Global Market Comments

January 14, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or IS THE BULL MARKET BACK?),

(SPY), (TLT), (MSFT), (AMZN), (CRM), (AAPL), (FXE),

(TESTIMONIAL)

Global Market Comments

January 14, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or IS THE BULL MARKET BACK?),

(SPY), (TLT), (MSFT), (AMZN), (CRM), (AAPL), (FXE),

(TESTIMONIAL)

During the Christmas Eve Massacre, a close friend sent me a research report he had just received entitled “30 Reasons Equities Will Fall in 2019.” It was laughable in its extreme negativity.

I thought this is it. This is the bottom. ALL of the bad news was there in the market. Stocks could only go up from here.

If I’d had WIFI at 12,000 feet on the ski slopes and if I’d thought you would be there to read them, I would have started shooting out Trade Alerts to followers right then and there. As it turned out, I had to wait a couple of days.

Two weeks later, and here I am basking in the glow of the hottest start to a new year in a decade, up 6.45%. So far in 2019, I am running a success rate of 100% ON MY TRADE ALERTS!

Don’t expect that to continue, but it is nice while it lasts.

I can clearly see how the year is going to play out from here. First of all, my Five Surprises of 2019 will play out during the first half of the year. In case you missed them, here they are.

*The government shutdown ends quickly

*The Chinese trade war ends

*The House makes no moves to impeach the president, focusing on domestic issues instead

*Britain votes to rejoin Europe

*The Mueller investigation concludes that Trump has an unpaid parking ticket in Queens from 1974 and that’s it.

*All of the above are HUGELY risk-positive and will trigger a MONSTER STOCK RALLY.

After that, the Fed will regain its confidence, raise interest rates two more times, and trigger a crash even worse than the one we just saw. We end up down on the year.

My long-held forecast that the bear market will start on May 10, 2019 at 4:00 PM EST is looking better than ever. However, I might be off by an hour. Those last hour algo-driven selloffs can be pretty vicious.

I make all of these predictions firmly with the knowledge that the biggest factors affecting stock prices and the economy are totally unpredictable, random, and could change at any time.

It was certainly an eventful week.

Fed governor Jay Powell essentially flipped from hawk to dove in a heartbeat, prompting a frenetic rally that spilled over into last week.

On the same day, China cut bank reserve requirements, instantly injecting $200 billion worth of stimulus into the economy. That’s the equivalent of spending $400 billion in the US. The last time they did this we saw a huge rally in stocks. It turns out that the Middle Kingdom has a far healthier balance sheet than the US.

Saudi Arabia chopped oil production by 500,000 barrels a day, sending prices soaring. It's not too late to get into what could be a 40% bottom to top rally to $62 (USO).

Macy's (M) disappointed, crushing all of retail with it, and taking down an overbought main market as well. It highlights an accelerating shift from brick and mortar to online, from analog to digital, and from old to new. Online sales in December grew 20% YOY. Will Amazon sponsor those wonderful Thanksgiving Day parades?

Home mortgage rates hit a nine-month low with the conventional 30-year fixed rate loan now wholesaling at an eye-popping 4.4%. Will it be enough to reignite the real estate market? It is actually a pretty decent time to start picking up investment properties with a long view.

My 2019 year to date return recovered to +6.45%, boosting my trailing one-year return back up to 31.68%. 2018 closed out at a respectable +23.67%.

