Global Market Comments

December 14, 2018

Fiat Lux

Featured Trade:

(DECEMBER 12 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (MU), (PYPL), (SPOT), (FXE), (FXY), (XLF), (MSFT), (AMZN), (TSLA), (XOM),

(SIGN UP NOW FOR TEXT MESSAGING OF TRADE ALERTS)

Global Market Comments

December 14, 2018

Fiat Lux

Featured Trade:

(DECEMBER 12 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (MU), (PYPL), (SPOT), (FXE), (FXY), (XLF), (MSFT), (AMZN), (TSLA), (XOM),

(SIGN UP NOW FOR TEXT MESSAGING OF TRADE ALERTS)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader December 12 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader

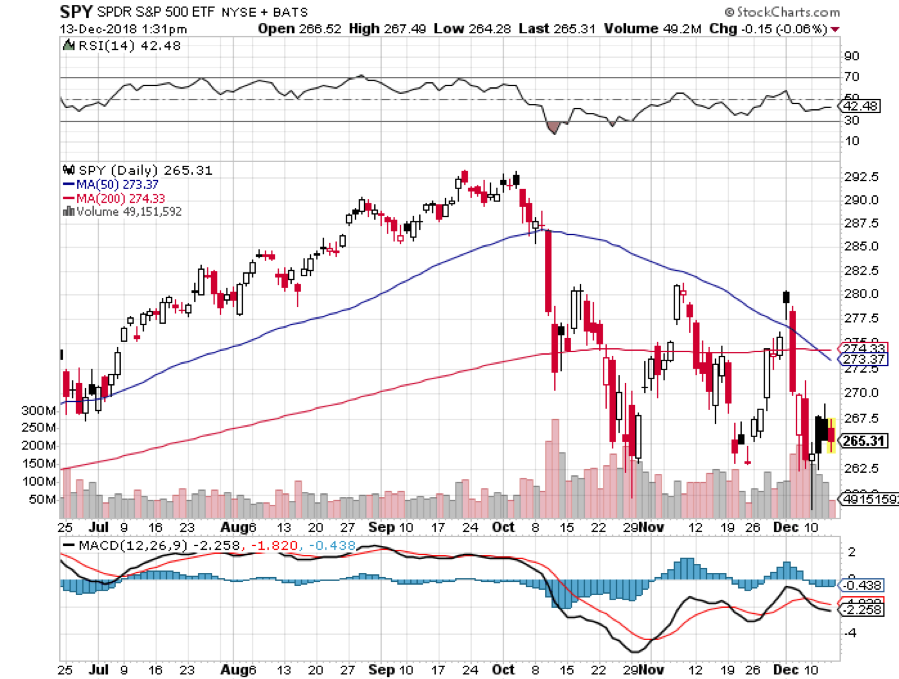

Q: Is the bottom in on the S&P 500 (SPX) or are we going to go on another retest?

A: It’s stuck right in the 2600-2800 range, and I think that’s probably where we bounce off of 2600 again. The question is whether or not we can clear the top of the range at 2800. If we can’t, I would fully expect a retest of this bottom in which case I could see it going down to 2500.

Q: You say you’ll go 100% cash by Dec 21st but also stated that the S&P 500 will go up 5% by the year's end. Should we stay in until we get the up 5% move?

A: Yes, all of our options positions expire by the 21st but if you’re just long in stocks, I would stay long, probably through the end of the year.

Q: Will the Chinese-U.S. dispute ruin the Tech industry?

A: No, I think the Trump Administration will have to do some kind of deal and call it a victory, otherwise the trade war will pull the U.S. into recession. If we go into the next presidential election with another recession—well, no one has ever survived that. Even with the China-U.S. dispute, the U.S. is still dominant in the Tech industry and will continue to do so for decades to come.

Q: China has managed to duplicate Micron Technology’s (MU) biggest selling chip, undercutting prices—thoughts?

A: True, Micron is the lowest value added of the major chip producers, therefore their stock has gotten hit the worst of any of the chip stocks down by about 46%, but I know Micron very well and they have a whole range of chips they’re currently upgrading, moving themselves up the value change to compete with this. So, that makes it a great company to own for the long term.

Q: I’m up 90% on my PayPal (PYPL) position—should I take a profit?

A: Yes! Absolutely! How many 90% profits have you had lately? You are hereby excused from this webinar to go execute this trade. And well-done Dr. Denis! And thank you for the offer of a free colonoscopy.

Q: What can you say about Spotify (SPOT)?

