Mad Hedge Biotech and Healthcare Letter

January 4, 2024

Fiat Lux

Featured Trade:

(A TURNAROUND TALE WORTH WATCHING)

(MRNA), (PFE)

Mad Hedge Biotech and Healthcare Letter

January 4, 2024

Fiat Lux

Featured Trade:

(A TURNAROUND TALE WORTH WATCHING)

(MRNA), (PFE)

Let's take a step back and get a bird's-eye view of what's shaking up in the biotech world.

Remember Moderna (MRNA)? The big shot of the Covid-19 vaccine saga? It’s suddenly back in the spotlight.

After a year that saw its shares nosedive by 45% — landing it in the not-so-coveted spot of one of 2023's worst S&P 500 performers — things are looking up. And, boy, are they looking up!

Moderna's woes weren't just about falling vaccine sales. Oh no, it was more than that. They had to scale back their manufacturing footprint, trimming costs left and right. The company doesn't see itself breaking even until 2026, but who's rushing?

Now, here's where it gets interesting. Moderna's not just sitting around licking its wounds. They've been busy bees, pouring money into their mRNA-based product pipeline. And guess what? It's starting to look like money well spent.

December brought some news that made investors sit up straight. In partnership with Merck (MRK), Moderna's cooking up a cancer treatment that's looking pretty darn promising. And it's not just any partnership.

We're talking about combining forces with Merck's Keytruda, the oncology heavyweight, raking in a cool $20.9 billion in 2022.

Moderna's mRNA-4157, however, is the new kid on the block. It's a custom-tailored cancer vaccine, shaping up to be a real game-changer. The idea? Target each patient's cancer uniquely, making it a one-two punch with treatments like Keytruda.

The latest data? It's the stuff of dreams. High-risk melanoma patients showed a 49% drop in cancer recurrence or death risk and a 62% plunge in distant metastasis or death risk. All this without ramping up severe side effects. The phase 3 trial is already on the drawing board and the scope? It's widening.

And, let's not forget the big picture. In 2020, around 325,000 cases of malignant melanoma were diagnosed.

If Moderna and Merck hit the bullseye with their candidate, they're looking at a vast market to tap into. And if this duo outperforms Keytruda alone for certain conditions, we're talking serious revenue potential.

Needless to say, these developments hint at a future where Moderna's not just about Covid-19 jabs. By 2026, this biotech company is projected to have a lineup of at least five products.

But why this sudden investor love? Part of it is the resurgence of COVID-19 cases and a new variant, JN.1, causing a stir. Adding to these are clearer visibility on vaccine sales and a more structured expense outlook.

On the back of these developments, Moderna's shares leaped 13% to $112.57. That's their best day since December 13, 2022, when they soared 20%. Meanwhile, Pfizer (PFE), their vaccine rival, saw a modest 3.8% bump in roughly the same period.

The broader Wall Street narrative? It's echoing optimism for Moderna. The average price target sits at $126.72, with shares currently hovering around $100. It's a glimpse of potential gains for the vaccine maker.

Clearly, Moderna is no longer just a one-trick pony. More importantly, their shares are currently a bargain, sporting a P/E ratio of just 7 against the market average of 26. This might be riskier than your usual index fund investment, but the growth potential? It's likely being underestimated.

Short-term, Moderna might see more dips as its Covid-19 vaccine windfall wanes. But long-term, their collaboration with Merck, along with other pipeline projects, spells growth.

Come 2025, Moderna's management is betting on a growth rebound, eyeing break-even by 2026. By 2028, they're aiming to add 15 more medicines to their arsenal. And with $7.6 billion in cash and equivalents, they're set to weather the storm without diluting shareholder value.

So, should you buy into Moderna now? It's not a half-bad idea.

If you're the patient type, ready to ride out some short-term turbulence for potential long-term gains, then Moderna's current narrative might just be your kind of investment story.