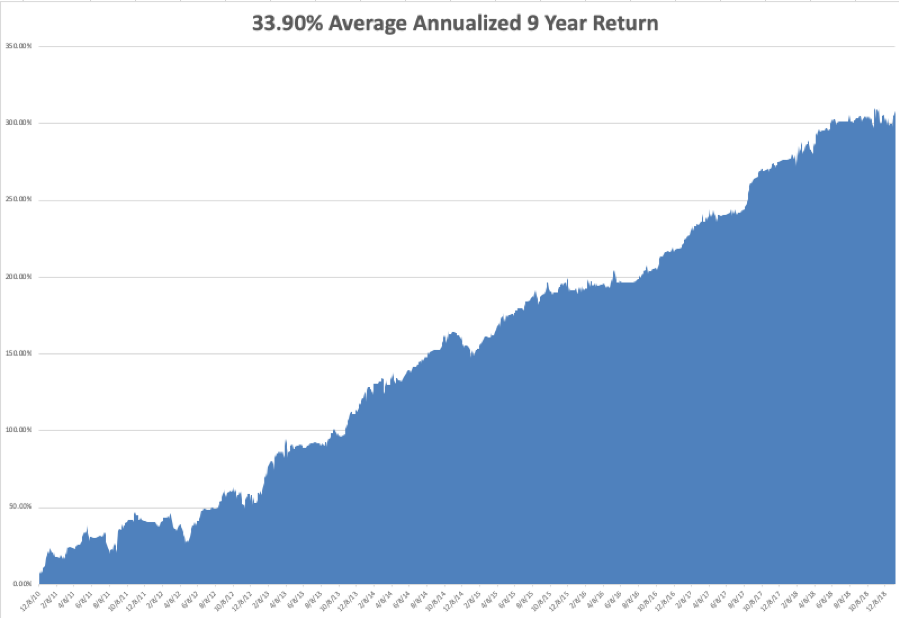

My nine-year return nudged up to +307.35, just short of a new all-time high. The average annualized return revived to +33.90.

I analyzed my Q4 performance on the chart below. While the (SPY) cratered -19.5% in three short months, my Trade Alert Service hung in with only a -4.9% loss. The quarter was all about defense, defense, defense. It was the hardest quarter I ever worked.

While everything failed last year, everything has proven a success this year. I came back from vacation a week early to pile everyone into big tech longs in Salesforce (CRM), Microsoft (MSFT), and Amazon (AMZN). I doubled up my short position in the bond market.

I even added a long position in the Euro (FXE) for the first time in years. If Britain votes to stay in Europe, it is going to go ballistic.

I also top ticketed a near-record rally by laying out a few short positions in Apple (AAPL) and the S&P 500 (SPY). I am now neutral, with “RISK ON” positions “RISK OFF” ones.

The upcoming week is very iffy on the data front because of the government shutdown. Some data may be delayed and other completely missing. All of the data will be completely skewed for at least the next three months. You can count on the shutdown to dominate all media until it is over.

On Monday, January 14 Citigroup (C) announces earnings.

On Tuesday, January 15, 8:30 AM EST, the December Producer Price Index is out. Delta Airlines (DAL), JP Morgan Chase (JPM), and Wells Fargo (WFC) announce earnings.

On Wednesday, January 16 at 8:30 AM EST, we learn December Retail Sales. Alcoa (AA) and Goldman Sachs (GS) announce earnings.

At 10:30 AM EST the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, January 17 at 8:30 AM EST, we get the usual Weekly Jobless Claims. At the same time, December Housing Starts are published. Netflix (NFLX) announces earnings.

On Friday, January 18, at 9:15 AM EST, December Industrial Production is out. The Baker-Hughes Rig Count follows at 1:00 PM. Schlumberger (SLB) announces earnings.

As for me, my girls have joined the Boy Scouts which has been renamed “Scouts.” Their goal is to become the first female Eagle Scouts.

So, I will retrieve my worn and dog-eared 1962 Boy Scout Manual and refresh myself with the ins and outs of square knots, taut line hitches, sheepshanks, and bowlines. Some pages are missing as they were used to start fires 55 years ago. I am already signed up to lead a 50-mile hike at Philmont in New Mexico next summer.

As for the Girl Scouts, they are suing the Boy Scouts to get the girls back, claiming that the BSA is infringing on its trademark, engaging in unfair competition, and causing “an extraordinary level of confusion among the public.”

Is there a merit badge for “Frivolous Lawsuits”?

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Winter 2018 was a time to remember as American tech shares were caught up in a perfect storm of a global growth scares, interest rate gyrations, and a political tug of war that sees no end in sight.

All of this made investors run for the hills after a huge run-up of tech shares since the February correction in 2018.

Even after all the chaos, there is one tech stock that has muscled out the noise and is hovering at all-time highs.

Coincidently, this is a name that I recommended last year as a strong 2019 play and I would like to reaffirm my prognosis by doubling down on cloud communications company Twilio.

Twilio will be a darling of 2019 because it seeks to upgrade a whole swath of communications in legacy companies that are scurrying to compete with the rest who have forged ahead.

