Mad Hedge Biotech & Healthcare Letter

May 4, 2021

Fiat Lux

FEATURED TRADE:

(A BAD NEWS BUY STOCK)

(AZN), (PFE), (BNTX), (MRNA), (JNJ)

Mad Hedge Biotech & Healthcare Letter

May 4, 2021

Fiat Lux

FEATURED TRADE:

(A BAD NEWS BUY STOCK)

(AZN), (PFE), (BNTX), (MRNA), (JNJ)

Along with Pfizer (PFE), BioNTech (BNTX), and Moderna (MRNA), one of the biggest potential winners in the COVID-19 vaccine race is AstraZeneca (AZN).

While the company did manage to develop a vaccine nearly as fast as the others, its product is now suffering the same fate as Johnson & Johnson’s (JNJ) candidate and is getting bogged down by blood clotting issues.

As if that isn’t enough, AstraZeneca’s plan to use its diabetes drug Farxiga as another potential COVID-19 treatment also flopped.

Needless to say, it looks like not a lot of things are going well for AstraZeneca in the past months.

Looking at its fundamentals though, it’s worth noting that AstraZeneca stock might just be one of those rare prime candidates for being bad news buys.

After all, the company never really had plans to profit from its COVID-19 vaccine venture. In fact, AstraZeneca has long announced that it would sell its vaccine at cost. Hence, any bad news from the vaccine won’t really affect the company’s sales.

For years, AstraZeneca has been focused on creating a hyper-growth product lineup in several of the pharmaceutical industry’s most profitable submarkets.

In fact, the Phase 3 advanced pipeline candidates of the company are some of the most promising candidates in the industry, with these soon-to-be-launched drugs already generating 24% growth in revenue as early as 2017.

Not including cancer, there are at least 2.1 billion people globally who suffer from various chronic diseases. That accounts for over 25% of the entire human population, thereby representing a massive and lucrative addressable market--the very same market that AstraZeneca has been targeting.

In the years to come, AstraZeneca is projected to release at least six blockbuster drugs—each one of them estimated to rake in more than $1.3 billion in sales annually.

At the moment, one of the company’s major growth drivers is its oncology franchise, which has an early-stage pipeline anticipated to rake in roughly $1.3 billion each year by 2026.

In particular, AstraZeneca’s recently released cancer drugs Imfinzi and Tagrisso are well-positioned to dominate the segment thanks to their leading efficacy when it comes to hard-to-treat cancer types.

Meanwhile, other sub-sectors are expected to contribute $2.65 billion annually.

So far, AstraZeneca operates in more than 70 countries, ensuring its presence in practically all potential addressable markets.

In China alone, the company’s new product sales have risen by 68%, while the rest of the emerging markets recorded 56% growth.

Despite the negative publicity of its COVID-19 vaccine recently, AstraZeneca still managed to report positive data for its first quarter earnings.

Within this period, the company generated $7.2 billion in revenue, which is 15% more than its earnings during the same time last year. Its earnings per share rose by 100% to reach $1.19, while its core earnings were up 55%.

This is a welcome surprise, especially since analysts predicted $0.75 per share for the company.

The rise in AstraZeneca’s stock performance was driven mostly by its best-selling drugs, including Tagrisso with $1.15 billion in sales in the first quarter of 2021 alone and showing off a 17% jump year-over-year.

Even with the failed COVID-19 treatment, the diabetes drug Fargixa soared this quarter with $625 million, indicating a 54% increase from its previous performance during the same period.

More importantly, AstraZeneca has been consistently paying investors a dividend since it started doing it 20 years ago—a trend that’s expected to continue since the company is poised to become one of the fastest growing businesses in the world with 15% growth annually.

Given its pipeline programs and current portfolio of products, AstraZeneca is on track to continue its hypergrowth through 2023. At this pace, we can expect an estimated 105% in total returns and compound annual growth rate returns at 30.2%.

Currently, AstraZeneca stock is experiencing some turbulence due to the bad news linked to its COVID-19 vaccine. Now would be the best time to buy the dips on the bad news.