Mad Hedge Biotech and Healthcare Letter

October 31, 2023

Fiat Lux

Featured Trade:

(A SEA OF POSSIBILITIES)

(PFE), (MRNA), (NVAX)

In the cutthroat world of pharmaceuticals, Pfizer (PFE) seems to be having a bit of a moment. And not the kind you'd want to experience yourself. With shares flirting dangerously close to their 52-week low, investors are left scratching their heads. Is this a rare stock market sale, or is Pfizer showing us warning signs?

Pfizer, a leader in the biotechnology and healthcare world, is currently wrestling with the whims of COVID-19 product sales, resulting in a not-so-insignificant 40.7% shrinkage in share value year to date. The Big Apple-based giant is feeling the heat, with revenues taking a hit and the company's crystal ball now showing a less rosy sales and profit forecast for 2023.

But let's not get lost in the sea of stock market blues. After all, Pfizer is no one-trick pony.

The company has actually been busy beefing up its portfolio with some promising assets. I’m talking Oxbryta for sickle cell disease and Nurtec ODT for those pesky migraine headaches. And let's not forget the potential show-stoppers in their pipeline: the respiratory syncytial virus vaccine Abrysvo and the mid-stage weight loss/diabetes drug Danuglipron. These could very well be the next big things in pharma.

Still, the numbers don't lie. Pfizer's second quarter showed a 54% year-over-year drop in revenue to $12.7 billion, and earnings per share took a 77% hit, plummeting to $0.41. And yes, there's the looming patent cliff, threatening to push 11 of its drugs, including heavy hitters like Eliquis, Ibrance, and Xeljanz, off the financial ledge by 2030.

But before you jump ship, consider this: Pfizer's not just sitting around waiting for the other shoe to drop. Aside from its potential blockbusters, it has a pipeline bursting at the seams with 90 programs, 23 of which are in the final stage of trials. And it’s planning to launch a whopping 19 new products in the next year and a half. Not too shabby, right?

Now, let's talk about FDA approvals. Pfizer's been collecting them like a kid collects baseball cards. Just recently, it added Velsipity for ulcerative colitis and a combination therapy for non-small-cell lung cancer to their collection. It's clear Pfizer is not just resting on its laurels.

In the vaccine arena, Pfizer, in collaboration with BioNTech (BNTX), is making waves with their combination vaccine trials. And they're not just dipping their toes in the water; they're diving in headfirst, ready to take on competitors like Moderna (MRNA) and Novavax (NVAX). It's another vaccine race, and Pfizer is in it to win it — again.

Then there's the $43 billion cherry on top: the acquisition of Seagen (SGEN). This move will inject some serious oncology magic into Pfizer's portfolio and contribute a hefty chunk of change to their revenue stream in the coming years.

Then, there’s the company’s dividend. Pfizer's not stingy when it comes to sharing the wealth. It has upped its quarterly dividend to $0.41 per share, marking 14 years of consecutive increases.

So, what's the verdict? Is Pfizer a sinking ship or a stock market treasure waiting to be discovered? The short-term might be a bit rocky, but Pfizer's long-term game looks strong. With a diversified portfolio, a robust pipeline, and a commitment to innovation, Pfizer is poised to ride out the storm and come out on top.

While the waters might be turbulent now, Pfizer's got the goods to navigate through and come out stronger on the other side. For the savvy investor with an eye on the future and a stomach for a bit of volatility, this pharma leader just might be the hidden gem you've been searching for. So, grab your financial compass and set your sights on Pfizer. It's time to dive in and discover the treasure that awaits.

We’ve just seen our last interest rate rise in the economic cycle. Yes, I know that our central bank took no action at their last meeting in September. The market has just done its work for it.

And the markets are no shrinking violet when it comes to taking bold action. The 50 basis points it took bond yields up over the last two weeks is far more than even the most aggressive, economy-wrecking, stock market-destroying Fed was even considering.

And that doesn’t even include the rate hikes no one can see, the deflationary effects of quantitative tightening, or QT. That is the $1 trillion a year the Fed is sucking out of the economy with its massive bond sales.