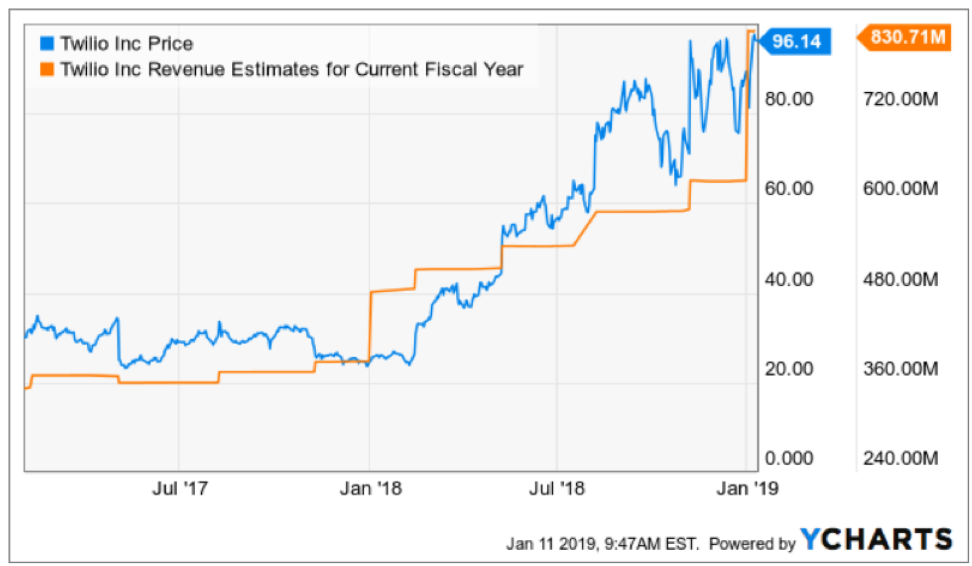

The start of 2019 has been a positive omen for Twilio shares, and are almost 10% higher in this short span of time.

It’s discernable that it is not only me who believes in this company and naysayers are few and far between.

Twilio doesn’t get as much PR as it should because making sure the back-end communication channels are executing at optimum levels is not exactly a sexy part of tech with shiny smartphones and wearable gadgets.

This company produces software and are good at what they do.

Many of you might not have even heard of them but I am sure you have heard of companies such as Uber, Lyft, and Airbnb.

Why do I mention these three private tech companies that are on the verge of going public this year?

Because this trio of unicorns is all powered by Twilio’s communication technology that is best of breed in their genre of cloud software.

More specifically, Twilio is a platform as a service (PaaS) firm offering programmatic phone call functions, can automate sending and receiving text messages, and performs other communication functions using its web service APIs.

When your shaggy-haired Uber driver calls asking you to reveal yourself out of a concrete apartment block or your lavish gated community, this is all facilitated by Twilio’s technology.

At the 2018 Twilio Signal Conference in San Francisco, Twilio indicated that its latest “call center in a box” product called Flex was up and running after announcing in March last year.

Prior to Twilio’s roll-out, this type of call center functionality was only reserved for the Fortune 500 companies that could afford expensive software to serve its minions of customers.

The small guy was left out in the cold as usual.

Twilio has reshaped the call center and, at $1 per hour or $150 per month, has made itself a gamechanger for SMEs who don’t have the manpower or capital to fund exorbitant back-end operations.

Twilio is really going after anyone with a light or bulky-shaped wallet as you see from their all-star lineup of customers. U-Haul, real estate website Trulia, and data analytic firms Scorpion and Centerfield are just a few of their customers proving the incredible flexibility and inclusive nature of the software.

It’s not a shock that this stock has gone ballistic in 2018 surging over 200% and I must admit investors need to wait for this molten hot stock to cool down.

But how can you blame a company that habitually beats any expectations by investors because of its super growth model and rapid broad-based adoption?

From the fourth quarter of last year, revenue accelerated to 48% YOY and Twilio followed that up with a blistering 54% YOY quarter.

Then they pulled a shocker guiding down only expecting 35% to 37% growth but dismantled any whiff of jangling investors' nerves by posting another quarterly growth rate of 54%.

If you average out the three-year sales growth rate, few can topple the 57% Twilio has registered.

Performance has been fantastic, to say the least, and Flex could be the product that widens their industry lead and fortifies the moat around them.

Airbnb, Uber, and Lyft will avoid tinkering with the back end of their operations before their 2019 IPOs boding well for Twilio who are on a hot streak scoring a series of big contracts.

And as their IPO dates creep closer, I firmly believe that the quiet story of Twilio will jump to the fore.