Global Market Comments

April 30, 2021

Fiat Lux

Featured Trade:

(APRIL 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(PFE), (MRNA), (USO), (DAL), (TSLA), (CRSP), (ROM), (QQQ), (T), (NTLA),

(EDIT), (FARO), (PYPL), (COPX), (FCX), (IWM), (GOOG), (MSFT), (AMZN)

Below please find subscribers’ Q&A for the April 28 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley, CA.

Q: There is talk of digital currencies being launched in the US. Is there any truth to that? How would that affect the dollar?

A: There is no truth to that; there is not even any serious discussion of digital currency at the US Treasury. My theory has always been that once Bitcoin works and is made theft-proof, the government will take it over and make that the digital US dollar. So far, Bitcoin has existed regulation-free; in fact, the IRS is counting on a trillion dollars in capital gains being taxed going forward in helping to address the budget deficit.

Q: If you have a choice, what’s the best vaccine to get?

A: The best vaccine is the one you can get the fastest. I know you’re a little slow on the rollout in Canada. Go for Pfizer (PFE) if you’re able to choose. You should avoid Moderna (MRNA) because 15% of people getting second shots have one-day symptoms after the second shot. But basically, you don’t get to choose, only kids get to choose because only Pfizer has done trials on people under the age of 21. So, if you take your kids in, they will all get Pfizer for sure.

Q: Should I buy Freeport McMoRan (FCX) here or wait for a bigger dip?

A: Freeport has just had a 25% move up in a week. I wouldn’t touch that. We put out the trade alert when it was in the mid $30s, and it's essentially at its maximum profit point now. So, you don't need to chase—wait for a bigger dip or a long sideways move before you get in.

Q: How do I trade copper if I don't do futures?

A: Buy (FCX), the largest copper producer in the US, and they have call options and LEAPS. By the way, if we do get another $5 dip in Freeport, which we just had, I would really do something like the (FCX) $45-$50 2023 LEAP. You can get 5 times your money on that.

Q: Time to buy oil stocks (USO) for the summer?

A: No, the big driver of oil right now is the pandemic in India. They are one of the world's largest consumers—you find out that most poor countries are using oil right now as they can’t afford the more expensive alternative sources of power. And when your biggest customer is looking at a billion corona cases, that’s bad for business. Remember, when you trade oil, you’re trading against a long-term bear trend.

Q: Would you buy Delta Airlines (DAL) at today’s prices?

A: Yes, I’m probably going to go run the numbers on today's call spread; I actually have 20% of cash left that I could spend. So that looks like a good choice—summer will be incredible for the entire airline industry now that they have all staved off bankruptcy. Ticket prices are going to start rising sharply with an impending severe aircraft shortage.

Q: What are your thoughts on the Buffet index which shows that stocks are more stretched vs GDP at any time vs 2000?

A: The trouble with those indicators is that they never anticipated A) the Fed buying $120 billion a month in US Treasury bonds, B) the Fed promising to keep interest rates at zero for three years, and C) an enormous bounce back from a once-in-a-hundred-year pandemic. That's why not just the Buffet Index but virtually all technical indicators have been worthless this year because they have shown that the market has been overbought for the last six months. And if you paid attention to your indicators, you were either left behind or you went short and lost your shirt. So, at a certain point, you have to ignore your technical indicators and your charts and just buy the damn market. The people who use that philosophy (and know when to use it, and it’s not always) are up 56% on the year.

Q: What trade categories are getting fantastic returns? It’s certainly not tech.

A: Well, we actually rotated out of tech last September and went into banks, industrial plays, and domestic recovery plays. And you can see in the stocks I just showed you in our model portfolio which one we’re getting the numbers from. Certainly, it was not tech; tech has only performed for the last four weeks and we jumped right back in that one also with positions in Microsoft (MSFT). So yes, it’s a constantly changing game; we’re getting rotations almost daily right now between major groups of stocks. The only way to play this kind of market is to listen to someone who’s been practicing for 52 years.

