Mad Hedge Technology Letter

May 23, 2019

Fiat Lux

Featured Trade:

(ANOTHER 5G PLAY TO LOOK AT)

(EQIX), (CSCO), (GOOGL), (MSFT), (ORCL)

Mad Hedge Technology Letter

May 23, 2019

Fiat Lux

Featured Trade:

(ANOTHER 5G PLAY TO LOOK AT)

(EQIX), (CSCO), (GOOGL), (MSFT), (ORCL)

One of the seismic outcomes from the upcoming rollout of 5G is the plethora of generated data and data storage that will be needed from it.

If you are a cloud purist and want to bet the ranch on data being the new oil, then look no further than Equinix (EQIX) who connects the world's leading businesses to their customers, employees, and partners inside the most-interconnected data centers.

On this global platform for digital business, companies come together worldwide on five continents to reach everywhere, interconnect everyone and integrate everything they need to reap a digital windfall.

And whether we like it or not, the future will be more interconnected than ever because of the explosion of data and the 5G that harnesses the data will allow business to reach across the globe and expand their addressable audience.

The stock has reacted like you would have thought with a victorious swing up after a tumultuous last winter.

The cherry on top was the positive earnings report earlier this month.

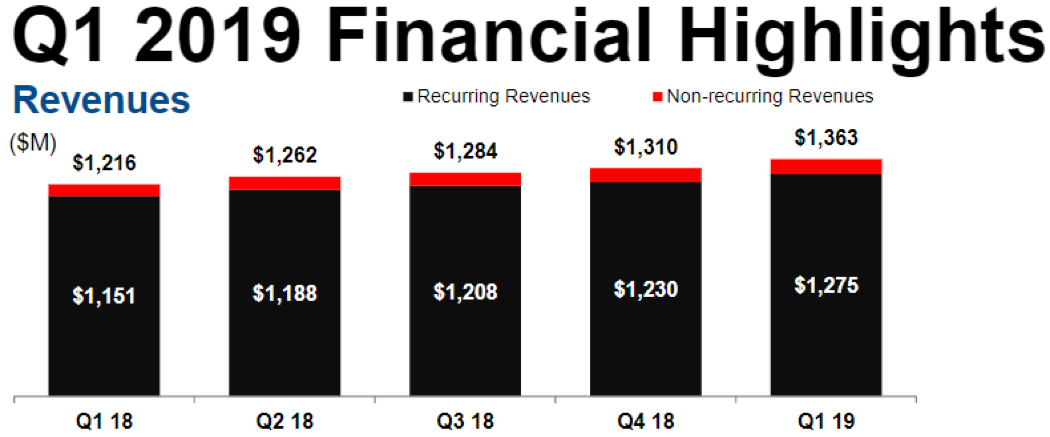

The highlights were impressive and plentiful with revenues for Q1 coming in at $1.36 billion, up 11% year-over-year meaningfully ahead of management expectations.

Equinix’s market-leading interconnection franchise is performing well, with revenues continuing to outpace colocation, growing 12% year-over-year, as the cloud ecosystem continues to scale.

Penetration in “lighthouse accounts” or early adopters increased nearly 50% from the Fortune 500 and 35% from the Global 2,000 demonstrating the expanding opportunity as Equinix unearths more value from the enterprise industry.

