Imagine you're the CEO of a major pharmaceutical company. You've got blockbuster drugs that are raking in billions, a cushy corner office, and a corporate jet at your disposal. Life is good.

But then, you look at the calendar and realize that your patents are about to expire. Suddenly, that jet feels more like a crop duster, and your corner office starts to feel like a broom closet.

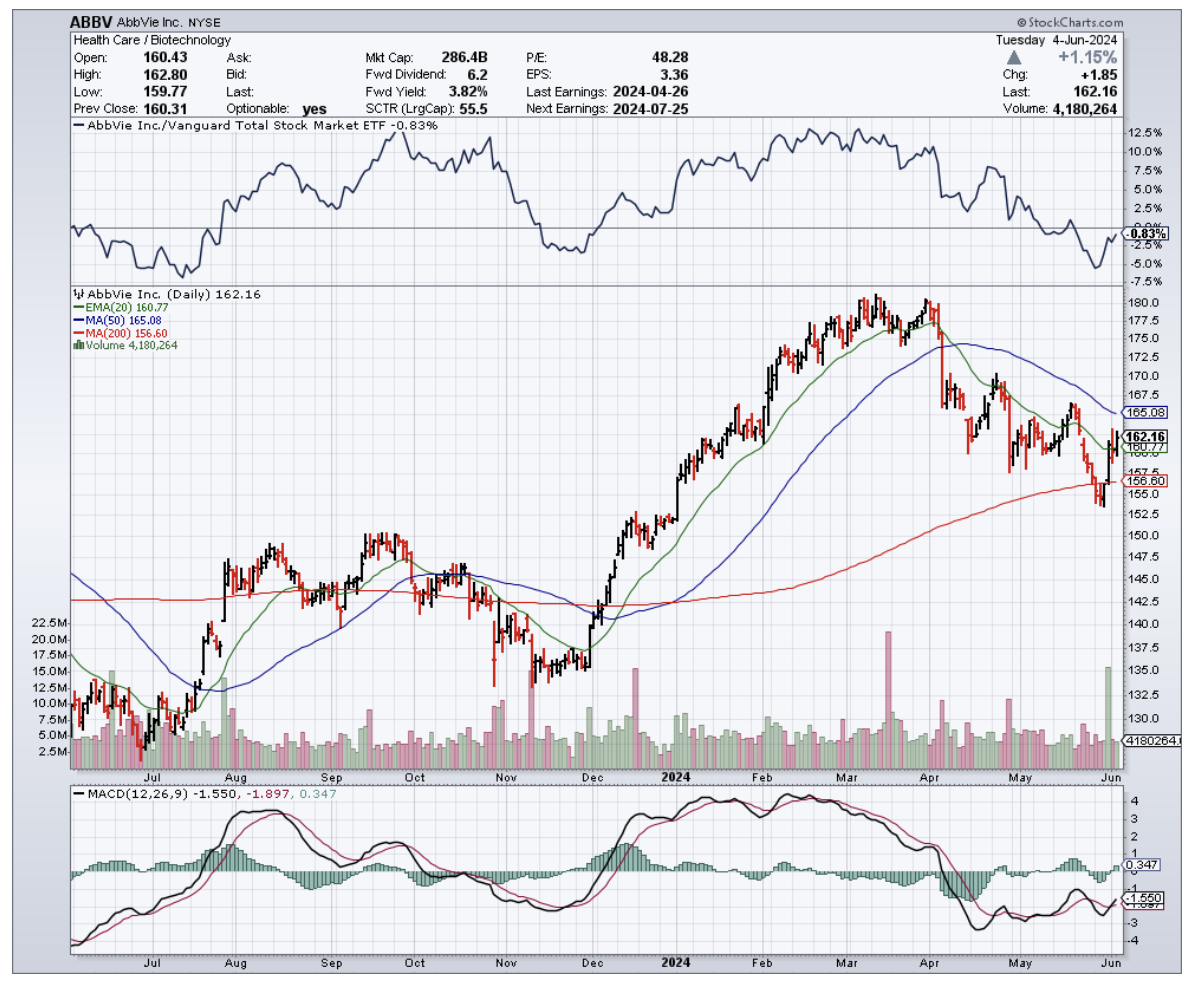

That's the reality facing Big Pharma right now. These pharma big shots are sweating bullets over losing their golden geese like AbbVie's (ABBV) Humira and Merck's (MRK) Keytruda.