Q: I am 83 years old and have four grandchildren. I want to invest around $20,000 with each child. I was thinking of your bullish view on Tesla (TSLA) on a long-term investment. Do you agree?

A: If those were my grandchildren, I would give them each $20,000 worth of the ProShares Ultra Technology Fund (ROM), the 2x long technology ETF. Unless tech drops 50% from here, that stock will keep increasing at twice the rate of the fastest-growing sector in the market. I did something similar with my kids about 20 years ago and as a result, their college and retirement funds for their kids have risen 20 times. So that’s what I would do; I would never bet everything on a single stock, I would go for a basket of high-tech stocks, or the Invesco QQQ NASDAQ Trust (QQQ) if you don’t want the leverage.

Q: Do you like Amazon (AMZN) splitting?

A: I don’t think they’ll ever split. Jeff Bezos worked on Wall Street (with me at Morgan Stanley) and sees splits as nothing more than a paper shuffle, which it is. It’s more likely that he’ll break up the company into different segments because when they get to a $5 trillion market cap, it will just become too big to manage. Also, by breaking Amazon up into five companies—AWS, the store, healthcare, distribution, etc., —you’re getting a premium for those individual pieces, which would double the value of your existing holdings. So, if you hold Amazon stock, you want it to face an antitrust breakup because the flotation will double the value of your total holdings. That has happened several times in the past with other companies, like AT&T (T), which I also worked on.

Q: When is Tesla going to move and why is it going up with earnings up 74%?

A: Well, the stock moved up a healthy 46% going into the earnings; it’s a classic sell the news market. Most stocks are doing that this quarter and they did so last quarter as well. And Tesla also tends to move sideways for years and then have these explosive moves up. I think the next double or triple will come when they announce mass production of their solid-state batteries, which will be anywhere from 2 to 5 years off.

Q: How can I renew my subscription?

A: You can call customer support at 347-480-1034 or email support@madhedgefundtrader.com and I guarantee you someone will get back to you.

Q: Top gene-editing stock after CRISPR Therapeutics (CRSP)?

A: There are two of them: one is Intellia (NTLA); it’s actually done better than CRISPR lately. The second is Editas (EDIT) and you’ll find out that the same professionals, including the Nobel prize winner Jennifer Doudna here at Berkeley, rotate among all three of these, and the people who run them all know each other. They were all involved in the late 2000's fundamental research on CRISPR, and they’re all frenemies. So yes, it's a three-company industry, kind of like the cybersecurity industry.

Q: What about PayPal (PYPL)?

A: I would wait for the earnings since so many companies are selling off on their announcements. See if they sell off 3-5%, then you buy it for the next leg up. That is the game now.

Q: Do you like any 3D printing stocks like Faro Technologies (FARO)?

A: No, that’s too much of a niche area for me, I’m staying away. And that's becoming a commodity industry. When they were brand new years ago, they were red hot, now not so much.

Q: Do you see the chip companies continuing their bull run for the next few months?

A: I do. If anything, the chip shortage will get worse. Each EV uses about 100 chips, and they’re mostly the low-end $10 chips. Ford (F) said production of a million cars will be lost due to the chip shortage. Ford itself has 22,000 cars sitting in a lot that are fully assembled awaiting the chips. Tesla alone has $300 worth of chips just in its inverters, and there are two inverters in every car. So, when you go from production of 500,000 cars to a million in one year, that's literally billions of chips.

Q: The airlines are packed; what are your thoughts?

A: Yes, one of the best ways to invest is to invest in what you see. If you see airlines are packed, buy airline stocks. If you can’t hire anyone, you know the economy is booming.

Q: What about the Russel 2000 (IWM)?

A: We covered it; it looks like it wants to break out to new highs from here. By the way, there are only 1,500 stocks left in the Russell 2000 after the pandemic, mergers, and bankruptcies.

Q: Are there other ways to play copper out there like (FCX)?