A: No, thank you—there’s lots of competition in the music streaming business. We are avoiding the entire space. The added value is not great, and many of these companies will have a short life. And with China’s Tencent growing like crazy, life for Spotify is about to become dull, mean, and brutish.

Q: What’s your view on currencies?

A: So you’re looking to make another fortune? Yes, I think the Euro (FXE) and the Yen (FXY) really are looking hard to rally, and the trigger could be dovish language in the next Fed meeting. Once the Fed slows its rate of interest rates rises, the currencies should take off like a scalded chimp.

Q: Will the banks (XLF) rally in the next 6 months for a better sell?

A: Many people are waiting for a rally in the banks so they can unload them and haven’t gotten it—they’re back to pre-election price levels. The issue here is structural, and you don’t get recoveries from major structural changes in an industry. It’s significant that this is the first bull market that had no net new employment in the banks whatsoever; the business is fading away. They are the new buggy whip makers. These gigantic national branch networks will all be gone in ten years because the banks can’t afford them.

Q: Would you enter the Microsoft (MSFT) trade today?

A: I actually think I would; Microsoft only pulled back 10% when everything else was dropping 30%, 40%, or 50%. That shows you how many people are trying to get into this name so if you could take a little short-term pain (like 5%), the stock outright is probably a screaming buy here. I think it’ll go to $200 one day, so here at $110-$111 it looks like a pretty good deal. The story here is that Microsoft is rapidly taking market share from Amazon (AMZN) in the cloud business and that’s going to continue.

Q: When will you be updating your long-term model portfolio?

A: I usually do it at the end of the year, and rarely make any big changes. I’ll still be selling short bonds and still like Tesla (TSLA) and Exxon (XOM).

Q: I just joined your service. What is the best way to get started?

A: I’ll give you the same advice that I gave every starting trader at Morgan Stanley (MS). Start trading on paper only. When you are making money reliably on paper, move up to using real money, but only with one contract per position. When that is successful, slowly increase your size to 2, 3, 5, 10, and 20 contracts. Pretty soon, you will be swinging around 1,000 contracts a lot like I do. The further you move down the learning curve the greater you can increase your size and your risk. If you never get past the paper stage at least it’s not costing you any money.

I hope this helps.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

September 24, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or IT’S FED WEEK),

(SPY), (XLI), (XLV), (XLP), (XLY), (HD), (LOW), (GS), (MS), (TLT),

(UUP), (FXE), (FCX), (EEM), (VIX), (VXX), (UPS), (TGT)

(TEN TIPS FOR SURVIVING A DAY OFF WITH ME)

20/20 hindsight is a wonderful thing, especially when all of your predictions come true.

In February, I announced that markets would trade in broad ranges until the run-up to the midterm elections. That is what has happened to a tee, with the decisive upside breakout taking place last week. From here on. You’re trying to buy dips for a year-end run-up to higher highs.

For many months I was the sole voice in the darkness crying out that the bull market was still alive, it was just resting. Now quality laggards are taking the lead, such as in Industrials (XLI), Health Care (XLV), Consumer Staples (XLP), and Consumer Discretionary (XLY).

Home Depot (HD), which I recommended a month ago has taken off for the races, as has competitor Lowes (LOW), thanks to a twin hurricane boost. Even the long dead banks have recently showed a pulse (MS), (GS).

Technology stocks are taking a long-needed rest after a torrid two-and-a-half-year run. But they’ll be back. They always come back.

It’s not only stocks that have broken out of ranges, so has the bond market (TLT), the U.S. dollar (UUP), and foreign currencies (FXE). Will commodity companies like Freeport-McMoRan (FCX) and emerging markets (EEM) be the last to pick themselves off the mat, or do they really need to see the end of the trade wars first?

Markets are essentially acting like the trade war is over and we won. Why would traders believe this? That’s what a Volatility Index touching $11 tells you and is why I have been telling them to avoid buying it all week. Because the president told them so.

Another not insignificant positive is that multinationals have been slow to repatriate foreign funds, so there is a lot more still abroad to buy back their own stocks.

Weekly jobless claims hit another half century low at 201,000. Major U.S. companies such as UPS (UPS) and Target (TGT) are planning record levels of Christmas hiring. By the way, this is what economic peaks look like.

The Senate passes a mini spending bill that keeps the government from shutting down until December 7. The budget deficit keeps on soaring, but apparently, I am the only one who cares. Live through a debt crisis like we had during the early 1980s and you’d feel the same way.

