Global Market Comments

July 11, 2022

Fiat Lux

Featured Trade:

(HOW TO FIND A GREAT OPTIONS TRADE)

Global Market Comments

July 11, 2022

Fiat Lux

Featured Trade:

(HOW TO FIND A GREAT OPTIONS TRADE)

Global Market Comments

July 8, 2022

Fiat Lux

Featured Trade:

(A NOTE ON ASSIGNED OPTIONS, OR OPTIONS CALLED AWAY)

(MSFT)

Mad Hedge Biotech and Healthcare Letter

July 5, 2022

Fiat Lux

Featured Trade:

(AN AAA-RATED STOCK POISED TO DELIVER MARKET-BEATING RETURNS)

(JNJ), (AAPL), (GOOGL), (AMZN), (MSFT), (TSLA), (META), (BRK.A)

More than six months after what appeared to be a never-ending assault on the biotechnology and healthcare industries, the sector seems to be slowly reviving.

While it is still too early to declare the pullback over, there are a few companies that provide a ray of hope for investors.

In the US, only four stocks have recorded a market capitalization of $1 trillion or higher: Apple (APPL), Alphabet (GOOGL), Amazon (AMZN), and Microsoft (MSFT). This year's market crash saw Tesla (TSLA) and Meta Platforms (META) departure from this elite group.

The market-wide selloff also made it more difficult for stocks to reach the $1 trillion mark. However, this does not necessarily preclude them from achieving this goal in the future.

Companies are rapidly expanding and equipped with the right tools and strategies to capitalize on growth opportunities, making them prime candidates to make the $1 trillion cut in a couple of years.

One of them is Johnson & Johnson (JNJ).

Almost everyone is familiar with JNJ's century-old brands, such as Band-Aids and Listerine. What many people probably do not realize is that the company's med-tech and pharmaceutical segments account for the vast majority of its total revenue.

In 2021, its pharmaceuticals segment alone comprised 55% of JNJ sales, while its medical devices unit contributed 29% to the company’s top line.

So far, the most promising drug in JNJ’s pharmaceutical segment is Tremfya. First-quarter sales for this psoriasis treatment jumped to a whopping 41% year over year to record an annualized $2.4 billion.

Meanwhile, JNJ's med-tech segment is poised for massive growth as a result of the strong demand for its electrophysiology products. These devices, used to keep hearts beating normally, have been identified as lucrative revenue streams and growth drivers in the long run.

The company has been working on spinning off its consumer segment into a separate publicly traded entity in the following months. This means that investors with JNJ stock will eventually end up owning shares of two different companies by 2023.

The decision to spin off its consumer health segment is part of the company's effort to shed a cyclical segment and become a health pure play focused on pharmaceuticals and medical devices.

Hence, now is an excellent time to buy JNJ shares.

While JNJ isn’t known as a high-growth stock, the company’s strategies have the potential to spur exponential growth and send shares soaring.

The next decade will be crucial for the company's success as it transforms. If the company executes its plans successfully, its current market capitalization of $467 billion could slowly but steadily increase to approximately $1 trillion.

J&J will be able to invest and concentrate its resources on segments with high sales and margins, which should increase the company's income and cash flows at a faster rate than at present.

Furthermore, JNJ's plan is expected to increase shareholder returns through higher dividends and share repurchases because of its growing cash flow. With these factors combined, JNJ's stock price will undoubtedly rise, as will its market cap.

On top of these, JNJ offers a 2.6% dividend yield. Admittedly, this isn’t remarkably high. However, investors can rely on its steady rise. Moreover, JNJ is a Dividend King. In fact, it recently raised its payout for the 60th year in a row.

If these aren’t enough to cement the company’s reputation as a solid investment, consider the fact that JNJ is one of the largest holdings in Warren Buffett’s (BRK.A) portfolio.

It’s also one of the only two publicly traded companies with the coveted AAA credit rating from S&P. For context, the US government only has an AA rating. Needless to say, this makes JNJ one of the safest—if not the safest—income stock to date.

Overall, JNJ has been diligent in getting all of its ducks in a row and is poised to provide market-beating returns to patient investors.