A: Yes; one is the (COPX)— a pure copper futures ETF. However, be careful with pure metal ETFs of any kind because they have huge contangos and you could get a 50% move up in your commodity while your ETF goes down 50% over the same time. This happens all the time in oil and natural gas, and to a lesser degree in the metals, so be careful about that. Before you get into any of these alternative ETFs, look at the tracking history going back and I think you'll see you're much better off just buying (FCX).

Q: How long do you typically hold onto your 2-year LEAPS? Based on my research, the time decay starts to accelerate after about 3 months to one year on LEAPS.

A: Actually, with LEAPS, the reason I go out to two years is that the second year is almost free, there's almost no extra cost. And it gives you more breathing room for this thing to work. Usually, if I get my timing right, my LEAP stocks make big moves within the first three months; by then, the LEAP has doubled in value, and then you have to think about whether you should keep it or whether there are better LEAPS out there (which there almost always are). So, you sell it on a double, which only took a 30% move in the stock, or you may be committed to the company for the long term, like a Microsoft or an Amazon. And then you just run it through the expiration to get a 400% or 500% profit in two years. That is how you play the LEAP game.

Q: Are these recorded?

A: Yes, we record these and we post them on the website after about 2 hours. Just log into the site, go to “my account”, then select your subscription type (Global Trading Dispatch or Technology Letter), and “webinars” will be one of the button choices.

Q: Can you also sell calls on LEAPS?

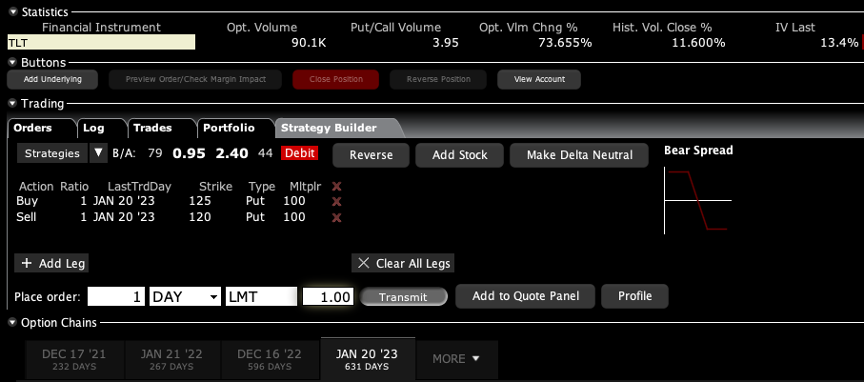

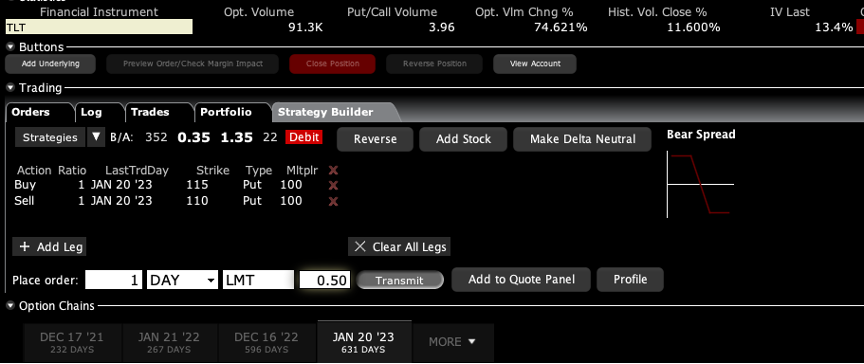

A: Yes and the only place to do that is the US Treasury market (TLT). There you either want to be short calls far above the market, out two years, or you want to be long puts. And by the way, if you did something like a $120-$125 put spread out to January 2023, then you’re looking at making about a 400% gain. That is a bet that 20-year interest rates only go up a little bit more, to 2.00%. If you really want to bet the ranch, do something like a $120-$122 and you might get a 1000% return.

