to make purchases privately throughout the United States, taking advantage of the cheap, instant, and open access that Bitcoin offers.

More than 400,000 storefronts will now accept Bitcoin through the Lightning Network, and any merchant is welcome to join through SHOP.

What was once hard to imagine is now becoming a reality. The future looks like it will bring millions of storefronts across the US accepting Bitcoin in the near future. Other countries may follow suit after seeing the success of this nation-state Bitcoin usage.

Sadly, financial institutions have been woefully inadequate to meet the needs of an increasingly digital consumer, and it’s now evident they are generations behind.

If we really think about it, there has been no innovation in the payment systems since 1949.

The launch of the Bitcoin payment system has revolutionized and disrupted well-established traditional credit card networks like Visa and MasterCard, bringing a new financial world order.

Several examples show how crypto adoption boosted a nation's economy, including Argentina, which adopted Strike’s Lightning payments system and saw its GDP rise 10.3% in 2021, the highest rise since 2004. Another example is El Salvador, which adopted Bitcoin as legal tender with the help of Strike and saw its GDP grow by double digits for the first time recently.

I am eagerly awaiting McDonald’s (MCD) and Walmart’s (WMT) announcement that they will start accepting Bitcoin.

That will really move the needle.

If some of these big players come on board, Bitcoin will also benefit from reduced volatility as well inspire the incremental investor to hold Bitcoin as a store of value.

Yet the wait goes on as Bitcoin is slowly accepted around the world and the more sovereign nations and large corporations that come into the fold, there is no doubt in my mind that this will be a main driving force behind higher Bitcoin prices.

Global Market Comments

October 23, 2020

Fiat Lux

Featured Trade:

(11 SURPRISES THAT WOULD DESTROY THIS MARKET),

(SPY), (USO), (AMZN), (MCD), (WMT), (TGT)

Note to readers: Sorry for the short letter today but PG&E is about to turn off my electric power to reduce the risk of a wildfire during these high, hot winds from the east so I’m sending you just a few quick thoughts.

The Teflon market is back.

Bad news is good news. Good news is good news.

What could be better than that?

However, there are a few issues out there lurking on the horizon that could pee on everyone’s parade.

Risks of an asymmetric outcome right now are huge. Let me call out the roster for you.

1) The China Trade War Escalates – Every day economic advisor Larry Kudlow tells us that the trade talks are progressing nicely, and every day the administration pulls the rug out from under him with new sanctions. The last chance to avoid the next recession is upon us. A trade deal is the rational thing to do. Oops! There's that “rational” word again.

2) Economic Data Gets Worse - After a great data run into the fall, they are suddenly rolling over. All of the forward-looking data is now 100% terrible.

3) The Fed Raises Interest Rates- This has been the world’s greatest guessing game for the past three years. Jay Powell has just promised NOT to raise interest rates for three years, so an increase would be completely out of the blue and have an outsize impact. The Fed lives in perpetual fear of the American economy going into the next recession with interest rates near zero! That would leave them powerless to do anything to engineer a revival.

3) Another Geopolitical Crisis - You could always get a surprise on the international front. But the lesson of this bull market is that traders and investors could care less about North Korea, ISIS, Al Qaida, Afghanistan, Iraq, Syria, Russia, the Ukraine, or the Chinese expansion in the South China Sea.

Every one of these black swans has been a buying opportunity of the first order, and they will continue to be so. At the end of the day, terrorists don’t impact American corporate earnings, nor do they own stocks.

4) A Recovery in Oil – The next drone attack against Saudi Arabia could send oil really flying. If it recovers too fast and rockets back to the $100 level, it could start to eat into stock prices, especially big energy-consuming ones, like transportation and industrials.

5) The End of US QE - The Fed’s $4.5 billion quantitative easing, relaunched in March, could end as soon as it gets the sense that the economy is recovering too fast. That would take the punch bowl away from the party. Anyone who said QE didn’t work obviously doesn’t own stocks.