It really is a miracle that the US economy is growing as fast as it is. After a warm 2.4% growth rate in Q2, Q3 looks to come in at a blistering 4%-5%. That is definitely NOT what recessions are made of.

Where is all this growth coming from?

Some of the credit goes to the pandemic spending, the free handouts we call got to avoid starvation while Covid ravaged the country. You probably don’t know this, but nothing happens fast in Washington. Government spending is an extremely slow and tedious affair.

By the time that contracts are announced, bids awarded, permits obtained, men hired, and the money spent, years have passed. That means money approved by Congress way back in 2020 is just hitting the economy now.

But that is not the only reason. There is also the long-term structural push that is a constant tailwind for investors:

Hyper-accelerating technology.

Yes, I know, there goes John Thomas spouting off about technology again. But it is a really big deal.

I have noticed that the farther away you get from Silicon Valley, the more clueless money managers are about technology. You can pick up more stock tips waiting in line at a Starbucks in Palo Alto than you can read a year’s worth of research on Wall Street.

What this means is that most large money managers, who are based on the east coast are constantly chasing the train that is leaving the station when it comes to tech.

On the west coast, managers not only know about the new tech, but the tech that comes after that and another tech that comes after that, if they are not already insiders in the current hot deal. This is how artificial intelligence stole a march on almost everyone, until a year ago, unless you were on the west coast already working in the industry. Mad Hedge has been using AI for 11 years.

You may be asking, “What does all of this mean for my pocketbook?” a perfectly valid question. It means that there isn’t going to be a recession, just a recession scare. That technology will bail us out again, even though our old BFF, the Fed, has abandoned us completely.

Which brings me to the current level of interest rates. I have also noticed that the farther away you get from New York and Washington, the less people know about bonds. On the west coast mention the word “bond” and they stare at you cluelessly. Indeed, I spent much of this year explaining the magic of the discount 90-day T-bill, which no one had ever heard of before (What! They pay interest daily?).

In fact, most big technology companies have positive cash balances. Look no further than Apple’s $140 billion cash hoard, which is invested in, you guessed it, 90-day T-bills when it isn’t buying its own stock, and is earning a staggering $7.7 billion a year in interest.

The great commonality in the recent stock market correction is easy to see. Any company that borrows a lot of money saw its stock get slaughtered. Technology stocks held up surprisingly well. That sets up your 2024 portfolio.

Put half your money in the Magnificent Seven stocks of Apple (AAPL), Amazon (AMZN), Meta (META), Microsoft (MSFT), Tesla (TSLA), (NVIDIA), and Salesforce (CRM).

Put your other half into heavy borrowers that benefit from FALLING interest rates, including bonds (TLT), junk bonds (JNK), (HYG), Utilities (XLU), precious metals (GOLD), (WPM), copper (FCX), foreign currencies (FXA), (FXE), (FXY), emerging markets (EEM).

As for me, I never do anything by halves. I’m putting all my money into Tesla. If I want to diversify, I’ll buy NVIDIA. Diversification is only for people who don’t know what is going to happen.

I just thought you’d like to know.