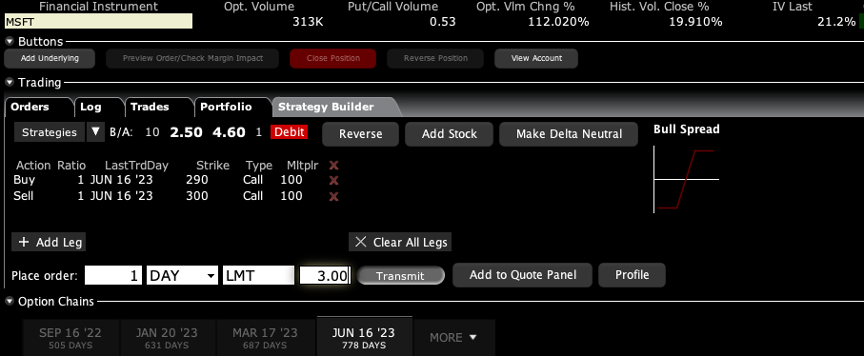

Q: What is the best LEAP to trade for Microsoft (MSFT)?

A: If you want to go out two years, I would do something like a June 2023 $290-$300 vertical bull call spread. There is an easy 67% profit in that one on only a 20% rise in the stock. I do front monthlies for the trade alert service, so we always have at least 10 or 20 trade alerts going out every month. And the one I currently have for is a deep in the money May $230-$240 vertical bull call spread which expires in 12 days.

Q: What is the best way to play Google (GOOG)?

A: Go 20% out of the money and buy a January 2023 $2,900-$3,000 vertical bull call spread for $20—that should make about 400%. If you want more specific advice on LEAPS, we have an opening for the Mad Hedge Concierge Service so send an email to support@madhedgefundtrader.com with subject line “concierge,” and we will reach out to you.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

I Think I See Another Winner

Mad Hedge Biotech & Healthcare Letter

April 13, 2021

Fiat Lux

FEATURED TRADE:

(MEGA CAP PHARMA UP FOR GRABS)

(MRK), (ABMD), (ILMN), (ALGN), (JNJ), (GILD), (PAND), (ALKS), (IMV)

Since the great 2007 financial crisis, many companies have been coping to recapture their former glory. The healthcare industry is not spared of this struggle.

This makes the continuous growth of Merck (MRK) all the more impressive, with the company reaching $195 billion in market capitalization and sustaining its rise for over 130 years.

Curiously, Merck’s share price is still in the mid-$70s.

Meanwhile, other large-cap biopharmaceutical companies that offer similar products and services are trading higher.

For instance, the share price for Abiomed (ABMD) is over $330 while Illumina (ILMN) is nearly $400, and Align Technology (ALGN) is at a whopping $600.

Like Merck, investors gravitate towards Abiomed, Illumina, and Align because of their capacity to generate long-term sustainable revenues and boost earnings.

Notably, though, none of them hold the same depth or even breadth of products and services that Merck offers.

Recently, Merck disclosed some of its initiatives to boost the company’s earnings in the near- and long term.

One of the most visible efforts is its collaboration with Johnson & Johnson (JNJ) to help with the manufacturing of JNJ-78436735, in which Merck received federal funding.

While JNJ is one of the biggest healthcare companies across the globe, with a market capitalization of roughly $425 billion, joining forces with Merck will substantially boost its vaccine manufacturing capacity.

For context, JNJ’s goal prior to Merck’s help is to deliver 100 million doses by the end of the second quarter of 2021.

With Merck’s assistance, JNJ can now realistically manufacture up to 3 billion doses in 2022 alone.

This means that JNJ can implement a massive vaccination drive in the next two years since its manufacturing capacity ensures that it can deliver shots to over one-third of the population.

This is obviously good news for everyone as it means that the virus will be contained, but the enhanced manufacturing capacity also means profit accretion for both JNJ and Merck.

This partnership with JNJ is possibly a key factor in Merck’s move to invest heavily in the vaccine business.

Merck recently announced its plans to allocate $20 billion to expand its global vaccine manufacturing network from 2021 to 2024. This would mean an annual investment of $5 billion.

Part of this global vaccine plan is Merck’s acquisition of Pandion Therapeutics (PAND) in 2020.