There is only so long this brilliant company can be kept under wraps.

If you take a long-term view of companies, this cloud company will be investor’s ticket to early retirement.

Even though Twilio has failed to become profitable, this year bodes well with EPS growth expected to be over 10%.

This year will be the precursor to 2020 when Twilio really invigorates earnings capability with analysts forecasting over 48% EPS growth in 2020.

Sometimes cloud companies must move mountains and absorb years of losses to finally breach the profitability marker, that time is about to come for Twilio and along with maintaining its riveting growth, the business model will become more sustainable with a vast improvement in cash flow.

Although Twilio’s competitive advantage is not as large as Microsoft (MSFT), this company has the same type of momentum going into 2019.

I believe many institutional investors have yet to hear this name echo around investment offices, and if any tech stock is going to be the darling of 2019, it will be Twilio.

I expect Twilio shares to shortly eclipse the $100 mark and maintain that level with an infusion of zeal that mimics Microsoft’s share price.

Notice that through hell and high water, any massive sell-off that crushes Microsoft swan diving below $100, shares find itself above $100 again in a jiffy.

I expect Twilio to exude similar characteristics, albeit with more volatility.

Twilio has the ability to rise 10% or even 15% on any given day on good news.

Being at all-time highs again only illustrates the attractiveness of the name.

In general, this should really be a software-as-a-service (SaaS) year for investors as the migration to these services picks up speed.

Any meaningful dip that can be attributed to outside forces should be bought because there are no fundamental problems with Twilio.

Don’t chase the stock here because it’s up almost 300% in the past 365 days - wait for it to fall into your wheelhouse.

To add the cherry on top, this company is far away from the geopolitical trade winds.

And even though fundamental differences have yet to be hashed out, at least it debugs one potential headwind to the fundamental story.

Twilio should outperform this year relative to the large tech stocks, it’s up to you if you want to ride on the coattails of this story or try your luck on less qualified names.

And not to toot my own horn, but this stock is already up almost 30% since I urged readers to pile into it.

I am strongly bullish Twilio.

There is only so much juice you can squeeze from a lemon before nothing is left.

Silicon Valley has been focused mainly on squeezing the juice out of the Internet for the past 30 years with intense focus on the American consumer.

In an era of minimal regulation, companies grew at breakneck speeds right into families' living quarters and it was a win-win proposition for both the user and the Internet.

The cream of the crop ideas was found briskly and the low hanging fruit was pocketed by the venture capitalists (VCs).

That was then, and this is now.

No longer will VCs simply invest in various start-ups and 10 years later a Facebook (FB) or Alphabet (GOOGL) appears out of thin air.

That story is over. Facebook was the last one in the door.

VCs will become more selective because brilliant ideas must withstand the passage of time. Companies want to continue to be relevant in 20 or 30 years and not just disintegrate into obsolescence as did the Eastman Kodak Company, the doomed maker of silver-based film.

The San Francisco Bay Area is the mecca of technology but recent indicators have presaged the upcoming trends that will reshape the industry.

In general, a healthy and booming local real estate sector is a net positive creating paper wealth for its local people and attracting money slated for expansion.

However, it's crystal clear the net positive has flipped and housing is now a buzzword for the maladies young people face to sustain themselves in the ultra-expensive coastal Northern California megacities.

The loss of tax deductions in the recent tax bill makes conditions even more draconian.

Monthly rental costs are deterring tech's future minions. Without the droves of talent flooding the area, it becomes harder for the industry to incrementally expand.

It also boosts the costs of existing development/operations staffers whose capital feeds back into the local housing market buying whatever they can barely afford for astronomical prices.

Another price spike ensues with first-time home buyers piling into already bare-bones inventory because of the fear of missing out (FOMO).

After surveying HR tech heads, it's clear there aren't enough artificial intelligence (A.I.) programmers and coders to fill internal projects.

Compounding the housing crisis is the change of immigration policy that has frightened off many future Silicon Valley workers.

There is no surprise that millions of aspiring foreign students wish to take advantage of America's treasure of higher education because there is nothing comparable at home.

The best and brightest foreign minds are trained in America and a mass exodus would create an even fiercer deficit for global dev-ops talent.

These U.S.-trained foreign tech workers are the main drivers of foreign tech start-ups.

Dangling carrots and sticks for a chance to start an embryonic project in the cozy confines of home is hard to pass up.

