Long term subscribers are well aware that I sent out a flurry of Trade Alerts at the beginning of the year, almost all of which turned out to be profitable.

Unfortunately, if you came in any time after January 17 you watched us merrily take profits on position after position, whetting your appetite for more.

However, there was nary a new Trade Alert to be had, nothing, nada, and even bupkiss. This has been particularly true with particular in technology stocks.

There is a method to my madness.

I was willing to bet big that the Christmas Eve massacre on December 24 was the final capitulation bottom of the whole Q4 move down, and might even comprise the grand finale for an entire bear market.

So when the calendar turned the page, I went super aggressive, piling into a 60% leverage long positions in technology stocks. My theory was that the stocks that had the biggest falls would lead the recovery with the largest rises. That is exactly how things turned out.

As the market rose, I steadily fed my long positions into it. As of today we are 80% cash and are up a ballistic 13.51% in 2019. My only remaining positions are a long in gold (GLD) and a short in US Treasury bonds (TLT), both of which are making money.

So, you’re asking yourself, “Where’s my freakin' Trade Alert?

To quote my late friend, Chinese premier Deng Xiaoping, “There is a time to fish, and there is time to mend the nets.” This is now time to mend the nets.

Stocks have just enjoyed one of their most prolific straight line moves in history, up some 20% in nine weeks. Indexes are now more overbought than at any time in history. We have gone from the best time on record to buy shares to the worst time in little more than two months.

My own Mad Hedge Market Timing Index is now reading a nosebleed 72. Not to put too fine a point on it, but you would be out of your mind to buy stocks here. It would be trading malpractice and professional negligent to rush you into stocks at these high priced level.

Yes, I know the competition is pounding you with trade alerts every day. If they work, it is by accident as these are entirely generated by young marketing people. Notice that none of them publish their performance, let alone on a daily basis like I do.

You can’t sell short either because the “I’s” have not yet been dotted nor the “T’s” crossed on the China trade deal. It is impossible to quantify greed in rising markets, nor to measure the limit of the insanity of buyers.

When I sold you this service I promised to show you the “sweet spots” for market entry points. Sweet spots don’t occur every day, and there are certainly none now. If you get a couple dozen a year, you are lucky.

What do you buy at market highs? Cheap stuff. That would include all the weak dollar plays, including commodities, oil, gold, silver, copper, platinum, emerging markets, and yes, China, all of which are just coming out of seven-year BEAR markets.

After all, you have to trade the market you have in front of you, not the one you wish you had.

So, now is the time to engage in deep research on countries, sectors, and individual names so when a sweet spot doesn’t arrive, you can jump in with confidence and size. In other words, mend your net.

Sweet spots come and sweet spots go. Suffice it to say that there are plenty ahead of us. But if you lose all your money first chasing margin trades, you won’t be able to participate.

By the way, if you did buy my service recently, you received an immediate Trade Alert to by Microsoft (MSFT). Let’s see how those did.

In December, you received a Trade Alert to buy the Microsoft (MSFT) January 2019 $90-$95 in-the-money vertical BULL CALL spread at $4.40 or best.

That expired at a maximum profit point of $1,380. If you bought the stock it rose by 10%.

In January, you received a Trade Alert to buy the Microsoft (MSFT) February 2019 $85-$90 in-the-money vertical BULL CALL spread at $4.00 or best.

That expired last week at a maximum profit point of $1,380. If you bought the stock it rose by 12%.

So, as promised, you made enough on your first Trade Alert to cover the entire cost of your one-year subscription ON THE FIRST TRADE!

The most important thing you can do now is to maintain discipline. Preventing people from doing the wrong thing is often more valuable than encouraging them to do the right thing.

That is what I am attempting to accomplish today with this letter.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/John-Thomas-London-SE.png514577Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-01 01:06:102019-07-10 21:45:22About the Trade Alert Drought

Long term subscribers are well aware that I sent out a flurry of Trade Alerts at the beginning of the year, almost all of which turned out to be profitable.

Unfortunately, if you came in any time after January 17 you watched us merrily take profits on position after position, whetting your appetite for more.