Another recent initiative of the company is its joint effort with Gilead Sciences (GILD) to develop long-lasting HIV treatments.

Gilead will be in charge of the US market, while Merck will handle the EU and the rest of the international markets.

For starters, the companies will focus on a combination of Merck’s Islatravir and Gilead’s Lenacapavir to create a long-lasting and well-tolerate HIV treatment.

Outside these partnerships, Merck has been working on strengthening its oncology segment.

In fact, its top-selling drug, Keytruda, can be used to medicate an extensive range of indications, which include colorectal, esophageal, and even lung cancers.

At this point, Keytruda is generating north of $16 billion in sales every year and exhibiting roughly 30% growth annually.

Since the drug continues to gain approvals for additional indications, it looks like its growth runway is definitely far from over.

Keytruda is poised to reach $24 billion in annual sales in a few years’ time, which puts it on track to become the best-selling drug in the world by 2023.

Although Keytruda will be under patent protection until 2028, Merck remains active in expanding its oncology pipeline.

By then, Merck is projected to have multiple immunotherapy staples in its portfolio not only derived from its own R&D but also via partnerships like its 2020 collaboration with Alkermes (ALKS) to work on an ovarian cancer study and Immunovaccine (IMV) to cooperate on a blood cancer study.

The total oncology market is estimated to be $200 billion annually, with over 30 million cases projected to be added by 2040.

Overall, Merck is a well-oiled company that continues to deliver good results thanks to strategic acquisitions and partnerships neatly tied up together in a particular domain.

While its rival biotechnology and pharmaceutical companies become hot properties in the market and pose higher price tags, Merck silently moves forward in the shadows of sustainability and familiarity.

Mad Hedge Biotech & Healthcare Letter

April 8, 2021

Fiat Lux

FEATURED TRADE:

(A LOW-KEY POST-COVID-19 RECOVERY STOCK)

(REGN), (MRNA), (NVAX), (BNTX) (PFE), (VIR), (LLY), (RHHBY), (NVS)

If you still remember the news about the flash recovery from COVID-19 of then-President Trump during the campaign period last year, then you know that the express cure was not delivered by any of the vaccine makers that were all the rage at the time like Moderna (MRNA), Novavax (NVAX), BioNTech (BNTX), or even Pfizer (PFE).

Instead, the cure was credited to a lesser-known cocktail of antibodies, called REGEN-COV, developed by Regeneron (REGN).

Recently, the same treatment was used in Germany in response to the shortage of COVID-19 vaccines and the demand for alternatives.

Despite the promising results and the highly publicized effects of Regeneron’s treatment, the company’s share price still hasn’t shown any meaningful upside.

Nonetheless, Regeneron still secured some agreements for REGEN-COV.

Based on the June 2020 agreement of Regeneron with the US government, the company expects to sell $260 million worth of REGEN-COV in the first quarter of 2021 for a fixed number of orders.

For the second quarter of 2021, though, the two parties set different terms for their deal.

Under these new terms, the US government will pay per dose regardless of REGEN-COV’s dose size.

Given the latest numbers from Regeneron’s trials, this could mean lower costs for the company.

Data from the clinical trials showed that REGEN-COV had the same effectiveness at the lower 1,200 mg dosage compared to the currently approved amount by the US FDA, which is 2,400 mg.

In fact, Regeneron’s treatment is reported to be as effective as the COVID-19 antibody therapies developed by Vir Biotechnology (VIR) and even Eli Lilly’s (LLY) candidate.

Looking at the positive results from Regeneron’s Phase 3 trials for REGEN-COV, it’s reasonable to expect higher sales than previously estimated.

Now, Regeneron shared that it aims to supply 1.25 million doses of the COVID-19 antibody therapy at the lower but equally effective 1,200 mg dose level.

If the FDA agrees to this emergency use authorization request, then Regeneron will be able to supply twice the number of COVID-19 doses.

If it delivers these doses by June 30, the US government will buy them for $2.6 billion regardless of the dosage used.

On average, Regeneron is expected to generate roughly $2.9 billion in sales for its COVID-19 antibody treatment.