That’s roughly $300 billion in products about to get kicked to the curb.

But these guys didn't get to the top by sitting on their hands. They've got a war chest of $1 trillion, and they're not afraid to use it.

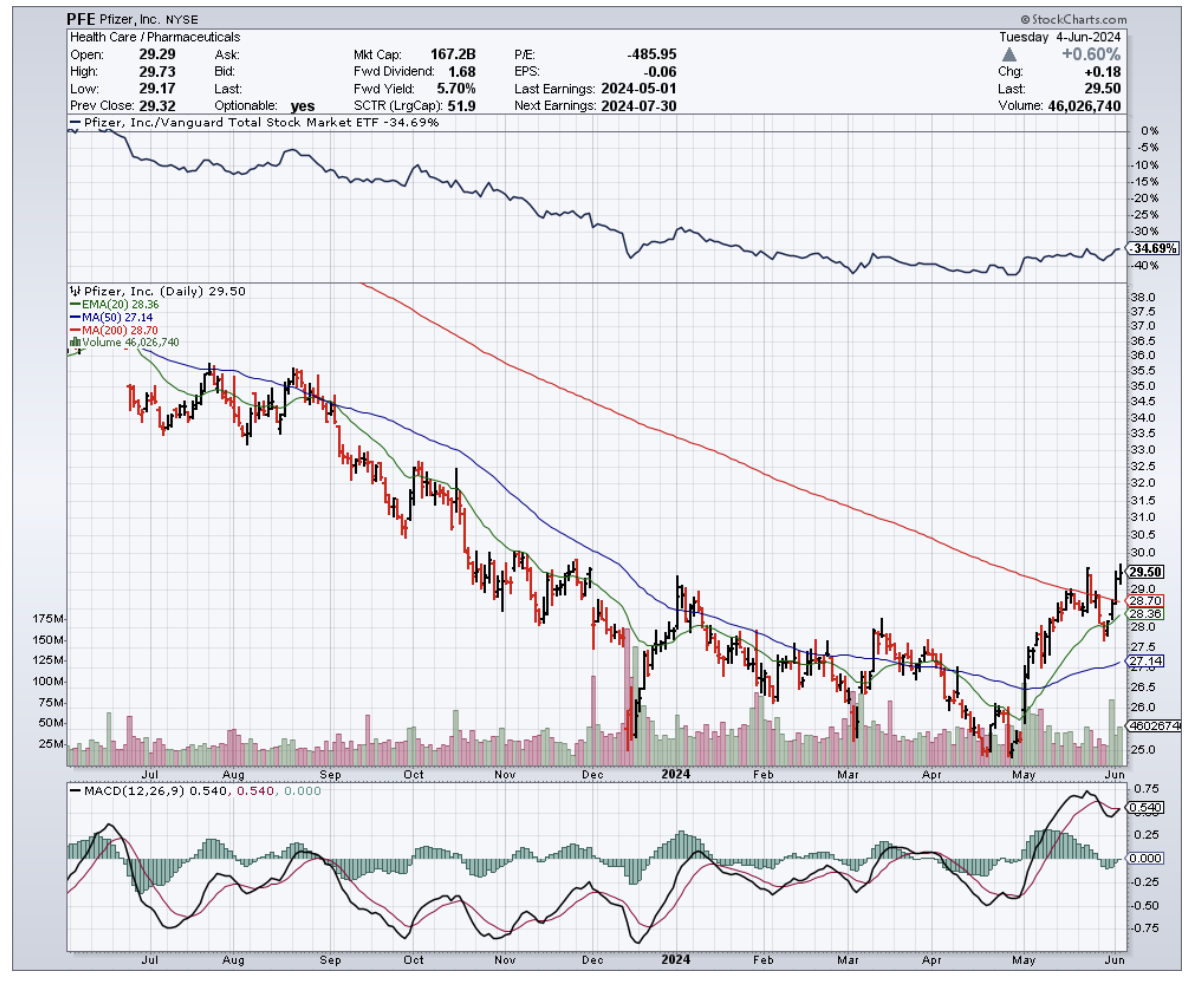

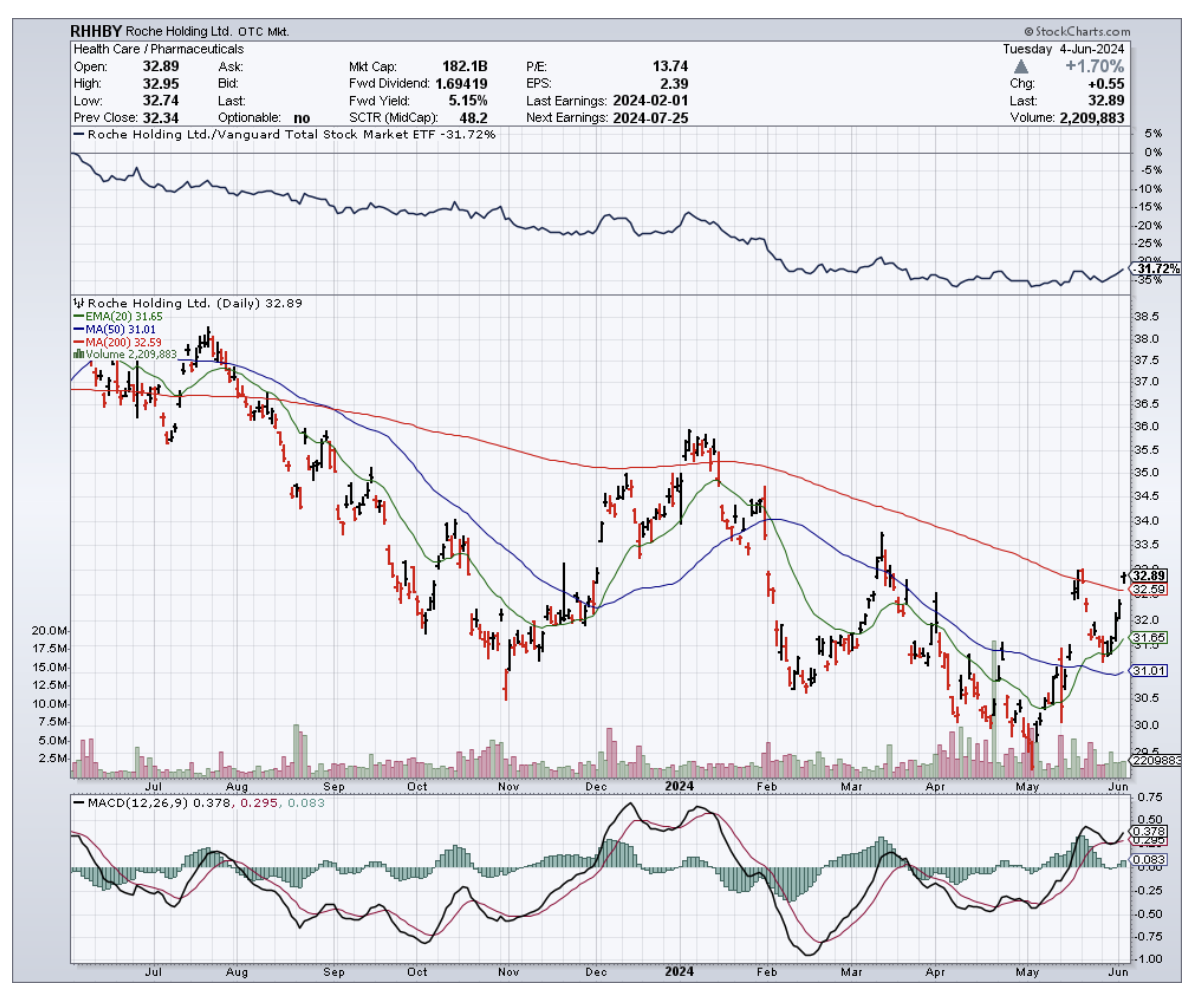

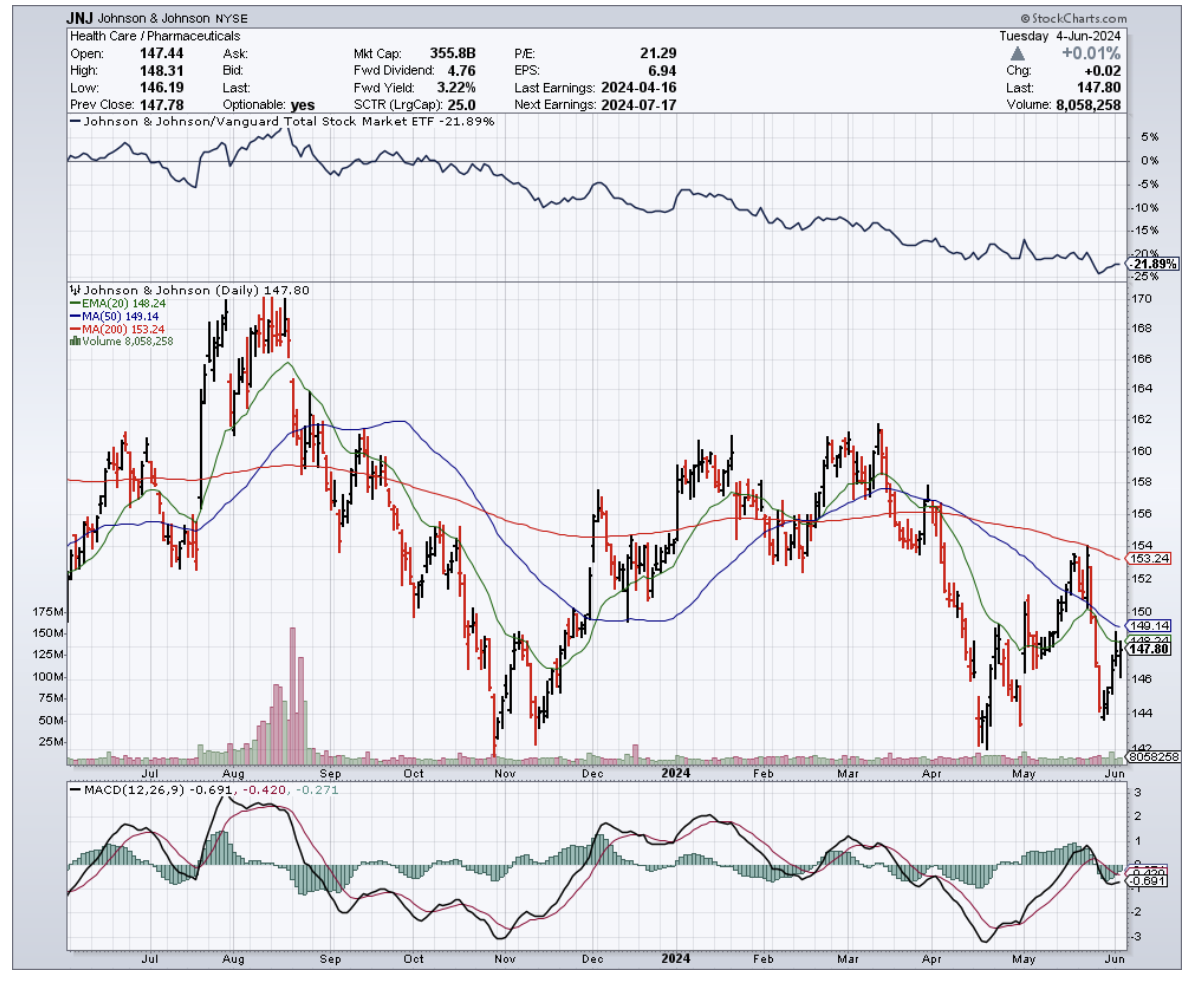

Major pharmaceutical giants like Pfizer (PFE), Roche (RHHBY), Johnson & Johnson (JNJ), AstraZeneca (AZN), and GlaxoSmithKline (GSK) are about to go on the mother of all shopping sprees.

Why the rush? Because they're staring down the barrel of a patent cliff that's going to make the Grand Canyon look like a pothole.