However, there was nary a new Trade Alert to be had, nothing, nada, and even bupkiss. This has been particularly true with particular in technology stocks.

There is a method to my madness.

I was willing to bet big that the Christmas Eve massacre on December 24 was the final capitulation bottom of the whole Q4 move down, and might even comprise the grand finale for an entire bear market.

So when the calendar turned the page, I went super aggressive, piling into a 60% leverage long positions in technology stocks. My theory was that the stocks that had the biggest falls would lead the recovery with the largest rises. That is exactly how things turned out.

As the market rose, I steadily fed my long positions into it. As of today we are 80% cash and are up a ballistic 13.51% in 2019. My only remaining positions are a long in gold (GLD) and a short in US Treasury bonds (TLT), both of which are making money.

So, you’re asking yourself, “Where’s my freakin' Trade Alert?

To quote my late friend, Chinese premier Deng Xiaoping, “There is a time to fish, and there is time to mend the nets.” This is now time to mend the nets.

Stocks have just enjoyed one of their most prolific straight line moves in history, up some 20% in nine weeks. Indexes are now more overbought than at any time in history. We have gone from the best time on record to buy shares to the worst time in little more than two months.

My own Mad Hedge Market Timing Index is now reading a nosebleed 74. Not to put too fine a point on it, but you would be out of your mind to buy stocks here. It would be trading malpractice and professional negligent to rush you into stocks at these high priced level.

Yes, I know the competition is pounding you with trade alerts every day. If they work, it is by accident as these are entirely generated by young marketing people. Notice that none of them publish their performance, let alone on a daily basis like I do.

You can’t sell short either because the “I’s” have not yet been dotted nor the “T’s” crossed on the China trade deal. It is impossible to quantify greed in rising markets, nor to measure the limit of the insanity of buyers.

When I sold you this service I promised to show you the “sweet spots” for market entry points. Sweet spots don’t occur every day, and there are certainly none now. If you get a couple dozen a year, you are lucky.

What do you buy at market highs? Cheap stuff. That would include all the weak dollar plays, including commodities, oil, gold, silver, copper, platinum, emerging markets, and yes, China, all of which are just coming out of seven-year BEAR markets.

After all, you have to trade the market you have in front of you, not the one you wish you had.

So, now is the time to engage in deep research on countries, sectors, and individual names so when a sweet spot doesn’t arrive, you can jump in with confidence and size. In other words, mend your net.

Sweet spots come and sweet spots go. Suffice it to say that there are plenty ahead of us. But if you lose all your money first chasing margin trades, you won’t be able to participate.

By the way, if you did buy my service recently, you received an immediate Trade Alert to by Microsoft (MSFT). Let’s see how those did.

In December, you received a Trade Alert to buy the Microsoft (MSFT) January 2019 $90-$95 in-the-money vertical BULL CALL spread at $4.40 or best.

That expired at a maximum profit point of $1,380. If you bought the stock it rose by 10%.

In January, you received a Trade Alert to buy the Microsoft (MSFT) February 2019 $85-$90 in-the-money vertical BULL CALL spread at $4.00 or best.

That expired last week at a maximum profit point of $1,380. If you bought the stock it rose by 12%.

So, as promised, you made enough on your first Trade Alert to cover the entire cost of your one-year subscription ON THE FIRST TRADE!

The most important thing you can do now is to maintain discipline. Preventing people from doing the wrong thing is often more valuable than encouraging them to do the right thing.

That is what I am attempting to accomplish today with this letter.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/John-Thomas-London-SE.png514577Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-02-26 07:08:472019-07-09 04:06:48About the Trade Alert Drought

When I was a war correspondent (Cambodia, Laos, Iraq, Kuwait, Indonesia), my seniors gave me a sage piece of advice that saved my life many times.

“Don’t stand next to the dummy.”

Don’t go near the guy wearing the Hawaiian shirt, NY Yankees baseball cap, and aviator sunglasses. You want to be dressed in the same color as the troops and blend in as much as possible. Otherwise, the enemy will aim at the dummy and hit you.