Global Market Comments

June 27, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE RECESSION TRADE IS ON)

(MSFT), (NVDA), (TSLA), (BRKB), (TLT), (SPY)

Any doubts that financial markets are fully discounting a recession were completely smashed last week.

It isn’t just the economic data that are rolling over like the Bismarck. Oil plunged 19%, copper is off 22% from its top, and bond yields have collapsed an astonishing 46 bases points in only two weeks, from 3.48% to 3.02%, a cataclysmic move in the bond market.

Asset classes most sensitive to a recession, like industrial commodities, suffered the biggest falls. That’s because if commodities don’t get used immediately they have to be stored at great expense and a million barrels of oil don’t look very pleasant in your backyard.

How did the stock market respond? It loved it. Stocks delivered the first positive week in June. The Dow Average rallied a healthy 1,900 points off the bottom, some 6.41%.

So what gives? Why is every asset class in the world getting trashed while stocks rocket?

It's really very simple. Stocks love lower interest rates. Cut borrowing costs and equities catch a bid. Lower rates more and stocks should further appreciate.

It's not like we are out of the woods yet. We could get another interest rate spike as we move into the next Fed move on interest rates on July 27. That could take us to new lows in stocks, but not by much. Any declines from here will be limited and are worth buying, as I have been arguing for weeks.

Always focus on what is going to happen next for we are in the “what happens next business.”

While broker reports, research, and the news focus on what happened in the past, or rarely today, it is what happens next that determines the performance of your investment portfolio.

Live in the future and there are never any surprises, only rewards.

Powell Highlights the Fed’s Inflation Commitment, even though the principal drivers, OPEX+ and the Ukraine War, are completely out of his control, in testimony in front of congress. The next two 75 basis point rate rises are a sure thing. Number three won’t happen if a recession kicks in before then.

Oil Dives as Recession Fears Mount, off 20% in a week. Oil is the last thing you want to hold going into a recession, as storage fears are at record highs a few tankers are available for charter. Avoid all energy plays like the plague. Too many other better fish to fry.

American Airlines, United Airlines, and Delta are Cutting Routes, to deal with staff shortages. Small cities where no money is made, like Toledo, Islip, and Dubuque are the main targets. Reno lost much of its airline services in the last recession for the same reason.

A Real Estate Selloff is Going Global, the effect of rising interest rates worldwide. Auckland, New Zealand, Vancouver, Canada, and Sydney, Australia have suddenly seen homes go heavily offered as free money disappears. The US could be next. In Incline Village, NV homes priced under $1 million are seeing aggressive price cuts to sell, while those over $5 million are maintaining prices.

Electric Vehicles Could Reach a 33% Market Share by 2028 and 54% by 2035, says AlixPartners, a research firm. Automakers are going to have to invest $526 billion to meet this demand. EVs are becoming a dominant factor in the US economy. Keep buying (TSLA) on dips, which has a 12-year head start over everyone and has an 80% global EV market share. You just missed a chance to buy the shares at $635 last week.

Existing Home Sales plunge 3.4% in May to 5.41 million units, Dow 8.6% YOY. Inventories fell slightly, with 1.16 million homes for sale. The median home price rose to a new all-time high of $407,600. Home sales priced under $250,000 are down 27% YOY. Mansions are still selling well nationally.

Industrial Production rises by a modest 0.2% in May. Their recession hasn’t hit here yet.

Bitcoin hit a $17,900 low Asian trading. Bitcoin crash is particularly compelling to watch as it has become a great risk indicator for all asset classes. Ignore it at your peril. It turns out that the wonder of 24/7 trading means it can go down a lot faster. I have no idea where the bottom is so don’t ask. This amount of fear is impossible to quantify.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil peaking out soon, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

With some of the greatest market volatility in market history, my June month-to-date performance exploded to +9.99%.