Meanwhile, if REGEN-COV gains full FDA approval and gets marketed commercially, then the treatment can rake in at least $3.5 billion and peak at $5 billion this year alone.

Outside its COVID-19 program, Regeneron actually recorded better-than-expected results last year despite the pandemic ravishing the economy.

For example, there was a rebound in demand for its top-selling Eylea, with sales of the wet age-related macular degeneration (AMD) drug rising by 10% in the fourth quarter of 2020 to reach a total of $1.34 billion.

Bolstering the dominance of Eylea in the AMD market and to combat emerging competitors like Roche (RHHBY) with Faricimab and Novartis (NVS) with Beovu, Regeneron is looking to expand the drug’s application to cover more age groups.

Meanwhile, another bestseller, Dupixent, reached $1.17 billion in sales last year.

This is an impressive climb for the atopic dermatitis medication, which was developed with Sanofi (SNY), since it only recorded $751.5 million in the same period in 2019.

That indicates roughly 75% growth, with over a million prescriptions written for Dupixent in the US alone.

However, only 6% of those eligible patients have been treated with Regeneron’s product thus far.

This means that Dupixent has a lot of room to grow, with this drug estimated to reach peak sales at $12.5 billion.

Needless to say, Dupixent is quickly transforming into a blockbuster treatment.

Since its approval for eczema in 2017, this drug has expanded its indication to cover moderate-to-severe atopic dermatitis not only among teens but also children. Notably, Dupixent holds a monopoly for this application to children.

Another revenue stream for Regeneron is its oncology sector led by Libtayo.

In 2020, net sales of this skin cancer treatment reached $348 million, showing an impressive 80% growth.

To date, Regeneron has at least 12 oncology treatments under clinical development.

In terms of the bottom line, Regeneron exceeded the expectations of $8.38 and reported adjusted earnings per share of $9.53 instead.

As vaccine rollouts continue to be a priority, it’s safe to say that the worst of the COVID-19 is just about in sight.

Consequently, investors are now looking into recovery and stocks that appear to be good buys when the coronavirus eventually becomes a thing of the past.

Regeneron is one of the attractive buys so far. While it has been underperforming in the past weeks, its business actually looks to be in great shape even if the pandemic goes on for longer.

Mad Hedge Biotech & Healthcare Letter

March 30, 2021

Fiat Lux

FEATURED TRADE:

(A PURE PLAY STOCK SELLING AT A BARGAIN)

(PFE), (BNTX), (MRNA), (AZN), (JNJ), (NVAX), (MRK), (VTRS), (LLY), (REGN)

It’s virtually impossible to find a period in history when drug development gained the unmitigated attention of the whole world.

Yet, this is exactly what happened in 2020 when we all waited with bated breath for the results of COVID-19 trials from the likes of Pfizer (PFE), BioNTech (BNTX), Moderna (MRNA), AstraZeneca (AZN), Johnson & Johnson (JNJ), and Novavax (NVAX).

Despite this, it is astounding that biopharmaceutical stocks are cheaper than they have ever been in the past 20 years.

Given the fact that its collaboration with BioNTech made a central figure in the COVID-19 vaccine race, I think it’s best to put a spotlight on Pfizer today.

Pfizer was the first biopharmaceutical company to successfully market a COVID-19 vaccine, BNT162b2.

Recently, Pfizer received another good news. The FDA is no longer demanding that the company transport BNT162b2 at ultra-low temperatures.

When Pfizer revealed its strong results last year, the world was impressed and no one barely noticed the ultra-cold storage requirement that the achievement entailed.

But with competitors already gaining approvals as well, this particular requirement started to pose noticeable challenges to Pfizer’s vaccine supply chain and made it extremely challenging transporting the much-needed vaccines to remote areas.

These challenges highlight the significance of the recent FDA announcement regarding BNT162b2.

In terms of market share, Pfizer holds a significant advantage over the others.

As of the year-end of 2020, the company supplied 65 million doses to developed markets.