We're talking $198 billion worth of branded drugs going off the patent cliff between 2021 and 2025. That's a gut-wrenching 56% jump from the last five years.

But don't think for a second that they're just going to sit back and watch their profits go up in smoke. No sir, they're on the hunt for the next big thing, and they've got their sights set on some juicy targets – and biotech is at the top of their list.

Leading the biotech charge are mRNA pioneers Moderna (MRNA) and BioNTech (BNTX), each sitting on a gold mine of potential blockbusters taking on everything from flu to cancer vaccines.

Underdogs like CRISPR (CRSP) biotech stars Intellia (NTLA) and Beam Therapeutics (BEAM) are also squarely in Big Pharma's acquisition crosshairs for their cutting-edge work in genetic disease treatments.

But beyond the headliners, don't overlook the sleeper hits that could catalyze the next big boom.

Oncology, in particular, is a prime hunting ground, accounting for 37% of pharma M&A deal value in 2023 as the $392 billion global cancer drug market continues to boom.

Companies like Turning Point Therapeutics (TPTX) and Zentalis Pharmaceuticals (ZNTL), with their promising targeted therapies for various solid tumors, are particularly attractive prospects.

Mirati Therapeutics (MRTX), focused on KRAS inhibitors, and Blueprint Medicines (BPMC), specializing in precision therapies, have also caught the eye of big pharma with their innovative approaches.

Additionally, companies with late-stage assets like MacroGenics (MGNX), Mereo BioPharma (MREO), and Tyra Biosciences (TYRA) could offer promising near-term revenue opportunities for acquiring companies looking to bolster their oncology portfolios.

Close behind are rare disease treatments, snagging 16% of new drug approvals and 9 of the top 100 deals last year in this $262 billion market ripe for more growth.

This lucrative sector has captivated pharma giants, who see potential in companies like Sarepta Therapeutics (SRPT) and Vertex Pharmaceuticals (VRTX), leaders in rare disease therapies with strong financial performance and consistent growth.

Aside from these, smaller biotechs like Amicus Therapeutics (FOLD) and Ultragenyx Pharmaceutical (RARE), focused on developing innovative therapies for a range of rare diseases, are attracting attention for their potential to address unmet medical needs and deliver substantial returns on investment.

But the real wild card everyone wants a piece of is cell and gene therapies. This medical Wild West is projected to explode to $66.8 billion by 2030, with the FDA already greenlighting 6 cutting-edge therapies like next-gen CAR-T treatments from Caribou Biosciences (CRBU) in 2023 alone.

Notably, the buying frenzy is very much already underway. In fact, 2023 saw the biggest biotech M&A spree in a decade, with a staggering $122.2 billion changing hands as the FDA approved 50% more new therapies.

Pharma mega-mergers also hit $135.5 billion as firms raced to reload pipelines.

Interestingly, these deals are only the tip of the iceberg. As Wall Street predicts, with record-smashing deals, sky-high demand, and new approvals surging, "biotech's got plenty of reasons to be cautiously optimistic."

Especially if interest rates finally cooperate, throwing gasoline on the M&A bonfire and making biotech the belle of the ball as soon as late 2024.

So keep your eyes peeled and your powder dry. I suggest you add these innovative biotech names to your watchlist, and you might just discover the next blockbuster drug or breakthrough therapy that could reshape medicine – and deliver explosive returns in the process.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-11 12:00:012024-06-11 12:03:04The Capital Cure

The ideal stocks are those you can just buy and hold for a long time. A healthcare and biotechnology company that perfectly fits the bill is Amgen (AMGN).

Amgen wasn’t an active participant in the COVID-19 race.

Instead, the biotechnology giant chose to stick with its circle of competence and focused on delivering remarkable results to its shareholders through boosting its revenue and increasing dividends.

Recently, this hyper-focus has paid off.

Amgen received FDA approval to market a drug that targets cancer cells in an area that researchers have been attempting to hit for decades.

The new treatment, Lumakras, will be the first of its kind to target a tumor growth process commonly known as KRAS for non-small cell lung cancer (NSCLC).

To understand the extent of Amgen’s breakthrough, scientists and researchers have been working on developing a KRAS blocker for over 40 years.

Prior to this, KRAS had been known as an “undruggable” target.

Basically, Amgen came up with a drug that can target the notorious and illusive cancer-causing protein—something that was previously considered the “Achilles heel” of lung cancer tumors.

More impressively, Lumakras was approved three months ahead of its schedule.

Based on the results of its Phase 2 trials, Lumakras can stall the progress of lung cancer in roughly 81% of the patients for a median time of 10 months.

In the Phase 3 trials, Amgen is looking into testing the drug in combination with other medications to hit the tumors that developed resistance to the pill.

A key factor in Lumakras’ launch is determining the types of patients who’d benefit most from the drug.

So far, Amgen has been collaborating with diagnostic partners, particularly Qiagen (QGEN) and Guardant Health (GH), for biomarker testing.

In terms of pricing, Amgen estimates monthly spending on Lumakras to be $17,900.

In the United States, roughly 30,000 patients of KRAS-mutated lung cancers are reported annually.

That puts Lumakras sales to at least $100 million for 2021 alone.

By 2025, the drug is expected to rake in roughly $1 billion annually, with sales growing to $1.51 billion in 2026.

These are actually conservative estimates that assume only a 50% success rate from Lumakras in the next few years.

Given the provisional and accelerated approval the drug has already received from the FDA though, it is safe to say that it can achieve at least 75% success rate, which means it can generate higher revenue.

The KRAS target is not limited to lung cancer. It also appears in other solid tumors, which Amgen continues to test Lumakras in a dozen other types, including colorectal cancer.

Depending on expansion plans, Lumakras sales can reach $3.2 billion by 2030.

Again, this expansion is a conservative estimate.

If the expansion for Amgen’s drug would be anything like AstraZeneca’s (AZN) blockbuster Tagrisso, which eventually became a recommended first-line therapy option for NSCLC, then Lumakras sales can peak at $4 to $5 billion.

Considering the potential of this market, it no longer comes as a surprise that competitors are hot on Amgen’s heels just days after Lumakras’ approval was announced.

The closest rival so far is Mirati Therapeutics (MRTX), which also has KRAS-inhibitor candidates in Phase 1 and Phase 2 trials.

Prior to that, Eli Lilly (LLY) and Johnson & Johnson (JNJ) tried their hands at KRAS mutation but failed.

Aside from Lumakras, Amgen has another blockbuster candidate in store for its shareholders: asthma drug Tezepelumab.

Developed in collaboration with AstraZeneca, this drug is already in the second late-stage pipeline and has been showing promising results so far.

Globally, there are about 2.5 million patients with severe asthma, with 1 million suffering from eosinophilic asthma in the United States. Amgen is hoping to target the latter population.

If Tezepelumab gets approved, it would be in direct competition against Sanofi (SNY) and Regeneron’s (REGN) asthma drug Dupixent. Peak sales for this asthma drug is estimated at roughly $3.5 billion.

Over the past 12 months, Amgen’s stock performance has been rangebound.

Although this is obviously frustrating for growth-oriented shareholders, I think the short-term volatility of the stock may present good opportunities for value-conscious investors.

That is, I view the drop in Amgen’s share price as another favorable buying opportunity.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-06-03 15:00:582021-06-13 14:01:46Another Buy-the-Dip Opportunity Dropped in our Lap

Multiple times every year, leading oncology researchers gather to share and discuss the latest developments in the field. During these events, biotech companies actively seek ways to snatch top billing, hoping to amp up their value not only within the industry but also to the public.

Needless to say, company stock prices tend to fluctuate dramatically based on the data and whether or not the companies lived up to the hype of their studies. Hence, these events have turned into must-attend conferences among the healthcare industry leaders and even institutional investors.

For everyday investors though, it’s too impractical to even consider the possibility of attending these grand shindigs. This is why we’re sharing with you a list of companies that are currently making strides or are anticipated to dominate the cancer research and treatment market in 2019 and in the years to come.

Bristol-Myers Squibb (BMY)

As always, no other field has been watched more intensely than the lung cancer market -- an area considered as the most lucrative in the immuno-oncology circle. In the recently concluded European Society for Medical Oncology Congress in Barcelona, all eyes were on the up-and-coming Opdivo/Yervoy combo of Bristol-Myers Squibb (BMY).

In the recent data it presented, Bristol disclosed that the combination of its cancer drugs Opdivo and Yervoy provided promising results to melanoma patients. According to their study, over 50% of melanoma patients survived after five years which is a huge leap from the 5% survival rate recorded over the same period prior to the introduction of immunotherapies.

With the company’s recent moves to beef up its cancer portfolio, the Opdivo/Yervoy combo is anticipated to turn into a strong competitor of Roche Holding Ltd. Genussscheine’s (ROG) Tecentriq. This combo also reinvigorates the ongoing rivalry between Bristol and Merck & Co. (MRK), with Opdivo/Yervoy aiming to dethrone the latter’s major moneymaker Keytruda.

However, this isn’t exactly the first time Bristol showed interest in dominating the oncology market. Wielding the power of its $81.05 billion market value, Bristol has signified its aggressive stance in pushing for the expansion of its cancer department.

The most highly publicized news from this front came in January this year courtesy of its announcement involving a $74 billion merger with Celgene Corporation (CELG). Now, it appears that we’re seeing the first of Bristol’s efforts to bolster its cancer drug lineup.

Although Bristol has been underperforming compared to its competitors for the majority of 2019, the stock has actually surpassed its rivals by roughly 5% in September. Following its 52-week low in July, the company has performed steadily higher to currently trading 6.5% below its 2019 high.

Hence, traders should be vigilant as a dip to a short-term trendline in the next weeks could offer a suitable entry point to eventually take advantage of the upside momentum.

Amgen (AMGN)

Another oncology frontrunner is Amgen (AMGN). The biotech giant recently presented its data on experimental treatments AMG 510 and AMG 160, which target some forms of colorectal cancer. So far, AMG 510 has provided higher response rates at 3% for patients across all levels of dosage.

These drugs form part of the rising trend of precision medicines, which zero in on particular gene mutations. This method is anticipated to be able to ward off cancer cells regardless of the organ where the disease originated.

In September, Amgen shared that the drug managed to shrink tumors by almost 50% during the trial period for advanced non-small lung cancer patients. Meanwhile, the drug’s disease control rate was recorded at 92%, with patients capable of tolerating AMG 510 without any dose-limiting toxicities.

These results prompted the FDA to send AMG 510 for “fast track” review. Aside from their own study, Amgen is also looking at a possible combination with Merck’s Keytruda in an effort to bolster its foothold in the lung cancer front.

If Amgen succeeds in the application of AMG 510 to colorectal cancer patients, the drug will be the first-ever approved treatment to target a mutated form of a gene commonly referred to as KRAS. This particular mutation called KRASG12C is prevalent in approximately 13% of non-small cell lung cancers, 3% to 5% of colorectal cancers, and almost 2% of solid tumor cancers.

In terms of revenue, the success of AMG 510 could lead to annual sales of $3 billion in the United States alone and $6.4 billion internationally. Aside from Amgen, Mirati Therapeutics Inc. (MRTX) has been actively pursuing treatments that aim to treat KRAS mutations as well.

Incyte Corporation (INCY)

At first blush, Incyte (INCY) is regarded as simply another young company striving to make a name for itself in the massive biotech market. Despite the success of bone marrow disorder drug Jakafi, a lot of investors still believe that the company only managed to stumble its way to growth. In fact, even those who actually started to invest in this biopharma firm still somehow see it as a company with an extremely limited potential.

Unfortunately for these investors, they’re missing out on a crucial detail. Although Incyte’s trajectory isn’t exactly moving at a blistering pace, the steady revenue growth of the company in 2019 is a strong indicator of meaningful profits in the succeeding years.

This growth would eventually land the company in the watchlist of every biotech investor, with the company stock already gaining 18% this year alone to boost its $16.10 billion market value.

One of the most exciting developments from Incyte is its bile duct cancer research which led to a potential oncology blockbuster drug Pemigatinib. So far, 36% of its test patients saw their tumors shrink with a preliminary median overall survival of 21.1 months.

Despite the promising results though, the company cautions on the modesty of its projected revenue as Pemigatinib specifically targets cholangiocarcinoma, which is a rare type of bile duct cancer. Incyte plans to submit the drug for review to the FDA before the year ends.

For now, Incyte is focused on the commercialization and development of its existing moneymakers. Aside from Jakafi, the company is also making waves in the rheumatoid arthritis market with Olumiant. Its myeloid leukemia treatment Iclusig is another potential golden goose on the rise as well.

So far, Incyte’s share price has been trading at approximately $15 range since April. The past two months showed a pullback though, with the stock finding key support from the lower trendline of the trading range at $72. For investors who intend to open a long position within these levels, you should set your take-profit order somewhere near $88. However, simply cut your losses if Incyte stock fails to hold $72 support.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-10-22 08:00:042019-10-22 07:55:20Special Cancer Issue - Part 1

I recently heard that some of my hedge fund friends were loading up on Amgen (AMGN) and now I know why. It’s a company I know well because my UCLA biochemistry professor was its first chairman.

Amgen has accomplished a major medical breakthrough. The company has revealed that its experimental drug, AMG 510, exhibited the ability to significantly shrink the size of tumors by 50%. The results were obtained from early-stage trials performed on advanced lung cancer patients.

In a nutshell, AMG 510 could become the first-ever approved treatment that can target a mutated gene called KRAS which is one of the most common mutations involved in non-small cell lung cancer (NSCLC). The American Cancer Society identified NSCLC as the leading cause of cancer death, accounting for a stunning 85% of lung cancers.

For decades, researchers have been searching for ways to address KRAS mutations, with the sought-after solution dubbed as the "the great white whale of drug discovery." With the first proof-of-concept presented a mere six years ago, the rapid development of Amgen’s new drug has impressed researchers in the field.

Simply put, this drug will be a game changer for particular types of cancer. Subsequently, its success would mean massive profits for Amgen shareholders.

The announcement of AMG 510’s promising results saw a jump in Amgen shares of 6.1% delivering a new two-year high. While this product remains in its initial phase, the fact that this cancer drug addresses a vital unmet need in oncology makes it a prime candidate in becoming the next blockbuster drug for Amgen.

Aside from lung cancer, this drug is also aimed at providing treatment for colorectal cancer and nearly uncurable pancreatic cancer (of which Steve Jobs died). To date, AMG 510 sales are estimated to initially reach more than $1 billion a year and peak at $2 billion.

With the extremely massive market for this particular drug, it comes as no surprise that Amgen is not alone in the race.

So far, two more biopharma companies are looking to develop similar medications: GlaxoSmithKline Plc (GSK) and Mirati Therapeutics (MRTX). While the former has yet to reveal the covalent inhibitor drug it’s currently developing, reports indicate that Mirati’s work involves a drug called MRTX849. Aside from these, no other information has been released by the two companies.

While these are encouraging results vis-à-vis its oncology department, how is Amgen doing so far this year with the rest of its business?

Based on its earnings report in the first quarter of 2019, Amgen recorded $5.6 billion in total revenues. This matches the amount the company reported during the same quarter in 2018. Despite the promising projects in its pipeline, Amgen’s product sales saw a 1% dip globally.

However, its new products showed double-digit increases in the first quarter. Osteoporosis and hypercalcemia drug Prolia reported a 20% increase while cardiovascular medication Repatha also showed a 15% revenue jump during the first quarter. Even the revenues for relapsed multiple myeloma treatment Kyprolis showed a 10% rise in this period.

As for its earnings per share (EPS), Amgen is coming in at $12.53. This indicates an EPS growth of 14.8% this year, which could lead to a projected 5.25% EPS growth for 2020.

Meanwhile, Amgen’s positive outlook particularly with AMG 510 as an additional blockbuster drug in its portfolio prompted the company to adjust its earnings expectations for this year. In terms of its expected revenue, Amgen raised it from $21.8 billion to $22.9 billion range to $22 billion to $22.9 billion.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/06/amgn510.png370439Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-06-12 05:02:012019-07-09 03:49:32Amgen’s Big Lung Cancer Breakthrough

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.