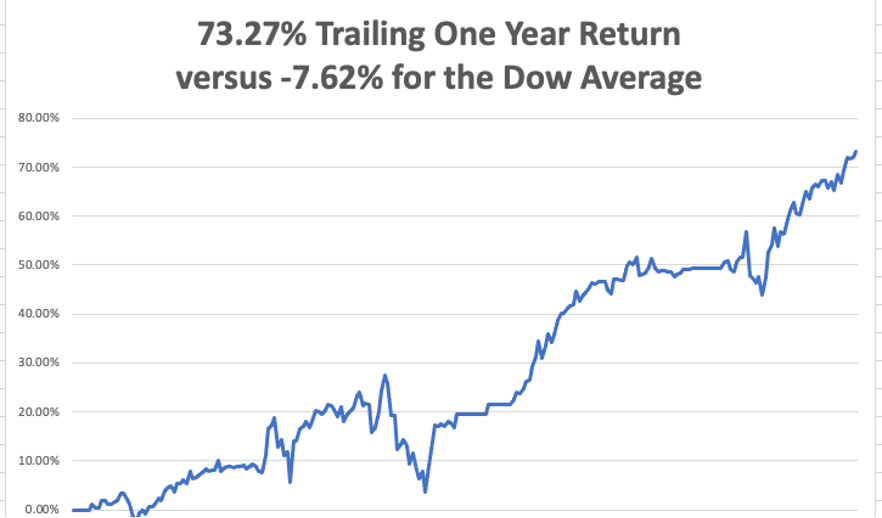

My 2022 year-to-date performance ballooned to 51.86%, a new high. The Dow Average is down -13.22% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 73.27%.

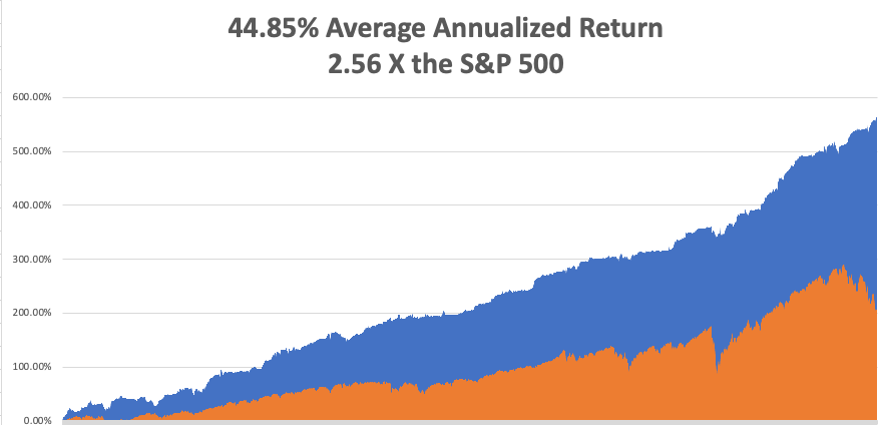

That brings my 14-year total return to 564.42%, some 2.56 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 44.85%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 87 million, up 300,000 in a week and deaths topping 1,016,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, June 27 at 8:30 AM, US Durable Goods for May are released.

On Tuesday, June 28 at 7:00 AM, the S&P Case Shiller National Home Price Index for April is out.

On Wednesday, June 29 at 7:00 AM, the final read of the US Q1 GDP is published.

On Thursday, June 30 at 8:30 AM, Weekly Jobless Claims are announced. We also get US personal Income & Spending.

On Friday, July 1 at 7:00 AM, the ISM Manufacturing PMI for June is disclosed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, as this pandemic winds down, I am reminded of a previous one in which I played a role in ending.

After a 30-year effort, the World Health organization was on the verge of wiping out smallpox, a scourge that had been ravaging the human race since its beginning. I have seen Egyptian mummies at the Museum of Cairo that showed the scarring that is the telltale evidence of smallpox, which is fatal in 50% of cases.

By the early 1970s, the dreaded disease was almost gone but still remained in some of the most remote parts of the world. So, they offered a reward to anyone who could find live cases.

To join the American Bicentennial Mt. Everest Expedition in 1976, I took a bus to the eastern edge of Katmandu and started walking. That was the farthest roads went in those days. It was only 150 miles to basecamp and a climb of 14,000 feet.

Some 100 miles in, I was hiking through a remote village, which was a page out of the 14th century, back when families though buckets of sewage into the street. The trail was lined with mud brick two-story homes with wood shingle roofs, with the second story overhanging the first.

As I entered the town, every child ran to their windows to wave, as visitors were so rare. Every smiling face was covered with healing but still bleeding smallpox sores. I was immune, since I received my childhood vaccination, but I kept walking.