The data for housing continues to be terrible, and we saw our first increase in inventories in three years.

Finally, with people camping out overnight and lines around the block, Apple’s CEO Tim Cook opens the doors to the Palo Alto, CA, store at 9:00 AM sharp on Friday to three new phones. But did the stock peak at $230, as it has in past release cycles?

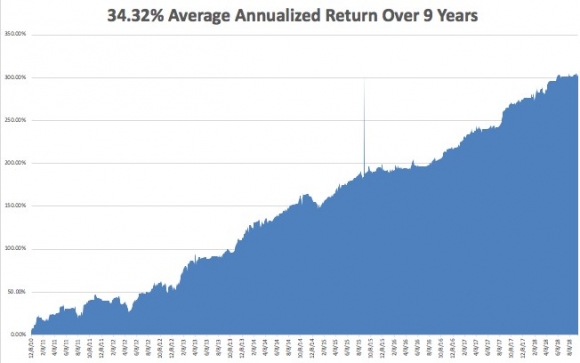

Last week, the performance of the Mad Hedge Fund Trader Alert Service forged a new all-time high and then gave it up on one bad trade. September is now unchanged at -0.32%. My 2018 year-to-date performance has retreated to 26.69%, and my trailing one-year return stands at 38.23%.

My nine-year return appreciated to 303.16%. The average annualized Return stands at 34.32%. I hope you all feel like you’re getting your money’s worth.

This coming week is all about the Fed, plus a plethora of housing data.

On Monday, September 24, at 10:30 AM, we learn the August Dallas Fed Manufacturing Survey.

On Tuesday, September 25, at 9:00 AM, the new S&P Corelogic Case-Shiller National Home Price Index for July, a three-month lagging indicator.

On Wednesday September 26, at 10:00 AM, the August New Home Sales is published. At 2:00 the Fed Open Market Committee announced its decision to raise interest rates by 25 basis points.

Thursday, September 27 leads with the Weekly Jobless Claims at 8:30 AM EST, which dropped 3,000 last week to 201,000, a new 43-year low. At the same time an update on Q2 GDP is published.

On Friday, September 28, at 9:45 AM, we learn the August Chicago Purchasing Managers Index. The Baker Hughes Rig Count is announced at 1:00 PM EST.

As for me,

Good luck and good trading.

Mad Hedge Technology Letter

May 10, 2018

Fiat Lux

Featured Trade:

(WHO'S TRYING TO BREAK INTO YOUR HOME NOW?),

(GRUB), (DPZ), (AMZN), (BABA), (YUM), (YELP), (MS)

Penetrating the home is the holy grail for tech companies, and soon the smart home will be full of gizmos and gadgets that will accompany Alexa.

Not so fast.

Before we enter the abode, there is a war taking place right before our eyes.

The last mile.

This industry focuses on monetizing the transportation route to people's doorsteps whether its food delivery, ride-shares, or a dog-walking app.

The intense obsession with this last mile stems from the shift in consumers' behavior because of online commerce.

People just aren't going out and buying stuff anymore like they used to do.

Particularly, Millennials have a pension for binge-watching Netflix while gorging on food deliveries.

In the current climate, brick-and-mortar's future prospects look bleak as foot traffic disappears and mega-malls shutter at an accelerating rate.

As a last resort, companies have no choice but to evolve, reinvent themselves, and execute a digital strategy based on fast fulfillment through a smartphone app to attract new transactions.

Enter the food delivery industry.

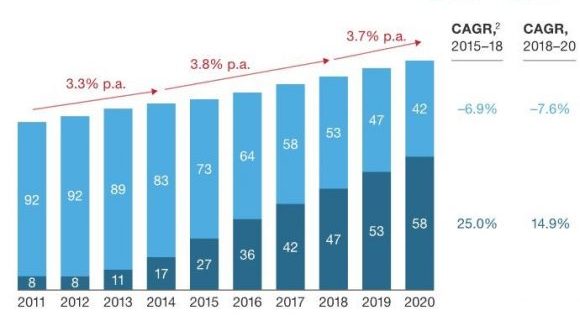

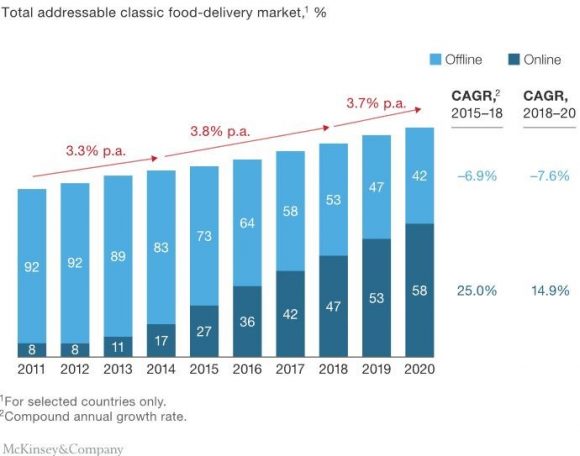

China's food delivery industry has matured faster than America's food delivery industry. And precious pearls of wisdom can be gleaned by the developments in China.