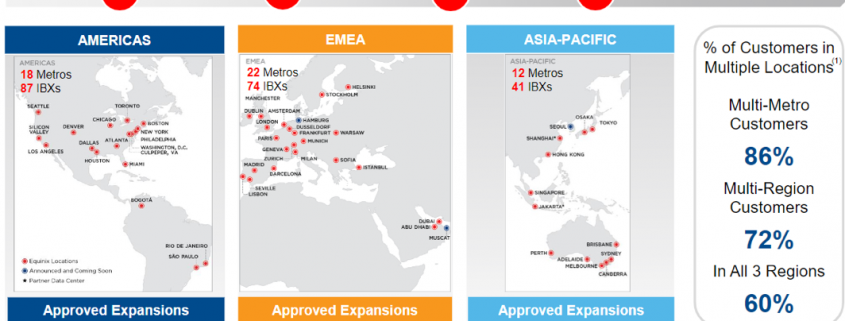

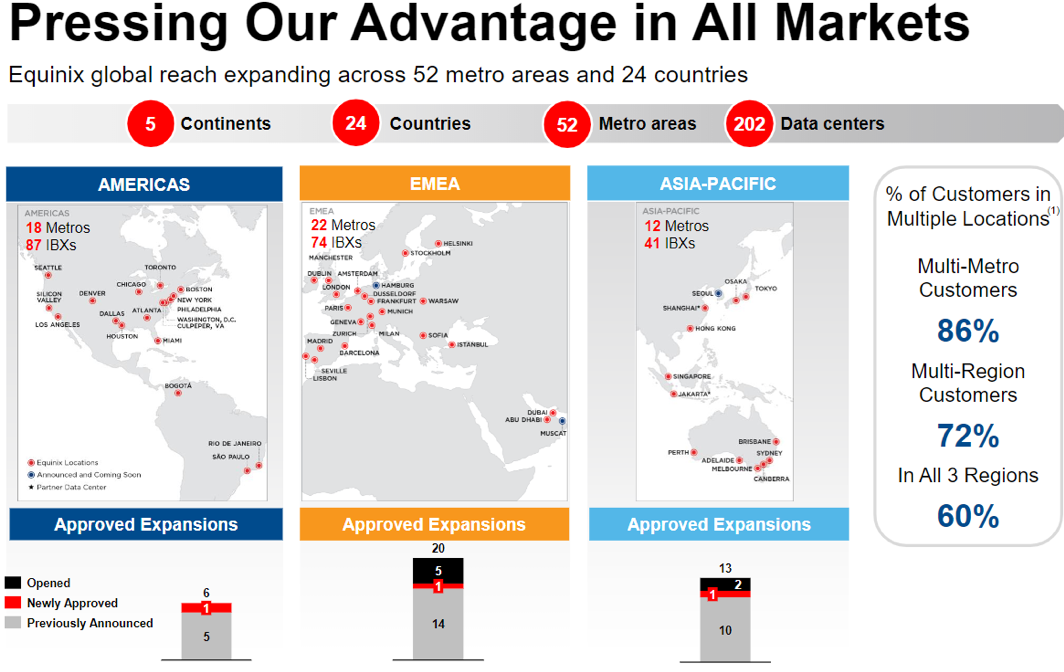

Equinix is now the market leader in 16 out of the 24 countries in which they operate, and they’re expanding its platform with 32 projects announced across 27 markets, with Q1 openings in Frankfurt, Hong Kong, London, Paris, and Shanghai.

Equinix’s network vertical experienced solid bookings led by strength in Access Point (AP), which is a hardware device or a computer's software that acts as a communication hub for users of a wireless device to connect to a wired LAN.

APs are important for providing heightened wireless security and for extending the physical range of service a wireless user has access to and driven by major telecommunication companies, mobile operators, and NSP resale.

Expansions this quarter include Hutchison, a leading British mobile network operator upgrading their infrastructure to support 5G and cloud services, as well as a leading Asian communication provider, migrating subsea cable notes and connecting to ECX Fabric for low latency.

Equinix’s financial services vertical experienced record bookings led by Europe, the Middle East and Africa (EMEA) and rapid growth in insurance and banking.

New contracts include a fortune 500 Global insurer transforming IT delivery with a cloud-first strategy, a top three auto insurer transforming network topology while securely connecting to multiple clouds, and one of the largest global payment and technology companies optimizing their corporate and commercial networks.

Demand in the social media sub-segment as providers are hellbent on improving user experience and expanding the scope of their business models.

Equinix’s gaming and e-commerce sub-segment grew the fastest year-over-year led by customers, including Tencent, neighbor, and roadblocks.

Cloud and IT verticals also captured strong bookings led by SaaS as the cloud diversifies towards a hybrid multi-cloud architecture.

A robust pipeline can be rejoiced around as cloud service providers continue to push to new frontiers and roll out additional services.

Developments include a leading SaaS provider expanding to support growth in new markets and with the Federal Government as well as an AI-powered commerce platform upgrading to enhance user experience support a rapidly growing customer base.

As digital transformation accelerates, the enterprise vertical continues to be Equinix’s sweet spot led by healthcare, legal and travel sub-segments this quarter and main catalysts to why I keep recommending reader into enterprise software companies.

The chips are being counted with new contracts from Air Canada, a top five North American airline deploying a hybrid multi-cloud strategy, Space X deploying infrastructure to interconnect dense network and partner ecosystems and one of the big four audit firms regenerating networks and interconnecting to multi-cloud to improve the user experience for both employees and clients.