Two months later, I returned to Katmandu and wrote to the WHO headquarters in Geneva about the location of the outbreak. A year later I received a letter of thanks at my California address and a check for $100. They told me they had sent in a team to my valley in Nepal and vaccinated the entire population.

Some 15 years later, while on customer calls in Geneva for Morgan Stanley, I stopped by the WHO to visit a scientist I went the school with. It turned out I had become quite famous, as my smallpox cases in Nepal were the last ever discovered.

The WHO certified the world free of smallpox in 1980. The US stopped vaccinating children for smallpox in 1972, as the risks outweighed the reward.

Today, smallpox samples only exist at the CDC in Atlanta frozen in liquid nitrogen at minus 346 degrees Fahrenheit in a high-security level 5 biohazard storage facility. China and Russia probably have the same.

That’s because scientists fear that terrorists might dig up the bodies of some British sailors who were known to have died of smallpox in the 19th century and were buried on the north coast of Greenland, remaining frozen ever since. If you need a new smallpox vaccine, you have to start from somewhere.

As for me, I am now part of the 34% of Americans who remain immune to the disease. I’m glad I could play my own small part in ending it.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

On Mt. Everest Smallpox Free in 1976

Global Market Comments

June 21, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or PREPARING FOR THE POST-RECESSION STOCK MARKET)

(NVDA), (SPY), (MSFT), (V), (TLT), (TSLA)

What if they gave a recession, and nobody came?

Better yet, what if we’re already in a recession that is about to end?

Q1 brought us a GDP growth of negative 1.5%. All we need is for the current quarter to bring in a negative number and we meet the textbook definition of a recession. That means an economic recovery could begin in as little as two weeks.

The way all asset classes traded worldwide last week confirms this view. What has really been impressive is how energy has gone from the most loved sector in the market to the most hated….in hours. Oil and energy stocks have seen the most extreme price reversals in their history, down some 20%.

If you truly believed that we were going into a recession, oil is the last thing in the world you want to own. It cost money to store and there is no storage. The Russians have locked up all they can get to place the oil that no one is buying because of the sanctions.

Tanker charters have disappeared as new buyers of Russian oil, like India and China, re-route crude from its traditional buyers in Europe.

And if you don’t sell maturing futures contracts, you have to take physical delivery of millions of barrels of oil. This is borne out by the futures market, which already has oil trading at a lowly $70 one year out. This is why the oil industry isn’t investing a dime in their own business. They’ve seen this movie before.

It isn’t just stocks and oil that are collapsing. It is everything, from copper to new home construction to retail sales. All of the loss in share prices this year, some 20%, is due to multiple compression, from 21 down to 17. Earnings are still rising. That shows there is no logic to the selling.

People just want out.

We have just about dotted all the “I”’s and crossed all their “T”’s to meet the requirements of a bear market bottom. Only 2% of stocks are now above their 50-day moving average. Equity put to call ratios are close to one. There has been massive selling of sectors that only recently started to plunge, like energy and utilities.

This has brought us a negative wealth effect that has sucked $13.1 trillion out of the real economy since November.

Watch for the trifecta of yields ($TNX), the US dollar (UUP), and oil (USO) rolling over. The “everything” bubble is over.

That makes the Bitcoin crash particularly compelling to watch, as it has become a great risk indicator for all asset classes. It broke $19,000 over the weekend. It turns out that 24/7 trading means it can go down a lot faster.

Crypto in general is having its “Lehman Brothers” moment. Crypto banks, NFTs, and brokers are dropping like flies as cascading margin calls wash through the system.

This was a field where there was margin on margin upon margin. Celsius, a crypto lender, has frozen $11 billion worth of deposits. As a long-time hedge fund manager, I can tell you that gating an asset class and preventing withdrawals brings certain death.

Some of these banks were guaranteeing 19% interest rates. It’s proof yet again that if it’s too good to be true, it usually isn’t.

All of this presages a crash in the inflation rate of epic proportions from the current 8.6%. We could be back to the Fed target of 2% by yearend if last week’s trends continue.

Since the Fed is so slow to act, the next two 0.75% rate hikes are in the bag. After that, even the Fed will release that it has a recession on its hands. All further rise hikes will cease, and they may even be back to cutting by 2023.