Ironically enough, there are more A.I. computer scientists of Chinese origin in America than there are in all of China.

There is a huge movement by the Chinese private sector to bring everyone back home as China vies to become the industry leader in A.I.

Silicon Valley is on the verge of a brain drain of mythical proportions.

If America allows all these brilliant minds to fly home not only to China but everywhere else, America is just training these workers to compete against American workers.

A premier example is Baidu co-founder Robin Li who received his master's degree in computer science from the State University of New York at Buffalo in 1994.

After graduation, his first job was at Dow Jones & Company, a subsidiary of News Corp., writing code for the online version of the Wall Street Journal.

During this stint, he developed an algorithm for ranking search results that he patented, flew back to China, created the Google search engine equivalent, and named it Baidu (BIDU).

Robin Li is now one of the richest people in China with a fortune of close to $20 billion.

To show it's not just a one-hit-wonder type scenario, three of the top five start-ups are currently headquartered in Beijing and not in California.

The most powerful industry in America's economy is just a transient training hub for foreign nationals before they go home to make the real moola.

More than 70% of tech employees in Silicon Valley and more than 50% in the San Francisco Bay Area are foreign, according to the 2016 census data.

Adding insult to injury, the exorbitant cost of housing is preventing burgeoning American talent from migrating from rural towns across America and moving to the Bay Area.

They make it as far West as Salt Lake City, Reno, or Las Vegas.

Instead of living a homeless life in Golden Gate Park, they decide to set up shop in a second-tier American city after horror stories of Bay Area housing starts to populate their friends' Instagram feeds and are shared a million times over.

This trend was reinforced by domestic migration statistics.

Between 2007 and 2016, 5 million people moved to California, and 6 million people moved out of the state.

The biggest takeaways are that many of these new California migrants are from New York, possess graduate degrees, and command an annual salary of more than $110,000.

Conversely, Nevada, Arizona, and Texas have major inflows of migrants that mostly earn less than $50,000 per year and are less educated.

That will change in the near future.

Ultimately, if VCs think it is expensive now to operate a start-up in Silicon Valley, it will be costlier in the future.

Pouring gasoline on the flames, Northern California schools are starting to fold like a house of cards due to minimal household formation wiping out student numbers.

The dire shortage of affordable housing is the region's No. 1 problem.

A 1,066-sq.-ft. property in San Jose's Willow Glen neighborhood went on sale for $800,000.

This would be considered an absolute steal at this price but the catch is the house was badly burned two years ago. This is the price for a teardown.

When you combine the housing crisis with the price readjustment for big data, it looks as if Silicon Valley has peaked or at the very least, it's not cheap.

Yes, the FANGs will continue their gravy train but the next big thing to hit tech will not originate from California.

VCs will overwhelmingly invest in data over rental bills. The percolation of tech ingenuity will likely pop up in either Nevada, Arizona, Texas, Utah, or yes, even Michigan.

Even though these states attract poorer migrants, the lower cost of housing is beginning to attract tech professionals who can afford more than a burned down shack.

Washington state has become a hotbed for bitcoin activity. Small rural counties set in the Columbia Basin such as Chelan, Douglas, and Grant used to be farmland.

The bitcoin industry moved three hours east of Seattle for one reason and one reason only - cost.

Electricity is five times cheaper there because of fluid access to plentiful hydro-electric power.

Many business decisions come down to cost, and a fractional advantage of pennies.

Globalization has supercharged competition, and technology is the lubricant fueling competition to new heights.

Once millennials desire to form families, the only choices are regions where housing costs are affordable and areas that aren't bereft of tech talent.

Cities such as Las Vegas and Reno in Nevada; Austin, Texas; Phoenix, Arizona; and Salt Lake City, Utah, will turn into hotbeds of West Coast growth engines just as Hangzhou, China-based Alibaba (BABA) turned that city into more than a sleepy backwater town with a big lake at its center.

The overarching theme of decentralizing is taking the world by storm. The built-up power levers in Northern California are overheated, and the decentralization process will take many years to flow into the direction of these smaller but growing cities.

Salt Lake City, known as Silicon Slopes, has been a tech magnet of late with big players such as Adobe (ADBE), Twitter (TWTR), and EA Sports (EA) opening new branches there while Reno has become a massive hotspot for data server farms. Nearby Sparks hosts Tesla's Gigafactory 1 along with massive data centers for Apple, Alphabet, and Switch.