6) A New War – If the US gets dragged into a major new ground war, in Iran, North Korea, Syria, Iraq, or elsewhere, you can kiss this bull market goodbye. Budget deficits would explode, the dollar would collapse, and there would be a massive exodus out of all risk assets, especially stocks.

7) US Corporate Earnings Collapse – They already have for the sectors of the economy where you can’t socially distance, like movie theaters, restaurants, and airlines. A much higher third wave of Covid-19 would do the trick nicely, bringing a new round of lockdowns. Do you think stocks (SPY) will notice?

8) Another Emerging Market (EEM) Crash - If the greenback resumes its long-term rise, another emerging market debt crisis is in the cards. Venezuela and Argentina are just the opening scenes.

When their local currencies collapse, it has the effect of doubling the principal balance of their loans and doubling the monthly payments, immediately.

This is the problem that is currently taking apart the Brazilian economy right now. It happened in 1998, and it looks like we are seeing a replay.

9) A Trump Victory – Since the stock market has spent the last six months discounting a Biden win, the opposite result would be a total out of the blue shock. Count on a 10% dive in the (SPY) immediately, and 20% eventually. Polls can be wrong. Who knew?

10) Inflation Returns – Steep tariff increases on everything Chinese is rapidly feeding into rising US consumer prices. What do you think the Amazon (AMZN) wage hike to $15 means? If McDonald’s (MCD), Walmart (WMT), and Target (TGT) join them, we’re there. This is a stock market preeminently NOT prepared for a return of inflation.

I know you already have trouble sleeping at night. The above should make your insomnia problem much worse.

Try a 10-mile hike with a heavy pack every night in the mountains. It works for me.

Down the Ambien, and full speed ahead!

Mad Hedge Technology Letter

March 28, 2019

Fiat Lux

Featured Trade:

(MACDONALD’S GOES HIGH TECH)

(MCD)

If McDonald's is using more technology, then maybe your company should be using more too.

In its most dynamic deal since divesting from Chipotle (CMG) in 2006, McDonald’s acquired artificial intelligence software company Dynamic Yield.

The company is an Israeli startup specializing in software that customizes content to the user.

The result of this ramp up in technology means that your McDonald's experience is about to improve, become easier and faster.

This is not your father’s McDonald’s.

At handpicked locations in America last year, McDonald's tested the artificial intelligence software which provides functions such as cross-selling different items on a sidebar and taking into consideration the current weather and time of day.

For example, on hot summer days the machine learning software will most likely recommend colder items such as desserts and soft drinks, and on colder days lean towards a hotter, more filling option.

Another likely consequence is after choosing a full meal of some sort, the software will further prompt the customer of the choice of popular à la carte items via the sidebar.

The theme of digital transformation is upon us and following the lead of other fast food companies such as Domino's Pizza (DPZ) will make operations more efficient and appeal to different segments of society.

The decision to gentrify and digitize the customer experience could be a result from a stagnating fast food industry that is in a price war down to the bottom.

Did you know you that you can buy 10 chicken nuggets for $1 at Burger King now?

Or even a simple cocktail at Applebee's for just $1?

QSRs (quick service restaurants) have lagged posher establishments caused by the cutting down of immigration and the struggling of the low-income class that is squeezing out fast food restaurants’ go-to clientele base.

And as construction rates have crashed because of the surging material costs induced by tariffs and a lack of foreign workers, McDonald's has been forced to look to replace demand.

Construction workers are a healthy portion of McDonald’s domestic lunch demand.

Not only is foot traffic being affected, but the fast food industry in America is saturated and funnily enough, when I travel to Europe every summer, this is one of the first comments I get from the Europeans.

The drive-thru menu will be one of the primary beneficiaries of this new software, and the projected enhancement of customer satisfaction should drive higher retention rates.

McDonald's plans to roll out kiosks that self-serve customers which is one stop on the way to a fully automated experience.

In the next 5 or 10 years, there might be only one or two McDonald's employees running a franchise.

McDonald's is clearly trending towards reducing employee headcount evident in their strategy of deciding to halt lobbying efforts to bring down the minimum wage.