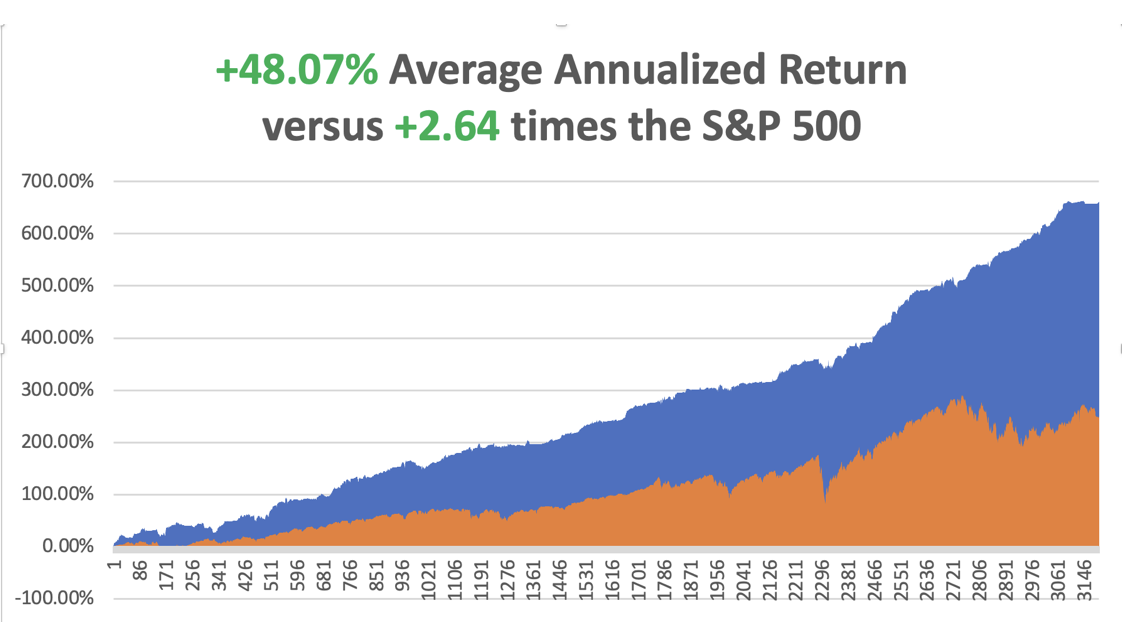

So far in October, we are up +2.96%. My 2023 year-to-date performance is still at an eye-popping +63.76%. The S&P 500 (SPY) is up +12.89% so far in 2023. My trailing one-year return reached +76.46% versus +22.57% for the S&P 500.

That brings my 15-year total return to +660.95%. My average annualized return has fallen back to +48.07%, another new high, some 2.64 times the S&P 500 over the same period.

Some 44 of my 49 trades this year have been profitable.

Chaos Reigns Supreme in Washington, with the firing of the first House speaker in history. Will the next budget agreement take place on November 17, or not until we get a new Congress in January 2025? Markets are discounting the worst-case scenario, with government debt in free fall. Definitely NOT good for stocks, which are reaching for a full 10% correction, half of 2023’s gains.

September Nonfarm Payroll Report Rockets, to 336,000, and August was bumped up another 50,000. The economy remains on fire. The headline Unemployment Rate remains steady at an unbelievable 3.8%. And that’s with the UAW strike sucking workers out of the system. This is supposed to by impossible with 5.5% interest rates. Throw out you economics books for this one!

JOLTS Comes in Hot at 9.61 million job openings in August, 700,000 more than the July report. The record labor shortage continues. Will the Friday Nonfarm Payroll Report deliver the same?

ADP Rises 89,000 in September, down sharply from previous months, showing that private job growth is growing slower than expected. August was revised down. It’s part of the trifecta of jobs data for the new month. The mild recession scenario is back on the table, at least stocks think so.

Weekly Jobless Claims Rise to 207,000, still unspeakably strong for this point in the economic cycle. Continuing claims were unchanged at 1.664%.

Traders Pile on to Strong Dollar, headed for new highs, propelled by rising interest rates. There is a heck of a short setting up for next year.

Yen Soars on suspected Bank of Japan intervention in the foreign exchange markets to defend the 150 line against the US dollar. The currency is down 35% in three years and could be the BUY of the century.

Kaiser Goes on Strike with 75,000 health care workers walking out on the west coast. The issue is money. The company has a long history of labor problems. This seems to be the year of the strike.

Oil (USO)Gets Slammed on Recession Fears, down 5% on the day to $85, in a clear demand destruction move and worsening macroeconomic picture. Europe and China are already in recession. It’s the biggest one-day drop in a year. Is the top in?

Tesla Delivers 435,059 Vehicles in September, down 5% from forecast, but the stock rose anyway. The Cybertruck launch is imminent, where the company has 2 million new orders. Keep buying (TSLA) on Dips. Technology is accelerating.

EVs have Captured an Amazing 8% of the New Car Market. They have been helped by a never-ending price war and generous government subsidies. EV sales are now up a miraculous 48% YOY and are projected to account for a stunning 23% of all California sales in Q3. Tesla is the overwhelming leader with a 52% share in a rapidly growing market, distantly followed by Ford (F) at 7% and Jeep at 5%. However, a slowdown may be at hand, with EV inventories running at 97 days, double that of conventional ICE cars. This could create a rare entry point for what will be the leading industry of this decade, if not the century. Buy more Tesla (TSLA) on bigger dips, if we get them.

Apple Upgrades New iPhone 15 to deal with overheating from third-party gaming. It will shut down some of its background activity, including some of the new AI functions, which were stressing the central processor. Third-party apps were adding to the problem, such as Uber and games from (META). This is really cutting-edge technology.

Moderna (MRNA) Bags a Nobel Prize in Chemistry. Katalin Kariko and Drew Weissman’s work helped pioneer the technology that enabled Moderna and the Pfizer Inc.-BioNTech SE partnership to swiftly develop shots. I got four and they saved my life when I caught Covid. I survived but lost 20 pounds in two weeks. It was worth it.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, October 9, there is no data of note released.

On Tuesday, October 10 at 8:30 AM EST, the Consumer Inflation Expectations is released.

On Wednesday, October 11 at 2:30 PM, the Producer Price Index is published.

On Thursday, October 12 at 8:30 AM, the Weekly Jobless Claims are announced. The Consumer Price Index is also released.

On Friday, October 13 at 1:00 PM the September University of Michigan Consumer Expectations is published. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, one of the many benefits of being married to a British Airways senior stewardess is that you get to visit some pretty obscure parts of the world. In the 1970s, that meant going first class for free with an open bar, and occasionally time in the cockpit jump seat.

To extend our 1977 honeymoon, Kyoko agreed to an extra round trip for BA from Hong Kong to Colombo in Sri Lanka. That left me on my own for a week in the former British crown colony of Ceylon.

I rented an antiquated left-hand drive stick shift Vauxhall and drove around the island nation counterclockwise. I only drove during the day in army convoys to avoid terrorist attacks from the Tamil Tigers. The scenery included endless verdant tea fields, pristine beaches, and wild elephants and monkeys.

My eventual destination was the 1,500-year-old Sigiriya Rock Fort in the middle of the island which stood 600 feet above the surrounding jungle. I was nearly at the top when I thought I found a shortcut. I jumped over a wall and suddenly found myself up to my armpits in fresh bat shit.

That cut my visit short, and I headed for a nearby river to wash off. But the smell stayed with me for weeks.

Before Kyoko took off for Hong Kong in her Vickers Viscount, she asked me if she should bring anything back. I heard that McDonald’s had just opened a stand there, so I asked her to bring back two Big Macs.

She dutifully showed up in the hotel restaurant the following week with the telltale paper bag in hand. I gave them to the waiter and asked him to heat them up for lunch. He returned shortly with the burgers on plates surrounded by some elaborate garnish and colorful vegetables. It was a real work of art.

Suddenly, every hand in the restaurant shot up. They all wanted to order the same thing, even though the nearest stand was 2,494 miles away.

We continued our round-the-world honeymoon to a beach vacation in the Seychelles where we just missed a coup d’état, a safari in Kenya, apartheid South Africa, London, San Francisco, and finally back to Tokyo. It was the honeymoon of a lifetime.

Kyoko passed away in 2002 from breast cancer at the age of 50, well before her time.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Sigiriya Rock Fort

Kyoko

Mad Hedge Biotech and Healthcare Letter

October 5, 2023

Fiat Lux

Featured Trade:

(FROM FRUSTRATING WHACK-A-MOLE ATTEMPTS TO PRECISION STRIKES)

(MRK), (MRNA)

The age-old battle against cancer is getting a revolutionary upgrade, with our own immune systems leading the charge. Imagine if our body's defense system could be tweaked, tuned, and harnessed to target and decimate previously unconquerable tumors specifically. With the global oncology market previously valued at a staggering USD 167.9 billion in 2021 and anticipated to grow to about USD 286.3 billion by 2030, the promise of that dream is becoming closer to reality.

Take a moment and think about drugs called PD-1 and PD-L1 inhibitors. No, they don't play the ancient game of "whack-a-mole" with cancer cells. Instead, they orchestrate a sophisticated game of hide-and-seek, unmasking these rogue cells from the vigilant gaze of our cancer-hunting T-cells. The result? Some of the deadliest cancers, like melanoma and certain lung malignancies, are now seeing remarkable increases in survival rates. These advancements are epitomized by companies like Merck (MRK), whose collaborations with biotech giants like Moderna (MRNA) have pushed the frontier of cancer treatment.

However, the innovation doesn't stop there. Enter the realm of personalized cancer vaccines, the latest generals in this battle. Their might was most notably exhibited when Moderna and Merck recently announced that their investigational personalized mRNA cancer vaccine, when combined with Merck's KEYTRUDA, showed promising results in a Phase 2b trial for melanoma treatment.

By employing genetic sequencing, these vaccines pinpoint unique mutations within an individual's cancer. Much like how the COVID-19 vaccines rev up our immune response, these personalized armaments rally T-cells to specifically target and decimate cancer cells brandishing those identified mutations. In fact, such advancements are so promising that Moderna envisions creating a vaccine tailored for every unique cancer mutation.

In 2022, Joe Biden set an ambitious goal of slicing cancer deaths by half in a quarter-century. With early detection, prevention strategies, and these groundbreaking treatments, this goal could very well be within reach. This is also timely since, forecasting a glimpse into 2023, the U.S. is bracing for approximately 1,958,310 fresh cancer diagnoses. Alongside this daunting figure, the shadows of the ailment further extend with an anticipated 609,820 individuals succumbing to the disease.

Let’s dive a bit deeper into the intricacies of immunotherapy. At its heart, it’s about training our body to do what it's naturally designed to do – recognize and obliterate invaders. But cancer, being the wily enemy it is, has learned to don an invisibility cloak. That's where our new drugs, like PD-1 and PD-L1 inhibitors, along with vaccines, step in - revealing these camouflaged enemies and bolstering our body's defense forces to strike back.

Needless to say, this shift in perspective on cancer is a game-changer. Gone are the days of merely categorizing it by body parts. Now, armed with insights into the unique biology of tumors, coupled with advancements from pharmaceutical behemoths like Merck and biotech pioneers like Moderna, hundreds of different cancers can be identified and targeted.

It's undeniable that collaborations, such as the one between Merck and Moderna, have signaled a paradigm shift in the battle against cancer. Their shared vision of pushing forward in the field of personalized cancer vaccines can potentially redefine how we approach oncology in the coming years.

Yet, as with all wars, there are casualties. The treatments, while promising, aren't without risks. Unbridling the immune system, for instance, can sometimes lead to unforeseen reactions, some of which can be fatal. Nonetheless, the consensus is clear: these treatments are generally safer and potentially more effective than the traditional chemotherapy approach.

But what does this mean for the average Joe or Jane grappling with a cancer diagnosis? Simply put, a shimmering beacon of hope. While some cancers remain resilient to these advances, others are showing remarkable progress. However, staying updated with the latest treatments is crucial. This might sometimes involve enrolling in trials or seeking genetic sequencing of one's cancer to unlock potential targeted therapies.

The bottom line, as put succinctly by oncologists working on these treatments: “We’re not in the 1990s anymore.” With key players like Merck and Moderna at the forefront of these innovations, we might just be on the brink of turning the tide in this relentless war. Make sure you don’t get left behind. Buy the dip.

Mad Hedge Biotech and Healthcare Letter

September 19, 2023

Fiat Lux

Featured Trade:

(A SHOT AT HOPE)

(MRNA), (IMTX), (MRK), (PFE), (BMY), (GH), (ILMN), (NVS), (RHHBY), (BGNE), (AZN)

In a quaint Boston lab, as the first rays of dawn broke, a team of scientists, led by Moderna (MRNA), embarked on a mission. Their goal? To craft a solution to one of humanity's most persistent adversaries: cancer.

The grim reality remains that cancer is a leading cause of death in the United States. The statistics are daunting, with over 1.9 million new cases anticipated in 2023 and a projected death toll exceeding 600,000. The financial implications mirror this gravity, with costs expected to soar from $156 billion in 2018 to a staggering $246 billion by 2030.

As the world watched with bated breath, Moderna, already a household name for its COVID-19 vaccine, was silently weaving a narrative that could redefine the future of oncology.

Needless to say, the biotechnology sector, a realm of ceaseless innovation, has been abuzz with Moderna's latest venture. Earlier this month, the biotech announced its agreement with the German drug developer Immatics (IMTX) to develop cancer vaccines and therapies. As part of the deal, Moderna will pay $120 million in cash and will also make additional milestone payments.

This collaboration is not just about the financials; it's a beacon of hope for millions.

The partnership is set to merge Moderna's mRNA technology with Immatics’s T-cell receptor platform, focusing on various therapeutic modalities such as bispecifics, cell therapies, and cancer vaccines. Their combined research aims to leverage mRNA technology for in vivo expression of Immatics's half-life extended TCR bispecifics targeting cancer-specific HLA-presented peptides, among other innovative approaches.

With an upfront investment of $120 million, Moderna has made it clear: they're in it to win it. And the stakes? Potentially life-changing cancer vaccines.

However, this isn’t Moderna’s first foray into the realm of cancer treatments.

Building on the momentum of the technology of its highly potent COVID-19 shots, Moderna announced a partnership with Merck (MRK) earlier this year, combining their efforts to come up with treatments that can drastically reduce the spread of skin cancer. By leveraging Merck's Keytruda with its own innovative vaccine, Moderna has showcased the potential of such collaborations in advancing cancer treatment.

After all, the global community oncology services market is not just growing; it's clearly thriving.

From $47.95 billion in 2022 to a projected $53.79 billion in 2023, the numbers speak for themselves. By 2027, this figure is set to skyrocket to $81.33 billion. Such exponential growth underscores the immense potential and critical importance of advancements in oncology.

Yet, as expected, Moderna isn't the only player on the field.

Giants like Novartis (NVS) and Roche (RHHBY) have also thrown their hats in the ring, collaborating with known international cancer organizations to democratize access to cancer medicines. Among the myriad of promising stocks these days, though, Moderna, China’s BeiGene, Ltd. (BGNE), and the UK’s AstraZeneca PLC (AZN) shine the brightest.

Other notable contributors to the fight against cancer include Bristol Myers Squibb (BMY), Guardant Health (GH), Illumina (ILMN), and Pfizer (PFE). Their diverse portfolios and relentless pursuit of innovation are set to shape the future of oncology.

But as the curtains draw on this narrative, the spotlight remains firmly on Moderna. Their success with the COVID-19 vaccine has already etched their name in the annals of medical history. With their sights now set on cancer vaccines, the world waits with eager anticipation.

In the grand tapestry of medical advancements, Moderna's endeavors in the cancer vaccine domain promise to be a golden thread. Their journey, fraught with challenges and uncertainties, is proof of human resilience and ingenuity. As investors, we're not left standing on the sidelines watching history unfold; we're granted an active role in it.

The potential of Moderna's innovations in oncology beckons a promising horizon. For those looking to make a mark in the annals of medical investments, this biotech offers a gateway to the future of oncology. Act now, and be part of this groundbreaking narrative.

Mad Hedge Biotech and Healthcare Letter

May 30, 2023

Fiat Lux

Featured Trade:

(A MONSTER STOCK ON THE RISE)

(VRTX), (MRNA), (ABBV), (CRSP)