The half a billion-dollars required to build a proper tech company will stretch further in Austin or Las Vegas, and most of the funds will be reserved for tech talent - not slum landlords.

The nail in the coffin will be the millions saved in state taxes.

The rise of the second-tier cities is the key to staying ahead of the race for tech supremacy.

Mad Hedge Technology Letter

December 24, 2018

Fiat Lux

Featured Trade:

(THE CLOUD FOR DUMMIES)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape or form.

Microsoft's (MSFT) pivot to its Azure enterprise business has sent its stock skyward, and it is poised to rake in more than $100 billion in cloud revenue over the next 10 years.

Microsoft's share of the cloud market rose from 10% to 13% and is catching up to Amazon Web Services (AWS).

Amazon leads the cloud industry it created and the 49% growth in cloud sales from 42% in Q3 2017 is a welcome sign that Amazon is not tripping up.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon (AMZN) relies on AWS to underpin the rest of its businesses and that is why AWS contributes 73% to Amazon's total operating income.

Total revenue for just the AWS division is an annual $5.5 billion business and would operate as a healthy stand-alone tech company if need be.

Cloud revenue is even starting to account for a noticeable share of Apple's (AAPL) earnings, which has previously bet the ranch on hardware products.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day. If you work in Silicon Valley you can triple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations. Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that's where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at any time from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing IT staff of prima donnas.

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them telecommute. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees. According to a recent survey, 79% of respondents already work outside of their office some of the time, while another 60% would switch jobs if offered this flexibility.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

Mad Hedge Technology Letter

December 18, 2018

Fiat Lux

Featured Trade:

(THE BIG TECHNOLOGY TRENDS OF 2019)

(MSFT), (AMZN), (BBY), (SONO), (ROKU), (ADBE), (AAPL), (BAC)

As an astute purveyor of technology, it is my job to share with you the upcoming tech trends of 2019.

Some might be easily discernable and some might be a headscratcher, but all must be tabbed up and considered in the current tech outlook that is unpredictable and fluctuating, to say the least.

Part of the moody tech sentiment has been influenced by a changeable macro landscape - the tech sector’s winter freeze was woefully volatile and unfairly capsized good companies with the bad.

There is no means to get around it – the administration's delicate situation as it relates to Beijing and the American tech sector is front and center, and any movement of tech stocks must carefully absorb the ongoings from this complicated relationship.

The number of obstacles that confront this sensitive situation means that the 90-day window granted to solve the trade quagmires appear too brief of a timeframe to really knock out every single disagreement on the table.

The uncertainty over trade policy has really ruffled some of tech’s strongest feathers such as America’s pride and joy Apple (AAPL).

Apple is a great long-term story, but it does not preside over many short-term positive catalysts that can resuscitate the stock.

Analysts' downgrade after downgrade has been most harrowing for the chip components that make up Apple and other consumer electronic devices such as televisions and tablets.

This scenario is expected to extend into 2019 with Bank of America Merrill Lynch (BAC) slashing their price target by nearly 30% on electronics retailer Best Buy (BBY) then sticking the fork in them by downgrading it to underperform.

The premise behind this downgrade was that Best Buy carved out 25% of revenue from television sales and even though Adobe (ADBE) analytics has calculated record online sales in the holiday season, the follow-through has largely been without television sales participating in the seasonal bonanza.

Piggybacking on this trope, I believe electronic device sales could be hard-pressed to eke out growth next year and are set up for a rude awakening.

Therefore, it is sensible to extrapolate this idea out and assume that smart hardware competing against the big boys such as smart speaker firm Sonos (SONO), who I urged readers to stay away at $16 in September, is set up for a painstaking 2019.

To reread the story, please click here.

The stock is now trading at $11 and a mix of weakening consumer device demand layered with the domination that is the Amazon Alexa has pushed up this company’s risk-reward levels to untold heights.

Rounding out the negatives is that content streaming platform Roku has also debuted its own version of a smart speaker.

Roku (ROKU) is one of my favorite long-time tech plays but has been dragged down by the broader trade war because a portion of its revenue is still captured by hardware such as the new speakers and Roku OTT boxes.

Differing from Apple, Roku earns most of their revenue from targeted ads on their proprietary platform, and this is its reason why most investors are in this stock that is set to capture a secular migratory wave of cord-cutters traversing to online streaming.