As much as I tried, at 6’4” I was never going to blend in anywhere in Asia. So, I went into the stock market instead.

Now 50 years later, I am facing another dummy problem. Except that the next hit I may take will be of the financial kind rather than the metallic one.

The reaction to the Trump tax cuts is going to be far worse than any benefits the privileged class was able to reap from the cuts in the first place. Listening to the proposals aired, I shudder: A maximum 70% tax rate, the end of special estate tax treatment, a millionaire’s surtax, and the banning of corporate share buybacks.

It’s that last one that that will be particularly damaging for the US economy. Often, a company’s best possible investment is in its own shares where returns are frequently higher than possible through investing in their own business. Just think of all those shares Apple (AAPL) bought at $25, now at $170, and Microsoft (MSFT) picked up at $10.

This is one of the only occasions were management and shareholder interests are one and the same. The event is tax-free as long as you don’t sell your shares. And companies don’t have to pay dividends on stock they have retired, boosting profits even further.

The media loves pandering to the most extreme views out there. I know because I used to do it myself. Cooler heads will almost certainly prevail when the tax code is completely rewritten again in two years. Still, one has to worry.

The week had plenty for we analysts and strategists to chew on.

Is the Fed pausing because of political pressure or an economy that is falling apart? Neither answer is good for equity holders. Start cutting back risk while you can. There are lots of bids on the way up, but none on the way down as December showed.

There has lately been a rising tide of weak data to confirm the negative view.

Factory orders nosedived 0.6% in November, the worst in a year. Funny how nobody wants to make stuff ahead of a recession. ISM Non-Manufacturing Index Cratered to 56.7. Should we be worried? Hell, yes! Why are we getting so many negative data points and stocks keep rising?

Farm sector bankruptcies are soaring, hitting a decade high. Apparently, the trade wars and global warming aren’t working for them. Ironically, ag prices are about to take off to the upside when a Chinese trade deal gets done. Buy the ags for a trade.

Tesla (TSLA) cut prices again in a blatant bid for market share and global domination. The low-end Tesla 3 price drops to $42,900. Next stop $35,000. Too bad they laid off my customer support personnel to cut costs. I can’t find my AM radio.

China trade talks (FXI) hit the skids, taking the stock market down with it as an administration official concedes they are “nowhere close to a deal” with the deadline 3 weeks off. Trump desperately needs a deal while the Chinese don’t, who think they can do better under the next president. If you disagree with this view in China, your organs get harvested and sold on the open market.

The European economy is also going down the drain with the EC’s forecast of economic growth cut from 1.9% to 1.3%. The US-China trade war is cited as a major factor. The global synchronizes slowdown accelerates. Looks like they’ll have more time to drink cheap wine and smoke Gauloises.

The Volatility Index (VIX) hit $15 and that seems to be the bottom for the time being. The market was more overbought than at any time since July. Is the “fear gauge” signaling that happy days are here again? I doubt it. Don’t whistle past the graveyard.

The Mad Hedge Market Timing Index is entering danger territory with a reading of 67 for the first time in five months. Better start taking profits on those aggressive leveraged longs you bought in early January. Your best performers are about to take a big hit. The market has since sold off 500 points, proving its value.

There wasn’t much to do in the market this week, given that I am trying to wind my portfolio down to 100% cash as the market peaks.

I stopped out of my short portion in Apple when my stop loss was triggered by pennies. The second I was out, it began a $6 selloff. Welcome to show business.

I used a major 3 ½ point rally in the bond market to put on a new double short position there. The yield on the ten-year US Treasury bond has to plunge to 2.40% in a month, a three-year low, for me to lose money on this position. It’s a bet that I am happy to make.

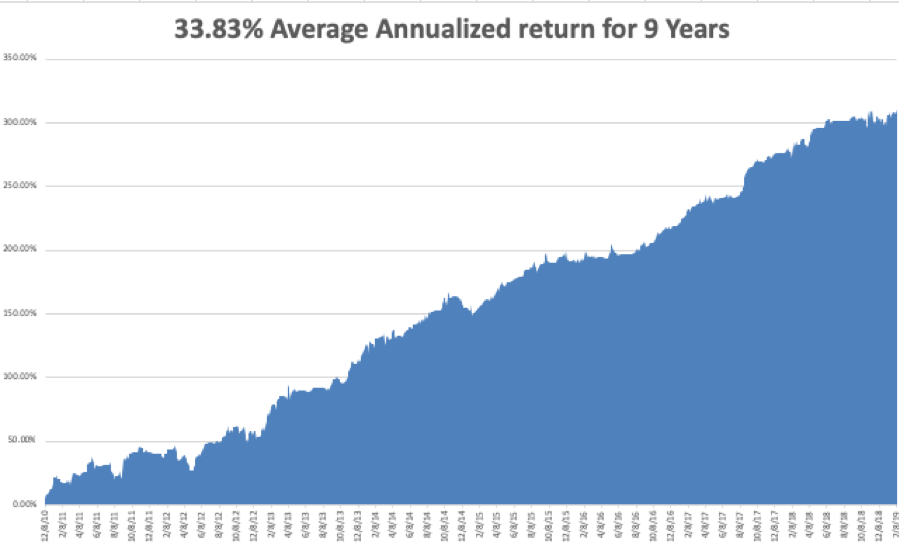

My 2019 year to date return leveled out at +10.03%, boosting my trailing one-year return back up to +35.75%.

My nine-year return maintained +310.17%, a new high.The average annualized return stabilized at +33.83%.

I am now 70% in cash and triple short the bond market.

Government data is finally starting to trickle out now that the government shutdown is over.

On Monday, February 11 there is nothing of note to report. Everything important is delayed.

On Tuesday, February 12, 10:00 AM EST, we get the January NFIB Small Business Index. Earnings for Activision Blizzard (ATVI) are out and should be a complete disaster, along with Twilio (TWLO).

On Wednesday, February 13 at 8:30 AM EST, the all-important January Consumer Price Index is published. Barrick Gold (GOLD) reports.

Thursday, February 14 at 8:30 AM EST, we get Weekly Jobless Claims. We also get December Retail Sales which should be good.

On Friday, February 15, at 8:30 AM EST, the February Empire State Index is out. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I will be battling my way through the raging snowstorms of the High Sierras trying to get over Donner Pass to my Lake Tahoe estate. Unless I clear the six feet of snow off the roof soon, or the house will get crushed from the weight as it did three years ago.

Where are all those illegal immigrants hanging out in front of 7-Eleven now that I need them?

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-02-11 01:06:222019-07-09 04:08:15The Market Outlook for the Week Ahead, or Don't Stand Next to the Dummy

Alphabet (GOOGL) is entangled in the same imbroglio as Apple (AAPL), that is why I have held back on issuing any trade alerts on this name.

The stalwart is still grinding out a respectable 20% of revenue growth in their core business but the underlying conundrum is that their hyper-growth segments are 5 times or more diminutive than their bread and butter of digital ads.

Apple is addressing the same type of strain in attempting to flip high octane revenue drivers into a bigger piece of the pie – the services business trails the hardware business by a large margin.

This phenomenon highlights how investors demand tech companies to grow at elevated rates and a maturing business model isn’t given any free passes.

Investors simply migrate towards higher growth names period.

That being said, Alphabet’s digital ad business is one of the premier tech divisions in all of technology and the American economy.

How powerful is it?

They did $32.6 billion in sales last quarter.

If you look at that number without context, it is quite impressive, but there are several lurking impediments.

This 20% QOQ growth is flatter than a pancake offering evidence that the best days are behind them.

No investors like to hear the dreaded “P word” thrown into a company’s business trajectory – peak.

In respect to revenue growth rates, I expect Google’s digital ad business to gradually decline relative to competition.

This segment also battles with the law of large numbers.

It’s simply difficult to accelerate revenue rates at a 25% YOY clip when revenues are already over $30 billion per quarter. Again, this is another Apple problem and a side effect of being overly successful in one part of the business model.

If investors' tepid reaction about these aspects of the core business telegraph dissatisfaction, then discovering further ancillary problems might be the final dagger in the heart.

Google search’s price per click cratered 29% YOY indicating that variables in the current marketing environment have significantly blunted Google’s pricing power.

Traffic Acquisition Cost (TAC) represents the cost for a company to acquire internet traffic onto their assets.

Alphabet faced a 15% YOY rise in TAC costs last quarter to $7.44 billion illustrating the difficulty in keeping these high costs down.

The bulk of the $7.44 billion stems from a widely known agreement with Apple contracting Google search as its default search engine on Apple devices.

This TAC expense has been surging the past few years and Alphabet has little negotiating power.

Expect an annual 15-20% rise in TAC expenses as long as Alphabet’s digital ads are expanding the standard vanilla 20% most investors expect them to grow.

As a whole, TAC costs soaked up 23% of the digital ad revenue which was in line with analysts’ expectations.

However, I expect this number to surpass 25% before winter because I believe Google search’s ad business will confront ceaseless growth problems.

Amazon’s (AMZN) new-found digital ad business is an influential factor in this story.

New marketing dollars aren’t being showered on Google as they once were, over 50% of product searches populate from Amazon.com today boding poorly for the future of Google search.

This optionality could be a large reason in driving the cost per click downwards.

CEO of Amazon Jeff Bezos refused to enter the digital ad game for years but his recent change of heart will correlate to subduing Google digital ad model.

Consumers are finding less incentive to search on Google for products when they just can smartly and efficiently search on Amazon directly.

Clearly, this only affects product searches and not searches on other informative content such as widely popular searches including “top 10 places to travel in Europe” or “best Thanksgiving recipes.”

Google’s “other revenues” is chugging along nicely with 31% YOY growth headed by Google’s cloud business and hardware division.

This is what Alphabet needs to focus on going forward similar to Microsoft and Amazon web services.

Yes, Google is the 3rd biggest cloud player but miles behind the top two.

Being in catch-up mode is no fun and is part of the reason capital expenditures exploded and came in $1.38 billion higher than expected.

Alphabet simply isn’t doing a good job at executing relative to Amazon and Microsoft frittering away more capital in the name of growth but not curating the type of growth that current expenses justify.

Higher costs damaged operating margins coming down 2% YOY to 21%.

Even more worrisome is that there has been no material progress on the Waymo business.

This is the year that Alphabet expected the technology to roll out to the masses.

However, this broad-based integration will not happen as fast as they would like.

I blame regulation and consumers' hesitation to quickly adopt this new technology.

Alphabet is reliant on this business to carry them to the next level of growth and I believe it can become a $100 billion per year business in a $2 trillion addressable market.

But when you peruse through the “Other Bets” category which houses Alphabet’s other companies such as health venture Verily, the $154 million in revenue was a huge miss against the $187.4 million expected.

Estimates aside, the pitiful fact that Waymo only brings in revenue of less than 1% of total revenue is disappointing.

Summing things up, Alphabet is a great company and is a long-term buy and hold stock even with short term transitory headaches.

In the near term, there is uneasiness about the decreasing profitability, exploding expense factors, a heavy reliance on weakening core business revenue, and a lack of top-line contribution of “other revenues” relative to their core business.

Long term, Alphabet’s game-changing investments have yet to show signs of life in terms of real revenue expansion even though Alphabet is the global leader of artificial intelligence and self-driving technology.

Investors would like to see actionable steps to incorporate this best of breed technology that funnels down to the top and bottom line.

Investors are stuck with a stale digital ads business that has locked the stock into a holding pattern essentially trading sideways for the past year until they prove they are ready to take the next step up.

Looking at Alphabet’s chart, the stock has iron-clad support at $1,000 which it tested in April 2018 and December 2018.

Using this entry point as the lower range would be sensible as I don’t foresee any demonstrably negative news blindsiding the stock, and I surmise that investors will start receiving positive news on Waymo’s roll out towards the middle of the year.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/02/ALPHABET-feb6.png564974Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-02-06 08:06:492019-02-06 08:05:39Alphabet Wows Them Again!

Great company – lousy time to be this great company.

That is the least I can say for GPU chip company Nvidia (NVDA) who issued a cataclysmic earnings alert figuring it was better to spill the negative news now to start the healing process earlier.

This stock is a great long-term hold because they are the best of breed in an industry fueled by a secular tailwind in GPUs.

But this doesn’t mean they will be gifted any freebies in the short term and, sad to say, they have been dragged, kicking and screaming, into the heart of the trade skirmish along with Apple (AAPL) and buddy Intel (INTC) amongst others.

The best thing a tech company can have going for them right now is to have no China exposure, that is why I am bullish on software companies such as PayPal, Twilio, and Microsoft.

I called the chip disaster back in summer of 2018 recommending to stay away like the plague.

The climate has worsened since then and like I recently said – don’t buy the dead cat bounce in chips because the bad news isn’t baked into the story yet or at least not fully baked.

It’s actually a blessing in disguise if banned in China if you are firms such as Facebook (FB), Google (GOOGL), and Amazon (AMZN).

I recently noted that a material end to this trade war could be decades away and the tech world is already being reconfigured around the monopoly board as we speak with this in mind.

Where do things stand?

The US administration took a scalp when Chinese communist backed DRAM chip maker Fujian Jinhua effectively shuttered its doors.

Victory in a minor battle will likely embolden the US administration into continuing its aggressive stance if it is working.

If you forgot who Fujian Jinhua was… they are the Chinese chip company who were indicted by the U.S. Justice Department for stealing intellectual property (IP) from Boise-based chip behemoth Micron (MU).

The way they allegedly stole the information was by poaching Taiwanese chip engineers who would divulge the secrets to the Chinese company buttressing China in pursuing their hellbent goal of being able to domestically supply enough quality chips in order to stop buying American chips in the future.

Officially, China hopes to ramp up its self-sufficiency ratio in the semiconductor industry to at least 70% by 2025 which dovetails nicely with the broader goal of Chinese tech hegemony.

Fujian Jinhua was classified as a strategically important firm to the Chinese state and knocking the wind out of their sails will have a reverberating effect around the Chinese tech sector and will deter Taiwanese chip engineers to act as a go-between.

According to a research note by Zhongtai Securities, Jinhua’s new plant was expected to have flooded the market with 60,000 chips per month and generate annual revenue of $1.2 billion directly competing with Micron with their own technology borrowed from Micron themselves.

Jinhua’s overall goal was to support a monthly manufacturing target of 240,000 chips spoiling Chinese tech companies with a healthy new stream of state-subsidized allotment of chips needed to keep costs down and build the gadgets and gizmos of the future.

For the most part, it was unforeseen that the US administration had the gall and calculative nous to combat the nurtured Chinese state tech sector.

However, I will say, it makes sense to pick off the Chinese tech space now before they stop needing American chips at all in 5-7 years and when all remnants of leverage disappear.

The short-term pain will be felt in the American chip tech sector which is evident with the horrid news Nvidia reported and the aftermath seen in the price action of the stock.

Nvidia expects top line revenue to shrink by $500 million or half a billion – it’s been a while since I saw such a massive cut in forecasts.

Half of revenue comes from the Middle Kingdom and expect huge downgrades from Apple on its earnings report too.

If this didn’t scare you, what will?

These short-term headwinds are worth it to the American tech sector as a whole.

To eventually ward off a future existential crisis when Chinese GPU companies start offering outside business actionable high quality chips curated with borrowed technology, funded by artificially low debt, and for half the price is worth its weight in gold.

The same story is playing out with Huawei around the globe but at the largest scale possible.

This is what happens when the foreign tech sector is up against companies who have access to unlimited state loans and is part of wider communist state policy to take over foundational technology globally.

I will also emphasize that the Chinese communist party has a seat on every board at any notable Chinese tech company influencing decisions at the top even more than the upper management.

If upper management stopped paying heed to the communist voice at the table, they would be out of business in a jiffy.

Therefore, Huawei founder Ren Zhengfei standing at a podium promulgating a scenario where Huawei is operating freely from the government is what dreams are made of.

It’s not a prognosis rooted in reality.

The communist party are overlords breathing down the neck of Huawei after any material decisions that can affect the company and subsequently the government’s position in the interconnected world.

The China blue print essentially entails a pan-Amazon strategy emphasizing large volume – low cost strategy.

Amazon was successful because investors would throw money at the company until it scaled up and wiped the competition away in one fell swoop.

Amazon is on a destructive path bludgeoning every American second-tier mall reshaping the economic world.

The unintended consequences have been profound with the ultimate spoils falling at the feet of CEO and Founder of Amazon Jeff Bezos, his phalanx of employees as well as Amazon stockholders which are mostly comprised of wealthy investors.

Well, Chairman Xi Jinping and the Chinese communist party are attempting to Amazon the American tech sector and the broader American economy.

The American economy could potentially become the second-tier mall in this analogy and the game playing out is an existential crisis for the likes of Advanced Micro Devices (AMD), Nvidia, Micron, Intel and the who’s who of semiconductor chips.

If stocks reacted on a 30-year timeframe, Nvidia would be up 15% today instead of reaching a trading day nadir of 17%.

What is happening behind the scenes?

American tech companies are moving supply chains or planning to move supply chains out of China.

This is an epochal manifestation of the larger trade war and a decisive development in the eyes of the American administration.

In fact, many industry analysts understand a logjam of failed trade solutions as a bonus to the Chinese.

However, I would argue the complete opposite.

Yes, the Chinese are waiting out the current administration to deal with a new one that might be more lenient.

But that will take another two years and publicly listed companies grappling with the performance of quarterly earnings don’t have two years like the Chinese communist party.

And who knows, the next administration might even seize the baton from the current administration and clamp down even more.

Be careful what you wish for.

Taiwanese company and biggest iPhone assembler Foxconn Technology Group is discussing plans to move production away from China to India.

India is a democratic country, the biggest democracy in Asia, and is a staunch ally of the United States.

CEOs of Google (GOOGL) and Microsoft (MSFT), some of Silicon Valley heavyweights, are from India and American tech companies have been making generational tech investments in India recently.

Warren Buffet even invested $300 million in an Indian FinTech company Paytm.

When you read stories about India being the new China, well it’s happening faster than anyone thought and on a scale that nobody thought, and the underlying catalyst is the overarching trade war fueling this quick migration.

Apple is already constructing low grade iPhones in India in the state of Karnataka since 2017, and these were the first iPhones made in India.

They won’t be the last either.

Wistron, major Taiwanese original design manufacturer, has since started producing the iPhone 6S model there as well.

And it is no surprise that China and its artificially priced smartphones have undercut Samsung and Apple in India grabbing the market share lead.

This is happening all over the emerging world.

And don’t forget if U.S. President Donald Trump revisits banning American chip companies supply channels to Chinese telecom company ZTE. That would be 70,000 Chinese jobs out the window in a nanosecond.

The current administration has drier powder than you think and this would hasten the deceleration of the Chinese economy and also move forward the American recession into 2019 boding negative for tech shares.

Therefore, I would recommend balancing out a trading portfolio with overweights and underweights because it is obvious that tech stocks won’t be coupled to a gondola trajectory to the peak of the summit this year.

It’s a stockpickers market this year with visible losers and winners.

And if China does get their way in the tech war, American chip companies will eventually become worthless squeezed out by mainland competition brought down by their own technology full circle.

They are first on the chopping board because their overreliance on Chinese revenue streams for the bulk of sales.

Among these companies that could go bust are Broadcom (AVGO), Qualcomm (QCOM), Qorvo (QRVO), Skyworks Solutions (SWKS) and as you expected Micron and Nvidia who are one of the main protagonists in this story.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-29 08:06:032019-07-09 04:53:00What’s Behind the NVIDIA Meltdown

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-28 01:07:082019-01-28 00:53:50January 28, 2019

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refuseing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visist to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.