What happens if the above scenario plays out? It’s back to the Roaring Twenties once again and my new American Golden Age.

And while we are talking about the possibility of stocks going up once again, let me fill you in on a trade that looks particularly compelling.

Sell Short the July 15 Tesla $500 puts.

That closed at $12.25 on Friday with 18 days until expiration. At an 82.3% implied volatility, Tesla is one of the most volatile stocks in the market so they will pay you fortunes for the puts. For each put you sell short, you earn $1,225. The $500 strike price is down 58.3% from the $1,200 high seen in January. This is for a company that is seeing vehicle sales rise by 40% this year, and gross sales up 50% (they raised prices three times).

In this trade, you WANT the share to get sold to you at $500. Just take delivery of the shares. Then you can ride them up to my ten-year forecast of $10,000 and get a 20-fold return. If you don’t get triggered on the puts, just do the trade again for August and take in another $1,225 and every month until you are, or the trade goes away.

I know this trade works as I have done it several times with these results.

How do you think I got three Teslas?

Fed Raises Rates by 75 Basis Points, the most in 28 years, lifting a great weight from the shoulders of the market. Stocks rallied as well as bonds. It was one of the most confusing market responses I can recall. Two more 75 basis point hikes are in the can. The overnight rate could be at 2.75% by September. This may not be THE bottom, but it is A bottom. I’m adding risk here.

Dow Average Breaks 30,000, for the first time in a year, down 8,000 in less than six months, or 21%. Jay Powell has really taken a whip to this market. Suddenly, money costs money. I see another 5% of downside easy, then a strong rally.

Tesla is Raising Prices on its Cars, passing on rising commodity prices directly to customers because they can. There is still a one-year wait to get a new Model X. $7.00 gasoline is a dream come true for all EV makers, which are getting overwhelmed with demand. Ford quit taking orders for their all-electric F-150 at 200,000 because they can’t fill them. It might be smart to sell short the Tesla July $500 puts expiring in 20 trading days for a generous premium. If the stock falls that far, just take delivery of the shares and then ride them up to $10,000.

Tesla Proposes 3:1 Stock Split, its third since the company went public in 2010. Elon Musk is not above financial engineering to boost the share price. A cheaper share price would suck in more Millennial investors who love the company. Keep buying (TSLA) on dips like this one.

Soaring Interest Rates Demolish New Home Construction, down 14.42% in May. It’s only going to get worse. Avoid homebuilders like the plague.

Weekly Jobless Claims come in at 229,000, down 3,000. Watch this number climb as recession fears rise. The risk of a hard landing is growing exponentially.

Bitcoin is Still in Free Fall, down 10% on the day, and is just cents from breaking the crucial $20,000 support level. There are no buyers anywhere, and margin calls are running rampant. Several cryptos are not at risk of going under. This is when you find out who’s been swimming without a swimsuit. I am so glad I avoided crypto this year.

Ten-Year Treasuries Hit 11-Year High, at a 3.48% yield. This is the beginning of the end for the bear market in bonds, the worst in history.

30-Year Fixed Rate Mortgages Rocket to 6.28%, from 5.5%, effectively shutting down the market. Now you REALLY have to worry about real estate. That’s up from 2.8% in November. Avoid homebuilders like (LEN), (PHM), and (KBH) on pain of death.

FDA Approves Covid Shots for Kids, down to six months. Two mini shots are all that is needed. It will do a lot to bring working parents back into the workforce, and address worries of grandparents like me.

Producer Price Index Jumps 10.8% YOY, fanning the flames of inflation. The April print was up 0.8% compared to 0.4% a month earlier according to the Labor Department. Russia’s war in Ukraine continues to roil food and oil supplies globally, and China has started re-imposing Covid-19 restrictions just weeks after loosening them in major cities

Strong Dollar is Demolishing US Corporate Profits, and the worst is yet to come. Weaker foreign currencies like the Euro (FXE) and the yen (FXY) means international sales bring in less dough. Blame the Fed for a steady diet of interest rate rises which make the greenback the most attractive currency in the world.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil peaking out soon, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