However, Roku TVs made by Chinese company TCL still draw in small portion of revenue and even though the China revenue is not as high on a relative basis as Apple’s 20%, the stock has floundered in the short-term.

If disruptors such as Roku can get hit savagely with a small portion of revenues from China, then I am convinced that any tech investor going into 2019 should stay away from hardware and hardware that is made in China.

The consensus is that the drawn-out trade war could become the X-factor in the 2020 election because the Chinese are willing to wait for the next guy on the carousel searching for a better deal.

If you thought Chinese supply chains had a tough time of it in 2018, then 2019 is poised to be even more treacherous.

What 2018 convincingly demonstrated was that the late economic price action is getting into later and later stages boding negative for tech stocks.

To construct a healthy tech portfolio going into 2019, the change in the tech partiality has made the pivot towards software much more important.

Investors need to mitigate Chinese supply chain risk and seek out domestic software plays.

That should be the playbook as tech investors are on pins and needles going into the new year.

The domestic economy is robust and tech investors should be attracted to top-quality cloud-based enterprise stocks that are profitable.

The FANG story collapsing in our face signaled to investors that it is time to cautiously consider whether to invest heavily into deep loss-maker tech growth stories.

A healthy rotation to premium quality tech with superior cash flow is one way to lock up stocks and slyly deflect the external factors shaking up the tech momentum.

PayPal (PYPL) is a stock that has large international exposure mainly in Europe, but none in China whose 3-year EPS growth rate is 26% and still driving sequential sales in the mid-20% range.

This is just one example of a stock that has the correct make-up in a harsh and brutal tech environment planted with invisible booby traps.

And the most tell-tale sign that the American economy is in for an all-out software frenzy is the number of head-spinning investments from big tech companies looking to expand their footprint into new talent spots around the country.

First, the farcical Amazon beauty pageant came to an end with the e-commerce giant announcing a three-part package deploying new operations in New York, Washington D.C., and Nashville as the next phase of digital growth ramps up.

Google (GOOGL) followed that up by plopping a software office in New York City devouring a huge chunk of the Chelsea neighborhood aimed at doubling the 7,000 employees already there.

Then it was Apple’s turn choreographing a significant investment in Austin, Texas that will cost them $1 billion along with juicing up operations in Seattle, San Diego, and Los Angeles.

They weren’t finished there and promised to double down its presence in Pittsburgh, New York and Boulder, Colorado over the next three years.

It’s clear that big tech has finally understood that it’s not invincible and milking the China supply chain for all its worth is now a taboo business practice that has bipartisan support firmly against it.

Like I said before, the trade war came 1-2 years too early for Apple, and these headline-grabbing talent investments in data centers and its staff underscore the sense of urgency to fully and comprehensively pivot towards a software and services company.

The transition has certainly been an excruciating process exposing the weak spots at a brilliant company at the worst possible time.

I blame CEO of Apple Tim Cook who is the operations expert in the building grappling with Apple overextending themselves in the Middle Kingdom that has come back to haunt him at night.

You would have thought that with the troves of big data on their hands, Apple’s consultants might have found a country allied with America to invest in such a massive supply chain.

This leads me to communicate with conviction that Microsoft (MSFT) is my favorite tech stock going into 2019 because it is the purest, scalable, high-quality software name with minimal hardware drag devoid of weak spots in its armor.

That was what the investment in GitHub for $7.5 billion was about, highlighting the value of owning the meeting place for coders, literally buying up a stash of over 28 million users and 57 million coding repositories in which 28 million are public.

Microsoft has also bought up six video game studios in 2018 attempting to capture a bigger piece of the pie for the video game market that has been throttled by Fortnite.

If the Microsoft baby gets thrown out with the bathwater, then the tech bear market is upon us in full force.

If you didn’t really believe content is king in 2018, then you will really feel the phenomenon further embedded into the economy and society in 2019.

Next year, almost all tech investments will result in more data centers and software engineers in the hope of pumping out the best content and data, whether it’s enterprise software, video games, or pure data storage.

In 2019, I am bullish on companies with a cloud-based bedrock able to grind out the best content in the world, backed by a strong balance sheet that dovetails nicely with a lack of China-based revenue exposure.

The uber-growth models could be taking a rest boding negatively for Uber, Lyft, and Airbnb who must convince a more skeptical tech audience with tighter purse strings as they inject yet another unique dimension into the tech world next year.