Genna Gent, McDonald’s Vice President of U.S. government relations, went on record sharing that “outlets owned by the company have an average starting wage that exceeds $10 per hour.”

Most fast-food companies would be frightened to discover the House Committee on Education and Labor advanced a bill earlier this month to increase the minimum wage from $7.25 to $15 per hour by 2024 thus incentivizing McDonald’s to pick up the pace of their digital transformation.

McDonald's is not only one of the biggest employers in America, but they are one of the largest in the world.

The company had 210,000 employees in 2018 and I believe they will be able to quickly get down to 150,000 with the new software streamlining employees’ tasks allowing franchises to reduce headcount.

Getting on top of the mobile app and optimizing delivery is another step to McDonald’s digital growth strategy.

The adoption of machine learning will at some point allow customers to reorder their favorite meals on demand or before they enter the establishment, and even possibly personalizing parts of a meal that can mix and match to create alternative meals.

And the beauty of all of this, the same software rolled out to the self-serving kiosks, drive-thru platform, and mobile app can be universally adopted and managed from the cloud causing massive savings from tech efficiencies.

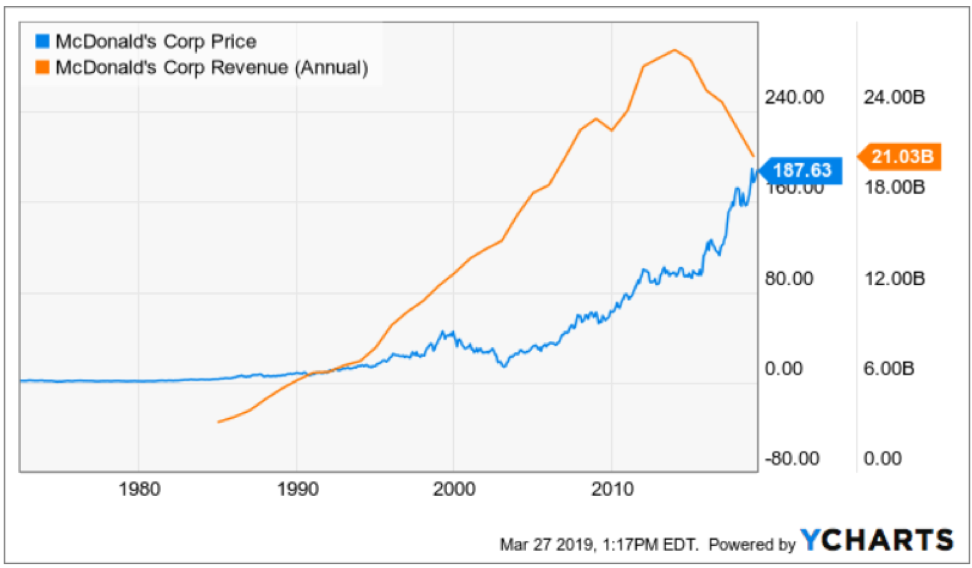

McDonald’s is not without its share of difficulties, sales have been plunging since 2014 and part of the response to this was to start the digital transformation.

This is just the second step of a long drawn own process that will automate the production process and customer experience.

On the flip side, the 3-year EPS growth rate is 16% demonstrating that even with falling sales, the efficiencies are falling down to the bottom line with the company profiting over $5 billion in 2018.

Ironically enough, McDonald’s profits were substantially lower with higher sales, indicating to management that a leaner version of itself has been justified.

I believe McDonald’s will continue to gentrify its menu, digitize its customer experience and production process, and sale deceleration will slow down while profit acceleration and EPS will increase.

This is a good omen for the stock’s trajectory and the company continues to be a good buy on the dip candidate because its upward share movement is entirely correlated to the increasing profitability which it continues to deliver on.

As we inch closer to a recession, deterioration of economic conditions could push an unintended growing number of customers through McDonald’s arched doors as they usually attract customers who earn less than $45,000 per year, looking to save some extra cash.

This could set the stage for a reawakening of increased sales.

Global Market Comments

October 3, 2018

Fiat Lux

Featured Trade:

(TAKING A LOOK AT GENERAL ELECTRIC LEAPS), (GE),

(TEN SURPRISES THAT WOULD DESTROY THIS MARKET),

(USO), (AMZN), (MCD), (WMT), (TGT)

Anyone wondering about the long term future of the US economy is amazed at how fast it is evolving.

There has been an unrelenting growth of services' share of American GDP, from 25% to 45% over the last sixty years.

Far and away the fastest growth area for the past eight years has been health care, thanks to Obamacare. With that program now headed for the dustbin of history, those job gains are about to be quickly unwound.

It takes one health care professional to take care of 14 Americans. If you eliminate health care for 20 million, that eliminates 1.42 million jobs.

That's what will happen if our national health care is eliminated without a replacement.

This is not necessarily a bad thing. Would you rather be mining coal or designing a website? Do you want to earn $12 an hour, or $150?

These statistics make us the envy of the world, as services are where the future lies. By creating so many key technologies, our country has been the most successful in the world in climbing up the value chain.

China can have all the $3 an hour jobs it wants.

Services largely comprise pure intellectual content, require no raw materials, and the end product can be transmitted over the Internet.

There is a reason why nearly a million foreign students have flocked to the US for an education.

Emerging nations like China and South Korea, which only see services generating 10%-15% of their GDP, are wracking their brains trying to figure out how to play catch up.

McDonald?s (MCD) has always figured large in my life.

I grew up next door to one of the first five stands built in the country, in the Los Angeles metropolitan area. That?s when visionary milkshake mixer salesman, Ray Kroc, started to franchise his revolutionary new ideas for delivering fast food.

One of my fondest childhood memories was when my mother used to take us out to dinner there. At 15 cents a burger you fed seven growing kids for a buck and still had money left over for French fries. We brought our own cokes in an ice chest to save money.

I always gummed up the works by asking for a hamburger that had mustard only and no pickles. I clearly did not fit into the company?s stripped down Speedee Service business model.

In high school, I managed to land a coveted minimum wage job ($1 an hour) under the Golden Arches. I learned first hand the harsh realities of working for a living, and that you didn?t necessarily want to know how the sausage was made.

Then, the Big Mac came out, the blockbuster beef equivalent of a Saturn V rocket. Chicken McNuggets, Egg McMuffins, and Filet of Fish followed (for the Catholics on Fridays), and it seemed the company could do no wrong.

In a few decades, the company grew into the world?s largest restaurant, expanding its list of franchises to a staggering 36,000 shops in 119 countries.

It became the planet?s largest consumer of beef and potatoes in the world. Its presence is ubiquitous on US military bases around the world. Its chocolate shake is said to be able to withstand a nuclear attack.

However, since 2011, the stock has largely failed to perform, and has greatly underperformed the S&P 500. Its business model is aging. Its menu needs a major reworking.

The company has suffered sales declines at existing locations in five out of the last six quarters, with the rate of decline accelerating this year.

The problem is that people just don?t want to buy what they make anymore.

I went into a store the other day, and I was appalled. It was almost empty.

The few customers it had all seemed sick, obese, or unemployed, wearing polyester clothes. They periodically ducked outside for a quick cigarette.

They needed a double bacon cheeseburger like a hole in the head. Health was not their priority. They were a market that was literally dying.

It is becoming increasingly clear that the American market is moving beyond McDonald?s. Can the long vaunted company now play catch up?

This is the big problem. Millennials, those aged 18-34, which should be the company?s highest growth market, aren?t showing much interest in the company?s secret sauce.

They are, in fact, adopting a complete different life style that doesn?t have Ronald McDonald anywhere in it. They are very cautious in what they put in their young bodies.

Think organic, locally grown, low fat, low calorie, non-GMO, high fiber, and no artificial hormones or coloring anywhere. Think of health food, and you don?t exactly run off to a McDonald?s to eat. McDonald?s has a serious brand problem.

Organic foods are booming, seeing sales growth of 30% a year nationally, with far higher profit margins.

If you don?t believe me, look no further than the stock chart of Whole Foods (WFM) below, which at one point, saw its shares gain 116% relative to (MCD).

This is also a generation that is vastly more environmentally conscious that the Gen Xer?s and baby boomers before them. Beef is the single most environmentally destructive food product you can buy, with all the waste and methane byproducts.

One quarter pound beef patty requires a profligate 450 gallons of water to produce. That?s double the daily ration for a family of four here in drought suffering California. And who knows what the hell they are putting in it to preserve it down a very long global supply chain.

McDonald?s did make some limited progress on this front by announcing that they would no longer put ?pink slime? into their beef patties. If you don?t know what ?pink slime? is, then you don?t want to know. Suffice it to say that it is definitely not a great new marketing angle for health food nuts.

The company is also encountering ferocious competition for the fast food dollar from the new, rapidly growing ?fast casual? industry. These include Five Guys, Shake Shack (SHAK), Chipotle Mexican Grill (CMG), and Panera Bread (PNRA).

These companies are all snapping up the high margin end of the market, even though any one of them is miniscule in size when compared to McDonald?s. Collectively, they are nipping at Ronald McDonald?s heels.

I can?t even get my own kids to eat at McDonald?s anymore, they preferring the legendary In and Out Burger on the West Coast (no double entendre intended), which emulates the McDonald?s stripped down menu of the early 1950?s.

(In and Out is a fascinating business story for another day, as the $2 billion, 300 stand LA based company is now controlled by a 33 year old four time married heiress named Lynsi Snyder.)

McDonald?s is one of the world?s largest and best managed companies. In 2014 it generated an impressive $4.8 billion profit on $27.4 billion in sales, producing a not too shabby net margin of 17.5%. So we?re not, by any means, talking chapter 11 material here.

But it is going ex growth, and that invites a lower stock multiple, and a lower stock price, something you, as equity investors should be aware of. Is (MCD)?s position in the Dow Average 30 at risk?

Yikes! That would be a disaster for shareholders!

The company has seen the writing on the wall. It recently brought in a new CEO, Steve Easterbrook, to shake things up. But so far, all of the changes he has implemented have been administrative in nature. There is no category killing super burger anywhere on the horizon.

McDonald?s does still have some huge advantages. Its efficiencies, purchasing power, and economies of scale are epic. But the business is so enormous that any incremental change is unlikely to move the needle on the earnings front.

It is the classic dilemma when navigating a supertanker.

Another headache arises from the snowballing minimum wage, or living wage movement, which has McDonald?s squarely in its crosshairs. This promises to be a big political campaign issue in 2016.

Several cities, like San Francisco and Seattle, have already boosted pay from $8 to $15 and hour, which would substantially increase (MCD)?s operating costs and cut its price advantage.

It is possible that McDonald?s could go the route of so many other legacy industries that were born here, and then migrated abroad when the home market disappeared. I?m thinking about cigarettes (Altria Group (MO), Kentucky Friend Chicken (YUM), and coal (PEA).

Indeed, on my last trip to China, I ate regularly at McDonald?s, and couldn?t help but notice that it had become the country?s hot high end date. But the burden of proof lies on the current management as to whether they can pull this off.

So, you won?t find me buying (MCD) shares anytime soon. If you must own it for that generous 3.6% dividend, at the very least you should be writing covered calls against your position to take in premium income to offset the lack of capital appreciation.

In the meantime, I?ll be grabbing a double cheeseburger and chocolate shake at In and Out Burger, even though the lines there can be miserable.

Watch Out, McDonald?s!

Watch Out, McDonald?s!

My former employer, The Economist, once the ever tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its ?Big Mac? index of international currency valuations.

Although initially launched as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success. The index counts the cost of McDonald?s (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the Hong Kong dollar, the Chinese Yuan (CYB), and the Thai Baht are cheap. I couldn?t agree more with many of these conclusions. It?s as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas. I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool, than a speedy lunch.

The Big Mac in Yen is Definitely Not a Buy

The Big Mac in Yen is Definitely Not a Buy