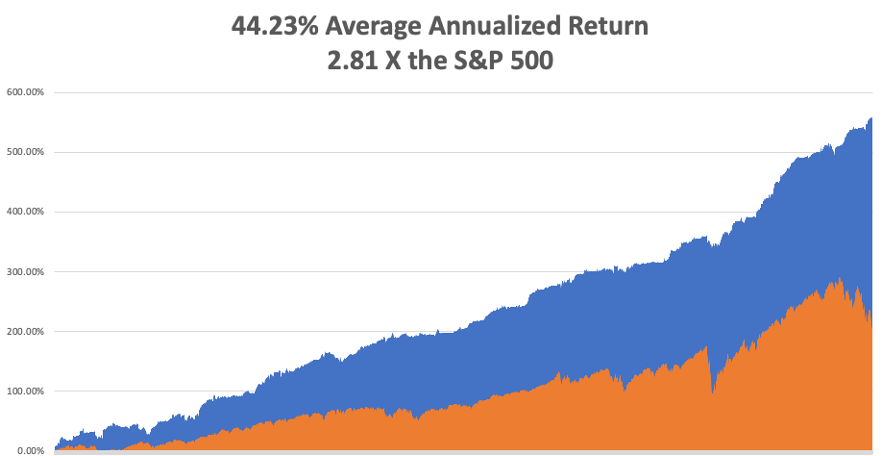

With some of the greatest market volatility in market history, my June month-to-date performance exploded to +5.91%.

My 2022 year-to-date performance ballooned to 47.78%, a new high. The Dow Average is down -17.66% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 69.35%.

Last week, we made an absolute killing with the June option expiration day, running six position into their maximum profit into the close. Those were in (NVDA), a double short in (SPY), (MSFT), (V), and (TLT).

I also used the big down 1,000-point days to add new July longs in (MSFT), (NVDA), (BRKB), and (TSLA). Putting on front month call spreads with the Volatility Index over $30 is like shooting fish in a barrel.

That brings my 14-year total return to 560.34%, some 2.40 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 44.23%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 86.3 million, up 300,000 in a week and deaths topping 1,014,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, June 20 markets are closed for the first-ever Juneteenth, the celebration of the freeing of the slaves.

On Tuesday, June 21 at 7:00 AM, Existing Home Sales for May are published.

On Wednesday, June 22 at 7:00 AM, MBA Mortgage Applications for the previous week are printed.

On Thursday, June 23 at 8:30 AM, Weekly Jobless Claims are announced.

On Friday, June 24 at 7:00 AM, New Home Sales for May are disclosed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, since I hike ten miles with a 50-pound pack every evening, it is not unusual for me to wake up feeling like I was run over by a truck.

But one morning was different. I had no energy. So, I took a Covid test. It was negative. The next morning, I was still weak, so I took the test again. Still negative.

It was only on the third morning that I produced a positive test. I had Covid-19.

I don’t know how the heck I got this disease as I had been so careful for the past 2 ½ years with my background in virology. No UCLA degree helped here. That’s why they call this variant the “stealth omicron BA.2”.

The scary thing was that I tested negative for three days while I was potentially spreading the virus.

Thank goodness for the two vaccinations and two booster shots I received. They saved my life. They headed off a long hospital stay, a long covid disability, or even death. Thank you, Pfizer!

So I quarantined myself, donned a mask whenever I left my bedroom, and shoved cash under the door whenever the kids needed to eat.

I became a couch potato of the first order, binge-watching Killing Eve, Yellowstone, and every Star Trek ever made (there are hundreds).

Fortunately, I did not lose my sense of taste or smell, as do many others. But when you sleep 18 hours a day, you don’t eat. In two weeks, I lost 15 pounds. I guess every virus has a silver lining. But every day, I felt better and better.

Of course, I had to keep working. I sent out a dozen trade alerts while I had Covid, and the newsletters and Hot Tips kept pouring out every day.

One day, I had to give two webinars and I almost passed out during the second one. I had to excuse myself for a minute and place my head between my knees to keep from blacking out.

No rest for the wicked!

I’m completely over it now. I had to cut more loops in my belts because my pants kept falling off. I can get into clothes which haven’t fit for 40 years. Fortunately, men’s fashion never go out of style.

And here’s the really great news. I am totally immune to all covid variants for a year. The disease acts as a fifth super booster.

Looks like it’s time to top up that bucket list again. If nothing else, Covid reminded me of the shortness of life and the transitory nature of opportunity. The response of a lot of Covid survivors has been to trash the budget, throw caution to the wind, and go do those things you always wanted to do.

Why should I be any different? There is no tomorrow, next week, or next year, only now.

I’ll be hitting the road.

See you at Harry’s Bar in Venice!

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Oops, I Got Covid

A Negative Test at Last

Mad Hedge Technology Letter

June 3, 2022

Fiat Lux

Featured Trade:

TECH RECESSION IS COMING)

(GOOGL), (MSFT), (AAPL), (TSLA)

The Nasdaq index isn’t pricing in a recession, but it absolutely should, as economic data streaming in shows cracks beneath the surface.

The Federal government finally went on record to admit the historically epic blunder they committed by categorizing inflation as “transitory,” with Treasury Secretary Janet Yellen acknowledging that she was “wrong.”

It's about time.

The colossal mismanagement of monetary policy by the Federal Reserve has had an extraordinary whiplash on tech shares and many have gotten burnt.

What we are experiencing now is high volatility that used to never exist in the stock market as an overleveraged system flooded by cheap money is now deleveraging.

Strong tech names like Google (GOOGL) and Microsoft (MSFT) have experienced 3% up or down days on just normal trading days with growth stocks like Tesla (TSLA) up or down 10% in just a day.

Retail traders are in over their head if they go at this alone and this is why the Mad Hedge Technology Letter is guiding you to safety.

Taking profits on the spikes and valleys is what we do best.

After months of strong consumer spending and supply-chain improvements, some of the country’s most outspoken corporate leaders have started to freak out.

Tech growth bellwether Tesla (TSLA) and their CEO Elon Musk just announced a 10% staff layoff, and that move could be the canary in the coal mine for the tech economy.

Musk clearly feels something isn’t right, and we could be approaching an economic cliff.

If that wasn’t the canary, then Microsoft's downgraded revenue expectations for next quarter’s earnings has to be as the strongest tech companies downgrade forecasts.

The probability of a recession has lurched higher, to around 50%, and this is all while the government preaches about how great the American consumer is doing.

Like many things about the US Federal government, don’t take what they say at face value because usually, the inverse is true.

The sense of doom has been especially evident in the banking sector, where Dimon told investors this week that they should be preparing for an economic “hurricane.”

State side is getting a little crusty, so then the international picture is a little rosier, right?

Wrong.

Apple is shifting its iPad production to Vietnam from China after China’s dystopian zero covid policy has effectively shut down the supply chain there.

The iPhone maker already produces some of its AirPods in Vietnam. The shift to move some iPad production to Vietnam may help it boost iPad revenue.

Ironically enough, as bad as the United States is doing now, the situation abroad is a lot worse.

Europe has completely capitulated to the military conflict and the German Producer Pricing Index has accelerated to 30%.

To make matters even worse, the European Central Bank still is maintaining a 0% net interest rate policy meaning there are Central Bank’s out there doing a lot worse job than the United States Federal Reserve.

Quite hard to believe this level of policy failure.

In short, this inflation problem hasn’t been solved at all and although it could come down a tick year-over-year, it still does nothing material to change the picture.

Even worse, a tech CEO has to be a complete fool to invest in growing capacity right now unless they have $10 billion of extra cash laying around which few companies have unless you’re Facebook, Google, Apple, Microsoft, or Tesla.

At the smaller and ground level, small tech and their balance sheets have been getting slaughtered and so has the American consumer.

Just because the American consumer goes from eating premium beef to chicken, doesn’t mean the consumer is strong.

Sooner or later, they will run out of things to substitute down from.

Same goes for smartphones, software programs, semiconductor chips, and cloud enterprise contracts.

We are in a substitute down phase and that doesn’t shout economic bullishness to me.

Maybe the American consumer can substitute driving a gas-powered car for riding a leg-powered bicycle, I wouldn’t put it past the current government to recommend this to the country.

In Europe, people have already been fed with the drive slower and dress warmer B.S. to cover up government mistakes.

Next, Europeans will need to endure the “eat less” policy come this summer and fall.