Global Market Comments

December 14, 2018

Fiat Lux

Featured Trade:

(DECEMBER 12 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (MU), (PYPL), (SPOT), (FXE), (FXY), (XLF), (MSFT), (AMZN), (TSLA), (XOM),

(SIGN UP NOW FOR TEXT MESSAGING OF TRADE ALERTS)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader December 12 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader

Q: Is the bottom in on the S&P 500 (SPX) or are we going to go on another retest?

A: It’s stuck right in the 2600-2800 range, and I think that’s probably where we bounce off of 2600 again. The question is whether or not we can clear the top of the range at 2800. If we can’t, I would fully expect a retest of this bottom in which case I could see it going down to 2500.

Q: You say you’ll go 100% cash by Dec 21st but also stated that the S&P 500 will go up 5% by the year's end. Should we stay in until we get the up 5% move?

A: Yes, all of our options positions expire by the 21st but if you’re just long in stocks, I would stay long, probably through the end of the year.

Q: Will the Chinese-U.S. dispute ruin the Tech industry?

A: No, I think the Trump Administration will have to do some kind of deal and call it a victory, otherwise the trade war will pull the U.S. into recession. If we go into the next presidential election with another recession—well, no one has ever survived that. Even with the China-U.S. dispute, the U.S. is still dominant in the Tech industry and will continue to do so for decades to come.

Q: China has managed to duplicate Micron Technology’s (MU) biggest selling chip, undercutting prices—thoughts?

A: True, Micron is the lowest value added of the major chip producers, therefore their stock has gotten hit the worst of any of the chip stocks down by about 46%, but I know Micron very well and they have a whole range of chips they’re currently upgrading, moving themselves up the value change to compete with this. So, that makes it a great company to own for the long term.

Q: I’m up 90% on my PayPal (PYPL) position—should I take a profit?

A: Yes! Absolutely! How many 90% profits have you had lately? You are hereby excused from this webinar to go execute this trade. And well-done Dr. Denis! And thank you for the offer of a free colonoscopy.

Q: What can you say about Spotify (SPOT)?

A: No, thank you—there’s lots of competition in the music streaming business. We are avoiding the entire space. The added value is not great, and many of these companies will have a short life. And with China’s Tencent growing like crazy, life for Spotify is about to become dull, mean, and brutish.

Q: What’s your view on currencies?

A: So you’re looking to make another fortune? Yes, I think the Euro (FXE) and the Yen (FXY) really are looking hard to rally, and the trigger could be dovish language in the next Fed meeting. Once the Fed slows its rate of interest rates rises, the currencies should take off like a scalded chimp.

Q: Will the banks (XLF) rally in the next 6 months for a better sell?

A: Many people are waiting for a rally in the banks so they can unload them and haven’t gotten it—they’re back to pre-election price levels. The issue here is structural, and you don’t get recoveries from major structural changes in an industry. It’s significant that this is the first bull market that had no net new employment in the banks whatsoever; the business is fading away. They are the new buggy whip makers. These gigantic national branch networks will all be gone in ten years because the banks can’t afford them.

Q: Would you enter the Microsoft (MSFT) trade today?

A: I actually think I would; Microsoft only pulled back 10% when everything else was dropping 30%, 40%, or 50%. That shows you how many people are trying to get into this name so if you could take a little short-term pain (like 5%), the stock outright is probably a screaming buy here. I think it’ll go to $200 one day, so here at $110-$111 it looks like a pretty good deal. The story here is that Microsoft is rapidly taking market share from Amazon (AMZN) in the cloud business and that’s going to continue.

Q: When will you be updating your long-term model portfolio?

A: I usually do it at the end of the year, and rarely make any big changes. I’ll still be selling short bonds and still like Tesla (TSLA) and Exxon (XOM).

Q: I just joined your service. What is the best way to get started?

A: I’ll give you the same advice that I gave every starting trader at Morgan Stanley (MS). Start trading on paper only. When you are making money reliably on paper, move up to using real money, but only with one contract per position. When that is successful, slowly increase your size to 2, 3, 5, 10, and 20 contracts. Pretty soon, you will be swinging around 1,000 contracts a lot like I do. The further you move down the learning curve the greater you can increase your size and your risk. If you never get past the paper stage at least it’s not costing you any money.

I hope this helps.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader