Mad Hedge Technology Letter

July 13, 2022

Fiat Lux

Featured Trade:

(HOT INFLATION NUMBER BODES POORLY FOR TECH STOCKS)

(LYFT), (UBER), (AMZN), (SHOP), (GOOGL), (SNAP), (META), (TWTR), (MELI), (EXPE), (TRIP)

Mad Hedge Technology Letter

July 13, 2022

Fiat Lux

Featured Trade:

(HOT INFLATION NUMBER BODES POORLY FOR TECH STOCKS)

(LYFT), (UBER), (AMZN), (SHOP), (GOOGL), (SNAP), (META), (TWTR), (MELI), (EXPE), (TRIP)

Fed swaps now fully price in 150 basis points of hikes over the next two meetings after awful inflation numbers came in showing inflation heading in the wrong direction.

The 9.1% inflation print was an acceleration of the 8.6% which was what we got last time.

I don’t want to beat a dead horse, but inflation accelerating and beating the expectations of 8.8%, is paramount to the trajectory of tech shares.

The awful number also underscores the magnitude of policy mistakes that the U.S. Fed Central Bank has overseen.

This is the only thing that matters because macro liquidity drives the trajectory of equities in the short term.

These clowns aren’t serious about tackling inflation, as I said a few times already and this proves it!

Itty bitty rate rises won’t stamp out 9.1% inflation and in fact, encourages it.

The Fed would need to raise the Fed Funds rate by 7.35% to 9.1% immediately from the current 1.75% for the real inflation rate to be non-inflationary.

According to the official Fed website, the Fed targets 2% inflation because they call this level “healthy.”

By their own measure, to achieve this 2% inflation, they would still need to raise rates by 5.35% immediately, but they absolutely won’t because Powell simply has no interest in doing his job, period.

These core expenses skyrocketing is why I keep and kept mentioning that Americans have less money to splurge on tech gadgets and software and again, this inflation report validates my thesis.

Think about pitiful tech stocks that didn’t work in bull markets like ride chauffeurs Lyft (LYFT) and Uber (UBER), I fully expect these companies to perform terribly over the next 6 months amid a rising rate backdrop.

Not only are they growth tech, but their business is directly tied to energy prices.

They are the poster boys for the pain tech companies will feel from hyperinflation.

The outlook is quite poor for technology in the short term, and we are still waiting to form a bottom. It will come back but we need a capitulation.

The accelerated rate of inflation means that we push back the big recovery in tech stocks.

Ecommerce stocks will suffer like Amazon (AMZN), Shopify (SHOP), and MercadoLibre (MELI) because of the decline in discretional spending for the consumer.

Digital ad giants like Google (GOOGL), Snap (SNAP), Meta (META), and Twitter (TWTR) will need to reckon with smaller ad budgets from 3rd party ad purchasers as companies cut back on marketing spend.

Don’t need to increase marketing spend when people have no money to spend on products.

Travel tech stocks like Expedia (EXPE) and Tripadvisor (TRIP) can expect summer to mark peak travel as Americans get more concerned about food and oil budgets after the summer of travel revenge from the arbitrary lockdowns.

It also means there will be a meaningful next leg down for tech stocks as many CFOs are now furiously crunching the new revenue and margin downgrades to reflect this heightened risk.

The new re-rating isn’t reflected yet in tech shares.

It’s already been a few months on the trot where many analysts say this is the top, they have been inaccurate every time.

Even if it is the top, inflation will stay higher for longer and stagflation is the consensus for 2023.

The clowns at the Fed not doing their job means that economic cycles will be shorter and a great deal more volatile because the smoothing effect of moderated inflation is now stripped out of calculations. This effectively means a contracted boom-bust trajectory for tech stocks which is unequivocally what we are seeing in market behavior.

Mad Hedge Technology Letter

March 26, 2021

Fiat Lux

Featured Trade:

(AVOID THIS KOREAN ECOMMERCE COMPANY)

(CPNG), (AMZN), (GRUB), (UBER), (JD), (SHOP), (MELI)

I might characterize Coupang (CPNG) as something akin to China’s JD.com.

It's an e-commerce company that has fulfillment solutions, not dissimilar to Amazon (AMZN) Fulfillment. They also have storefronts that they provide for businesses, which isn't dissimilar to say, a Shopify (SHOP).

Even combining aspects of Amazon and Shopify are there but they don’t have the powerful AWS cloud business.

Similar to JD.com (JD), which is a Chinese e-commerce platform, Coupang has differentiated itself by owning its entire logistics and delivery system.

What is different about Coupang versus the other players in Korean e-commerce is that they own their own inventory for the most part.

That means that they have inventory sitting on their balance sheets.

They have responsibility for pushing that through. But it also means, since they directly negotiate with the manufacturers of these items, they're able, for the most part, to get lower prices.

Total Korean e-commerce spend was $128 billion in 2019, which is expected to grow to $206 billion by 2024, implying a CAGR of approximately 10%.

This is where Coupang has a chance but in a rising interest rate environment and with competition on the New York exchanges from Amazon (AMZN), Shopify (SHOP), even MercadoLibre (MELI), I don’t believe Coupang is more attractive than these 3 in its current form as it relates to American investors pouring money into their stock.

Is it an advantage if 70% of Koreans live within seven miles of the Coupang logistic centers?

Certainly, there is that train of thought.

The massive investments into fulfillment centers mean they can surpass the delivery speed of many of its competitors because South Korea is essentially one capital city with millions upon millions hovering on top of each other like many other parts of Asia.

The problem I can have with this scenario is that margins could suffer because a busy Korean lifestyle doesn't lend itself to things like in-store shopping as readily as it does in the United States, and it could manifest itself with Koreans tapping into higher frequency in which they buy online which will push up total spend, but margins will decrease because you are buying stuff that won’t move the needle higher because you've paid for the service.

I can easily see someone just buying one item for delivery in the morning and doing that seven days per week.

Now I need a set of tweezers, I'm going to order that. Tomorrow, I need cotton pads, I’m going to order that.

Over time, operating margin will get butchered with a business like this.

And what do you know? I’m right, they have been losing billions upon billions the past few years with no end in sight.

How long will the external investors subsidize their losses?

At a broader level, mobile phone penetration is already at 96% of Koreans and 40% of Koreans order groceries online, so it’s hard for me to digest where the addressable market can expand from here because they have already collected so much of the available harvest.

This IPO does feel a little bit like an ex-growth dump on the retail investor and that’s not saying shares can’t appreciate at all, but investors believing this is the next Amazon are sorely mistaken.

They are not Amazon, not even close, and they are also confined to one small market where the population has peaked and will start decreasing in numbers.

The population is only 15% of the U.S. and incomes in the U.S. are vastly higher, so how does Coupang become an Amazon without the AWS business?

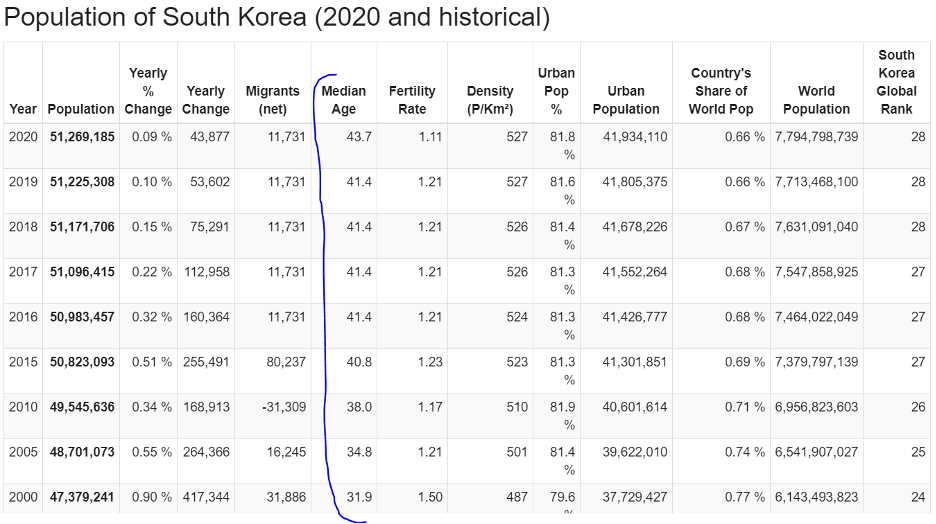

Just as disturbing, the median age in Korea has ballooned from 31.9 in 2000 to 43.7 in 2020 and this cohort doesn’t strike me as the group in the glory years of family formation, peak spend, or technological know-how.

As the Korean population starts to decline in 2025 and the median age creeps up from 43.7 to 50, then aside from adult diapers, where does the incremental growth come from in Korea?

I just don’t see it.

Personal incomes are going to rise at an annualized rate of about 3% every year and I believe much of the total spend will be fought out attempting to woo the big buyers which offer a point of attack for competition that should come around in the next 2 to 3 years.

They also have Coupang Eats, not dissimilar to Grubhub (GRUB) or Uber (UBER) Eats. They have grocery delivery, and even an integrated payment processor. All of these things that took Amazon much longer to build out, admittedly, were a little before their time there, Coupang has already integrated that into the platform.

For this, I give them credit, but they are still nothing like Amazon in terms of potency and scale.

In 2019, active customers rose 34% and that’s what a prototypical growth company should do.

It’s not shocking.

Then an analyst would think that with covid and all that public chaos pinning consumers at home, surely, Coupang would grow active customers by 50% of even 60% in 2020, right?

But active customers only grew 18% in 2020, and they provided zero insight about why active customer growth slowed nearly in half year-over-year, and that for me shows, Coupang is severely limited by what Korea can offer in terms of growth and total spend.

If readers want to get into the Korean economy then I would advise to wait on other Korean homegrown entrepreneur-led startups with IPOs in the pipeline by Krafton Inc., the creator of hit game PUBG, and the country’s biggest mobile-only bank Kakao Bank. Unlike Coupang, those firms are profitable.

Ultimately, total e-commerce spend for all Internet buyers in Korea is expected to grow from approximately $2,600 in 2019 to approximately $4,300 in 2024 on a per buyer basis and Coupang will take advantage of that but I don’t foresee the 30% annual rise in underlying shares that others do.

I can definitely visualize a grind up with periodical substantial selloffs because of missed targets and disappointing forecasts.

That’s not the type of price action I want to see.

The signs point to Coupang maturing immediately and the executive management creating a special clause to allow them to dump shares right after the IPO illustrates that this tech company will stall out moving forward.

Normally, management must wait 6 months after going public before the lock-up period ends.

Highly unusual and can you believe it? They even gave stock shares to their courier drivers at the IPO, making me pause, then come to the conclusion that I rather invest in a tech company returning incremental value to the shareholders and not the manual labor that is paid by an hourly wage. How bizarre!

Avoid Coupang like the plague.

Mad Hedge Technology Letter

December 18, 2020

Fiat Lux

Featured Trade:

(TECH IN 2021)

(ZM), (WORK), (NVDA), (AMD), (QCOM), (SQ), (PYPL), (INTU), (PANW), (OKTA), (CRWD), (SHOP), (MELI), (ETSY), (NOW), (AKAM), (TWLO)

The tech sector has been through a whirlwind in 2020, and if investors didn’t lose their shirt in March and sell at the bottom, many of them should have ended the year in the green.

My prediction at the end of 2019 that cybersecurity and health cloud companies would outperform came true.

What I didn’t get right was that almost every other tech company would double as well.

Saying that video conferencing Zoom (ZM) is the Tech Company of 2020 is not a revelation at this point, but it shows how quickly a hot software tool can come to the forefront of the tech ecosystem.

M&A was as hot as can be as many cash-heavy cloud firms try to keep pace with the Apples and Googles of the tech world like Salesforce’s purchase of workforce collaboration app Slack (WORK).

Not only has the cloud felt the huge tailwinds from the pandemic, but hardware companies like HP and Dell have been helped by the massive demand for devices since the whole world moved online in March.

What can we expect in 2021?

Although I don’t foresee many tech firms making 100% returns like in 2020, they are still the star QB on the team and are carrying the rest of the market on their back.

That won’t change and in fact, tech will need smaller companies to do more heavy lifting come 2021.

The only other sector to get through completely unscathed from the pandemic is housing, and unsurprisingly, it goes hand in hand with converted remote offices that wield the software that I talk about.

The world has essentially become silos of remote offices and we plug into the central system to do business with each other with this thing called the internet.

In 2021, this concept accelerates, and cloud companies could easily check in with 20%-30% return by 2022. The true “growth” cloud firms will see 40% returns if external factors stay favorable.

This year was the beginning of the end for many non-tech businesses and just because vaccines are rolling out across the U.S. doesn’t mean that everyone will ditch the masks and congregate in tight, indoor places.

There is nothing stopping tech from snatching more turf from the other sectors and the coast couldn’t be clearer minus the few dealing with anti-trust issues.

I can tell you with conviction that Facebook, Google, Apple, and Amazon have run out of time and meaningful regulation will rear its ugly head in 2021.

We are already seeing the EU try to ratchet up the tax coffers and lawsuits up the wazoo on Facebook are starting to mount.

Eventually, they will all be broken up which will spawn even more shareholder value.

Even Fed Chair Jerome Powell told us that he thinks stocks aren’t expensive based on how low rates have become.

That is the green light to throw new money at growth stocks unless the Fed signal otherwise.

As we head into the 5G world, I would not bet against the semiconductor trade and the likes of Nvidia (NVDA), AMD (AMD), Qualcomm (QCOM) should overperform in 2021.

Communication is the glue of society and communications-as-a-platform app Twilio (TWLO) will improve on its 2020 form along with cloud apps that make the internet more efficient and robust like Akamai (AKAM).

Workflow cloud app ServiceNow (NOW) is another one that will continue its success.

The uninterrupted shift to the cloud will not stop in 2021 and will be a strong growth driver for numerous tech companies next year.

I will not say this is a digital revolution, but as corporate executives realize they haven’t spent enough on the cloud in the lead-up to the pandemic and must now play catch-up in order to satisfy new demands in the business.

The most recent CIO survey was the thesis that cloud and digital adoption at 10% of enterprise and 15% of consumer spend entering 2020 would continue to accelerate post-pandemic and into 2021-2022.

A key dynamic playing out in the tech world over the next 12 to 18 months is the secular growth areas around cloud and cybersecurity that are seeing eye-popping demand trends.

Consumers will still be stuck at home, meaning e-commerce will still be big winners in 2021 such as Shopify (SHOP), Etsy (ETSY), and MercadoLibre (MELI).

The reliance on e-commerce will open the door for more tech companies to participate in the digital flow of transactions and the U.S. will finally catch up to the Chinese idea of paying through contactless instruments and not cards.

This highly benefits U.S. fintech companies like Square (SQ) and PayPal (PYPL). Intuit (INTU) and its accounting software is another niche player that will dominate.

Intuit most recently bought Credit Karma for $8.1 billion signaling deeper penetration into fintech.

Since we are all splurging online, we need cybersecurity to protect us and the likes of Palo Alto Networks (PANW), Okta (OKTA), and CrowdStrike Holdings, Inc. (CRWD).

The side effect of the accelerating shift to digital and cloud are troves of data that need to be stored, thus anything related to big data will also outperform.

Most of the information created (97%) has historically been stored, processed, or archived.

As new mountains of digital gold are created, we expect AI will have an increasingly critical role.

I believe that 2021 will finally see the integration of 5G technology ushering in another wave of digital migration and data generation that the world has never seen before and above are some of the tech companies that will make out well.

The average household is using 38x the amount of internet data they were using ten years ago and this is just the beginning.

Mad Hedge Technology Letter

November 30, 2020

Fiat Lux

Featured Trade:

(THE GREEN LIGHT FOR E-COMMERCE)

(AMZN), (W), (OSTK), (WMT), (TGT), (MELI), (EBAY), (CRM), (ADBE)

Data from Adobe Analytics is in and it suggests that e-commerce is delivering on its expected domination over retail.

I can’t ignore the helping hand of the pandemic which has deemed pedestrian shopping malls too dangerous to set foot in and for analog businesses that survive, it is essentially coming down to whether a digital footprint has been developed or not.

There is only so much a PPP loan can do to paper over the cracks of a non-digital business.

At some point, CEOs will need to wake up and understand that survival means a migration to digital.

Forecasts show that Black Friday online sales will register between $8.9 billion and $10.6 billion, which represents growth of up to 42% year over year.

The data firm expects Black Friday and Cyber Monday to become the two largest online sales days in history as consumers shift more spending toward e-commerce amid the public health crisis.

By last Friday morning, Salesforce projected online sales in the U.S. for Black Friday to spike 15% to $11.9 billion.

The truth is that many shoppers got their shopping done even before Thursday and Friday with digital sales in the U.S. spiking 72% year over year on Tuesday and were up 48% on Wednesday.

E-commerce companies front-ran the actual holidays to eke out more profit in the anticipation of competitors offering earlier sales.

According to Adobe, Thanksgiving sales hit a record $5.1 billion, up 21.5% over 2019 and this aggressive growth rate can be considered the new normal.

Smartphones continued to account for an increasing segment of online sales, with this year’s $3.6 billion up 25.3%, while alternative deliveries — a sign of the e-commerce space maturing — also continued to grow, with in-store and curbside pickup up 52% on 2019.

Shopify said that over 70% of its sales are being made using smartphones.

What are the hot gift items?

Electronics, tech, toys, and sports goods being the most popular categories — at the right price will help retailers continue to experience elevated sales volume.

Adobe said a survey of consumers found that 41% said they would start shopping earlier this year than previous years due to much earlier discounts.

This season is headed for record-breaking levels as consumers power online sales for both holiday gifts and necessities.

Not all big-box retailers were open over the holidays and getting that extra surge from the likes of daily needs such as paper towels, cleaning products, and garbage bags has boosted the top-line growth as well.

We have seen the perfect storm of elements fuse together to help the bottom line records of the likes we have never observed.

Comps will be difficult to beat next year if the vaccine solution starts coming online by next winter and considering that the worst economic damage is behind us.

Next year, the U.S. consumer will have more to spend setting up a tough but possible beat to next year’s numbers along with the high likelihood that tech stocks will experience another leg up.

There will be a lot happening in between, such as a new U.S. administration that is primed for a different economic polic; but it’s impossible not to love the narrative of certain e-commerce companies such as Shopify (SHOP), MercadoLibre (MELI), Target (TGT), Walmart (WMT), Etsy (ETSY), Wayfair (W), eBay (EBAY), Overstock.com (OSTK), Amazon (AMZN) and the companies that measure their data like Salesforce (CRM) and Adobe (ADBE).

If we ever could anoint when a year became the year of technology, then this would be it in 2020.

The base case for next year is that the borders and states will still grapple with the virus and the knock-on effects to society, economy, and politics as the capacity to produce the virus won’t meet demand for at least a year.

Tech stocks are primed to outperform non-tech next year and even though multiples are high, the momentum suggests that this group of stocks will be the gift that keeps giving as the Fed has offered generous liquidity conditions to tech investors.

Mad Hedge Technology Letter

October 5, 2020

Fiat Lux

Featured Trade:

(THE AMAZON OF LATIN AMERICA)

(MELI), (AMZN), (ASML)

If you thought you missed profiting off of Amazon then you’re in luck; you still have another chance with the South American iteration of Amazon – MercadoLibre (MELI).

This e-commerce and payments platform in Latin America boasts presence in 18 countries within South and Central America but derives the bulk of its revenue from three countries: Brazil, Argentina, and Mexico.

MELI is the entrenched e-commerce player in the region and has multiple retailer solutions such as MercadoLibre Marketplace (an online platform for the buying and selling of merchandise), Mercado Pago (an online payments solution), and Mercado Envios (a logistics solution).

The company's market-leading position revolves around a strong network effect that has allowed it to expand its exploding user base as well as its gross merchandise volume (GMV).

In 2015, MELI had around 145 million registered users, and that number has more than tripled by 2020.

The tectonic shift toward digital transactions network caused by the pandemic means the number of items sold jumped 66% year over year to 284 million, and the number of unique active users climbed 27% year over year.

It’s undeniable that the company has strong tailwinds backing its overarching story.

MELI was already primed for a strong growth trajectory before the pandemic crushed the global economy.

The company was savvy in introducing new and useful services over the years to solve digital bottlenecks, and its suite of services made customers stickier toward its platform.

Hosting an integrated e-commerce and payments platform meant an unrelenting buildup of new vendors and users coming on board over time.

MELI looks set to take the next step in e-commerce penetration.

Although its growth has been phenomenal over the last decade, I believe the company may be on the cusp of doubling its growth rate because of the rapid digitalization by businesses.

A share repurchase program has been set in motion and I do believe they will dip into this financial tool once the global economy stabilizes.

Getting into the weeds, MELI expanded its category-take rates to Chile and Mexico in Q2 2020, with Brazil and Argentina set for last half of 2020.

For online marketplaces like what Amazon and eBay offer, the take rate refers to the fees and commissions that the companies collect on sales by third-party sellers which is critical to overall revenue.

The successful take rate rationalization could drive sellers to list more of their inventory and reduce prices.

With this increased supply, MELI should be seeing the cascading benefits of an improving shopping experience and rising conversion rates.

Scaling this beautifully translates to lower per-unit logistic costs such as sequential 23% decrease in unit shipping costs.

Ala Amazon, its drive to step up the buildout of its own logistics network to take down the dependency on Correios in Brazil is yielding meaningful results and also places the company to potentially buttress a greater amount of free shipping subsidies as the unit cost of deliveries continues to swan dive.

Logistics transforming into a higher reliability, faster shipping times, and greater cost savings offering can be passed along to the consumer upgrading the quality of service.

Soon, MELI is expected to invest in Consumer Electronics and price competitiveness could see the company grab market share taking down yet another adjacent industry.

At some point, like Amazon, MELI will target the grocery market and will have the logistic infrastructure in place to do the same type of 1-day “free” shipping that Amazon guarantees.

On the digital payments side of the business, MELI has sold over 1 million mobile point-of-sale (mPOS) devices, versus 900,000 during Q1 2020, driven primarily by smaller merchants.

The individual bull case for MELI is rock-solid but feeling out the global state of affairs is a must in a quickly changing environment.

With an onslaught of stimulus in Europe and the U.S. to deal with the pandemic, China’s economy beginning to recover, and a weaker dollar, foreign markets are becoming more attractive to U.S. investors.

Emerging markets could turn from stock market pariah to darling in a nanosecond and if investors are comfortable with targeting companies in higher growth markets, then MELI should be an option.

Emerging markets broadly have lagged behind developed market peers over the past decade, even as some fund managers have found investing in domestically-oriented companies in India, China, or Brazil hugely rewarding—just look at the outperformance by foreign brand names like Alibaba Group (BABA), Meituan Dianping and HDFC Bank (HDFC) in India just to name a few.

It’s true that more developed markets have the advantages of greater trading liquidity, minimal systemic risk, better corporate governance, and greater access to dollar-denominated debt that emerging markets’ companies don’t benefit from.

Therefore, investors seeking a conservatively biased portfolio should only focus on U.S. tech brand names that have moats around their business model.

Another second derivate play would be to find U.S. tech companies that siphon a big chunk of sales in emerging markets and are U.S. companies like Apple (AAPL), Nvidia (NVDA), and Mastercard (M).

Each secures between one-third and two-thirds of sales from emerging markets. But with those companies vulnerable to the geopolitical trip wire between the U.S. and China, proportioning a small amount of the portfolio to a Latin American tech growth firm could produce alpha.

Another quick recommendation is ASML, a semiconductor chip company from the Netherlands.

It’s an option generating outsized sales coming from emerging markets but is headquartered in an economically responsible country.

This Dutch tech firm boasts positive free cash flow yields, a sign the company is generating ample cash to operate and also reinvest in itself.

Investors who can stomach greater risk levels and desire growth should take a serious look at MELI, plus the myriad of other tech recommendations I offered if MELI doesn’t suit your appetite.