Channel bookings also registered continued strength delivering over 20% of bookings with accelerated growth rates selling to Equinix’s key cloud players and technology alliance partners, including Cisco (CSCO), Google (GOOGL), Microsoft (MSFT), and Oracle (ORCL).

New channel wins this quarter includes a win with Anixter for a leading French transportation and freight logistics company deploying mobility platform, as well as a win with AT&T for a top-five U.S. Bank accessing our network and cloud provider.

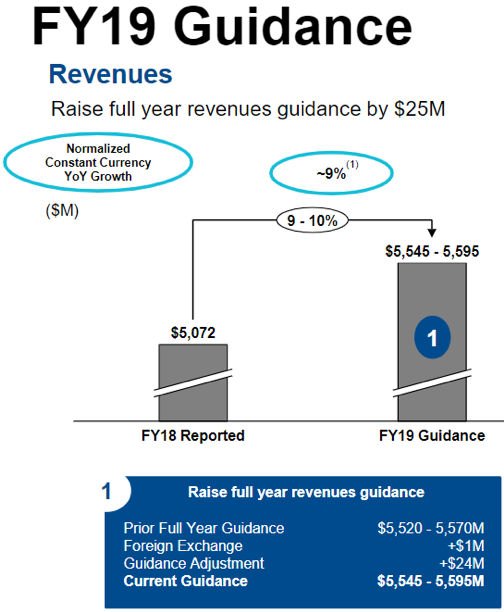

Management signaled to investors they are expecting a great year with full-year revenue guidance of $5.6B, a 9-10% year-over-year boost and a $25M revision from the previous guidance.

Equinix can boast 65 consecutive quarters of increasing revenues, which eclipses every other company in the S&P 500, and it anticipates 8%-10% in annual revenue growth through 2022.

This is an incredibly stable yet growing business and the 2.17% dividend yield, although not the highest, is another sign of a healthy balance sheet for a profitable company.

If you had any concerns about this stock, then just take a look at its 3-year EPS growth rate of 73% which should tell you that the massive operational scale of Equinix is starting to allow efficiencies to take hold dropping revenue straight down to the bottom line.

If you are searching for a company that cuts across every nook and cranny of the tech sector by taking advantage of the unifying demand and storage requirements of big data, then this is the perfect company for you.

This company will only become more vital once 5G goes online and being the global wizards of the data center will mean the stock goes higher in the long-term.

Global Market Comments

May 17, 2019

Fiat Lux

Featured Trade:

(APRIL 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(MSFT), (GOOGL), (AAPL), (LMT), (XLV), (EWG), (VIX), (VXX), (BA), (TSLA), (UBER), (LYFT), (ADBE),

(HOW TO HANDLE THE FRIDAY, MAY 17 OPTIONS EXPIRATION), (INTU),

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader May 15 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Where are we with Microsoft (MSFT)?

A: I think Microsoft is really trying to bottom here. It’s only giving up $8 from its recent high, that's why I went long yesterday, and you can be hyper-conservative and only do the June $110-$115 vertical bull call spread like I did. That will bring in a 13.68% profit in 28 trading days, which these days is pretty good. This morning would have been a great entry point for that spread if you couldn’t get it yesterday.

Q: How will tariffs affect Apple (AAPL) when they hit?

A: The price of your iPhone goes up $140—that calculation has already been done. All of Apple's iPhones are made in China, something like 220 million a year. There’s no way that can be moved, they need a million people for the production of these phones. It took them 20 years to build that facility and production capacity; it would take them 20 years to move it and it couldn't be done anywhere else in the world. So, that's why Apple led the charge on the downside and that's why it will lead the charge to the upside on any trade war resolution.

Q: How bad is the trade war going to get?

A: The market is betting now by only going down 1,400 Dow points it will be resolved on June 28th in Osaka. If that doesn’t happen it could get a lot worse. It could get down to my down 2,250-point target, and if it continues much beyond that, then we’ll get the whole full 4,500 points and be back at December lows. After that, you’re really looking at a global recession, a global depression, and ultimately nearing 18,000 in Dow, the 2016 low.

Q: Will global trade wars force US Treasuries down to around 2.10% on the ten year?

A: Yes. Again, the question is how bad will it get? If we resolve the trade war in six weeks, treasuries will probably double bottom here at around a 2.33% yield. If we go beyond that, then 2.10% is a chip shot and we go into a real live recession. The truth is no one knows anything, and we really don’t have any influence over what happens.

Q: How will equities digest and increase in European tariffs for cars?

A: It would completely demolish the European economy—especially that of Germany (EWG) which has 50% of its economy dependent on exports (primarily cars) and mostly to the U.S. And if we wipe out our biggest customer, Europe, then that would spill over here very quickly. Anybody who sells to Europe—like all the big Tech companies—would get slaughtered in that situation.

Q: Is it time to buy the Volatility Index (VIX)?

A: It’s too late to buy (VIX) now. I don’t want to touch it until we get down to that $12-$13 handle again because the time decay on this is enormous. Time decay is more than 50% a year, so your timing has to be perfect with trading any (VIX) products, whether it’s the (VXX), the (VIX) futures, the (VIX) options, or so on. There are countless people shorting (VIX) here, and they will short it all the way down to $12 again.

Q: What should I do about Boeing at this point?

A: We went long, got out, took our profit and caught this rally up to $400 a share. Then (BA) gave it up and it broke down. It’s a really tempting long here. Along with Apple, Boeing has the largest value of exports to China of any company. They have orders for hundreds of airlines from China, so they are an easy target, especially if there is a ramp up in the intensity of the trade war. That said, something like a June $270-$300 vertical bull call spread is very tempting, especially with elevated volatility up here, so I’m watching that very closely. We’re looking for the recertification of the 737 MAX bounce which could happen in the next few weeks; if that does happen it should rally at least back up to 380.

Q: Are your moving averages simple or exponential?

A: I just use the simple. I find that the simpler a concept is, the more people can understand it, and the more people buy it; that’s why I always try to keep everything simple and leave the algorithms for the computers.

Q: What stocks are insulated from a US/China trade war?

A: None. When the whole market goes risk off, people sell everything. Remember that an overwhelming portion of the market is now indexed with passive investment funds, so they just go straight risk on/risk off. It makes no difference what the fundamentals are, it makes no difference who has a lot of Chinese business or a little—everyone gets hit and everyone will get boosted when the trade war ends. There is no place to hide except cash, which is why I went 100% cash going into this. People seem to forget that cash has option value and having a lot of cash going into one of these situations is actually worth a lot of money in terms of opportunities.

Q: Do you have any thoughts on Uber’s (UBER) bad performance?

A: Yes, the whole sector was wildly overvalued, but no one knew that until they brought it to market and found out the real supply and demand for the issue. The smartest company of the year has to be Lyft (LYFT), which got a nice valuation by doing their issue first and keeping it small. So, they kind of rained on Uber’s parade; at one point, Uber was down 25% from their IPO price. That’s awful.

Q: Is Trump forcing the Fed to drop rates with all this tariff threat?

A: Yes, and if you remember, Trump really ramped up the attacks on the Fed in December. And my bet is at the first sign the trade talks were in trouble, they wanted to lower rates to offset the hit to the U.S. economy. There was no economic reason to suddenly demand huge interest rate cuts last December other than a falling stock market. The tariffs amount to a $72 billion tax increase on the American consumer, felt mostly at the low end, and that is terrible for the economy in that it reduces purchasing power by exactly that much.

Q: Would you buy the dollar as a safe haven trade?

A: No, I would not. The dollar may actually go down some more, especially with the collapse in our interest rates and European interest rates bottoming at negative levels. The best thing in the world in a high-risk environment like this is cash—don’t try to get clever and buy something you think will outperform. You could be disappointed.

Q: Why is healthcare (XLV) behaving so badly?

A: You don’t want to get into political football ahead of an election. That said, they're already so cheap that any kind of recovery could very well take healthcare up big, especially on an individual company basis. This is a sector where individual stock selection is crucial.

Q: Would you buy deep in the money calls on PayPal (PYPL)?

A: Yes, I would. Wait for a down day. Today we’re up slightly, but if we have a weak afternoon and a weak opening tomorrow morning, that would be a good time to add more longs in technology. PayPal is absolutely at the top of the list, as are names like Adobe (ADBE) and Alphabet (GOOGL).

Q: Should I be buying LEAPS in this environment?

A: No; a LEAP is a one-year long term deep out-of-the-money call spread. That was a great December bottom trade. The people who bought leaps then made huge fortunes. We’re too high here to consider leaps for the main market unless it's for something that’s just been bombed out, like a Tesla (TSLA) or a Boeing (BA), where you had big drops—then I would look at LEAPS for the super decimated stocks. But the rest of the market is still too high for thinking about leaps. Wait a couple of months and we may get back to those December lows.

Q: What happened to your May 10th bear market call?

A: Actually, it’s kind of looking good. It’s looking in fact like the market topped on May 2nd. If saner heads prevail, the trade war will end (or at least we’ll get a fake agreement) and the market will go to a new high. If not, then that May 10th target forecast I made two years ago IS the final top.

Q: You’re saying today we’re at a bottom?

A: We’re at a bottom for a short-term trade with a June 21st target. That was the expiration date of the options spreads I did this week. Whether this is the final bottom in the whole down move for a longer term, no one has any idea, even if they try to say differently. This is totally dependent on political developments.

Q: What do you have to say about Lockheed Martin (LMT)?

A: This sector usually does well with a wartime background. Expect that to continue for the foreseeable future. But at a certain point, the defense stocks which have had fantastic runs under Trump will start to discount a democratic win in the next election. If that does happen, defense will get slaughtered. I would be using any future strength to sell out of the whole defense area. Peace could be fatal to this sector.

Global Market Comments

May 15, 2019

Fiat Lux

(SPECIAL CHINA ISSUE)

Featured Trade:

(WHY CHINA IS DRIVING UP THE VALUE OF YOUR TECH STOCKS)

(QCOM), (AVGO), (AMD), (MSFT), (GOOGL), (AAPL), (INTC), (LSCC)

Reduce the supply on any commodity and the price goes up. Such is dictated by the immutable laws of supply and demand.

This logic applies to technology stocks as well as any other asset. And the demand for American tech stocks has gone global.

Who is pursuing American technology more than any other? That would be China.

Ray Dalio, founder and chairman of hedge fund Bridgewater Associates, described the first punch thrown in an escalating trade war as a “tragedy,” although an avoidable one.

Emotions aside, the REAL dispute is not over steel, aluminum, which have a minimal effect of the US economy, but rather about technology, technology, and more technology.

China and the U.S. are the two players in the quest for global tech power and the winner will forge the future of technology to become chieftain of global trade.

Technology also is the means by which China oversees its population and curbs negative human elements such as crime, which increasingly is carried out through online hackers.

China is far more anxious about domestic protest than overseas bickering which is reflected in a 20% higher internal security budget than its entire national security budget.

You guessed it: The cost is predominantly and almost entirely in the form of technology, including CCTVs, security algorithms, tracking devices, voice rendering software, monitoring of social media accounts, facial recognition, and cloud operation and maintenance for its database of 1.3 billion profiles that must be continuously updated.

If all this sounds like George Orwell’s “1984”, you’d be right. The securitization of China will improve with enhanced technology.

Last year, China’s communist party issued AI 2.0. This elaborate blueprint placed technology at the top of the list as strategic to national security. China’s grand ambition, as per China’s ruling State Council, is to cement itself as “the world’s primary AI innovation center” by 2030.

It will gain the first-mover advantage to position its academia, military and civilian areas of life. Centrally planned governments have a knack for pushing through legislation, culminating with Beijing betting the ranch on AI 2.0.

China possesses legions of engineers, however many of them lack common sense.

Silicon Valley has the talent, but a severe shortage of coders and engineers has left even fewer scraps on which China’s big tech can shower money.

Attempting to lure Silicon Valley’s best and brightest also is a moot point considering the distaste of operating within China’s great firewall.

In 2013, former vice president and product spokesperson of Google’s Android division, Hugo Barra, was poached by Xiaomi, China’s most influential mobile phone company.

This audacious move was lauded and showed China’s supreme ability to attract Silicon Valley’s top guns. After 3 years of toiling on the mainland, Barra admitted that living and working in Beijing had “taken a huge toll on my life and started affecting my health.” The experiment promptly halted, and no other Silicon Valley name has tested Chinese waters since.

Back to the drawing board for the Middle Kingdom…

China then turned to lustful shopping sprees of anything tech in any developed country.

Midea Group of China bought Kuka AG, the crown jewel of German robotics, for $3.9 billion in 2016. Midea then cut German staff, extracted the expertise, replaced management with Chinese nationals, then transferred R&D centers and production to China.

The strategy proved effective until Fujian Grand Chip was blocked from buying Aixtron Semiconductors of Germany on the recommendation of CFIUS (Committee on Foreign Investment in the United States).

In 2017, America’s Committee on Foreign Investment and Security (CFIUS), which reviews foreign takeovers of US tech companies, was busy refusing the sale of Lattice Semiconductor, headquartered in Portland, Ore., and since has been a staunch blockade of foreign takeovers.

CFIUS again in 2018 put in its two cents in with Broadcom’s (AVGO) attempted hostile takeover of Qualcomm (QCOM) and questioned its threat to national security.

All these shenanigans confirm America’s new policy of nurturing domestic tech innovation and its valuable leadership status.

Broadcom, a Singapore-based company led by ethnic Chinese Malaysian Hock Tan, plans to move the company to Delaware, once approved by shareholders, as a way to skirt around the regulatory issues.

Microsoft (MSFT) and Alphabet (GOOGL) are firmly against this merger as it will bring Broadcom intimately into Apple’s (APPL) orbit. Broadcom supplies crucial chips for Apple’s iPads and iPhones.

Qualcomm will equip Microsoft’s brand-new Windows 10 laptops with Snapdragon 835 chips. AMD (AMD) and Intel (INTC) lost out on this deal, and Qualcomm and Microsoft could transform into a powerful pair.

ARM, part of the Softbank Vision Fund, is providing the architecture on which Qualcomm’s chips will be based. Naturally, Microsoft and Google view an independent operating Qualcomm as healthier for their businesses.

The demand for Qualcomm products does not stop there. Qualcomm is famous for spending heavily on R&D — higher than industry peers by a substantial margin. The R&D effort reappears in Qualcomm products, and Qualcomm charges a premium for its patent royalties in 3G and 4G devices.

The steep pricing has been a point of friction leading to numerous lawsuits such as the $975 million charged in 2015 by China’s National Development and Reform Commission (NDRC) which found that Qualcomm violated anti-trust laws.

Hock Tan has an infamous reputation as a strongman who strips company overhead to the bare bones and runs an ultra-lean ship benefitting shareholders in the short term.

CFIUS regulators have concerns with this typical private equity strategy that would strip capabilities in developing 5G technology from Qualcomm long term. 5G is the technology that will tie AI and chip companies together in the next leg up in tech growth.

Robotic and autonomous vehicle growth is dependent on this next generation of technology. Hollowing out CAPEX and crushing the R&D budget is seriously damaging to Qualcomm’s vision and hampers America’s crusade to be the undisputed torchbearer in revolutionary technology.

CFIUS’s review of Broadcom and Qualcomm is a warning shot to China. Since Lattice Semiconductor (LSCC) and Moneygram (MGI) were out of the hands of foreign buyers, China now must find a new way to acquire the expertise to compete with America.

Only China has the cash hoard to take a stand against American competition. Europe has been overrun by American FANGs and is solidified by the first mover advantage.

Shielding Qualcomm from competition empowers the chip industry and enriches Qualcomm’s profile. Chips are crucial to the hyper-accelerating growth needed to stay at the top of the food chain.

Implicitly sheltering Qualcomm as too important to the system is an ink-drenched stamp of approval from the American government. Chip companies now have obtained insulation along with the mighty FANGs. This comes on the heels of Goldman Sachs (GS) reporting a lack of industry supply for DRAM chips, causing exorbitant pricing and pushing up semiconductor companies’ shares.

All the defensive posturing has forced the White House to reveal its cards to Beijing. The unmitigated support displayed by CFIUS is extremely bullish for semiconductor companies and has been entrenched under the stock price.

It is likely the hostile takeover will flounder, and Hock Tan will attempt another round of showmanship after Broadcom relocates to Delaware as an official American company paying American corporate tax. After all, Tan did graduate from MIT and is an American citizen.

The chip companies are going through another intense round of consolidation as AMD (AMD) was the subject of another takeover rumor which lifted the stock. AMD is the only major competitor with NVIDIA (NVDA) in the GPU segment.

The cash repatriation has created liquid buyers with a limited amount of quality chip companies. Qualcomm is a firm buy, and investors can thank Broadcom for showing the world the supreme value of Qualcomm and how integral this chip stalwart is to America’s economic system.

Mad Hedge Technology Letter

May 14, 2019

Fiat Lux

Featured Trade:

(CHINA’S COUNTERATTACK)

(AAPL), (MSFT), (ADBE), (PYPL), (QCOM), (MU), (JD), (BABA), (BIDU)

Global Market Comments

May 14, 2019

Fiat Lux

Featured Trade:

(FIVE STOCKS TO BUY AT THE BOTTOM),

(AAPL), (AMZN), (SQ), (ROKU), (MSFT)

Ratcheting up the trade tensions, China is pulling the trigger on retaliatory tariffs on $60 billion worth of U.S. goods, just days after the American administration said it would levy higher tariffs on $200 billion in Chinese goods.

American President Donald Trump accused China of reneging on a “great deal.”

The mushrooming friction between the two superpowers gives even more credence to my premise that hardware stocks should be avoided like the plague.

I have stood out on my perch in 2019 and proclaimed to buy software stocks and if you need one name to hide out in then I would confidently choose Microsoft (MSFT).

Microsoft has little exposure to China and will be rewarded the most on a relative basis.

The last place you want to get caught out is buying hardware stocks exposed to China and Apple is quickly turning into the largest piece of collateral damage along with airplane manufacturer Boeing.

Remember that 20% of Apple’s revenue comes from China and Apple bet big to solidify a complex supply chain through Foxconn Technology Group in China.

When history is recorded, CEO of Apple Tim Cook not hedging his bets exposing Apple’s revenue machine could go down as one of the worst ever managerial decisions by tech management.

The forced intellectual property transfers in China from western corporations was the worst kept secret in corporate America.

Being an operational guru as he is, and the hordes of data that Apple have access to, this was a no brainer and Cook should have mitigated his risks by investing in a supply chain that was partially outside of China, and not incrementally spreading out the supply chain through other parts of Asia is coming back to bite him.

China's most recent tariffs will come into effect on June 1, adding up to 25% to the cost of U.S. goods that are covered by the new policy from China's State Council Customs Tariff Commission.

The result of these newly minted tariffs is that importers will probably elect to avoid absorbing the costs themselves and pass the price hikes to the consumer sapping demand.

The American consumer still retains its place as the holy grail of the American economic bull case, but this will test the thesis.

For the short term, it would be foolish to hang out to Chinese companies listed in New York through American depository receipts (ADR) such as JD.com (JD), Alibaba (BABA).

Baidu (BIDU) is a company that I am flat out bearish on because of a weakening strategic position versus Alibaba and Tencent in China.

Even with no trade war, I would tell investors to short Baidu, and the chart is nothing short of disgusting.

Wei Jianguo, a former vice-minister at the Chinese Ministry of Commerce who handled foreign trade, said to the South China Morning Post that “China will not only act as a kung fu master in response to U.S. tricks but also as an experienced boxer and can deliver a deadly punch at the end.”

It is clear that any goodwill between the two heavyweight powers has evaporated and the hardliners inside the communist party pulled all the levers possible to back out at the last second.

Many of us do not understand, but there is a complicated political game perpetuating inside the Chinese communist party pitting reformists against staunch traditionalists.

This is not only Chairman Xi’s decision and appearing weak on the global stage is the last concession the communist government will subscribe to.

Along with the iPhone company, semiconductor stocks will be ones to avoid.

The list starts out with the chip companies leveraged the most to Chinese revenue as a proportion of total sales including Qualcomm (QCOM) with 65% of revenue in China, Micron (MU) who has 57% of sales in China, Qorvo who has half of sales from China, Broadcom who has 48% of sales from China, and Texas Instruments rounding out the list with 43% of total revenue from China.

The first 5 months of the year saw constant chatter that the two sides would kiss and makeup and chip stocks benefitted from that tsunami of positive momentum.

The picture isn’t as pretty when you flip the script, and chip stocks could suffer a gut-wrenching summer if the two sides drift further apart.

After Microsoft, other software names I would take comfort in with the added bonus of strong balance sheets are Veeva Systems (VEEV), PayPal (PYPL), and Adobe (ADBE).

The new tariffs will burden American households to up to $2 billion per month going forward, and new purchases for discretionary items like extra electronics will be put on the back burner extending the refresh cycle and saddling chip companies and Apple with a glut of iPhone and chip inventory.

Buy software companies on the dip.

Global Market Comments

May 3, 2019

Fiat Lux

Featured Trade:

(LAST CHANCE TO ATTEND THE LAS VEGAS MAY 9 GLOBAL STRATEGY LUNCHEON)

(APRIL 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (LYFT), (TSLA), (TLT), (XLV), (UBER),

(AAPL), (AMZN), (MSFT), (EDIT), (SGMO), (CLLS)