The Chinese food delivery industry is a $32 billion industry compared to a $5 billion industry in America.

Consolidation ran rampant in the early days while the migration to mobile was more pronounced in China. The multiple players burning cash faster than Elon Musk were subsidized by private funds.

Then Tencent and Alibaba (BABA) snapped up the last two remaining combatants resulting in a blossoming of a new duopoly.

Alibaba's Ele.me commands about half the market share in China while Tencent's Meituan-Dianping has a 43% share.

Meituan-Dianping is valued at $30 billion at the last stage of fundraising making it the fourth biggest unicorn in the world.

The food delivery industry could gradually mirror the situation in China, but America is still in its nascent stage, and the industry still offers viable growth chances for the participants.

The industry leader is Grubhub and it has been able to avoid the insane cash burn with which Chinese food deliverers grappled.

Shockingly, Grubhub turns a profit showing how last mile delivery in China has been reduced to a data grab.

The margins are juicier stateside.

On March 1, 2017, Grubhub's shares were trading at $33. Fast-forward to today and the shares are doing extraordinarily well, topping $102 giving investors more than a 300% return on capital in more than a year.

Grubhub was able to perform this feat in the face of harsh downgrades caused by Amazon's epic rise as the No. 4 player.

Numerous Amazon induced sell-offs could not hold back the stock with each stock dump being an attractive entry point.

Morgan Stanley's (MS) Brian Nowak went neutral on the stock in June 2017 and issued a price target between a range of $43 and $47 because of enhanced competition.

The analysts were all wrong again.

Grubhub has secured 34% of the market share followed by Uber Eats at 20% and Amazon at 11%. The third player was Eat24, which was recently acquired by Grubhub bolstering its market position an additional 16% to 50%.

The key metric for Grubhub is DAG - Daily Active Grubs.

This number was up 35% YOY to 437,000. Management has highlighted Tier 2 and Tier 3 cities as noticeable growth levers, and the Tier 1 cities such as New York and Chicago remain solid.

The rampant growth resulted in $233 million for the quarter, which is up 49% YOY. The integration of Eat24 will result in cost efficiencies and synergies across its operation.

Grubhub also entered into a partnership with online restaurant review platform Yelp (YELP) integrating the Grubhub platform onto the Yelp platform.

Actions speak volumes and aggressive tactics securing further market share gains are required to stave off Amazon whose rapid ascent has management's nerves hanging by a thread.

Despite being defensive in nature, the Yelp and Eat24 deals should give Grubhub a wider digital footprint stimulating business.

Grubhub also agreed to a deal with Yum! Brands (YUM) to lure premium restaurant assets such as KFC and Taco Bell into the Grubhub ecosphere.

The company has many irons in the fire and will not rest on its laurels.

After last quarter, Grubhub tallied up 15.1 million active diners, which is up 72% YOY. Annual guidance came in at between $930 million to $965 million.

To put the diminutive size in perspective, Grubhub liaises with 80,000 restaurants while Ele.me in China served 1.2 million restaurants.

Rough estimates show that 11% of Americans will use food delivery apps by 2020.

The nascent industry in America has a long runway ahead as the American consumer has been slower than the Chinese to adopt a thoroughly digital life.

This will all change.

Amazon is swiftly ramping up its food delivery business in conjunction with food ordering platform Olo based in New York. Outsourcing back-end support and partnering with Olo is a sign that Amazon sees this as a side job.

Amazon is still in the process of blending in Whole Foods within the existing framework of the company. Last mile food delivery is not a pure Amazon type of business.

Any potential business Amazon hopes to disrupt is leveraged by advantages in execution of volume (using state-of-the-art fulfillment centers) and low margins.

Thus, groceries fit these criteria to a T. However, value-added food meals delivered to the home cannot take advantage of the expensive fulfillment centers because the products' main point of transport is the restaurant's kitchen.