Meanwhile, the 2021 forecast for this product is at nearly 2 billion doses. This is estimated to rake in roughly $15 billion in revenue for Pfizer.

In comparison, Moderna’s advanced purchase deals are estimated to be worth $18 billion.

To sustain immunity, there’s the possibility that the vaccine would be needed annually.

This could lead to substantial demand for doses, with a two-dose vaccine like BNT162b2 projected to reach about 10 billion doses every year.

Realistically, the rising need for doses and the manufacturing requirements will obviously pressure profit margins.

However, if the vaccine does turn out to be an annual necessity, then it could become a valuable asset.

The entire COVID-19 market is estimated at $39 billion in 2021 and $23 billion in 2022.

Pfizer and even Moderna’s first mover advantage can easily help them dominate the market this year.

This means that the competition will heat up by 2022.

To ensure that it keeps the lead, Pfizer has commenced the Phase 1 trial for a COVID-19 pill.

Pfizer’s pill, dubbed PF-07321332, aims to inhibit the enzymes that cause the SARS-CoV-2 virus to replicate. The goal is to create an antiviral drug that works pretty much the same way as the one developed for HIV and Hepatitis C.

If the trials generate positive results, then PF-07321332 could be taken at the first sign of infection.

So far, lab results have shown the pill’s potent capacity to prevent the SARS-CoV-2 virus and other coronaviruses from replicating.

Pfizer isn’t the only one that came up with the idea of a COVID-19 pill. Merck (MRK), Eli Lilly (LLY), and Regeneron (REGN) have been conducting tests for their own version of the antiviral.

However, Pfizer is more than its COVID-19 programs.

In the past, investors wondered about the long-term growth potential of this company. Some questions are linked to its Upjohn unit, which included several products that lost patent exclusivity.

This segment clouded Pfizer’s pure play revenue and even its earnings growth. However, these questions were put to an end last year when Upjohn’s finally separated from Pfizer and formed a new company, Viatris (VTRS), with Mylan.

The effect of this move showed an amplified growth for Pfizer almost immediately.

In the fourth quarter alone of 2020, the company reported $11.68 billion in revenue, indicating a 12% increase year-over-year. If we exclude the sales from the COVID-19 vaccine, Pfizer’s revenue was still up by 8%.

Every key product segment in the company recorded revenue growth, which is remarkable considering the effects of the pandemic.

Revenue for its oncology sector went up 23% to reach $3 billion, with breast cancer treatment Ibrance leading the charge with an 11% boost to its sales to hit $1.4 billion.

To ensure that it corners the market, Pfizer also launched biosimilars Zirabev and Ruxience in the same quarter. Both generated $171 million in total.

Outside its COVID-19 program, other products in Pfizer’s vaccine segment significantly contributed to the 17% increase in revenue to reach $2 billion.

For example, the pneumonia vaccine Prevnar generated $1.8 billion thanks to the 10% boost in its revenue year-over-year.

As for Pfizer’s rare disease unit, revenue went up 24% to reach $865 million.

The segment leader so far is cardiomyopathy treatment Vyndagel, which achieved a jaw dropping 96% year-over-year boost in its revenue to generate $429 million. This product won’t face patent loss until 2026, so Pfizer still has a few more years to take advantage of it.

Pfizer’s revenues in 2020 were up 2% at $41.9 billion. Considering that it still managed to boost sales despite the pandemic, there’s a good chance that 2021 will be a better year for the company.

In fact, Pfizer estimates that it would reach nearly $60 billion in revenue, with an annualized EPS of roughly $3.15 in 2021.

Global sales in the biotechnology and healthcare industry are projected to be worth $1.2 trillion annually. This is a massive market that is all but guaranteed.

The S&P 500 trades at nearly 21.5x forward earnings, with pharmaceutical companies trading at only 13.2x. That’s a whopping 60% discount.

Considering that drug stocks have historically traded at roughly the same level as the S&P 500, the current situation still offers an unmistakable promise even if nothing else happens.

Continuous development in the sector not only advances our quality of life but also offers reasonable returns to investors.