The analysts' bearish calls revolve around the grim margin prospects.

They could be correct, but the timing of the call is too early.

Yes, the opportunity to ruin margins is there for the taking in this industry.

Grubhub earned $99 million off of a miniscule $683 million of revenue in 2017, and technological innovations will devour margins to the bone.

After the mythical run-up in the face of the Amazon threat, the stock is expensive, but the company is still healthy and expects another record year.

Any sniff of margin headwinds will cripple the stock trajectory. It's not a matter of if but when.

Any big data play is ripe for competition because of the appreciation of the value of the data itself. Buy low and sell high.

At the height of competition in China, consumers were eating for free along with free deliveries because of the massive subsidies with companies seeking to gain market share any way possible.

Any similar repeat would put Grubhub's stock in the doldrums.

There are alternatives in the last mile food space.

Domino's Pizza (DPZ) is not a food delivery business nor is it a tech company.

However, it is a restaurant that fuels growth with one of the best digital strategies in the food business.

Domino's Pizza is an A.I. play.

The stock's epic rise is directly correlated with a smorgasbord of tech enhancements.

In 2014, Domino's launched DOM, a virtual ordering assistant created by A.I. voice recognition technology.

The heavy investments into the tech side have borne fruit with 65% of Domino's sales resulting from a myriad of digital platforms.

CEO J. Patrick Doyle has chimed in promulgating the desire for 100% digital sales.

Doyle believes voice is the future and implementing voice into Domino's structure will free up workers' time to focus on producing the pizzas instead of manning the phone lines thus reducing operating costs.

Domino's has been investing in its A.I. capabilities for the past five years and would be a better way to play the food space with a few extra degrees of separation with Amazon than Grubhub.

The digital strategy is about five years in, and during that time, Domino's has seen its stock rise from $46.57 to $245 today and most analysts attribute the success to its excellent digital strategy.

Would I take a flyer on Grubhub? Yes.

Would I rather buy Microsoft? Yes.

_________________________________________________________________________________________________

Quote of the Day

" 'User' is the word used by the computer professional when they mean 'idiot.' " - said Pulitzer Prize-winning American author Dave Barry.

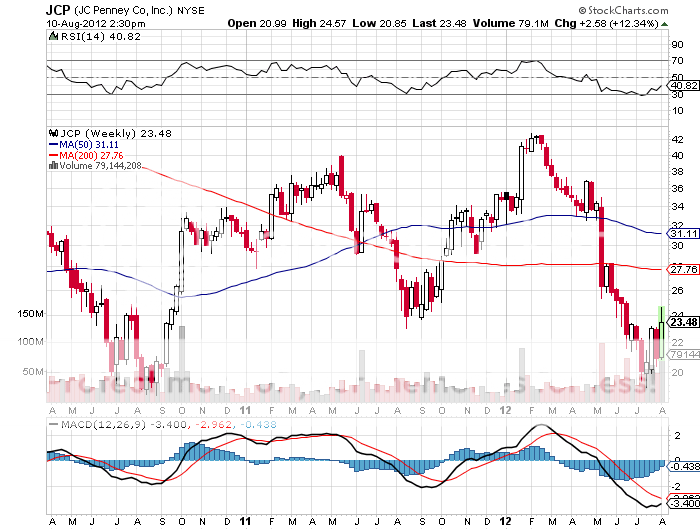

The stock of the day last Friday was, no doubt, JC Penny (JCP), one of the most heavily shorted stocks in the market, which announced Q2, 2012 earnings. Despite a huge miss, the stock soared by 20% because the losses were not as bad as many expected. This leads to the question of whether traders should double up or bail on the existing short positions.

As the dispassionate analyst that I am, who only looks at numbers in the cold, harsh light of reality, the figures could not have been more disappointing. Q2 EPS showed a loss of $0.37/shares versus an expected loss of $0.25. Revenues came in at $3 billion compared to an estimate of $3.2 billion.

Worst of all, same store sales cratered by -21.7% YOY while traffic was off -12%. This is despite offering kids free haircuts. Gross margins shrank and Internet sales were off 30%. To top it all, the company announced that it would no longer provide future guidance. Moody?s immediately followed with a downgrade of the company?s debt from Ba1 to Ba3.

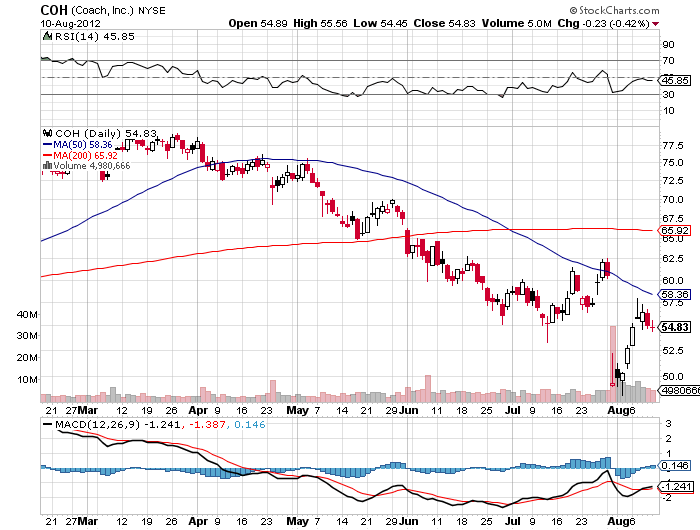

The new CEO, Ron Johnson, has no retail experience and says he needs 4 years for a turnaround. In the meantime, competitor Macys is making good money and selling at 11X earnings with the best CEO in business. Well established luxury brand Coach (COH) sells for a 14X multiple. If you fall in love with retail and absolutely have to be in this sector, there are far better fish to fry. Personally, I would rather lie down and take a long nap.

The hedgies still in this name are clearing gunning for a chapter 11. So a chance to sell again 20% higher than yesterday in the face of bad news has to be attractive. But with such a huge share of the company?s outstanding shares already sold short, the risk reward here is not great. I would have ridden the stock down from $40 to $20 and then said, ?Thank you very much?, rather than chase the last few dollars just to prove I?m right.

The company only has to get a little right to trigger a bigger short squeeze. Technicians were clearly focused on a potential multiyear double bottom on the charts. Besides, I was never one for sloppy seconds, and don?t need a haircut.

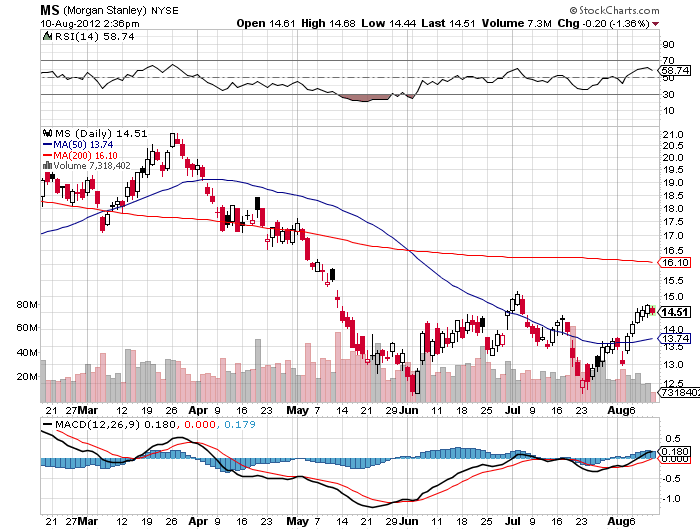

Looking for a better stock to sell short at the top of the recent range with dire fundamentals? I?d rather short Morgan Stanley on an up day.

JC Penny: Better Fish to Fry

This year, your bonus is that you get to keep your job. That is the bad news that will be dished out to many disappointed staff during annual reviews at the major Wall Street firms this year.

We all know that volumes have been trading at subterranean levels which have created a real drought of commission incomes. New regulations imposed by Dodd-Frank and the Volker rule mean that banks have to become boring, no longer able to juice earnings with trading revenues. For boring, read less profitable, leading to smaller budgets for compensation. This is the price of preventing banks from committing suicide with your money in hand.

Industry compensation experts are seeing bonus cuts of up to 30%. Equity divisions are seeing the greatest cuts, followed by bond departments, and investment banking. Senior staff are being nudged toward early retirement to further reduce overhead. Only private wealth managers are seeing pay increases, thanks to their ability to charge rich fees for enhanced customer service and place high margin products, like local municipal bonds.

The scary thing is that shrinking payouts is a trend that could continue for years, unless a new bull market suddenly appears out of nowhere. When I first started working on Wall Street nearly 40 years ago, one out of three taxi drivers were brokers rendered jobless by deregulated commissions. Be careful next time you cross the street. You might get hit with some free investment advice.

Did You Say ?Buy? or ?Sell??